Chapter 3 Solutions

136

Chapter 3: Adjusting and Closing Entries Discussion Questions: Key Points 1. Revenue is recognized when it is earned using the accrual basis of accounting and when cash is received using the cash basis of accounting a. July 19 b. June 28 2. The matching principle requires companies to match expenses with the revenues they helped create. Proper matching is required in order to produce accurate financial information. 3. The time period that revenue is recognized is important because accurate financial statements cannot be produced unless the revenues are recorded in the proper period. 4. A deferral occurs when there has been a prepayment. Deferrals would only be associated with the accrual basis of accounting. A deferral would be recorded when the company is paid in advance for services to be rendered later or when a company pays for expenses in advance that are going to be used up later (e.g., supplies, insurance). 5. Adjusting entries are prepared in order to bring all of the account balances up to date. 6. Assets and expenses are both increased with debits. Assets eventually become expenses over time and use. 7. The determining factor is the benefit period with which the expenditure is associated. If the benefit period is in the future or extending from the present into one or more future accounting periods, an asset is debited. If the expenditure is associated with an item that will be used up in the present accounting period, an expense is debited. It is important to note that dollar amount is not necessarily the determining factor. a. Expense Waybright Kemp Financial Accounting 1e 133

description

Solutions

Transcript of Chapter 3 Solutions

Chapter 3: Adjusting and Closing Entries

Discussion Questions: Key Points

1. Revenue is recognized when it is earned using the accrual basis of accounting and when cash is received using the cash basis of accounting

a. July 19b. June 28

2. The matching principle requires companies to match expenses with the revenues they helped create. Proper matching is required in order to produce accurate financial information.

3. The time period that revenue is recognized is important because accurate financial statements cannot be produced unless the revenues are recorded in the proper period.

4. A deferral occurs when there has been a prepayment. Deferrals would only be associated with the accrual basis of accounting. A deferral would be recorded when the company is paid in advance for services to be rendered later or when a company pays for expenses in advance that are going to be used up later (e.g., supplies, insurance).

5. Adjusting entries are prepared in order to bring all of the account balances up to date. 6. Assets and expenses are both increased with debits. Assets eventually become expenses

over time and use.7. The determining factor is the benefit period with which the expenditure is associated. If

the benefit period is in the future or extending from the present into one or more future accounting periods, an asset is debited. If the expenditure is associated with an item that will be used up in the present accounting period, an expense is debited. It is important to note that dollar amount is not necessarily the determining factor.

a. Expenseb. Asset

8. When a company is paid in advance for services to be delivered later, a deferred revenue journal entry in which cash is debited and unearned revenue is credited will be recorded. The deferred revenue account would need to be adjusted for the amount of the prepayment that has been earned during the period.

9. Accumulated depreciation is a contra-asset account. It is reported on the balance sheet along with the asset account that it modifies.

10. The closing process has two objectives: 1) to transfer the revenue, expense and dividends account balances into retained earnings, and 2) to get those accounts ready for the next accounting period by starting them out at zero. Retained earnings is the only account that is involved but not closed.

Waybright Kemp Financial Accounting 1e 133

Short Exercises

(5-10 min.) S 3-1

1. b

2. c

3. d

4. a

(5-10 min.) S 3-2

1. d

2. c

3. b

4. f

5. a

6. e

7. g

134 Solutions Manual

(5-10 min.) S 3-3

Type of Adjusting Entry Related Income Statement Account

a. Accrued expense Interest expense

b. Deferred revenue Service revenue

c. Accrued revenue Service revenue

d. Deferred expense Supplies expense

e. Deferred expense Depreciation expense

(5-10 min.) S 3-4

Journal

DATE ACCOUNTS

POST

REF. Dr. Cr.

June 30Rent expense ($4,500/6months)

750

Prepaid rent 750

Record rent expense for June.

Prepaid rent Rent expenseBal. 4,500 June 30 750 June 30 750Bal. 3,750

Waybright Kemp Financial Accounting 1e 135

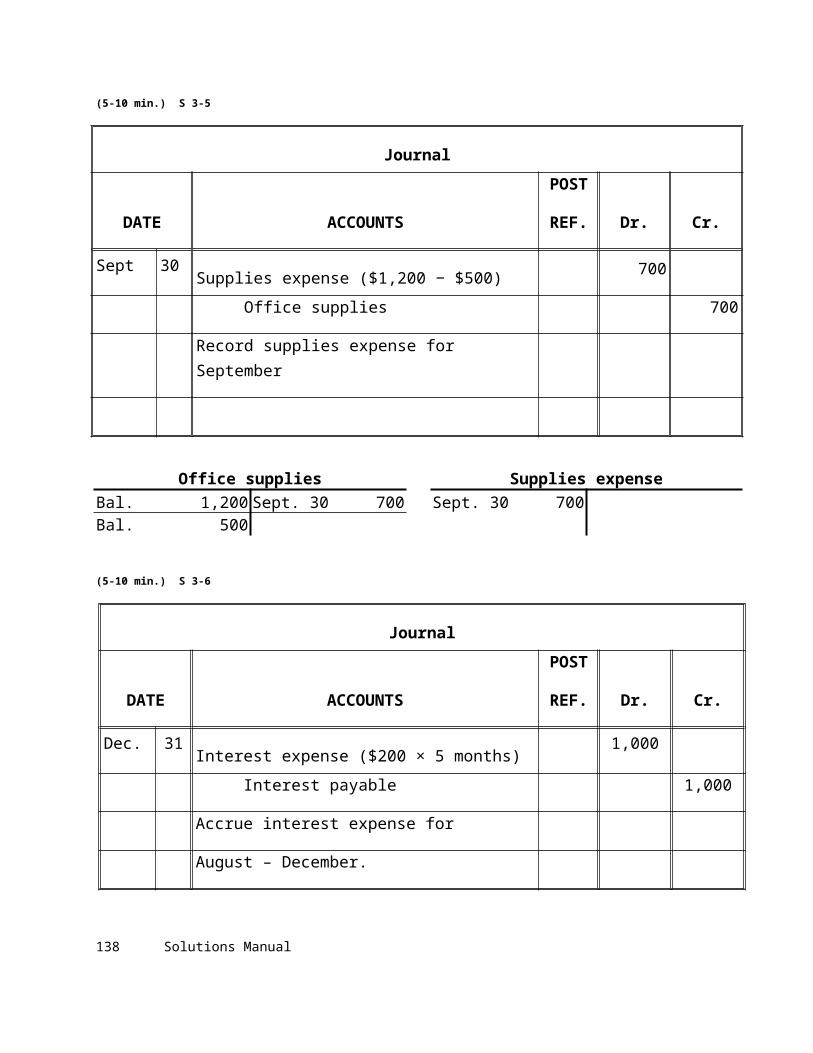

(5-10 min.) S 3-5

Journal

DATE ACCOUNTS

POST

REF. Dr. Cr.

Sept 30Supplies expense ($1,200 − $500)

700

Office supplies 700

Record supplies expense for September

Office supplies Supplies expenseBal. 1,200 Sept. 30 700 Sept. 30 700Bal. 500

(5-10 min.) S 3-6

Journal

DATE ACCOUNTS

POST

REF. Dr. Cr.

Dec. 31Interest expense ($200 × 5 months)

1,000

Interest payable 1,000

Accrue interest expense for

August – December.

Interest payableInterest expense

Dec. 31 1,000 Dec. 31 1,000

136 Solutions Manual

(5-10 min.) S 3-7

Journal

DATE ACCOUNTS

POST.

REF. Dr. Cr.

Dec. 31Unearned subscription revenue

($2,400/12× 9 months)1,800

Subscription revenue 1,800

Record subscription revenue

Earned for April – December.

Unearned subscription revenue Subscription revenue

Dec. 31 1,800 Apr 1 2,400 Dec. 31 1,800

Bal. 600

Waybright Kemp Financial Accounting 1e 137

(5-10 min.) S 3-8

Journal

DATE ACCOUNTS

POST

REF. Dr. Cr.

1. Dec. 31Accounts receivable 1,500

Service revenue 1,500

Accrue service revenue.

2. Salary expense 2,300

Salary payable 2,300

Accrue salary.

3. Interest expense 375

Interest payable 375

Accrue interest.

(5-10 min.) S 3-9

You would record $1,350 of service revenue at the end of September. Under the accrual basis of accounting, revenues are recorded when earned regardless of when cash is received. Therefore, both the $1,200 you have received as well as the $150 that is still owed to you would be recorded as service revenue.

138 Solutions Manual

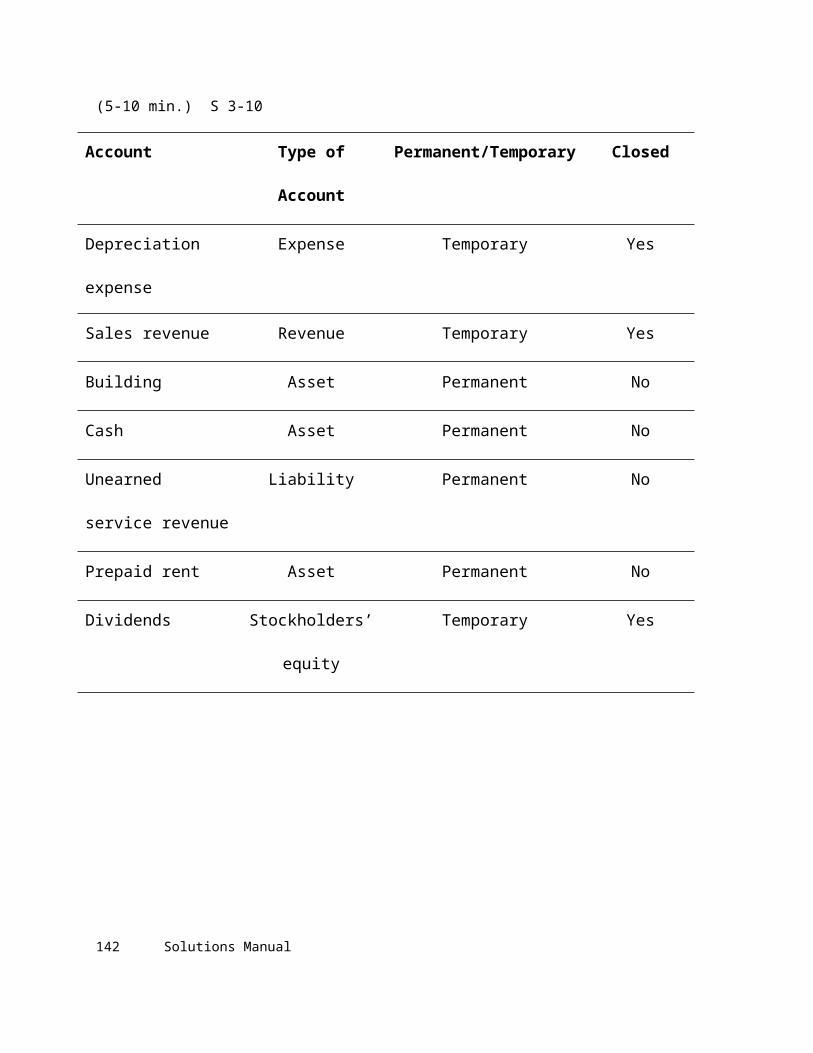

(5-10 min.) S 3-10

Account Type of Account Permanent/Temporary Closed

Depreciation expense Expense Temporary Yes

Sales revenue Revenue Temporary Yes

Building Asset Permanent No

Cash Asset Permanent No

Unearned service

revenue

Liability Permanent No

Prepaid rent Asset Permanent No

Dividends Stockholders’

equity

Temporary Yes

Waybright Kemp Financial Accounting 1e 139

(10-15 min.) S 3-11

Req 1

Net income = $700 ($1,200 service revenue - $500 total expenses)

Req 2

Change in Retained earnings = $200 ($700 net income - $500 dividends)

Req 3

Journal

DATE ACCOUNTS

POST

REF. Dr. Cr.

Dec. 31Service revenue

1,200

Retained earnings 1,200

Close revenue accounts

Retained earnings 500

Building rent expense 200

Salary expense 300

Close expense accounts

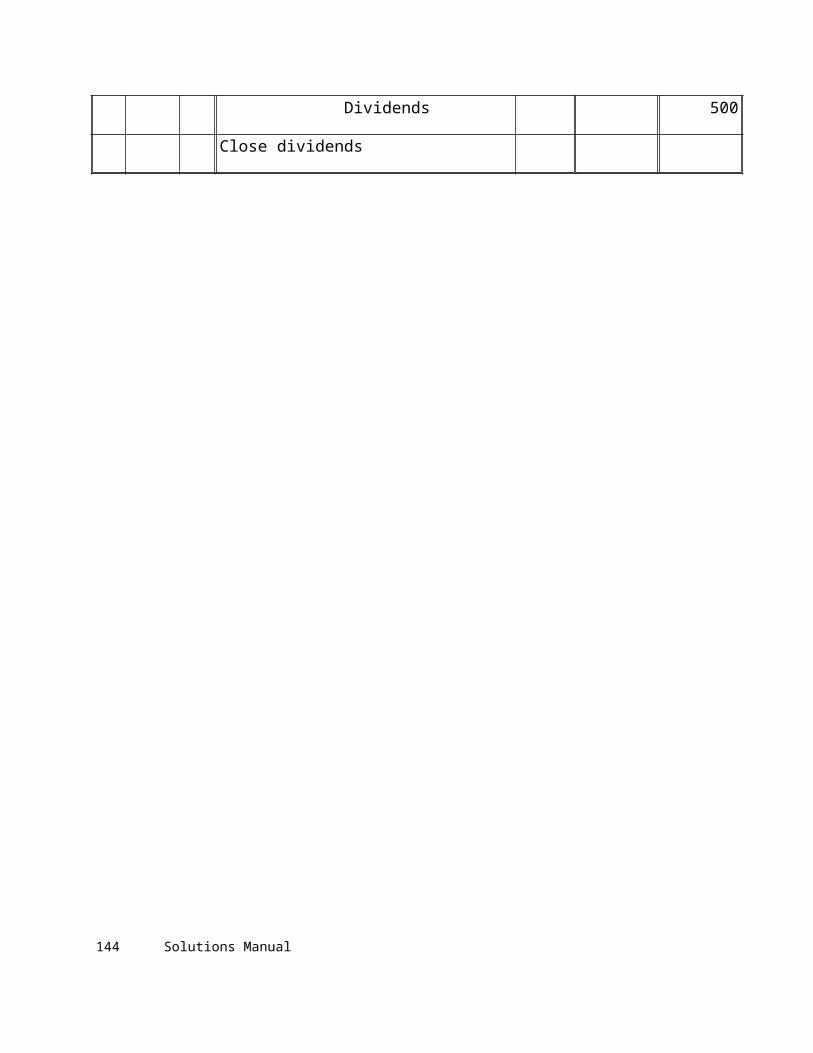

Retained earnings 500

Dividends 500

Close dividends

140 Solutions Manual

(5-10 min.) S 3-12

Type of Entry (ADJ

or CL)

AccountsPost.Ref. Dr. Cr.

ADJ Salary expense 400 Salary payable 400

CL Service revenue 900 Retained earnings 900

CL Retained earnings 1,500 Dividends 1,500

ADJ Unearned revenue 800 Service revenue 800

(5-10 min.) S 3-13

Simmons Realty, Inc.Post-Closing Trial Balance October 31, 2010

ACCOUNT DEBIT CREDITCashAccounts receivablePrepaid insurancePrepaid rentBuildingAccounts payableNotes payableCommon StockRetained earningsTotal

$1,8502,4501,300

9751,800

________$8,375

3002,0005,0001,075

$8,375

Waybright Kemp Financial Accounting 1e 141

Exercises

(10-15 min.) E 3-14A

Req 1

The accounts used include the assets Cash and Accounts Receivable, the liability Unearned Service Revenue, and the revenue Service Revenue.

Req 2

Journal

DATE ACCOUNTS

POST

REF. Dr. Cr.

Cash175

Unearned service revenue 175

Collect revenue in advance.

Accounts receivable 340

Service revenue 340

Accrue service revenue.

Cash 150

Service revenue 150

Collect cash for services performed

142 Solutions Manual

(5-10 min.) E 3-15A

Missing amounts are in italics. A B C D

Beginning prepaid insurance$ 300 $ 600 $ 700 $ 400

Payments for Prepaid

insurance during the year 1,200 $900 1,300 1,500

Total amount to account for 1,500 1,500 2,000 1,900

Ending Prepaid insurance 400 500 800 1,100

Insurance expense $ 1,100 $ 1,000 $ 1,200 $ 800

Journal

DATE ACCOUNTS

POST

REF. Dr. Cr.

a.Insurance expense

1,100

Prepaid insurance 1,100

Record insurance expense.

Waybright Kemp Financial Accounting 1e 143

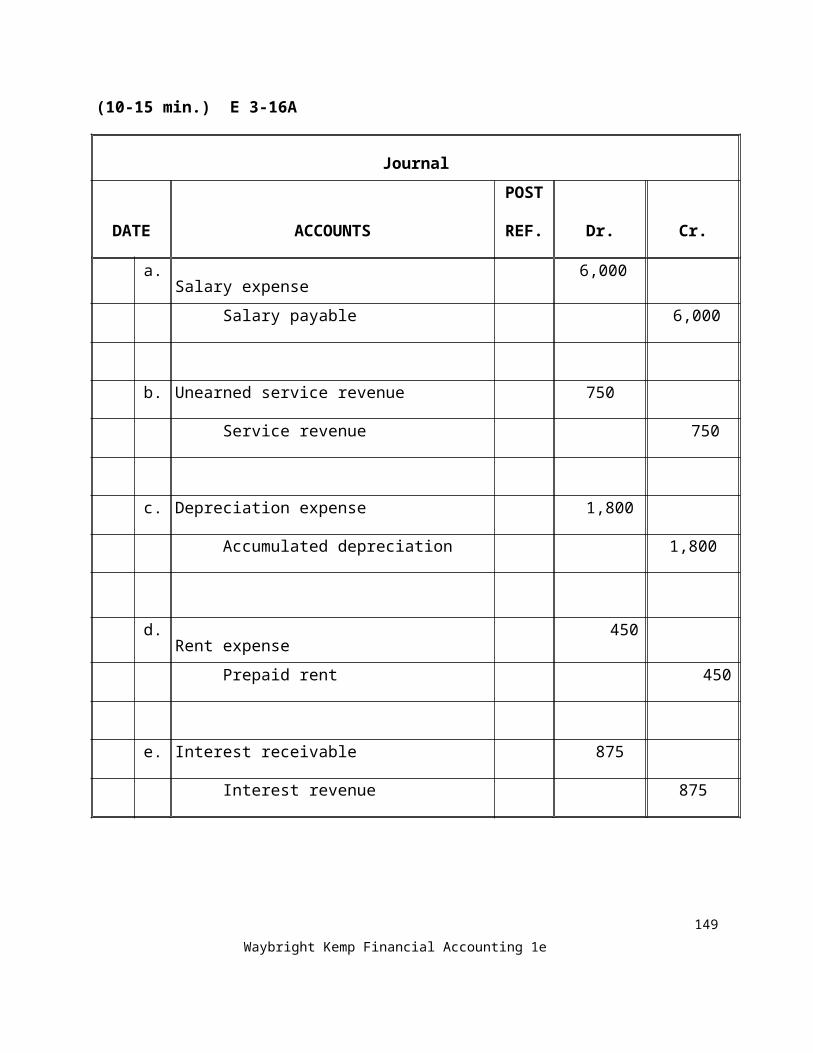

(10-15 min.) E 3-16A

Journal

DATE ACCOUNTS

POST

REF. Dr. Cr.

