Chapter 6

21

6-1 Chapter 6 The Risk of Changing Interest Rates

-

Upload

thomas-baxter -

Category

Documents

-

view

13 -

download

0

description

Chapter 6. The Risk of Changing Interest Rates. Short Horizon Investors. Maturity. 0. 1. n. Time. P 0. P 1. y 0. y 1. P 1 , the price at Time 1, is important. Long Horizon Investors. Maturity. 0. 1. 2. n. Time. P 0. C. C. C + PAR. Reinvest. - PowerPoint PPT Presentation

Transcript of Chapter 6

6-1

Chapter 6

The Risk of Changing Interest

Rates

6-2

Short Horizon Investors

nMaturity

Time

P1, the price at Time 1, is important.

P0 P1

y0 y1

10

6-3

Long Horizon Investors

P0 C C + PAR

Maturity

Time

Reinvest

Value at some distant date n is important.

10 2

C

n

6-4

Bond Price

Interest Rates

n2 )y1(

Parc

)y1(

c

y1

cP

6-5

Bond Price

Interest Rates

Actual Price

Change

P0

P1

y1y0

6-6

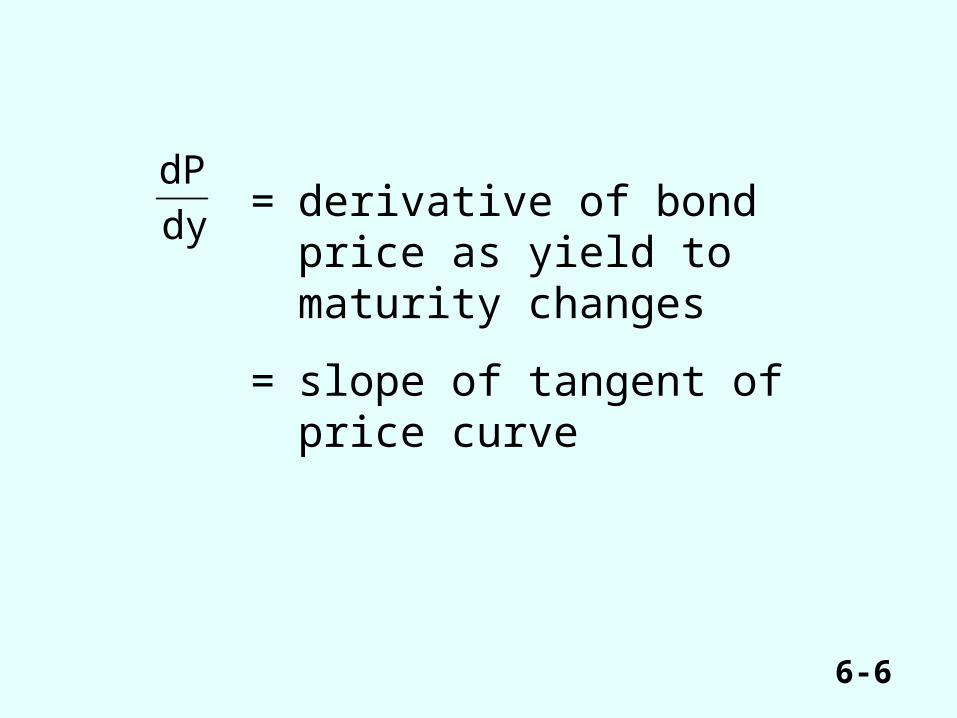

