Chapter 5 Corporate Debt Securities. Financing of Corporate Investments:

101

Chapter 5 Corporate Debt Securities

-

Upload

margaret-bennett -

Category

Documents

-

view

224 -

download

5

Transcript of Chapter 5 Corporate Debt Securities. Financing of Corporate Investments:

Chapter 5

Corporate Debt Securities

Corporate Debt Securities

• Financing of Corporate Investments:

FinancingCorporate

sInvestmentST

sInvestmentLT

FinancingExternal

FinancingInternal

.etc,mergers

,ansionexp,nsacquisitio

,equipment,Plants:LT

.etc,ceviableReAccounts

,sInventorie:ST

earningsretained:Internal

.etc,loansterm,notestermMedium

,BondsCorporate,Stock:LT

Creditoflines,CP:ST

:External

sInvestmentCorporate

Corporate Debt Securities

Corporate Finance Issues:• Internal Verses External Financing

• Capital Structure Decisions: Debt/Equity mix

General Features of Corporate Bonds

General Features:• Principal • Maturity• Interest Rates• Call and Redemption Features• Security• Protective Covenants

Principal and Sinking Funds

• Many corporate bonds pay a principal of $1,000 at maturity.

• To minimize principal risk, many bonds have sinking fund arrangements: provision requiring the issuer to make scheduled payments into a fund.

• Sinking funds can be used to call bonds or buy them up in the secondary market.

• Note: An alternative to a sinking fund in reducing principal risk is a serial bond: bond issue consisting of different maturities.

Sinking Fund Features

• Many sinking fund agreements have provisions requiring an orderly retirement of the issue.

• In recent years, this has been commonly handled by

the issuer being required to buy up a certain portion of the bond issue each year either at a stipulated call price or in the secondary market at its market price.

• This sinking fund call option provision benefits the issuer and is a disadvantage to the bondholder.

Sinking Fund Features

• Sinking funds are usually applied to a particular bond issue. – There are, though, nonspecific sinking funds (sometimes

referred to as tunnel, funnel or blanket sinking funds) that are applied to a company’s total outstanding bonds.

– For most bonds, the periodic sinking fund payments are the same each period.

• Some indentures do allow the sinking fund to increase over time or to be determined by the level of earnings, and some sinking fund provisions give the issuer the option to double the stipulated amount.

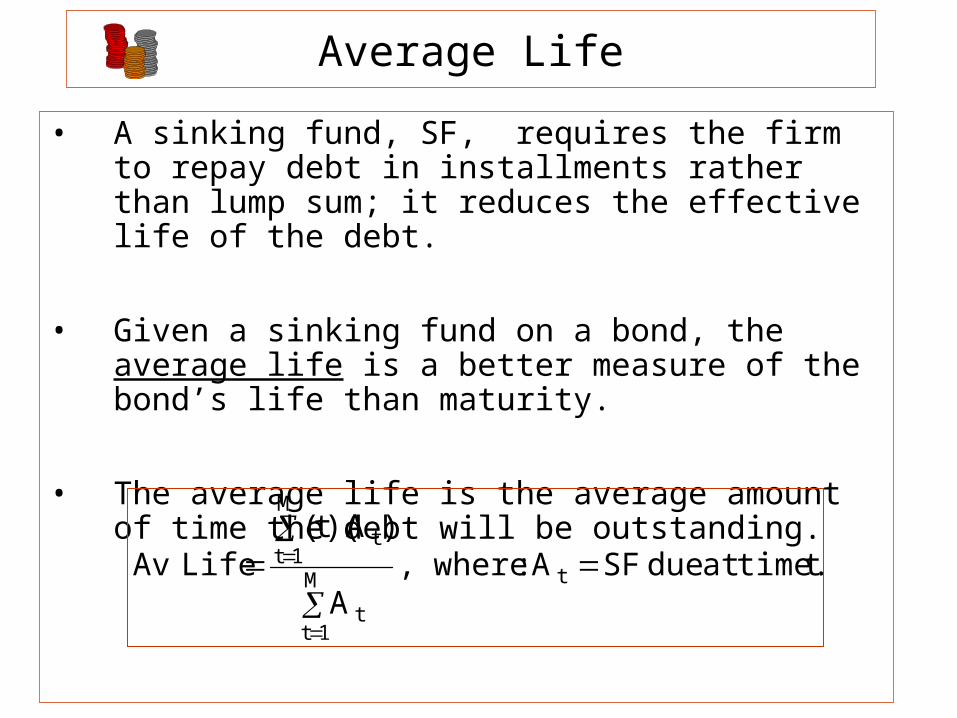

Average Life

• A sinking fund, SF, requires the firm to repay debt in installments rather than lump sum; it reduces the effective life of the debt.

• Given a sinking fund on a bond, the average life is a better measure of the bond’s life than maturity.