a.Salary expense

6,000

Salary payable 6,000

b. Unearned service revenue 750

Service revenue 750

c. Depreciation expense 1,800

Accumulated depreciation 1,800

d.Rent expense

450

Prepaid rent 450

e. Interest receivable 875

Interest revenue 875

144 Solutions Manual

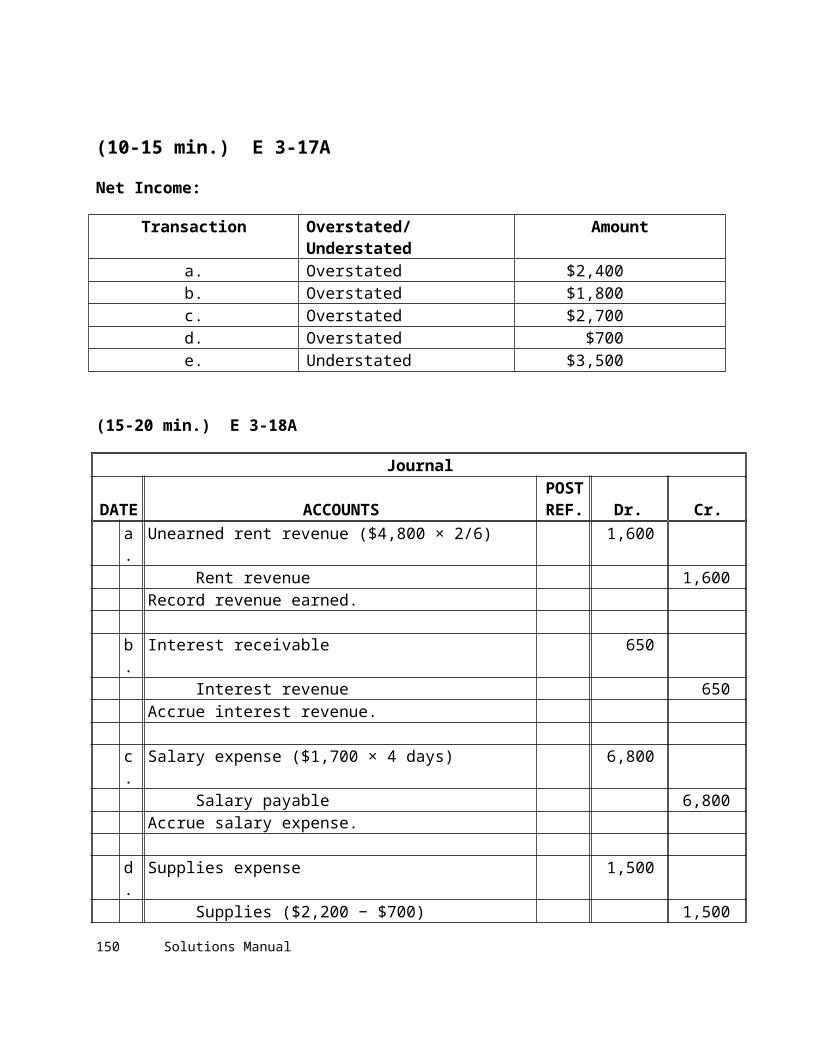

(10-15 min.) E 3-17A

Net Income:

Transaction Overstated/Understated Amounta. Overstated $2,400b. Overstated $1,800c. Overstated $2,700d. Overstated $700e. Understated $3,500

(15-20 min.) E 3-18A

Journal

DATE ACCOUNTSPOSTREF. Dr. Cr.

a. Unearned rent revenue ($4,800 × 2/6) 1,600Rent revenue 1,600

Record revenue earned.

b. Interest receivable 650Interest revenue 650

Accrue interest revenue.

c. Salary expense ($1,700 × 4 days) 6,800Salary payable 6,800

Accrue salary expense.

d. Supplies expense 1,500Supplies ($2,200 − $700) 1,500

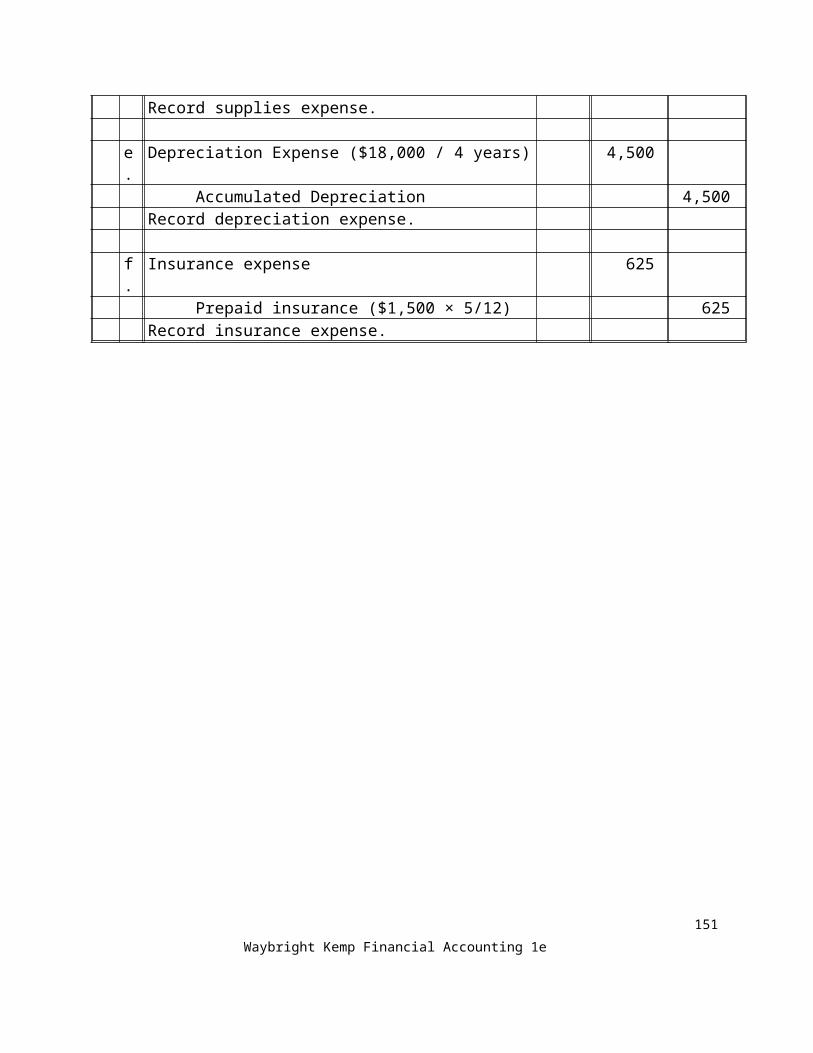

Record supplies expense.

e. Depreciation Expense ($18,000 / 4 years) 4,500Accumulated Depreciation 4,500

Record depreciation expense.

f. Insurance expense 625Prepaid insurance ($1,500 × 5/12) 625

Record insurance expense.

Waybright Kemp Financial Accounting 1e 145

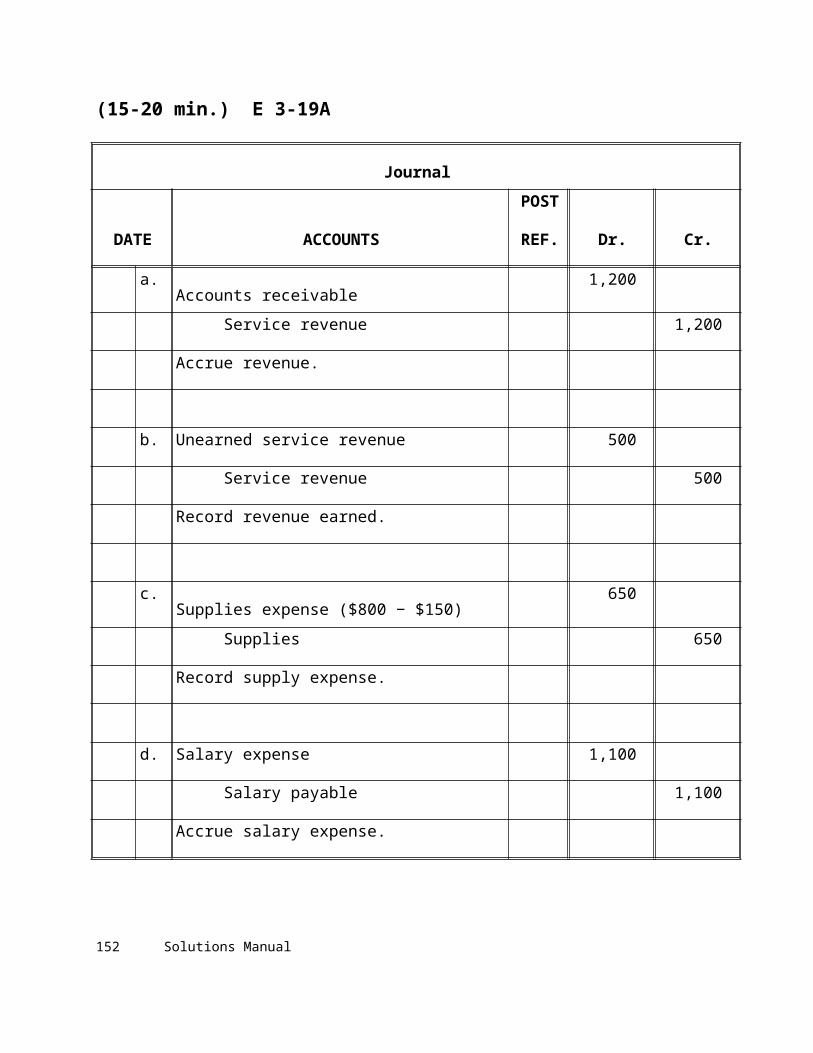

(15-20 min.) E 3-19A

Journal

DATE ACCOUNTS

POST

REF. Dr. Cr.

a.Accounts receivable

1,200

Service revenue 1,200

Accrue revenue.

b. Unearned service revenue 500

Service revenue 500

Record revenue earned.

c.Supplies expense ($800 − $150)

650

Supplies 650

Record supply expense.

d. Salary expense 1,100

Salary payable 1,100

Accrue salary expense.

146 Solutions Manual

(continued) E 3-19A

Accounts receivable SuppliesBal. 1,500 Bal. 800 (c) 650(a) 1,200 Bal. 150Bal. 2,700

Salary payable Unearned service revenue(d) 1,100 (b) 500 Bal. 900Bal. 1,100 Bal. 400

Service revenue Salary expenseBal. 3,900 Bal. 1,700(a) 1,200 (d) 1,100(b) 500 Bal. 2,800Bal. 5,600

Supplies expense(c) 650Bal. 650

Waybright Kemp Financial Accounting 1e 147

(15-20 min.) E 3-20A

Req. 1

Accounts receivable Supplies21,000 2,800 (a) 1,200

(e) 1,500 Bal. 1,600Bal 22,500

Accumulated depreciation, equipment Accumulated depreciation, building

5,600 28,000 (b) 1,400 (c) 2,000

Bal 7,000 Bal 30,000

Salary expense Supplies expense14,000 (a) 1,200

(d) 2,900 Bal 1,200

Bal 16,900

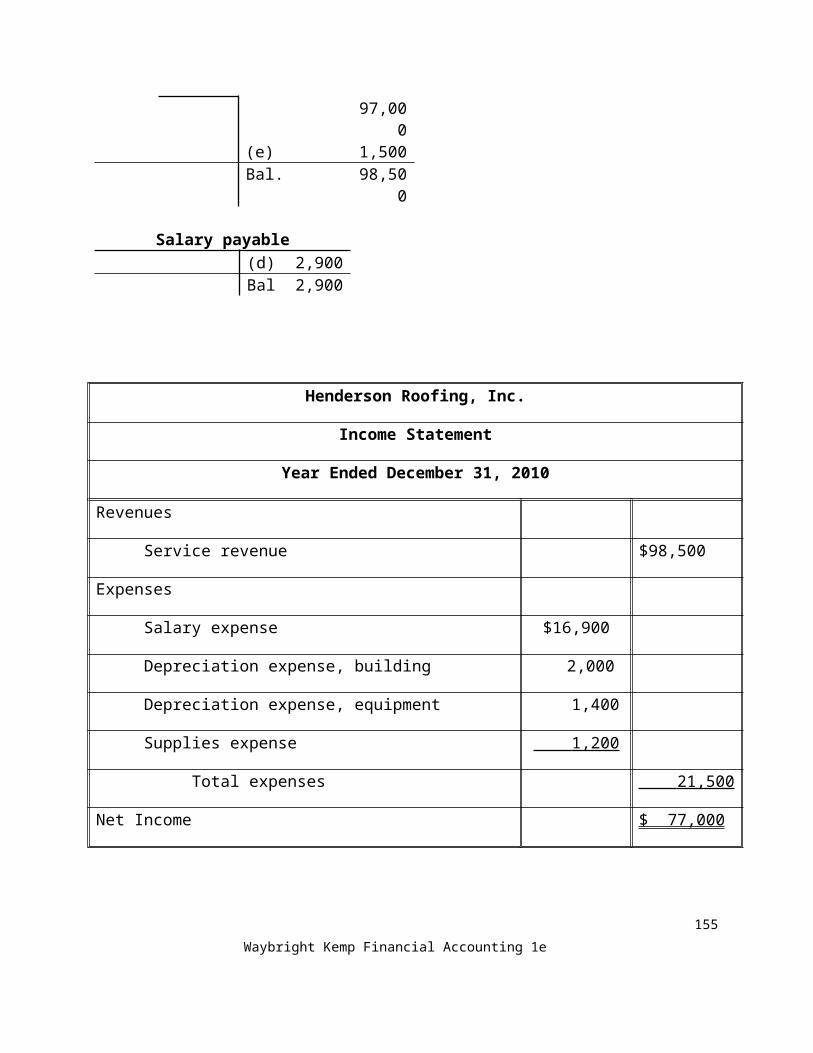

Depreciation expense, equipment Depreciation expense, building(b) 1,400 (c) 2,000 Bal 1,400 Bal 2,000

Service revenue 97,000

(e) 1,500Bal. 98,500

Salary payable (d) 2,900

Bal 2,900

148 Solutions Manual

Henderson Roofing, Inc.

Income Statement

Year Ended December 31, 2010

Revenues

Service revenue $98,500

Expenses

Salary expense $16,900

Depreciation expense, building 2,000

Depreciation expense, equipment 1,400

Supplies expense 1,200

Total expenses 21,500

Net Income $ 77,000

Req. 2

Operations were successful, as shown by the $77,000 of net income the business earned during

the year. The reason is revenues were greater than expenses.

Waybright Kemp Financial Accounting 1e 149

(10-15 min.) E 3-21A

Req. 1

Sigma Security, Inc.Statement of Retained EarningsYear Ended December 31, 2010

Retained earnings, January 1, 2010 $ 32,000Less: Net loss (11,000)Subtotal 21,000Less: Dividends ($800 × 12 months) (9,600)Retained earnings, December 31, 2010 $ 11,400

Req. 2

Retained earnings had a net decrease of $20,600 for the year (End $11,400 – Beg $32,000). This

resulted from the current net loss ($11,000) and dividends paid ($9,600).

(10-15 min.) E 3-22A

SuppliesBal. 2,800Purchase of supplies 8,700 Supplies expense 9,800Bal. 1,700

Salary payableBal. 2,800

Cash payment 52,300 Salary expense 53,200Bal. 3,700

Unearned service revenueBal. 18,000

Service revenue 108,100 Cash receipts 106,400Bal. 16,300

150 Solutions Manual

(15-20 min.) E 3-23A

Country Cookin Catering, Inc.Income Statement

Month Ended March 31, 2010Revenue: Service revenueExpenses: Salary expense Rent expense Depreciation expense, equipment Supplies expense Total ExpensesNet Income

$3,6001,200

600300

$18,600

5,700$12,900

Country Cookin Catering, Inc.Statement of Retained EarningsMonth Ended March 31, 2010

Retained earnings, March 1, 2010Add: Net income for the MonthSubtotalLess: DividendsRetained earnings, March 31, 2010

$5,80012,90018,700 800

$17,900

Waybright Kemp Financial Accounting 1e 151

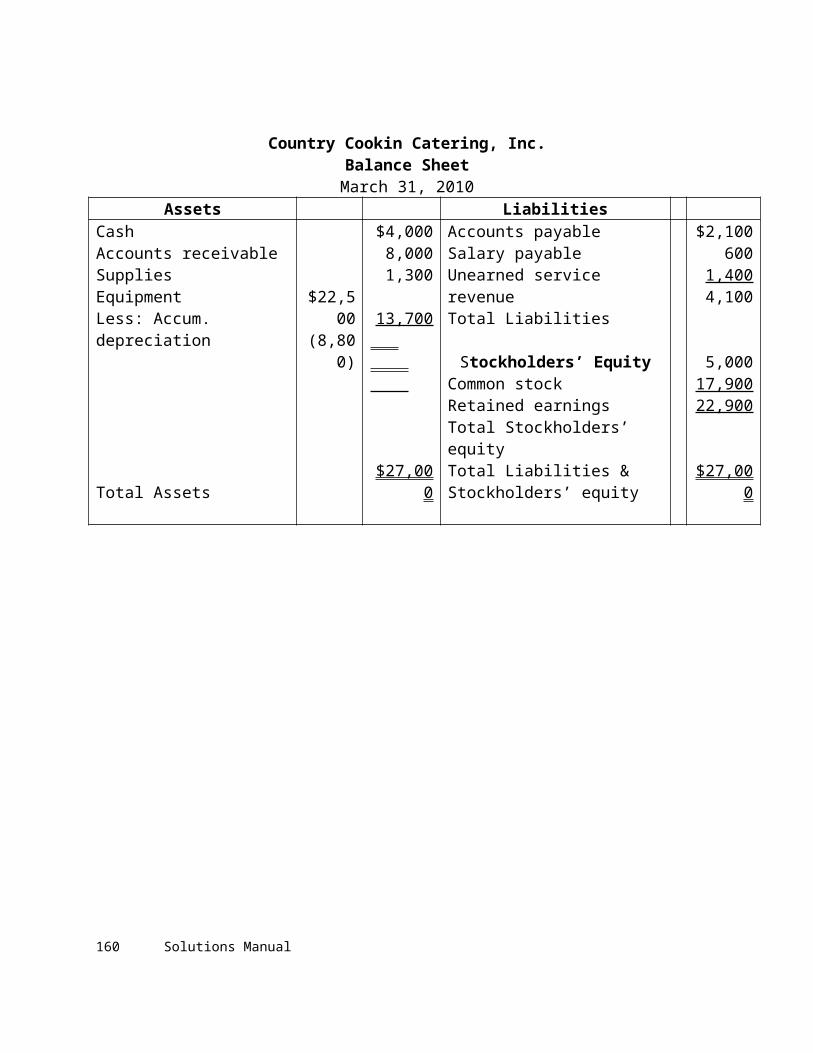

Country Cookin Catering, Inc.Balance SheetMarch 31, 2010

Assets LiabilitiesCashAccounts receivableSuppliesEquipmentLess: Accum. depreciation

Total Assets

$22,500(8,800)

$4,0008,0001,300

13,700

$27,000

Accounts payableSalary payableUnearned service revenueTotal Liabilities

Stockholders’ EquityCommon stockRetained earningsTotal Stockholders’ equity Total Liabilities & Stockholders’ equity

$2,100600

1,4004,100

5,00017,90022,900

$27,000

152 Solutions Manual

(10-15 min.) E 3-24A

Journal

DATE ACCOUNTS

POST

REF. Dr. Cr.

Apr 30Service revenue

127,000

Interest revenue 800

Retained earnings 127,800

Close revenue accounts

Retained earnings 35,800

Salary expense 18,500

Depreciation expense 8,200

Building rent expense 5,100

Interest expense 2,300

Supplies expense 1,700

Close expense accounts

Retained earnings 18,000

Dividends 18,000

Close dividends

A to Z Electrical, Inc.’s ending retained earnings is $80,500 ($6,500 + $127,800 - $35,800 - $18,000).