dy

dP= derivative of bond price as

yield to maturity changes

= slope of tangent of price curve

6-7

Duration as an Approximation of Price Change

Price

Interest rate

Slope of tangent equals numerator of durationActual price change equals P0 P1

Duration approximation of price changeequals P0 P´1

Price

Tangent

P0

P1

P´1

y0 y1

6-8

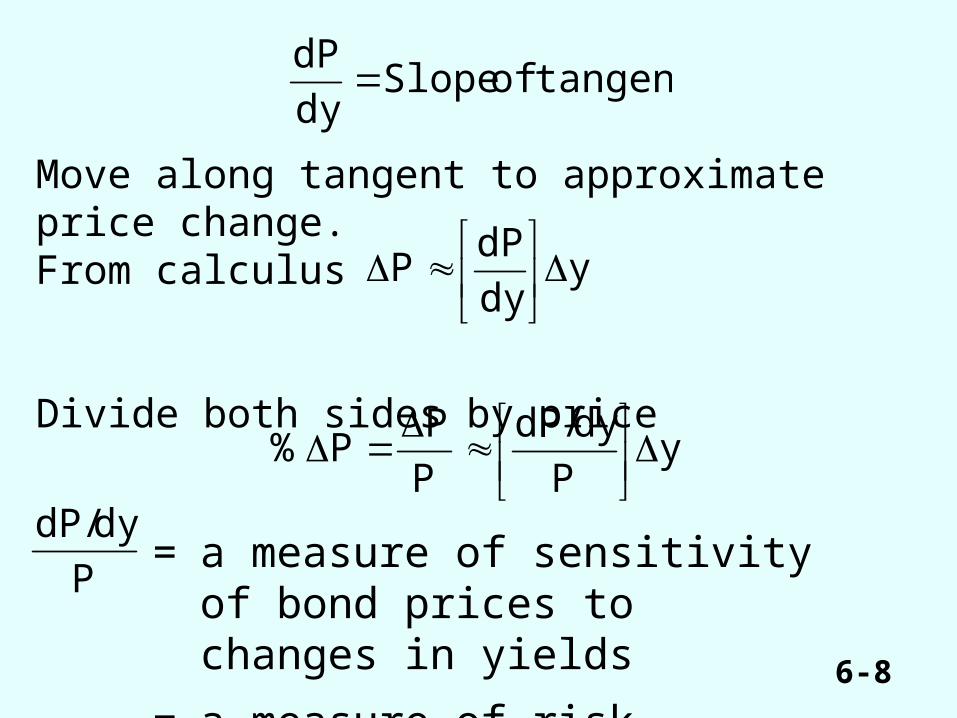

tangent of Slope dy

dP

Move along tangent to approximate price change.From calculus

Divide both sides by price

ydy

dPP

yP

dy/dP

P

PP%

P

dy/dP= a measure of sensitivity of bond

prices to changes in yields

= a measure of risk

6-9

Percent Price [Duration][Yield Change].Change

P

dy/dPis called “modified” duration.

6-10

Macaulay’s Duration (DUR)

Often used by short horizon investors as a measure of price sensitivity.

DUR= % change in price as yield changes

DUR = .-[dP /dy](1 + y)

