Chapter 3 Quanto Multiple-reset Options

25

18 Chapter 3 Quanto Multiple-reset Options 3.1 Framework The content of this chapter is as follows: 3.2 is the price and risk analysis of Type I quanto multiple-reset option; 3.3 is the price and risk analysis of Type II quanto multiple-reset option; 3.4 is the price and risk analysis of Type III quanto multiple-reset option; 3.5 is the price and risk analysis of Type IV quanto multiple-reset option. 3.2 Price and Risk Analysis of Type I Quanto Multiple-reset Option 3.2.1 Pricing Model First of all, we interpret the final payoff of the Type I quanto multiple-reset put. Let { } 1 2 , ,..., n tt t is the date at which the exercise price will be resetted, called the reset date, and 1 n T t + = , which is the maturity of this put. ( ) I QRP T represents the final payoff of the Type I quanto multiple-reset put, which can be written as follows: In which, The Type I quanto multiple-reset put is the multiple-reset put whose final value is computed in foreign currency first at the maturity date, and transferred into the value denominated in domestic currency by the current exchange rate. Consequently, this kind of quanto multiple-reset put is suitable for the investor who invests their money in foreign stocks and pays more attention to the risk of the foreign stock price than the exchange rate. Based on the definition of the final payoff in Eq(3- 1) and (3- 2), we can use the Martingale Pricing method to price the fair price of the Type I quanto multiple-reset { } ( ) () ( ) ( ),0 I n QRP T XT Max K t ST = ⋅ - (3- 1) 1 1 ( ) (( ), ( ),..., ( ), ) n n n Kt Max S t St St K - = (3- 2)

Transcript of Chapter 3 Quanto Multiple-reset Options

18

Chapter 3 Quanto Multiple-reset Options

3.1 Framework

The content of this chapter is as follows: 3.2 is the price and risk analysis of Type

I quanto multiple-reset option; 3.3 is the price and risk analysis of Type II quanto

multiple-reset option; 3.4 is the price and risk analysis of Type III quanto

multiple-reset option; 3.5 is the price and risk analysis of Type IV quanto

multiple-reset option.

3.2 Price and Risk Analysis of Type I Quanto Multiple-reset Option

3.2.1 Pricing Model

First of all, we interpret the final payoff of the Type I quanto multiple-reset put.

Let { }1 2, ,..., nt t t is the date at which the exercise price will be resetted, called the

reset date, and 1nT t += , which is the maturity of this put. ( )IQRP T represents the

final payoff of the Type I quanto multiple-reset put, which can be written as follows:

In which,

The Type I quanto multiple-reset put is the multiple-reset put whose final value is

computed in foreign currency first at the maturity date, and transferred into the value

denominated in domestic currency by the current exchange rate. Consequently, this

kind of quanto multiple-reset put is suitable for the investor who invests their money

in foreign stocks and pays more attention to the risk of the foreign stock price than the

exchange rate.

Based on the definition of the final payoff in Eq(3- 1) and (3- 2), we can use the

Martingale Pricing method to price the fair price of the Type I quanto multiple-reset

{ }( ) ( ) ( ) ( ),0I

nQRP T X T Max K t S T= ⋅ − (3- 1)

1 1( ) ( ( ), ( ),..., ( ), )n n nK t Max S t S t S t K−= (3- 2)

19

put as follows:13

In which, ( )dN ⋅ represents the d-dimensional cdf of joint stndard normal,

iA∑ represents each of the correlation matrix in the d-dimensional cdf of joint

stndard normal. All the parameters in Eq(3- 3) are illustrated as follows:

1

2

( )( )2 ,

sf j i

A

j

s j i

r t t

d i jt t

σ

σ

− −= <

− (3- 4)

2

2

0ln( ) ( )2

sf i

A

K

s i

Sr t

Kdt

σ

σ

+ +=

(3- 5)

2

2

( )( )2 ,

sf i h

A

h

s i h

r t t

d h it t

σ

σ

+ −= <

−

(3- 6)

3

2

( )( )2 ,

sf j i

A

j

s j i

r t t

d i jt t

σ

σ

+ −= <

− (3- 7)

4

2

0ln( ) ( )2

sf j

A

j

s j

Sr t

Kdt

σ

σ

+ −= (3- 8)

13 The detailed derivation is illustrated in Appendix A.

2 2 2

2

1 1

1

3 3

3

4 4

4

5

1 1

( )0 0 0 1 1 1

1

1 1 1

1 1 1

0

0 1 1

( , , ..., ; )

( , ..., ; )

( , ..., ; )

( , ..., ; )

( , ...,

f i

f

A A A

i k i A

nI r T t A A

n i i n Ai

A A

n i i n A

r T A A

n n A

A

n

N d d d

QRP X S e N d d

N d d

Ke N d dX

S N d

−

− −

− + + +=

− + + +

−

+ +

+

∑ ⋅ = ⋅ − − ∑ − − − ∑

⋅ − − ∑+

− − −

∑

5

51; )A

n Ad +

∑

(3- 3)

20

5

2

0ln( ) ( )2

sf j

A

j

s j

Sr t

Kdt

σ

σ

+ += (3- 9)

1 1

2 1

1 2

2 1

1 2

1 1

1 3

1 ...

1 ...

1

i i i i

i i n i

i i i i

i i n i

i i i i

n i n i

A A

t t t t

t t t t

t t t t

t t t t

t t t t

t t t t

+ +

+ +

+ +

+ +

+ +

+ +

− −

− −

− − = = − −

− − − −

∑ ∑

M M O M

L

(3- 10)

1 1

1 1

2

1 1

1

2

1

1

1

i i i

i i

i i i

i i

i i i i

i i

A

t t t t

t t

t t t t

t t t

t t t t

t t t

−

−

− −

− −

− − = −

− − −

∑

L

L

M M O M

L

(3- 11)

1 1

2 1

1 2

2 1

1 2

1 1

54

1

1

1

n

n

n n

A A

t t

t t

t t

t t

t t

t t

+

+

+ +

= =

∑ ∑

L

L

M M O M

L

(3- 12)

If we let 1n = , the reset date be 0t and the maturity of the put be 1nT t += and

put them back into Eq(3- 3), we’ll have the pricing formula of the Type I quanto

single-reset put as follows:

We can compare the Eq(3- 13) with the result in Jiang(2004), and we can find

0 32 1

4 4

4

5 5

5

( )

0 0 0 2 2

2 1 2

0

0 2 1 2

( ) ( ) ( )

( , ; )

( , ; )

f

f

r T t AA AI

k

r T A A

A

A A

A

QRP X S N d e N d N d

Ke N d dX

S N d d

− −

−

= ⋅ ⋅ − − −

⋅ − − ∑ +

− − − ∑

(3- 13)

21

the two pricing formulas are consistent.

On the other hand, we can rewrite Eq(3- 3) as follows:

Based on Eq(3- 14), we can find that the Type I quanto multiple-reset put( IQRP )

is composed of the n units of Contingent Forward-Start Put14 and a conditional

quanto put15. In order to more easily explain how the 2 kinds of options affect the

Type I quanto multiple-reset put, we take a numerical example to illustrate it.

We assume that there exist two kinds of Type I quanto reset option with exercise

price both equal to 5 and whose maturity dates are both the day after three months.

One of them is a Type I quanto single-reset option whose reset date is the day after a

month, represented by *

IQRP . The other one is a Type I quanto double-reset option

whose reset date is the last day of the first and second month, represented by IQRP .

The domestic and foreign risk-free rates are 1.5% and 4.5%. The initial price of the

foreign stock and exchange rate are 5 and 32.5. The data of the volatility of the

foreign stock and exchange rate are as follows: 50%Sσ = , 35%Xσ = , , 0.5S Xρ = . We

substitute all of the parameters we assume into Eq(3- 13), Eq(3- 3)~(3- 12) and Eq(2-

14 That is

I

AiQRP .

15 That is I

BQRP .