Waybright Kemp Financial Accounting 1e 153

(10-15 min.) E 3-25A

Kurlz Salon, Inc.Statement of Retained EarningsYear Ended December 31, 2010

Retained earnings, January 1, 2010Add: Net income for the MonthSubtotalLess: DividendsRetained earnings, December 31, 2010

$188,000139,000327,000 76,000 $251,000

(10-15 min.) E 3-26A

Cunningham Photography, Inc.Post-Closing Trial Balance

December 31, 2010ACCOUNT DEBIT CREDITCashAccounts receivableSuppliesEquipmentAccumulated depreciation, equipmentAccounts payableSalary payableUnearned service revenueCommon stockRetained earningsTotal

$9,45033,1001,900

68,000

. $112,450

$19,70011,4502,5005,600

30,00043,200

$112,450

154 Solutions Manual

(10-15 min.) E 3-27A

Journal

DATE ACCOUNTS

POST

REF. Dr. Cr.

Dec. 31Service revenues

73,000

Retained earnings 73,000

Close revenue accounts

Retained earnings 52,300

Salary expense 31,000

Rent expense 18,600

Depreciation expense, equipment 1,600

Depreciation expense, furniture 400

Supplies expense 700

Close expense accounts

Retained earnings 14,000

Dividends 14,000

Close dividends

Waybright Kemp Financial Accounting 1e 155

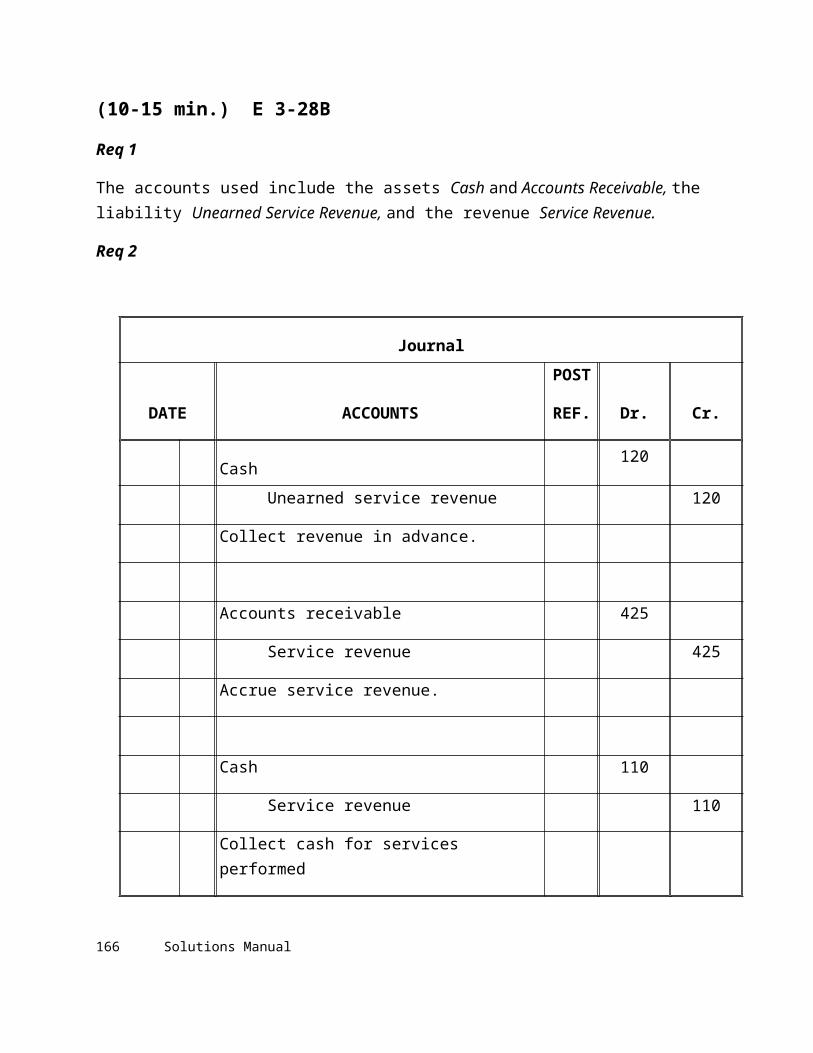

(10-15 min.) E 3-28B

Req 1

The accounts used include the assets Cash and Accounts Receivable, the liability Unearned Service Revenue, and the revenue Service Revenue.

Req 2

Journal

DATE ACCOUNTS

POST

REF. Dr. Cr.

Cash120

Unearned service revenue 120

Collect revenue in advance.

Accounts receivable 425

Service revenue 425

Accrue service revenue.

Cash 110

Service revenue 110

Collect cash for services performed

156 Solutions Manual

(5-10 min.) E 3-29B

Missing amounts are in italics. A B C D

Beginning prepaid insurance$ 800 1,100 $ 1,600 $ 300

Payments for Prepaid

insurance during the year 1,500 $600 1,600 2,400

Total amount to account for 2,300 1,700 3,200 2,700

Ending Prepaid insurance 700 1,200 600 1,300

Insurance expense $ 1,600 $ 500 $ 2,600 $ 1,400

Journal

DATE ACCOUNTS

POST

REF. Dr. Cr.

a.Insurance expense

1,600

Prepaid insurance 1,600

Record insurance expense.

Waybright Kemp Financial Accounting 1e 157

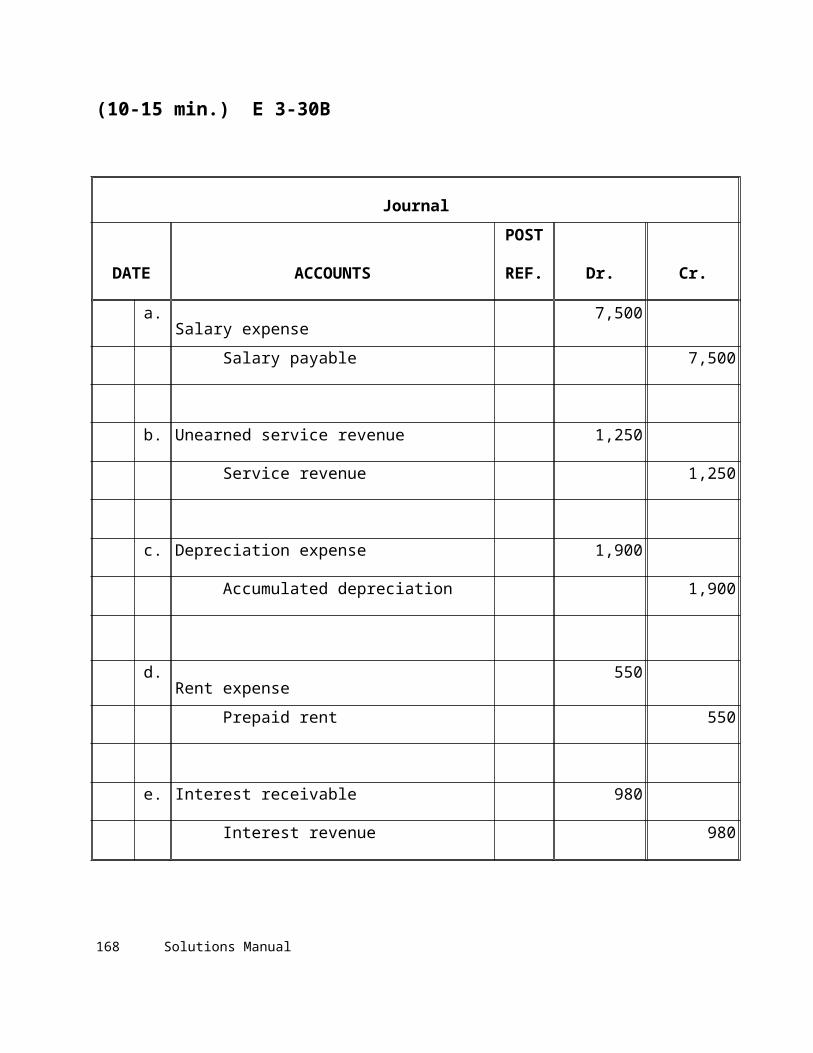

(10-15 min.) E 3-30B

Journal

DATE ACCOUNTS

POST

REF. Dr. Cr.

a.Salary expense

7,500

Salary payable 7,500

b. Unearned service revenue 1,250

Service revenue 1,250

c. Depreciation expense 1,900

Accumulated depreciation 1,900

d.Rent expense

550

Prepaid rent 550

e. Interest receivable 980

Interest revenue 980

158 Solutions Manual

(10-15 min.) E 3-31B

Net Income:

Transaction Overstated/Understated Amounta. Overstated $2,500b. Overstated $1,000c. Overstated $3,100d. Overstated $800e. Understated $4,500

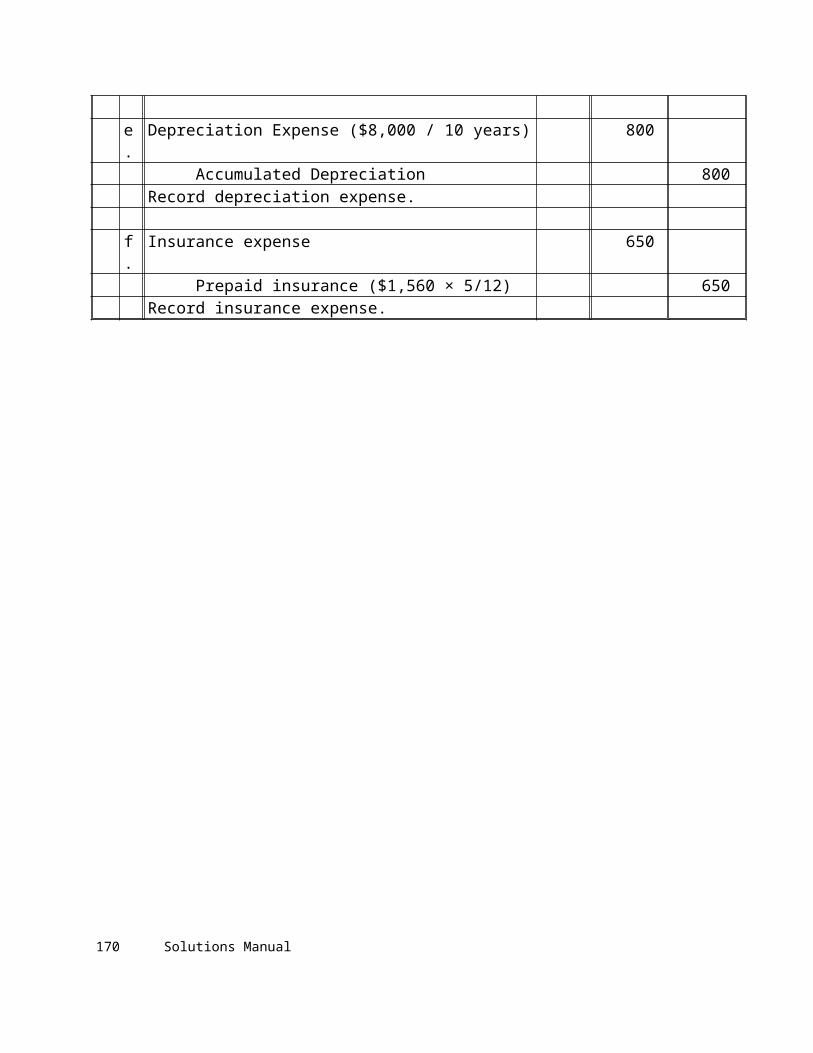

(15-20 min.) E 3-32B

Journal

DATE ACCOUNTSPOSTREF. Dr. Cr.

a. Unearned rent revenue ($3,000 × 2/6) 1,000Rent revenue 1,000

Record revenue earned.

b. Interest receivable 520Interest revenue 520

Accrue interest revenue.

c. Salary expense ($2,900 × 2 days) 5,800Salary payable 5,800

Accrue salary expense.

d. Supplies expense 1,200Supplies ($1,400 − $200) 1,200

Record supplies expense.

e. Depreciation Expense ($8,000 / 10 years) 800Accumulated Depreciation 800

Record depreciation expense.

f. Insurance expense 650Prepaid insurance ($1,560 × 5/12) 650

Record insurance expense.

Waybright Kemp Financial Accounting 1e 159

(15-20 min.) E 3-33B

Journal

DATE ACCOUNTS

POST

REF. Dr. Cr.

a.Accounts receivable

2,200

Service revenue 2,200

Accrue revenue.

b. Unearned service sevenue 300

Service revenue 300

Record revenue earned.

c.Supplies expense ($1,100 − $150)

950

Supplies 950

Record supply expense.

d. Salary expense 700

Salary payable 700

Accrue salary expense.

160 Solutions Manual

(continued) E 3-33B

Accounts receivable SuppliesBal. 1,900 Bal. 1,100 (c) 950(a) 2,200 Bal. 150Bal. 4,100

Salary payable Unearned service revenue(d) 700 (b) 300 Bal. 1,300Bal. 700 Bal. 1,000

Service revenue Salary expenseBal. 5,300 Bal. 3,100(a) 2,200 (d) 700(b) 300 Bal. 3,800Bal. 7,800

Supplies expense(c) 950Bal. 950

Waybright Kemp Financial Accounting 1e 161

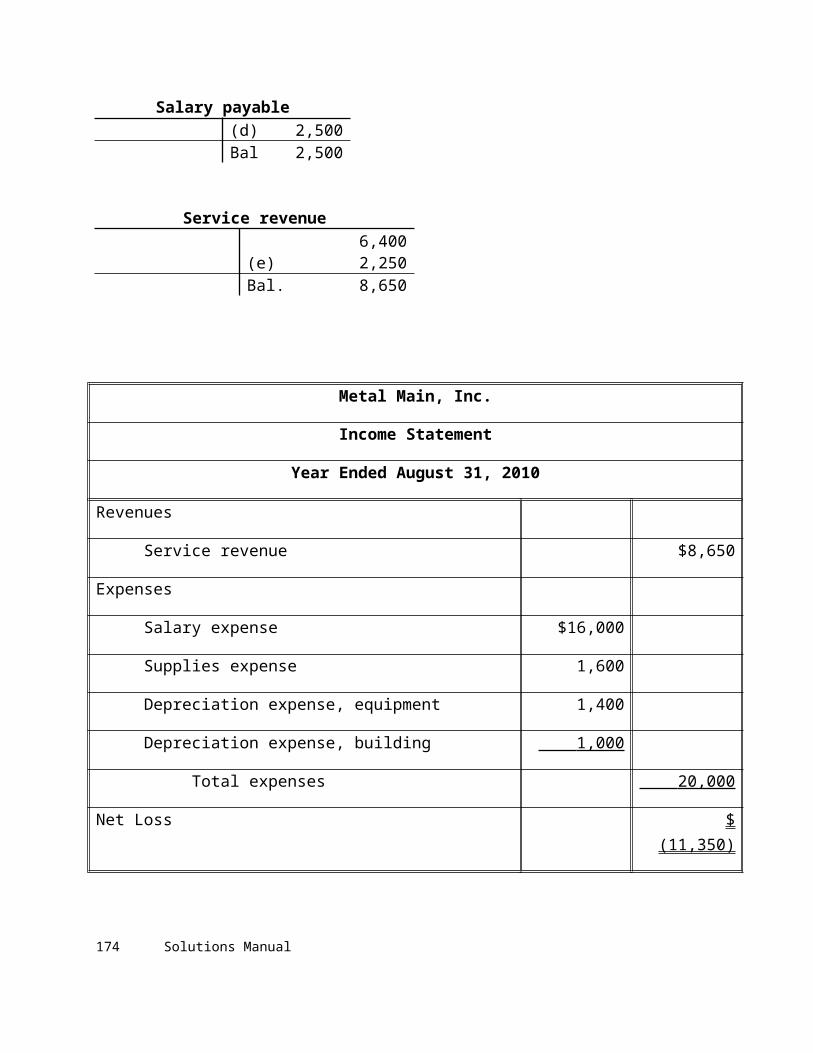

(15-20 min.) E 3-34B

Req. 1

Accounts receivable Supplies19,200 2,200 (a) 1,600

(e) 2,250 Bal. 600Bal 21,450

Accumulated depreciation, equipment Accumulated depreciation, building

4,200 46,000 (b) 1,400 (c) 1,000

Bal 5,600 Bal 47,000

Depreciation expense, equipment Depreciation expense, building(b) 1,400 (c) 1,000 Bal 1,400 Bal 1,000

Salary expense Supplies expense13,500 (a) 1,600

(d) 2,500 Bal 1,600

Bal 16,000

Salary payable (d) 2,500

Bal 2,500

Service revenue 6,400

(e) 2,250Bal. 8,650

162 Solutions Manual

Metal Main, Inc.

Income Statement

Year Ended August 31, 2010

Revenues

Service revenue $8,650

Expenses

Salary expense $16,000

Supplies expense 1,600

Depreciation expense, equipment 1,400

Depreciation expense, building 1,000

Total expenses 20,000

Net Loss $ (11,350)

Req. 2

Operations were not successful from the standpoint that the business incurred a net loss of

$11,350 during the year. The reason is expenses were greater than revenues.

Waybright Kemp Financial Accounting 1e 163

(10-15 min.) E 3-35B

Req. 1

Zeta Safety, Inc.Statement of Retained EarningsYear Ended December 31, 2010

Retained earnings, January 1, 2010 $ 34,000Less: Net loss (5,000)Subtotal 29,000Less: Dividends ($550 × 12 months) (6,600)Retained earnings, December 31, 2010 $ 22,400

Req. 2

Retained earnings had a net decrease of $11,600 for the year (End $22,400 – Beg $34,000). This

resulted from the current net loss ($5,000) and dividends paid ($6,600).

