CHAPTER 7 - Indiana State University: Faculty Websitesisu.indstate.edu/acharmo/tax-sm-2005/Comp...

30

CHAPTER 7 DEDUCTIONS AND LOSSES: CERTAIN BUSINESS EXPENSES AND LOSSES SOLUTIONS TO PROBLEM MATERIALS Status : Q/P Questi on/ Presen t in Prior Proble m Topic Editio n Editio n 1 Bad debts: cash basis taxpayer Unchange d 1 2 Bad debts: business versus nonbusiness New 3 Bad debts: worthlessness Unchange d 3 4 Bad debts: recovery Unchange d 4 5 Bad debts: nonbusiness for corporations Unchange d 5 6 Bad debts: related party Unchange d 6 7 Worthless securities New 8 Section 1244 stock Unchange d 8 9 Issue ID Unchange d 9 10 Casualty loss: definition New 11 Theft loss Unchange d 11 12 Casualty loss: personal casulty loss and multiple years Unchange d 12 13 Casualty loss: disaster area Unchange d 13 14 Casualty loss: measurement rule Unchange 14 7-1

Transcript of CHAPTER 7 - Indiana State University: Faculty Websitesisu.indstate.edu/acharmo/tax-sm-2005/Comp...

CHAPTER 7

DEDUCTIONS AND LOSSES: CERTAINBUSINESS EXPENSES AND LOSSES

SOLUTIONS TO PROBLEM MATERIALS

Status: Q/PQuestion/ Present in PriorProblem Topic Edition Edition

1 Bad debts: cash basis taxpayer Unchanged 12 Bad debts: business versus nonbusiness New3 Bad debts: worthlessness Unchanged 34 Bad debts: recovery Unchanged 45 Bad debts: nonbusiness for corporations Unchanged 56 Bad debts: related party Unchanged 67 Worthless securities New8 Section 1244 stock Unchanged 89 Issue ID Unchanged 9

10 Casualty loss: definition New11 Theft loss Unchanged 1112 Casualty loss: personal casulty loss and multiple

yearsUnchanged 12

13 Casualty loss: disaster area Unchanged 1314 Casualty loss: measurement rule for partial

destruction and complete destructionUnchanged 14

15 Casualty loss: insurance claim Unchanged 1516 Casualty loss: cost of repairs method Unchanged 1617 Casualty loss: 10% of AGI floor Unchanged 1718 Casualty loss: miscellaneous itemized deductions New19 Casualty loss: 10% of AGI floor Unchanged 1920 Issue ID Unchanged 2021 Issue ID New22 Research expenditures Unchanged 2223 Research expenditures Unchanged 2324 Issue ID Unchanged 24

7-1

7-2 2005 Comprehensive Volume/Solutions Manual

Status: Q/PQuestion/ Present in PriorProblem Topic Edition Edition

25 Net operating loss: carryback and carryforward Unchanged 2526 Bad debts: business Unchanged 26

27 Bad debts: nonbusiness Unchanged 2728 Bad debts: business New

* 29 Bad debt and § 1244 stock Unchanged 29* 30 Section 1244 stock Unchanged 30* 31 Casualty loss: personal New* 32 Casualty loss: disaster area loss Modified 32* 33 Casualty loss: business versus personal use

propertyUnchanged 33

* 34 Casualty loss: insurance recovery Unchanged 34* 35 Research expenditures Unchanged 35* 36 Net operating loss: absent Unchanged 36* 37 Net operating loss and personal casualty gain Unchanged 37* 38 Cumulative Modified 38* 39 Cumulative Modified 39

ResearchProblem

1 Bad debts Unchanged2 Theft loss New3 Internet activity Unchanged

*The solution to this problem is available on a transparency master.

Deductions and Losses: Certain Business Expenses and Losses 7-3

CHECK FIGURES

26. $26,000 in current year.27. $5,000 STCL in 2004 with $3,000

deducted; $0 deducted in 2003.28. $72,000 bad debt deduction.29. $103,000.30. Mary should sell half each year.31. $44,900.32. $60,000 loss should be taken

currently.33. AGI of $105,000; $39,400 itemized

deduction.

34. Net cash benefit of $7,800 of filing an insurance claim.

35.a. 2004 $353,000; 2005 $422,000; 2006 $0.

35.b. 2004 $0; 2005 $0; 2006 $77,502.36. $36,000.37. $43,000.38. Refund due for 2004 $11,125.39. Refund due for 2003 $921.

7-4 2005 Comprehensive Volume/Solutions Manual

DISCUSSION QUESTIONS

1. No deduction is allowed for the bad debts of a cash basis taxpayer because no income has been reported. p. 7-3

2. Ron has a nonbusiness bad debt. The debt is unrelated to Ron’s trade or business. The use to which the borrowed funds are put is of no consequence in classifying the bad debt as a nonbusiness bad debt. pp. 7-4 and 7-5

3. A legal action need not be initiated against the debtor, but all of the surrounding facts and circumstances must indicate that such an action would not result in a collection of the debt. p. 7-4

4. If an account receivable has been written off as uncollectible during the current tax year and is subsequently collected during the current tax year, the write-off entry is reversed. If the account receivable recovered was written off during a previous tax year, income is created subject to the tax benefit rule. p. 7-4

5. The nonbusiness bad debt provisions are not applicable to corporations. p. 7-5

6. A bona fide debt exists when a debtor-creditor relationship is based on a valid and enforceable obligation to pay a fixed or determinable sum of money. The determination is based on an examination of the prevailing facts and circumstances. pp. 7-5 and 7-6

7. Mary cannot take a loss on her current year’s tax return for the decline in the stock value. Since the securities have not been disposed of by Mary in a market transaction, a recognized loss is allowed only if the securities become completely worthless during the year. p. 7-6

8. For small business stock, the ordinary loss treatment is limited to $50,000 ($100,000 for married individuals filing jointly) per tax year. Thus, the taxpayer is able to receive ordinary loss treatment on what otherwise would have been a capital loss (i.e., stock is a capital asset). An ordinary loss may be used, without limitation, in computing taxable income. A capital loss, after netting against capital gains, is limited to $3,000 per tax year. pp. 7-7 and 7-8

9. Joe and Amanda should be concerned with the following tax issues:

Did the original Blue common stock become worthless?