2 2 2

2

1 1

1

3 32 2 2

2 3

( )

0 1 1

1 1 10 0

0 1 1 1 1 1

( , , ..., ; )

( , ..., ; )

( , , ..., ; ) ( , ..., ; )

f i

IAi

r T t A A A

i k i A

A AI

n i i n A

A AA A A

i k i A n i i n A

QRP

S e N d d d

N d dQRP X

S N d d d N d d

− −

−

− + + +

− − + + +

∑ ⋅ − − − ∑= ∑ ⋅ − − ∑ 144444444444424444444444 3

( ) { }{ }

4 4

4

5 5

5

1

1

1 1 1

0

0 1 1 1

1

{ ( ) ( ),..., ( ), }

( , ..., ; )

( , ..., ; )

( ) ( ( ) ( )

f

IB

i n

IAi

n

i

r T A A

n n A

A A

n n A

QRP

nI I

Ai B

i

rT Q

i S t Max S t S t K

QRP

Ke N d dX

S N d d

QRP QRP

e E X T S t S T I

=

−

+ +

+ +

=

+−

=

⋅ − − ∑ +

− − − ∑

= +

= ⋅ − ⋅

∑

∑

44

14444444244444443

144444444442444 3

( ) { }{ }1

1

{ ( ),..., ( ), }( ) ( ( )

n

IB

n

i

rT Q

K Max S t S t K

QRP

e E X T K S T I

=

+−

=+ ⋅ − ⋅

∑4444444

144444444424444444443

(3- 14)

22

15) to find the fair price of the Type I quanto single-reset put( *

IQRP ), Type I quanto

multiple-reset put( IQRP ) and Type I quanto put( IQP ) as follows:

Table 1 The Computation of IQRP

(1) 1

I

AQRP 5.7653

(2) 2

I

AQRP 3.8191

(3) 1 2

I I

A AQRP QRP+ (1)+(2) = 9.5844

(4) I

BQRP 11.3926

(5) IQRP (3) + (4) = 20.9770

Table 2 The Price of *

IQRP , IQRP and IQP IQRP 20.9770

*

IQRP 18.7044 IQP 14.7249

According to the result in Table 1, the price of this kind of quanto multiple-reset

put is $20.9770, which can be composed of a series of Contingent Forward-Start Put,

priced at $9.5844, and a conditional quanto put, priced at $11.3926. In addition, based

on Table 2, the price of this kind of quanto multiple-reset put is $20.9770, quanto

single-reset put is $18.7044 and quanto put is $14.7249. The spread between IQRP

and *

IQRP is $2.2726, which can be seen as the reset premium at the second reset

date, and the spread between *

IQRP and IQP is $3.9795, which can be seen as the

reset premium at the first month.

Let’s make more detailed comparison among the Type I quanto put, quanto

single-reset put and quanto multiple-reset put. We can see that the value of the quanto

multiple-reset put decrease along with the increase of the stock price in the early stage,

but it will increase along with the increase of the stock prices when the stock price

exceeds a certain critical value. It is a very different characteristic that the value of the

general put always decreases along with the increase of the stock price. It may be the

main reason that after the foreign stock price exceed the certain critical stock price,

the quanto multiple-reset put starts to be out-of-the-money and has a very large

probability to be resetted, so that the put becomes in-the-money by the reset and its

value is increased, as shown in Figure 3- 1. Furthermore, the price behavior of the

quanto single-reset put is similar to what of the multiple-reset put. However, relative

to that of the multiple-reset put, the price of the single-reset put does not increase very

obviously. Moreover, we can see that the critical stock price of the quanto single-reset

23

put is higher than that of the quanto multiple-reset put, which means along with the

increasing foreign stock price, the value of the quanto multiple-reset put will be

inverse earlier than which of the quanto single-reset put.

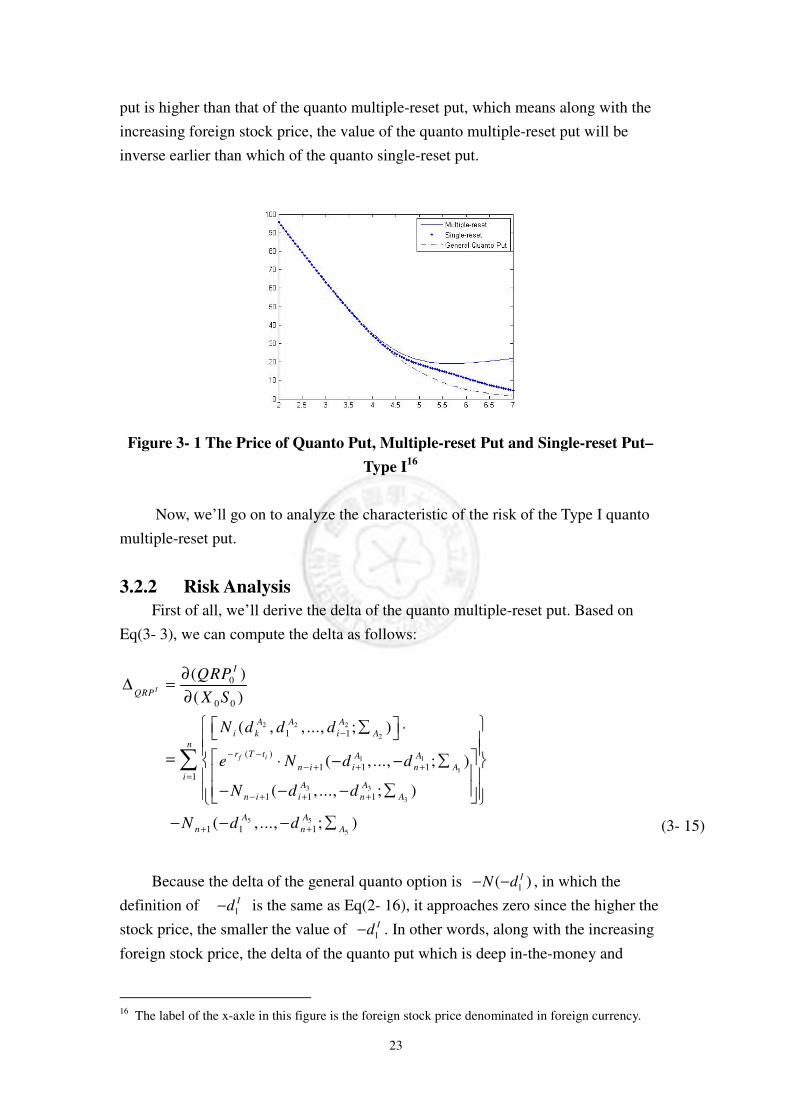

Figure 3- 1 The Price of Quanto Put, Multiple-reset Put and Single-reset Put–

Type I16

Now, we’ll go on to analyze the characteristic of the risk of the Type I quanto

multiple-reset put.

3.2.2 Risk Analysis

First of all, we’ll derive the delta of the quanto multiple-reset put. Based on

Eq(3- 3), we can compute the delta as follows:

Because the delta of the general quanto option is 1( )IN d− − , in which the

definition of 1

Id− is the same as Eq(2- 16), it approaches zero since the higher the

stock price, the smaller the value of 1

Id− . In other words, along with the increasing

foreign stock price, the delta of the quanto put which is deep in-the-money and

16 The label of the x-axle in this figure is the foreign stock price denominated in foreign currency.

2 2 2

2

1 1

1

3 3

3

5 5

5

0

0 0

1 1

( )

1 1 11

1 1 1

1 1 1

( )

( )

( , , ..., ; )

( , ..., ; )

( , ..., ; )

( , ..., ; )

I

f i

I

QRP

A A A

i k i A

nr T t A A

n i i n Ai

A A

n i i n A

A A

n n A

QRP

X S

N d d d

e N d d

N d d

N d d

−

− −

− + + +=

− + + +

+ +

∂∆ =

∂

∑ ⋅ = ⋅ − − ∑ − − − ∑

− − − ∑

∑

(3- 15)