Price

6-11

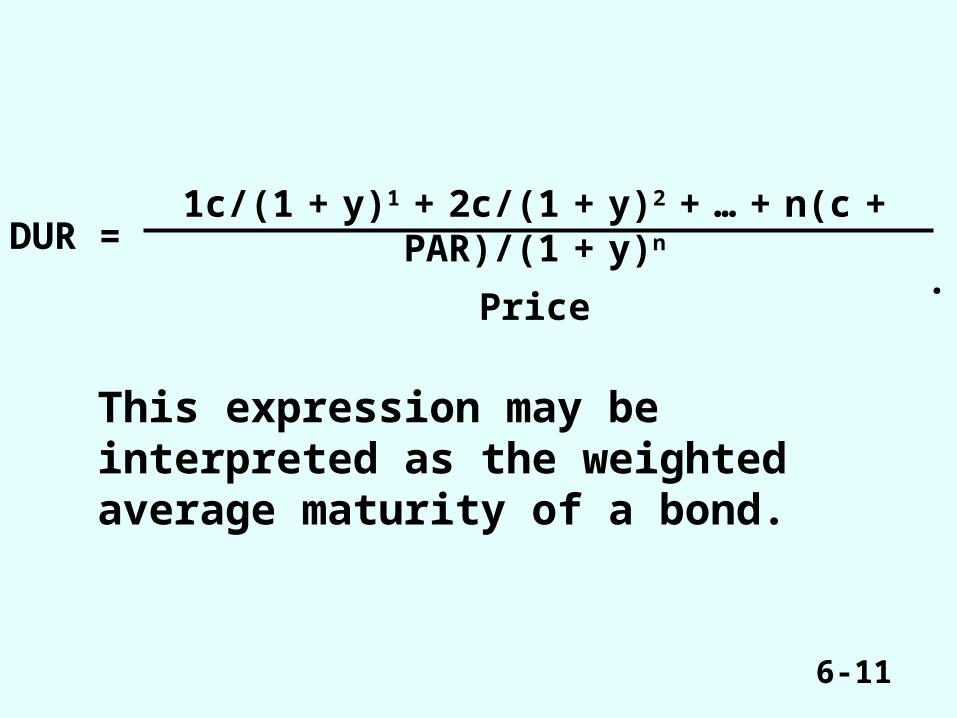

This expression may be interpreted as the weighted average maturity of a bond.

DUR = .

1c/(1 + y)1 + 2c/(1 + y)2 + … + n(c + PAR)/(1 + y)n

Price

6-12

Macaulay’s Duration for Special Types of Bonds

Bond Price Volatilities for Special Types of Bonds

Type of bond Duration

Zero-coupon n

Par

Perpetual (1 + y)/y

)PVA)(y1( y,n

6-13

Simplified Way of Computing Macaulay’s Duration

6-14

Duration for Various Coupons and Maturities YTM of 8%

Coupon

Maturity 0 0.04 0.06 0.08 0.10 0.121 1 1 1 1 1 1 5 5 4.59 4.44 4.31 4.20 4.11

10 10 8.12 7.62 7.25 6.97 6.7415 15 10.62 9.79 9.24 8.86 8.5720 20 12.26 11.23 10.60 10.18 9.8825 25 13.25 12.15 11.53 11.12 10.84 30 30 13.77 12.73 12.16 11.80 11.55

Note: Perpetual bond has duration of 1.08/0.08 = 13.50.

6-15

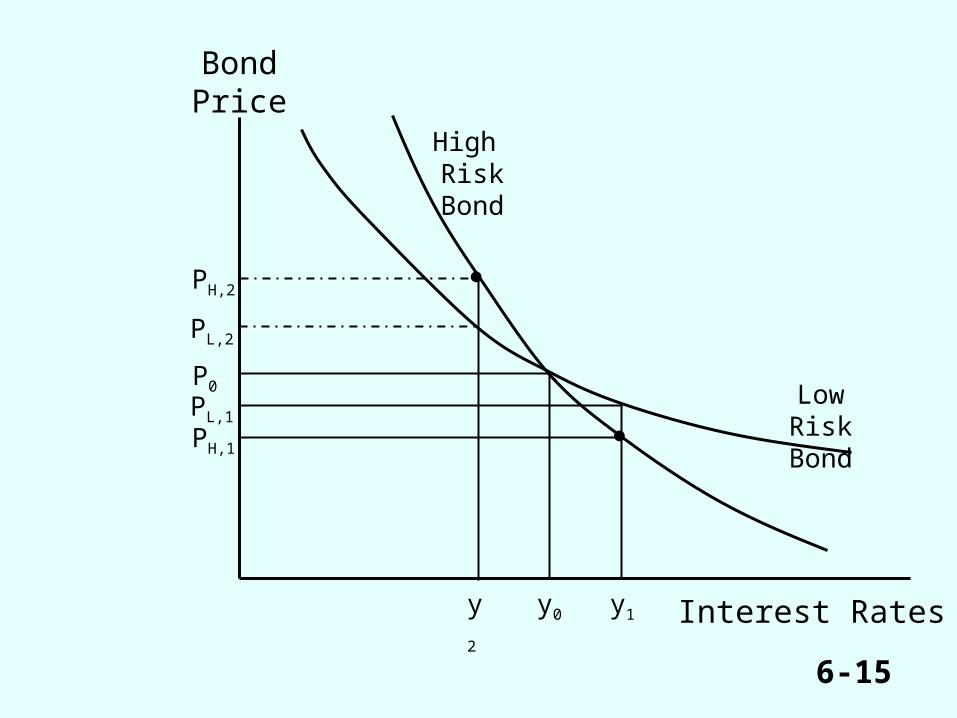

Bond Price

Interest Rates

P0

PH,2

y1y2

y0

High RiskBond

LowRisk Bond

PH,1

PL,1

PL,2

6-16

Duration versus MaturityDuration

Zero-c

oupon

Discount

ParPremium

1

1Maturity

1 + yy

1 + yy

.