In what year did it become worthless?

What is the amount of the loss?

What is the character of the loss?

Was the stock § 1244 stock?

pp. 7-3 to 7-8

10. If the sea wall damage is the result of progressive deterioration, the definition of a casualty loss has not been satisfied. Consequently, Jim can take no deduction for his

Deductions and Losses: Certain Business Expenses and Losses 7-5

personal use property. However, if Jim can show that the damage is the result of a sudden, unexpected, and violent storm, then he can take a casualty loss. p. 7-9

11. To claim a theft loss, Janice must show that the property was actually stolen. Losses due to mislaying or losing property cannot be deducted. If there is no positive proof that a theft occurred, all of the details and evidence should be presented. If the reasonable inferences point to a theft, the deduction will be allowed. If the inferences point to a mysterious disappearance, the deduction will be disallowed. In this particular situation, the inferences would tend to point to a theft of the coat rather than mislaying the coat. Therefore, Jancie could take a theft loss for the coat. p. 7-10

12. The amount of the loss for the partial claim in 2003 is reduced by the $100 per event floor and by the 10% of AGI floor for the 2003 taxable year. The loss in 2004 is reduced by 10% of the 2004 AGI. p. 7-10 and Example 11

13. The taxpayer may elect to treat a disaster area loss as having occurred in the taxable year immediately preceding the taxable year in which the disaster actually occurred. Doing so provides immediate relief to disaster victims in the form of accelerated tax benefits. p. 7-11

14. The amount of the loss is the lesser of (1) the difference between the fair market value of the property before the event and the fair market value of the property immediately after the event or (2) the adjusted basis of the property. Note that for personal use property this lesser of provision applies to both partial destruction and for complete destruction. For business or investment property, the lesser of rule applies only for partial destruction. p. 7-11

15. The loss is to business use property. Therefore, if the taxpayer does not file an insurance claim, the loss need not be reduced by the proceeds that could have been received from the insurance company. Such a reduction would have been required if the property were personal use property. p. 7-12

16. The cost of repairs can be used as a method for measuring the amount of a casualty loss if the repairs are necessary to restore the property to its condition before the casualty, the amount spent for the repairs is not excessive, and the repairs do not extend beyond the damage suffered. In addition, the value of the property after the repairs must not, as a result of the repairs, exceed the value of the property immediately before the casualty. p. 7-12

17. The 10% of AGI floor applies to both the first and second year. The AGI of the first year determines the 10% floor for that year. The AGI of the second year determines the 10% floor for that year. p. 7-12

18. The loss from the theft of the bearer bonds would not be subject to the $100 and 10% of adjusted gross income floors which apply for casualty and theft losses to personal use property. The loss is to investment property. However, this loss is a miscellaneous itemized deduction. p. 7-14

19. By subjecting only the casualty loss in excess of casualty gains to a floor equal to 10% of adjusted gross income, the taxpayer is given a loss deduction at least as great as the casualty gains included in the tax return. If the entire casualty loss were subject to the 10% of the adjusted gross income floor, the casualty loss deduction could be less than the casualty gains. For example, if the taxpayer has $4,000 of casualty gains, $6,000 of casualty losses, and adjusted gross income of $100,000, the taxpayer will in effect have a

7-6 2005 Comprehensive Volume/Solutions Manual

casualty loss deduction of $4,000 since the loss offsets the gain. If the whole casualty loss were subject to 10% of adjusted gross income, the deduction would be zero.pp. 7-14 and 7-15

20. Monte should be concerned with the following tax issues:

Has a casualty loss been sustained?

The amount of the loss.

The year the loss should be claimed.

What effect will the $40,000 expenditure have on Monte’s adjusted basis for the land?

pp. 7-8 to 7-11

21. The tax issues for Henry are as follows:

Is this a casualty loss?

Is this property used in a trade or business?

What is the amount of the loss?

The basis for computing the loss.

The decline in fair market value.

pp. 7-8 to 7-13

22. All costs incident to the development of an experimental or pilot model, a plant process, a product, a formula, an invention, or similar property, and the improvement of already existing property of the type mentioned. The term does not include expenditures such as those for the ordinary testing or inspection of materials or products for quality control or those for efficiency surveys, management studies, consumer surveys, advertising, or promotion. pp. 7-16 and 7-17

23. The following three alternatives are allowed for research and experimental expenditures:

Expense in the year paid or incurred.

Defer and amortize over not less than 60 months.

Capitalize and deduct when the project is abandoned or deemed worthless.

pp. 7-17 and 7-18

24. The tax issues for Power and Light are as follows:

Are the expenditures for environmental impact studies research and experimental expenditures?

Are the expenditures for environmental impact studies deductible business expenses?

