CHAPTER 5 DEDUCTIONS AND LOSSES: IN GENERAL …isu.indstate.edu/acharmo/smpdf/CH05.pdf ·...

32

CHAPTER 5 DEDUCTIONS AND LOSSES: IN GENERAL SOLUTIONS TO PROBLEM MATERIALS Status: Q/P Question/ Present in Prior Problem Topic Edition Edition 1 Allowed income and deductions Unchanged 1 2 Deductions for and from AGI Unchanged 2 3 Deductions from AGI Unchanged 3 4 Deductions for and from AGI Unchanged 4 5 Deductions for and from AGI Unchanged 5 6 Deductions for and from AGI Unchanged 6 7 Deductions for and from AGI; deduction disallowance New 8 Ordinary and necessary requirement Unchanged 8 9 Reasonable compensation Unchanged 9 10 Business versus nonbusiness losses Unchanged 10 11 Reporting procedures Unchanged 11 12 Method of accounting: cash versus accrual Unchanged 12 13 Actually paid requirement for cash basis taxpayer Unchanged 13 14 All events and economic performance tests Unchanged 14 15 Reserves and economic performance test Unchanged 15 16 Illegal activities Unchanged 16 17 Issue ID Unchanged 17 18 Legal expenses Unchanged 18 19 Illegal activities Unchanged 19 20 Political contributions Unchanged 20 21 Lobbying expenditures New 22 Excessive executive compensation New 23 Investigation of a business New 24 Hobby/business Unchanged 24 25 Vacation home rental: classification New 26 Vacation home rental: IRS approach versus court approach New 5-1

Transcript of CHAPTER 5 DEDUCTIONS AND LOSSES: IN GENERAL …isu.indstate.edu/acharmo/smpdf/CH05.pdf ·...

CHAPTER 5

DEDUCTIONS AND LOSSES: IN GENERAL

SOLUTIONS TO PROBLEM MATERIALS

Status: Q/P Question/ Present in Prior Problem Topic Edition Edition

1 Allowed income and deductions Unchanged 12 Deductions for and from AGI Unchanged 23 Deductions from AGI Unchanged 34 Deductions for and from AGI Unchanged 45 Deductions for and from AGI Unchanged 56 Deductions for and from AGI Unchanged 67 Deductions for and from AGI; deduction

disallowance New

8 Ordinary and necessary requirement Unchanged 89 Reasonable compensation Unchanged 9

10 Business versus nonbusiness losses Unchanged 1011 Reporting procedures Unchanged 1112 Method of accounting: cash versus accrual Unchanged 1213 Actually paid requirement for cash basis taxpayer Unchanged 1314 All events and economic performance tests Unchanged 1415 Reserves and economic performance test Unchanged 1516 Illegal activities Unchanged 1617 Issue ID Unchanged 1718 Legal expenses Unchanged 1819 Illegal activities Unchanged 1920 Political contributions Unchanged 2021 Lobbying expenditures New 22 Excessive executive compensation New 23 Investigation of a business New 24 Hobby/business Unchanged 2425 Vacation home rental: classification New 26 Vacation home rental: IRS approach versus

court approach

New

5-1

5-2 2004 Comprehensive Volume/Solutions Manual

Status: Q/P Question/ Present in Prior Problem Topic Edition Edition

27 Issue ID Unchanged 2728 Conversion of a residence to rental property Unchanged 2829 Another taxpayer’s obligation Unchanged 2930 Personal expenses versus deductible legal expenses New 31 Issue ID Unchanged 3132 Tax-exempt income/expenses Modified 32

* 33 Deductions for and from AGI Unchanged 33* 34 Deductions for and from AGI Modified 34* 35 Deductions for and from AGI Modified 35

36 Reasonable salaries Unchanged 36* 37 Business and nonbusiness losses Unchanged 37

38 Cash method versus accrual method Modified 3839 Cash basis and prepaid expenses Unchanged 39

* 40 Economic performance test Unchanged 4041 Legal expenses and public policy limitations Unchanged 41

* 42 Illegal business Unchanged 4243 Political contributions New 44 Excessive executive compensation Unchanged 44

* 45 Excessive executive compensation Unchanged 4546 Investigation of a business Modified 4647 Investigation of a business Unchanged 4748 Hobby/business Unchanged 48

* 49 Hobby losses/business New 50 Vacation home rental: exclusion Unchanged 50

* 51 Vacation home rental: Court’s approach and IRS’s approach

Unchanged 51

* 52 Vacation home rental: primarily rental use Unchanged 52* 53 Taxable income calculation and vacation home Unchanged 53* 54 Another taxpayer’s obligations Unchanged 54

55 Capital expenditure and amortization Unchanged 5556 Capital expenditures and amortization Unchanged 5657 Losses between related parties Unchanged 5758 Deductions between related parties and constructive

ownership Unchanged 58

* 59 Losses between related parties Unchanged 5960 Tax-exempt income/expenses Unchanged 6061 Another taxpayer’s obligations and classifying

deductions for and from AGI New

* 62 Cumulative Modified 62* 63 Cumulative Unchanged 63 *The solution to this problem is available on a transparency master.

Deductions and Losses: In General 5-3

CHECK FIGURES 33. AGI reduced by $3,575. 34.a. AGI is $52,500. 34.b. Select itemized deductions of

$7,500. 35. With IRA contribution $6,340;

without IRA contribution $5,815. 36.a. Reduce taxable income of Thrush,

Inc. 36.b. Thrush’s taxable income $0 if

deemed reasonable; children report $25,000 each.

37.a. $5,000. 37.b. For AGI. 38.a. $500,000 under cash method. 38.b. $545,000 under accrual method. 39. $12,000. 40. $85,000. 41. Only the $500 attorney fee is

deductible. 42.a. $477,400. 42.b. $700,000. 43. $0. 44. Adopt the performance-based

compensation program. 45. Salary and bonus $8.16 million;

retirement plan contribution $456,000.

46. $26,000. 47.a. $30,000. 47.b. $30,000. 47.c. $0. 47.d. $2,000. 48.a. $109,000. 48.b. $98,000. 49.a. Net increase in taxable income

$5,860. 49.b. Net decrease in taxable income

$5,700. 50. No impact on AGI.

51.a. Net rental income $0; itemized deduction $10,082.

51.b. Net rental income $0; itemized deduction $4,500.

52. Net rental loss $12,272; itemized deduction $300.

53. $23,507. 54.a. $15,500. 54.b. $0. 54.c. Chelsie should give or loan $1,000 to

Velma and Clyde who then pay $1,000 to Boyd.

55. Amortized over a 15-year period in both cases.

56.a. $173,000 allocated to listed assets. 56.b. $27,000 is either for goodwill or

covenant not to compete. 56.c. No check figure provided. 57.a. Loss is not deductible. 57.b. Gain $3,000; loss $8,000; gain $0. 58. Robin may deduct $2,000 in 2003

for loan from Paul, but can’t deduct $2,000 for Irene’s loan until 2004; Irene and Paul have interest income of $2,000 each in 2004.

59.a. $0. 59.b. $15,000 recognized loss. 59.c. $0. 59.d. $1,500 recognized loss. 59.e. $45,000 recognized gain. 60. $5,850. 61.a. Deduct $11,000. 61.b. $0. 61.c. From AGI. 61.d. Gift of $6,000 by Robert to Anne

who then pays and deducts her obligations.

62. Refund due $3,707. 63. Refund due $1,856.

5-4 2004 Comprehensive Volume/Solutions Manual

DISCUSSION QUESTIONS 1. While the Code provides an all-inclusive definition of income, deductions must be

specifically provided for in the Code in order to be permitted. p. 5-2 2. Terry would prefer deductions for AGI because they are allowable in addition to the

standard deduction. Deductions from AGI are claimed only when they exceed the standard deduction and are in lieu thereof. Additionally, deductions which reduce AGI may increase those itemized deductions which are subject to AGI floors such as medical expenses (7.5%) and miscellaneous itemized deductions (2%). pp. 5-2 and 5-3

3. Deductions from AGI benefit the taxpayer only if the taxpayer itemizes deductions. If

itemized deductions are less than the standard deduction, they provide no tax benefit. p. 5-2

4. a. Not deductible. b Deduction from AGI. c. Deduction from AGI (subject to the 7.5% of AGI floor). d. Deduction for AGI. e. Deduction for AGI. pp. 5-3, 5-4, and Concept Summary 5-3 5. a. Deduction for AGI. b. Not deductible. c. Deduction for AGI. d. $400 deduction from AGI. The $100 principal payment is not deductible. e. Deduction for AGI. pp. 5-3, 5-4, and Concept Summary 5-3 6. Investment expenses associated with rental property or royalty property are deductible

for AGI. Other investment expenses are deductible from AGI. Evidently, Susan has invested in rental or royalty property, whereas Larry has invested in other investment property. p. 5-5

7. a. The payment to General Ryan clearly is not deductible. Although its purports to

be a consulting fee, it has all of the earmarks of a bribe. General Ryan has put himself in a conflict-of-interest situation, and it is not likely that the U.S. Air Force allows its personnel to compromise their duties. The payment to General Morales, however, can be viewed differently. Not only is General Morales retired, but the standards under the Foreign Corrupt Practices Act are less stringent. If General Morales does provide some consulting service, a deduction is in order.