24

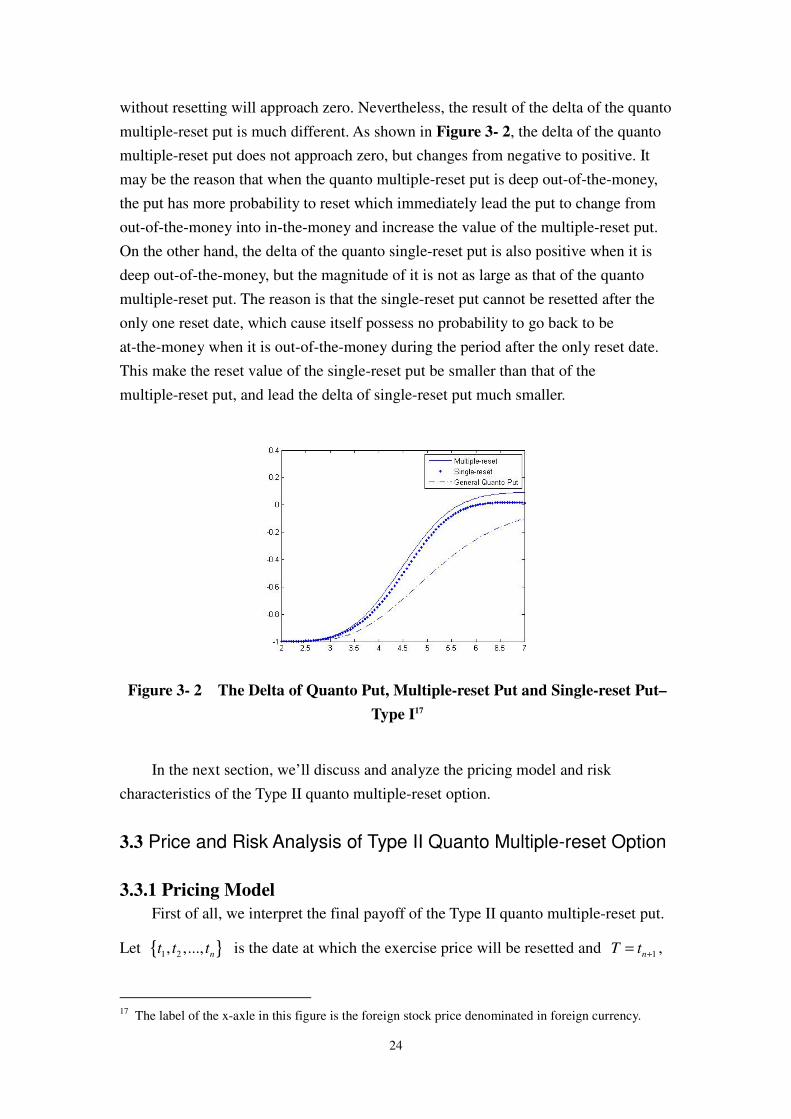

without resetting will approach zero. Nevertheless, the result of the delta of the quanto

multiple-reset put is much different. As shown in Figure 3- 2, the delta of the quanto

multiple-reset put does not approach zero, but changes from negative to positive. It

may be the reason that when the quanto multiple-reset put is deep out-of-the-money,

the put has more probability to reset which immediately lead the put to change from

out-of-the-money into in-the-money and increase the value of the multiple-reset put.

On the other hand, the delta of the quanto single-reset put is also positive when it is

deep out-of-the-money, but the magnitude of it is not as large as that of the quanto

multiple-reset put. The reason is that the single-reset put cannot be resetted after the

only one reset date, which cause itself possess no probability to go back to be

at-the-money when it is out-of-the-money during the period after the only reset date.

This make the reset value of the single-reset put be smaller than that of the

multiple-reset put, and lead the delta of single-reset put much smaller.

Figure 3- 2 The Delta of Quanto Put, Multiple-reset Put and Single-reset Put–

Type I17

In the next section, we’ll discuss and analyze the pricing model and risk

characteristics of the Type II quanto multiple-reset option.

3.3 Price and Risk Analysis of Type II Quanto Multiple-reset Option

3.3.1 Pricing Model

First of all, we interpret the final payoff of the Type II quanto multiple-reset put.

Let { }1 2, ,..., nt t t is the date at which the exercise price will be resetted and 1nT t += ,

17 The label of the x-axle in this figure is the foreign stock price denominated in foreign currency.

25

which is the maturity of this put. ( )IIQRP T represents the final payoff of the Type II

quanto multiple-reset put, which can be written as follows:

In which,

The Type II quanto multiple-reset put is the multiple-reset put whose exercise

price is denominated in domestic currency, which means the underlying asset is the

foreign stock denominated in domestic currency, and resets at each reset point. At

maturity, the final payoff is paid in the domestic currency directly. Consequently, this

kind of quanto multiple-reset put is suitable for the investor who invests their money

in foreign stocks and pays attention to the risk not only of the foreign stock price but

also of the exchange rate. In addition, it can be more easily to understand the value of

this option because it is denominated in domestic currency rather than foreign

currency.

Based on the definition of the final payoff in Eq(3- 16) and (3- 17), we can use

the Martingale Pricing method to price the fair price of the Type II quanto

multiple-reset put as follows: 18

In which, ( )dN ⋅ represents the d-dimensional cdf of joint stndard normal,

18 The detailed derivation is illustrated in Appendix B.

{ }( ) ( ) ( ) ( ),0II

nQRP T Max K t X T S T= − (3- 16)

1 1 1 1( ) ( ( ) ( ), ( ) ( ),..., ( ) ( ), )n n n n nK t Max X t S t X t S t X t S t K− −= (3- 17)

2 2 2

2

1 1

1

3 3

3

4 4

4

5

1 1

( )0 0 0 1 1 1

1

1 1 1

1 1 1

0 0 1 1

( , , ..., ; )

( , ..., ; )

( , ..., ; )

( , ..., ; )

( , ...,

i

A A A

i k i An

II r T t A A

n i i n Ai

A A

n i i n A

A ArT

n n A

A

n

N d d d

QRP X S e N d d

N d d

Ke N d d

X S N d d

−

− −

− + + +=

− + + +

−+ +

+

∑ ⋅ = ⋅ − − ∑

− − − ∑

⋅ − − ∑+

− − −

∑

5

51; )A

n A+

∑

(3- 18)

26

iA∑ represents each of the correlation matrix in the d-dimensional cdf of joint

stndard normal. All the parameters in Eq(3- 18) are illustrated as follows:

1

2

( )( )2 ,

sxj i

A

j

SX j i

r t t

d i jt t

σ

σ

− −= <

− (3- 19)

2

2

0 0ln( ) ( )2SX

iA

K

SX i

X Sr t

Kdt

σ

σ

+ += (3- 20)

2

2

( )( )2 ,

SXi h

A

h

SX i h

r t t

d h it t

σ

σ

+ −= <

− (3- 21)

3

2

( )( )2 ,

sxj i

A

j

sx j i

r t t

d i jt t

σ

σ

+ −= <

− (3- 22)

4

2

0 0ln( ) ( )2sx

jA

j

sx j

X Sr t

Kdt

σ

σ

+ −= (3- 23)

5

2

0 0ln( ) ( )2sx

jA

j

sx j

X Sr t

Kdt

σ

σ

+ += (3- 24)

The definition of sxσ is the same as Eq(2- 4), and 1A∑ ,

2A∑ ,3A∑ ,

4A∑

and 5A∑ is the same as Eq(3- 10)~(3- 12).

If we let 1n = , the reset date be 0t and the maturity of the put be 1nT t += and

put them back into Eq(3- 18), we’ll have the pricing formula of the Type II quanto

single-reset put as follows:

27

We can compare the Eq(3- 25) with the result in Jiang(2004), and we can find

the two pricing formulas are consistent.

On the other hand, we can rewrite Eq(3- 18) as follows:

Similar to the prior section, based on Eq(3- 14), we can find that the Type II

quanto multiple-reset put( IIQRP ) is composed of the n units of Contingent

Forward-Start Put19 and a conditional quanto put20. Similarly, in order to more easily

explain how the 2 kinds of options affect the Type II quanto multiple-reset put, we

take the same numerical example to illustrate it. In this example, because of the

exercise price denominated in domestic currency, we assume the initial exercise price

19 That is

II

AiQRP .

20 That is II

BQRP .

0 32 1

4 4

4

5 5

5

( )

0 0 0 2 2

2 1 2

0 0 2 1 2

( ) ( ) ( )

( , ; )

( , ; )

r T t AA AII

k

A ArT

A

A A

A

QRP X S N d e N d N d

Ke N d d

X S N d d

− −

−

= ⋅ ⋅ − − −

⋅ − − ∑ +

− ⋅ − − ∑

(3- 25)

2 2 2

2

1 1

1

3 32 2 2

2 3

( )

0 1 1

1 1 10 0

0 1 1 1 1 1

( , ,..., ; )

( ,..., ; )

( , ,..., ; ) ( ,..., ; )

i

IIAi

r T t A A A

i k i A

A AIIn i i n A

A AA A A

i k i A n i i n A

QRP

S e N d d d

N d dQRP X

S N d d d N d d

− −

−

− + + +

− − + + +

∑ ⋅ −

− − ∑ = ∑ ⋅ − − ∑ 14444444444442444444444 3

( ) { }{ }

4 4

4

5 5

5

1 1

1

1 1 1

0 0 1 1 1

1

{ ( ) ( ) ( ) ( ),..., ( ) ( ), }

( ,..., ; )

( ,..., ; )

( ( ) ( ) ( ) ( )

