Chapter 7 Profit Maximization and Competitive Market.

21

Chapter 7 Profit Maximization and Competitive Market

-

Upload

jennifer-sullivan -

Category

Documents

-

view

242 -

download

1

Transcript of Chapter 7 Profit Maximization and Competitive Market.

Chapter 7

Profit Maximization and Competitive Market

Model of Perfectly Competitive Market

• The model of perfect competition rests on three basic assumptions:

1. Price taking.2. Product homogeneity.3. Free entry and exit.

Price Taking

• Many firms compete in the market.• Firm faces a significant number of direct competitors for its

products.

• Each individual firm sells a sufficiently small proportion of total market output, its decisions have no impact on market price.

• A price taking consumer is a consumer whose actions have no effect on the market price of the good or service s/he buys.

• A price taking producer is a producer whose actions have no effect on the market price of the good or service it sells.

Product homogeneity

• When the products of al of the firms in a market are perfectly substitutable with one another.

• when products are homogeneous, no firm can raise the price of its product above the price of other firms without losing most or all of its business.

• Example: Most agricultural products are homogeneous: Because product quality is relatively similar among farms in a given region.

• In contrast, when products are heterogeneous, each firm has the opportunity to raise its price above that of its competitors without losing all of its sales.

• Example: Premium ice creams such as Haagen-Dazs, for example, can be sold at higher prices because Haagen-Dazs has different ingredients and is perceived by many consumers to be a higher-quality product.

Free entry and exit• We say there is free entry and exit into and from an industry whennew producers can easily enter into and leave an industry.• Thus it is easy to for a buyer to switch from one supplier to another.• There should be no obstacles in the form of government regulationsor limited access to key resources to prevent new producers fromentering the market.• There must also be no additional costs associated with shutting down and

leaving an industry.

• Example: The pharmaceutical industry, is not perfectly competitive because Merck, Pfizer, and few other firms hold patents that give them unique rights to produce drugs. Any new entrant would either have to invest in research and development to obtain its own competing drugs or pay substantial license fees to one or more firms already in the market. R&D expenditures or license fees could limit a firm’s ability to enter the market.

Marginal Revenue (MR) & Marginal Cost (MC)

• the additional revenue resulting from the sale of an additional unit of output is called marginal revenue (MR)

• MR = TR/q• the additional cost resulting from the sale of

an additional unit of output is called marginal cost (MC)

• MC = TC/q

MR > MC

• If marginal revenue exceeds marginal cost, the production of an additional unit of output adds more to revenue than to costs.

• In this case, a firm is expected to increase its level of production to increase its profits.

MR < MC

• If marginal cost exceeds marginal revenue, the production of the last unit of output costs more than the additional revenue generated by the sale of this unit.

• In this case, firms can increase their profits by producing less.

• A profit-maximizing firm will produce more output when MR > MC and less output when MR < MC.

MR = MC

• If MR = MC, however, the firm has no incentive to produce either more or less output.

• The firm's profits are maximized at the level of output at which MR = MC.

Goal of Profit Maximization

• To analyze decision making at the firm, let’s start with a very basic question–What is the firm trying to maximize?

• A firm’s owners will usually want the firm to earn as much profit $ as possible

• We will view the firm as a single economic decision maker whose goal is to maximize its owners’ or stakeholders’ profit.

Profit Maximization

Profit is defined as the firm’s sales revenue minus its costs of production

Profit = Total Revenue – Total Cost

Profit = (profit per unit) x # of units = (P – ATC) x Q

Total Revenue• The total inflow of receipts from selling a given amount of

output• Each time the firm chooses a level of output, it also

determines its total revenue– Why?

• Because once we know the level of output, we also know the highest price the firm can charge

• Total revenue—which is the number of units of output times the price per unit—

• Total Revenue(TR)= Price(P) x Quantity(Q)• Average Revenue is how much revenue a firm is getting by

producing one item.• Average Revenue(AR) = Total Revenue(TR) / Quantity(Q)

Profit Maximization in a Competitive Market

• Since in a competitive market there is price taking meaning that no matter how much a firm produces, there will be no impact on the Price as far as Quantity produced or demanded.

• Therefore P= MR = MC• Example: when a farmer is deciding how many acres of wheat to plant in a

given year, he can take the market price of wheat let’s say, $4 per bushel as a given price. That price will not be affected by his acreage decision.