Deductions and Losses: Certain Business Expenses and Losses 7-7

pp. 7-16 and 7-17

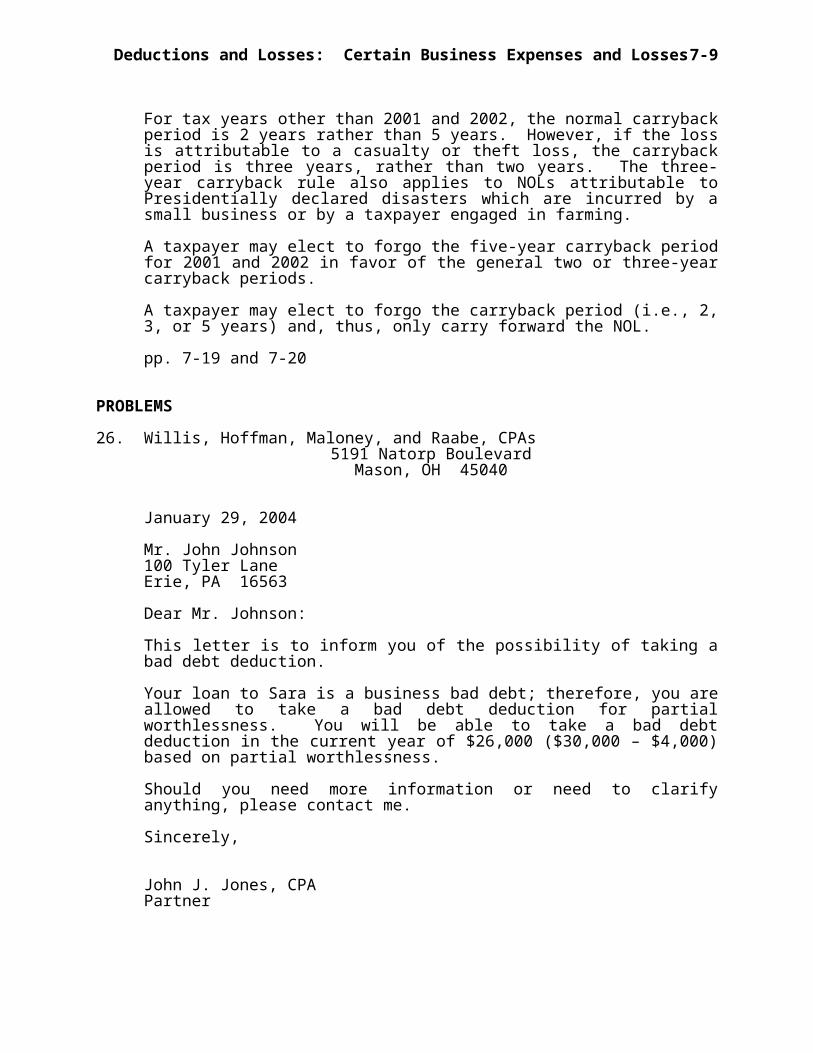

25. A net operating loss generally must be carried back initially to the fifth year preceding the year of the loss for tax years 2001 and 2002. Unused amounts (after applying the loss against income of the five carryback years) are carried forward chronologically for up to twenty years, beginning with the first year subsequent to the year of the loss.

For tax years other than 2001 and 2002, the normal carryback period is 2 years rather than 5 years. However, if the loss is attributable to a casualty or theft loss, the carryback period is three years, rather than two years. The three-year carryback rule also applies to NOLs attributable to Presidentially declared disasters which are incurred by a small business or by a taxpayer engaged in farming.

A taxpayer may elect to forgo the five-year carryback period for 2001 and 2002 in favor of the general two or three-year carryback periods.

A taxpayer may elect to forgo the carryback period (i.e., 2, 3, or 5 years) and, thus, only carry forward the NOL.

pp. 7-19 and 7-20

PROBLEMS

26. Willis, Hoffman, Maloney, and Raabe, CPAs5191 Natorp Boulevard

Mason, OH 45040

January 29, 2004

Mr. John Johnson100 Tyler LaneErie, PA 16563

Dear Mr. Johnson:

This letter is to inform you of the possibility of taking a bad debt deduction.

Your loan to Sara is a business bad debt; therefore, you are allowed to take a bad debt deduction for partial worthlessness. You will be able to take a bad debt deduction in the current year of $26,000 ($30,000 – $4,000) based on partial worthlessness.

Should you need more information or need to clarify anything, please contact me.

Sincerely,

John J. Jones, CPAPartner

7-8 2005 Comprehensive Volume/Solutions Manual

TAX FILE MEMORANDUM

January 29, 2004

From: John J. Jones

Subject: Bad Debt Deduction

John Johnson’s $30,000 loan to Sara is a business bad debt. Therefore, a bad debt deduction is allowed for partial worthlessness of $26,000 (i.e., Sara has filed for bankruptcy and John has been notified that the most he can expect to receive is $4,000). John will be able to claim an additional bad debt deduction in the year when a final settlement has been reached with respect to the loan assuming the amount collected is less than $4,000.

pp. 7-3 to 7-5

27. In 2003, Sue has no bad debt deduction. No attempt has been made to collect on the loan and no deduction is allowed for partial worthless of a nonbusiness bad debt. In 2004, Sue is allowed a bad debt deduction of $5,000 ($6,000 debt – $1,000 received). The loss will be treated as a short-term capital loss and, as such, can only be used to offset only $3,000 of ordinary income if Sue does not have any capital gains. pp. 7-4 and 7-5

28. The bad debt is a business bad debt. However, the amount of Ron’s bad debt is limited to Ron’s basis in the debt. Therefore, the bad debt of $80,000 (80% X $100,000 face value of the receivable) is limited to a deduction of $72,000 for Ron; that is, his basis in the debt. p. 7-4