IIB

i i n n

n

i

A ArT

n n A

A A

n n A

QRP

nII II

Ai B

i

rT Q

i i X t S t Max X t S t X t S t K

Q

Ke N d d

X S N d d

QRP QRP

e E X t S t X T S T I

=

−+ +

+ +

=

+−

=

⋅ − − ∑ +

− ⋅ − − ∑

= +

= − ⋅

∑

∑

444

144444424444443

( ) { }{ }1 1

1

{ ( ) ( ),..., ( ) ( ), }( ( ) ( )

IIAi

n n

IIB

n

i

RP

rT Q

K Max X t S t X t S t K

QRP

e E K X T S T I

=

+−

=+ − ⋅

∑14444444444444244444444444443

14444444444244444444443

(3- 26)

28

is 05 162.5K X= × = . Substitute all of the parameters we assume into Eq(3- 13),

Eq(3- 3)~(3- 12) and Eq(2- 15) and we’ll find the fair price of the Type II quanto

single-reset put( *

IIQRP ), Type II quanto multiple-reset put( IIQRP ) and Type II quanto

put( IIQP ) as follows:

Table 3 The Computation of IIQRP

(1) 1

II

AQRP 8.9683

(2) 2

II

AQRP 5.8968

(3) 1 2

II II

A AQRP QRP+ (1)+(2) = 14.8651

(4) II

BQRP 17.7289

(5) IIQRP (3) + (4) = 32.5940

Table 4 The Price of *

IIQRP , IIQRP and IIQP IIQRP 32.5940

*

IIQRP 29.0463 IIQP 20.4631

According to the result in Table 3, the price of this kind of quanto multiple-reset

put is $32.5490, which can be composed of a series of Contingent Forward-Start Put,

priced at $14.8651, and a conditional quanto put, priced at $17.7289. In addition,

based on Table 4, the price of this kind of quanto multiple-reset put is $32.5740,

quanto single-reset put is $29.0463 and quanto put is $20.4631. The spread between IIQRP and *

IIQRP is $3.5477, which can be seen as the reset premium at the second

reset date, and the spread between *

IIQRP and IIQP is $8.5832, which can be seen

as the reset premium at the first month.

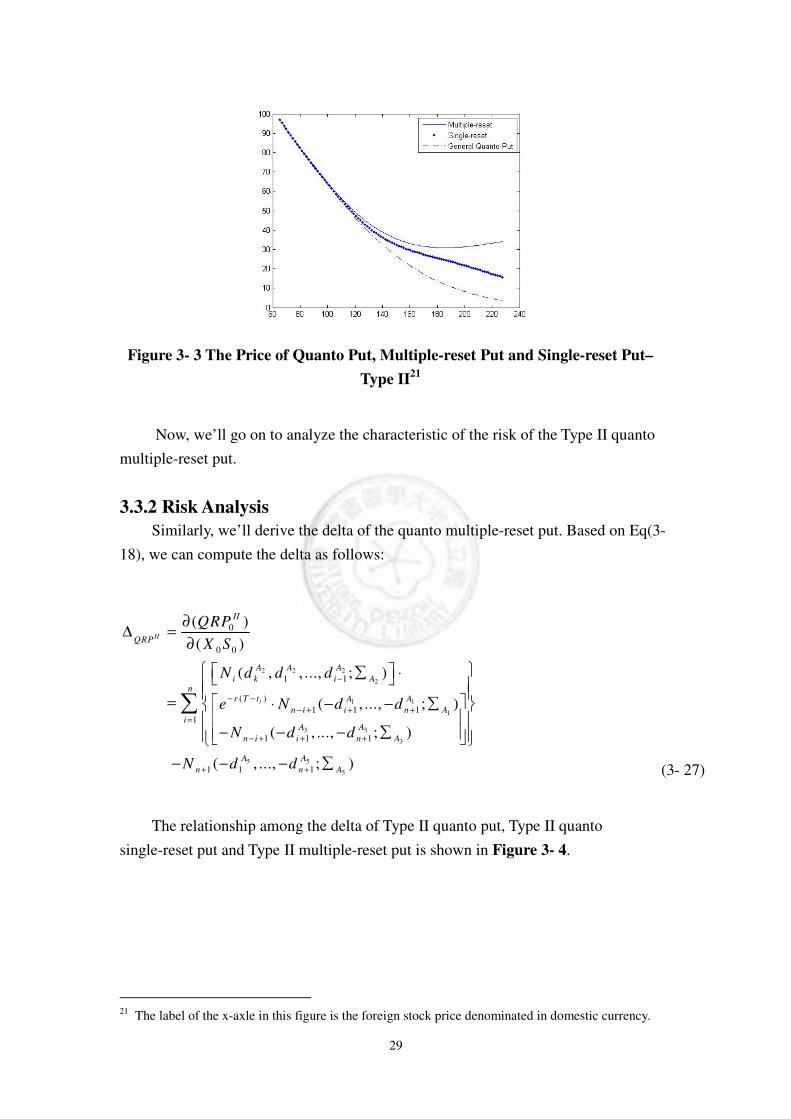

Similar to the prior section, let’s make more detailed comparison among the

Type II quanto put, quanto single-reset put and quanto multiple-reset put. Also, as

shown in Figure 3- 3, we can see that the value of the quanto multiple-reset put

decrease along with the increase of the stock price in the early stage, but it will

increase along with the increase of the stock prices when the stock price exceeds a

certain critical value. It is a very different characteristic that the value of the general

put always decreases along with the increase of the stock price. The main reason is the

same as which we explain in the prior section, so we don’t describe it again.

29

Figure 3- 3 The Price of Quanto Put, Multiple-reset Put and Single-reset Put–

Type II21

Now, we’ll go on to analyze the characteristic of the risk of the Type II quanto

multiple-reset put.

3.3.2 Risk Analysis

Similarly, we’ll derive the delta of the quanto multiple-reset put. Based on Eq(3-

18), we can compute the delta as follows:

The relationship among the delta of Type II quanto put, Type II quanto

single-reset put and Type II multiple-reset put is shown in Figure 3- 4.

21 The label of the x-axle in this figure is the foreign stock price denominated in domestic currency.

2 2 2

2

1 1

1

3 3

3

5 5

5

0

0 0

1 1

( )

1 1 11

1 1 1

1 1 1

( )

( )

( , , ..., ; )

( , ..., ; )

( , ..., ; )

( , ..., ; )

II

i

II

QRP

A A A

i k i An

r T t A A

n i i n Ai

A A

n i i n A

A A

n n A

QRP

X S

N d d d

e N d d

N d d

N d d

−

− −

− + + +=

− + + +

+ +

∂∆ =

∂

∑ ⋅ = ⋅ − − ∑

− − − ∑

− − − ∑

∑

(3- 27)

30

Figure 3- 4 The Delta of Quanto Put, Multiple-reset Put and Single-reset Put–

Type II22

We can see that the delta of the quanto multiple-reset put does not approach zero

when it is deep out-of-the-money, but changes from negative to positive. On the other

hand, the delta of the quanto single-reset put is also positive when it is deep

out-of-the-money, but the magnitude of it is not as large as that of the quanto

multiple-reset put. The main reason is the same as which we explain in the prior

section, so we don’t describe it again.

In the next section, we’ll discuss and analyze the pricing model and risk

characteristics of the Type III quanto multiple-reset option.

3.4 Price and Risk Analysis of Type III Quanto Multiple-reset Option

3.4.1 Pricing Model

Equally, we interpret the final payoff of the Type III quanto multiple-reset put.

Let { }1 2, ,..., nt t t is the date at which the exercise price will be resetted and 1nT t += ,

which is the maturity of this put. ( )IIIQRP T represents the final payoff of the Type

III quanto multiple-reset put, which can be written as follows:

22 The label of the x-axle in this figure is the foreign stock price denominated in domestic currency.

{ }( ) ( ) ( ),0III

nQRP T Max K t S Tχ= ⋅ − (3- 28)

31

In which, χ represents the fixed exchange rate decided initially and

The Type III quanto multiple-reset put is the multiple-reset put whose exercise

price is resetted at each reset point. At maturity, the final payoff is liquidated by

foreign currency and transferred into the domestic value by the fixed exchange rate

decided at the beginning. Consequently, this kind of quanto multiple-reset put is equal

to a multiple-reset put whose underlying asset is the foreign stock and transferred into

domestic value by a fixed rate. By this kind of quanto multiple-reset put, we can not

only protect the put value against the decline of foreign stock price, which cause the

value of the put decrease, but also capture the capital gain of the rise of the foreign

stock price. Therefore, the Type III quanto multiple-reset put is suitable for the

investor who invests their money in foreign stocks and pays attention to the risk not

only of the foreign stock price but also of the exchange rate.

