Chapter 34

62

Chapter 34 Exchange Rates and the Balance of Payments

-

Upload

griffith-myers -

Category

Documents

-

view

24 -

download

0

description

Chapter 34. Exchange Rates and the Balance of Payments. The price of one currency in terms of another is set by the interaction of supply and demand in international financial markets. Among the participants in these markets are governments seeking to change or maintain exchange rates. - PowerPoint PPT Presentation

Transcript of Chapter 34

Chapter 34

Exchange Rates and the Balance of Payments

Slide 34-2

Introduction

The price of one currency in terms of another is set by the interaction of supply and demand in

international financial markets.

Among the participants in these markets are governments seeking to change or maintain

exchange rates.

Slide 34-3

Learning Objectives

Distinguish between the balance of trade and the balance of payments

Identify the key accounts within the balance of payments

Outline how exchange rates are determined in the markets for foreign exchange

Slide 34-4

Learning Objectives

Discuss factors that can induce changes in equilibrium exchange rates

Understand how policymakers can go about attempting to fix exchange rates

Explain alternative approaches to limiting exchange rate variability

Slide 34-5

The Balance of Payments and International Capital Movements

Determining Foreign Exchange Rates

The Gold Standard and the International Monetary Fund

Fixed Exchange Rates

Chapter Outline

Slide 34-6

Did You Know That...

Exchange rates between currencies are a factor in determining the location of vehicle production?

The recent decline in the value of the dollar against the yen and the euro led foreign automakers to locate more vehicle assembly in the U.S.?

Slide 34-7

Balance of Trade– The value of goods and services bought and sold

in the world market

– The difference between exports and imports of goods

Balance of Payments– A summary record of a country’s economic

transactions with foreign residents and governments over a year

The Balance of Payments and International Capital Movements

Slide 34-8

Surplus (+) and Deficit (-) Items on the International Accounts

Surplus Items (+) Deficit Items (-)

Exports of merchandise Imports of merchandise

Private and government gifts from Private and governmental gifts to foreigners foreigners

Foreign use of domestically owned Use of foreign-owned transportation transportation

Foreign tourists’ expenditures in this country Tourism expenditures abroad

Foreign military spending in this country Military spending abroad

Interest and dividend receipts from foreigners Interest and dividends paid to foreigners

Sales of domestic assets to foreigners Purchases of foreign assets

Funds deposited in this country by foreigners Funds placed in foreign depository institutions

Sales of gold to foreigners Purchases of gold from foreigners

Sales of domestic currency to foreigners Purchases of foreign currency

Table 34-1

Slide 34-9

Accounting Identities

– Statements that certain numerical measurements are equivalent by accepted definition

The Balance of Payments and International Capital Movements

Slide 34-10

The Balance of Payments and International Capital Movements

When family expenditures exceed income, the family must do one of the following:

– Reduce its money holdings, or sell stocks, bonds, or other assets

– Borrow

– Receive gifts from friends or relatives

– Receive a public transfer from a government

Cannot continue indefinitely

Slide 34-11

Accounting identities

– Net lending by households must equal net borrowing by businesses and governments

Disequilibrium

– When a situation cannot continue indefinitely

The Balance of Payments and International Capital Movements

Slide 34-12

Households, businesses, and governments must reach equilibrium.

When nations trade or interact, certain identities or constraints must hold.

The Balance of Payments and International Capital Movements

Slide 34-13

Three categories of balance of payments transactions

– Current account transactions

– Capital account transactions

– Official reserve account transactions

The Balance of Payments and International Capital Movements

Slide 34-14

Current account transactions

– Merchandise trade transactions• Importing and exporting of merchandise• Balance = merchandise exports - merchandise

imports

The Balance of Payments and International Capital Movements

Slide 34-15

Current account transactions

– Service exports and imports• Invisible or intangible items

– Shipping– Insurance– Tourism– Banking– Income from investments

The Balance of Payments and International Capital Movements

Slide 34-16

Current account transactions

– Unilateral transfers• Gifts by citizens • Gifts by governments

The Balance of Payments and International Capital Movements

Slide 34-17

Example: Multinational Firms in Trade Statistics

When economic activities are conducted by multinational firms, there are different trade statistics that will be calculated depending on whether the activities are measured according to the ownership of resources or according to the location of productive activities.

Slide 34-18

Example: Multinational Firms in Trade Statistics

When the U.S. Commerce Department reports trade statistics on an ownership basis, exports and imports are adjusted to reflect purchases and sales involving foreign affiliates of U.S. firms.