29. Salary $180,000§ 1244 ordinary loss (95,000) Short-term capital gain on § 1244 stock $25,000Short-term capital loss (nonbusiness bad debt) (7,000)Net short-term capital gain 18,000Adjusted gross income $103,000

pp. 7-4 to 7-8

30. Sell all of the stock in the current year:

Current year’s AGISalary $80,000Ordinary loss (§ 1244 limit) (50,000)Long-term capital gain $ 8,000Long-term capital loss (30,000) ($80,000 – $50,000)Long-term capital loss (limit) (3,000 )AGI $27,000

Next year’s AGISalary $90,000Long-term capital gain $10,000Long-term capital loss carryover (19,000) ($30,000 – $11,000)

Deductions and Losses: Certain Business Expenses and Losses 7-9

Long-term capital loss (limit) (3,000 )AGI $87,000

Total AGICurrent year $ 27,000Next year 87,000 Total $114,000

Sell half of the stock this year and half next year:

Current year’s AGISalary $80,000Ordinary loss (§ 1244 stock) (40,000)Long-term capital gain 8,000AGI $48,000

Next year’s AGISalary $90,000Ordinary loss (§ 1244 stock) (40,000)Long-term capital gain 10,000AGI $60,000

Total AGICurrent year $ 48,000Next year 60,000Total $108,000

Mary’s combined AGI for the two years is lower if she sells half of her § 1244 stock this year and half next year. pp. 7-7 and 7-8

31. Casualty gainHome [$70,000 – ($400,000 – $350,000)] $20,000

Casualty lossCar [$20,000 – ($55,000 – $0)] ($35,000)Contents [$10,000 – ($60,000 – $10,000)] (40,000)Total ($75,000)Less: $100 floor (100)

($74,900)

Casualty loss in excess of casualty gain ($54,900)Less: 10% AGI (10% X $100,000) (10,000 )Total itemized deduction ($44,900)

pp. 7-11 to 7-16

32. The loss is a business loss. Therefore, for the farm building and the farm equipment that were completely destroyed, the adjusted basis is used in calculating the amount of the casualty loss. For the barn that was damaged, the lower of the adjusted basis or the decline in value is used in calculating the amount of the casualty.

Building ($90,000 – $70,000) $20,000Equipment ($40,000 – $25,000) 15,000

7-10 2005 Comprehensive Volume/Solutions Manual

Barn ($50,000 – $25,000) 25,000Total loss $60,000Because the President declared the area a disaster area, Olaf and Anna could claim the loss on last year’s return or on the current year’s tax return.

If Olaf applies the loss to the prior year, the benefit of the loss will be at a tax rate of 28%. If the loss is applied to the current year, the benefit will be at a tax rate of 33% rather than 28% and thus, provide a tax savings of $19,800 ($60,000 X 33%) rather than $16,800 ($60,000 X 28%).

Olaf should include the loss on the current year’s tax return, since the tax savings is $3,000 ($19,800 – $16,800) greater.

pp. 7-8 to 7-16

33. Business Personal Portion Portion

Total (50%) (50%)

Cost $800,000 $400,000 $400,000Depreciation (150,000) (150,000) -0-Adjusted basis $650,000 $250,000 $400,000

Loss on building:Loss ($900,000 – $200,000) $700,000 $250,000* $350,000Less: Insurance reimbursement $600,000 (300,000)(300,000)Loss (gain) ($ 50,000)$ 50,000

Business contents loss $220,000Less: Insurance recovery (175,000)Loss $ 45,000

AGI before effects of accident $100,000Business gain—building 50,000Business loss—contents (45,000 )AGI $105,000

Personal casualty loss—building $ 50,000Personal casualty loss—contents ($65,000 – $65,000) -0-Less: $100 per event floor (100)

10% of AGI floor (10% X $105,000) (10,500 )Itemized deduction $ 39,400

*Adjusted basis is less than the decline in FMV of $350,000 ($700,000 X 50%).

pp. 7-8 to 7-16

Deductions and Losses: Certain Business Expenses and Losses 7-11

34. Willis, Hoffman, Maloney, and Raabe, CPAs5191 Natorp Boulevard

Mason, OH 45040

January 26, 2004

Mr. Sam Smith450 Colonel’s WayWarrensburg, MO 64093

Dear Mr. Smith:

This letter is to inform you of the tax and cash flow consequences of filing a claim versus not filing a claim with your insurance company for reimbursement for damages to your business use car.

If an insurance claim is filed, you will have a taxable gain of $2,000 computed as follows:

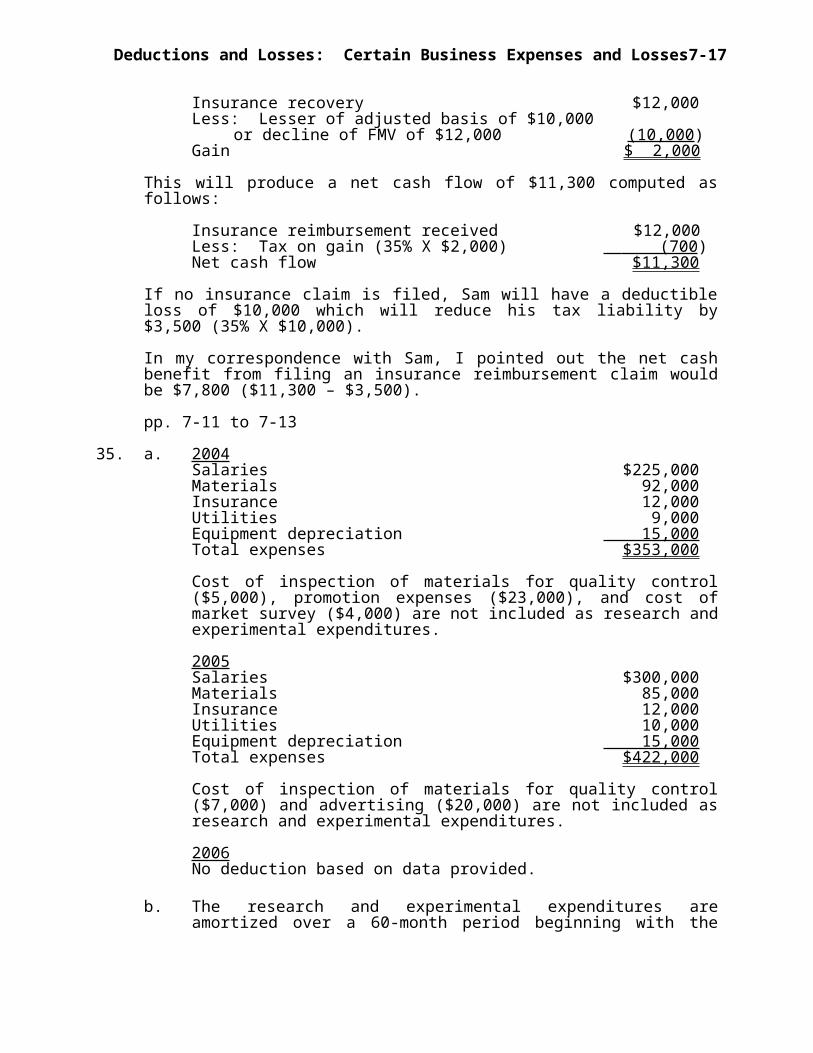

Insurance recovery $12,000Less: Lesser of adjusted basis of $10,000 or decline of FMV of $12,000 (10,000)Gain $ 2,000

This will produce a net cash flow of $11,300 computed as follows:

Insurance reimbursement received $12,000Less: Tax on gain (35% X $2,000) (700 )Net cash flow $11,300

If no insurance claim is filed, you will have a deductible loss of $10,000 which will reduce your tax liability by $3,500 (35% X $10,000).

The net cash benefit resulting from filing an insurance reimbursement claim would be $7,800 ($11,300 – $3,500).

Should you need more information or need to clarify anything, please contact me.

Sincerely,

John J. Jones, CPAPartner

TAX FILE MEMORANDUM

January 26, 2004

From: John J. Jones

Subject: Tax consequences for Sam Smith if he does not file an insurance claim for reimbursement for damages to his business use car

If an insurance claim is filed, Sam will have taxable gain of $2,000 computed as follows:

7-12 2005 Comprehensive Volume/Solutions Manual

Insurance recovery $12,000Less: Lesser of adjusted basis of $10,000 or decline of FMV of $12,000 (10,000)Gain $ 2,000

This will produce a net cash flow of $11,300 computed as follows:

Insurance reimbursement received $12,000Less: Tax on gain (35% X $2,000) (700 )Net cash flow $11,300

If no insurance claim is filed, Sam will have a deductible loss of $10,000 which will reduce his tax liability by $3,500 (35% X $10,000).

In my correspondence with Sam, I pointed out the net cash benefit from filing an insurance reimbursement claim would be $7,800 ($11,300 – $3,500).

pp. 7-11 to 7-13

35. a. 2004Salaries $225,000Materials 92,000Insurance 12,000Utilities 9,000Equipment depreciation 15,000Total expenses $353,000

Cost of inspection of materials for quality control ($5,000), promotion expenses ($23,000), and cost of market survey ($4,000) are not included as research and experimental expenditures.

2005Salaries $300,000Materials 85,000Insurance 12,000Utilities 10,000Equipment depreciation 15,000Total expenses $422,000

Cost of inspection of materials for quality control ($7,000) and advertising ($20,000) are not included as research and experimental expenditures.

2006No deduction based on data provided.

b. The research and experimental expenditures are amortized over a 60-month period beginning with the month in which the taxpayer first realizes benefits from the experimental expenditures (i.e., July 2006 for Blue Corporation). The monthly amortization is $12,917 ($775,000 ÷ 60)

2004No deduction for research and experimental expenditures.

Deductions and Losses: Certain Business Expenses and Losses 7-13

2005No deduction for research and experimental expenditures.

2006Deduction for research and experimental expenditures:

$12,917 X 6 months = $77,502

pp. 7-16 to 7-18

36. Salary $40,000Interest income 1,000Business bad debt (2,000)Nonbusiness bad debt (short-term capital loss) ($6,000) Short-term capital loss (3,000) Total short-term capital loss ($9,000) Long-term capital gain 4,000Net short-term capital loss ($5,000) Capital loss limit ( 3,000 )Adjusted gross income $36,000

pp. 7-3 to 7-5

37. Salary $40,000Interest income 1,000Business bad debt (2,000)Nonbusiness bad debt ($ 6,000) Short-term capital loss (3,000 ) Total short-term capital loss ($ 9,000) Short-term capital gain* 10,000Net short-term capital gain 1,000Long-term capital gain $ 4,000Long-term capital loss* (1,000) Net long-term capital gain 3,000Adjusted gross income $43,000

*Personal casualty gains exceed personal casualty losses ($10,000 – $1,000 = $9,000) and therefore, all personal casualty items are treated as capital gains and losses.

