Chapter 5 transactions that affect revenue, expenses, and

25

Chapter 5

-

Upload

iva-walton -

Category

Economy & Finance

-

view

3.613 -

download

5

description

Lesson for effects on Owner Equity accounts

Transcript of Chapter 5 transactions that affect revenue, expenses, and

Chapter 5

Dave Thomas was the man behind Wendy’s International. The original restaurant in Columbus Ohio, open in 1969 and is called Wendy’s Old Fashioned Hamburgers.

What do you think?Wendy’s earns revenue by selling meals. Can you think of at least six examples of expenses that a Wendy’s restaurant might have?

Section 1

The reason for having temporary and permanent accounts.

The rules of debit and credit for revenue, expense, and withdrawal accounts

Temporary capital account

Permanent accounts

Supplies

Debit Credit

End. Bal. 875

Supplies

Debit Credit

Beg. Bal. 875

Beginning of Next Accounting Period

Owner’s Capital Account

Debit Credit

_ +

Decrease Increase

Side Side

Normal

Balance

1. A revenue account is increase (+) on the credit side

2. A revenue account is decreased (-) on the debit side

3. The normal balance for a revenue account is the increase side, or the credit side. Revenue accounts normally have credit balances

1. An expense account is increased on the debit side.

2. An expense account is decreased on the credit side.

3. The normal balance for an expense account is the increase side, or the debit side. Expense accounts normally have debit balances.

Computing the Balance in a T Account

To make it easier to find an account balance:1. Add amounts and write a sum total on each side

of the account2. Subtract the lesser subtotal from the other

subtotal to find the account balance.

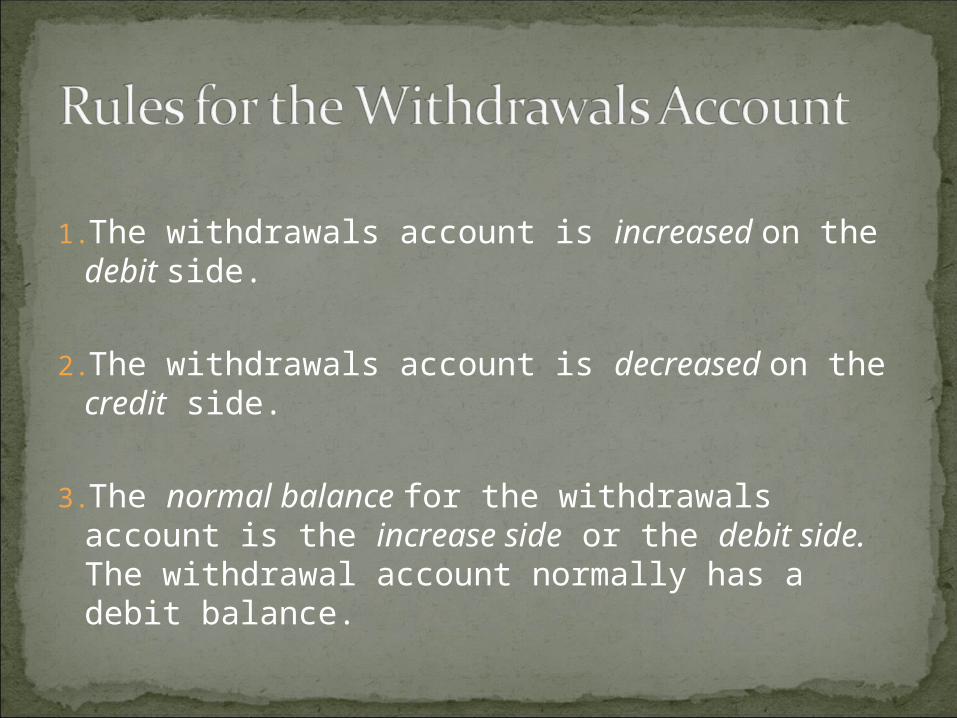

1.The withdrawals account is increased on the debit side.

2.The withdrawals account is decreased on the credit side.

3.The normal balance for the withdrawals account is the increase side or the debit side. The withdrawal account normally has a debit balance.

Debit and CreditsDebits are used to

1.Decrease (-) revenue2.Increase (+) expenses3.Increase (+) withdrawals Credits are used to:1.Increase (+) revenue2.Decrease (-) expenses3.Decrease (-) withdrawals

Using a Toll-Free NumberMany businesses offer a toll-free telephone line for customers and business associates. Suppose you’re an accountant for Procter & Gamble in Cincinnati, Ohio. Your friend Mike just moved to Houston and asks if your company has a 800 number he can use to call you. Your company does offer an 800 number, and you would like to hear from Mike. However, you also know that your company pays for each incoming call.

Ethical Decision Making: What are the ethical

issues? What are the

alternatives? Who are the affected

parties? Ho do the alternatives

affect the parties ? What would you do?

Problem 5-1

Section 2

How to analyze transactions that affect revenue, expense, and withdrawal accounts

Revenue recognition

On October 15, Roadrunner provided delivery services for the Sims Corporation. A check for $1,200 was received in full payment.

On October 16, Roadrunner mailed Check 103 for $700 to pay the month’s rent.

On October 18, Beacon Advertising prepared an advertisement for Roadrunner. Roadrunner will pay Beacon’s $75 fee later.

October 20, Roadrunner billed City News $1,450 for delivery services.

October 28, Roadrunner paid a $125 telephone bill with Check 104.

On October 29, Roadrunner wrote Check for $600 to have the office repainted.

On October 31, Maria Sanchez wrote check 106 to withdraw $500 cash for personal use.

Account Name Debit Balance Credit Balances

101 Cash in Bank $21,125

105 Accounts Receivables-City News

1,450

110 Accounts Receivables-Green Company

115 Computer Equipment 3000

120 Office Equipment 200

125 Delivery Equipment 12000

201 Accounts Payable – Beacon Advertising

75

205 Accounts Payable – North Shore Auto

11650

301 Maria Sanchez, Capital 25,400

302 Maria Sanchez, withdrawal 500

303 Income Summary

401 Delivery Revenue 2,650

501 Advertising Expense 75

505 Maintenance 600

510 Rent Expense 700

515 Utilities Expense 125

$39,775 $39,775

Thinking Critically --- page 109

Analyzing Accounting --- page 109

Problem 5-2 Identifying Accounts Affected by Transactions --- page 109