CHAPTER 4 FINDINGS AND DISCUSSIONS 4.1 Goodwill ...thesis.binus.ac.id/Asli/Bab4/BAB 4_07-01.pdfNO....

31

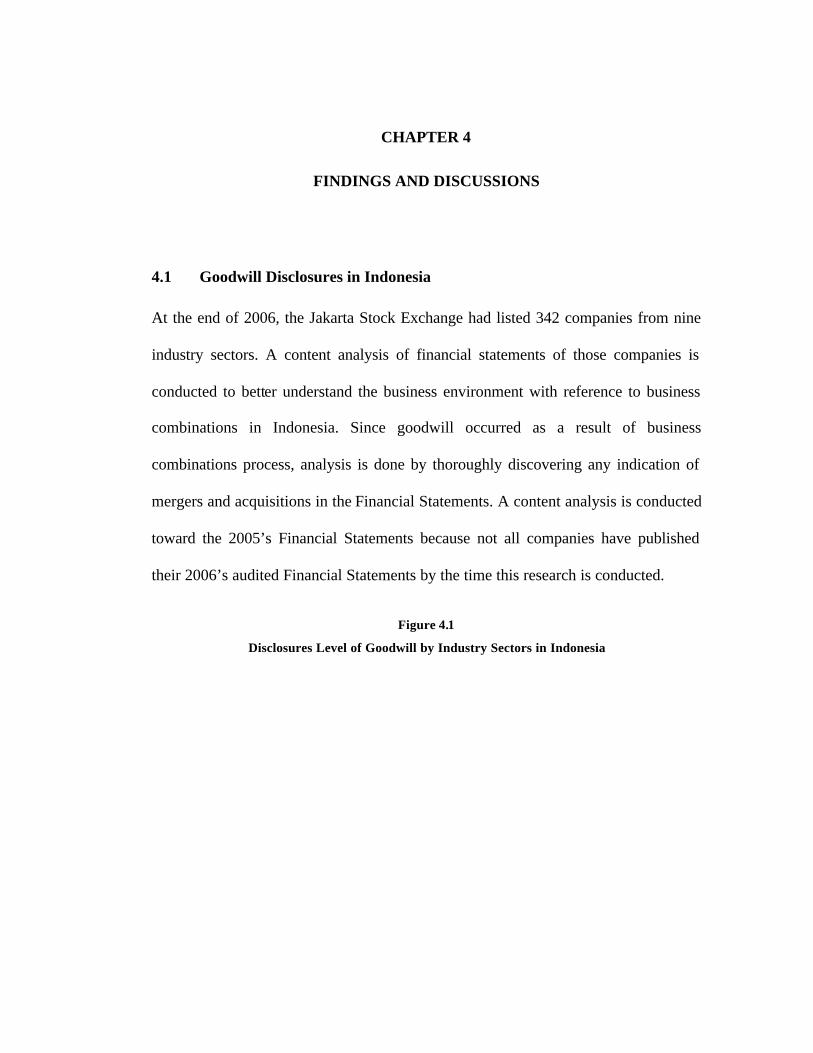

CHAPTER 4 FINDINGS AND DISCUSSIONS 4.1 Goodwill Disclosures in Indonesia At the end of 2006, the Jakarta Stock Exchange had listed 342 companies from nine industry sectors. A content analysis of financial statements of those companies is conducted to better understand the business environment with reference to business combinations in Indonesia. Since goodwill occurred as a result of business combinations process, analysis is done by thoroughly discovering any indication of mergers and acquisitions in the Financial Statements. A content analysis is conducted toward the 2005’s Financial Statements because not all companies have published their 2006’s audited Financial Statements by the time this research is conducted. Figure 4.1 Disclosures Level of Goodwill by Industry Sectors in Indonesia

Transcript of CHAPTER 4 FINDINGS AND DISCUSSIONS 4.1 Goodwill ...thesis.binus.ac.id/Asli/Bab4/BAB 4_07-01.pdfNO....

CHAPTER 4

FINDINGS AND DISCUSSIONS

4.1 Goodwill Disclosures in Indonesia

At the end of 2006, the Jakarta Stock Exchange had listed 342 companies from nine

industry sectors. A content analysis of financial statements of those companies is

conducted to better understand the business environment with reference to business

combinations in Indonesia. Since goodwill occurred as a result of business

combinations process, analysis is done by thoroughly discovering any indication of

mergers and acquisitions in the Financial Statements. A content analysis is conducted

toward the 2005’s Financial Statements because not all companies have published

their 2006’s audited Financial Statements by the time this research is conducted.

Figure 4.1

Disclosures Level of Goodwill by Industry Sectors in Indonesia

31

4

9 98

65

17

02468

1012141618

AGRIMINING

BASIC IND. & CHEMICALS MISC.

CONSUMER GOODS

PROP, REAL EST. & BLDG CONST

INFRASTR, UTIL. & TRANSPORT

FINANCE

TRADE, SERV. & INVEST.

INDUSTRY

NO

. OF

CO

MP

AN

IES

It was found that from a population of 342 companies, 62 companies (18%) disclosed

goodwill under the non-current asset section in the balance sheet of 2005. The

majority of goodwill disclosure is from trade, service and investment industry

(27.4%). Both basic industry and chemicals, and the consumer goods industry take

the second place at 14.5%. Business acquisitions might be an advantageous strategy

for these industries to expand as well as to maintain an excellent performance.

As shown in Figure 4.1, industry with the lowest goodwill disclosure level is the

mining industry (1.6%). There are 10 mining companies listed in the Jakarta Stock

Exchange and the existence of goodwill is found in three of them. However, two

companies include the amount of goodwill as part of the account “oil and gas

properties” and do not disclose it clearly as goodwill. Consequently, the actual

amount of goodwill is undetectable. The other company discloses goodwill normally

as a separate account on the balance sheet.

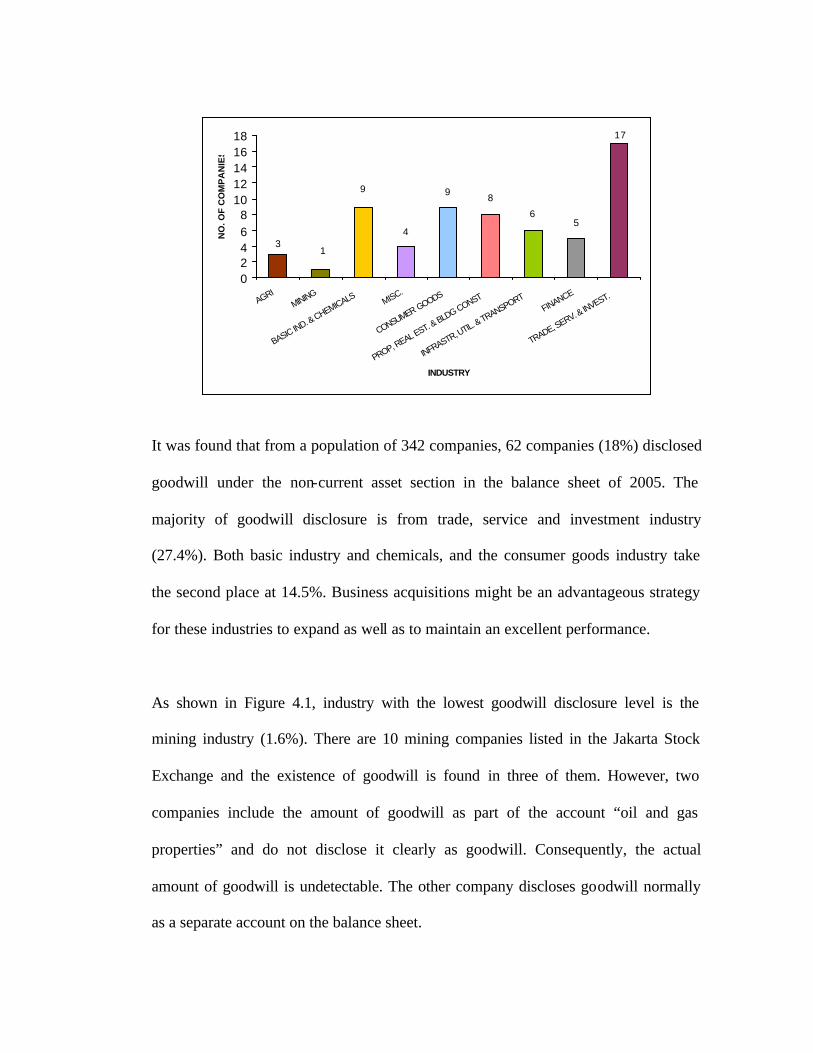

4.1.1 The Size of Goodwill Compared To Total Assets

General observation, goodwill is not a material asset in most of the companies in

Indonesia. As much as 87.1% listed companies only have goodwill le ss than 5% from

their total assets. In fact, 59.68% listed companies only have goodwill of less than 1%

from their total assets. Only about 13% companies have goodwill of more than 5% of

their total assets and these companies came from various industries such as

advertising, printing and media, mining, and telecommunication.

Figure 4.2

Classification of Goodwill Proportion to Total Assets

59.68%

27.42%

12.90%

LESS THAN 1% BETWEEN 1% - 5% MORE THAN 5%

THE PROPORTION OF GOODWILL TO TOTAL ASSETS

4.1.2 Various Goodwill Terminologies Adopted in Indonesia

From the sample of 62 companies, the author found several terminologies that

represent the account of goodwill. The most popular terminology used by 50% of

firm observation is “net goodwill” or “goodwill after accumulated amortization” The

next popular terminology used is a simply “Goodwill”, which is adopted by 19% of

the 62 companies. Although these companies do not describe the net amount of

goodwill after accumulated amortization, the term “goodwill” actually represents so.