Slide 34-19

Balancing the current account

– Net exports plus unilateral transfers plus net investment income exceeds zero• Current account surplus

– Net exports plus unilateral transfers plus net investment income is negative• Current account deficit

The Balance of Payments and International Capital Movements

Slide 34-20

The Balance of Payments and International Capital Movements

A current account surplus means the import of money or money equivalent which means a capital account deficit

A current account deficit must be paid by the export of money or money equivalent which means a capital account surplus

Slide 34-21

Capital account transactions

– Deals with the buying and selling of real and financial assets

The Balance of Payments and International Capital Movements

Slide 34-22

The current account and capital account must sum to zero, in the absence of interventions by finance ministries or central banks.

The Balance of Payments and International Capital Movements

Capital Account Current Account 0

Slide 34-23

Official reserve account transactions

– Foreign currencies

– Gold

– Special Drawing Rights (SDRs)• Reserve assets created by the International

Monetary Fund that countries can use to settle international payments

The Balance of Payments and International Capital Movements

Slide 34-24

Official reserve account transactions

– The reserve position in the International Monetary Fund

– Financial assets held by an official agency such as the U.S. Treasury Department

The Balance of Payments and International Capital Movements

Slide 34-25

The Balance of Payments and International Capital Movements

What affects the balance of payments?

– Relative rate of inflation

– Political stability

Slide 34-26

The Balance of Payments and International Capital Movements

What affects the balance of payments?

– Inflation among trading partners

– Political stability

Slide 34-27

Determining ForeignExchange Rates

Foreign Exchange Market

– The market for buying and selling foreign currencies

Exchange Rates

– The price of one currency in terms of another

Slide 34-28

Determining ForeignExchange Rates

Demand for and supply of foreign currency

– U.S. transactions involving imports constitute a supply of dollars and demand for some foreign currency

– The opposite is true for export transactions

Slide 34-29

Determining ForeignExchange Rates

The equilibrium foreign exchange rate

– Appreciation• An increase in the value of a currency in terms

of other currencies

– Depreciation• A decrease in the value of a currency in terms

of other currencies

Slide 34-30

Deriving the Demandfor Japanese Yen

Figure 34-2, Panels (a) and (b)

0

D

Quantity of Japanese Laptopsper Week

Panel (b)U.S. Demand Curve for Japanese Laptop Computers

100

1,500

300

1,250

500

1,000

700

750

Pric

e p

er

Un

it ($

)

Slide 34-31

Deriving the Demandfor Japanese Yen

Figure 34-2, Panels (c) and (b)

0

D

Quantity of Japanese Laptopsper Week

Panel (b)U.S. Demand Curve for Japanese Laptop Computers

100

1,500

300

1,250

500

1,000

700

750

Pric

e p

er

Un

it ($

)

Slide 34-32

Deriving the Demandfor Japanese Yen

Figure 34-2, Panels (d) and (e)

0

D1

Quantity of YenDemanded per Week (millions)

Panel (e)U.S. Derived Demand for Yen

10

.0150

30

.0125

50

.0100

70

.0075

Pric

e p

er

Fra

nc

($)