Deductions and Losses: In General 5-5

b. If the payment is deductible, it is deductible for AGI, since it is a § 162 trade or business expense.

pp. 5-6 and 5-13

8. The free airline flight valued at $500 is excludible from Wanda’s gross income as a no-

additional-cost service. See Chapter 4. The $800 of travel expenses is not deductible as a § 212 deduction because the 25 share investment is insignificant in value in relation to the travel expenses incurred. p. 5-7 and Example 5

9. The term reasonableness is used in conjunction with compensation for services such as

salaries. If the courts find salaries to be unreasonable upon considering all relevant facts, then excessive payments are generally treated as dividends. Dividend treatment would have the effect of increasing the corporation’s taxable income since dividends are not deductible. pp. 5-7 to 5-9 and Example 6

10. The tax consequences to Dave for the residence and the business parts of the building are

different. The casualty loss on the residence part must be reduced by $100 and then the aggregate of all personal use property casualty losses for the tax year must be reduced by 10% of AGI. The remaining amount is deductible as an itemized deduction.. No such reductions are required for the casualty loss on the business portion and the loss is deductible as a deduction for AGI. p. 5-9

11. Rental income and expenses are reported on Schedule E (Supplemental Income or Loss)

of Form 1040. p. 5-9 and Figure 5-1 12. The cash basis taxpayer generally takes a deduction in the year of the payment.

Exceptions exist for capital expenditures and for certain prepayments. An accrual basis taxpayer takes a deduction in the year incurred. That is, both the all events test and the economic performance test must be satisfied. Under the all events test, a deduction cannot be claimed until (1) all the events have occurred to create the taxpayer’s liability, and (2) the amount of the liability can be determined with reasonable accuracy. Economic performance is met only when the service, property, or use of property giving rise to the liability is actually performed for, provided to, or used by the taxpayer. pp. 5-9 to 5-12

13. Cash basis taxpayers can deduct an expense only when it has been paid with cash or other

property. Borrowing the money to pay the expense (or charging it on a bank credit card) constitutes actual payment.

However, actual payment does not ensure a current deduction. For example, capital

expenditures must be capitalized. Subsequently, the expenditure may be amortized, depleted, or depreciated. Except in certain circumstances, prepaid items cannot be deducted.

p. 5-11 14. The all events test and the economic performance test must be met before an accrual

basis taxpayer can deduct an expense. For the all events test to be satisfied, (1) all the events must have occurred to create the taxpayer’s liability, and (2) the amount of the liability can be determined with reasonable accuracy. Once these requirements are satisfied, the deduction is permitted only if economic performance has occurred. The economic performance test is met only when the service, property, or use of property

5-6 2004 Comprehensive Volume/Solutions Manual

giving rise to the liability is actually performed for, provided to, or used by the taxpayer. pp. 5-11, 5-12, and Example 9.

15. The reason the reserve method cannot be used for tax purposes is that the economic

performance test is not satisfied. p. 5-12 and Example 12 16. Bribes and kickbacks generally are not deductible, as such expenditures are considered to

be contrary to public policy. However, deductions for foreign bribes and kickbacks are permitted if the payments do not violate the U.S. Foreign Corrupt Practices Act of 1977. The reason for the more liberal treatment for the foreign payments is to ensure that U.S. companies are not placed at a competitive disadvantage in the international marketplace. p. 5-13

17. The two issues involved are whether the payment should be made and, if made, is it

deductible. If made to the representatives of a U.S. company, it would be a bribe. Not only would it be nondeductible, it could result in criminal charges. If the payment is made to the representative of the foreign company, more than likely it would be an accepted trade practice in that country. In this case, since the payment would not violate the U.S. Foreign Corrupt Practices Act of 1977, it would therefore be deductible. p. 5-13

18. No. Legal fees incurred in connection with a criminal defense are deductible only if the

crime is associated with the taxpayer’s trade or business or income-producing activity. Since Stuart does not satisfy this requirement, the attorney’s fee is not deductible. p. 5-14

19. Only c., the price paid for drugs purchased for resale. Whether the business is legal or

illegal, cost of goods sold is allowed as a reduction from total sales in arriving at gross income from the business. Thus, cost of goods sold is treated as a negative income item rather than as a deduction. p. 5-15

20. No, a deduction is not permitted for political contributions. p. 5-15 21. Lobbying expenses generally are not deductible. Therefore, if Melissa pays the $1,500 to

a professional lobbyist, the payment is not deductible. However a de minimis exception provides that in-house lobbying expenditures not exceeding $2,000 per year can be deducted. Thus, if Melissa spends the $1,500 on in-house lobbying expenditures, she can deduct this amount. Note that if the in-house expenditures had exceeded $2,000, none of the in-house expenditures could have been deducted. p. 5-15

22. An employer can deduct a maximum of $1 million annually for compensation payments

to a covered executive. Covered executives include the chief executive officer and the four other most highly compensated officers. The provision applies only if the employer is a publicly held corporation. Employee compensation excludes:

• Commissions based on individual performance. • Certain performance-based compensation dependent on company performance. • Payments to tax-qualified retirement plans. • Payments that are excludible from the employee’s gross income.

pp. 5-15 and 5-16

Deductions and Losses: In General 5-7

23. If the taxpayer’s present occupation is the same as or similar to the business being investigated, the expenses are fully deductible whether or not the business is acquired.

If the taxpayer’s present occupation is unrelated to the business being investigated, no

deduction is allowed if the business is not acquired. If the business is acquired, the expenses must be capitalized. The taxpayer may elect to amortize the amount over a period of not less than 60 months, beginning with the month in which the business is started. pp. 5-16 and 5-17

24. The deduction for hobby expenses, except for items otherwise deductible such as

mortgage interest and property taxes, cannot exceed the gross income from the hobby. Thus, it would appear that the effect on Emma’s adjusted gross income would be $0 as Emma’s hobby income is exactly offset by hobby expenses. However, the hobby expenses, except for items otherwise deductible, are classified as miscellaneous itemized deductions that are subject to the 2% floor. Consequently, to the extent that Emma’s allowable hobby expenses are reduced by the 2% floor, Emma’s AGI will increase. pp. 5-17 to 5-20

25. a. Since the property was rented for fewer than 15 days, it is classified as primarily personal. The rent income is excluded from gross income, and only the property taxes and mortgage interest are deductible as itemized deductions. Example 24

b. It was used personally for less than 15 days (as well as less than 10% of the total

rental days). So it is classified as primarily rental. Expenses must be allocated between rental use and personal use and a loss can be deducted. Examples 25 and 26

c. It was used personally for more than 10% of the rental days, so it is classified as

personal/rental. Expenses must be allocated between rental use and personal use and no loss is allowed. Examples 27 to 29

26. The IRS approach allocates property taxes and mortgage interest, like other expenses, on

the basis of days of use. The court approach allows 365 days as the basis for the allocation.

The IRS approach results in harsher tax treatment because it allocates more of the already deductible expenses to the rental activity. This results in a smaller deduction for usually nondeductible items such as utilities, maintenance, and depreciation.

The court’s approach is more favorable for the taxpayer because less property taxes and mortgage interest are allocable to the rental activity. Larger deductions for other expenses such as utilities, maintenance, and depreciation can then be taken. This preserves a larger itemized deduction for property taxes and mortgage interest.