Another 18% companies use the term “excess gain of investment over net assets of

subsidiaries”. These companies typically own less than 1% goodwill over total assets.

However, the latter term represents the same meaning as goodwill. The rational of

“hiding” the word goodwill behind other term probably because that the goodwill

amount is not material. Table 4.1 also shows that 6% companies use the account

“intangible assets” and 6% companies use other terms, such as “goodwill and other

intangible assets” and “other assets”.

Those companies which disclose goodwill as something else and not clearly as

goodwill on the face of the balance sheet may deviate from Indonesia’s General

Accepted Accounting Principal (GAAP) which actually requires goodwill to be

presented on the face of the balance sheet.

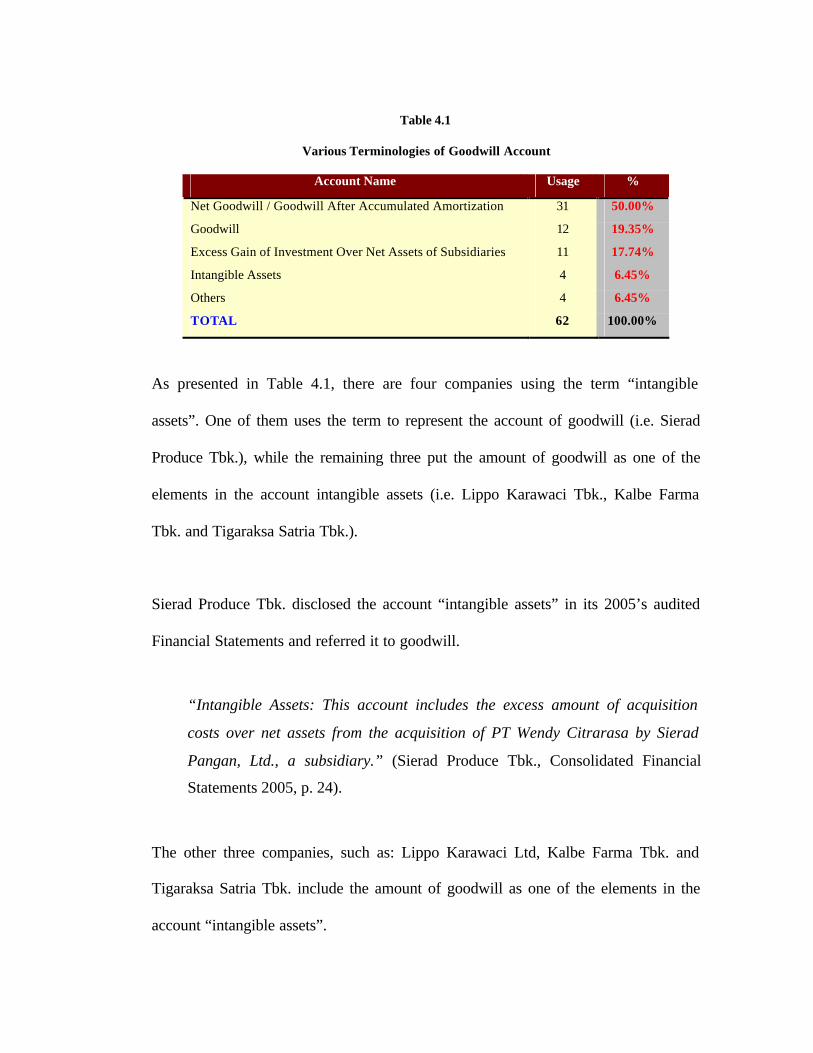

Table 4.1

Various Terminologies of Goodwill Account

Account Name Usage %

Net Goodwill / Goodwill After Accumulated Amortization 31 50.00%

Goodwill 12 19.35%

Excess Gain of Investment Over Net Assets of Subsidiaries 11 17.74%

Intangible Assets 4 6.45%

Others 4 6.45%

TOTAL 62 100.00%

As presented in Table 4.1, there are four companies using the term “intangible

assets”. One of them uses the term to represent the account of goodwill (i.e. Sierad

Produce Tbk.), while the remaining three put the amount of goodwill as one of the

elements in the account intangible assets (i.e. Lippo Karawaci Tbk., Kalbe Farma

Tbk. and Tigaraksa Satria Tbk.).

Sierad Produce Tbk. disclosed the account “intangible assets” in its 2005’s audited

Financial Statements and referred it to goodwill.

“Intangible Assets: This account includes the excess amount of acquisition

costs over net assets from the acquisition of PT Wendy Citrarasa by Sierad

Pangan, Ltd., a subsidiary.” (Sierad Produce Tbk., Consolidated Financial

Statements 2005, p. 24).

The other three companies, such as: Lippo Karawaci Ltd, Kalbe Farma Tbk. and

Tigaraksa Satria Tbk. include the amount of goodwill as one of the elements in the

account “intangible assets”.

“The excess amount that can not be identified between the acquisition cost of

investment and the fair value of net assets of subsidiaries (goodwill) is

amortized using the straight-line method over twenty (20) years. The group of

management believes that the amortization period of twenty (20) years is

appropriate due to the prospective benefits of the acquiring subsidiaries. That

unidentified excess amount is reported as part of "Intangible Assets", while the

less amount is reported as “negative goodwill” in the consolidated balance

sheets.” (Kalbe Farma Tbk., Consolidated Financial Statements 2005, p.14).

“Intangible assets consist of brand name, copyrights and formula, as well as

computer software.” (Kalbe Farma Tbk., Consolidated Financial Statements

2005, p.38).

“Intangible Assets include: (a) Computer Software License; the acquisition cost

of computer software license SAP is capitalized as assets and amortized using

the straight-line method over 5 (five) years, (b) Goodwill; the excess amount

between the acquisition cost of investment and the fair value of net assets of

subsidiaries is recognizes as goodwill or negative goodwill and amortized using

the straight-line method over 20 years, (c) Brand Name; brand name is

recognized at cost and amortized using the straight-line method over 10 years.”

(Tigaraksa Satria Tbk., Consolidated Financial Statements 2005, p.12)

“Intangible Assets: The excess amount of investment over net assets of

subsidiaries (goodwill) is amortized using the straight-line method over 20

(twenty) years. The acquisition costs of accounting software is deferred and

amortized using the straight-line method based on its benefits life over 5 (five)

years.” (Lippo Karawaci Tbk., Consolidated Financial Statements 2005, p. 17)

Last but not least, there are four companies using other terms, such as “goodwill and

other intangible assets” (i.e. Indosat Tbk. and Telekomunikasi Indonesia Tbk.),

“intangible assets goodwill” (i.e. Infoasia Teknologi Global Tbk.), and “other assets”

(Indonesia Prima Properti Tbk.).

Indosat, Ltd used the account “goodwill and other intangible assets” to disclose

goodwill, brand, customer base, and spectrum license, while Telekomunikasi

Indonesia Tbk. used it to disclose goodwill and the rights to operate the business of

its subsidiaries.

“Other intangible assets occurred from the acquisition of Dayamitra,

Pramindo, AWI and KSO IV, and involve the rights to operate the business in

KSO area. Goodwill occurred from the acquisition of GSD.” (Telekomunikasi

Indonesia Tbk., Consolidated Financial Statements 2005, p.54).

Infoasia Teknologi Global Tbk. used the term “intangible assets goodwill” on the

face of 2005’s Balance Sheet; while on the Notes to Consolidated Financial

Statements, they use the term “goodwill”. The dissimilarity of terminologies for one

account might confuse readers, even though both terms refer to the same meaning.

Indonesia Prima Properti Tbk. included the amount of goodwill as part of the account

“other assets” in the Consolidated Financial Statements 2005. However, in the

Consolidated Financial Statements 2004, the company used the account “goodwill”.

According to the Notes to Consolidated Financial Statement 2005, the amount of

goodwill after accumulated amortization for that period is zero. Thus, the company

used the account “other assets” in 2005 to re-disclose the 2004’s goodwill amount.

The inclusion of goodwill among other intangible assets under one specific account,

by nature, is inappropriate. PSAK No. 19 article 12 states that intangible asset can be

clearly distinguished from goodwill if that asset can be separated from the firm’s

entity. Such intangible assets as patents, copyrights, trademarks, and trade secrets are

“separable” because its value is identifiable. Goodwill, on the other hand, can not be

separated from the firm’s entity and exchanged or sold singly due to its unidentifiable

characteristic. Seeing that the nature and characteristic of goodwill is different from

other intangible assets, it should be separated from other intangible assets and

recognized separately in the balance sheet.

Business combinations of oil and gas industry use different accounting treatment

pertaining to goodwill. Goodwill of the acquired oil and gas companies is recognized

under the account “Oil and Gas Properties1” if applicable for capitalization and is

amortized over the life of the Production Sharing Contracts (PSC) using the unit of

production method2. Negative goodwill is treated in a normal manner. There are two

companies using such treatment; Medco Energi International Tbk. and Energi Mega

Persada Tbk.

1 Indonesian: Aktiva minyak dan gas bumi 2 Notes to the Consolidated Financial Statements of PT Medco Energi International and PT Energi

Mega Persada

4.1.3 The Compliance of Goodwill Disclosures with PSAK 22

From the author’s observation the compliance rate of goodwill disclosure in

Indonesia is considerably low. From 62 sample companies, there are 33 companies

(53.23%) that have met all the disclosure requirements of goodwill as stated in the

PSAK 22 article 66. It means that almost a half of those companies failed to meet the

standard.

The similar result also founded in US in 1988, when the accounting standard of

goodwill was still amortization. Duval, et.al (1992) conducted a survey in 1988

among 621 firms of New York and American Stock Exchange. Twenty-one percent

did not disclose net goodwill, 58 percent did not disclose accumulated goodwill

amortization and 76 percent did not disclose goodwill amortization expense.