Slide 34-33

Determining ForeignExchange Rates

Supply of Japanese Yen– Price of U.S. microprocessor = $200

– Exchange rate = $0.01 for 1 yen

– 200,000 yen ($200@$0.01/yen) = 1 microprocessor

– Exchange rate = $0.0125

– 16,000 Yen ($200@ $0.0125/Yen) = 1 microprocessor

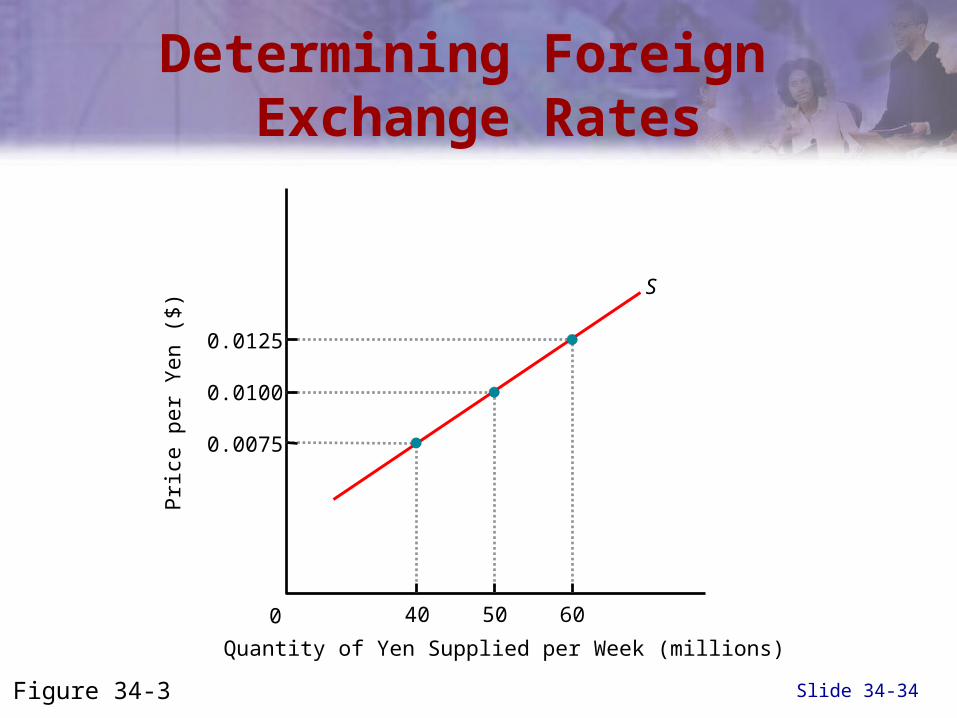

Slide 34-34

Determining Foreign Exchange Rates

Figure 34-3

0

S

Quantity of Yen Supplied per Week (millions)

Pric

e pe

r Y

en (

$)

40

0.0075

50

0.0100

60

0.0125

Slide 34-35

Total Demand for and Supply of Japanese Yen

Figure 34-4

0

Trillions of Yen per Year

S

2

0.0125

D

3

0.0100E

Pric

e pe

r Y

en($

)

Slide 34-36Figure 34-5

A Shift in the Demand Schedule

0

S

D1

D2

Trillions of Yen per Year

4

0.0120E 2

3

0.0100E 1

Pri

ce p

er

Ye

n (

$)

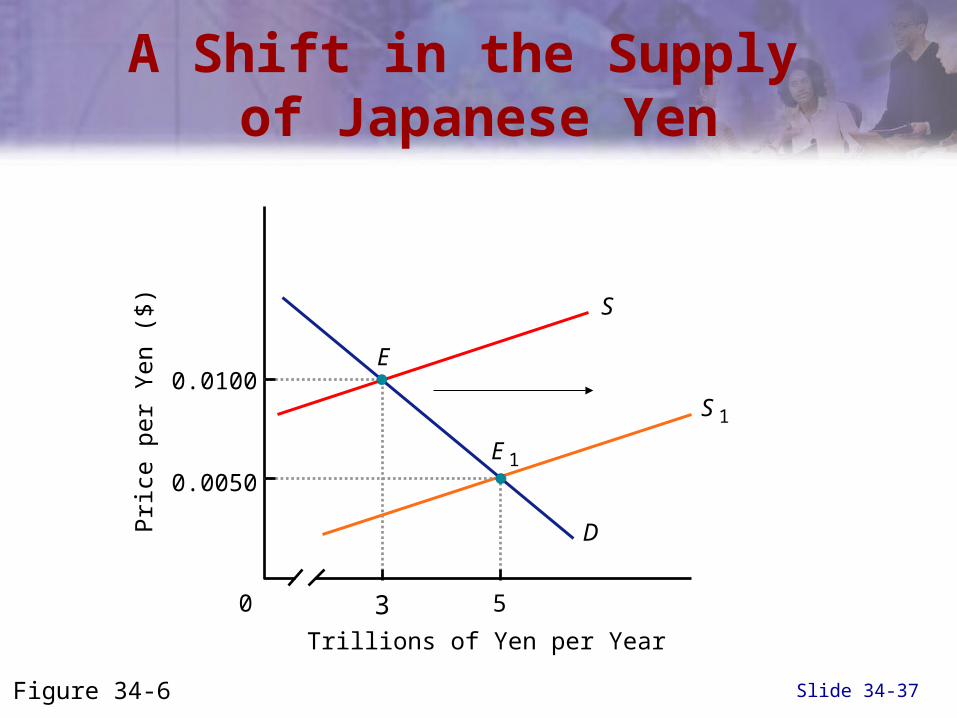

Slide 34-37Figure 34-6

A Shift in the Supply of Japanese Yen

0

Trillions of Yen per Year

S 1

S

D

3

0.0100E

E 1

5

0.0050Pric

e pe

r Y

en (

$)

Slide 34-38

International Example: South Africa’s Currency Appreciation

Gold and platinum are key South African exports.

The increased demand for these commodities has also increased the demand for South African rand.

As interest rates in South Africa became relatively higher, the demand for South African financial assets also increased.

Slide 34-39

International Example: South Africa’s Currency Appreciation

The result of these changes has been an appreciation of the rand.

The dollar price of the rand has doubled since the end of 2001.