• The average life is the average amount of time the debt will be outstanding.

.ttimeatdueSFA:where,A

)A)(t(LifeAv tM

1tt

M

1tt

Average Life

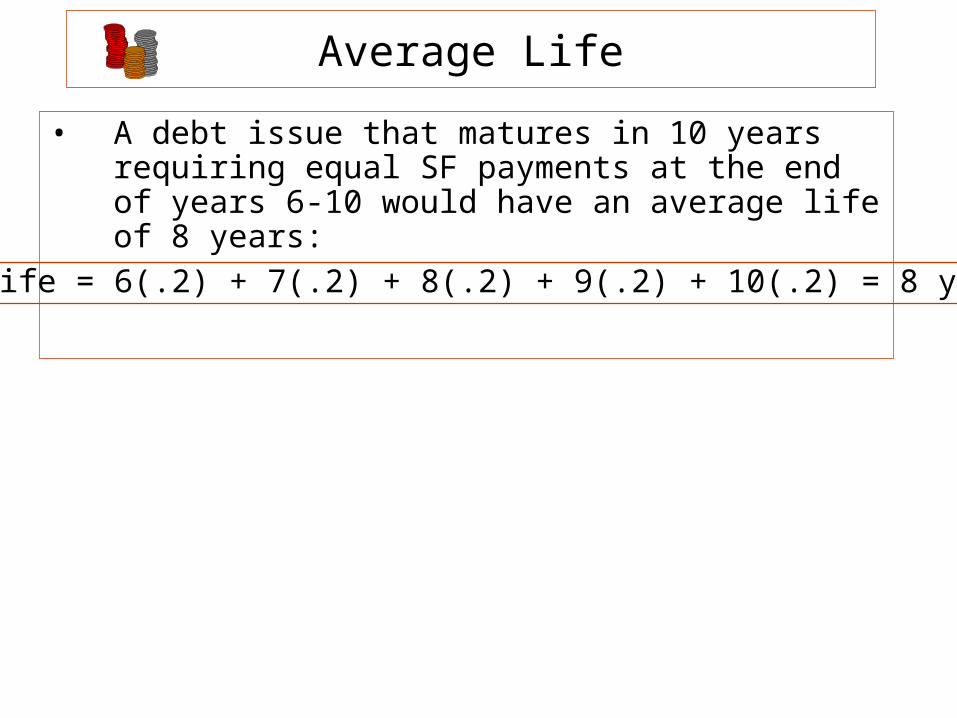

• A debt issue that matures in 10 years requiring equal SF payments at the end of years 6-10 would have an average life of 8 years:

Av life = 6(.2) + 7(.2) + 8(.2) + 9(.2) + 10(.2) = 8 yrs

Maturity

• Firms often choose a maturity in which the outflow obligations are in line with their expected inflows.

• Original Maturity Range: 10yrs. - 30 yrs.

• 1990’s average maturity = 15 yrs.

• Lower maturities in 1980s and 1990s reflects changing technology.

• Point of interest: In 1993, Coke issued a $150M debenture with a maturity of 100 years.

Interest Rate Features

• Based on how they pay interests, there are several types of corporate bonds:– Coupon Bonds– Zero-Coupon Bonds– Deep-Discount Bonds– Floating-Rate Bonds

Coupon Bonds

• Most corporate bonds are coupon bonds paying interest semiannually.

• Many foreign bonds pay interest annually.

• U.S. corporate bonds often used a day count convention of 30/360.

• Most issuers of debt securities select a coupon rate that makes the bond sell initially at par.

Coupon Bonds

• At one time, most bonds were sold with an attached coupon. They were known as bearer bonds since the bonds were paid to the person who had physical possession.

• Today, U.S. bonds are registered bonds. The interest on registered bonds is paid by the issuer or trustee to all bondholders who are registered with the issuer.

Zero-Coupon Bonds

• Zero-coupon corporate bonds were first introduced in the U.S. in the early 1980s.

• Beatrice Foods sold a 10-year, $250M zero coupon priced at $255 per $1,000 face value.

Deep-Discount Bonds

• Corporations also issue deep-discount bonds: – Low coupon rate– Bonds sell at a price below par.

• Some investors, particularly pension funds, find zero and deep discount bonds attractive because they have less reinvestment risk.

Floating-Rate Bonds

• Floating-Rate Bonds (FRN) or floaters pay a coupon rate that varies in relation to another bond, benchmark rate, or formula.

• FRNs originated in Europe.

• Introduced in U.S. in 1974 by Citicorp.

• By 1990, there were approximately 500 floating-rate offerings, with two-thirds offered by banks and financial institutions.

Call and Redemption Features

• The option redemption provision is a call option that gives the issuer the right to buy back the issue.

• Some noncallables may have a hidden call provision written in their sinking fund agreement.