(10-15 min.) E 3-36B

SuppliesBal. 1,700Purchase of supplies 9,000 Supplies expense 9,500Bal. 1,200

Salary payableBal. 4,000

Cash payment 55,500 Salary expense 56,000Bal. 4,500

Unearned service revenueBal. 17,000

Service revenue 59,900 Cash receipts 58,000Bal. 15,100

164 Solutions Manual

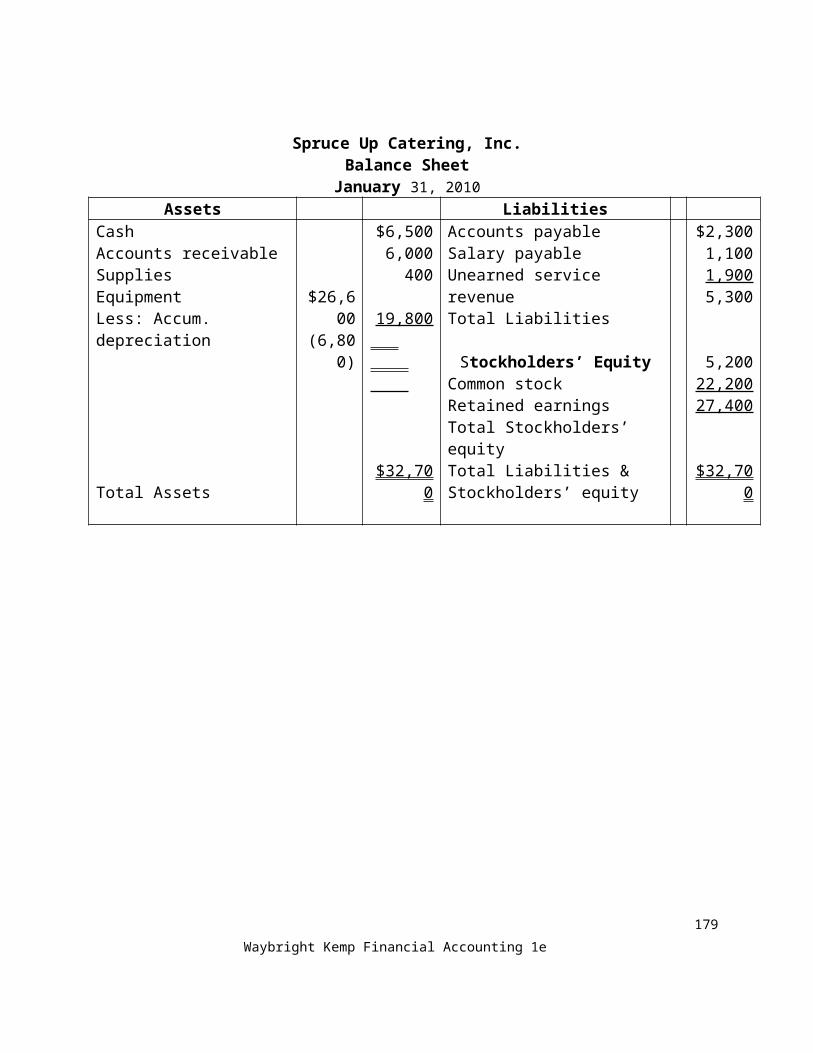

(15-20 min.) E 3-37B

Spruce Up Catering, Inc.Income Statement

Month Ended January 31, 2010Revenue: Service revenueExpenses: Salary expense Rent expense Depreciation expense, equipment Supplies expense Total ExpensesNet Income

$3,8001,7001,500

900

$20,100

7,900$12,200

Spruce Up Catering, Inc.Statement of Retained EarningsMonth Ended January 31, 2010

Retained earnings, January 1, 2010Add: Net income for the MonthSubtotalLess: DividendsRetained earnings, January 31, 2010

$11,10012,20023,300 1,100 $22,200

Waybright Kemp Financial Accounting 1e 165

Spruce Up Catering, Inc.Balance Sheet

January 31, 2010Assets Liabilities

CashAccounts receivableSuppliesEquipmentLess: Accum. depreciation

Total Assets

$26,600(6,800)

$6,5006,000

400

19,800

$32,700

Accounts payableSalary payableUnearned service revenueTotal Liabilities

Stockholders’ EquityCommon stockRetained earningsTotal Stockholders’ equity Total Liabilities & Stockholders’ equity

$2,3001,1001,9005,300

5,20022,20027,400

$32,700

166 Solutions Manual

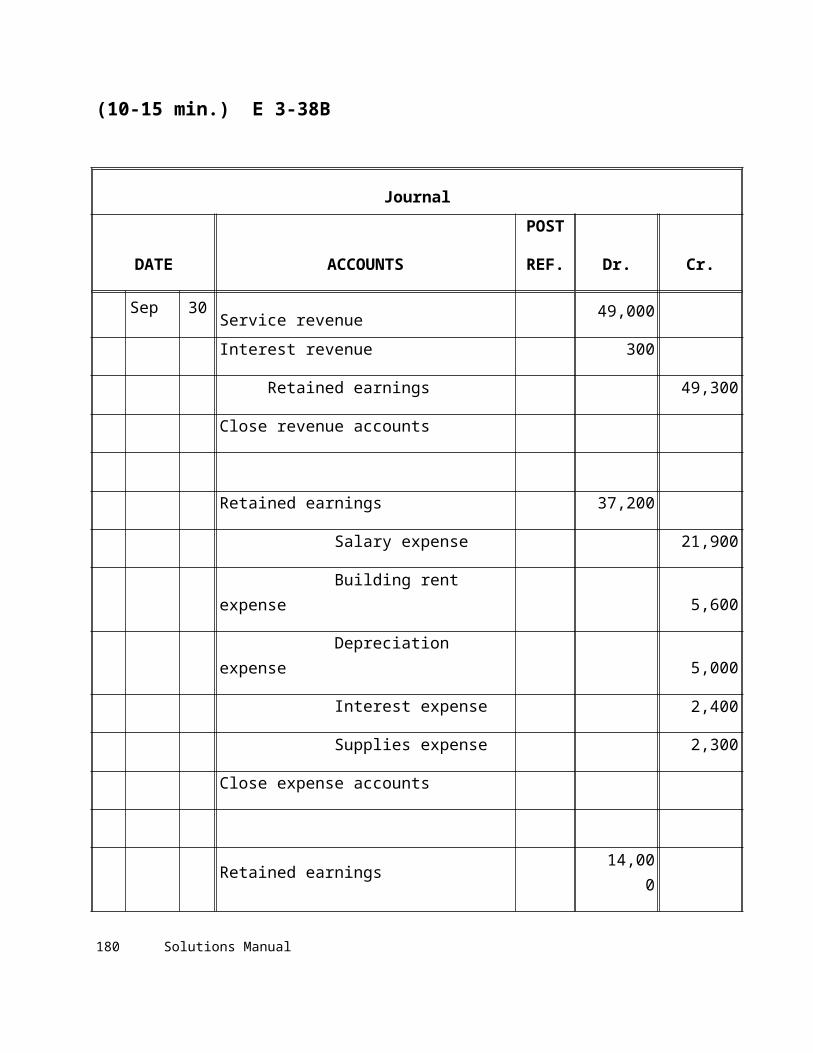

(10-15 min.) E 3-38B

Journal

DATE ACCOUNTS

POST

REF. Dr. Cr.

Sep 30Service revenue

49,000

Interest revenue 300

Retained earnings 49,300

Close revenue accounts

Retained earnings 37,200

Salary expense 21,900

Building rent expense 5,600

Depreciation expense 5,000

Interest expense 2,400

Supplies expense 2,300

Close expense accounts

Retained earnings 14,000

Dividends 14,000

Close dividends

Juba Electrical, Inc.’s ending retained earnings is $6,000 ($7,900 + $49,300 - $37,200 - $14,000).

Waybright Kemp Financial Accounting 1e 167

(10-15 min.) E 3-39B

Resch Restore, Inc.Statement of Retained EarningsYear Ended January 31, 2010

Retained earnings, February 1, 2009Add: Net income for the MonthSubtotalLess: DividendsRetained earnings, January 31, 2010

$77,000189,000266,000 82,000

$184,000

(10-15 min.) E 3-40B

Fonzarelli Photo, Inc.Post-Closing Trial Balance

March 31, 2010ACCOUNT DEBIT CREDITCashAccounts receivableSuppliesEquipmentAccumulated depreciation, equipmentAccounts payableSalary payableUnearned service revenueCommon stockRetained earningsTotal

$10,25025,000

60017,000

. $52,850

$5,0008,8005,2002,200

20,00011,650

$52,850

168 Solutions Manual

(10-15 min.) E 3-41B

Journal

DATE ACCOUNTS

POST

REF. Dr. Cr.

Aug 31Service revenues

77,000

Retained earnings 77,000

Close revenue accounts

Retained earnings 37,800

Salary expense 27,000

Rent expense 6,000

Depreciation expense, equipment 1,500

Depreciation expense, furniture 1,300

Supplies expense 2,000

Close expense accounts

Retained earnings 14,000

Dividends 14,000

Close dividends

Waybright Kemp Financial Accounting 1e 169

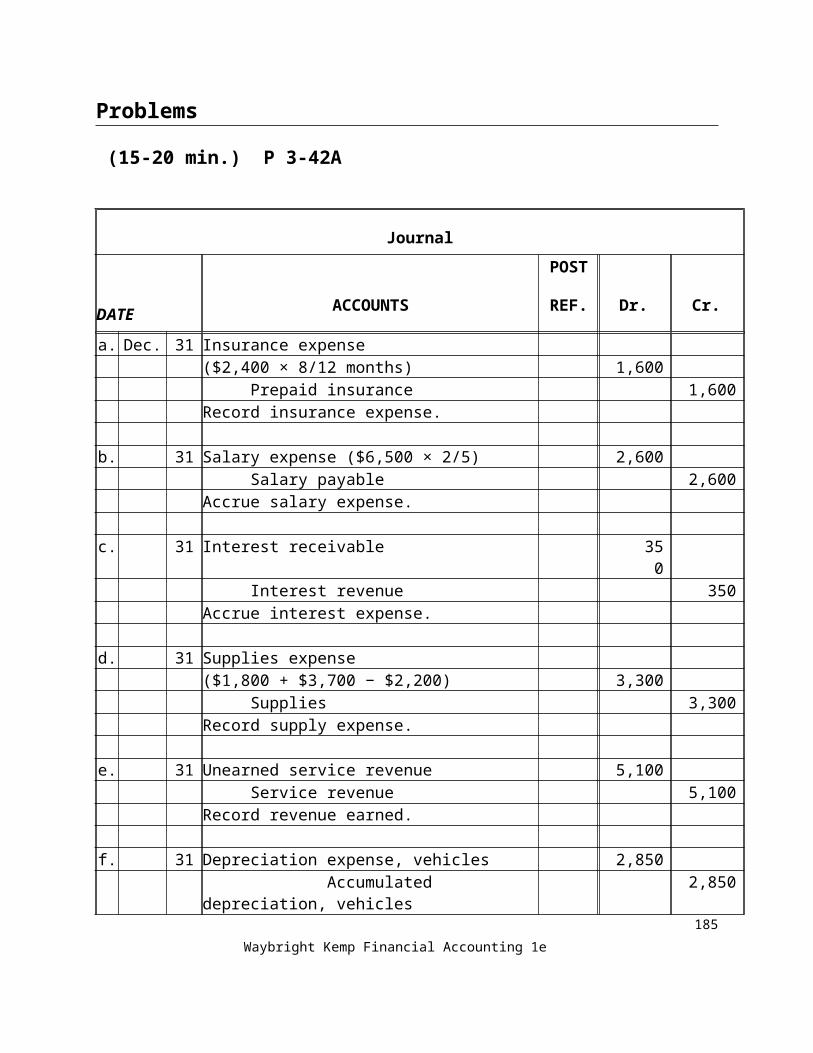

Problems

(15-20 min.) P 3-42A

Journal

DATEACCOUNTS

POST

REF. Dr. Cr.

a. Dec. 31 Insurance expense($2,400 × 8/12 months) 1,600

Prepaid insurance 1,600Record insurance expense.

b. 31 Salary expense ($6,500 × 2/5) 2,600Salary payable 2,600

Accrue salary expense.

c. 31 Interest receivable 350 Interest revenue 350

Accrue interest expense.

d. 31 Supplies expense($1,800 + $3,700 − $2,200) 3,300

Supplies 3,300Record supply expense.

e. 31 Unearned service revenue 5,100Service revenue 5,100

Record revenue earned.

f. 31 Depreciation expense, vehicles 2,850 Accumulated depreciation, vehicles 2,850

Depreciation expense, equipment 1,200Accumulated depreciation, equipment 1,200

Record depreciation expense.

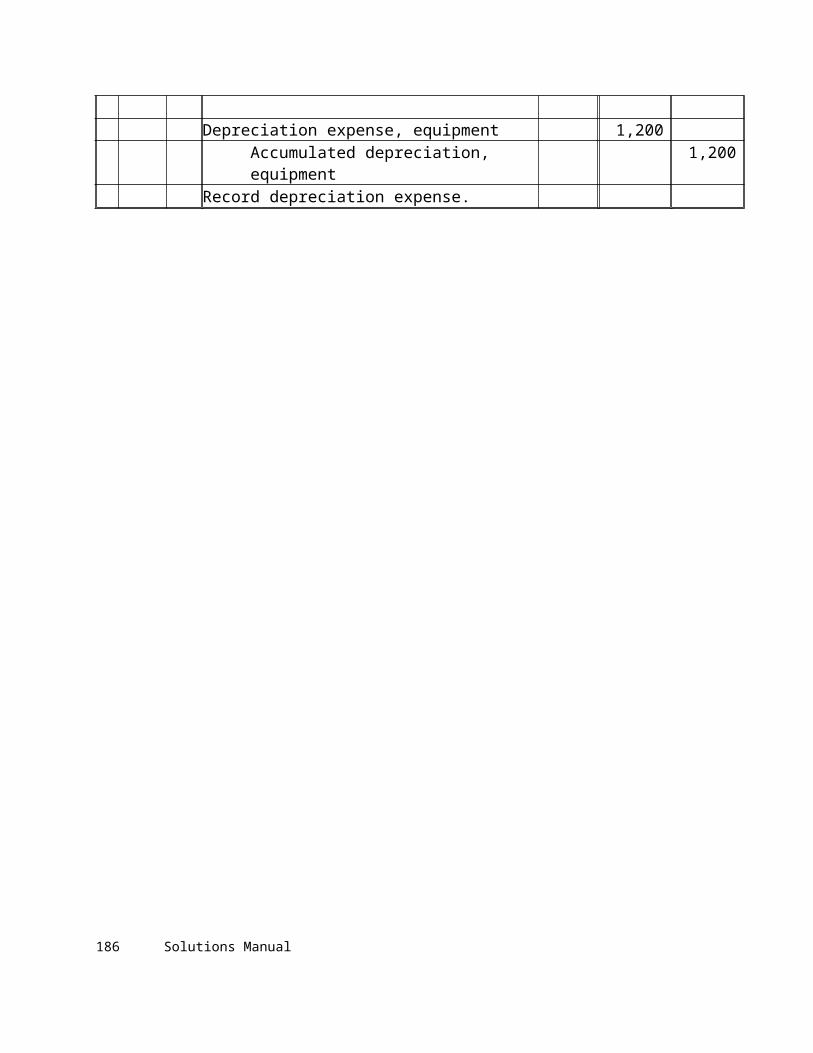

170 Solutions Manual

(15-20 min.) P 3-43A

Journal

DATE ACCOUNTS

POST

REF. Dr. Cr.

June 30 Supplies expense ($1,100 - $0) 1,100Supplies ($1,400 − $300) 1,100

Record supplies used.

30 Rent expense ($4,200 - $3,500) 700 Prepaid rent ($2,800 - $2,100) 700Record Prepaid rent expired

30 Depreciation expense, equipment ($1,500 - $1,250)

250

Accumulated depreciation,equipment ($7,750 − $7,500) 250

Record depreciation.

30 Salary expense ($24,650 - $23,400) 1,250Salary payable ($1,250 − $0) 1,250

Accrue salary expense.

30 Interest expense ($400 - $250) 150 Interest payable ($150 - $0) 150Accrue interest expense

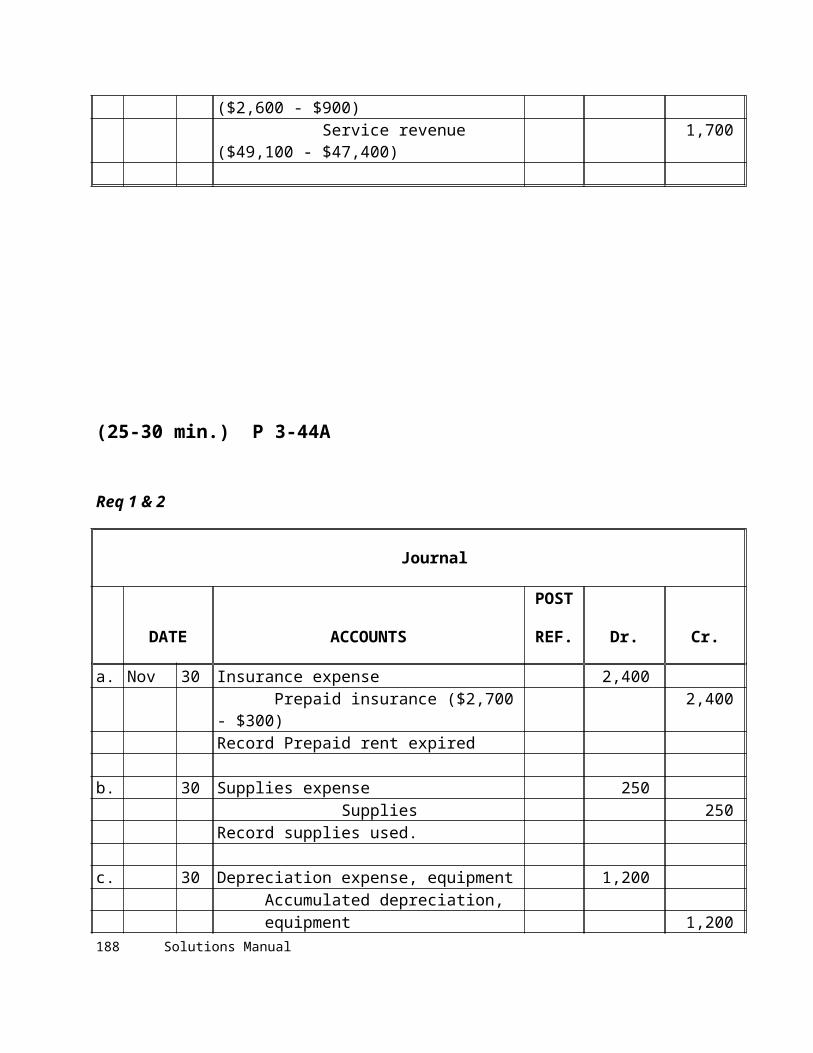

30 Unearned service revenue ($2,600 - $900) 1,700 Service revenue ($49,100 - $47,400) 1,700

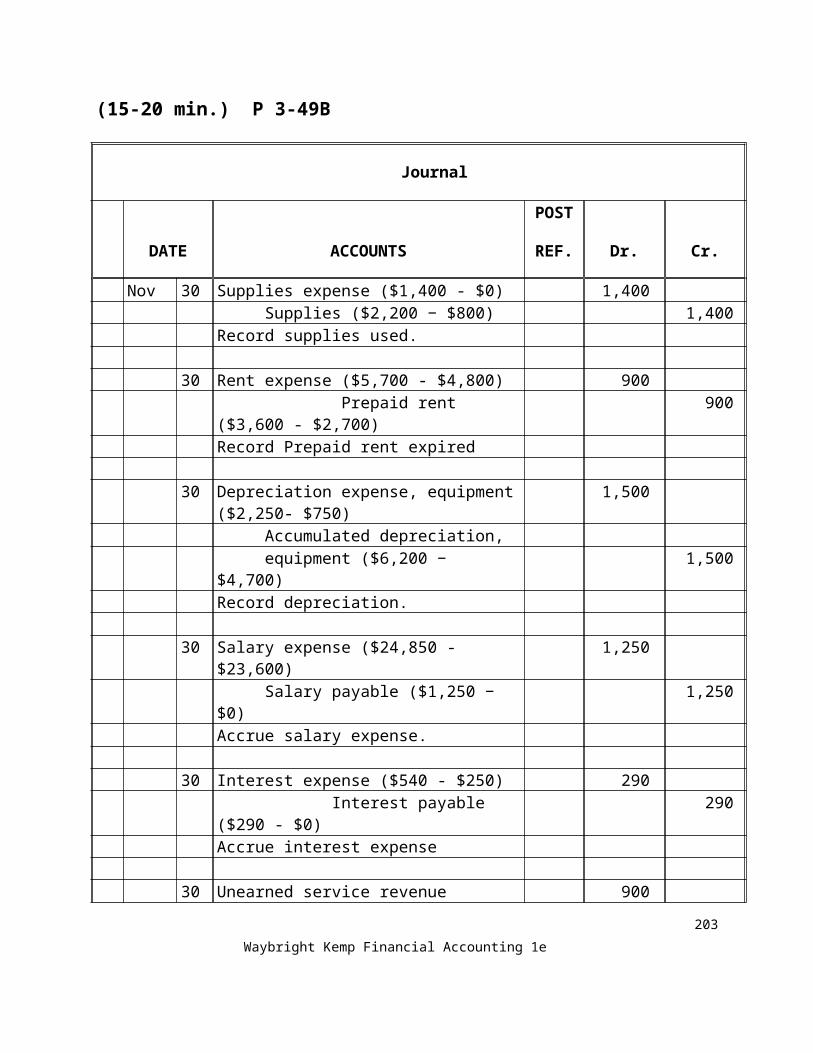

Waybright Kemp Financial Accounting 1e 171

(25-30 min.) P 3-44A

Req 1 & 2

Journal

DATE ACCOUNTS

POST

REF. Dr. Cr.