Slide 34-40

Determining ForeignExchange Rates

Market determinants of exchange rates

– Changes in real interest rates

– Changes in productivity

– Changes in product preferences

– Perceptions of economic stability

Slide 34-41

The Gold Standard and the International Monetary Fund

Gold Standard

– An international monetary system in which nations fix their exchange rates in terms of gold

– All currencies are fixed in terms of all others, and any balance of payments deficits or surpluses can be made up by shipments of gold

Slide 34-42

The Gold Standard and the International Monetary Fund

Gold standard

– A balance of payments deficit• More gold flowed out than flowed in• Equivalent to an restrictive monetary policy

– A balance of payments surplus• More gold flowed in than out• Equivalent to an expansionary monetary policy

Slide 34-43

The Gold Standard and the International Monetary Fund

Problems with the gold standard

– A nation gives up control of its monetary policy

– New gold discoveries often caused inflation

Slide 34-44

The Gold Standard and the International Monetary Fund

Bretton Woods and the International Monetary Fund

– 1944—representatives of capitalist countries met in Bretton Woods, New Hampshire• Created a new international payment system to replace

the gold standard

– Members could change the par value once by 10 percent and after that par value changes needed IMF approval

Slide 34-45

The Gold Standard and the International Monetary Fund

End of the old IMF

– On August 15, 1971, President Richard Nixon suspended the convertibility of the dollar into gold.

– On December 18, 1971, the United States devalued the dollar relative to the currencies of 14 major industrial nations.

Slide 34-46

Current Foreign Exchange Rate Arrangements

Figure 34-7

Slide 34-47

Fixed versus Floating Exchange Rates

To maintain a fixed exchange rate, the central bank of a country can buy and sell currencies.

It must use its own foreign exchange reserves to engage in these financial market transactions.

Slide 34-48

A Fixed Exchange Rate

Figure 34-8

The Bank of Malaysia buysringgit with dollars shifting the demand for ringgit to the right

• The supply of ringgit shifts to the right as Thai residents demand more U.S. goods

• The value of the ringgit will fall

Slide 34-49

International Example:Central Banks’ Currencies of Choice

A central bank allocates foreign exchange reserves based on its perception of which currencies will be needed most frequently to alter the demand for its own currency.

The U.S. dollar is the currency most commonly held in foreign exchange reserves; but the euro, the Japanese yen, and the British pound also comprise a measurable portion of these accounts.

Slide 34-50

Fixed Exchange Rates

Pros and cons of fixed exchange rates

– Pros• Limiting foreign exchange risk

– The possibility that changes in the value of a nation’s currency will result in variations in market value of assets

Slide 34-51

Fixed Exchange Rates

Pros and cons of fixed exchange rates– Cons

• A country’s residents can avoid foreign exchange risk by hedging– A financial strategy that reduces the chance

of suffering losses arising from foreign exchange risk

• A nation’s output and employment can fall in the short run if demand for its products decreases and its labor is relatively immobile

Slide 34-52

The Dirty Float and Managed Exchange Rates

Dirty Float

– A system between flexible and fixed exchange rates in which central banks occasionally enter foreign exchange markets to influence rates

Slide 34-53

Managed Exchange Rates

What do you think?

– Is it possible to “manage” foreign exchange rates?

One study concludes that neither the Fed nor the central banks of the other G7 can successfully influence exchange rates in the long run.

Slide 34-54

Managed Exchange Rates

Crawling Pegs

– An automatically adjusting target for the value of a nation’s currency

– The exchange rate gradually adjusts the upward or downward by a country’s central bank buying or selling its currency as needed to keep it consistent with long-run forces.

Slide 34-55

Managed Exchange Rates

Target Zones

– Upper and lower limits or bands for values of an exchange rate are established and maintained by central banks

Slide 34-56

Issues and Applications: Japan’s Finance Ministry Learns a New Currency Trick

As the value of the dollar has declined against the Japanese yen in recent years, American consumers must pay more for Japanese-made goods.

In response, the Japanese government began buying dollars on the foreign exchange market.

Of late, the government has been using private banks to implement the foreign exchange transactions needed to arrest the yen appreciation.

Slide 34-57

Summary Discussion of Learning Objectives

The balance of trade versus the balance of payments

– Balance of trade • Exports of goods-imports

– Balance of payments• A system of account for all transactions

between a nation’s residents and the rest of the world

Slide 34-58

Summary Discussion of Learning Objectives

The key accounts within the balance of payments

– Current account

– Capital account

– Official reserve transactions account

Slide 34-59

Summary Discussion of Learning Objectives

Exchange rate determination in the market for foreign exchange

– The equilibrium exchange rate is the exchange rate at which the quantity of a country’s currency is equal to the quantity supplied

Slide 34-60

Summary Discussion of Learning Objectives

Factors that can induce changes in equilibrium exchange rates

– Changes in desired imports or exports

– Changes in real interest rates

– Changes in relative productivity

– Tastes and preferences of consumers

– Perceptions of stability

Slide 34-61

Summary Discussion of Learning Objectives

How policymakers can attempt to keep exchange rates fixed– A country’s central bank increases the demand for its

country’s currency if the exchange rate begins to fall

Alternative approaches to limiting exchange rate variability– Dirty floats

– Crawling pegs

– Target zones

End of Chapter 34Exchange Rates and the Balance of Payments