Call and Redemption Features

• Many bonds have a deferred call feature that prohibits the issuer from calling the bond before a certain period of time has expired.

• Nonrefundable Clause: Specifies that during a designated nonrefundable period the issuer cannot use proceeds from a debt issue that ranks superior to or in par with the bond to finance the refunding of the bond.

Call and Redemption Features

• Design of Call Provisions– Example:

• The first year price is equal to the public offering price plus coupon

• Thereafter the call price decreases by equal amounts to equal par

• Thereafter the call price is equal to par.

Call and Redemption Features

• The call provision may also impose limits on the issuer’s ability to exercise the call: – Example: The debt issue is nonrefundable for 5

years or for five years the bond can only be called from proceeds coming from excess cash or equity.

Call and Redemption Features

Optional Redemption Provision – Example: – A bond has a maturity of 25 years, 10% coupon

– Bond issued at 95 ($950, F = $1,000)

– The initial year’s redemption (or call) price is equal to the offering price plus coupon: 95 + 10 = 105

– Bond is callable at par during the last five years

– Call price steps down by equal amounts in 20 steps ((105-100)/20)) to equal 100

– For the first five years the bond is not refundable out of proceeds of a debt issue that ranks senior or on par with this bond

Call and Redemption Features

Year Call Price

1

2

3

4

5

▪

▪

20

21-25

105.00

104.75

104.50

104.25

103.75

▪

▪

100.25

100.00

Security: Mortgage Bonds

• Mortgage Bonds are bonds secured by a lien on a specific asset of the issuer such as property or buildings.

• If there is a default, the lender can seize the asset and sell it. The extra protection that the mortgage provides lowers the risk on the bond and therefore lowers its required return.

Security: Mortgage Bonds

• Often in a mortgage bond, there are provisions in the indenture that allow the mortgaged asset to be sold provided it is replaced with a suitable substitute.

• Some mortgage bonds also have a release and substitution provision that allows for the asset to be sold with the proceeds used to retire the bonds.

• Mortgage bonds are sometimes sold in a series, similar to a serial bond issue, with the bonds of each series secured by the same mortgage. Generally, it is more efficient for a company to issue a series of bonds under one mortgage and one indenture than it is to arrange collateral and draw up a new indenture for each new bond issue.

Security: Equipment-Trust Bonds

• Equipment-Trust Bonds are bonds secured by equipment or plants.

• Equipment-trust bonds are sometimes formed through a lease-and-buy-back agreement with a third party or trustee.

Security: Equipment-Trust Bonds

Lease-and-buy-back Agreement:• Under this type of agreement, a trustee (e.g., bank, leasing company, or

the manufacturer) might purchase the equipment (plane, machine, etc.) and lease it to a company who would agree to take title to the equipment at the termination date of the lease. Alternatively, the company could buy the equipment and sell it the trustee who would then lease it to them.

• The trustee would finance the equipment purchase from the company or

the manufacturer by selling equipment trust bonds (sometime called equipment trust certificates).

• Each period the trustee would then collect rent from the company and pay the interest and principal on the certificates.

• At maturity, the certificates would be paid off, the trustee would transfer the title of the equipment to the company, and the lease would be terminated.

Security: Equipment-Trust Bonds

• Lease-and-buy-back agreements work well when the underlying equipment is relatively standard (e.g., plane, railroad car, or computer) and therefore can be easily sold in the event the company defaults on the lease.

• Airlines and railroad companies are big users of this type of financing.

Security: Collateral-Trust Bonds

• A collateral-trust bond is a bond secured by a lien on the company's holdings of other company's stocks and bonds, other securities and financial claims, or the issuer’s subsidiaries.

• The legal arrangements governing collateral-trust bonds generally require the issuer to deliver to the trustee the pledged securities

• Note: If the securities are stock or the stock of a subsidiary, the issuer/company typically retains its voting rights.

Security: Collateral-Trust Bonds

Features• The issuer is usually required to maintain the value of the

securities, positing addition collateral (e.g., cash or more securities) if the collateral decreases in value.

• There are also provisions in the indenture allowing for the issuer to withdraw the collateral provided there is an acceptable substitute.

• Some collateral-trust bonds are sold as a series, with the same indenture and financial collateral defining each series.

Priority of Claims

• Note: With secured bonds there is a need to establish a priority of claims when more than one debt obligation is secured by the same asset (senior, junior or subordinate).

Closed-End and Open-End Bonds

• A closed-end bond prohibits the asset securing the bond from being used to secure any other debt.

• An open-end bond allows the asset securing the bond to be used as collateral on other debt.

• A typical case is an open‑end bond accompanied with an after‑acquired property clause. This clause dictates that all property or assets acquired after the issue be added to the property already pledged.