a. Nov 30 Insurance expense 2,400 Prepaid insurance ($2,700 - $300) 2,400

Record Prepaid rent expired

b. 30 Supplies expense 250 Supplies 250Record supplies used.

c. 30 Depreciation expense, equipment 1,200Accumulated depreciation,equipment 1,200

Record depreciation.

d. 30 Utilities expense 300 Accounts payable 300Accrue utilities expense

e. 30 Salary expense 450Salary payable 450

Accrue salary expense.

f. 31 Unearned service revenue ($2,200 - $800) 1,400 Service revenue 1,400Record unearned revenue earned

172 Solutions Manual

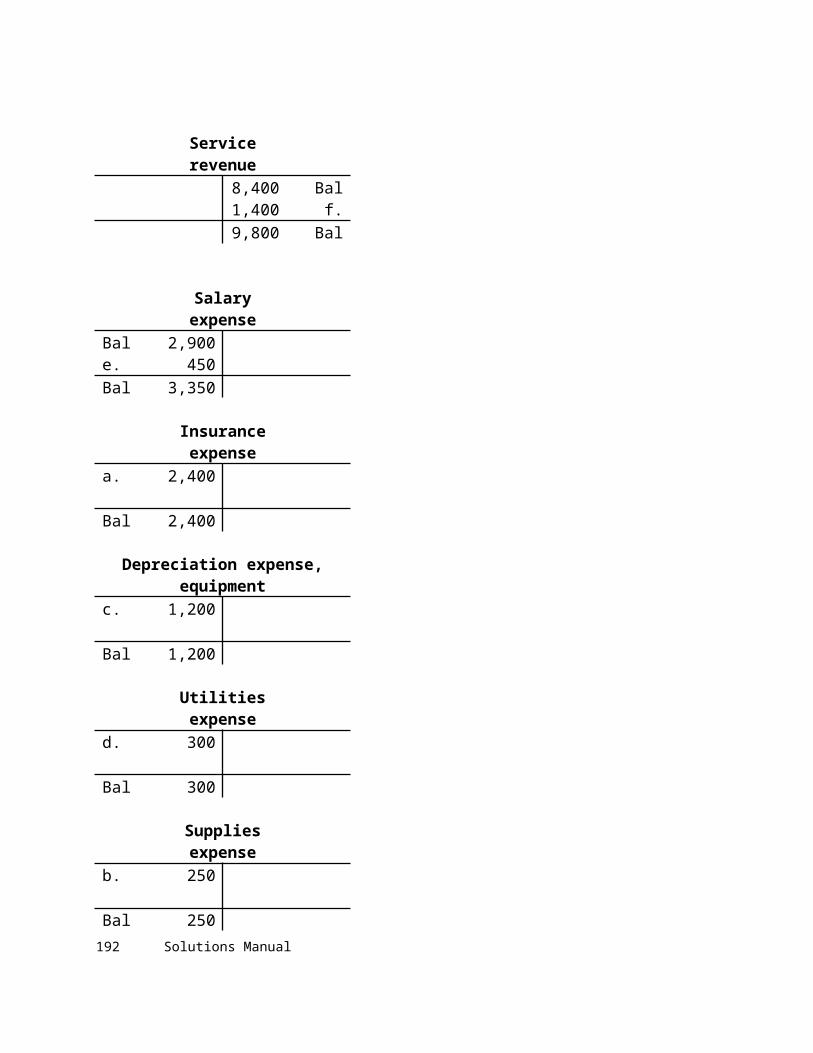

Req 1 & 2

Cash

Supplies

Bal 22,800 Bal 900 250 b.

Bal 22,800

Bal 650

Equipment

Accounts receivable Bal 83,800

Bal 39,400

Bal 83,800

Bal 39,400Accumulated depreciation, equipment

64,300 BalPrepaid insurance 1,200 c.

Bal 2,700 2,400 a. 65,500 Bal

Bal 300

Accounts payable

Common stock

1,900 Bal 50,000 Bal

300 d.

2,200Bal

50,000 Bal

Salary payable Retained earnings

450 e. 29,300 Bal

Waybright Kemp Financial Accounting 1e 173

450Bal

29,300 Bal

Unearned service revenue Dividends

f. 1,400 2,200 Bal Bal 3,600

800Bal

Bal 3,600

174 Solutions Manual

Service revenue

8,400 Bal 1,400 f.

9,800 Bal

Salary expense

Bal 2,900e. 450

Bal 3,350

Insurance expense

a. 2,400

Bal 2,400

Depreciation expense, equipmentc. 1,200

Bal 1,200

Utilities expense

d. 300

Bal 300

Supplies expense

b. 250

Bal 250

Waybright Kemp Financial Accounting 1e 175

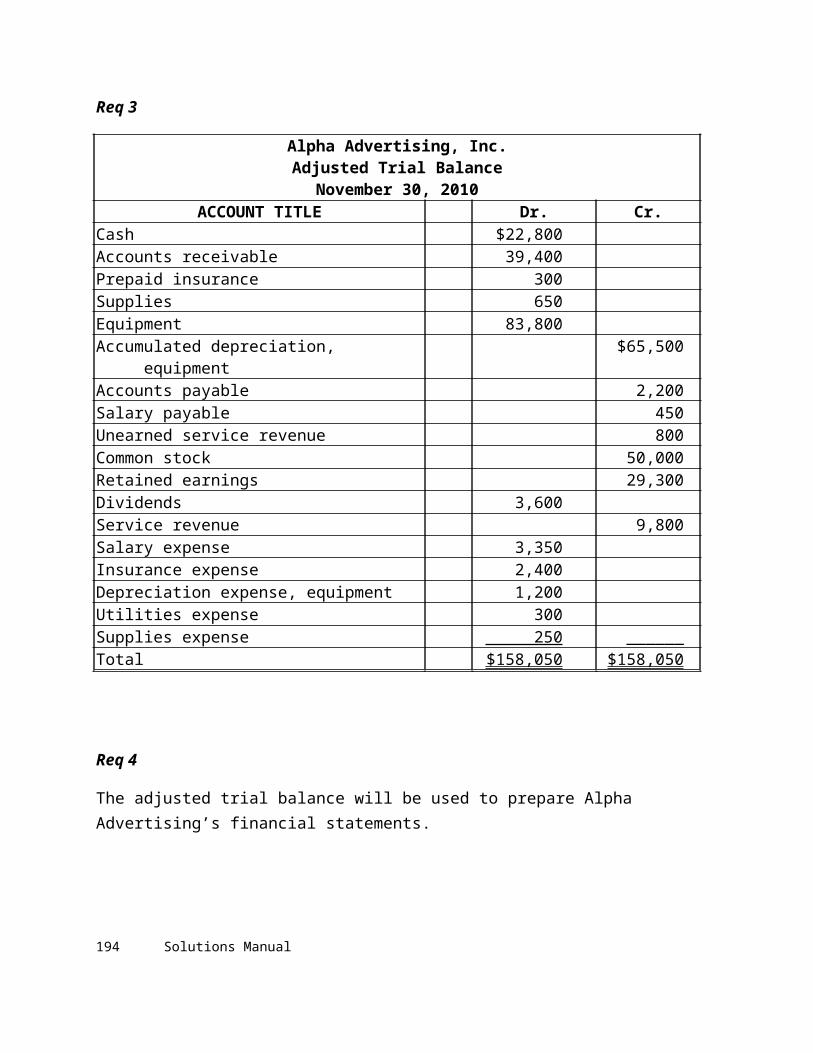

Req 3

Alpha Advertising, Inc. Adjusted Trial Balance

November 30, 2010ACCOUNT TITLE Dr. Cr.

Cash $22,800Accounts receivable 39,400Prepaid insurance 300Supplies 650Equipment 83,800Accumulated depreciation, equipment $65,500Accounts payable 2,200Salary payable 450Unearned service revenue 800Common stock 50,000Retained earnings 29,300Dividends 3,600Service revenue 9,800Salary expense 3,350Insurance expense 2,400Depreciation expense, equipment 1,200Utilities expense 300Supplies expense 250 ______Total $158,050 $158,050

Req 4

The adjusted trial balance will be used to prepare Alpha Advertising’s financial statements.

176 Solutions Manual

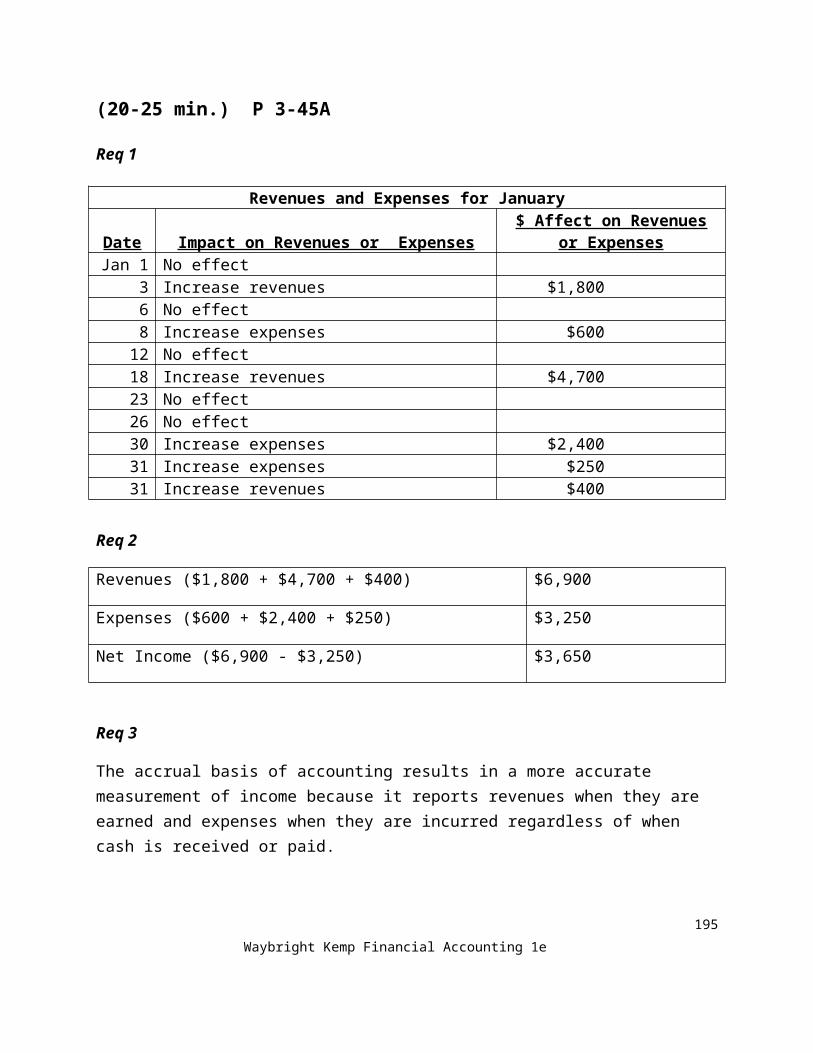

(20-25 min.) P 3-45A

Req 1

Revenues and Expenses for January

Date Impact on Revenues or Expenses$ Affect on Revenues or

ExpensesJan 1 No effect

3 Increase revenues $1,8006 No effect8 Increase expenses $600

12 No effect18 Increase revenues $4,70023 No effect26 No effect30 Increase expenses $2,40031 Increase expenses $25031 Increase revenues $400

Req 2

Revenues ($1,800 + $4,700 + $400) $6,900

Expenses ($600 + $2,400 + $250) $3,250

Net Income ($6,900 - $3,250) $3,650

Req 3

The accrual basis of accounting results in a more accurate measurement of income because it reports revenues when they are earned and expenses when they are incurred regardless of when cash is received or paid.

Waybright Kemp Financial Accounting 1e 177

(20-25 min.) P 3-46A

Req 1

Lighthouse Realty, Inc.

Income Statement

Year Ended December 31, 2010

Revenue:

Service revenue $97,000

Interest revenue 650

Total Revenues $97,650

Expenses:

Salary expense $51,000

Rent expense 18,000

Depreciation Expense, Equipment 4,200

Utilities expense 2,700

Interest Expense 1,300

Supplies Expense 700

Total expenses 77,900

Net Income $19,750

178 Solutions Manual

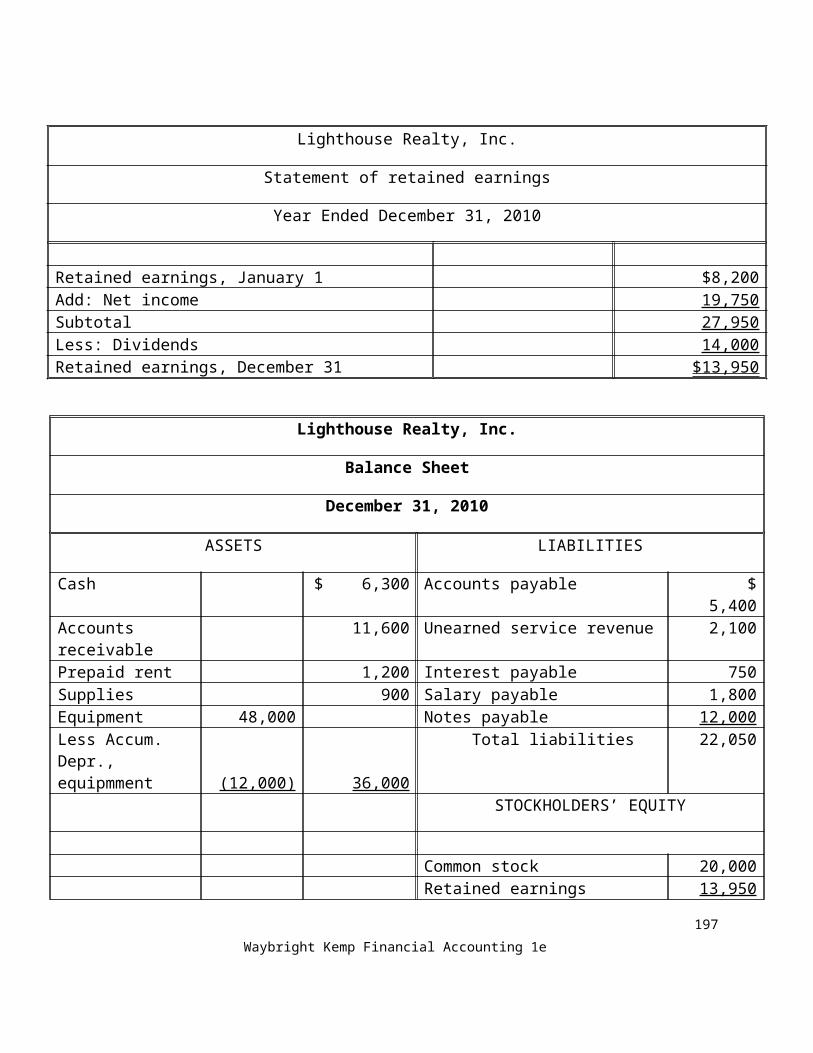

Lighthouse Realty, Inc.

Statement of retained earnings

Year Ended December 31, 2010

Retained earnings, January 1 $8,200Add: Net income 19,750Subtotal 27,950Less: Dividends 14,000Retained earnings, December 31 $13,950

Lighthouse Realty, Inc.

Balance Sheet

December 31, 2010

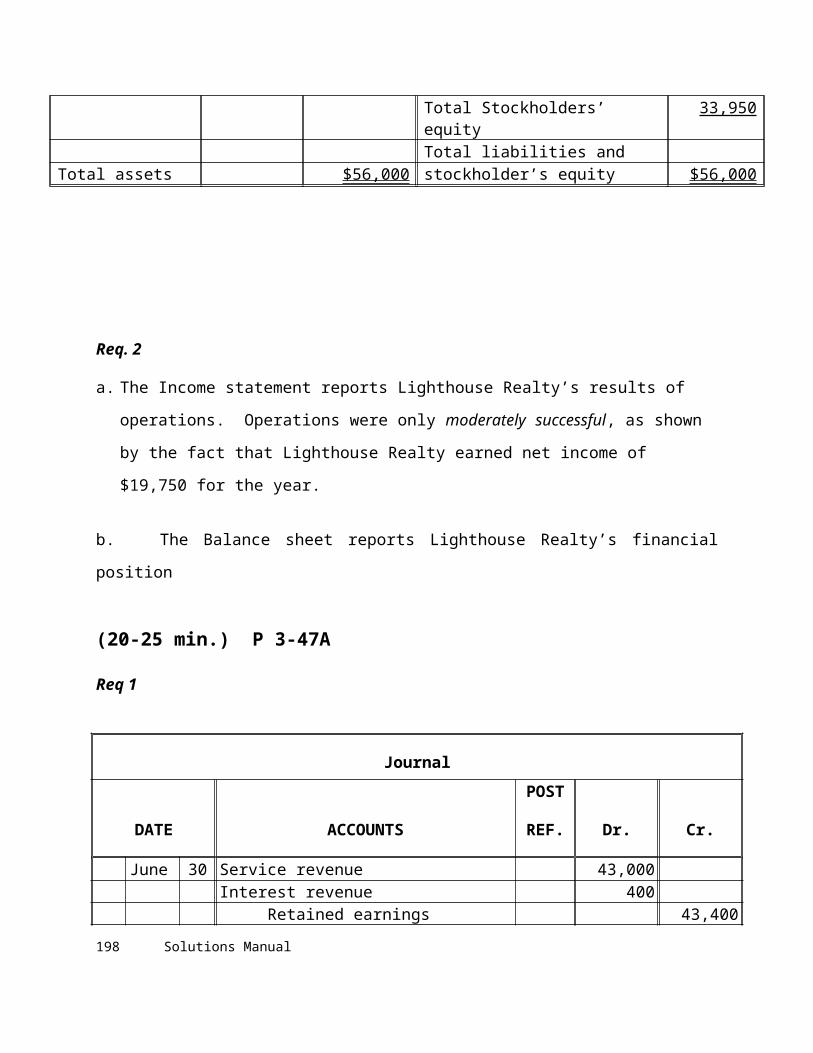

ASSETS LIABILITIES

Cash $ 6,300 Accounts payable $ 5,400Accounts receivable 11,600 Unearned service revenue 2,100Prepaid rent 1,200 Interest payable 750Supplies 900 Salary payable 1,800Equipment 48,000 Notes payable 12,000Less Accum. Depr., equipmment (12,000) 36,000

Total liabilities 22,050

STOCKHOLDERS’ EQUITY

Common stock 20,000Retained earnings 13,950Total Stockholders’ equity 33,950Total liabilities and

Total assets $56,000 stockholder’s equity $56,000

Waybright Kemp Financial Accounting 1e 179

Req. 2

a. The Income statement reports Lighthouse Realty’s results of operations. Operations were

only moderately successful, as shown by the fact that Lighthouse Realty earned net income

of $19,750 for the year.

b. The Balance sheet reports Lighthouse Realty’s financial position

(20-25 min.) P 3-47A

Req 1

Journal

DATE ACCOUNTS

POST

REF. Dr. Cr.

