Chapter 3 I

59

Chapter 3 Introduction to Risk Management

-

date post

06-Dec-2015 -

Category

Documents

-

view

218 -

download

0

Transcript of Chapter 3 I

Chapter 3

Introduction to Risk Management

3-2

Accident 1• April 2010

On April 5, the Massey Energy-owned Upper Big Branch mine in Montcoal, West Virginia, exploded, killing 29 of the 31 miners at the site. The accident, the worst in the United States since Kentucky's Finley Coal Company disaster in 1970, was blamed on high levels of methane, which caused the explosion after a spark was generated from the mine's mantrip, the shuttle used to transport workers through the mine. The tragedy brought to light Massey's track of safety violations and fatalities. In 2009, Massey Energy was fined $382,000 for serious violations, some in reference to improper ventilation. In the month before the explosion, authorities cited the mine for 57 safety infractions, and the day before the explosion, the mine received two additional citations. The Upper Big Branch coal mine disaster put a critical spotlight on the inadequacies of worker safety in U.S. mines.

3-3

Accident 2

• May 2010Just before midnight on May 8, an explosion occurred at Russia's largest underground coal mine near Kemerovo Oblast, due to a buildup of methane gas. The mine, owned by Russian coal company Raspadskaya, had a history of safety violations and deaths. In March 2001, a methane explosion killed four miners and injured six, and in January 2010 one worker was killed after a partial mine collapse. The most recent explosion killed 66 …………………

3-4

Accident 3, 4…

• August 2010Part of the San Jose copper/gold mine near Copiapo, Chile, collapsed on August 5, leaving 33 miners trapped 2,300 feet below ground for 69 days. The mine, owned by Compania Minera San Esteban, had a history of instability and accidents, including one death. Between 2004 and 2010, the company received 42 fines for breaching safety regulations……..

• October 2010On October 16, 37 men were killed in an explosion caused by a gas leak at a coal mine located in China's Henan Province.

• http://www.rmmag.com

3-5

Recent accident

• On 13 May 2014, an explosion at a coal mine in Soma, Manisa, Turkey, caused an underground mine fire, which burned until 15 May. In total, 301 people were killed

• http://en.wikipedia.org/wiki/Soma_mine_disaster

3-6

Worlds Worst Mining Disaster• Benxihu Colliery (the mine was in territory invaded

by the Japanese) labor. On April 26, 1942, a coal-dust explosion - 1,549 dead.

• Courrières mine disaster• A coal-dust explosion ripped through this mine in

Northern France on March 10, 1906. 1,099 died,• Japan coal mining disasters• On Dec. 15, 1914, a gas explosion at the Mitsubishi

Hojyo coal mine in Kyūshū, Japan, killed 687, • Welsh coal mining disasters (UK)• Oct. 14, 1913, the death toll was 439,

• http://worldnews.about.com/od/disasters/tp/Worlds-Worst-Mining-Disasters.htm

3-7

Recent case: UBS trader Adoboli held over $2bn loss• UBS has become the latest bank to experience a

rogue trading scandal as it revealed that a 31-year-old trader had been arrested in London on suspicion of blowing a $2bn hole in its books, exactly three years after Lehman Brothers collapsed

• UBS warned that the discovery – which drew parallels with the €4.9bn ($6.8bn) hit caused to Société Générale by Jérôme Kerviel in 2008 – could push the group into a loss for the third quarter

• September 15, 2011 9:35 pm FT.com.

Note: UBS 2014second-quarter profit before tax CHF 1.2 billion (about $1.3 billion)

3-8

FT said

• The revelation that a trader in “Delta One” – an area of derivative trading activity that is one of the only remaining ways for banks to take big bets with their own money – could cause such a catastrophic loss has prompted calls for fresh restrictions on investment banks.

• “Management doesn’t understand what’s going on in the Delta One desks,” said Terry Smith, chief executive of Tullett Prebon, the interdealer broker. “If you sat down with a CEO and asked them to please explain what happens they would try but they couldn’t give you an accurate answer because they don’t understand.”

3-9

Why these types of serious accident keep on happening? What do you think?

• Is there any risk management, apart from the issues of safety?

• Too expensive for risk management, or they just ignore it?

