CHAPTER 6: BUSINESS FORMATION Choosing the Form that Fits.

16

CHAPTER 6: BUSINESS FORMATION Choosing the Form that Fits

-

Upload

isaac-garrett -

Category

Documents

-

view

254 -

download

3

Transcript of CHAPTER 6: BUSINESS FORMATION Choosing the Form that Fits.

CHAPTER 6: BUSINESS FORMATION

Choosing the Form that Fits

CHOICES, CHOICES, CHOICES

The form of ownership of a business is a big decision.

Form of ownership affects:

• Operation• Start-up Costs• Profit Distribution• Taxes• Management Succession plans• Liability Exposure• Managerial Ability• Business Goals

The “Big Three” is Becoming the “Big Four”:

• Sole Proprietorship• Partnership• Corporation• Limited Liability

Company

BUSINESS FORMS: COMPARING THE NUMBERS

SOLE PROPRIETORSHIP: BUSINESS AT ITS MOST BASIC

Advantages: Ease of Formation

Retention of Control

Pride of Ownership

Retention of Profits

Possible Tax Advantages

Disadvantages: Limited Financial

Resources

Unlimited Liability

Limited ability to attract and maintain talented employees

Lack of Permanence

MOST COMMON TYPES OF SOLE PROPRIETORSHIPS

Source for Table: “Sole Proprietorship Returns”, by Kevin Pierce Statistics of Income Bulletin, Summer, 2005, Figure A, p.9; website: http://www.irs.gov/pub/irs-soi/03solp.pdf )

PARTNERSHIPS: TWO HEADS CAN BE BETTER THAN ONE

Advantages: Pooled Financial

Resources

Shared Responsibilities

Ease of Formation

Tax Advantages

Disadvantages: Unlimited Liability

Disagreements

Difficulty in withdrawing from agreement

Lack of Continuity

GENERAL VS LIMITED PARTNERSHIPS

General Partnerships All partners have the right to participate in

the management of the firm and share in any profits/losses.

Limited Partnerships All partners contribute financially and

share in the profits but the limited partner(s) cannot actively participate in management have limited liability

LIMITED PARTNERSHIPS

Limited Partnership – includes at least one

general partner and at least one limited partner

Limited Liability Partnership – All partners are actively

involved but they have some form of limited liability. The

amount of liability differs per state.

CORPORATIONS: AN ARTIFICIAL REALITY A corporation is a legal entity, separate

and distinct from its owners. Corporations are owned by stockholders. The Board of Directors

Elected by stockholders to oversee the operation of their company and protect their interests

Oversee the operation of corporation and protect investors’ interest

Establish mission and set objectives

Rarely get involved in day-to-day management

Responsible for monitoring the performance of the corporate officers

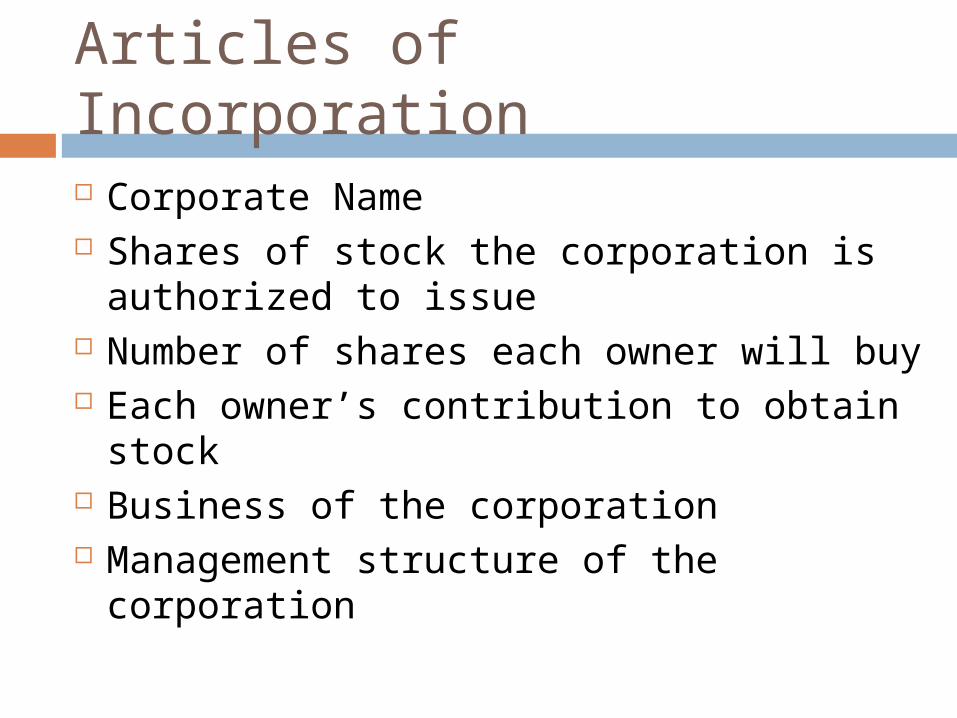

Articles of Incorporation

Corporate Name Shares of stock the corporation is

authorized to issue Number of shares each owner will buy Each owner’s contribution to obtain stock Business of the corporation Management structure of the corporation

CORPORATIONS

Advantages: Limited Liability

Permanence

Easy to Transfer Ownership

Ability to Raise Capital

Specialized Management

Disadvantages: Expense/complexity of

formation and operation

Double Taxation

Paperwork and Regulation

Conflicts of Interest

LIMITED LIABILITY COMPANY: THE NEW KID ON THE BLOCK

Advantages: Limited Liability

Tax Pass-Through

Simplified Management and Operation

Flexible Ownership

Disadvantages: Franchise Taxes

Foreign Status in other States

State Law Differences

Limited to Select Industries

COMPARING BUSINESS FORMS

SoleProprietorshi

ps

Partnerships Corporations

LOW HIGH

HIGH LOW

DEGREE OF COMPLEXITY AND PERPETUITY

DEGREE OF PERSONAL LIABILITY

CORPORATE RESTRUCTURING

Large corporations constantly look for ways to grow and

achieve competitive advantage.

Mergers – two companies agree to a

combination of equals.

Acquisitions – when one firm buys

another.

TYPES OF MERGERS AND ACQUISITIONS

Type of Merger

Definition Objective Example

Horizontal Combine firms in same industry.

•Increase size•Increase market

power•Gain efficiency

AT&T and SBC

Vertical Combine companies with

buyer-seller relationship.

•Provide tighter integration and increase control

Time Warner and

Turner Broadcasti

ng

Conglomerate

Combination of unrelated

companies.

•Increase company’s diversity.

GE acquiring

RCA

DIVESTITURES: WHEN LESS IS MORE

Divestitures allow the firm to streamline their operations and focus

Spin-off – setting up the division or part of the business as a separate company

Sell stock to existing stockholders

Carve-out – setting up a separate business from an operation

Sell stock to outside investors