Examples 28 and 29

27. In prior years, the beach home has been classified as a rental property since the personal use (exactly 14 days) did not exceed the greater of 14 days or 10% of rental days (200 X 10% = 20 days). Thus, if the total available deductions exceeded the rental income, the loss could be deducted on Karen and Andy’s tax return. If Sarah is permitted to use the beach house for 7 days, the total personal use days of 21 will exceed the statutory limit of 20 days (i.e., 10% of rental days of 200). In this case, the deductions are permitted only to the extent of the rental income. What needs to be determined are whether the

5-8 2004 Comprehensive Volume/Solutions Manual

deductions do exceed the rental income and whether Sarah wants to use it for a full 7 days. pp. 5-20 to 5-22

28. Hank can deduct property taxes and mortgage interest from January 1 to March 1 as an

itemized deduction from AGI. The home was his personal residence during that period. For the rest of the year, from March 1 through December 31, he can deduct property taxes, mortgage interest, depreciation and all other expenses for AGI as rental expenses. The “qualified rental period” requirements have been met. He has converted his personal residence into rental property and no allocation of expenses need be made, even if there is a rental loss. p. 5-24

29. a. For Ray to deduct the interest part of the payment, he needs to make the payment

to the mortgage company. Thus, Ted could give the money to Ray and then Ray pays the mortgage company.

b. If Ted pays the mortgage company directly, Ted is not permitted to deduct the

mortgage interest since it is not his obligation. Ray would not be permitted to deduct the interest part of the payment since he did not make the payment.

c. The obligation is that of Ray and not that of Ted. Thus, Ted is not permitted to

deduct the interest even if he makes the mortgage payment directly to the mortgage company.

pp. 5-24 to 5-26 30. Edna can deduct only those legal expenses associated with the divorce for which she is

able to show that the origin and character of the claim are directly related to a trade or business, an income-producing activity, or the determination, collection, or refund of a tax. As personal legal expenses are not deductible, only those legal payments which relate to the items mentioned above qualify. pp. 5-28, 5-27, and Example 33

31. The tax issue is whether Ella will be able to deduct the loss on the sale of Peach, Inc. stock. If the relative is a § 267 related party, the realized loss to Ella will be disallowed. Otherwise, the realized loss will be recognized by Ella.

Under these facts, the timing of the gift to the other relative has no effect on the sales

transaction. However, if the facts were different and Ella were selling an asset other than stock (e.g., land that has declined in value) to her controlled corporation, then relevant additional tax issues would be whether the gift relative is a related party or not for constructive ownership purposes and the timing of the gift (i.e., whether the gift is made before or after the asset sale). pp. 5-28 and 5-29

32. a. Although Jake receives interest payments of $3,600, all of this amount is excluded from his gross income. Interest on municipal bonds is tax-exempt.

b. None of Jake’s interest payments of $2,300 on the loan can be deducted. The

proceeds of the loan were used to purchase tax-exempt bonds. Consequently, the interest expense deduction is disallowed. Likewise, none of the principal payments of $600 can be deducted.

pp. 5-30 and 5-31

Deductions and Losses: In General 5-9

PROBLEMS 33. Since these expenses relate to Beth’s CPA practice and all are paid by her, she can deduct

her expenses and those for Steve in calculating AGI. The expenses reduce her AGI by $3,575.

Conference registration ($500 + $500) $1,000 Airline tickets ($900 + $600) 1,500 Taxi fares 75 Lodging ($700 + $300) 1,000 $3,575

pp. 5-2 and 5-3 34. a. Gross income: Salary income $60,000 Net rent 6,000 Dividend income 3,500 $69,500 Deductions for AGI: Alimony paid $12,000 Contribution to traditional IRA 3,000 Loss on sale of real estate 2,000 (17,000) Adjusted gross income $52,500

b. Itemized deductions: Mortgage interest on residence $4,900 Property tax on residence 1,200 Contribution to church 1,100 State income tax 300 Medical expenses [$3,250 – ($52,500 X 7.5%)] -0- Total itemized deductions $7,500 Since the standard deduction for 2003 of $4,750 is less than Daniel’s itemized deductions

of $7,500, Daniel should itemize deductions in 2003. The Federal income tax of $7,000 is not deductible. pp. 5-3 to 5-5

35. With IRA Without IRA Contribution Contribution Gross income $10,200 $10,200 Contribution to IRA (3,000) (-0-) AGI $ 7,200 $10,200 Itemized deductions: Charitable contribution $2,000 $2,000 Medical expenses [$2,200 – (7.5% X AGI)] 1,660 1,435 Casualty loss [($3,500 – $100) – (10% X AGI)] 2,680 2,380 Total itemized deductions $6,340 $5,815 Thus, the $3,000 IRA contribution would increase Julie’s itemized deductions by $525

($6,340 – $5,815). pp. 5-3, 5-4, and Example 2

5-10 2004 Comprehensive Volume/Solutions Manual

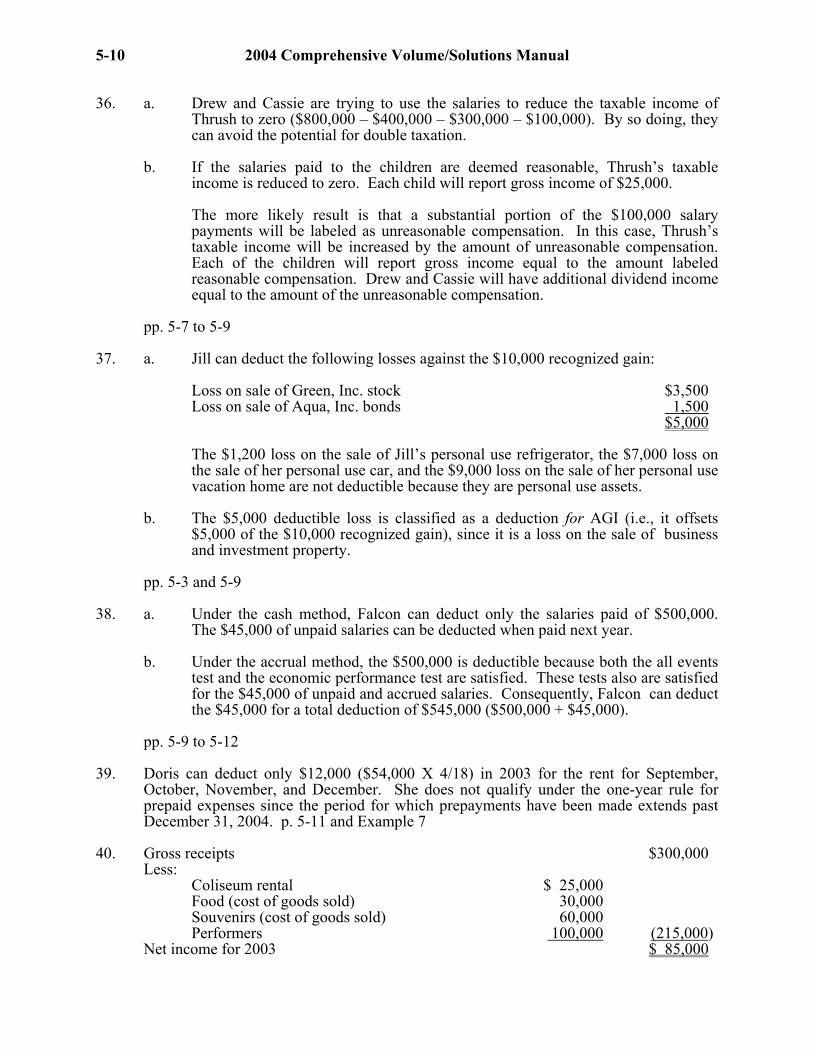

36. a. Drew and Cassie are trying to use the salaries to reduce the taxable income of Thrush to zero ($800,000 – $400,000 – $300,000 – $100,000). By so doing, they can avoid the potential for double taxation.

b. If the salaries paid to the children are deemed reasonable, Thrush’s taxable

income is reduced to zero. Each child will report gross income of $25,000. The more likely result is that a substantial portion of the $100,000 salary

payments will be labeled as unreasonable compensation. In this case, Thrush’s taxable income will be increased by the amount of unreasonable compensation. Each of the children will report gross income equal to the amount labeled reasonable compensation. Drew and Cassie will have additional dividend income equal to the amount of the unreasonable compensation.

pp. 5-7 to 5-9

37. a. Jill can deduct the following losses against the $10,000 recognized gain: Loss on sale of Green, Inc. stock $3,500 Loss on sale of Aqua, Inc. bonds 1,500 $5,000

The $1,200 loss on the sale of Jill’s personal use refrigerator, the $7,000 loss on the sale of her personal use car, and the $9,000 loss on the sale of her personal use vacation home are not deductible because they are personal use assets.

b. The $5,000 deductible loss is classified as a deduction for AGI (i.e., it offsets

$5,000 of the $10,000 recognized gain), since it is a loss on the sale of business and investment property.

pp. 5-3 and 5-9 38. a. Under the cash method, Falcon can deduct only the salaries paid of $500,000.