Based on the definition of the final payoff in Eq(3- 28) and (3- 29), we can use

the Martingale Pricing method to price the fair price of the Type III quanto

multiple-reset put as follows23:

In which, ( )dN ⋅ represents the d-dimensional cdf of joint stndard normal,

iA∑ represents each of the correlation matrix in the d-dimensional cdf of joint

stndard normal. All the parameters in Eq(3- 30) are illustrated as follows:

23 The detailed derivation is illustrated in Appendix C.

1 1( ) ( ( ), ( ),..., ( ), )n n nK t Max S t S t S t K−= (3- 29)

, 2 2 2

2

1 1

1

3 3

3

4 4

4

( )

1 1

( )0 1 1 1

1

0 1 1 1

1 1 1

0

( , , ..., ; )

( , ..., ; )

( , ..., ; )

( , ..., ; )

f S X S X i

i

r r t A A A

i k i An

r T t A A

n i i n Ai

III A A

n i i n A

A ArT

n n A

e N d d d

S e N d d

QRP N d d

Ke N d d

S

ρ σ σ

χ

− − +

−

− −

− + + +=

− + + +

−+ +

∑ ⋅ ⋅ − − ∑

= − − − ∑

⋅ − − ∑+

−

∑

, 5 5

5

( )

1 1 1( , ..., ; )f S X S Xr r T A A

n n Ae N d dρ σ σ− − +

+ +

− − ∑

(3- 30)

32

1

2

,( )( )2 ,

sf S X s X j i

A

j

s j i

r t t

d i jt t

σρ σ σ

σ

− − −= <

− (3- 31)

2

2

0,ln( ) ( )

2s

f S X s X iA

K

s i

Sr t

Kdt

σρ σ σ

σ

+ − += (3- 32)

2

2

,( )( )2 ,

sf S X s X i h

A

h

s i h

r t t

d h it t

σρ σ σ

σ

− + −= <

−

(3- 33)

3

2

,( )( )2 ,

sf S X s X j i

A

j

s j i

r t t

d i jt t

σρ σ σ

σ

− + −= <

− (3- 34)

4

2

0,ln( ) ( )

2s

f S X s X jA

j

s j

Sr t

Kdt

σρ σ σ

σ

+ − −= (3- 35)

5

2

0,ln( ) ( )

2s

f S X s X jA

j

s j

Sr t

Kdt

σρ σ σ

σ

+ − += (3- 36)

The definitions of 1A∑ ,

2A∑ ,3A∑ ,

4A∑ and5A∑ are the same as Eq(3-

10)~(3- 12).

If we let 1n = , the reset date be 0t and the maturity of the put be 1nT t += and

put them back into Eq(3- 30), we’ll have the pricing formula of the Type III quanto

single-reset put as follows:

We can compare the Eq(3- 37) with the result in Jiang(2004), and we can find

, 0 2

0 31

4 4

4

, 5 5

5

( )

0

( )

2 2

0 2 1 2

( )

0 2 1 2

( )

( ) ( )

( , ; )

( , ; )

f S X S X

f S X S X i

r r t A

k

r T t AA

A AIII rT

A

r r t A A

A

S e N d

e N d N d

QRP Ke N d d

S e N d d

ρ σ σ

ρ σ σ

χ

− − +

− −

−

− − +

⋅ ⋅ − − −

= ⋅ + ⋅ − − ∑

− ⋅ − − ∑

(3- 37)

33

the two pricing formulas are consistent.

On the other hand, we can rewrite Eq(3- 30) as follows:

Similar to the prior section, based on Eq(3- 38), we can find that the Type III

quanto multiple-reset put( IIIQRP ) is composed of the n units of Contingent

Forward-Start Put24 and a conditional quanto put25. Similarly, in order to more easily

explain how the 2 kinds of options affect the Type III quanto multiple-reset put, we

take the same numerical example to illustrate it. In this example, we assume the fixed

rate decided at the beginning is 0 32.5Xχ = = . Substitute all of the parameters we

assume into Eq(3- 37), Eq(3- 30)~(3- 36) and Eq(2- 24) and we’ll find the fair price

of the Type III quanto single-reset put( *

IIIQRP ), Type III quanto multiple-reset

put( IIIQRP ) and Type III quanto put( IIIQP ) as follows:

Table 5 The Computation of IIIQRP

(1) 1

III

ARP26 0.1779

24 That is

III

AiRP .

25 That is III

BRP .

26 The values of 1

III

ARP , 2

III

ARP and III

BRP are denominated in foreign currency.

, 2 2 2

2

1 1

1

3 3

3

( )

1 1

( )0 1 1 1

1

1 1 1

0

( , , ..., ; )

( , ..., ; )

( , ..., ; )

f S X S X i

i

IIIAi

r r t A A A

i k i An

r T t A A

n i i n Ai

A A

n i i n AIII

RP

rT

n

e N d d d

S e N d d

N d d

QRP

Ke N

ρ σ σ

χ

− − +

−

− −

− + + +=

− + + +

−

∑ ⋅ ⋅ − − ∑ − − − ∑

=

⋅+

∑

144444444424444444443

( )

4 4

4

, 5 5

5

B

1 1 1

( )

0 1 1 1

1

{ ( ) ( ),

( , ..., ; )

( , ..., ; )

( ( ) ( )

f S X S X

III

i n

A A

n A

r r T A A

n n A

RP

nII II

Ai B

i

rT Q

i S t Max S t

d d

S e N d d

RP RP

e E S t S T I

ρ σ σ

χ

χ

+ +

− − +

+ +

=

+−

=

− − ∑

− − − ∑

= ⋅ +

− ⋅

=

∑

144444444424444444443

{ }{ }

( ) { }{ }

1

1

..., ( ), }1

{ ( ),..., ( ), }( ( )

IIIAi

n

IIIB

n

S t K

i

RP

rT Q

K Max S t S t K

RP

e E K S T I

=

+−

=

+ − ⋅

∑144444444424444444443

1444444442444444443

(3- 38)

34

(2) 2

III

ARP 0.1121

(3) 1 2

III III

A ARP RP+ (1) + (2) = 0.2900

(4) III

BRP 0.3942

(5) IIIQRP [ ](3) (4)χ ⋅ + = 22.2356

Table 6 The Price of *

IIIQRP , IIIQRP and IIIQP IIIQRP 22.2356

*

IIIQRP 19.8926 IIIQP 15.0265

According to the result in Table 5, the price of this kind of quanto multiple-reset

put is $22.2356, which can be composed of a series of Contingent Forward-Start Put,

priced at 0.2900, which is denominated in foreign currency, and a conditional quanto

put, priced at 0.3942, which is also denominated in foreign currency. In addition,

based on Table 6, the price of this kind of quanto multiple-reset put is $22.2356,

quanto single-reset put is $19.8926 and quanto put is $15.0625. The spread between IIIQRP and *

IIIQRP is $2.1523, which can be seen as the reset premium at the

second reset date, and the spread between *

IIIQRP and IIIQP is $4.8701, which can

be seen as the reset premium at the first month.