• Safety precaution costs outweighed expected losses in monetary term? – Judge Learned Hand's rules (BPL formula) to be

covered in the Pinto case– Let’s look at The Ford Pinto Case.– If you were the CEO of Ford….– http://www.youtube.com/watch?v=kBdfcR-8hEY

right to kill?

3-10

Agenda

• Meaning of Risk Management• Objectives of Risk Management• Steps in the Risk Management Process• Benefits of Risk Management• Personal Risk ManagementOutcomes• Understand the processes and techniques

used to deal with different types of risk• Apply rules to the Pinto case

3-11

Meaning of Risk Management

• Risk Management is a process that identifies loss exposures faced by an organization and selects the most appropriate techniques for treating such exposures

• A loss exposure is any situation or circumstance in which a loss is possible, regardless of whether a loss occurs (covered)– E.g., a plant that may be damaged by an

earthquake, or an automobile that may be damaged in a collision

• New forms of risk management consider both pure and speculative loss exposures

3-12

Objectives of Risk Management

• Risk management has objectives before and after a loss occurs

• Pre-loss objectives:– Prepare for potential losses in the most

economical way– Reduce anxiety (Are what mine owners doing?)– Meet any legal obligations

How about riots in local government in the mainland? High speed train accident.Building of a new power plant causing new pollution?

3-13

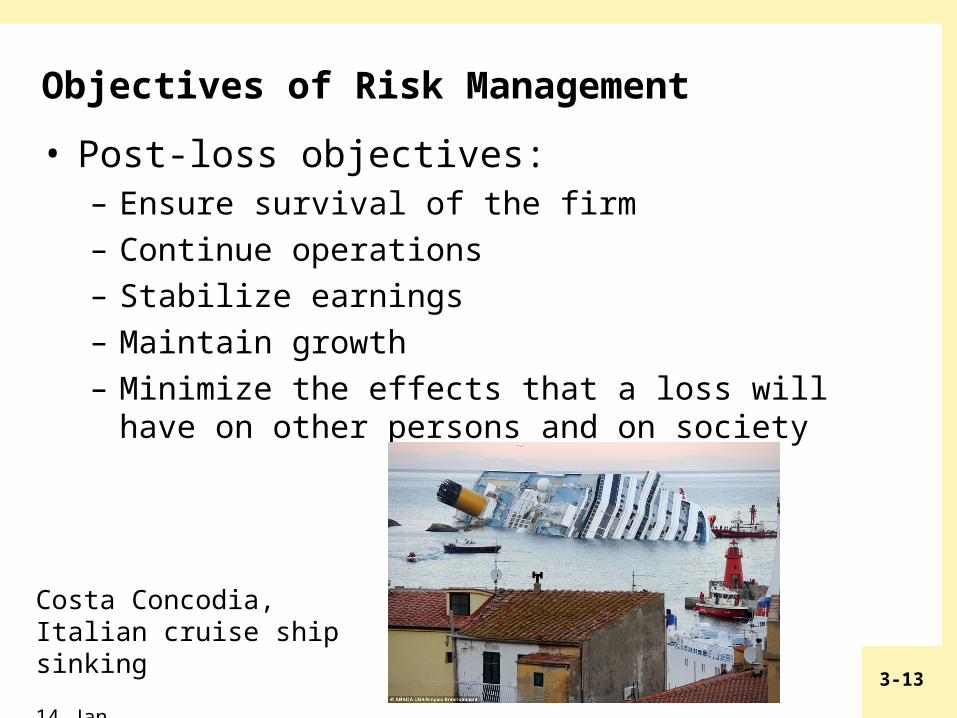

Objectives of Risk Management

• Post-loss objectives:– Ensure survival of the firm– Continue operations– Stabilize earnings– Maintain growth– Minimize the effects that a loss will have on