According to the PSAK No. 22 article 66, a financial statement should disclose:

a) Accounting treatment for goodwill including its amortization periods

b) If the benefits life of goodwill is more than five years, an explanation of

reasons and considerations being used

c) If goodwill not to be amortized using the straight- line method, other method

used and its reasons

d) Goodwill reconciliation at the beginning and end of the period

The author have conducted a thorough examination over financial statements of the

62 sample companies to indicate if those companies have followed goodwill

disclosure requirements stated in the PSAK 22 article 66. The examination results are

presented below.

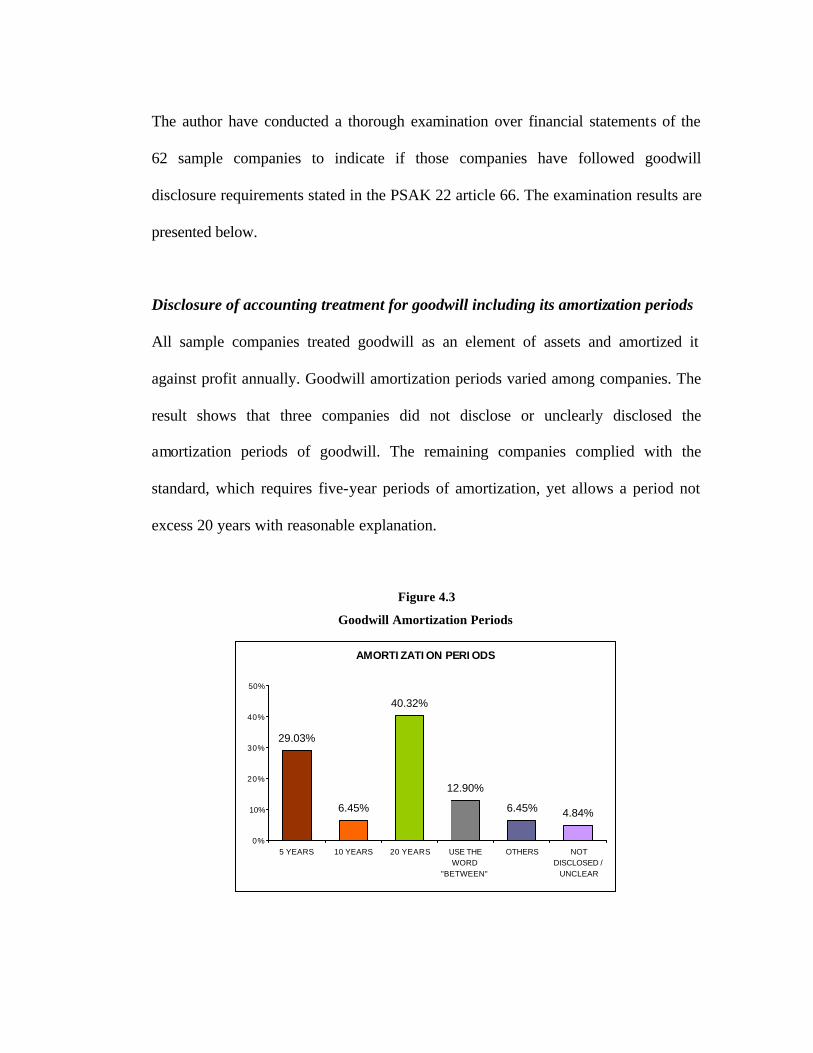

Disclosure of accounting treatment for goodwill including its amortization periods

All sample companies treated goodwill as an element of assets and amortized it

against profit annually. Goodwill amortization periods varied among companies. The

result shows that three companies did not disclose or unclearly disclosed the

amortization periods of goodwill. The remaining companies complied with the

standard, which requires five-year periods of amortization, yet allows a period not

excess 20 years with reasonable explanation.

Figure 4.3

Goodwill Amortization Periods

AMORTIZATION PERIODS

29.03%

6.45%

40.32%

12.90%

6.45% 4.84%

0%

10%

20%

30%

40%

50%

5 YEARS 10 YEARS 20 YEARS USE THEWORD

"BETWEEN"

OTHERS NOTDISCLOSED /

UNCLEAR

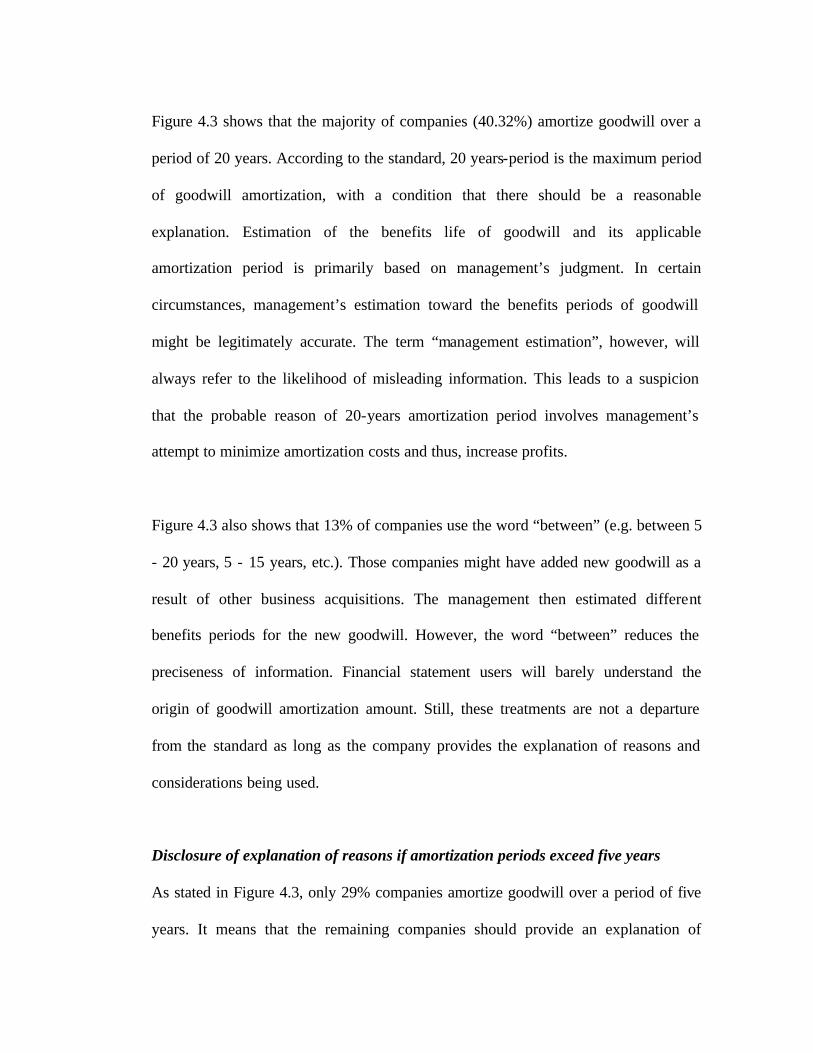

Figure 4.3 shows that the majority of companies (40.32%) amortize goodwill over a

period of 20 years. According to the standard, 20 years-period is the maximum period

of goodwill amortization, with a condition that there should be a reasonable

explanation. Estimation of the benefits life of goodwill and its applicable

amortization period is primarily based on management’s judgment. In certain

circumstances, management’s estimation toward the benefits periods of goodwill

might be legitimately accurate. The term “management estimation”, however, will

always refer to the likelihood of misleading information. This leads to a suspicion

that the probable reason of 20-years amortization period involves management’s

attempt to minimize amortization costs and thus, increase profits.

Figure 4.3 also shows that 13% of companies use the word “between” (e.g. between 5

- 20 years, 5 - 15 years, etc.). Those companies might have added new goodwill as a

result of other business acquisitions. The management then estimated different

benefits periods for the new goodwill. However, the word “between” reduces the

preciseness of information. Financial statement users will barely understand the

origin of goodwill amortization amount. Still, these treatments are not a departure

from the standard as long as the company provides the explanation of reasons and

considerations being used.

Disclosure of explanation of reasons if amortization periods exceed five years

As stated in Figure 4.3, only 29% companies amortize goodwill over a period of five

years. It means that the remaining companies should provide an explanation of

reasons and considerations that affect their decision to amortize goodwill over a

period more than five years.