6-17

(Risk)

Feasible

Low Risk

High Risk

30

Duration versus MaturityDuration

Zero-c

oupon

Discount

ParPremium

1

1Maturity

1 + yy

1 + yy

.

6-18

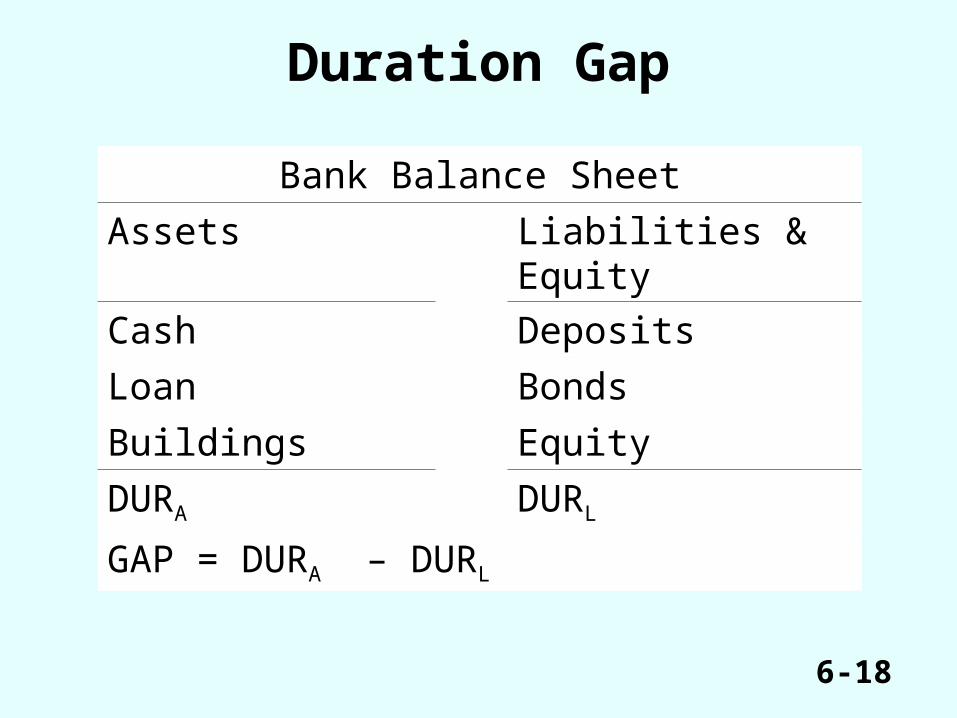

Duration Gap

Bank Balance Sheet

Assets Liabilities & Equity

Cash Deposits

Loan Bonds

Buildings Equity

DURA DURL

GAP = DURA – DURL

6-19

Immunization at a Horizon Date

Points in Time

0 n

The zero coupon strategy

Buy zero coupon bond-$P

Receive par value+$X

6-20

Points in Time0

Maturity strategy

Receive par + 1 coupon

2 n

Buy coupon-bearingbond

1

-$P +c +c c + Par

Reinvest coupons

. . .

Receive coupons

. . .

6-21

Points in Time0 n

Duration strategy

Buy coupon-bearingbond

Maturity of bond

1 2

-$P +c +c c + Par

Reinvest coupons

m. . .

. . .

Receive coupons + reinvest

Sell original bond + reinvested coupons

c

![CHAPTER 6 [Read-Only] 6.pdfCHAPTER 6 FRANCHISES. CHAPTER OBJECTIVES! ... step procedure suggested in the chapter.](https://static.fdocuments.in/doc/165x107/5ca1bdc188c993ce7d8cc542/chapter-6-read-only-6pdfchapter-6-franchises-chapter-objectives-step-procedure.jpg)