The $45,000 of unpaid salaries can be deducted when paid next year. b. Under the accrual method, the $500,000 is deductible because both the all events

test and the economic performance test are satisfied. These tests also are satisfied for the $45,000 of unpaid and accrued salaries. Consequently, Falcon can deduct the $45,000 for a total deduction of $545,000 ($500,000 + $45,000).

pp. 5-9 to 5-12 39. Doris can deduct only $12,000 ($54,000 X 4/18) in 2003 for the rent for September,

October, November, and December. She does not qualify under the one-year rule for prepaid expenses since the period for which prepayments have been made extends past December 31, 2004. p. 5-11 and Example 7

40. Gross receipts $300,000

Less: Coliseum rental $ 25,000 Food (cost of goods sold) 30,000 Souvenirs (cost of goods sold) 60,000 Performers 100,000 (215,000) Net income for 2003 $ 85,000

Deductions and Losses: In General 5-11

Since Duck is an accrual basis taxpayer, it may accrue and deduct the costs of the performers of $100,000 even though not paid until January 5, 2004 (i.e., the economic performance test is satisfied). However, the cleaning cost of $10,000 may not be deducted until 2004 when the services are performed (i.e., at that time, the economic performance test is satisfied). pp. 5-11 and 5-12

41. Only the $500 paid to the attorney to draft the tenant lease is deductible by Doug. This

expense is an ordinary and necessary expense incurred in connection with rental property held for the production of income. The tickets and the related legal expenses are not deductible because they are personal in nature. Even if they were related to the conduct of a trade or business or the production of income, they would be disallowed as a deduction because they violate public policy. The $1,000 payment for negotiating a reduction in child support payments is personal in nature. pp. 5-13 and 5-14

42. a. The effect of the illegal betting parlor on Chris’s AGI is as follows: Gross income $900,000

Deductible expenses: Salaries $360,000 Rent 24,000 Utilities 3,600 Telephone 5,000 Life insurance premiums 30,000 (422,600) Increase in AGI $477,400

Neither the illegal kickbacks of $40,000 nor the bribes to police of $20,000 is

deductible since these expenses violate public policy.

b. For an illegal drug activity, all of the expenses are disallowed. Therefore, it would appear that the illegal drug operation would increase Chris’s AGI by $900,000. However, the $200,000 cost of goods sold is viewed as a reduction in calculating gross income rather than as an expense. Therefore, the illegal drug operation increases Chris’s AGI by $700,000 ($900,000 – $200,000).

p. 5-14 and Example 16 43. Polly’s deduction for the political contributions is $0. Political contributions cannot be

deducted. p. 5-15 44. a. Under the first option, the salary of Amber’s president would be $1,170,000

($900,000 + $270,000). Since Amber is a publicly held corporation, only $1,000,000 of this salary is deductible, with the balance of $170,000 being disallowed as excessive executive compensation. The $26,000 ($20,000 + $6,000) contribution to the defined contribution pension plan would be deductible.

Under the second option, all of the compensation paid to the president is deductible assuming the statutory requirements for a performance-based compensation program are satisfied. Thus, only the second option provides Amber with a deduction for all of the president’s proposed compensation. pp. 5-15 and 5-16

5-12 2004 Comprehensive Volume/Solutions Manual

b. Willis, Hoffman, Maloney, and Raabe, CPAs 5191 Natorp Boulevard

Mason, OH 45040

September 18, 2003 Ms. Agnes Riddle Chairperson of the Board of Directors Amber, Inc. 100 James Tower Cleveland, OH 44106 Dear Ms. Riddle: I am responding to your inquiry regarding the proposed compensation plans for Amber’s president. Under one proposal, both the salary and the pension contribution will be increased by 30%. Under the other option, a performance-based compensation program will be implemented which is projected to provide about the same additional compensation and pension contribution for the president. The 30% increase option will produce a salary of $1,170,000 and a pension contribution of $26,000. Of this amount, only $1,026,000 ($1,000,0000 salary and $26,000 pension contribution) can be deducted by Amber. The salary paid to the president in excess of $1,000,000 is disallowed as excessive executive compensation.

Under the performance-based compensation option, all of the compensation (salary, bonus, and pension contribution) can be deducted assuming that the performance-based compensation satisfies the following requirements:

Such compensation is based on company performance according to a formula approved by a board of directors compensation committee (comprised solely of two or more outside directors) and by shareholder vote. The performance must be certified by this compensation committee.

I recommend that you adopt the performance-based compensation option. I believe that it will better achieve Amber’s objective of placing a greater emphasis on the relationship between performance and compensation. In addition, under this approach, all of the compensation can be deducted on Amber’s Form 1120. If you would like to have me work with you in developing this program, let me know. Sincerely, Rex Edward, CPA Partner pp. 5-15 and 5-16

Deductions and Losses: In General 5-13

45. Since Vermillion is a publicly held corporation, it is subject to the excessive executive compensation deduction limit for the CEO and the four other most highly compensated officers of $1 million each. Since the 5 percent bonus does not satisfy the requirements that must be met to exclude it from covered compensation, the bonus is included with the salary in applying the limit. Thus, Vermillion may deduct the following:

Retirement Plan Salary Contribution CEO $1,000,000 $ 80,000 Executive vice president 1,000,000 72,000 Treasurer 1,000,000 64,000 Marketing vice president 1,000,000 60,000 Operations vice president 1,000,000 56,000 Distribution vice president 1,260,000 48,000 Research vice president 1,100,000 44,000 Controller 800,000 32,000 $8,160,000 $456,000 The limit does not apply to the distribution vice president or the research vice president because they are not included in the covered group (i.e., CEO plus top 4). The retirement plan contribution is excluded from the definition of covered compensation. pp. 5-15 and 5-16

46. Even though Jenny decides not to pursue the expansion of her restaurant chain into

another city, the investigation expenses of $25,000 are deductible in the current year. Because Jenny is in the restaurant business, all investigation expenses associated with the restaurant business are deductible in the year paid or incurred. Since Jenny was not in the hotel business, she can deduct only part of the investigation expenses for the hotel. Because she does open the hotel, she can amortize the $30,000 of investigation expenses over a 60-month period, beginning with December, the month in which the business is started. Therefore, she also may deduct $1,000 ($30,000/60 months X 2 months) in the current year, for a total of $26,000. pp. 5-16 and 5-17

47. a. He could deduct $30,000. p. 5-16 and Example 18

b. He could deduct $30,000. p. 5-16 and Example 18 c. None of Tim’s expenses is deductible. p. 5-16 and Example 19 d. Because operations began on September 1, 2003, he could deduct 4 month’s

amortization, or $2,000 [($30,000/60) X 4 months]. p. 5-17 and Example 20 48. a. Louis would include the $9,000 in AGI and show $9,000 of expenses as

miscellaneous itemized deductions subject to the 2%-of-AGI limitation. His AGI is $109,000 ($100,000 + $9,000), and the 2% floor is $2,180 ($109,000 X 2%). So the deduction would be $6,820 ($9,000 – $2,180).

b. If the activity is a business, he would have a $2,000 ($9,000 – $11,000) loss that

is a deduction for AGI. His AGI becomes $98,000 ($100,000 – $2,000). Examples 22 and 23 49. a. If the miniature horse activity is held to be a hobby, Samantha’s deductions

associated with the hobby may not exceed her gross income from the activity.