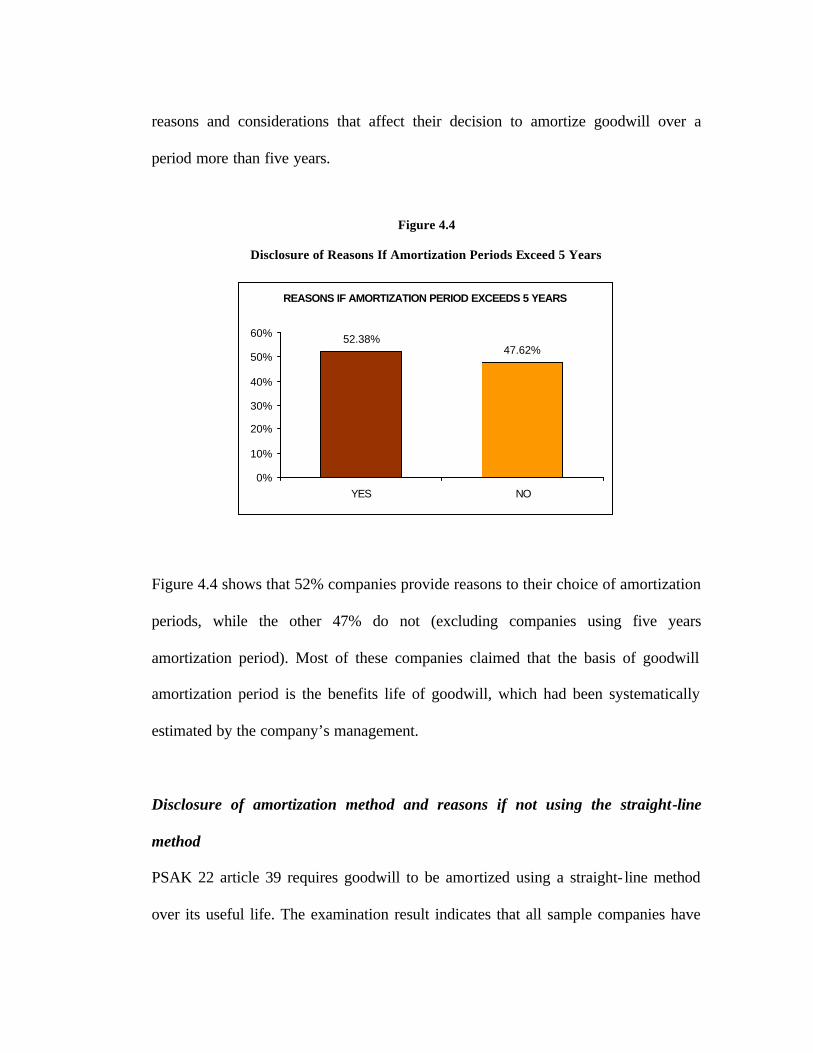

Figure 4.4

Disclosure of Reasons If Amortization Periods Exceed 5 Years

REASONS IF AMORTIZATION PERIOD EXCEEDS 5 YEARS

52.38%47.62%

0%

10%

20%

30%

40%

50%

60%

YES NO

Figure 4.4 shows that 52% companies provide reasons to their choice of amortization

periods, while the other 47% do not (excluding companies using five years

amortization period). Most of these companies claimed that the basis of goodwill

amortization period is the benefits life of goodwill, which had been systematically

estimated by the company’s management.

Disclosure of amortization method and reasons if not using the straight-line

method

PSAK 22 article 39 requires goodwill to be amortized using a straight- line method

over its useful life. The examination result indicates that all sample companies have

applied the straight- line method for goodwill amortization. Thus, no company

requires explanation of other method of amortization.

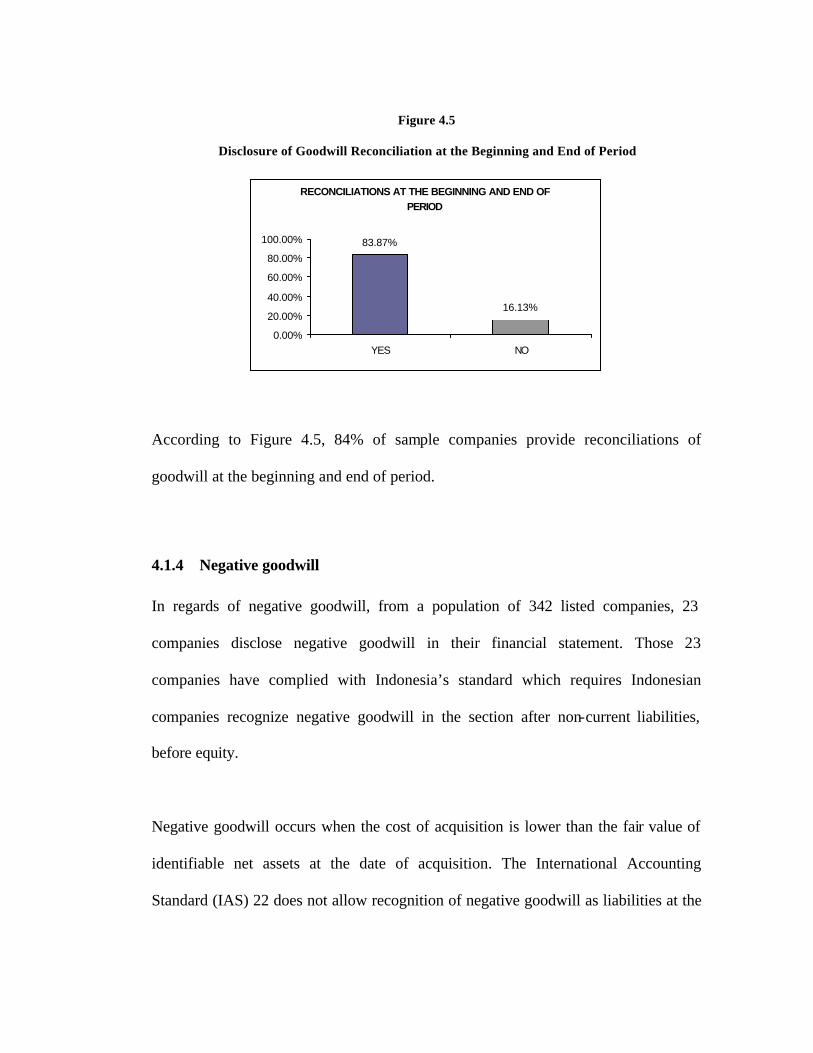

Disclosure of goodwill reconciliation at the beginning and end of the period

Goodwill reconciliation refers to a note containing goodwill information, which

includes (PSAK 22 article 66):

§ The gross amount of goodwill and accumulated amortization at the beginning

of the period

§ Additional goodwill amount recorded throughout the period

§ Amortization amount for the period

§ Reconciliation of subsequent changes or identification of the value of assets

and liabilities after the date of acquisition

§ Deductions of goodwill amount made throughout the period

§ The gross amount of goodwill and its accumulated amortization at the end of

the period

Figure 4.5

Disclosure of Goodwill Reconciliation at the Beginning and End of Period

RECONCILIATIONS AT THE BEGINNING AND END OF PERIOD

83.87%

16.13%

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

YES NO

According to Figure 4.5, 84% of sample companies provide reconciliations of

goodwill at the beginning and end of period.

4.1.4 Negative goodwill

In regards of negative goodwill, from a population of 342 listed companies, 23

companies disclose negative goodwill in their financial statement. Those 23

companies have complied with Indonesia’s standard which requires Indonesian

companies recognize negative goodwill in the section after non-current liabilities,

before equity.

Negative goodwill occurs when the cost of acquisition is lower than the fair value of

identifiable net assets at the date of acquisition. The International Accounting

Standard (IAS) 22 does not allow recognition of negative goodwill as liabilities at the

time of the acquisition. Otherwise, the excess of acquirer’s interest in the net fair

value of acquiree’s identifiable assets, liabilities and contingent liabilities over cost

shall be reassessed and recognized immediately in the statement of profit or loss. This

accounting treatment is also applied in other countries such as US, UK, and Australia.

However, just like positive goodwill, Indonesian accounting standard for negative

goodwill is different from that standard. Under the PSAK No. 22 article 46, negative

goodwill should be treated as the following:

“If the cost of acquisition is lower than the fair value of identifiable assets

and liabilities at the date of transaction, then the fair value of the acquired

non-monetary assets should be eliminated in a proportional manner, until all

the residual amount is eliminated. If after all the fair value of the non-

monetary assets is eliminated, still there is residual amount that has not been

eliminated, then the remaining residual amount is considered as negative

goodwill and treated as deferred income, and be recognized as revenue

systematically over a period not less than 20 years” (IAI 2004, freely

translated by author).

4.2 Hypotheses Tested

This thesis studies the nature of goodwill with reference to its accounting treatment in

Indonesia. Analysis is referred to the “future economic benefit” nature of goodwill as

one factor to the existing treatment. The four hypotheses being tested are:

H1: There is a positive relationship between goodwill and the company’s earnings

presented in the financial statements at the same accounting periods.

H2: There is a positive relationship between goodwill and earnings achieved by

the grouped sample companies (classified by goodwill proportion to total

assets) at the same respective periods.

H3: There is a positive relationship between the amount of goodwill presented in

the financial statements and earnings achieved during the following years.

H4: There is a positive relationship between the initial goodwill amount (the

purchased amount of goodwill) and earnings achieved within a period after

the initial recognition of goodwill.

4.2.1 Relationship between Goodwill and the Company’s Earnings

The first hypothesis is intended to test the correlation between goodwill and earnings

presented in a company’s financial report at the same respective years.

The first hypothesis can be stated in the null and alternate as follows:

H0: There is no positive relationship between net goodwill and the company’s

earnings presented in the financial statements at the same accounting periods.

Statistically expressed: H0: ? = 0

where ? is the relationship between goodwill and the company’s earnings presented

in the financial statements within the same accounting periods.

H1: There is a positive relationship between net goodwill and the company’s

earnings presented in the financial statements at the same accounting periods.