other persons and on society

Costa Concodia, Italian cruise ship sinking

14 Jan. 2012,http://www.dailymail.co.uk

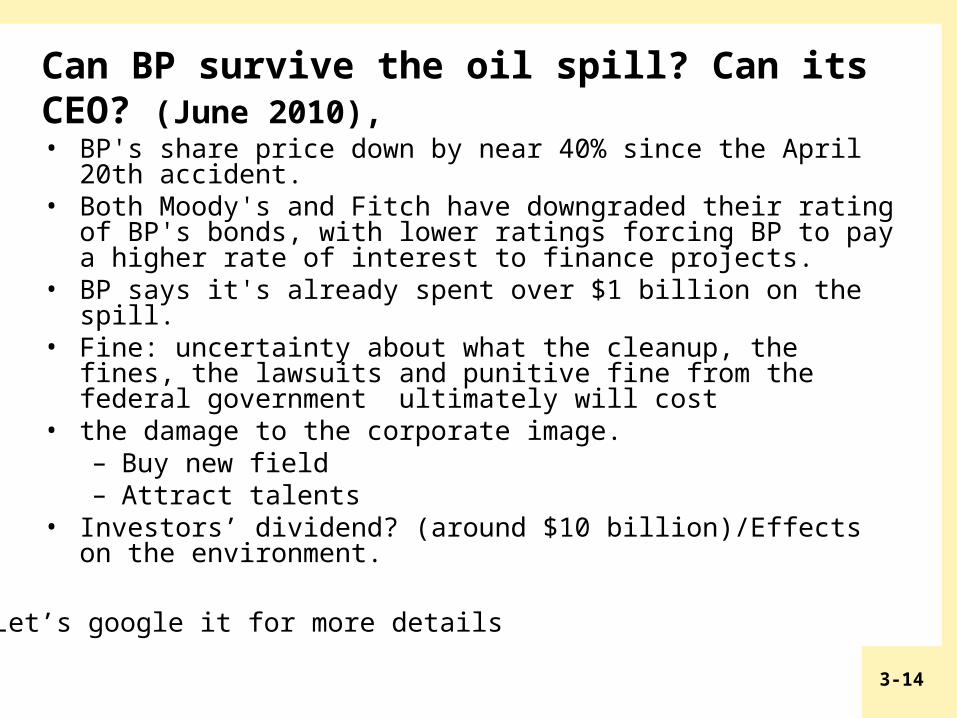

3-14

Can BP survive the oil spill? Can its CEO? (June 2010), • BP's share price down by near 40% since the April 20th

accident. • Both Moody's and Fitch have downgraded their rating of BP's

bonds, with lower ratings forcing BP to pay a higher rate of interest to finance projects.

• BP says it's already spent over $1 billion on the spill. • Fine: uncertainty about what the cleanup, the fines, the

lawsuits and punitive fine from the federal government ultimately will cost

• the damage to the corporate image. – Buy new field– Attract talents

• Investors’ dividend? (around $10 billion)/Effects on the environment.

Let’s google it for more details

3-15

References

-The 1989 Exxon Valdez spill (occurred in Prince William Sound, Alaska), which eventually cost ExxonMobil $4.5 billion (some report $7 billion), including clean-up costs, legal settlements and punitive damages.

-Dividend: about $10 billion-BP will generate about $25 billion to $34 billion (of

operating income) in year 2010, depending on oil prices ranging from $60 per barrel to $80 per barrel. Would you do insurance based on above figures after adjusting

for inflation?