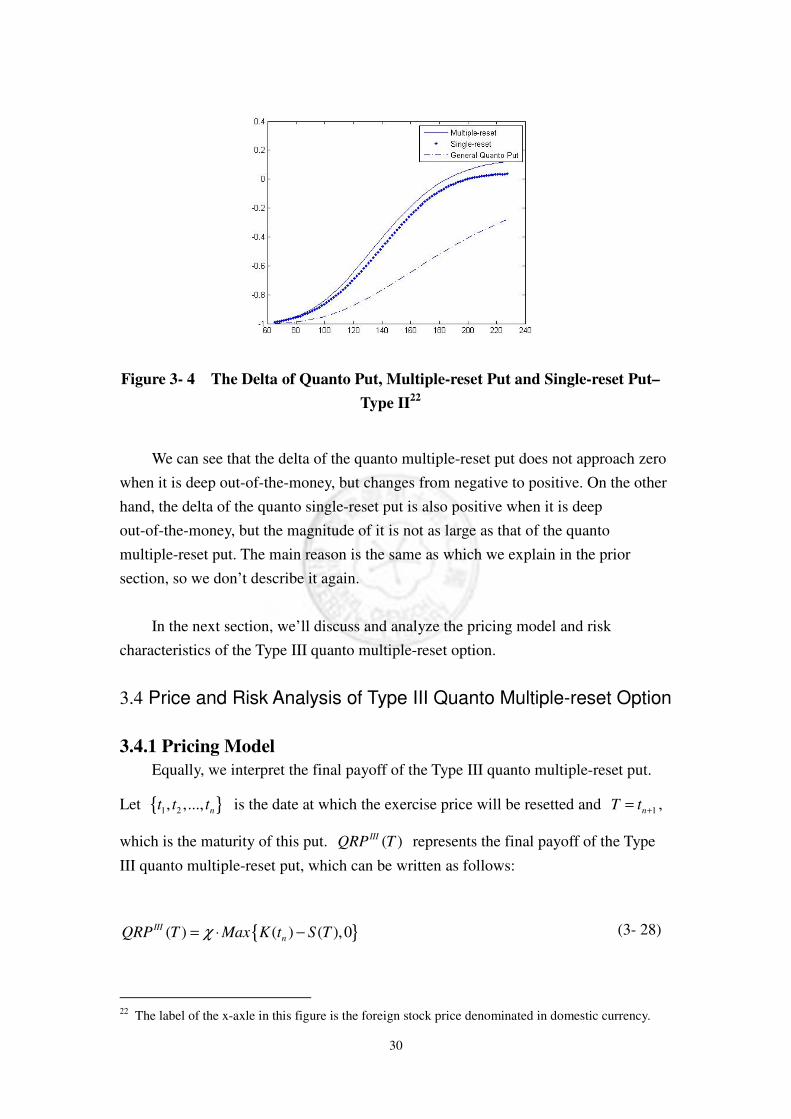

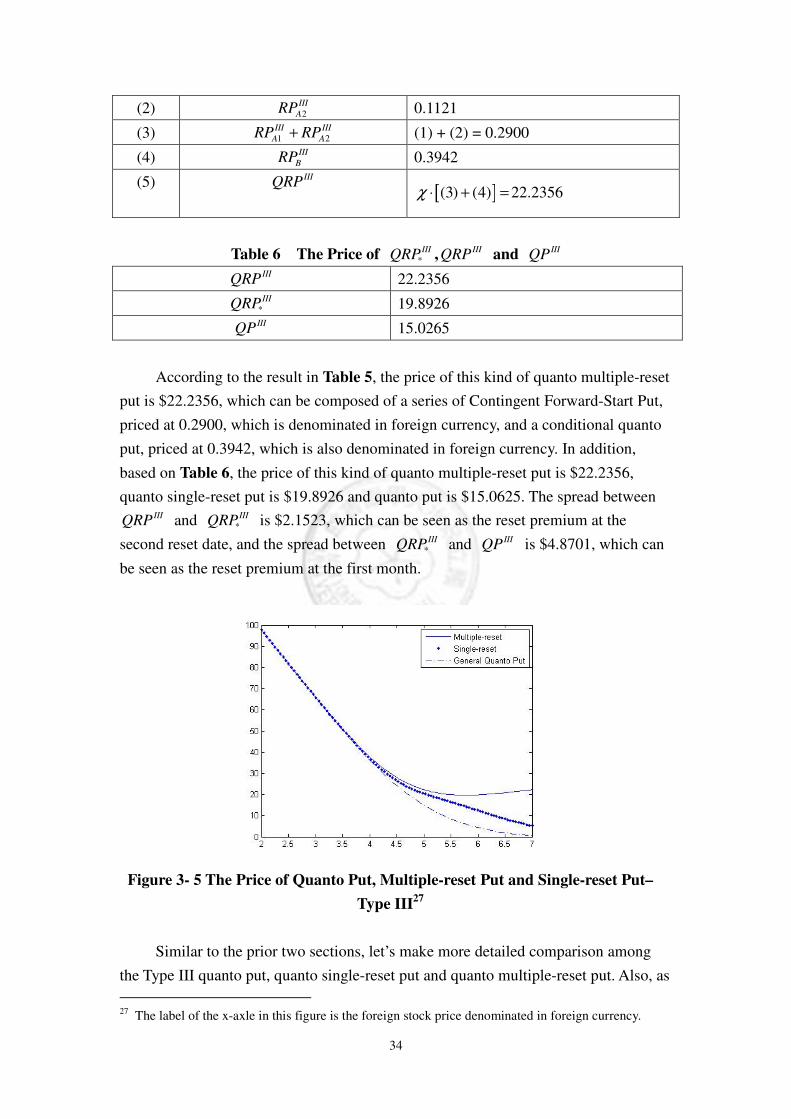

Figure 3- 5 The Price of Quanto Put, Multiple-reset Put and Single-reset Put–

Type III27

Similar to the prior two sections, let’s make more detailed comparison among

the Type III quanto put, quanto single-reset put and quanto multiple-reset put. Also, as

27 The label of the x-axle in this figure is the foreign stock price denominated in foreign currency.

35

shown in Figure 3- 5, we can see that the value of the quanto multiple-reset put

decrease along with the increase of the stock price in the early stage, but it will

increase along with the increase of the stock prices when the stock price exceeds a

certain critical value. It is a very different characteristic that the value of the general

put always decreases along with the increase of the stock price. The main reason is the

same as which we explain in the prior section, so we don’t describe it again.

Now, we’ll go on to analyze the characteristic of the risk of the Type III quanto

multiple-reset put.

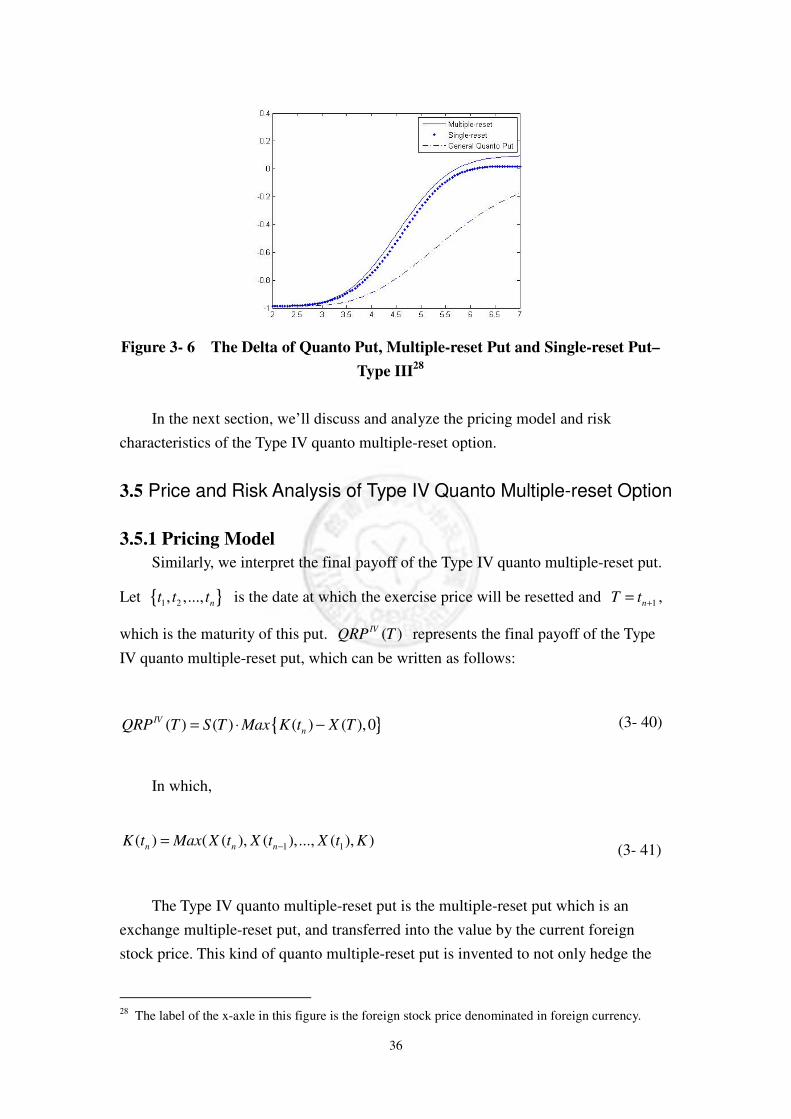

3.4.2 Risk Analysis

Similarly, we’ll derive the delta of the quanto multiple-reset put. Based on Eq(3-

30), we can compute the delta as follows:

The relationship among the delta of Type III quanto put, Type III quanto

single-reset put and Type III multiple-reset put is shown in Figure 3- 6. We can see

that the delta of the quanto multiple-reset put does not approach zero when it is deep

out-of-the-money, but changes from negative to positive. On the other hand, the delta

of the quanto single-reset put is also positive when it is deep out-of-the-money, but

the magnitude of it is not as large as that of the quanto multiple-reset put. The main

reason is the same as which we explain in the prior section, so we don’t describe it

again.