Statistically expressed: H1: ? ? 0

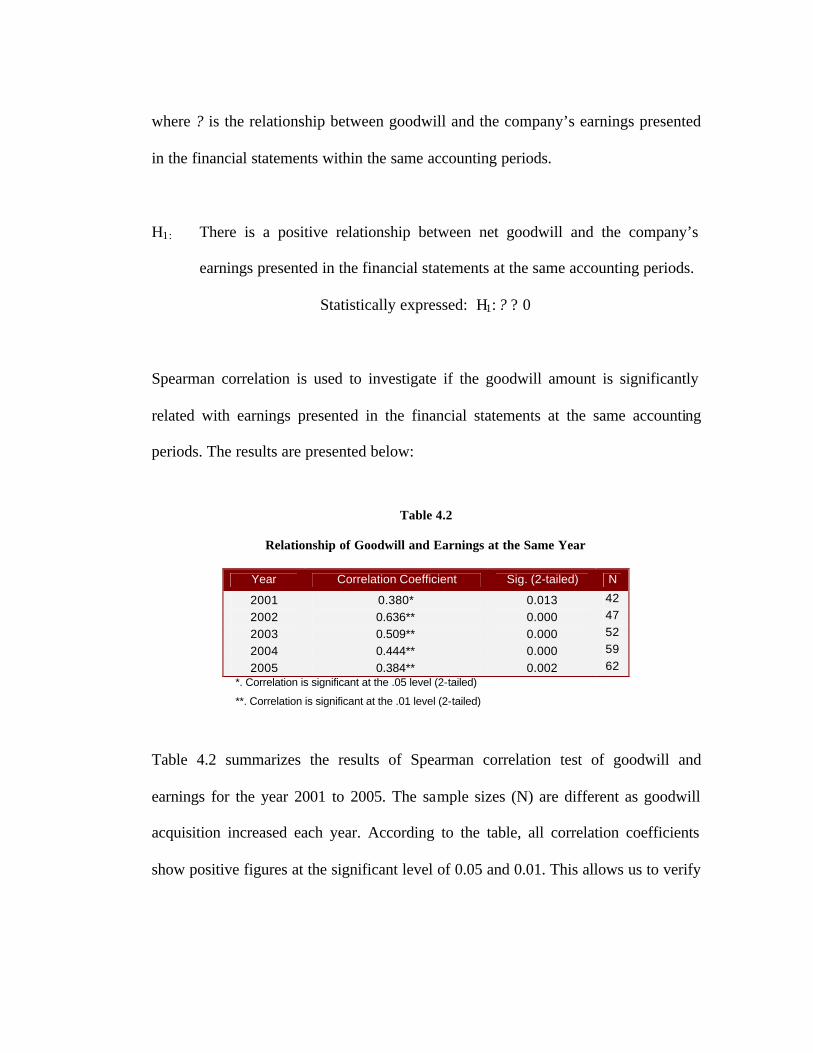

Spearman correlation is used to investigate if the goodwill amount is significantly

related with earnings presented in the financial statements at the same accounting

periods. The results are presented below:

Table 4.2

Relationship of Goodwill and Earnings at the Same Year

Year Correlation Coefficient Sig. (2-tailed) N

2001 0.380* 0.013 42

2002 0.636** 0.000 47

2003 0.509** 0.000 52

2004 0.444** 0.000 59

2005 0.384** 0.002 62 *. Correlation is significant at the .05 level (2-tailed)

**. Correlation is significant at the .01 level (2-tailed)

Table 4.2 summarizes the results of Spearman correlation test of goodwill and

earnings for the year 2001 to 2005. The sample sizes (N) are different as goodwill

acquisition increased each year. According to the table, all correlation coefficients

show positive figures at the significant level of 0.05 and 0.01. This allows us to verify

that net goodwill amount presented in the financial statements positively and

significantly related to a company’s earnings at the same respective period.

This hypothesis, therefore, answers the second research question: Is there positive

correlation between goodwill amount and earnings? These findings are similar to

Archel’s study, in which he reported the existence of strong relationship between

goodwill and profits from a sample ranges from 42 to 48 groups of companies, listed

in the Spanish Stock Exchange, for the year 1992 to 1996.

4.2.2 Does the size of goodwill have an effect on a business’s capacity to earn

higher profits?

The author categorized the sample companies by goodwill proportion to total assets

into three different groups. It is then interesting to investigate further if the goodwill

size will bring a significant difference on the result findings.

Group Net Goodwill to Total Assets

1 Less Than 1%

2 Between 1% - 5%

3 More than 5%

The advantage of categorization is to minimize the divergence of sample data. For

that reason, the second hypothesis is conducted toward the grouped sample data,

using the same idea of the first hypothesis. The author anticipates that correlation test

results will be more consistent and reliable to explain the relationship of goodwill and

earnings at the same respective periods. Moreover, the result findings may also

explain how the size of goodwill can affect a business’s capacity to earn higher

profits.

The second hypothesis can be stated in the null and alternate as follows:

H0: There is no positive relationship between net goodwill and earnings achieved

by the grouped sample companies at the same respective periods.

Statistically expressed: H0: ? = 0

where ? is the relationship between net goodwill and earnings achieved by groups of

companies (classified by goodwill proportion total assets) at the same respective

periods.

H1: There is a positive relationship between net goodwill and earnings achieved

by the grouped sample companies at the same respective periods.

Statistically expressed: H1: ? ? 0

As the sample companies are separated by groups, the sample sizes for each test

reduce. The ranges of sample sizes for Group 1 are between 21 and 37 companies.

Group 2 requires sample size of 14 to 21 companies. And Group 3, the smallest

group, only has sample size of 7 to 9 companies. As small number of the company

samples may affect the accuracy and consistency of results, two correlation test

methods are used. Both Pearson and Spearman Correlation Tests are conducted to

indicate positive correlation between net goodwill and earnings at the same respective

accounting period.

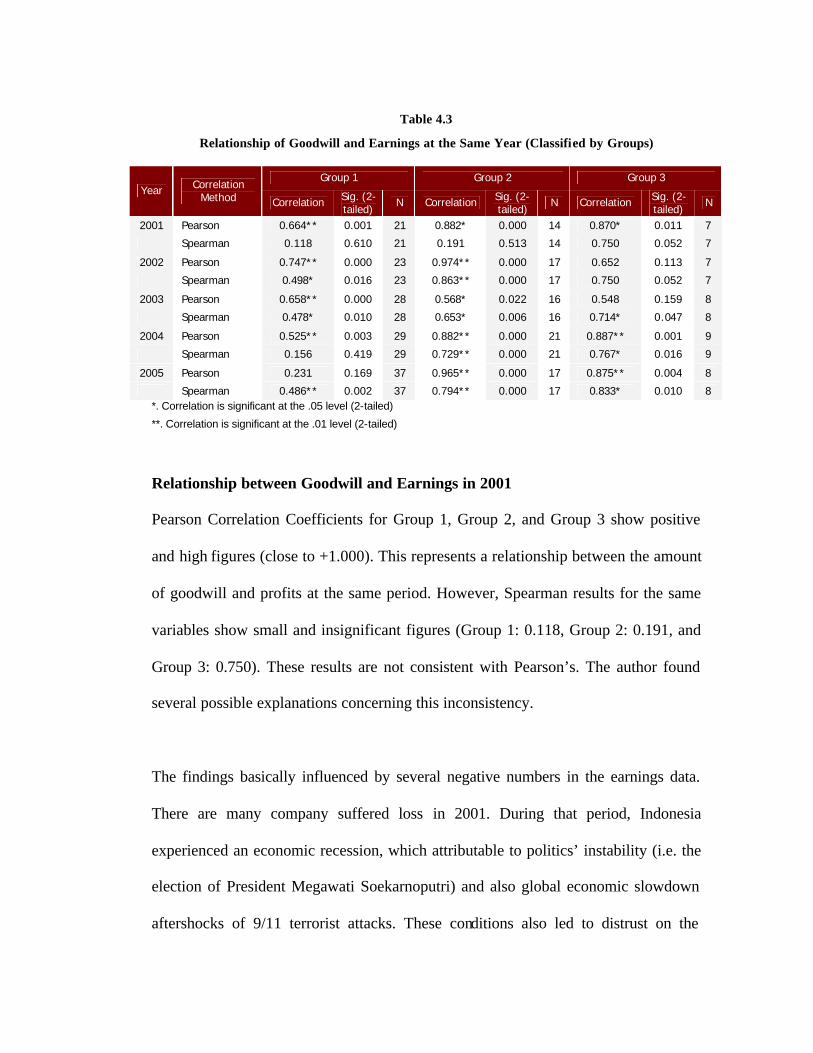

Table 4.3

Relationship of Goodwill and Earnings at the Same Year (Classified by Groups)

Group 1 Group 2 Group 3 Year Correlation

Method Correlation Sig. (2-tailed)

N Correlation Sig. (2-tailed)

N Correlation Sig. (2-tailed)

N

2001 Pearson 0.664** 0.001 21 0.882* 0.000 14 0.870* 0.011 7

Spearman 0.118 0.610 21 0.191 0.513 14 0.750 0.052 7

2002 Pearson 0.747** 0.000 23 0.974** 0.000 17 0.652 0.113 7

Spearman 0.498* 0.016 23 0.863** 0.000 17 0.750 0.052 7

2003 Pearson 0.658** 0.000 28 0.568* 0.022 16 0.548 0.159 8

Spearman 0.478* 0.010 28 0.653* 0.006 16 0.714* 0.047 8

2004 Pearson 0.525** 0.003 29 0.882** 0.000 21 0.887** 0.001 9

Spearman 0.156 0.419 29 0.729** 0.000 21 0.767* 0.016 9

2005 Pearson 0.231 0.169 37 0.965** 0.000 17 0.875** 0.004 8

Spearman 0.486** 0.002 37 0.794** 0.000 17 0.833* 0.010 8 *. Correlation is significant at the .05 level (2-tailed)

**. Correlation is significant at the .01 level (2-tailed)

Relationship between Goodwill and Earnings in 2001

Pearson Correlation Coefficients for Group 1, Group 2, and Group 3 show positive

and high figures (close to +1.000). This represents a relationship between the amount

of goodwill and profits at the same period. However, Spearman results for the same

variables show small and insignificant figures (Group 1: 0.118, Group 2: 0.191, and

Group 3: 0.750). These results are not consistent with Pearson’s. The author found

several possible explanations concerning this inconsistency.

The findings basically influenced by several negative numbers in the earnings data.

There are many company suffered loss in 2001. During that period, Indonesia

experienced an economic recession, which attributable to politics’ instability (i.e. the

election of President Megawati Soekarnoputri) and also global economic slowdown

aftershocks of 9/11 terrorist attacks. These conditions also led to distrust on the

investors side (Harian Bisnis Indonesia 3, 2001). Thus, the sample data for 2001 are

not considered as “normal data” and the correlation tests results might not be reliable

or valid.