5-14 2004 Comprehensive Volume/Solutions Manual

Income $22,000 Deduct: Mortgage interest (10% of $24,000) $ 2,400 Property taxes on farm improvements 800 Property taxes on home (10% of $2,200) 220 (3,420) Balance $18,580 Deduct: Other expenses Entry fees $ 1,000 Feed and vet 4,000 Supplies 900 Publications and dues 500 Travel 2,300 Salary and wages 8,000 (16,700) Balance $ 1,880 Depreciation: On horse equipment $ 3,000 On farm improvements 7,000 On home (10% office portion) 1,000 Total $11,000 Limited to (1,880) Net Income $ -0- The items are handled as follows: AGI $100,000 Plus: Horse income 22,000 New AGI $122,000 Itemized deductions: Interest and taxes on farm (hobby portion) $ 3,420 Interest and taxes on home ($26,200 – $2,620) 23,580 $27,000 Other expenses and depreciation ($16,700 + $1,880) of hobby $18,580 Less: 2% of AGI ($122,000) (2,440) $16,140 Note that the deductions for the miniature horse operation are $19,560 ($3,420 +

$16,140) of which $3,420 were deductible anyway. The net increase in taxable income is:

Income $22,000 Otherwise nondeductible expenses (16,140) Net increase in taxable income $ 5,860

b. If the miniature horse activity is classified as a business, Samantha would be able to deduct $9,120 for AGI as follows:

Remainder of income after other expenses and before amounts that affect basis (depreciation) [see Part (a.) above] $ 1,880

Less: Depreciation (11,000) Deduction for AGI ($ 9,120)

Deductions and Losses: In General 5-15

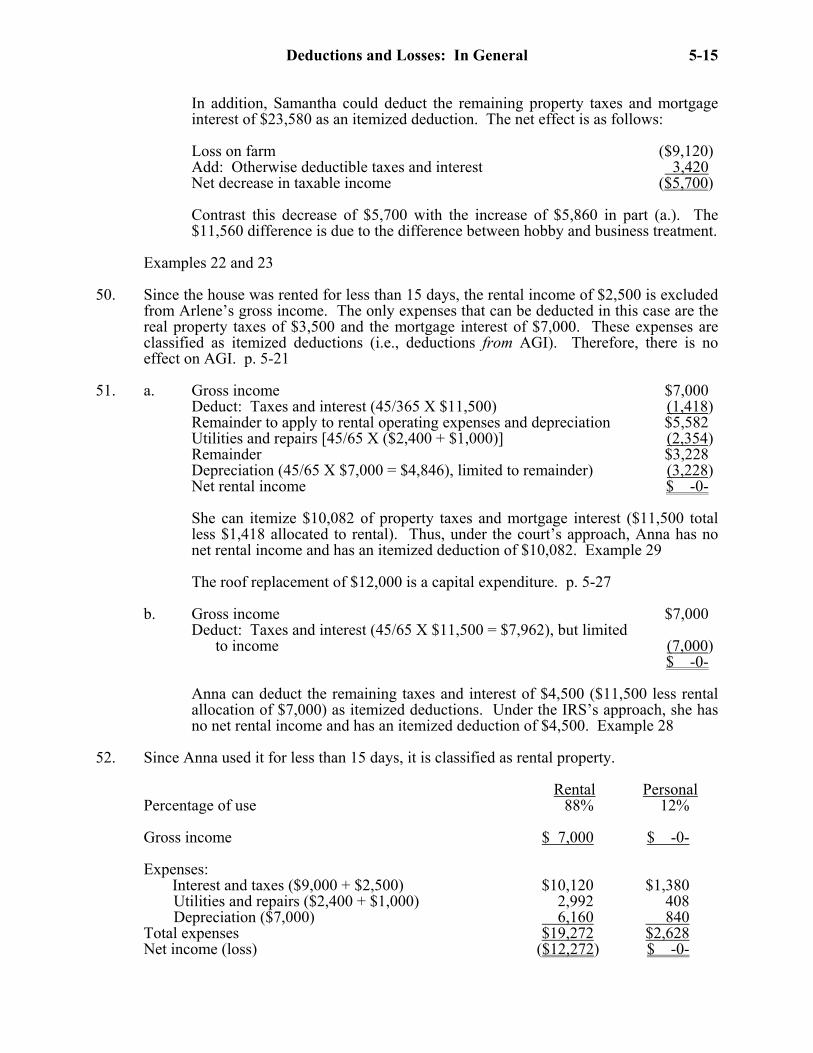

In addition, Samantha could deduct the remaining property taxes and mortgage interest of $23,580 as an itemized deduction. The net effect is as follows:

Loss on farm ($9,120) Add: Otherwise deductible taxes and interest 3,420 Net decrease in taxable income ($5,700)

Contrast this decrease of $5,700 with the increase of $5,860 in part (a.). The $11,560 difference is due to the difference between hobby and business treatment.

Examples 22 and 23

50. Since the house was rented for less than 15 days, the rental income of $2,500 is excluded from Arlene’s gross income. The only expenses that can be deducted in this case are the real property taxes of $3,500 and the mortgage interest of $7,000. These expenses are classified as itemized deductions (i.e., deductions from AGI). Therefore, there is no effect on AGI. p. 5-21

51. a. Gross income $7,000 Deduct: Taxes and interest (45/365 X $11,500) (1,418) Remainder to apply to rental operating expenses and depreciation $5,582 Utilities and repairs [45/65 X ($2,400 + $1,000)] (2,354) Remainder $3,228 Depreciation (45/65 X $7,000 = $4,846), limited to remainder) (3,228) Net rental income $ -0-

She can itemize $10,082 of property taxes and mortgage interest ($11,500 total less $1,418 allocated to rental). Thus, under the court’s approach, Anna has no net rental income and has an itemized deduction of $10,082. Example 29

The roof replacement of $12,000 is a capital expenditure. p. 5-27

b. Gross income $7,000 Deduct: Taxes and interest (45/65 X $11,500 = $7,962), but limited to income (7,000) $ -0-

Anna can deduct the remaining taxes and interest of $4,500 ($11,500 less rental allocation of $7,000) as itemized deductions. Under the IRS’s approach, she has no net rental income and has an itemized deduction of $4,500. Example 28

52. Since Anna used it for less than 15 days, it is classified as rental property. Rental Personal Percentage of use 88% 12% Gross income $ 7,000 $ -0- Expenses:

Interest and taxes ($9,000 + $2,500) $10,120 $1,380 Utilities and repairs ($2,400 + $1,000) 2,992 408 Depreciation ($7,000) 6,160 840

Total expenses $19,272 $2,628 Net income (loss) ($12,272) $ -0-

5-16 2004 Comprehensive Volume/Solutions Manual

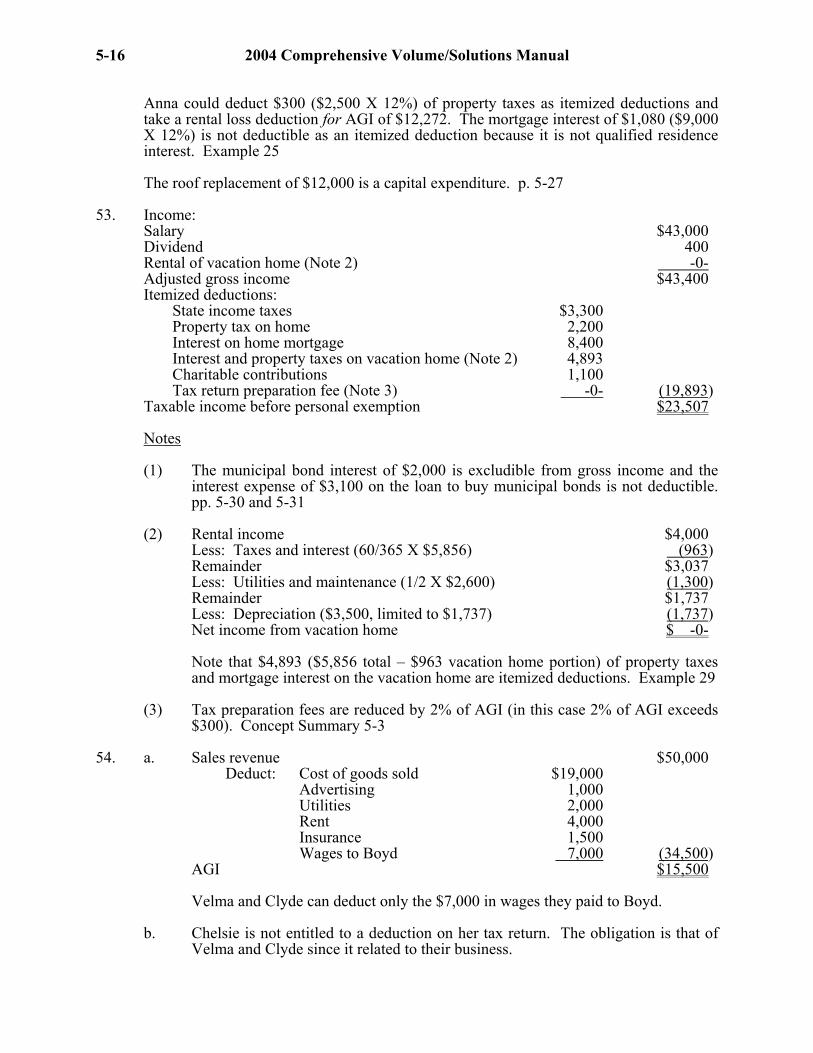

Anna could deduct $300 ($2,500 X 12%) of property taxes as itemized deductions and take a rental loss deduction for AGI of $12,272. The mortgage interest of $1,080 ($9,000 X 12%) is not deductible as an itemized deduction because it is not qualified residence interest. Example 25 The roof replacement of $12,000 is a capital expenditure. p. 5-27