pp. 7-3 to 7-5 and 7-14 to 7-16

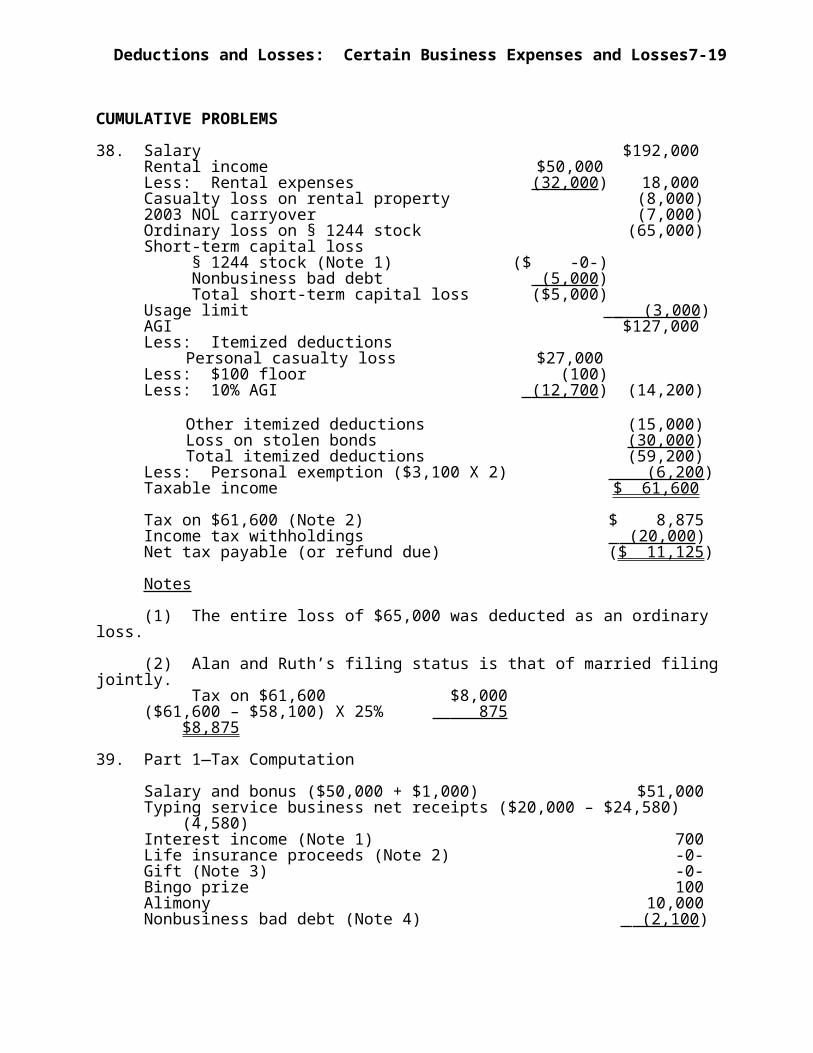

CUMULATIVE PROBLEMS

38. Salary $192,000Rental income $50,000Less: Rental expenses (32,000) 18,000Casualty loss on rental property (8,000)2003 NOL carryover (7,000)Ordinary loss on § 1244 stock (65,000)Short-term capital loss

7-14 2005 Comprehensive Volume/Solutions Manual

§ 1244 stock (Note 1) ($ -0-)Nonbusiness bad debt (5,000)Total short-term capital loss ($5,000)

Usage limit (3,000 )AGI $127,000Less: Itemized deductions

Personal casualty loss $27,000Less: $100 floor (100)Less: 10% AGI (12,700 ) (14,200)

Other itemized deductions (15,000)Loss on stolen bonds (30,000)Total itemized deductions (59,200)

Less: Personal exemption ($3,100 X 2) (6,200)Taxable income $ 61,600

Tax on $61,600 (Note 2) $ 8,875Income tax withholdings (20,000 )Net tax payable (or refund due) ($ 11,125)

Notes

(1) The entire loss of $65,000 was deducted as an ordinary loss.

(2) Alan and Ruth’s filing status is that of married filing jointly.Tax on $61,600 $8,000