Debentures

• Debentures are bonds that are not secured by a specific asset.

• Unsecured debt with original maturities of 10 years or less are referred to as notes, while unsecured debt with original maturities greater than 10 years are referred to as debentures.

• Both are often referred to as debentures.

Debentures

• Debenture holders are general creditors.

• When corporations issue a number of debentures, some may be issued that are subordinate to others (in terms of their claim on assets in the case of bankruptcy) -- subordinate debentures.

• Debenture are often issued with protective covenants: restrictions on additional debt, etc.

• Debenture could be sold with credit enhancements (e.g., letter of credit from a third party).

Guaranteed Bonds

• Guaranteed bonds are bonds issued by one company and guaranteed by another economic entity.

• The guarantee often applies to both the interest and principal.

• With the guarantee, the default risk of the bond shifts from the borrower to the financial capacity of the insurer.

Guaranteed Bonds

Guarantors:

• The guarantor could be the parent company

• The guarantor could be another company securing the issue, perhaps in return for an option on an equity interest in the project the bond is financing.

• There may also be multiple guarantors. In a joint venture, for example, a limited partnership may be formed with several companies who jointly agree to guarantee the bond issue of the venture.

Guaranteed Bonds

Guarantors:

• For some corporate issues, a financial institution may provide the guarantee. – For example, banks for a fee provide corporations

with credit enhancements in the form of letters of credit that guarantee the interest and principal payment on the corporation’s debt obligation.

• Insurance companies also provide coverage of

corporate bonds.

Protective Covenants

• The board of directors hires the managers and officers of a corporation.

• Since the board represents the stockholders, this

arrangement can create a moral hazard problem in which the managers may engage in activities that could be detrimental to the bondholders.

• Example: Managers might use the funds provided by creditors to finance projects different and riskier than bondholders were expecting.

Protective Covenants

• Since bondholders cannot necessarily seek redress from managers after they’ve make decisions that could harm them, they need to include rules and restriction on the company in the bond indenture.

• Such provisions are known as protective or restrictive covenants.

Protective Covenants

• Protective Covenants impose restrictions on the borrower that are designed to protect the bondholders.

• The covenants often specify the financial tests

that must be met before borrowers can incur additional debt (debt limitations) or pay dividends or share repurchase (dividend limitations).

• Example: a covenant that prohibits issuing long-term debt if it would cause the interest coverage ratio (EBIT/Interest) to fall below 3.

Types of Protective Covenants

1. Limitations on debt

2. Limitations on dividends

3. Limitations on share repurchases

4. Limitations that prohibit issuing long-term debt if certain ratios (e.g., interest coverage ratio) are lowered.

5. Limitations on liens

6. Limitations on borrowing from subsidiaries

7. Limitations on mergers, acquisitions, and asset sales

8. Limitations on selling assets and leasing them

Protective Covenants: Event Risk

• Over the last two decades, there has been an increase in the number of mergers, corporate restructurings, and stock and bond repurchases.

• Often these events benefit the stockholders at the expense

of the bondholders, possibly resulting in a downgrade in a bond’s quality ratings and a lowering of its price.

• Bond risk resulting from such actions is known as event risk.

• Certain protective covenants such as poison puts and net worth maintenance clauses have been used to minimize event risk.

Protective Covenants: Poison Put

• A poison put clause in the indenture gives the bondholders the right to sell the bonds back to the issuer at a specified price under certain conditions arising from a specific event such as a takeover, change in control, or an investment rating downgrade.

Protective Covenants: Net Worth Maintenance Clause

• A net worth maintenance clause requires that the issuer redeem all or part of the debt or to give bondholders the right to sell (offer-to-redeem clause) their bonds back to the issuer if the

company’s net worth falls below a stipulated level.

Corporate Bonds with Special Features

• Income Bond

• Participating Bond

• Deferred Coupon Bond

• Tax-Exempt Corporate Bond

• Bonds with Warrants

• Convertible Bond

• Putable Bond

• Extendable Bond

• Credit-Sensitive Bond

• Commodity-Linked Bond

• Voting Bond

• Assumed Bond

Income Bond

• Income Bonds: Bonds that pay interest only if earnings are sufficient. – Often issued by new companies or companies

that are being reorganized.– Similar to preferred stock, except that they

have the tax advantage of being debt.

Participating Bond

• Participating Bonds: Bonds that pay a minimum rate plus an additional rate up to a specified maximum if earnings are sufficient.

Deferred Coupon Bond

• Deferred Coupon Bonds allow the issuer to defer coupon interest. Types of deferred coupon bonds: – Straight Deferred: Interest can be deferred if earnings

are not sufficient; interest does accumulate -- cumulative.

– Reset Bond: Bond starts with a low interest that is later increased.

– Payment-in-Kind Bond: Issuer has the option at the coupon date to pay interest or issue a new bond.