June 30 Service revenue 43,000Interest revenue 400

Retained earnings 43,400Close revenue accounts

Retained earnings 32,950 Salary expense 24,500 Rent expense 6,000 Depreciation expense, equipment 1,200 Utilities expense 700 Supplies expense 550Close expense accounts

Retained earnings 2,000 Dividends 2,000Close dividends

180 Solutions Manual

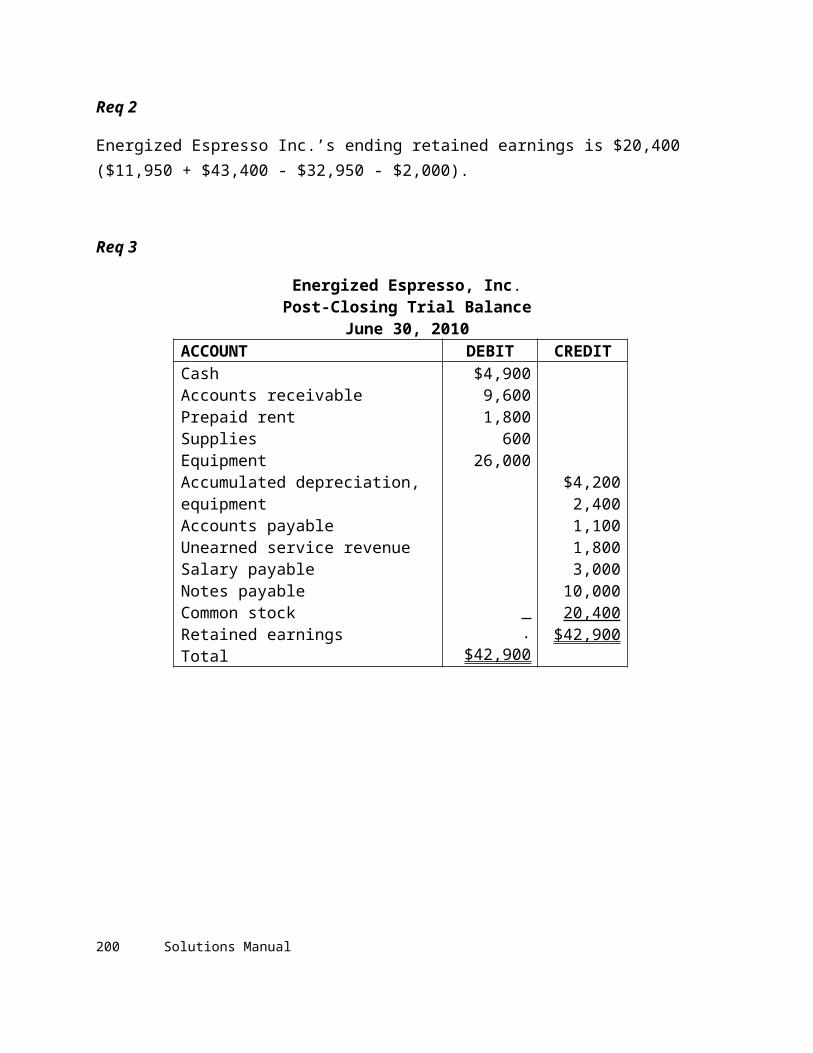

Req 2

Energized Espresso Inc.’s ending retained earnings is $20,400 ($11,950 + $43,400 - $32,950 - $2,000).

Req 3

Energized Espresso, Inc.Post-Closing Trial Balance

June 30, 2010ACCOUNT DEBIT CREDITCashAccounts receivablePrepaid rentSuppliesEquipmentAccumulated depreciation, equipmentAccounts payableUnearned service revenueSalary payableNotes payableCommon stockRetained earningsTotal

$4,9009,6001,800

60026,000

. $42,900

$4,2002,4001,1001,8003,000

10,00020,400

$42,900

Waybright Kemp Financial Accounting 1e 181

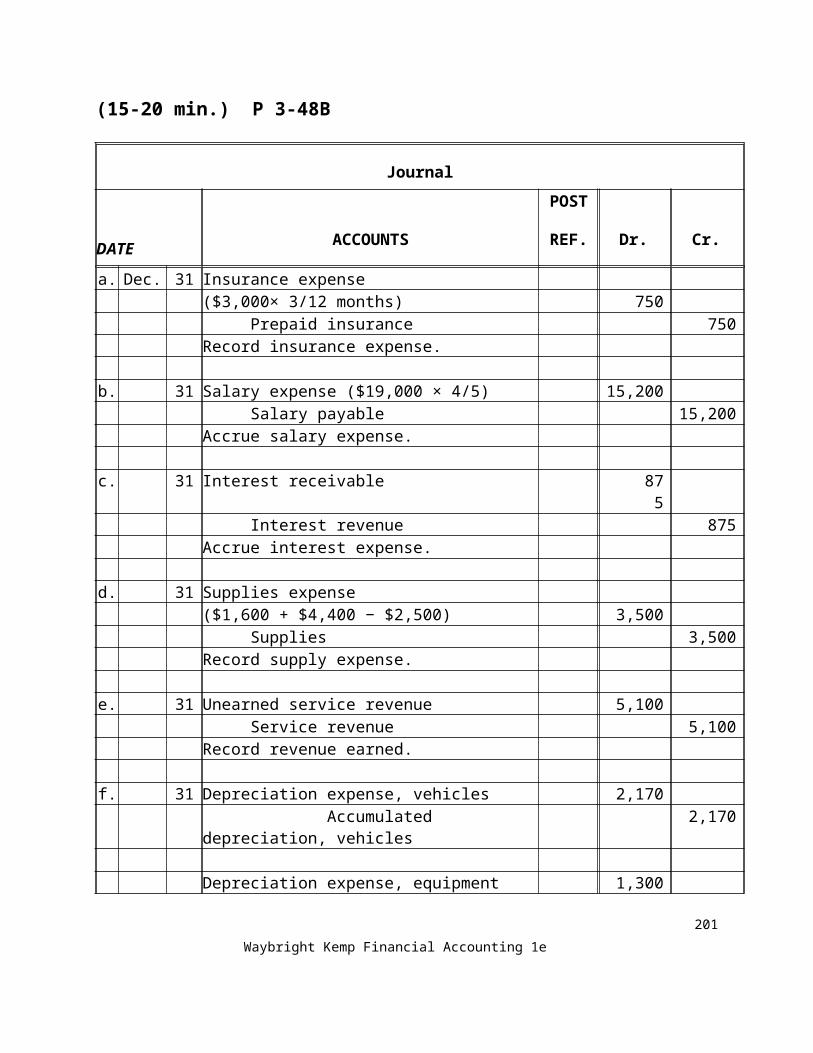

(15-20 min.) P 3-48B

Journal

DATEACCOUNTS

POST

REF. Dr. Cr.

a. Dec. 31 Insurance expense($3,000× 3/12 months) 750

Prepaid insurance 750Record insurance expense.

b. 31 Salary expense ($19,000 × 4/5) 15,200Salary payable 15,200

Accrue salary expense.

c. 31 Interest receivable 875 Interest revenue 875

Accrue interest expense.

d. 31 Supplies expense($1,600 + $4,400 − $2,500) 3,500

Supplies 3,500Record supply expense.

e. 31 Unearned service revenue 5,100Service revenue 5,100

Record revenue earned.

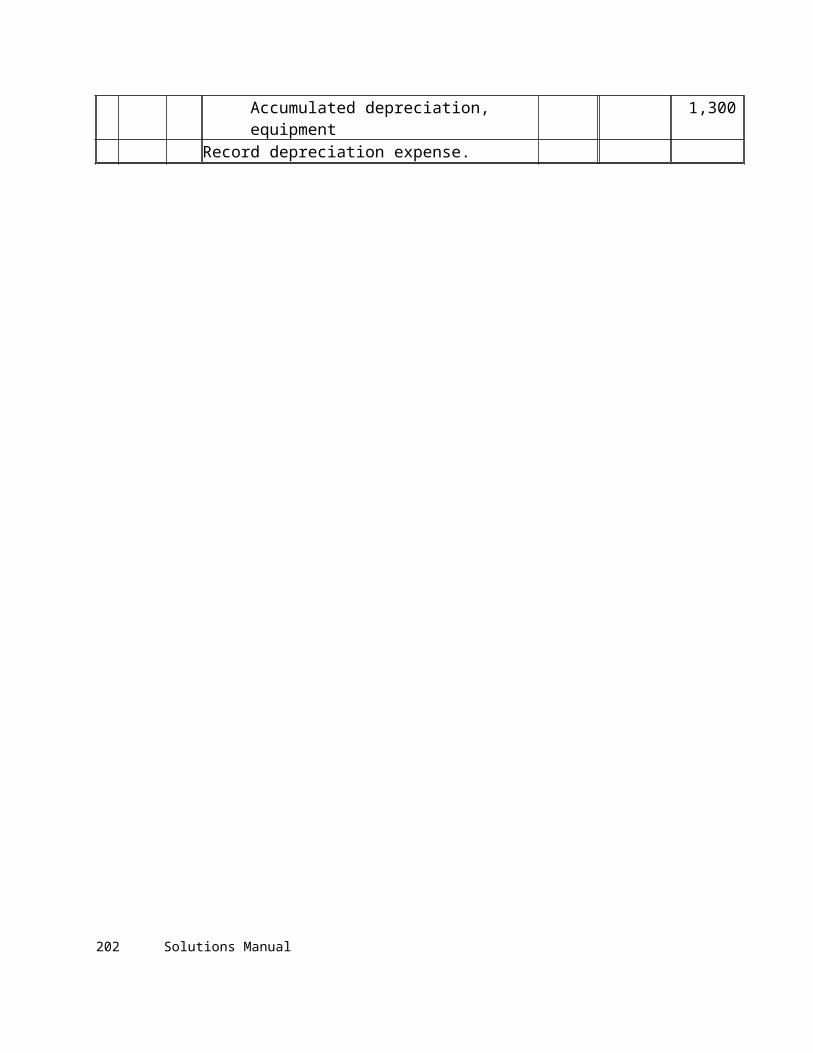

f. 31 Depreciation expense, vehicles 2,170 Accumulated depreciation, vehicles 2,170

Depreciation expense, equipment 1,300Accumulated depreciation, equipment 1,300

Record depreciation expense.

182 Solutions Manual

(15-20 min.) P 3-49B

Journal

DATE ACCOUNTS

POST

REF. Dr. Cr.

Nov 30 Supplies expense ($1,400 - $0) 1,400Supplies ($2,200 − $800) 1,400

Record supplies used.

30 Rent expense ($5,700 - $4,800) 900 Prepaid rent ($3,600 - $2,700) 900Record Prepaid rent expired

30 Depreciation expense, equipment ($2,250- $750)

1,500

Accumulated depreciation,equipment ($6,200 − $4,700) 1,500

Record depreciation.

30 Salary expense ($24,850 - $23,600) 1,250Salary payable ($1,250 − $0) 1,250

Accrue salary expense.

30 Interest expense ($540 - $250) 290 Interest payable ($290 - $0) 290Accrue interest expense

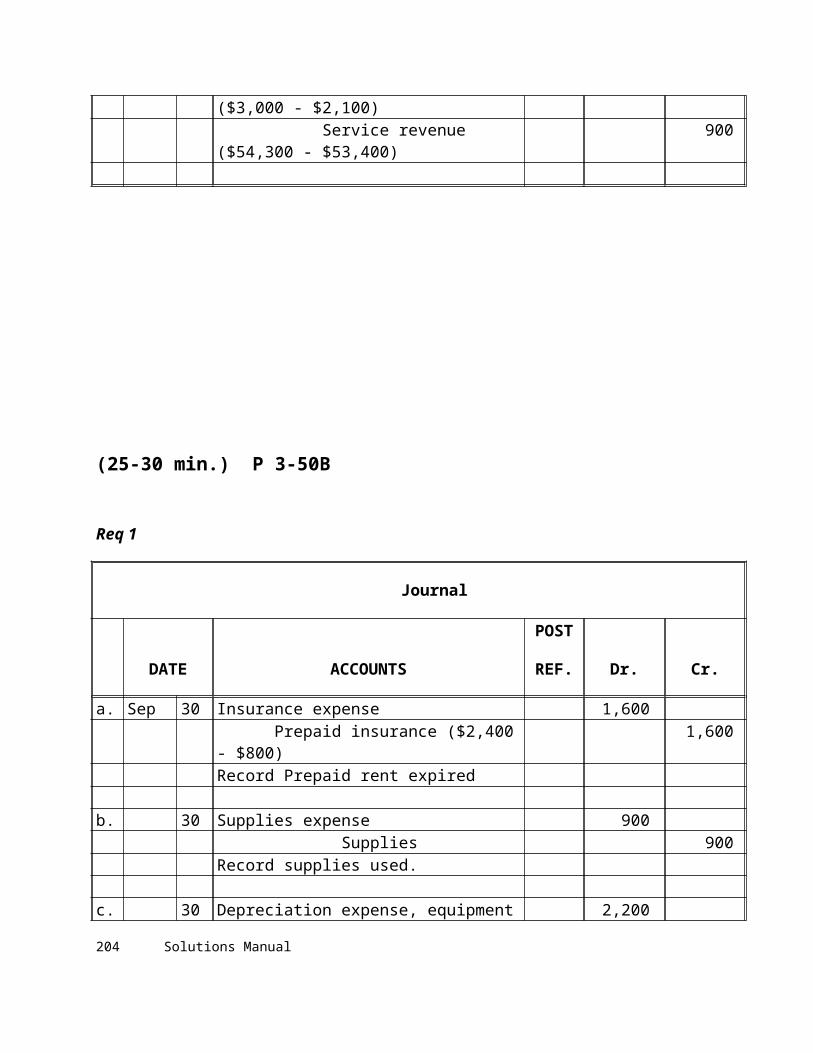

30 Unearned service revenue ($3,000 - $2,100) 900 Service revenue ($54,300 - $53,400) 900

Waybright Kemp Financial Accounting 1e 183

(25-30 min.) P 3-50B

Req 1

Journal

DATE ACCOUNTS

POST

REF. Dr. Cr.

a. Sep 30 Insurance expense 1,600 Prepaid insurance ($2,400 - $800) 1,600

Record Prepaid rent expired

b. 30 Supplies expense 900 Supplies 900Record supplies used.

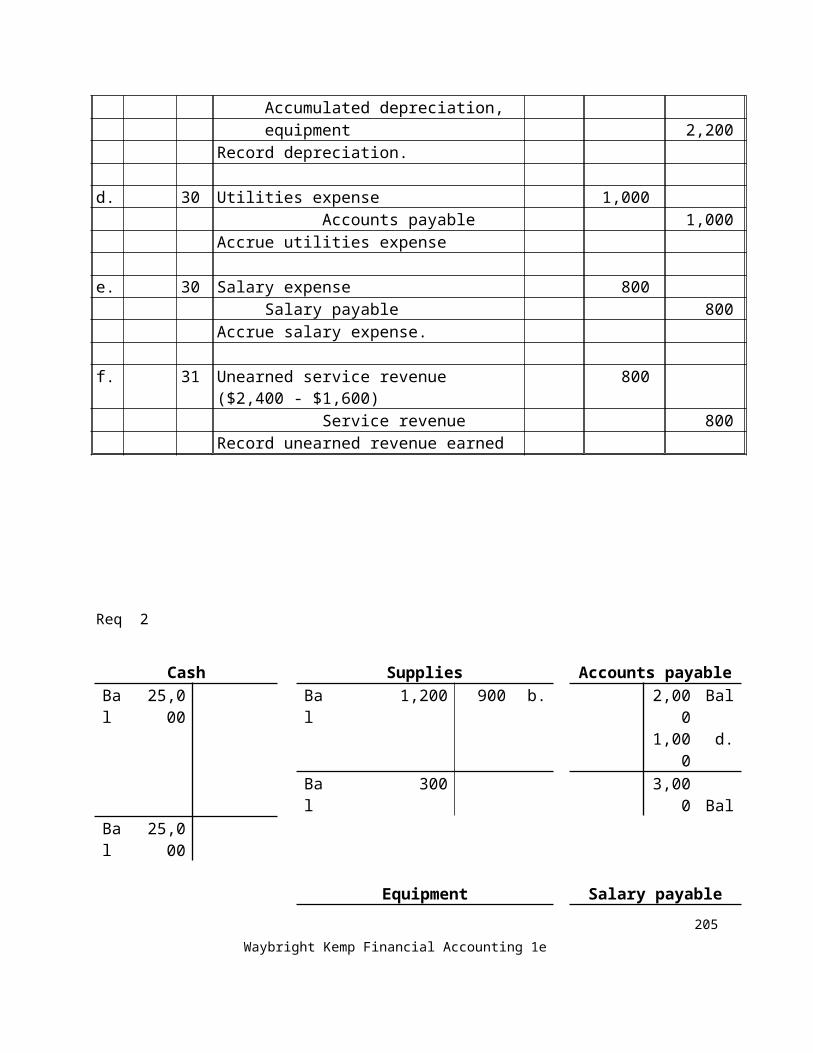

c. 30 Depreciation expense, equipment 2,200Accumulated depreciation,equipment 2,200

Record depreciation.

d. 30 Utilities expense 1,000 Accounts payable 1,000Accrue utilities expense

e. 30 Salary expense 800Salary payable 800

Accrue salary expense.

f. 31 Unearned service revenue ($2,400 - $1,600) 800 Service revenue 800Record unearned revenue earned

184 Solutions Manual

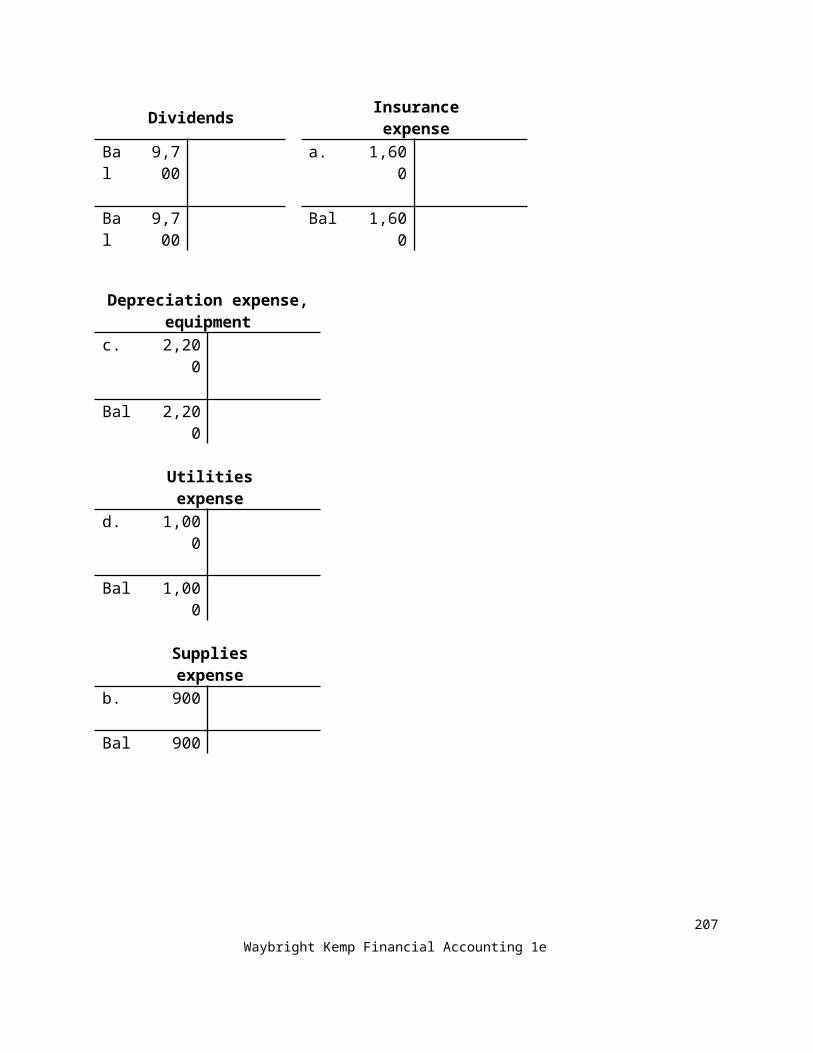

Req 2

Cash

Supplies

Accounts payableBal 25,000 Bal 1,200 900 b. 2,000 Bal

1,000 d.

Bal 300 3,000 BalBal 25,000

Equipment Salary payableAccounts receivable Bal 59,000 800 e.

Bal 17,400 Bal 59,000 800 BalBal 17,400

Accumulated depreciation, equipment

Unearned service revenue

50,000 Bal f. 800 2,400 BalPrepaid insurance 2,200 c.