53. Income:

Salary $43,000 Dividend 400 Rental of vacation home (Note 2) -0- Adjusted gross income $43,400 Itemized deductions:

State income taxes $3,300 Property tax on home 2,200 Interest on home mortgage 8,400 Interest and property taxes on vacation home (Note 2) 4,893 Charitable contributions 1,100 Tax return preparation fee (Note 3) -0- (19,893)

Taxable income before personal exemption $23,507 Notes

(1) The municipal bond interest of $2,000 is excludible from gross income and the interest expense of $3,100 on the loan to buy municipal bonds is not deductible. pp. 5-30 and 5-31

(2) Rental income $4,000

Less: Taxes and interest (60/365 X $5,856) (963) Remainder $3,037 Less: Utilities and maintenance (1/2 X $2,600) (1,300) Remainder $1,737 Less: Depreciation ($3,500, limited to $1,737) (1,737) Net income from vacation home $ -0-

Note that $4,893 ($5,856 total – $963 vacation home portion) of property taxes

and mortgage interest on the vacation home are itemized deductions. Example 29 (3) Tax preparation fees are reduced by 2% of AGI (in this case 2% of AGI exceeds

$300). Concept Summary 5-3 54. a. Sales revenue $50,000 Deduct: Cost of goods sold $19,000 Advertising 1,000 Utilities 2,000 Rent 4,000 Insurance 1,500 Wages to Boyd 7,000 (34,500) AGI $15,500

Velma and Clyde can deduct only the $7,000 in wages they paid to Boyd. b. Chelsie is not entitled to a deduction on her tax return. The obligation is that of

Velma and Clyde since it related to their business.

Deductions and Losses: In General 5-17

c. If Chelsie had made a gift of the $1,000 to Velma and Clyde or had she loaned the $1,000 to them, then they could deduct it assuming they pay the $1,000 to Boyd.

pp. 5-24 to 5-26

55. From a tax perspective, the same tax consequences are produced regardless of whether the $360,000 is allocated to goodwill or to a covenant not to compete. Under either circumstance, the asset is a § 197 intangible. Therefore, the $360,000 must be capitalized and can be amortized over 15 years (i.e., $24,000 per year). p. 5-27

56. a. Jay is selling the assets of the sole proprietorship. Of the sales price of $200,000,

$173,000 is allocated to the listed assets in accordance with their fair market values. The recognized gain on each asset is the difference between its fair market value and its basis. The residual $27,000 ($200,000 – $173,000) appears to represent a payment for goodwill. Therefore, since Jay has a basis of $0 for the goodwill, he has a gain of $27,000. Since goodwill is a capital asset, the gain is classified as a long-term capital gain. Long-term capital gains are eligible for beneficial tax rates.

b. Lois is purchasing the assets of the sole proprietorship. Her basis for each asset is

the amount paid for it (i.e., the fair market value). It appears that the excess $27,000 ($200,000 – $173,000) represents a payment for goodwill. The goodwill is amortized over a statutory 15-year period.

Another option for Lois would be to get Jay to agree that part or all of the $27,000

is a payment for a covenant not to compete. Even though Jay is age 70 and indicates he is going to retire, this would give Lois additional security. Like goodwill, the covenant is amortizable over a statutory 15-year period regardless of the life of the covenant.

c. Whether an allocation is made to a covenant does not affect the tax consequence

to Lois (both are amortizable over a 15-year period). Goodwill is a capital asset to Jay, whereas the sale of a covenant not to compete would produce ordinary income. Since Jay, is in the 35% marginal tax bracket, there is a benefit to him of using the alternative tax on capital gains in calculating his tax liability. Therefore, assuming Lois is secure that Jay is going to retire (i.e., she does not need the legal protection of a covenant), she may negotiate to have part of Jay’s tax benefit of the goodwill assigned to her through an adjustment of the $200,000 purchase price.

pp. 5-27 and 5-34 57. a. Janet’s $27,000 loss ($55,000 amount realized – $82,000 adjusted basis) is not

deductible due to § 267. p. 5-28 and Example 35 b. If sold for $85,000, Fred’s recognized gain is $3,000 [$85,000 (sales price) less

$55,000 (basis), reduced by the $27,000 loss that previously was not allowed to Janet].

If sold for $47,000, a $8,000 loss [$47,000 (sales price) less $55,000 (basis)] is recognized by Fred. The $27,000 loss that was realized by Janet is not deductible by either Janet or Fred and is lost permanently.

5-18 2004 Comprehensive Volume/Solutions Manual

If sold for $60,000, there is no recognized gain to Fred [$60,000 (sales price) less $55,000 (basis), reduced by $5,000 of the $27,000 loss that previously was not recognized by Janet]. The remaining $22,000 of unrecognized loss is lost permanently as a deduction for both Janet and Fred. p. 5-28 and Examples 35 to 37

c. Willis, Hoffman, Maloney, and Raabe, CPAs

5191 Natorp Boulevard Mason, OH 45040

June 25, 2003 Ms. Janet Saxon 32 Country Lane Lawrence, KS 66045 Dear Ms. Saxon: As you requested in your note, I am providing you with the tax consequences of the proposed sale of stock to your brother Fred. Although you would have a potential loss of $27,000 ($55,000 selling price – $82,000 cost), you would not be able to recognize this loss on your tax return. The tax law disallows the recognition of losses between certain related parties. If you do sell the stock to Fred, his tax basis for calculating gain or loss on a subsequent sale by him would be his cost of $55,000. However, if he should sell it at a gain, he could use as much of your $27,000 disallowed loss as necessary to reduce his gain to zero. From a planning perspective, you could recognize the $27,000 loss on your tax return if you were to sell the stock to an unrelated party rather than selling it to Fred. If you would like to discuss this further, please let me know. Sincerely, Ellen Allen, CPA Tax Partner

58. Robin Corporation can take a deduction for interest of $2,000 in 2003 on the loan from

Paul, but must defer the deduction of $2,000 on the loan from Irene until 2004 when it is paid. Both Irene and Paul have interest income in 2004 when it is received. The reason for the different treatment is that Paul owns his 14% plus (by attribution) Irene’s 26% for a total of 40%. Since this is not greater than 50%, he is unrelated to Robin.

