Chapter 4: Time Value of Money - myCSU · Learning Objectives 1. To understand the concept of the...

17

Transcript of Chapter 4: Time Value of Money - myCSU · Learning Objectives 1. To understand the concept of the...

Chapter 4: Time Value of Money

Class Slides

Learning Objectives

1. To understand the concept of the time value of money.

2. To be able to compute the future or present value of money (i.e., compounding and discounting).

Money that you have today is worth more than the same amount of money received in the future - Effect of Inflation - Can Invest Money Issues related to time value of money become more critical as period of time increases – this is quite germane to most capital projects being evaluated

Time Value of Money

Process of going from today’s value of money (Present Value) to some future value of money (Future Value)

Compounding

Calculating the future value of money - compounding

Future Value = Present Value + Interest Earned

Where, Interest Earned = Present Value * Interest Rate

(i)

Create a timeline

FV = PV + I Which is the same as: FV = PV + (PV*i) Simplifying: FV = PV(1 + i)

Compounding for One Period

FVn = PV(1 + i)n

Where: FVn = future value in time period n PV = present value i = stated interest rate n = number of time periods

The General Compounding Formula

Compounding more frequently than annually

Not unusual for funds to compound more frequently

than annually; e.g.,

Semiannually = two times per year or every six

months

In Semiannual compounding: number of compounding

periods doubles, but

Interest rate of compounding is halved each period

Time Period (year) 0 1 2 |_1%____| 1%______|_1%____ | 1%_____| Value ($) $100 $101.00 $102.01 $103.03 $104.06

(Present (Future Value) Value)

Timeline showing present value (PV) and future value (FV) of $100 invested for two years at a 2%

annual rate, compounded semiannually

Effective Annual Rate (EAR)

A tool used to compare opportunities with different compounding schedules. In effect, EAR annualizes everything, enabling apples-to-apples comparison The compounding rate that would have increased the initial investment to the higher future value (i.e., the amount calculated for the scenario with more frequent compounding), assuming annual compounding.

Effective Annual Rate Example Assume initial $100 deposit

Compounding 2% semiannually

EAR calculation:

$100(1 + i) = $102.01

(1 + i) = ($102.01/$100)

i = ($102.01/$100) – 1

= (1.0201 – 1.000)

= .0201 = 2.01%

Formula for EAR

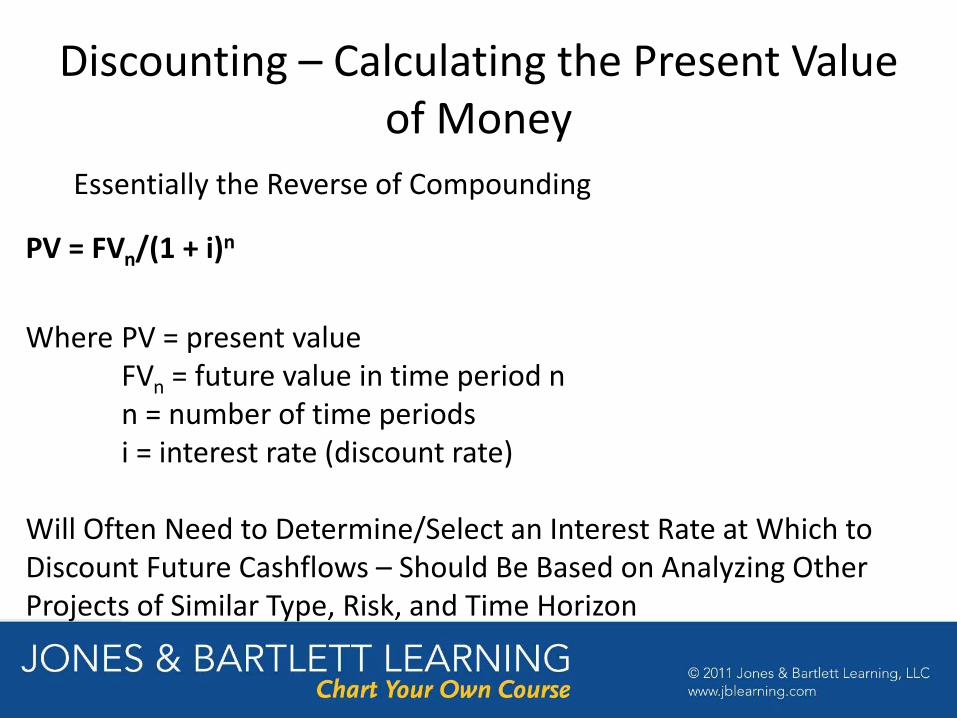

Discounting – Calculating the Present Value of Money

Essentially the Reverse of Compounding

PV = FVn/(1 + i)n

Where PV = present value FVn = future value in time period n n = number of time periods i = interest rate (discount rate) Will Often Need to Determine/Select an Interest Rate at Which to Discount Future Cashflows – Should Be Based on Analyzing Other Projects of Similar Type, Risk, and Time Horizon

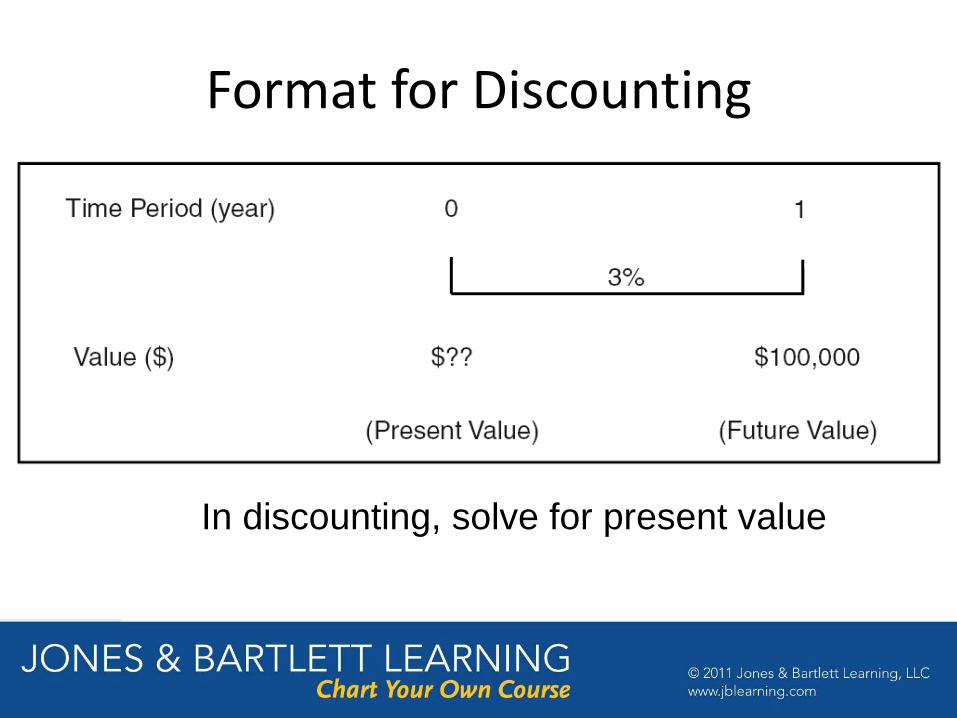

Format for Discounting

In discounting, solve for present value

Summary

All management decisions involving time value of

money require compounding and discounting

Key stage is to identify the “missing variable” – that

is, what are we solving for?

Start with a timeline