Tax-Exempt Bond

• Tax-Exempt Bonds: Under IRS codes, firms can issue tax-exempt bonds for specific purposes (e.g., financing solid waste disposal facilities).

• Holders of the tax-exempt bond do not have to pay federal income taxes on the interest payments they receive.

Bonds with Warrants

• A warrant is a security or a provision in a security that gives the holder the right to buy a specified number of shares of stock or another designated security at a specified price.

• A warrant is call option issued by the corporation. • As a sweetener, some corporate bonds, such as a

subordinated debenture, are sold with warrants.

• A warrant that is attached to the bond can only be exercised by the bondholder.

• Often, the warrant can be detached from the bond as of a particular date and sold separately.

Convertible Bond

• A convertible bond is one that has a conversion provision that grants the bondholder the right to exchange the bond for a specified number of shares of the issuer's stock.

• A convertible bond is similar to a bond with a non-

detachable warrant. – Like a regular bond, it pays interest and principal, and like

a warrant, it can be exchanged for a specified number of shares of stock.

• Convertible bonds are often sold as a subordinate debenture (convertible debentures). The conversion feature of the bond, in turn, serves as a sweetener to the bond issue.

Putable Bonds

• Putable bonds give the bondholder the right to sell the bond back to the borrower at a specific (exercise) price. – The exercise price is usually set equal to par.– Expiration may be some time before maturity or

the put option may specify one or more dates, each with different exercise prices.

Putable Bonds

• The put option benefits the holder: – If rates increase, the holder can exercise the put, selling

the bond on the put and then investing in higher yielding securities.

• The put also gives the bondholder some reassurance against claim dilution that could result if the firm borrowed more or another firm effected a leverage buyout. – That is, the put gives the bondholders protection against

the value of their bond decreasing because of lower quality ratings.

Extendable Bond

• Extendable bonds give the issuer and/or the investor the option to extend the security’s maturity.

Credit-Sensitive Bond

• Credit Sensitive Bond: This is a bond that has a coupon that varies inversely with the issuer’s credit ratings.– Example: 10% with A Ratings, 11% with BBB,

etc.

• Problem: The coupon rates increase when the company does not need the higher rates.

Commodity-Linked Bond

• Commodity-Linked Bonds: Bonds in which the principal and/or coupon are tied to the price of a particular commodity (e.g., oil, price index, etc.).

• They are designed to enable the producer of a commodity to hedge its exposure to sharp declines in commodity prices.

• Example: An oil producer could design an oil-index bond with interest payments that rise and fall with oil prices.

Voting and Assumed Bonds

• Voting Bonds: Provide voting privileges to holders. – Voting is usually limited to certain issues or

conditions.

• Assumed Bonds: Bonds whose obligations are taken over by another corporation.– Result of mergers or reorganizations.

Bankruptcy

• The bond indenture specifies the events of default (e.g., the borrower fails to pay interest or principal).

• If an issuer defaults, the amount that bondholders receive depends on the security pledged and the priority of claims.

• For the bondholder, how the bankruptcy is handled is also important.

Bankruptcy

• A company is bankrupt or insolvent when the value of its liabilities exceeds the value of its assets.

• A company is in default if it cannot meet is obligations.

• The relation between insolvency and default is time.

Bankruptcy

• Alternatives in the case of default:1. The company can voluntarily file for

bankruptcy with the courts.

2. The bondholders (via a trustee) with other creditors can sue.

3. The company and the bondholders can work out an agreement.

Bankruptcy

• There have been many large corporations that have declared bankruptcy.

• Examples: Enron, Texaco, Federated Department Stores, Continental Airlines, Penn Central, Eastern Airlines, Southland Corporation, and Pan Am.

Bankruptcy

• Note: There are occasions when a company is currently solvent but files for bankruptcy in order to obtain protection against future claimants.

• In 1982, the Manville Corporation was solvent but filed for bankruptcy because of the legal claims against it due to asbestos-related diseases.

Bankruptcy

• In the U.S., The Bankruptcy Reform Act of 1994 governs bankruptcy. The act provides a framework under which liquidation or reorganization are considered.

• Provisions in the act govern:

1. Filing

2. Debtor-in-Possession

3. Formulation of a Plan

4. Disclosure Statement

5. Approval

Bankruptcy

• The courts may decide the company is worth more as a going concern than its liquidation value.

• Note: Reorganization often results in new securities being issued. In such cases, debt securities may be:

• Extended • Composed (e.g., changed into a voting or

participating bond) • Reduced

Quality Ratings

• As noted in Chapter 4, there are three major rating companies in the United States:

1. Moody's Investment Services

2. Standard and Poor's

3. Fitch Investors Service

Quality Ratings

• Moody's and Standard and Poor's are the two most widely used companies.