Relationship between Goodwill and Earnings in 2002

Year 2002 was the end of economic recession and the beginning of recovery.

Although there were still some negative figures in earnings, business performances of

major companies were much improved. From the table, Pearson and Spearman

Correlation Coefficients for 2002 show positive figures, and some even show high

and significant figures (Group 1, Pearson: 0.747; Spearman: 0.498 and Group 2,

Pearson: 0.974, Spearman: 0.863). This might allow us to confirm that the amount of

goodwill and a company’s earnings are positively correlated.

Relationship between Goodwill and Earnings in 2003

Pearson and Spearman Correlation Coefficients for 2003 show positive results.

Notice that the Spearman tests generated higher correlation coefficient for groups

with higher proportion of goodwill (Group 1: 0.478, Group 2: 0.653, and Group 3:

0.714). We can possibly say that the higher the proportion of goodwill that a

company holds, the higher its contributions to earnings. After all, we agree that there

is a positive relationship between net goodwill and earnings at the same respective

periods.

3 Indonesian newspaper, in English: Indonesian Business Daily.

Relationship between Goodwill and Earnings in 2004

Pearson correlation coefficients for all groups show positive and significant figures

(Group 1: 0.525, Group 2: 0.882, and Group 3: 0.887). Spearman correlation also

yields positive and significant figures, except for Group 1 (r = 0.156). This might

suggest that, for a group of “small-goodwill” companies, the amount of goodwill does

not significantly affect earnings. However, Group 2 and Group 3 generate positive

and significant figures of 0.729 and 0.767 respectively. Again, both Pearson’s and

Spearman’s results show greater outcomes for groups with higher proportion of

goodwill. Not only the findings signify the existence of relationship between net

goodwill and earnings at the same periods, it also proves that the proportion of

goodwill that a company holds affect its contributions to the company’s earnings.

Relationship between Goodwill and Earnings in 2005

Pearson and Spearman Correlations for Group 2 and Group 3 show that goodwill and

earnings are positively and significantly related (Group 2, Pearson: 0.965; Spearman:

0.794 and Group 3, Pearson: 0.875, Spearman: 0.833). However, Spearman’s and

Pearson’s results are inconsistent for Group 1 (Pearson: 0.231 and Spearman: 0.486,

significant at the 0.01 level). This might indicate that the amount of goodwill does not

consistently contribute to company’s earnings for Group 1. Nevertheless, the

outcomes verify the existence of relationship between net goodwill and company’s

earnings at the same respective periods.

In summary, all figures presented in Table 4.3 are positive. These findings strengthen

the conclusion for hypothesis one that there is a positive relationship between net

goodwill and the company’s earnings presented in the financial statements at the

same accounting periods. Moreover, based on the 2003’s, 2004’s and 2005’s results,

the correlation coefficients are higher and more significant for groups with larger

proportion of goodwill. The findings answer the third research question: Does the size

of goodwill have an effect on a business’s capacity to earn higher profits? It is found

that the proportion of goodwill that a company holds relates to its contributions to the

company’s earnings. In other words, the size of goodwill has an effect on a business’s

capacity to earn higher profits.

4.2.3 Is Goodwill an Asset?

The third hypothesis is intended to verify the nature of goodwill as having the

essential characteristics of assets. While goodwill had clearly met the two

characteristics of assets (i.e. the occurrence of past transaction and the rights to

control the assets), the “future economic benefits” of goodwill is often debatable. The

term “future economic benefits” most likely refers to the returns that a company

achieves after an investment is made. The returns on goodwill (investment) will

appear during the periods subsequent to its recognition in the financial statements.

Hence, the third hypothesis will test net goodwill and its effect to the future benefits

of a company, in this case, earnings achieved during the following years.

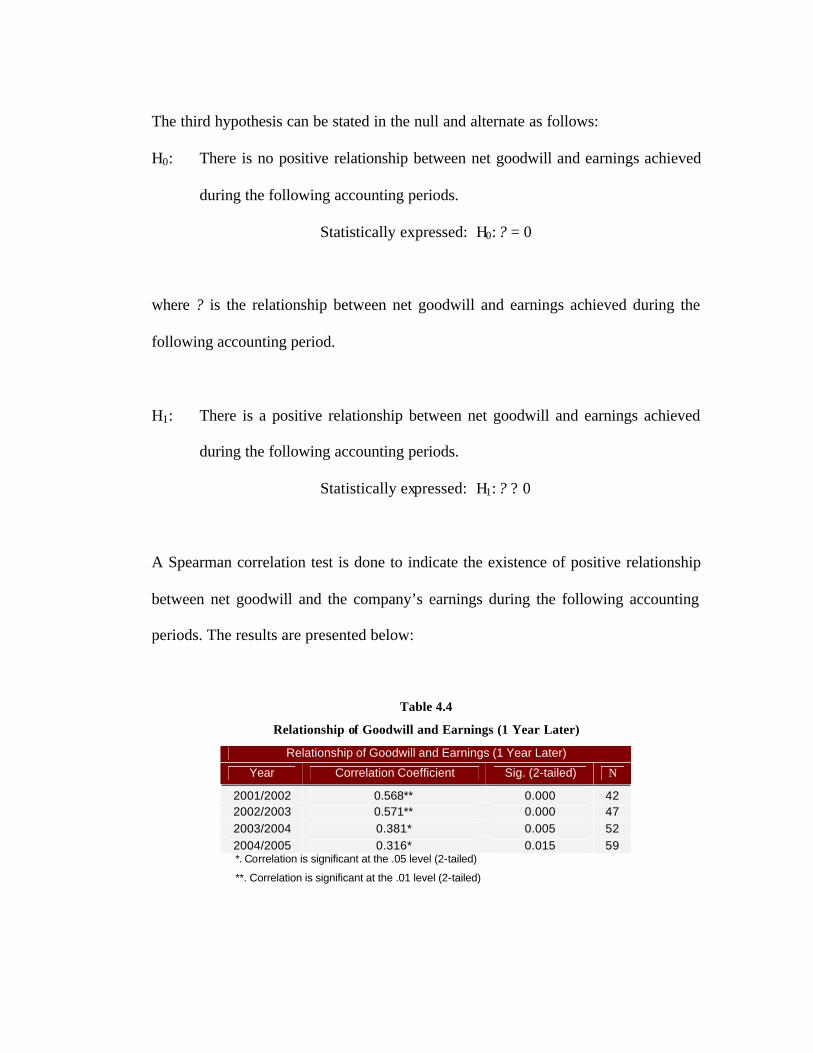

The third hypothesis can be stated in the null and alternate as follows:

H0: There is no positive relationship between net goodwill and earnings achieved

during the following accounting periods.

Statistically expressed: H0: ? = 0

where ? is the relationship between net goodwill and earnings achieved during the

following accounting period.

H1: There is a positive relationship between net goodwill and earnings achieved

during the following accounting periods.

Statistically expressed: H1: ? ? 0

A Spearman correlation test is done to indicate the existence of positive relationship

between net goodwill and the company’s earnings during the following accounting

periods. The results are presented below:

Table 4.4

Relationship of Goodwill and Earnings (1 Year Later) Relationship of Goodwill and Earnings (1 Year Later)

Year Correlation Coefficient Sig. (2-tailed) N

2001/2002 0.568** 0.000 42 2002/2003 0.571** 0.000 47 2003/2004 0.381* 0.005 52 2004/2005 0.316* 0.015 59 *. Correlation is significant at the .05 level (2-tailed)

**. Correlation is significant at the .01 level (2-tailed)

Table 4.4 summarizes the results of Spearman correlation test between net goodwill

at one specific period and earnings achieved at the next period (one year later). In this

test, we did not include the 2005’s net goodwill as the 2006’s earnings are not

provided by the time this research is conducted. All results show positive figures at

the significant level of 0.05 and 0.01. Thus, there is a positive and significant

relationship between net goodwill and earnings achieved at the following accounting

period.

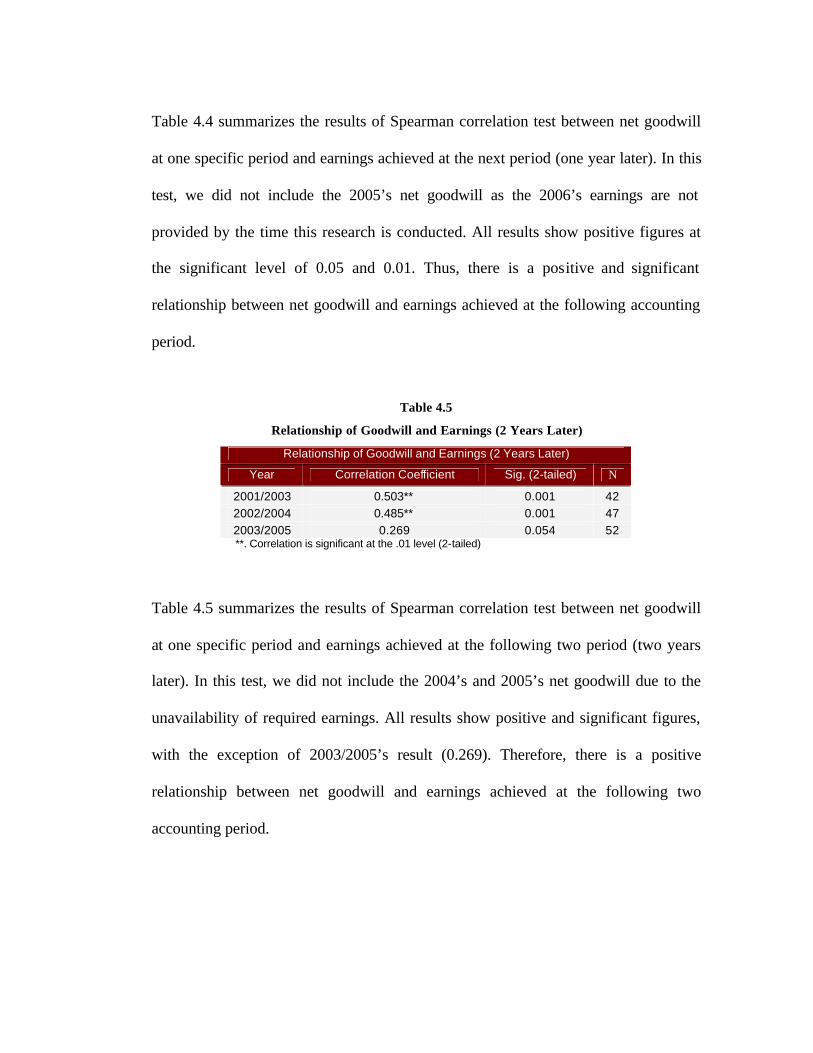

Table 4.5

Relationship of Goodwill and Earnings (2 Years Later) Relationship of Goodwill and Earnings (2 Years Later)