, 2 2 2

2

1 1

1

3 3

3

,

0

0

( )

1 1

( )

1 1 11

1 1 1

( )

1

( )

( )

( , , ..., ; )

( , ..., ; )

( , ..., ; )

III

f S X S X i

i

f S X S X

III

QRP

r r t A A A

i k i An

r T t A A

n i i n Ai

A A

n i i n A

r r T

n

QRP

S

e N d d d

e N d d

N d d

e N

ρ σ σ

ρ σ σ

χ

− − +

−

− −

− + + +=

− + + +

− − +

+

∂∆ =

∂

∑ ⋅

= ⋅ − − ∑ − − − ∑

−

∑

5 5

51 1( , ..., ; )A A

n Ad d +− − ∑

(3- 39)

36

Figure 3- 6 The Delta of Quanto Put, Multiple-reset Put and Single-reset Put–

Type III28

In the next section, we’ll discuss and analyze the pricing model and risk

characteristics of the Type IV quanto multiple-reset option.

3.5 Price and Risk Analysis of Type IV Quanto Multiple-reset Option

3.5.1 Pricing Model

Similarly, we interpret the final payoff of the Type IV quanto multiple-reset put.

Let { }1 2, ,..., nt t t is the date at which the exercise price will be resetted and 1nT t += ,

which is the maturity of this put. ( )IVQRP T represents the final payoff of the Type

IV quanto multiple-reset put, which can be written as follows:

In which,

The Type IV quanto multiple-reset put is the multiple-reset put which is an

exchange multiple-reset put, and transferred into the value by the current foreign

stock price. This kind of quanto multiple-reset put is invented to not only hedge the

28 The label of the x-axle in this figure is the foreign stock price denominated in foreign currency.

{ }( ) ( ) ( ) ( ),0IV

nQRP T S T Max K t X T= ⋅ − (3- 40)

1 1( ) ( ( ), ( ),..., ( ), )n n nK t Max X t X t X t K−= (3- 41)

37

downward exchange risk but also allow the investor to capture the capital gain from

the appreciation of the exchange rate. Consequently, it is suitable for the investor who

invests their money in foreign stocks and pays more attention to the risk of the

exchange rate than the foreign stock price.

Based on the definition of the final payoff in Eq(3- 40) and (3- 41), we can use

the Martingale Pricing method to price the fair price of the Type IV quanto

multiple-reset put as follows29:

Similarly, in which, ( )dN ⋅ represents the d-dimensional cdf of joint stndard

normal, iA∑ represents each of the correlation matrix in the d-dimensional cdf of

joint stndard normal. All the parameters in Eq(3- 42) are illustrated as follows:

1

2

,( )( )2 ,

Xf S X s X j i

A

j

X j i

r r t t

d i jt t

σρ σ σ

σ

− − + −= <

− (3- 43)

2

2

0,ln( ) ( )

2X

f S X S X iA

K

X i

Xr r t

Kdt

σρ σ σ

σ

+ − + += (3- 44)

2

2

,( )( )2 ,

Xf S X S X i h

A

h

X i h

r r t t

d h it t

σρ σ σ

σ

− + + −= <

− (3- 45)

3

2

,( )( )2 ,

Xf S X S X j i

A

j

X j i

r r t t

d i jt t

σρ σ σ

σ

− + + −= <

− (3- 46)

29 The detailed derivation is illustrated in Appendix D.

2 2 2

2

, 1 1

1

3 3

3

, 4

1 1

( )( )0 0 0 1 1 1

1

1 1 1

( )

1 1

0

( , ,..., ; )

( ,..., ; )

( ,..., ; )

( ,...,

f S X S X i

f S X S X

A A A

i k i A

nIV r r T t A A

n i i n Ai

A A

n i i n A

r r T A

n n

N d d d

QRP S X e N d d

N d d

Ke N d dS

ρ σ σ

ρ σ σ

−

− − + −

− + + +=

− + + +

− − +

+ +

∑ ⋅ = ⋅ − − ∑ − − − ∑

⋅ − −+

∑

4

4

5 5

5

1

0 1 1 1

; )

( ,..., ; )

A

A

A A

n n AX N d d+ +

∑

− − − ∑

(3- 42)

38

4

2

0,ln( ) ( )

2X

f S X S X jA

j

X j

Xr r t

Kdt

σρ σ σ

σ

+ − − += (3- 47)

5

2

0,ln( ) ( )

2X

f S X S X jA

j

X j

Xr r t

Kdt

σρ σ σ

σ

+ − + += (3- 48)

The definitions of 1A∑ ,

2A∑ ,3A∑ ,

4A∑ and5A∑ are the same as Eq(3-

10)~(3- 12).

If we let 1n = , the reset date be 0t and the maturity of the put be 1nT t += and

put them back into Eq(3- 42), we’ll have the pricing formula of the Type IV quanto

single-reset put as follows:

We can compare the Eq(3- 49) with the result in Jiang(2004), and we can find

the two pricing formulas are consistent.

On the other hand, we can rewrite Eq(3- 49) as follows:

, 0 32 1

, 4 4

4

5 5

5

( )( )

0 0 0 2 2

( )

2 1 2

0

0 2 1 2

( ) ( ) ( )

( , ; )

( , ; )

f S X S X

f S X S X

r r T t AA AIV

k

r r T A A

A

A A

A

QRP S X N d e N d N d

Ke N d dS

X N d d

ρ σ σ

ρ σ σ

− − + −

− − +

= ⋅ ⋅ − − −

⋅ − − ∑ +

− − − ∑

(3- 49)

39

Based on Eq(3- 50), we can find that the Type IV quanto multiple-reset

put( IVQRP ) is composed of the n units of Contingent Forward-Start Put30 and a

conditional quanto put31. Similarly, in order to more easily explain how the 2 kinds of

options affect the Type IV quanto multiple-reset put, we take the same numerical

example to illustrate it. In this example, because K is the exercise price of the

exchange rate put, we assume it is 0 32.5K X= = . Substitute all of the parameters we

assume into Eq(3- 49), Eq(3- 42)~(3- 48) and Eq(2- 28) and we’ll find the fair price

of the Type IV quanto single-reset put( *

IVQRP ), Type IV quanto multiple-reset

put( IVQRP ) and Type IV quanto put( IVQP ) as follows:

Table 7 The Computation of IVQRP

(1) 1

IV

AQRP 3.8702

(2) 2

IV

AQRP 2.6005

(3) 1 2

IV IV

A AQRP QRP+ (1) + (2) = 6.4706

(4) IV

BQRP 7.5621

(5) IVQRP 14.0328

30 That is

IV

AiQRP .

31 That is IV

BQRP .

, 2 2 2

2

1 1

1

3 32 2 2

2 3

( )( )

0 1 1

1 1 10 0

0 1 1 1 1 1

( , , ..., ; )

( , ..., ; )

( , , ..., ; ) ( , ..., ; )

f S X S X i

IVAi

r r T t A A A

i k i A

A AIV

n i i n A

A AA A A

i k i A n i i n A

QRP

X e N d d d

N d dQRP S

X N d d d N d d

ρ σ σ− − + −

−

− + + +

− − + + +

∑ ⋅ − − − ∑= ∑ ⋅ − − ∑ 144444444 2

( )

, 4 4

4

5 5

5

1

( )

1 1 1

0

0 1 1 1

1

{ ( ) ( )

( , ..., ; )

( , ..., ; )

( ) ( ( ) ( )

f S X S X

IVB

i n

n

i

r r T A A

n n A

A A

n n A

QRP

nIV IV

Ai B

i

rT Q

i X t Max X t

Ke N d dS

X N d d

QRP QRP

e E S T X t X T I

ρ σ σ

=

− − +

+ +

+ +

=

+−

=

⋅ − − ∑ +

− − − ∑

= +

= ⋅ − ⋅

∑

∑

4444 4444444444443

144444444424444444443

{ }{ }

( ) { }{ }

1

1

,..., ( ), }1

{ ( ),..., ( ), }( ) ( ( )

IVAi

n

IVB

n

X t K

i

QRP

rT Q

K Max X t X t K

QRP

e E S T K X T I

=

+−

=+ ⋅ − ⋅

∑14444444444244444444443

144444444424444444443

(3- 50)