($61,600 – $58,100) X 25% 875 $8,875

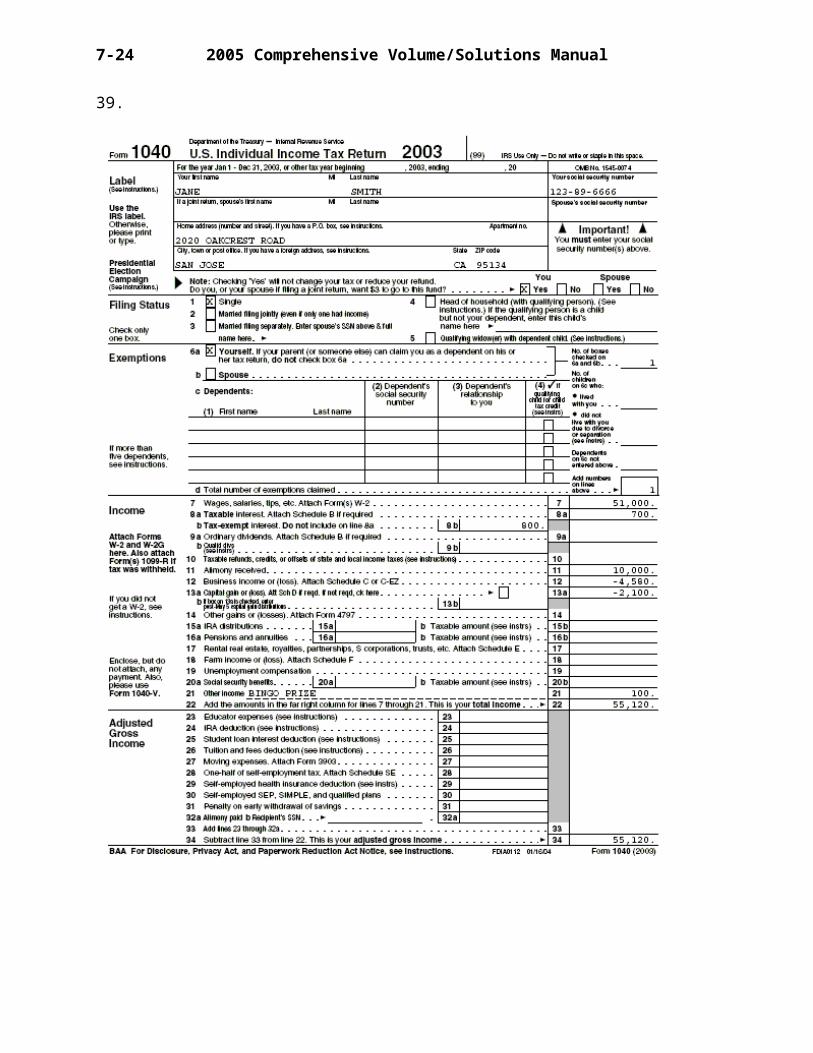

39. Part 1—Tax Computation

Salary and bonus ($50,000 + $1,000) $51,000Typing service business net receipts ($20,000 – $24,580) (4,580)Interest income (Note 1) 700Life insurance proceeds (Note 2) -0-Gift (Note 3) -0-Bingo prize 100Alimony 10,000Nonbusiness bad debt (Note 4) (2,100 )Adjusted gross income $55,120Less: Itemized deductions

Home mortgage interest $9,000Casualty loss: Lesser of adjusted basis

of $4,000 or FMV of $5,000 $4,000Less: Insurance proceeds (1,500)

$2,500Less: $100 floor (100) Less: 10% AGI floor (5,512) -0- Total itemized deductions (9,000)

Less: Personal exemption (3,050 )Taxable income $43,070

Deductions and Losses: Certain Business Expenses and Losses 7-15

Tax on taxable income (from Tax Table) $ 7,579Less: Federal income tax withheld and estimated tax payments

($7,500 + $1,000) (8,500 )Net tax payable (or refund due) for 2003 ($ 921)

Notes

(1) The $800 interest on the City of San Jose bonds is tax-exempt.

(2) Life insurance proceeds of $60,000 payable as the result of the death of Jane’s sister are excludible from gross income.

(3) The $5,000 gift from Jane’s aunt is excludible from gross income.

(4) The $2,100 loss on the loan to her friend, Joan Jensen, is deductible as a nonbusiness bad debt (i.e., short-term capital loss).

See the tax return solution beginning on page 7-18 of the Solutions Manual.

Part 2—Tax Planning

Salary and bonus $51,000Gross receipts from business $26,000Less:

Office rent $7,000Supplies 4,840Utilities and telephone 5,148Wages 5,500Payroll taxes 550Equipment rentals 3,300 (26,338)

Net business income (338)Interest income 700Alimony 10,000Adjusted gross income $61,362Less:

Itemized deductions $ 9,000Personal exemption 3,100 (12,100 )