Year Correlation Coefficient Sig. (2-tailed) N

2001/2003 0.503** 0.001 42 2002/2004 0.485** 0.001 47 2003/2005 0.269 0.054 52 **. Correlation is significant at the .01 level (2-tailed)

Table 4.5 summarizes the results of Spearman correlation test between net goodwill

at one specific period and earnings achieved at the following two period (two years

later). In this test, we did not include the 2004’s and 2005’s net goodwill due to the

unavailability of required earnings. All results show positive and significant figures,

with the exception of 2003/2005’s result (0.269). Therefore, there is a positive

relationship between net goodwill and earnings achieved at the following two

accounting period.

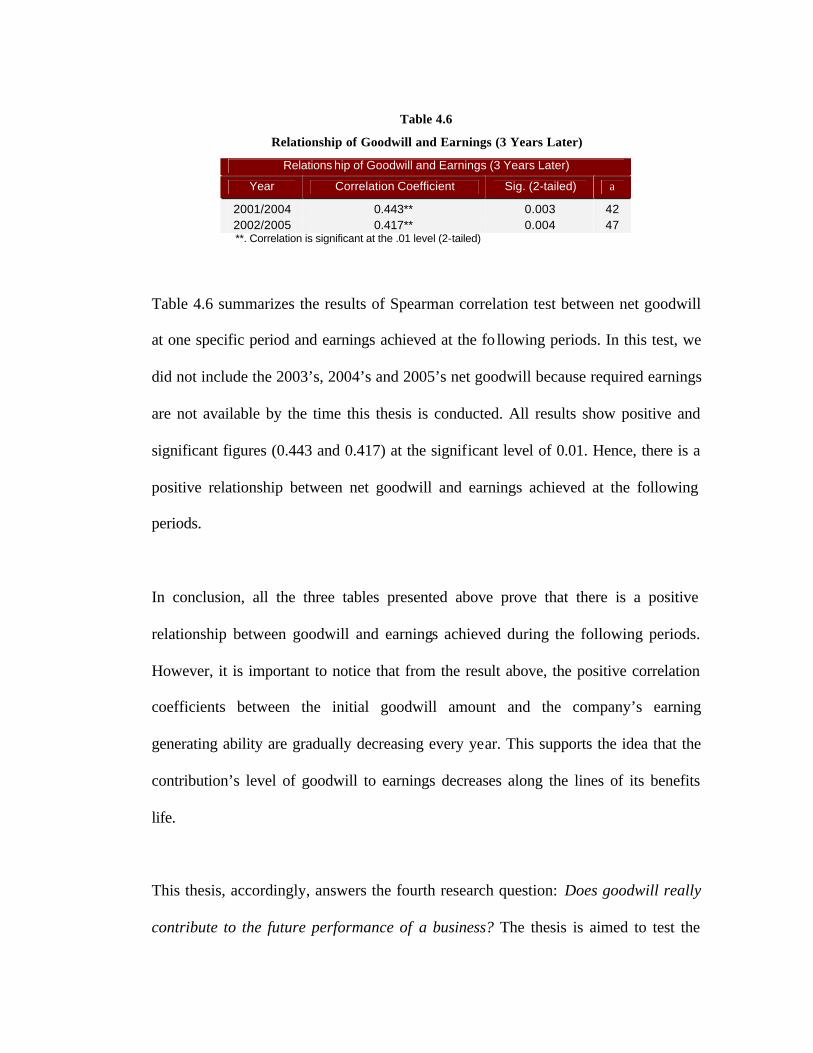

Table 4.6

Relationship of Goodwill and Earnings (3 Years Later) Relations hip of Goodwill and Earnings (3 Years Later)

Year Correlation Coefficient Sig. (2-tailed) a

2001/2004 0.443** 0.003 42 2002/2005 0.417** 0.004 47 **. Correlation is significant at the .01 level (2-tailed)

Table 4.6 summarizes the results of Spearman correlation test between net goodwill

at one specific period and earnings achieved at the fo llowing periods. In this test, we

did not include the 2003’s, 2004’s and 2005’s net goodwill because required earnings

are not available by the time this thesis is conducted. All results show positive and

significant figures (0.443 and 0.417) at the significant level of 0.01. Hence, there is a

positive relationship between net goodwill and earnings achieved at the following

periods.

In conclusion, all the three tables presented above prove that there is a positive

relationship between goodwill and earnings achieved during the following periods.

However, it is important to notice that from the result above, the positive correlation

coefficients between the initial goodwill amount and the company’s earning

generating ability are gradually decreasing every year. This supports the idea that the

contribution’s level of goodwill to earnings decreases along the lines of its benefits

life.

This thesis, accordingly, answers the fourth research question: Does goodwill really

contribute to the future performance of a business? The thesis is aimed to test the

relationship between goodwill and earnings, which may indicate that the amount of

goodwill contributes to the future performance of a company. Thus, based on the

results of the hypotheses testing, goodwill possesses future economic benefits that

contribute to the actual earnings of a company.

4.2.4 Is the company able to raise synergy in the early years of business

combinations?

Previously, the third hypotheses focuses on the amount of net goodwill and its effect

to the company’s earnings during the following periods. However, the test does not

consider the acquisition date as well as the initial amount of goodwill. Hence, we

might fail to see the information regarding the contribution of goodwill at the early

stages of its benefits life. Basically, the usefulness of an asset reaches its maximum in

the first years of its utilization. Extending Archel’s study, the author tried to analyze

the periods at which goodwill seemingly having its optimum benefits.

The fourth hypothesis is aimed to test the initial amount of goodwill and its effect to

the company’s future earnings. Using the same idea as the third hypothesis,

correlation tests are applied to the company’s earnings achieved during the periods

after the initial recognition of goodwill, in this case, the following accounting

periods. The difference is, instead of using net goodwill (goodwill after accumulated

amortization), this test will use the initial amount of goodwill at the date of

acquisition.

The fourth hypothesis can be stated in the null and alternate as follows:

H0: There is a positive relationship between the initial goodwill amount and

earnings achieved during a period after the initial recognition of goodwill.

Statistically expressed: H0: ? = 0

where ? is the relationship between the initial goodwill amount and earnings achieved

during a period after the initial recognition of goodwill.

H1: There is a positive relationship between the initial goodwill amount and

earnings achieved during a period after the initial recognition of goodwill.

Statistically expressed: H1: ? ? 0

Pearson correlation test is done to identify the existence of relationship between the

initial goodwill amount and earnings achieved after goodwill is recognized in the

financial statements. The sample sizes of each test are 20 and below, which might be

insufficient to generate accurate and consistent results. Subsequently, Spearman

correlation test is done to examine the significance and the consistency of correlations

and support Pearson test results. The results are presented below:

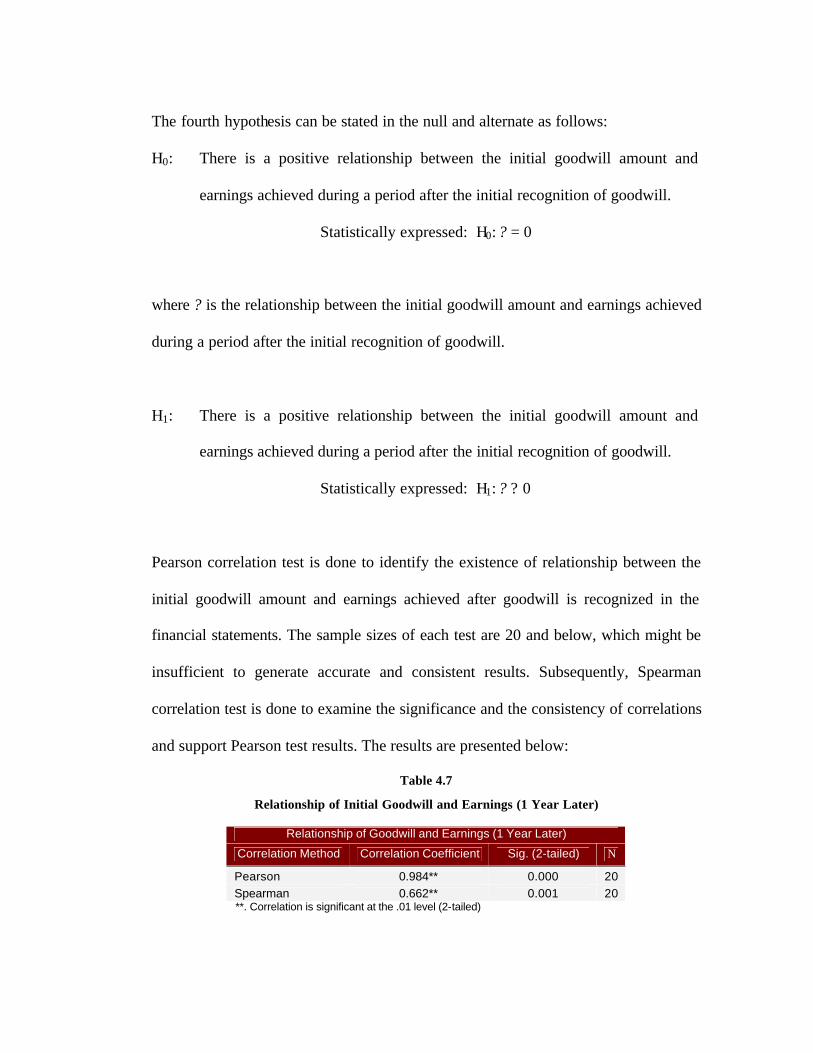

Table 4.7

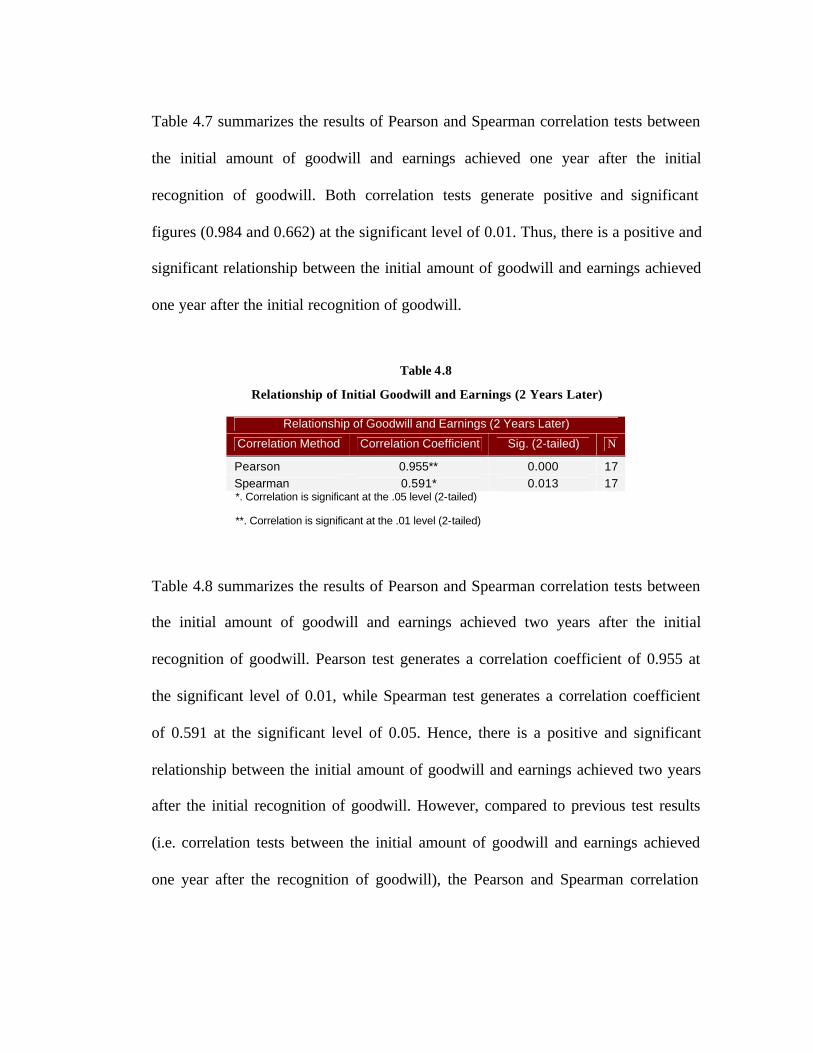

Relationship of Initial Goodwill and Earnings (1 Year Later)

Relationship of Goodwill and Earnings (1 Year Later)

Correlation Method Correlation Coefficient Sig. (2-tailed) N

Pearson 0.984** 0.000 20 Spearman 0.662** 0.001 20 **. Correlation is significant at the .01 level (2-tailed)

Table 4.7 summarizes the results of Pearson and Spearman correlation tests between

the initial amount of goodwill and earnings achieved one year after the initial

recognition of goodwill. Both correlation tests generate positive and significant

figures (0.984 and 0.662) at the significant level of 0.01. Thus, there is a positive and

significant relationship between the initial amount of goodwill and earnings achieved

one year after the initial recognition of goodwill.

Table 4.8

Relationship of Initial Goodwill and Earnings (2 Years Later)

Relationship of Goodwill and Earnings (2 Years Later)

Correlation Method Correlation Coefficient Sig. (2-tailed) N

Pearson 0.955** 0.000 17 Spearman 0.591* 0.013 17 *. Correlation is significant at the .05 level (2-tailed)

**. Correlation is significant at the .01 level (2-tailed)

Table 4.8 summarizes the results of Pearson and Spearman correlation tests between

the initial amount of goodwill and earnings achieved two years after the initial

recognition of goodwill. Pearson test generates a correlation coefficient of 0.955 at

the significant level of 0.01, while Spearman test generates a correlation coefficient

of 0.591 at the significant level of 0.05. Hence, there is a positive and significant

relationship between the initial amount of goodwill and earnings achieved two years

after the initial recognition of goodwill. However, compared to previous test results

(i.e. correlation tests between the initial amount of goodwill and earnings achieved

one year after the recognition of goodwill), the Pearson and Spearman correlation

coefficients are smaller. This signifies that the contribution level of goodwill is

greater at the first year, rather than at the second year.

Table 4.9

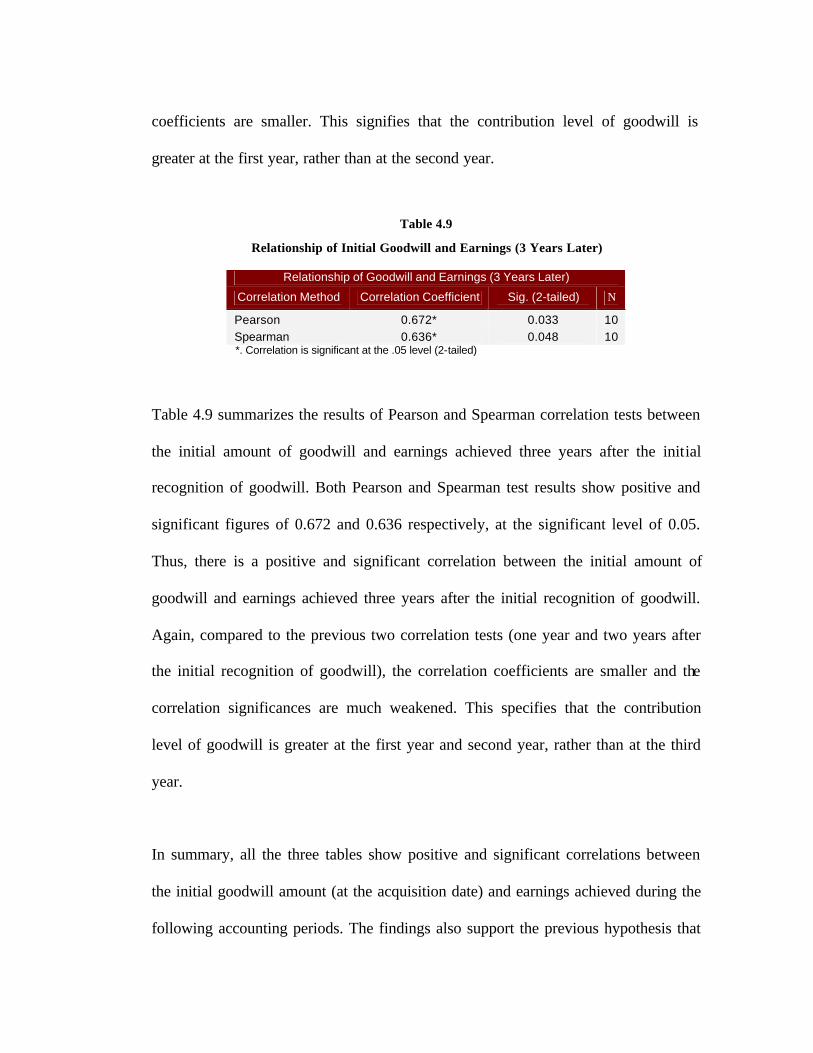

Relationship of Initial Goodwill and Earnings (3 Years Later)

Relationship of Goodwill and Earnings (3 Years Later)

Correlation Method Correlation Coefficient Sig. (2-tailed) N

Pearson 0.672* 0.033 10 Spearman 0.636* 0.048 10 *. Correlation is significant at the .05 level (2-tailed)

Table 4.9 summarizes the results of Pearson and Spearman correlation tests between

the initial amount of goodwill and earnings achieved three years after the initial

recognition of goodwill. Both Pearson and Spearman test results show positive and

significant figures of 0.672 and 0.636 respectively, at the significant level of 0.05.

Thus, there is a positive and significant correlation between the initial amount of

goodwill and earnings achieved three years after the initial recognition of goodwill.

Again, compared to the previous two correlation tests (one year and two years after

the initial recognition of goodwill), the correlation coefficients are smaller and the

correlation significances are much weakened. This specifies that the contribution

level of goodwill is greater at the first year and second year, rather than at the third

year.

In summary, all the three tables show positive and significant correlations between

the initial goodwill amount (at the acquisition date) and earnings achieved during the

following accounting periods. The findings also support the previous hypothesis that

goodwill contributes to the future benefits of a company. Furthermore, the correlation

coefficients between the initial goodwill amount and earnings are higher and also

more significant at the first years after the initial recognition of goodwill. The results

may reflect that companies are able to derive the synergy from Business

Combinations in the early years. Nonetheless, the effect of Business Combinations to

the company’s ability in generating profit is declining through times.