Irene, however, owns her shares (26%), plus (by attribution) her husband’s shares (14%), her father’s shares (25%), and her mother’s shares (15%) for a total of 80% ownership. Section 267 disallows the deduction for the accrued expense in 2003 because Irene and Robin are related parties. pp. 5-28 and 5-29

Deductions and Losses: In General 5-19

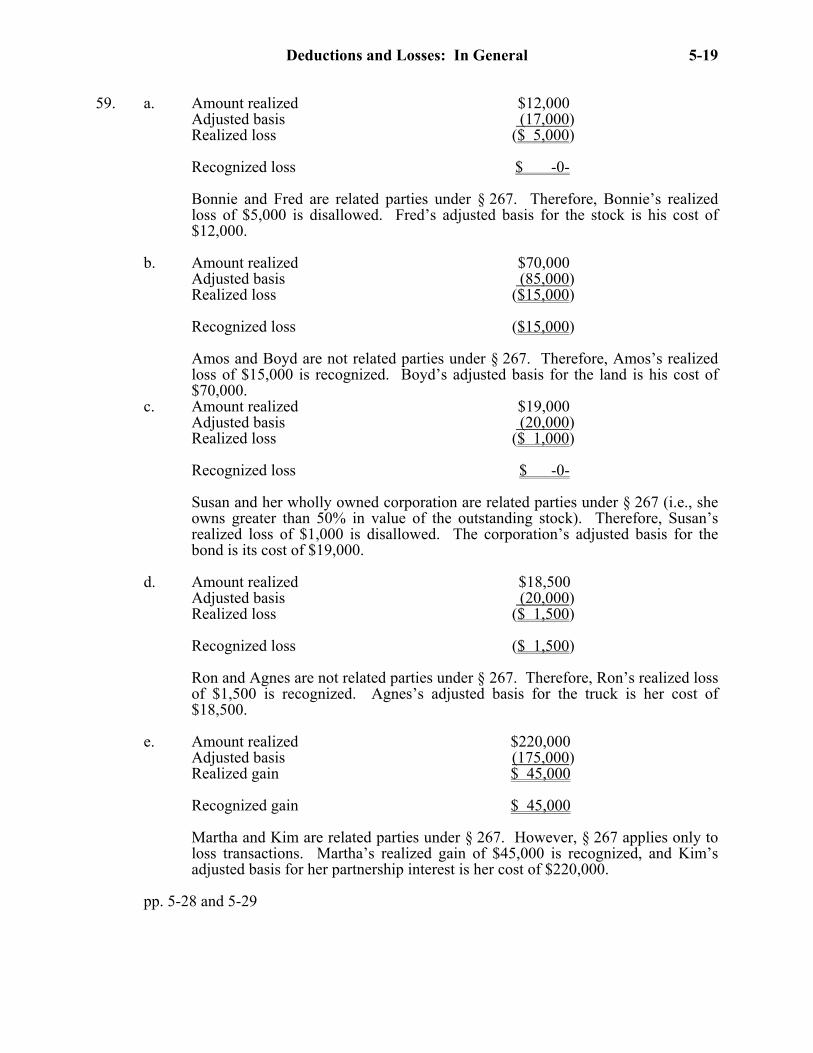

59. a. Amount realized $12,000 Adjusted basis (17,000) Realized loss ($ 5,000) Recognized loss $ -0- Bonnie and Fred are related parties under § 267. Therefore, Bonnie’s realized

loss of $5,000 is disallowed. Fred’s adjusted basis for the stock is his cost of $12,000.

b. Amount realized $70,000 Adjusted basis (85,000) Realized loss ($15,000) Recognized loss ($15,000) Amos and Boyd are not related parties under § 267. Therefore, Amos’s realized

loss of $15,000 is recognized. Boyd’s adjusted basis for the land is his cost of $70,000.

c. Amount realized $19,000 Adjusted basis (20,000) Realized loss ($ 1,000) Recognized loss $ -0- Susan and her wholly owned corporation are related parties under § 267 (i.e., she

owns greater than 50% in value of the outstanding stock). Therefore, Susan’s realized loss of $1,000 is disallowed. The corporation’s adjusted basis for the bond is its cost of $19,000.

d. Amount realized $18,500 Adjusted basis (20,000) Realized loss ($ 1,500) Recognized loss ($ 1,500) Ron and Agnes are not related parties under § 267. Therefore, Ron’s realized loss

of $1,500 is recognized. Agnes’s adjusted basis for the truck is her cost of $18,500.

e. Amount realized $220,000 Adjusted basis (175,000) Realized gain $ 45,000 Recognized gain $ 45,000

Martha and Kim are related parties under § 267. However, § 267 applies only to loss transactions. Martha’s realized gain of $45,000 is recognized, and Kim’s adjusted basis for her partnership interest is her cost of $220,000.

pp. 5-28 and 5-29

5-20 2004 Comprehensive Volume/Solutions Manual

60. Chris can deduct only the interest attributable to taxable income. The interest attributable to the municipal interest income is not deductible. Thus, only $5,850 ($65,000/ $100,000 X $9,000) is deductible. p. 5-30 and Example 39

61. a. Robert can only deduct amounts which are his obligations. He may not deduct amounts that are obligations of his daughter, Anne. Therefore, Robert can deduct the following as itemized deductions:

Property taxes on his home $ 3,000 Mortgage interest 8,000

Total $11,000 The repairs of $1,200 and the utilities of $2,700 paid by Robert associated with

his home are nondeductible personal expenditures. The roof replacement costs of $4,000 on Robert’s home are not deductible, but he can add them to his adjusted basis for the home.

b. Anne cannot deduct any of the expenses that would otherwise be deductible by

her (i.e., property taxes of $1,500 and mortgage interest of $4,500) because she did not pay them.

c. Robert’s deductions are deductions from AGI (itemized deductions).

d. Anne could deduct the property taxes of $1,500 and the mortgage interest of

$4,500 as itemized deductions if she paid them. Therefore, Robert should make a gift of $6,000 to Anne so that she could pay these expenses.

pp. 5-6, 5-24 to 5-26, and 5-33

CUMULATIVE PROBLEMS 62. Tax Compliance Salaries ($94,000 + $45,000) [Note 1] $139,000 Interest on certificates of deposit 2,100 Dividend income 900 Share of S corporation income [Note 2] 400 Award 1,500 Alimony [Note 3] (36,000) AGI [Note 4] $107,900 Itemized deductions: Medical expenses [Note 5] $ -0- Charitable contributions 3,900 State income taxes ($4,700 + $2,000 + $1,000) 7,700 Home mortgage interest 9,000 Property taxes 3,100 (23,700) $ 84,200 Personal and dependency exemptions (2 X $3,050) [Notes 6 and 7] (6,100) Taxable income $ 78,100 Tax on $78,100 [Note 8] $14,793 Less: Withholding ($14,500 + $4,000) (18,500) Net tax payable (or refund due) for 2003 ($ 3,707)

Deductions and Losses: In General 5-21

Notes

(1) The medical insurance premiums of $5,200 ($3,000 + $2,200) paid by their employers are excludible. Likewise, the $4,700 of medical benefits received under the plan by Mary Jane are excludible.

(2) Mary Jane includes her share of the S corporation income of $400 in her gross

income even though she received cash distributions of only $350. (3) The alimony of $36,000 that John pays to June is deductible. Child support

payments of $12,000 are not deductible. See Chapter 3. (4) The investigation expenses of $6,000 incurred by John and associated with the

retail computer franchise are not deductible. This result occurs because John was not in a business that was the same as or similar to the one being investigated, and the new business was not acquired.

(5) John pays medical insurance premiums of $1,500 and Mary Jane pays $1,100.

Their medical expense deduction is $0 since their payments are less than 7.5% of AGI (7.5% X $107,900 = $8,093).

(6) Mary Jane’s father does not qualify as a dependent. John and Mary Jane do

provide over half of his support (i.e., $7,000 furnished by them compared to $3,600 provided by her father). However, the father’s gross income of $5,400 ($1,900 salary + $3,500 unemployment compensation benefits) exceeds the allowable amount of less than $3,050. Since the gross income test is not satisfied, John and Mary Jane may not take the dependency deduction for her father. Note that the Social Security benefits of $3,200 were not included in the father’s gross income.

(7) June is the custodial parent. Since there is no indication that June has waived her

right to the dependency deduction for Rod, she qualifies for the dependency deduction rather than John.

(8) Since they are filing jointly, their tax liability for 2003 is calculated as follows:

On $47,450 $ 6,518 $30,650 X 27% 8,275 $14,793

Tax Planning

CLIENT LETTER

Willis, Hoffman, Maloney, and Raabe, CPAs 5191 Natorp Boulevard

Mason, OH 45040 December 16, 2003 Mr. and Ms. John Sanders 204 Shoe Lane Blacksburg, VA 24061

5-22 2004 Comprehensive Volume/Solutions Manual

Dear Mr. and Ms. Sanders: I am responding to your inquiry regarding whether Mr. Sanders should receive a $30,000 bonus in 2003 or delay receiving it until 2004. Based on the data provided by you, I have calculated your tax liability for both years assuming the bonus is received in 2003 and assuming the bonus is received in 2004.* The tax liability results are as follows:

Bonus received in 2003

2003 tax liability $22,893 2004 tax liability 3,525 Total $26,418 Bonus received in 2004 2003 tax liability $14,793 2004 tax liability 9,231 Total $24,024 If you delay the receipt of the bonus until 2004, you will save $2,394 ($26,418 – $24,024). This ignores any earnings (net of taxes) you could receive on the $30,000 if you receive the bonus in 2003. However, since the decision is to receive the bonus in December, 2003 or January, 2004, the amount of such earnings are likely to be negligible. If I can be of further assistance, let me know.