• Both have been rating bonds for almost 100 years.

• Today, they rate about 2,000 companies, in additional to municipals and other debt obligations.

• Standard and Poor's, Moody’s, and Fitch publish notices of companies whose credit ratings are under scrutiny for a change that could be either an upgrade or downgrade.

Primary Market for Corporate Bonds

• In the primary market, bonds are sold either

– Open Market

– Private Placement

Open Market Sales

• Open market sales are handled through investment bankers who will either:

• Underwrite the issue: Investment banker agrees to buy at a set price and then hopefully sell at a higher one.

• Form underwriting syndicate

• Use best effort

• Provide a standby underwriting agreement

Leading Underwriting Firms of Debt and Equity Issues in 2001

Underwriter Share

1. Citicorp/Salomon Smith Barney2. Merrill Lynch3. Credit Suisse First Boston4. J.P. Morgan Chase5. Goldman Sachs6. Morgan Stanley7. Lehman Brothers8. UBS Warburg9. Deutsche Bank10. Banc of America Securities

12.0%10.6%8.5%7.7%7.4%6.8%6.4%6.2%5.5%4.0%

Source: Wall Street Journal, January 1, 2002

Underwiting Points

• Agreed-upon price is known as the firm commitment

• Difference in price is known as the price spread or

floatation cost (approximately 1%)

• Usually a number underwritng syndicates bid on a large issue

• There is underwriting risk: Rates increase (bond prices decrease) in the market between the time the investment banker buys the bonds and sells them

Procedures for Issuing Bonds

1. Preparing Indenture

2. Registration

3. Forming Selling Group

4. Advertising Issue (issuing a preliminary prospectus or red herring)

5. Selling Issue Through Selling Group

SEC Rule 415: Shelf-Registration Rule

• Rule 415, known as the `shelf registration rule', allows a firm to register an inventory of securities of a particular type for up to two years.

• The firm can then sell the securities whenever it wishes during that time – the securities remain on the shelf.

• To minimize costs, a company planning to finance a number of projects over a period of time could register a large issue and then sell parts of the issue at different times.

Private Placement• An alternative to selling securities to the public is

to sell them directly to institutional investors through a private placement.

• During the 1980s an increasing proportion of new corporate bonds were sold through private placement.

• Because they are sold through direct negotiation with the buyer, privately placed bonds usually have fewer restrictive covenants than publicly issued ones, and they are more tailor-made to both the buyer's and seller's particular needs.

SEC Rule 144A

• Historically, one of the disadvantages of privately placed bonds was their lack of marketability due to the absence of an active secondary market.

• Under the SEC Act of 1933, firms could only offer securities privately (which did not require SEC registration) to investors deemed sophisticated – insurance companies, pension funds, banks, and endowments.

SEC Rule 144A• In 1991, the SEC adopted Rule 144A under SEC Act 1933.

• Under this rule, issuer could sell unregistered securities to one or more investment bankers who could resell the securities to ‘qualified investment buyers’ (QIBs). QIBs could then sell freely with each other in securities that had not been registered.

• The adoption of SEC Rule 144A eliminated some of the restrictions on the secondary trading of privately placed bonds by institutional investors.

• SEC Rule 144A created a secondary market for privately placed bonds.

Secondary Market for Corporate Bonds

• Many corporate bonds are traded on the OTC market where they are handled by dealers.

• Many corporate bonds are held by institutional investors who tend to hold bonds to maturity. As a result, the secondary market for some bonds can be relatively thin.

Secondary Market Spreads

• It is important to remember that the degree of trading activity determines a bond’s degree of marketability and the spread between a dealer’s bid and asked prices.

• In the corporate bond markets the spreads range from a low of ¼ to ½ of point (good marketability) to as high as 2% (poor marketability).

• For an investor who plans to buy a bond at its initial offering and hold it to its maturity a thin market is not a concern.

• The spread is a major concern, though, to a bond speculator or a fund manager who needs marketability or whose profit margins could be negated by a large spread.

OTC and NYSE Corporate Bonds

• While a sizable amount of secondary market bond trading occurs on the OTC market, there are still over large number of bonds listed on NYSE.

• Dealers on the OTC market who have a large and broad market trade many of these listed bonds.

• The NYSE promotes the OTC trading by allowing its members to trade listed bond off the exchange if they can obtain a better price.

Information on Corporate Bonds

• Information on the trading of existing corporate bonds is reported in– Wall Street Journal – Financial sections of many newspapers

• Information on bond yields and prices for a large number of bonds can be found in – The Daily Bond Buyer – Commercial and Financial Chronicle

Information on Corporate Bonds

• Information on specific bonds can be found in – Moody's Bond Mannual – Moody’s Bond Record provides summary information – Moody’s Bond Survey provides information on new

issues– S&P Corporation Record provides information on new

issues – S&P Bond Guide provides summary information

• The above information includes: quality rating, use of the bond proceeds, information on the issuer, collateral, guarantees, call and other options, restrictions, and sinking fund arrangements.