Bal 2,400 1,600 a. 52,200 Bal 1,600 Bal

Bal 800

Common stock

Service revenue

25,000 Bal 16,200 Bal 800 f.

25,000 Bal 17,000 Bal

Retained earnings

Salary expense

22,800 Bal Bal 3,700 e. 800

22,800 Bal Bal 4,500

Dividends

Insurance expense

Bal 9,700 a. 1,600

Bal 9,700 Bal 1,600

Waybright Kemp Financial Accounting 1e 185

Depreciation expense, equipment

c. 2,200

Bal 2,200

Utilities expense

d. 1,000

Bal 1,000

Supplies expense

b. 900

Bal 900

186 Solutions Manual

Req 3

Nina’s Novelty, Inc., Adjusted Trial Balance

September 30, 2010ACCOUNT TITLE Dr. Cr.

Cash $25,000Accounts receivable 17,400Prepaid insurance 800Supplies 300Equipment 59,000Accumulated depreciation, equipment $52,200Accounts payable 3,000Salary payable 800Unearned service revenue 1,600Common stock 25,000Retained earnings 22,800Dividends 9,700Service revenue 17,000Salary expense 4,500Insurance expense 1,600Depreciation expense, equipment 2,200Utilities expense 1,000Supplies expense 900 ______Total $122,400 $122,400

Req 4

The adjusted trial balance will be used to prepare Nina’s Novelty, Inc.s financial statements.

Waybright Kemp Financial Accounting 1e 187

(20-25 min.) P 3-51B

Req 1

Revenues and Expenses for January

Date Impact on Revenues or Expenses$ Affect on Revenues or

ExpensesMay 1 No effect

3 Increase revenues $2,5006 No effect8 Increase expenses $500

12 No effect18 Increase revenues $3,50023 No effect26 No effect30 Increase expenses $1,30031 Increase expenses $90031 Increase revenues $1,100

Req 2

Revenues ($2,500 + $3,500 + $1,100) $7,100

Expenses ($500 + $1,300 + $900) $2,700

Net Income ($7,100 - $2,700) $4,400

Req 3

The accrual basis of accounting results in a more accurate measurement of income because it reports revenues when they are earned and expenses when they are incurred regardless of when cash is received or paid.

188 Solutions Manual

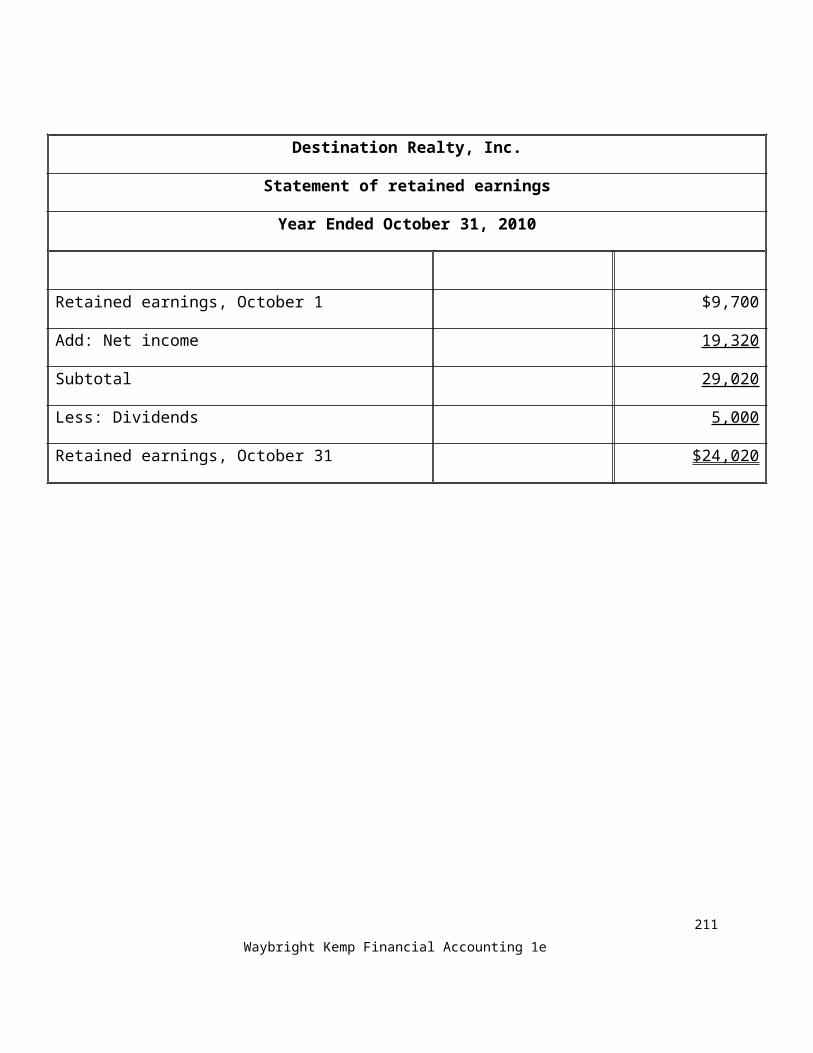

(20-25 min.) P 3-52B

Req 1

Destination Realty, Inc.

Income Statement

Year Ended October 31, 2010

Revenue:

Service revenue $85,000

Interest revenue 420

Total Revenues $85,420

Expenses:

Salary expense $40,000

Rent expense 20,000

Depreciation Expense, Equipment 2,500

Utilities expense 1,800

Interest Expense 1,100

Supplies Expense 700

Total expenses 66,100

Net Income $19,320

Waybright Kemp Financial Accounting 1e 189

Destination Realty, Inc.

Statement of retained earnings

Year Ended October 31, 2010

Retained earnings, October 1 $9,700

Add: Net income 19,320

Subtotal 29,020

Less: Dividends 5,000

Retained earnings, October 31 $24,020

190 Solutions Manual

Destination Realty, Inc.

Balance Sheet

October 31, 2010

ASSETS LIABILITIES

Cash $ 6,500 Accounts payable $ 4,300

Accounts receivable 12,100 Unearned service revenue 2,800

Prepaid rent 2,500 Interest payable 720

Supplies 500 Salary payable 9,000

Equipment 42,500 Notes payable 8,000

Less Accum. Depr., equipmment (11,300) 31,200

Total liabilities 24,820

STOCKHOLDERS’ EQUITY

Common stock 3,960

Retained earnings 24,020

Total Stockholders’ equity 27,980

Total liabilities and

Total assets $52,800 stockholder’s equity $52,800

Req. 2

a. The Income statement reports Destination Realty’s results of operations. Operations were

only moderately successful, as shown by the fact that Destination Realty earned net income

of $19,320 for the year.

b. The Balance sheet reports Destination Realty’s financial position

Waybright Kemp Financial Accounting 1e 191

(20-25 min.) P 3-53B

Req 1

Journal

DATE ACCOUNTS

POST

REF. Dr. Cr.

Sep 30Service revenue

41,000

Interest revenue 1,000

Retained earnings 42,000

Close revenue accounts

Retained earnings 27,000

Salary expense 18,500

Rent expense 5,400

Depreciation expense, equipment 1,700

Utilities expense 800

Supplies expense 600

Close expense accounts

Retained earnings 4,000

Dividends 4,000

Close dividends

192 Solutions Manual

Req 2

Java Jolt Inc.’s ending retained earnings is $22,200 ($11,200 + $42,000 - $27,000 - $4,000).

Req 3

Java Jolt, Inc.Post-Closing Trial Balance

September 30, 2010ACCOUNT DEBIT CREDITCashAccounts receivablePrepaid rentSuppliesEquipmentAccumulated depreciation, equipmentAccounts payableUnearned service revenueSalary payableNotes payableCommon stockRetained earningsTotal

$5,8007,0002,300

30030,000

. $45,400

$3,8003,0001,9001,400

10,0003,100

22,200$45,400

Waybright Kemp Financial Accounting 1e 193

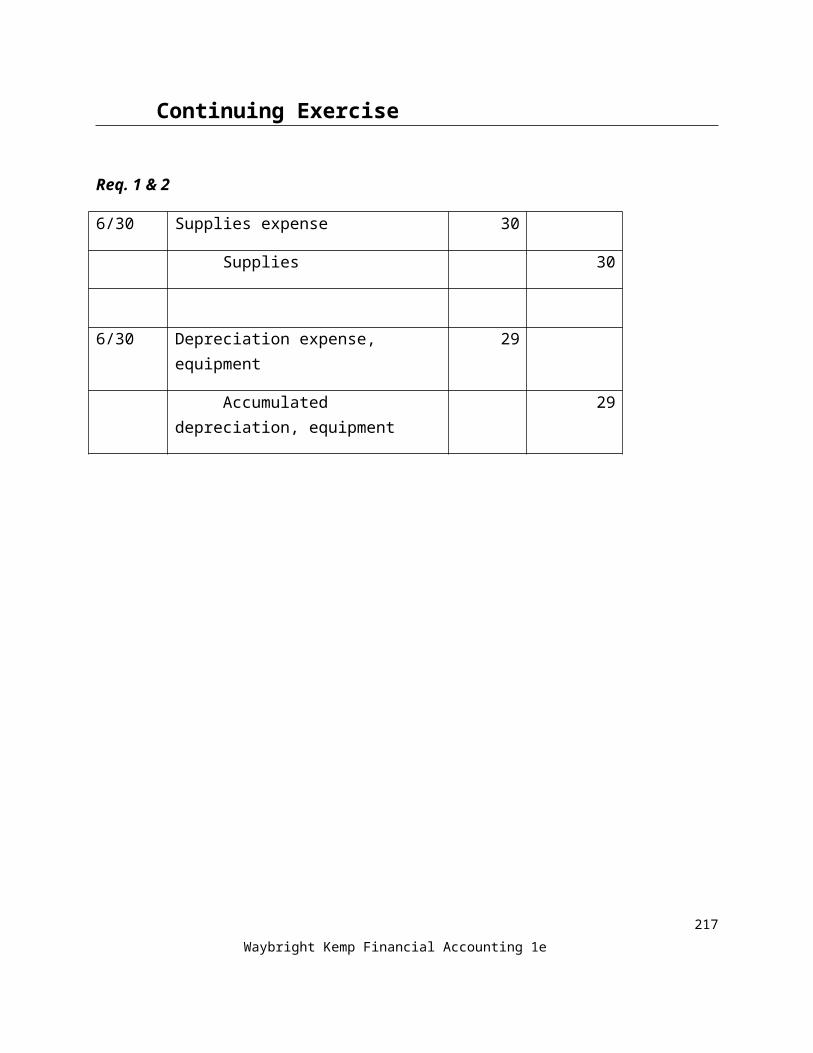

Continuing Exercise

Req. 1 & 2

6/30 Supplies expense 30

Supplies 30

6/30 Depreciation expense, equipment 29

Accumulated depreciation, equipment 29

194 Solutions Manual

Assets = Liabilities + Stockholders’ equity

Cash Lawn supplies Accounts payable Common stock6/1 1,000 20 6/5 6/8 50 30 6/30 1,400 6/3 1,000 6/16/17 500 50 6/8

6/30 50 Bal. 20 1,400 Bal. 1,000 Bal.Bal. 1,480

Equipment Retained

earnings

6/3 1,400 Clo. 80 700 Clo.

Bal. 1,400 620 Bal.

Accounts receivable

Accumulated depreciation, equipment

Service revenue

6/6 200 50 6/30 29 6/30 200 6/6 500 6/17

Bal. 150 29 Bal. Clo. 700 700 Bal. 0 Bal.

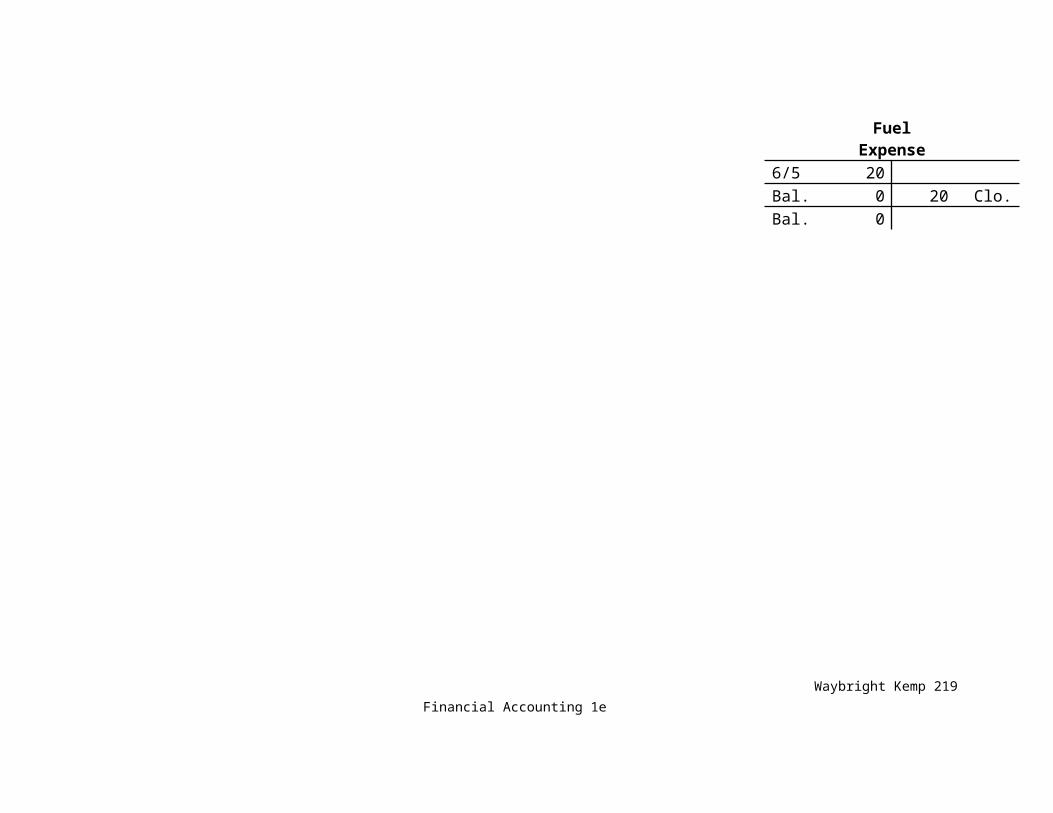

Fuel Expense

6/5 20 Bal. 0 20 Clo.Bal. 0

Waybright Kemp Financial Accounting 1e 195

Depreciation expense, equipment

6/30 29 Bal. 29 29 Clo.Bal. 0

Supplies expense

6/30 30 Bal. 30 30 Clo.Bal. 0

196 Solutions Manual

Req. 3

Graham’s YardCare, Inc.Adjusted Trial Balance

June 30, 2010ACCOUNT DEBIT CREDITCashAccounts receivableLawn suppliesEquipmentAccumulated depreciation, equipmentAccounts payableCommon stockService revenueFuel expenseDepreciation expense, equipmentSupplies expenseTotal

$1,48015020

1,400

2029

30 $3,129

$ 291,4001,000

700

. $3,129

Req. 4

6/30 Service revenue 700

Retained earnings 700

6/30 Retained earnings 79

Depreciation expense, equipment 29

Supplies expense 30

Fuel expense 20

6/30 Note – there were no dividends so no entry is required to close dividends

Waybright Kemp Financial Accounting 1e 197

Req 5

Graham’s YardCare, Inc.Post closing Trial Balance

June 30, 2010ACCOUNT DEBIT CREDITCashAccounts receivableLawn suppliesEquipmentAccumulated depreciation, equipmentAccounts payableCommon stockRetained earningsTotal

$1,48015020

1,400

. $3,050

$ 291,4001,000

621 $3050

198 Solutions Manual

Continuing Problem

Req 1

DATE ACCOUNTS

POST.

REF. Dr. Cr.