• We then have a horizontal demand curve, it can sell an additional unit of output without lowering the price. As a result, when it sells an additional unit, the firm’s total revenue increases by an amount equal to the price: one bushel of wheat sold for $4 yields additional revenue of $4. Thus marginal revenue is constant at $4.

Problem 1

Problem 1

• Questions:• Find the MR and MC?• At which quantity we have profit

maximization?

Problem 2

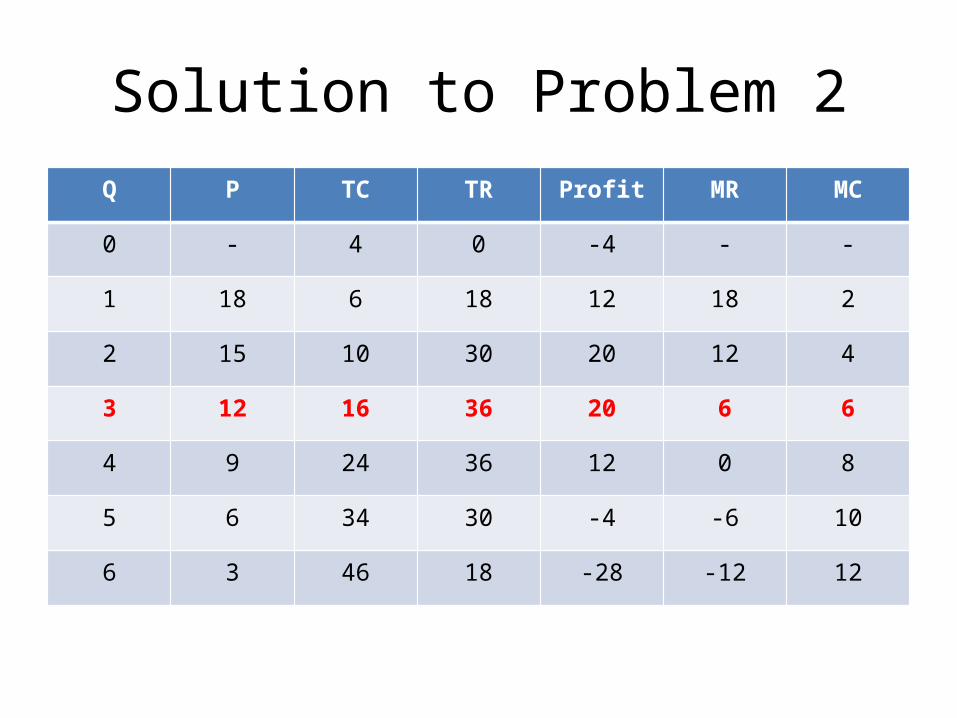

• Calculate the TR and Profit for the following firm• What quantity of production maximizes profit?

Q P TC

0 - 4

1 18 6

2 15 10

3 12 16

4 9 24

5 6 34

6 3 46

Solution to Problem 2Q P TC TR Profit MR MC

0 - 4 0 -4 - -

1 18 6 18 12 18 2

2 15 10 30 20 12 4

3 12 16 36 20 6 6

4 9 24 36 12 0 8

5 6 34 30 -4 -6 10

6 3 46 18 -28 -12 12

Problem 3

• Assuming the market price of a good is $8 and the firm’s total cost TC= 40 + 0.5Q + 0.05Q2

• What is the ideal quantity to be produced to maximize profit?

• What is the firms Profit at the ideal quantity?

Solution to Problem 3

• In Perfectly competitive market:• P = MC• MC= d(TC)/d(Q)=0.5 + 0.1Q• MC= 0.5 + 0.1Q• P= 0.5 +0.1 Q • 8= 0.5 +0.1Q• 0.1Q= 7.5 Q = 75• TR= 8*75 = $600• TC= 40+0.5(75)+ 0.5 (75*75) = $358.75• Profit= TR – TC = 600 – 358.75 = $241.25

Problem 4

• In a perfect competitive market we have the following curves for demand and supply.

• Qd= 100 – 10P• Qs= 50P – 200• The firm’s marginal cost is MC = 4 + Q• How much output does this firm has to

produce in order to maximize its profit?

Solution to Problem 4

• First we find the equilibrium price:• 100 – 10P = 50P – 200• 60P = 300• P = $5• In a competitive market P=MC• 5= 4 + Q• Q = 1