Information on Corporate Bonds

• For new corporate bond issues, investors also can obtain the prospectus from the SEC.

• For distressed companies, a good source for information is Dunn & Bradstreet’s Business Failure Record.

Bond Indices

• Dow Jones Bond Average: This is an average of the prices of 20 corporate, 10 utility, and 10 industrial bonds.

• There also are a number of bond yield indices formed by pooling several bond issues of similar characteristics and quality ratings. – One of the more popular of these is Moody's corporate

bond index that is reported in the Federal Reserve Bulletin and the Shearson‑Lehman’s index.

Commercial Paper

• Commercial Paper (CP): Short-term securities issued by corporations to finance their working capital or to provide funds for credit given their customers.

• Buyers of CP: Institutional investors and corporations investing their excess cash.

Commercial Paper Features

1. Most CP issues are sold on a pure discount basis, although there are some that are sold with coupon interest.

2. The original maturities of CP range from three days (weekend paper) to 270 days, with the average original maturity being 60 days.

– The Securities Act of 1933 exempted companies issuing CP from registering with the SEC if the issue were less than 270 days. As a result of this provision, many CP issues have maturities of less than 270 days; this reflects the desire by issuers to avoid the time‑consuming SEC registration.

Commercial Paper Features

3. CP issues are usually sold in denominations from $100,000, although some are sold in $25,000 denominations.

4. CP is often described as unsecured. The unsecured feature of CP means that there is no specific asset being pledged to secure the issue.

5. Many CP issuers back up their paper with an unused line of credit from a bank. The line of credit is a safeguard in the event the CP issuer cannot pay off the principal or sell new CP to finance the principal payment on the maturing issue.

Commercial Paper Features

6. Many smaller, lower quality companies also obtain a letter of credit from a bank or financial institution to secure their issues.

• A letter of credit is a certificate in which the bank or institution promises to repay the principal or interest if the issuer defaults.

• Paper sold with this type of credit enhancement is called LOC paper, documented paper, or credit-supported CP.

• Credit enhancements can also take the form of a surety bond from an insurance company.

Commercial Paper Features

7. Some companies collateralize their issue with other assets.

• Included in this group of asset-based paper is securitized CP, often issued by a bank holding company.

• In these cases, a bank holding company sells CP to finance a pool of credit card receivables, leases, or other short‑term assets, with the assets being used to secure the CP issue.

Types Commercial Paper

• Direct CP: CP sold by the corporation directly to investors. Direct CP is often sold by captive finance companies (GMAC, Ford Credit, etc.) with the proceeds used to finance the parent company’s installment loans.

• Dealer Paper (Industry Paper): CP sold by dealers (e.g., Shearson-Lehman, dealers that are part of a bank holding company, etc. ). Dealers buy the paper from corporations, then sell it to investors.

Medium Term Notes

• Medium‑term note (MTN) is a debt instrument sold on a continuing basis to investors who are allowed to choose from a group of bonds from the same corporation, but with different maturities.

Medium Term Notes: History

• MTN were first introduced in the 1970s when General Motors Acceptance Corporation (GMAC) sold such instruments to finance its automobile loans.

• MTN took off in the early 1980s when Merrill Lynch began acting as an agent in issuing MTNs and also as a dealer by making a secondary market for the notes.

• The market for MTNs grew from a $3.8 billion market in 1982 to a $150 billion one in 1998.

Medium Term Notes

• MTN’s growth can be attributed to the flexibility they provided corporations in the types of securities they can offer, and given the Security Exchange Commission Rule 415, the flexibility related to when they can offer them.

Medium Term Notes: Issuing Process

1. A corporation planning to issue a MTN first files a shelf registration form with the SEC. The filing includes a prospectus of the MTN program (different notes, their maturities, par values, and the like).

2. By filing a shelf registration form, the corporation is able to enter the market constantly or intermittently, giving it the flexibility to finance a number of different short-, intermediate-, and long-term projects over a two-year period.

Medium Term Notes: Issuing Process

3. Typically, the MTNs are sold through investment banking firms who act as agents.

– The agents will often post the maturity range for the possible notes in the program and their offering rates.

– The rates are often quoted in terms of a spread over a Treasury security with a comparable maturity.