July 1 Prepaid rent 5,400Cash 5,400

4 Cash 2,100Service revenue 2,100

9 Cash 3,600Unearned service revenue 3,600

12 Supplies 750Accounts payable 750

15 Accounts receivable 2,800Service revenue 2,800

16 Salary expense 675Cash 675

22 Cash 3,100 Accounts receivable 3,100

25 Accounts payable 2,800 Cash 2,800

28 Cash 1,200 Service revenue 1,200

30 Dividends 600 Cash 600

Waybright Kemp Financial Accounting 1e 199

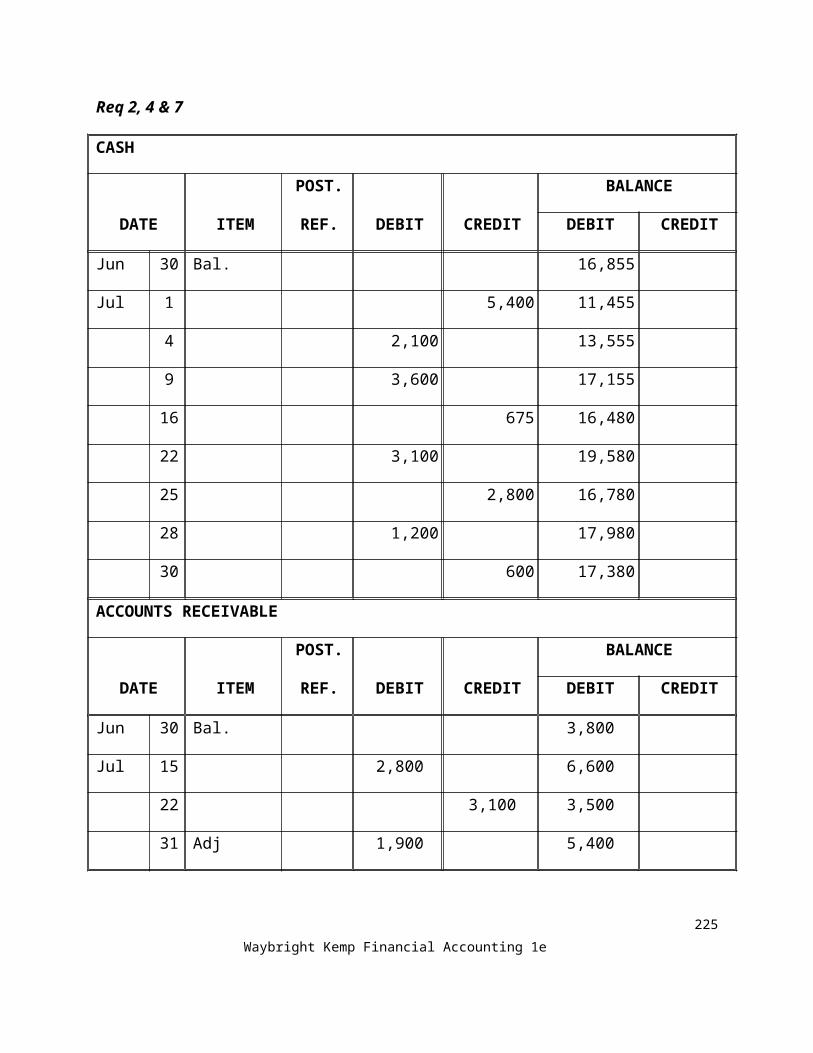

Req 2, 4 & 7

CASH

POST. BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

Jun 30 Bal. 16,855

Jul 1 5,400 11,455

4 2,100 13,555

9 3,600 17,155

16 675 16,480

22 3,100 19,580

25 2,800 16,780

28 1,200 17,980

30 600 17,380

ACCOUNTS RECEIVABLE

POST. BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

Jun 30 Bal. 3,800

Jul 15 2,800 6,600

22 3,100 3,500

31 Adj 1,900 5,400

200 Solutions Manual

SUPPLIES

POST. BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

Jun 30 Bal. 1,610

Jul 12 750 2,360

31 Adj 2,010 350

PREPAID RENT

POST. BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

Jul 1 5,400 5,400

31 Adj 1,800 3,600

Waybright Kemp Financial Accounting 1e 201

LAND

POST. BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

Jun 30 Bal 15,000

OFFICE FURNITURE

POST. BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

Jun 30 Bal 3,300

ACCUMULATED DEPRECIATION, OFFICE FURNITURE

POST. BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

Jul 31 Adj 210 210

EQUIPMENT

POST. BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

Jun 30 Bal. 4,700

202 Solutions Manual

ACCUMULATED DEPRECIATION, EQUIPMENT

POST. BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

Jul 31 Adj 400 400

VEHICLES

POST. BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

Jun 30 Bal. 31,000

ACCUMULATED DEPRECIATION, VEHICLES

POST. BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

Jul 31 Adj 650 650

ACCOUNTS PAYABLE

POST. BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

Jun 30 Bal. 3,890

Jul 12 750 4,640

25 2,800 1,840

Waybright Kemp Financial Accounting 1e 203

SALARIES PAYABLE

POST. BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

Jul 31 Adj 675 675

UNEARNED SERVICE REVENUE

POST. BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

Jul 9 3,600 3,600

Jul 31 Adj 800 2,800

NOTES PAYABLE

POST. BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

Jun 30 Bal. 31,000

204 Solutions Manual

COMMON STOCK

POST. BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

Jun 30 Bal. 38,500

RETAINED EARNINGS

POST. BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

Jul 31 Clo 20,800 20,800

31 Clo 12,745 8,055

31 Clo 3,400 4,655

DIVIDENDS

POST. BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

Jun 30 Bal. 2,800

Jul 30 600 3,400

Jul 31 Clo 3,400 -0-

Waybright Kemp Financial Accounting 1e 205

SERVICE REVENUE

POST. BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

Jun 30 Bal. 12,000

Jul 4 2,100 14,100

15 2,800 16,900

28 1,200 18,100

31 Adj 1,900 20,000

31 Adj 800 20,800

31 Clo 20,800 -0-

SALARY EXPENSE

POST. BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

Jun 30 Bal. 2,700

Jul 16 675 3,375

Jul 31 Adj 675 4,050

Jul 31 Clo 4,050 -0-

206 Solutions Manual

RENT EXPENSE

POST. BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

Jun 30 Bal 1,800

Jul 31 Adj 1,800 3,600

Jul 31 Clo 3,600 -0-

UTILITIES EXPENSE

POST. BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

Jun 30 Bal. 1,225

Jul 31 Clo 1,225 -0-

ADVERTISING EXPENSE

POST. BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

Jun 30 Bal 325

Jul 31 Clo 325 -0-

Waybright Kemp Financial Accounting 1e 207

MISCELLANEOUS EXPENSE

POST. BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

Jun 30 Bal 275

Jul 31 Clo 275 -0-

SUPPLIES EXPENSE

POST. BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

Jul 31 Adj 2,010 2,010

Jul 31 Clo 2,010 -0-

DEPRECIATION EXPENSE, EQUIPMENT

POST. BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

Jul 31 Adj 400 400

Jul 31 Clo 400 -0-

208 Solutions Manual

DEPRECIATION EXPENSE, OFFICE FURNITURE

POST. BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

Jul 31 Adj 210 210

Jul 31 Clo 210 -0-

DEPRECIATION EXPENSE, VEHICLES

POST. BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

Jul 31 Adj 650 650

Jul 31 Clo 650 -0-

Req. 3

Aqua Elite, Inc.

Unadjusted Trial Balance

July 31, 2010

ACCOUNT DEBIT CREDIT

Cash $ 17,380Accounts receivable 3,500Supplies 2,360

Prepaid rent 5,400Land 15,000Office furniture 3,300 Equipment 4,700Vehicles 31,000Accounts payable $ 1,840Notes payable 31,000Unearned service revenue 3,600

Waybright Kemp Financial Accounting 1e 209

Common stock 38,500Dividends 3,400Service revenue 18,100Salary expense 3,375Rent expense 1,800Utilities expense 1,225Advertising expense 325Miscellaneous expense 275 Total $93,040 $93,040

Req 4

DATE ACCOUNTS

POST.

REF. Dr. Cr.

July 31 Rent expense 1,800Prepaid rent 1,800

31 Supplies expense 2,010Supplies 2,010

31 Depreciation expense, equipment 400Depreciation expense, furniture 210Depreciation expense, vehicles 650

Accumulated depreciation, equipment 400 Accumulated depreciation, furniture 210 Accumulated depreciation, vehicles 650

31 Accounts receivable 1,900 Service revenue 1,900

31 Salary expense 675Salary payable 675

31 Unearned service revenue 800Service revenue 800

210 Solutions Manual

Req 5

Aqua Elite, Inc.

Adjusted Trial Balance

July 31, 2010

ACCOUNT DEBIT CREDIT

Cash $ 17,380Accounts Receivable 5,400Supplies 350

Prepaid Rent 3,600Land 15,000Office Furniture 3,300 Accumulated depreciation, Office Furniture 210Equipment 4,700Accumulated Depreciation, Equipment 400Vehicles 31,000Accumulated Depreciation, Vehicles 650Accounts Payable 1,840Salaries Payable 675Notes Payable 31,000Unearned Service Revenue 2,800Common stock 38,500Dividends 3,400Service Revenue 20,800Salary Expense 4,050Rent Expense 3,600Supplies Expense 2,010Utilities Expense 1,225Depreciation Expense, Equipment 650Depreciation Expense, Equipment 400Advertising Expense 325Miscellaneous Expense 275Depreciation Expense, Office Furniture 210 Total $96,875 $96,875

Waybright Kemp Financial Accounting 1e 211

Req 6

Aqua Elite, Inc.

Income Statement

Three Months Ended July 31, 2010

Service Revenue 20,800Expenses: Salary Expense $4,050 Rent Expense 3,600 Supplies Expense 2,010 Utilities Expense 1,225 Depreciation Expense, Vehicles 650 Depreciation Expense, Equipment 400 Advertising Expense 325 Miscellaneous Expense 275 Depreciation Expense, Office Furniture 210Total expenses 12,745 Net Income $8,055

212 Solutions Manual

Aqua Elite, Inc.

Statement of retained earnings

Three Months Ended July 31, 2010

Retained earnings, May 1 $0

Add: Net income 8,055

Subtotal 8,055

Less: Dividends 3,400

Retained earnings, July 31 $4,655

Waybright Kemp Financial Accounting 1e 213

Aqua Elite, Inc.

Balance Sheet

July 31, 2010

ASSETS LIABILITIES

Cash $ 17,380 Accounts Payable $ 1,840

Accounts Receivable 5,400 Salaries Payable 675

Supplies 350 Unearned Service Revenue 2,800

Prepaid Rent 3,600 Notes Payable 31,000

Land 15,000

Office Furniture 3,300 Total liabilities 36,315

Less Accum. Depr., Office Furniture (210) 3,090

STOCKHOLDERS’ EQUITY

Equipment 4,700

Less Accum. Depr., Equipmment (400) 4,300

Common Stock 38,500

Vehicles 31,000 Retained Earnings 4,655

Less Accum. Depr., Vehicles (650) 30,350

Total Stockholders’ equity 43,155

Total liabilities and

Total assets $79,470 stockholder’s equity $79,470

214 Solutions Manual

Req7

DATE ACCOUNTS

POST.

REF. Dr. Cr.

July 31Service revenues

20,800

Retained earnings 20,800

31 Retained earnings 12,745

Salary expense 4,050

Rent expense 3,600

Supplies expense 2,010

Depreciation expense 1,260

Utilities expense 1,225

Advertising expense 325

Miscellaneous expense 275

31 Retained earnings 3,400

Dividends 3,400

Waybright Kemp Financial Accounting 1e 215

Req 8

Aqua Elite, Inc.

Post-Closing Trial Balance

July 31, 2010

ACCOUNT DEBIT CREDIT

Cash $ 17,380

Accounts receivable 5,400

Supplies 350

Prepaid rent 3,600

Land 15,000

Office furniture 3,300

Accumulated depreciation, office furniture 210

Equipment 4,700

Accumulated depreciation, equipment 400

Vehicles 31,000

Accumulated depreciation, vehicles 650

Accounts payable 1,840

Salaries payable 675

Unearned service revenue 2,800

Notes payable 31,000

Common stock 38,500

Retained earnings _ 4,655

Total $80,730 $80,730

216 Solutions Manual

Ethics in ActionCase #1

Yes, she is acting unethically, since she needs to record all the adjustments to properly

reflect the current period activity.

It does matter as there will not be a proper matching of total salary expense incurred for

the accounting period in which the revenues were earned. This will overstate the current

period net income and understate the liabilities as of the end of the period. Also, the net

income in the following period will be understated.

The adjusted trial balance should include all the adjustments for the accounting period

because the financial statements are created from the adjusted trial balances. As a result

of Jennifer’s failure to include all the adjustments, the resulting financial statements will

not be accurate and thus could be potentially misleading to any user.

Case #2

Yes, Jim should have informed the banker of the mistake and redone the current year’s

second quarter income statement. Regardless of why the financial statements were

wrong, once Jim became aware of the problem, he should have taken necessary steps to

correct it. The banker is relying on the financial statements to provide accurate

information.

Unethical behavior occurs when there is intentional deception. Mistakes can and do occur

throughout the accounting cycle. Providing wrong financial information purely due to a

mistake does not constitute unethical behavior. However, once Jim became aware of the

problem, he should have immediately taken action to correct the mistake. His silence in

allowing the erroneous income statement to remain unchanged does constitute unethical

behavior.

Regardless of whether or not the loan will be repaid, the fact remains that it was obtained

with false and misleading information of which Jim was fully aware.

Waybright Kemp Financial Accounting 1e 217

Financial Analysis

Req 1 & 3

Accumulated Depreciation Accrued Salaries, Bonus, Vacation, and Other benefits

Bal. 168,067 a 34,952 Bal. 34,952b 22,839 c 29,437Bal. 190,906 Bal. 29,437

Accrued Product Warranty Accrued Cooperative Advertisinga 10,862 Bal. 10,862 a 6,877 Bal. 6,877

d 9,746 e 6,457Bal. 9,746 Bal. 6,457

Other Accrued Liabilitiesa 9,858 Bal. 9,858

f 12,445Bal. 12,445

Req 2

DATE ACCOUNTS

POST.

REF. Dr. Cr.

aAccrued Salaries, Bonus, Vacation, and Other Benefits 34,952Accrued Product Warranty 10,862Accrued Cooperative Advertising 6,877Other Accrued Liabilities 9,858 Cash 62,549

b Depreciation Expense 22,839 Accumulated Depreciation 22,839

c Salary and Benefit Expense 29,437218 Solutions Manual

Accrued Salaries, Bonus, Vacation, and Other Benefits 29,437

d Product Warranty Expense 9,746 Accrued Product Warranty 9,746

e Advertising Expense 6,457 Accrued Cooperative Advertising 6,457

f Miscellaneous Expense 12,445 Other Accrued Liabilities 12,445

Waybright Kemp Financial Accounting 1e 219

Industry Analysis

Both companies are using the accrual basis of accounting. That can be determined by looking at the Consolidated Balance Sheets and recognizing certain accounts which would only be present if the accrual basis of accounting is being used. Some of those accounts are Accounts Receivable, Prepaid Expenses, Accounts Payable and Accrued Expenses. Since these accounts appear on the balance sheet for both companies, that tells the reader of the financial statements that the accrual basis of accounting is being used.

If one company was using the accrual basis of accounting and the other was using the cash basis, it would be much more difficult to compare the two companies. Since the basis of accounting affects the income statement as well as the balance sheet, the timing of the recognition of revenue and expenses would be different. On the balance sheet the company using the cash basis of accounting would be understating liabilities and assets. In order to properly reflect the financial position of a company in accordance with generally accepted accounting principles (GAAP), the accrual basis of accounting should be used.

Small Business Analysis

Since the financial statements of BCS Consultants, Inc. are prepared on the accrual basis of accounting, not paying the employees will have no affect on the net income. In Chapter 2 we learned the accrual basis of accounting recognizes expenses when they are incurred, not when they are paid. Therefore, the payroll expenses will be on the income statement regardless of whether the employees are paid on the last day of the month or the first day of the next month.

Regarding the large insurance payment last month, we learned in Chapter 3 that this is what is known as a deferred expense, meaning we defer recognition of the expense until it’s actually incurred. In other words, Jerry will have to make an adjusting entry at the end of the month to recognize one-sixth of that insurance payment as insurance expense this month. So it will have the affect of decreasing net income when we make the adjusting entry.

That brings us to the cash balance. Jerry is correct in his assumption that not paying the employees until after the first of the month will cause his cash balance to be higher. That will show on the Balance Sheet. But he is incorrect in thinking that the bankers won’t know why his cash balance is higher. When the Banker looks at the balance sheet, he or she will see the liability for the wages payable and realize that a portion of the cash reflected on the balance sheet will be needed to pay this liability.

220 Solutions Manual

Written CommunicationDear Client:

Let me apologize for the error that was committed on this year’s tax return that we prepared for you. Here’s a brief summary of what we failed to do: At the end of every year, the accounting books and records should go through what’s referred to as the closing process. During this process, all of the revenues and expenses of the business are zeroed out, along with the dividend account. This allows these accounts to be set back to zero so that the results of each year can be accounted for separately from the results of the prior year. Because we failed to prepare the closing entries for your business at the end of the first year of operations, the net income from that year ($25,000) carried over to the next year. The second year of operations should have resulted in net taxable income to you of $50,000, but because the closing process was not done, the first and second year were both being shown on this year’s tax return.

Obviously, no one wants to pay income tax twice on the same amount. That’s why it is so vitally important to go through the closing process each and every year, to ensure that every year’s net income is accurately calculated.

Again, I apologize for this error. I should have discovered it during my review of your return. We will immediately correct the situation by preparing the closing entries for year number one and ensure that the closing entries were made for year number two. Then we will issue a new, correct tax return for you at no charge.

Waybright Kemp Financial Accounting 1e 221

Comprehensive Problem

Req 1

Journal Entry

Date Accounts Debit Credit

a. Cash 7,5

00

Delivery Truck Truck 15,0

00

Common stock 22,5

00 Common Stock

b. Supplies 3

00

Accounts payable 3

00

c. Prepaid insurance 1,2

00

Cash 1,2

00

d. Cash 8

00

Service revenue 8

00

e. Accounts receivable 4,5

00

Service revenue 4,5

00

f. Salary expense 6

00

Cash 6

00

g. Cash 1,1

00 Service revenue 1,1

222 Solutions Manual

00

h. Cash 1,5

00

Unearned service revenue 1,5

00

i. Cash 2,5

00

Accounts receivable 2,5

00

j. Fuel expense

80

Accounts payable

80

k. Accounts receivable 1,6

00

Service revenue 1,6

00

l. Rent expense 7

50

Cash 7

50

m. Accounts payable

50

Cash

50

n. Dividends 5

00

Cash 5

00

Waybright Kemp Financial Accounting 1e 223

Req. 2, 4 & 6

Cash Accounts receivable a. 7,500 1,200 c. e. 4,500 2,500 i. d. 800 600 f. k. 1,600

g. 1,100 750 l. Bal 3,600

h. 1,500 50 m. i. 2,500 500 n. Bal

10,300

Supplies Prepaid insurance b. 300 c. 1,200 Bal 300 225 Adj Bal 1,200 200 Adj Bal 75 Bal 1,000

Truck Accumulated depreciation

a. 15,00

0 375 Adj Bal

15,000 375 Bal

Accounts payable Salary payable m. 50 300 b. 600 Adj

8

0 j. 600 Bal

330 Bal

Unearned service revenue Common stock

1,500 h. 22,500 a. Adj 500 1,500 Bal 22,500 Bal

1,000 Bal

224 Solutions Manual

Dividends Retained earnings n. 500 Clo 2,830 8,500 Clo Bal 500 500 Clo Clo 500 Bal -0- 5,170 Bal

Service Revenue Salary Expense 800 d. f. 600

4,500 e. Bal 600

1,100 g. Adj 600

1,600 k. Bal 1,200 1,200 Clo 8,000 Bal Bal -0-

500 Adj Clo 8,500 8,500 Bal

-0- Bal

Depreciation Expense Insurance Expense Adj 375 Adj 200 Bal 375 375 Clo Bal 200 200 Clo Bal -0- Bal -0-

Fuel Expense Rent Expense j. 80 l. 750 Bal 80 80 Clo Bal 750 750 Clo Bal -0- Bal -0-

Supplies Expense Adj 225 Bal 225 225 Clo Bal -0-

Waybright Kemp Financial Accounting 1e 225

Req. 3

Water's Landscaping, Inc.Unadjusted Trial Balance

January 31, 2010 Account Debit Credit Cash 10,300 Accounts receivable 3,600 Supplies 300 Prepaid insurance 1,200 Truck 15,000 Accounts payable 330

Unearned service revenue 1,500

Common stock 22,500 Dividends 500 Service revenue 8,000 Rent expense 750 Salary expense 600 Fuel expense 80 Total $ 32,330 $ 32,330

226 Solutions Manual

Req. 4

Journal Entry

Date Accounts Debit Credit

a. Salary expense 600

Salary payable 600

b. Depreciation expense 375

Accumulated depreciation 375

c. Insurance expense 200

Prepaid insurance 200

d. Supplies expense 225

Supplies 225

e. Unearned service revenue 500

Service revenue 500

Waybright Kemp Financial Accounting 1e 227

Req. 5

Water's Landscaping, Inc.

Adjusted Trial Balance

January 31, 2010

Account Debit Credit

Cash 10,300

Accounts receivable 3,600

Supplies 75

Prepaid insurance 1,000

Truck 15,000

Accumulated depreciation 375

Accounts payable 330

Unearned service revenue 1,000

Salaries payable 600

Common stock 22,500

Dividends 500

Service revenue 8,500

Salary expense 1,200

Rent expense 750

Depreciation expense 375

Supplies expense 225 Insurance expense 200 Fuel expense 80 Total $ 33,305 $ 33,305

228 Solutions Manual

Water's Landscaping, Inc.Income Statement

Month Ended January 31, 2010

Revenue:Service revenue $8,500

Expenses: Salary expense $1,200 Rent expense 750 Depreciation expense 375 Supplies expense 225 Insurance expense 200 Fuel expense 80

Total expenses 2,830Net income $5,670

Water's Landscaping, Inc.Statement of Retained Earnings

Retained earnings, January 31, 2010Retained earnings, January 1, 2010 $0 Add: Net Income 5,670

5,670 Less: Dividends (500)Retained earnings, January 31, 2010 $ 5,170

Water's Landscaping, Inc.Balance Sheet

31-Jan-10ASSETS LIABILITIES

Current liabilities:Cash $10,300 Accounts payable 330Accounts receivable 3,600 Salary payable $600 Supplies 75 Unearned service revenue 1,000Prepaid insurance 1,000 Total Liabilities 1,930Truck 15,000

Less: Accum depreciation -375 14,625 Stockholders' Equity Common stock 22,500 Retained earnings 5,170

Total Stockholders' Equity 27,670

Total Assets $29,600 Total Liabilities and Stockholders' Equity $29,600

Waybright Kemp Financial Accounting 1e 229

Req. 6

Journal Entry

Date Accounts Debit Credit

Service revenue 8,5

00

Retained earnings 8,5

00

Retained earnings 2,8

30

Salary expense 1,2

00

Rent expense 7

50

Depreciation expense

3

75

Supplies expense

2

25

Insurance expense

2

00

Fuel expense

80

Retained earnings 5

00

Dividends 5

00

230 Solutions Manual

Req. 7

Water's Landscaping, Inc.Post-closing Trial Balance

January 31, 2010 Account Debit Credit Cash 10,300 Accounts receivable 3,600 Supplies 75 Prepaid insurance 1,000 Truck 15,000

Accumulated depreciation 375

Accounts payable 330

Unearned service revenue 1,000

Salaries payable 600 Common stock 22,500 Retained earnings 5,170 Total $ 29,975 $ 29,975

Waybright Kemp Financial Accounting 1e 231