40

Table 8 The Price of *

IVQRP , IVQRP and IVQP IVQRP 14.0328

*

IVQRP 12.4890 IVQP 10.1264

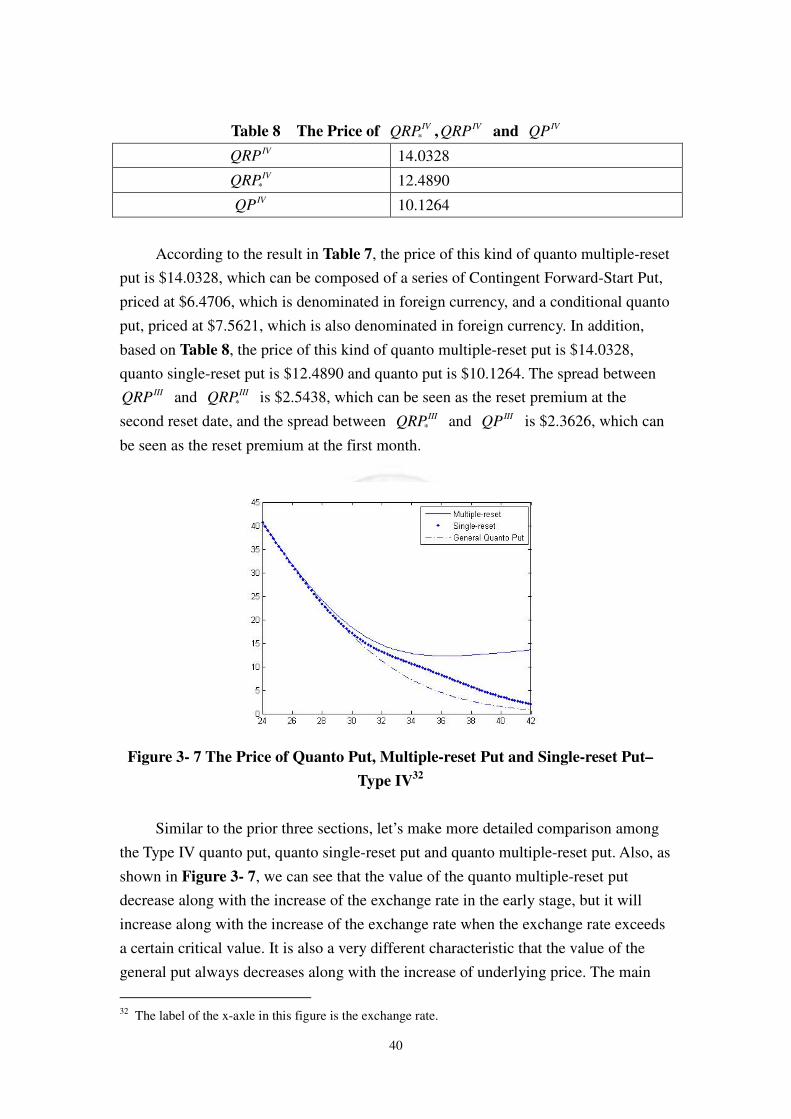

According to the result in Table 7, the price of this kind of quanto multiple-reset

put is $14.0328, which can be composed of a series of Contingent Forward-Start Put,

priced at $6.4706, which is denominated in foreign currency, and a conditional quanto

put, priced at $7.5621, which is also denominated in foreign currency. In addition,

based on Table 8, the price of this kind of quanto multiple-reset put is $14.0328,

quanto single-reset put is $12.4890 and quanto put is $10.1264. The spread between IIIQRP and *

IIIQRP is $2.5438, which can be seen as the reset premium at the

second reset date, and the spread between *

IIIQRP and IIIQP is $2.3626, which can

be seen as the reset premium at the first month.

Figure 3- 7 The Price of Quanto Put, Multiple-reset Put and Single-reset Put–

Type IV32

Similar to the prior three sections, let’s make more detailed comparison among

the Type IV quanto put, quanto single-reset put and quanto multiple-reset put. Also, as

shown in Figure 3- 7, we can see that the value of the quanto multiple-reset put

decrease along with the increase of the exchange rate in the early stage, but it will

increase along with the increase of the exchange rate when the exchange rate exceeds

a certain critical value. It is also a very different characteristic that the value of the

general put always decreases along with the increase of underlying price. The main

32 The label of the x-axle in this figure is the exchange rate.

41

reason is the same as which we explain in the prior three sections, so we don’t

describe it again.

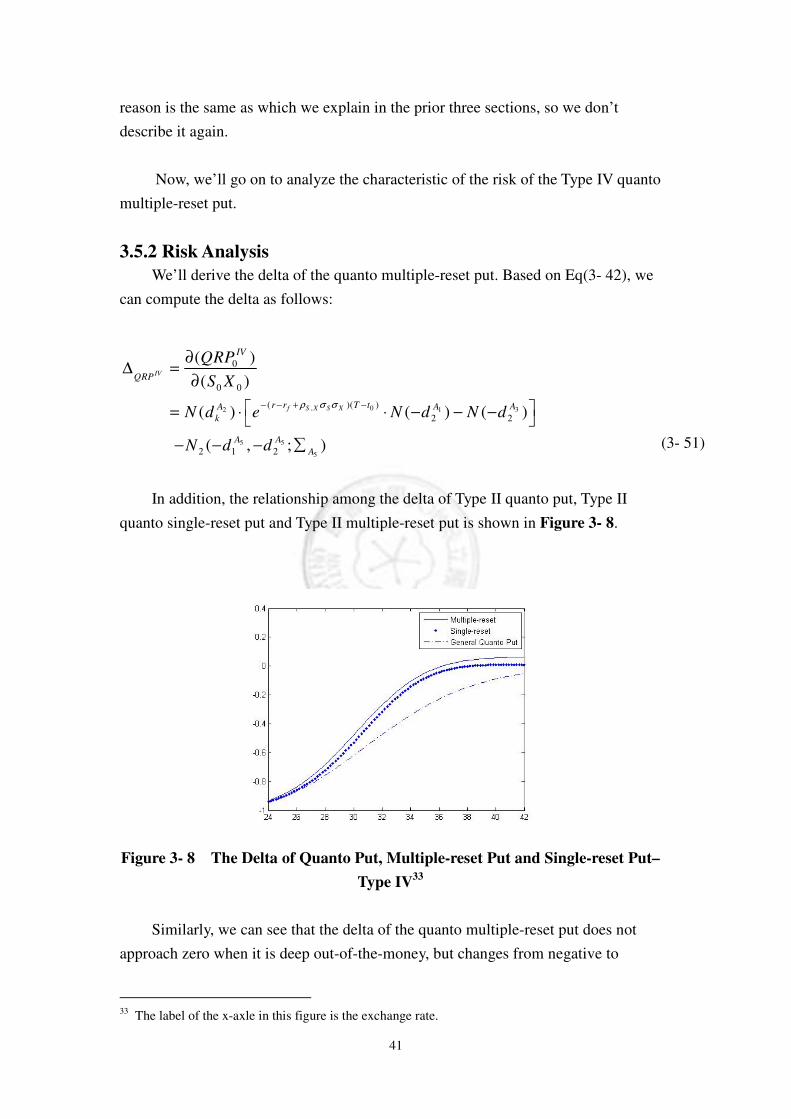

Now, we’ll go on to analyze the characteristic of the risk of the Type IV quanto

multiple-reset put.

3.5.2 Risk Analysis

We’ll derive the delta of the quanto multiple-reset put. Based on Eq(3- 42), we

can compute the delta as follows:

In addition, the relationship among the delta of Type II quanto put, Type II

quanto single-reset put and Type II multiple-reset put is shown in Figure 3- 8.

Figure 3- 8 The Delta of Quanto Put, Multiple-reset Put and Single-reset Put–

Type IV33

Similarly, we can see that the delta of the quanto multiple-reset put does not

approach zero when it is deep out-of-the-money, but changes from negative to

33 The label of the x-axle in this figure is the exchange rate.

, 0 32 1

5 5

5

0

0 0

( )( )

2 2

2 1 2

( )

( )

( ) ( ) ( )

( , ; )

IV

f S X S X

IV

QRP

r r T t AA A

k

A A

A

QRP

S X

N d e N d N d

N d d

ρ σ σ− − + −

∂∆ =

∂

= ⋅ ⋅ − − −

− − − ∑

(3- 51)

42

positive. On the other hand, the delta of the quanto single-reset put is also positive

when it is deep out-of-the-money, but the magnitude of it is not as large as that of the

quanto multiple-reset put. The main reason is the same as which we explain in the

prior three sections, so we don’t describe it again.