Medium Term Notes: Example

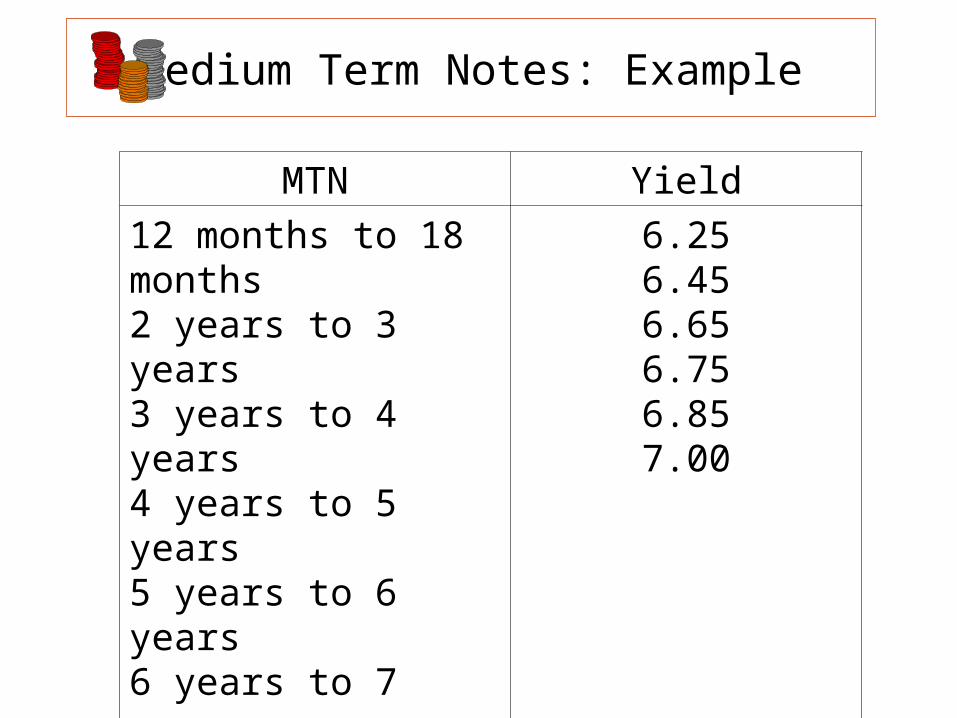

MTN Yield

12 months to 18 months2 years to 3 years3 years to 4 years4 years to 5 years5 years to 6 years6 years to 7 years

6.256.456.656.756.857.00

Medium Term Notes: Issuing Process

4. An investor interested in one of the note offerings will notify the agent who, in turn, contacts the issuing corporation for a confirmation.

5. Once a MTN issue is sold, then the company can file a new registration to sell a new MTN issue – an action known as reloading.

Medium Term Notes: Reverse Inquiry

• In addition to providing issuing corporations with flexibility in their capital budget, a MTN program also gives institutional investors, such as pensions and life insurance companies, an opportunity to choose notes whose maturities best fit their liabilities, thereby minimizing their market risk.

Medium Term Notes: Reverse Inquiry

• In many instances, the market for MTNs starts with institutional investors indicating to agents the type of maturity they want (e.g., $10M of notes with a maturity of 6.25 years); this is known as reverse inquiry.

• On a reverse inquiry, the agent will inform the

corporation of the investor’s request; the corporation could then agree to sell the notes with that maturity from its MTN program, even if they are not posted.

Medium Term Notes: Points

• Today, MTNs are issued not only by corporations, but also by bank holding companies, government agencies, supranational institutions, and sovereign countries.

• MTNs vary in terms of their features; some, for example, are offered with fixed rates while other pay a floating rate.

• There are also MTNs that are combined with other instruments in what is referred to as a structured MTN.

Websites

• For more information on corporate bankruptcy, see “What Every Investor should Know About Corporate Bankruptcy,” at www.sec.gov/investor/pubs/bankrupt.htm

• Corporate bonds spreads and other information on corporate bonds can be found by going to www.bondsonline.com

Websites: Moody’s, S&P, and Fitch

• Moody’s rating changes and watch list can be found by going to www.moodys.com and clicking on “Watchlist” (registration is required).

• Standard and Poor’s rating changes and watch list can be found by going to www.standardandpoors.com and clicking on “Credit Rating Actions.”

• Fitch’s rating changes can be found by going to www.fitchratings.com and clicking on “Corporates” and “Issuer List.”

Websites: Yields

• For information on Moody’s corporate bond yields go to www.bondmarkets.com and click on “Bond Market Statistics.” For information on bond market trends click “Research Report.”

• For information on security laws go to www.sec.gov and click on “Market Regulations” under “SEC Divisions.”

• For information on current yields go to http://bonds.yahoo.com and click on “Corporate Bond Rates.” For identifying bonds that have certain features, click on “Bond Screener.”

Websites: CP and MTNs

• For historical data on CP rates go to www.bondmarkets.com and click on “Statistics” under “Research,” and then click on “Money Market Instruments.”

• For information on MTNs go to www.federalreserve.gov/releases/medterm/about.htm

• For information on the size of the market for MTNs go to

www.federalreserve.gov/releases/medterm