Sincerely,

Rene Ross, CPA Partner

*2003 tax rates used

TAX FILE MEMORANDUM December 9, 2003 Tax File Memorandum FROM: Gene Ross SUBJECT: John and Mary Jane Sanders Tax Planning Regarding Timing of Bonus

John Sanders, a regular tax client, has an opportunity to receive a $30,000 bonus in December 2003 or in January 2004. He has asked that we recommend to him whether he receive the bonus in 2003 or delay it until 2004. Expected differences in the data provided for the 2003 return and that for the 2004 return are as follows: (1) They are expecting twins in January 2004.

Deductions and Losses: In General 5-23

(2) Mary Jane will quit work on December 31, 2003 to stay home with the twins. Therefore, her salary will decrease by $45,000 and the state income taxes withheld on the $45,000 will decrease by $2,000.

(3) Mary Jane does not expect to receive the $1,500 award. (4) Medical benefits received by Mary Jane in 2004 will be $5,000 rather than the

$4,700 received in 2003. Based on the data provided for the 2003* taxes and the above assumptions, I made the following calculations:

Tax with the Bonus: 2003 2004 Taxable income in 2003 $ 78,100 $78,100 Bonus 30,000 30,000 Less: Mary Jane’s salary (45,000) Award (1,500) Additional exemptions for twins (6,100) Plus: Decrease in itemized deductions 2,000 Taxable income with bonus $108,100 $57,500 Tax $ 22,893 $ 9,231 Tax without the Bonus: Taxable income with bonus $108,100 $57,500 Less: Bonus (30,000) (30,000) Taxable income without bonus $ 78,100 $27,500 Tax $ 14,793 $ 3,525 Tax taking the bonus in 2003 For 2003 $22,893 For 2004 3,525 Total tax

$26,418 Tax taking the bonus in 2004 For 2003 $14,793 For 2004 9,231 Total tax

$24,024 They will save $2,394 ($26,418 – $24,024) by deferring the bonus to January,

2004. *2003 tax rates used 63. Salary $ 75,000

Inheritance (Note 1) -0- Gift (Note 1) -0- Life insurance proceeds (Note 1) -0- Gain on stock sale (Note 2) 3,000

5-24 2004 Comprehensive Volume/Solutions Manual

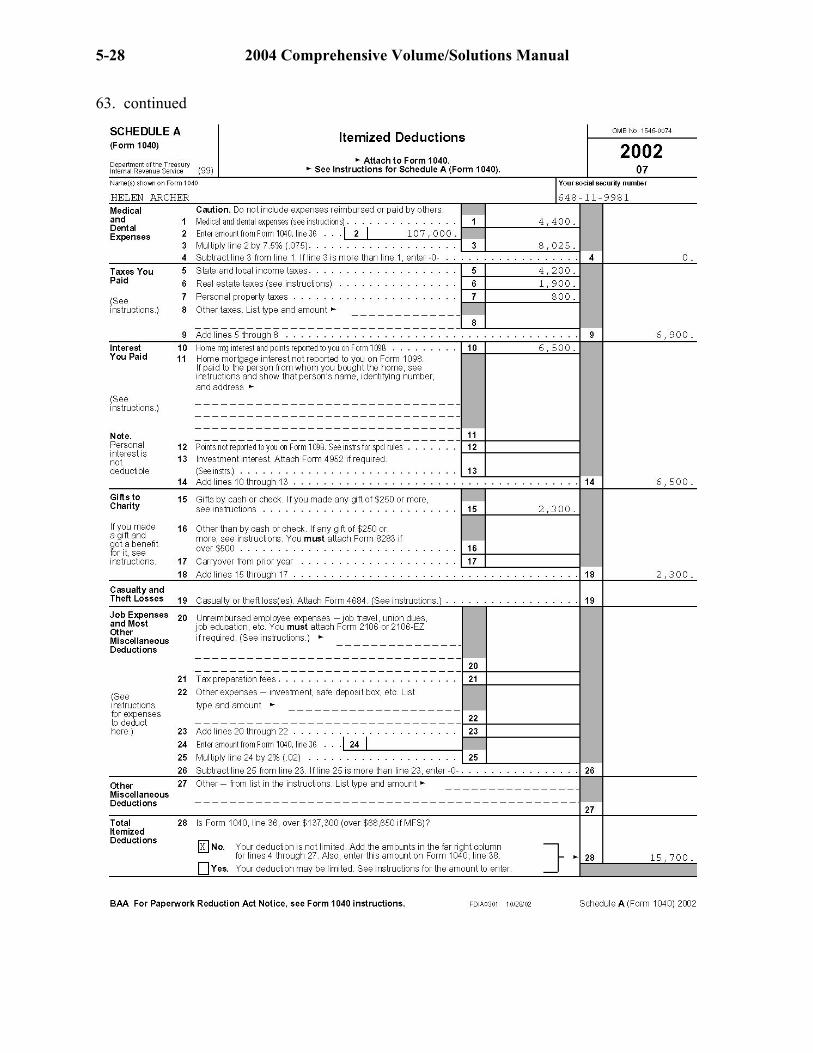

Interest income (Note 3) 3,500 Dividend income 1,200 Prize 800 Alimony 20,000 Partnership income (Note 4) 3,500 Gross income $107,000 Deductions for AGI -0- AGI $107,000 Itemized deductions: Charitable contributions ($1,500 + $800) $2,300 Home mortgage interest 6,500 Property taxes ($1,900 + $800) 2,700 State income taxes ($3,200 + $1,000) 4,200 Medical expenses (Note 5) -0- (15,700) $ 91,300 Less: Personal and dependency exemptions (Note 6) (6,000) Taxable income $ 85,300 Tax on $85,300 (Note 7) $ 18,044 Less: Withholding and estimated tax ($10,000 + $9,900) (19,900) Net tax payable (or refund due) for 2002 ($ 1,856) Notes

(1) The inheritance of $200,000, life insurance proceeds of $100,000, and the gift of

$10,000 all are excludible from Helen’s gross income. (2) Helen’s adjusted basis for the Amber stock is $20,000, the purchase price. A

cousin is not a related party. Even if a cousin were a related party, Helen’s adjusted basis would still be the purchase price of $20,000. No related party problem would arise because the cousin had a recognized gain on the sale of the stock to Helen. Therefore, Helen has a recognized loss of $1,000 ($19,000 amount realized – $20,000 adjusted basis). Since her holding period for the stock is long-term, the loss is classified as long-term capital loss. Helen has a gain on the sale of the Falcon stock of $4,000 ($15,000 amount realized – $11,000 adjusted basis). Since her holding period for the stock is short-term, the gain is classified as short-term capital gain. Thus, she has a net gain of $3,000 ($4,000 – $1,000).

(3) The $3,500 of interest received from First Savings Bank is includible in Helen’s

gross income. The $1,700 of interest received on the City of Springfield school bonds is excludible from gross income.

(4) Helen reports her distributive share of the partnership taxable income of $3,500

rather than the amount of the distribution she received of $2,900. (5) Helen’s deductible medical expenses are $0.

Helen $5,000 Jason (Note 6) 600 $5,600 Less reimbursement (1,200)

$4,400 Less 7.5% of $107,000 (8,025)

Deductions and Losses: In General 5-25

Deductible medical expenses $ -0- (6) Helen can take a dependency exemption for Jason since she is the custodial parent

and did not waive (i.e., no Form 8332) the exemption in 2002. Albert providing more of Jason’s support than Helen does is irrelevant. Therefore, Helen’s deduction for personal and dependency exemptions is $6,000 ($3,000 X 2).

(7) The tax liability from the Tax Table for a head-of-household is $18,044. See the tax return solution beginning on p. 5-26 of the Solutions Manual.

5-26 2004 Comprehensive Volume/Solutions Manual

63.

Deductions and Losses: In General 5-27

63. continued

5-28 2004 Comprehensive Volume/Solutions Manual

63. continued

Deductions and Losses: In General 5-29

63. continued

5-30 2004 Comprehensive Volume/Solutions Manual

63. continued

Deductions and Losses: In General 5-31

63. continued

5-32 2004 Comprehensive Volume/Solutions Manual

63. continued