Taxable income $49,262

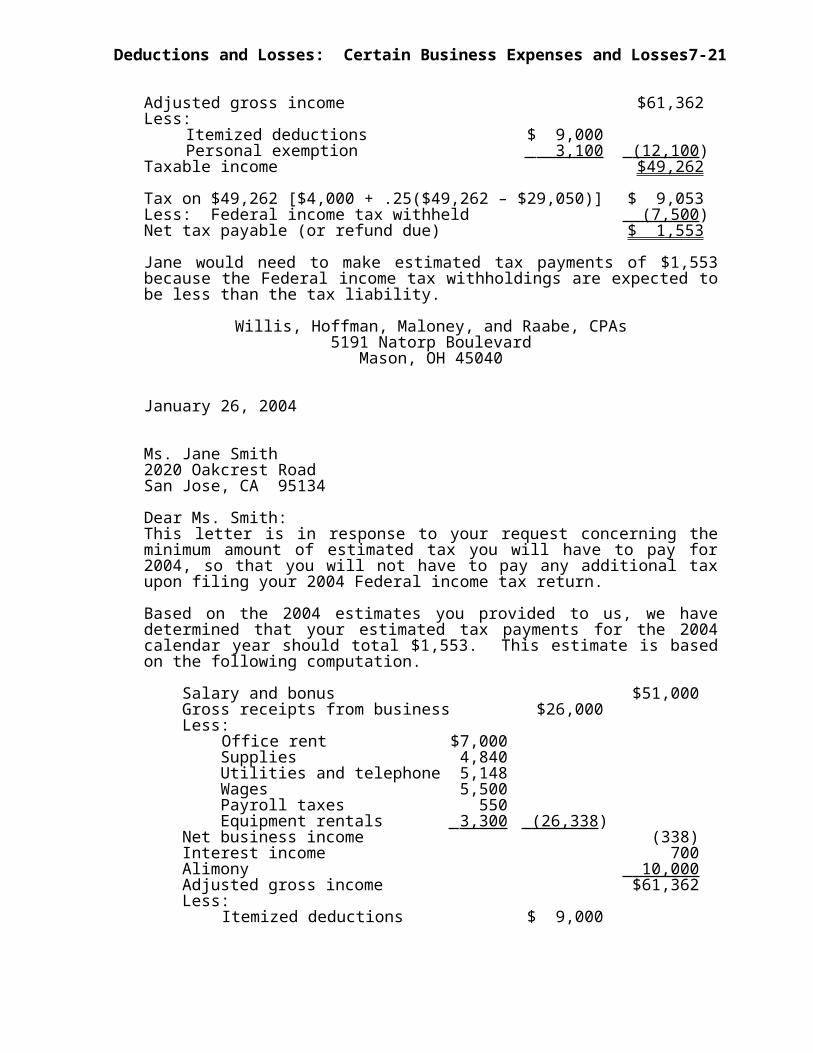

Tax on $49,262 [$4,000 + .25($49,262 – $29,050)] $ 9,053Less: Federal income tax withheld (7,500)Net tax payable (or refund due) $ 1,553

Jane would need to make estimated tax payments of $1,553 because the Federal income tax withholdings are expected to be less than the tax liability.

Willis, Hoffman, Maloney, and Raabe, CPAs5191 Natorp Boulevard

Mason, OH 45040

January 26, 2004

7-16 2005 Comprehensive Volume/Solutions Manual

Ms. Jane Smith2020 Oakcrest RoadSan Jose, CA 95134

Dear Ms. Smith:This letter is in response to your request concerning the minimum amount of estimated tax you will have to pay for 2004, so that you will not have to pay any additional tax upon filing your 2004 Federal income tax return.

Based on the 2004 estimates you provided to us, we have determined that your estimated tax payments for the 2004 calendar year should total $1,553. This estimate is based on the following computation.

Salary and bonus $51,000Gross receipts from business $26,000Less:

Office rent $7,000Supplies 4,840Utilities and telephone 5,148Wages 5,500Payroll taxes 550Equipment rentals 3,300 (26,338 )

Net business income (338) Interest income 700Alimony 10,000 Adjusted gross income $61,362Less:

Itemized deductions $ 9,000Personal exemption 3,100 (12,100)

Taxable income $49,262

Tax on $49,262 $ 9,053Less: Federal income tax withheld (7,500 )Net tax payable $ 1,553

Should you need more information or need to clarify anything, please contact me.

Sincerely yours,

John J. Jones, CPAPartner

TAX FILE MEMORANDUM

January 10, 2004

From: John J. Jones

Subject: Jane Smith’s 2004 estimated tax

Deductions and Losses: Certain Business Expenses and Losses 7-17

Today I talked with Jane Smith concerning her 2004 estimated tax. She wanted to know the minimum amount of estimated tax she would have to pay for the calendar year 2004 so that she would not have to pay any additional tax upon filing her 2004 Federal income tax return.

The following projections for 2004 were provided by Jane Smith:

Items remaining unchanged from 2003:Salary—$50,000Christmas bonus—$1,000Interest expense on home mortgage—$9,000Interest income—$700Alimony—$10,000

Gross receipts from typing services—$26,000Office rent will remain unchanged—$7,000

All other expenses for typing services will increase 10% from 2003:Supplies—$4,400 in 2003; $4,840 in 2004Utilities and telephone—$4,680 in 2003; $5,148 in 2004Wages—$5,000 in 2003; $5,500 in 2004Payroll taxes—$500 in 2003; $550 in 2004Equipment rentals—$3,000 in 2003; $3,300 in 2004

The following 2003 items will not recur in 2004:Life insurance proceeds—$60,000Gift—$5,000Bingo winnings—$100Bad debt—$2,100Stolen silverware

Based on these estimates for 2004, Jane Smith should make 2004 estimated tax payments totaling $1,553. The determination was made as follows:

Salary and bonus $51,000Gross receipts from business $26,000Less:

Office rent $7,000Supplies 4,840Utilities and telephone 5,148Wages 5,500Payroll taxes 550Equipment rentals 3,300 (26,338)

Net business income (338)Interest income 700Alimony 10,000Adjusted gross income $61,362Less:

Itemized deductions $ 9,000Personal exemption 3,100 (12,100)

Taxable income $49,262

7-18 2005 Comprehensive Volume/Solutions Manual

Tax on $49,312 $ 9,053Less: Federal income tax withheld (7,500 )Net tax payable $ 1,553

The answers to the Research Problems are incorporated into the 2005 Comprehensive Volume of the Instructor’s Guide with Lecture Notes to Accompany WEST FEDERAL TAXATION: COMPREHENSIVE VOLUME.

Deductions and Losses: Certain Business Expenses and Losses 7-19

39.

7-20 2005 Comprehensive Volume/Solutions Manual

39. continued

Deductions and Losses: Certain Business Expenses and Losses 7-21

39. continued

7-22 2005 Comprehensive Volume/Solutions Manual

39. continued

Deductions and Losses: Certain Business Expenses and Losses 7-23

39. continued

7-24 2005 Comprehensive Volume/Solutions Manual

39. continued

Deductions and Losses: Certain Business Expenses and Losses 7-25

39. continued

![[PPT]PowerPoint Presentation · Web viewJane Logue and Jayne Stewart - Learner Voice Wendy Burton and Jackie Howie – CPD\CPL Document title Transforming lives through learning](https://static.fdocuments.in/doc/165x107/5b3525987f8b9a7e4b8cdcc5/pptpowerpoint-presentation-web-viewjane-logue-and-jayne-stewart-learner.jpg)