Chapter 7: Geospatial Database CHAPTER 7 Development of a ...

description

Chapter 7

Learning Objectives (part 1 of 3)

Describe the different types of installment loans

Compute the monthly payment for an installment loan

Explain why a monthly payment is not one-twelfth of an annual payment

Construct a loan amortization table and explain the two reasons why it is important

Learning Objectives (part 2 of 3)

Show the impact on the amortization table of adding extra principal to a payment

Explain how an add-on rate loan works

Construct an amortization table for an add-on rate loan

Identify the lenders who most commonly provide installment loans

Learning Objectives (part 3 of 3)

Evaluate whether it is better to take out an auto loan or a home equity loan to buy an auto

Discuss what happens when you default on a loan with collateral

List the protections a consumer has from a debt collector

Discuss the two primary chapters for declaring bankruptcy: 7 and 13

Describe how bankruptcy works under each chapter

Types of Installment Loans Auto Loan

New or Used Home Improvement Loan Marine loan Signature Secured Personal Loan

Household goods Certificate of Deposit

Computation of Monthly Payment

Payment x PVIFA = Loan Amount Payment = the payment made each

period PVIFA = the present value interest factor

for the annuity based on the number of payments and the interest rate of the loan

Loan Amount = Amount initially borrowed Payment = Loan Amount / PVIFA

Example #1 (annual payments)

Andy wants to take out a $10,000 home improvement loan. His local bank indicates he can have a five-year loan at an 8 percent interest rate with annual payments. What would his annual payment be?

Answer: $10,000 / 3.9927 = $2,504.56

Example #2 (annual payments)

Andy wants to take out a $10,000 home improvement loan. His local bank indicates he can have a five-year loan at an 8 percent interest rate with monthly payments. What would his monthly payment be?

Answer: $10,000 / 49.3169 = $202.77

Relationship of monthly payment to annual payment

Monthly payment is less than one-twelth the annual payment because the monthly payment allows a faster pay down of principal, which allows lower interest charges over time.

Loan Amortization Table Two reasons why it is important

Indicates how much would be owed if loan were paid off at any point in time (lenders occasionally miscalculate this number)

Indicates how much of each payment is interest, in case the interest on the loan is tax deductible.

Example of a Loan Amortization Table

Loan = $1,000, Term = 12 monthsInterest Rate = 12 percent

Mo. Beginning PMT Interest Repay. End# of Month of Prin. Of Month1 $1,000.00 $88.85 $10.00 $78.85 $921.152 $921.15 $88.85 $9.21 $79.64 $841.53 $841.51 $88.85 $8.42 $80.43 $761.08

Impact of Adding Money to a Payment

Loan terms same as previous exampleAdd $100 to first payment

Mo. Beginning PMT Interest Repay. End# of Month of Prin. Of Month1 $1,000.00 $188.85 $10.00 $178.85 $821.152 $821.15 $88.85 $8.21 $80.64 $741.513 $741.51 $88.85 $7.41 $81.44 $659.07

How an add-on rate loan works

Total Interest Due = Amount Borrowed x add-on rate x Maturity in Years

Monthly Payment = (Amount Borrowed + Interest) / Maturity in months

Amortization of interest based on Rule of 78

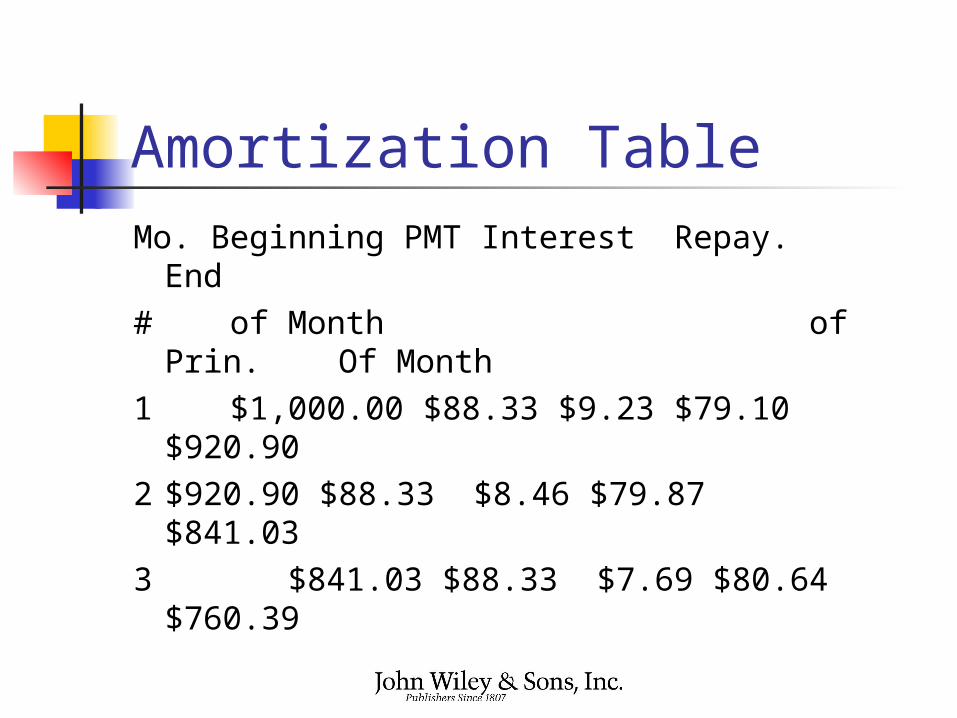

Example

$1,000 at 6% add-on rate for one year

Interest = $1,000 x .06 x 1 year = $60

Monthly payment = ($1,000 + $60) / 12 months = $88.33

Amortization TableMo. Beginning PMT Interest Repay. End# of Month of Prin. Of Month1 $1,000.00 $88.33 $9.23 $79.10

$920.902 $920.90 $88.33 $8.46 $79.87

$841.033 $841.03 $88.33 $7.69 $80.64

$760.39

Lenders of Installment Loans Commercial banks Mutual Savings banks Savings & Loans Credit Unions Consumer Finance Company

Auto Loan vs. Home Equity Loan to buy an auto Higher fees for a home equity loan Interest deductible on home equity

loan With auto loan, loan is due if auto sold If pay off loan early enough, auto loan

may be cheaper despite non-deductibility of interest

With home loan, lose home if default

Loan defaults Always better to try to work out an

adjustment directly with lender After default, lender may seize

property pledged as collateral If collateral sold, borrower still

owes if sale net proceeds are insufficient to cover the principal due

Protections from a debt collector

Defined by the Fair Debt Collection Practices Act

Contact only between 8 am and 9 pm

No contact at work if know employer disapproves

May not harass, oppress, or abuse, and may not lie

Declaring Bankruptcy Chapter 7

Liquidation chapter Chapter 13

Reorganization chapter

Chapter 7 Bankruptcy Exempt & Nonexempt property Nonexempt is sold & proceeds

turned over to creditors All debt that can be discharged is

so done, Stays on record for 10 years

Chapter 13 bankruptcy Can use only if owe less than

$250,000 in unsecured debt $750,000 in secured debt

Works like a court imposed debt consolidation loan

Stays on record for 7 years No mercy shown if fail to make

promised payments

![Chapter 7 [Chapter 7]](https://static.fdocuments.in/doc/165x107/61cd5ea79c524527e161fa6d/chapter-7-chapter-7.jpg)