3-16

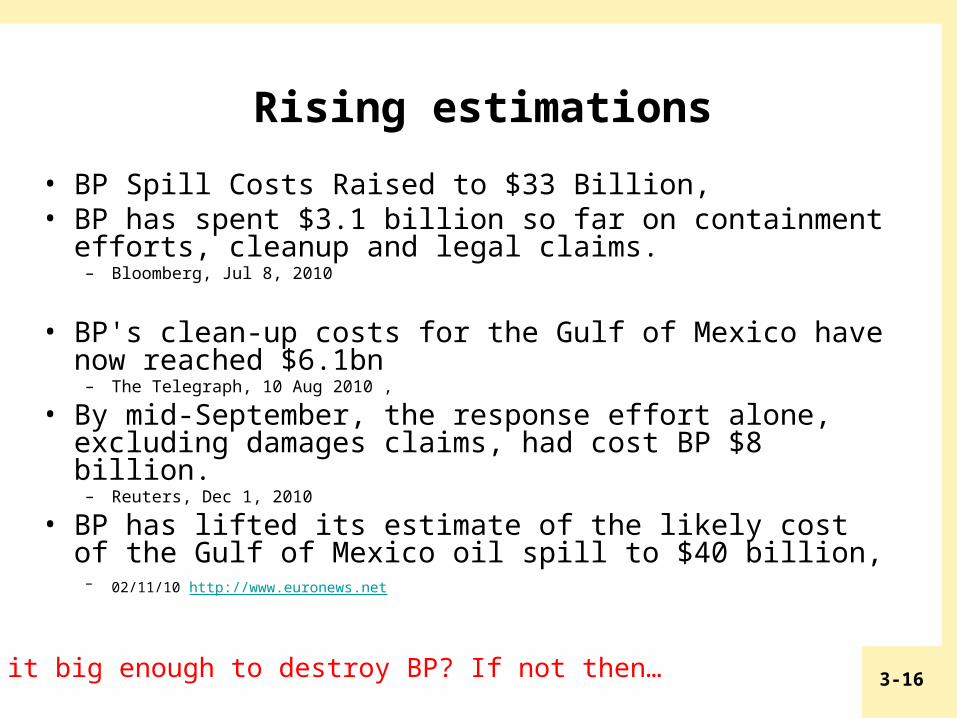

Rising estimations

• BP Spill Costs Raised to $33 Billion, • BP has spent $3.1 billion so far on containment efforts, cleanup

and legal claims. – Bloomberg, Jul 8, 2010

• BP's clean-up costs for the Gulf of Mexico have now reached $6.1bn

– The Telegraph, 10 Aug 2010 ,

• By mid-September, the response effort alone, excluding damages claims, had cost BP $8 billion.

– Reuters, Dec 1, 2010

• BP has lifted its estimate of the likely cost of the Gulf of Mexico oil spill to $40 billion,

– 02/11/10 http://www.euronews.net

Is it big enough to destroy BP? If not then…

3-17

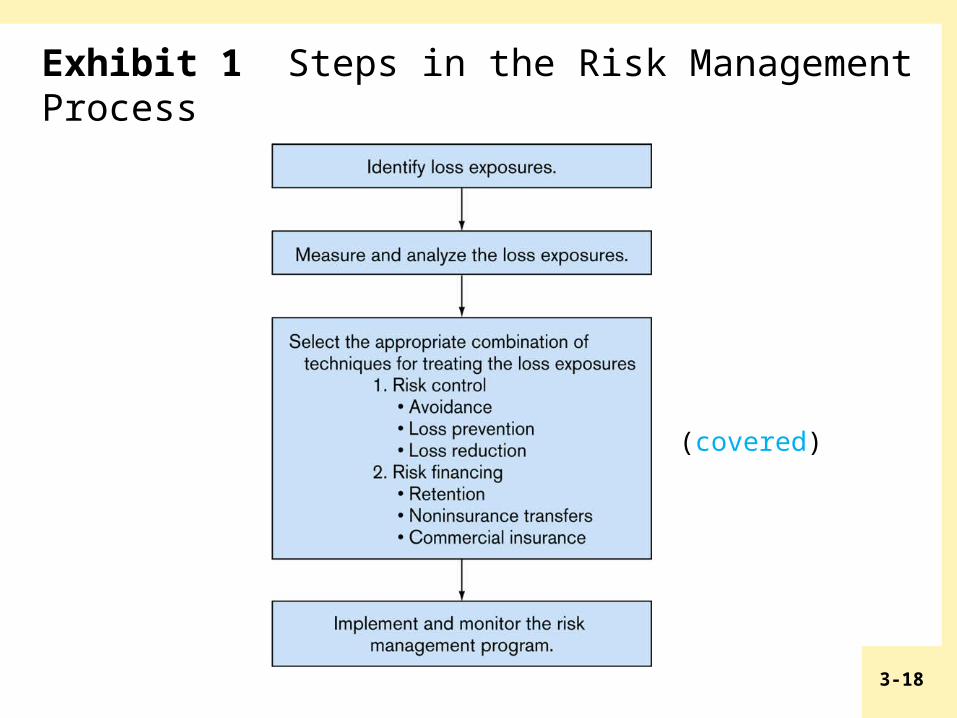

Risk Management Process

• Identify potential losses

• Measure and analyze the loss exposures

• Select the appropriate combination of techniques for treating the loss exposures

• Implement and monitor the risk management program

3-18

Exhibit 1 Steps in the Risk Management Process

(covered)

3-19

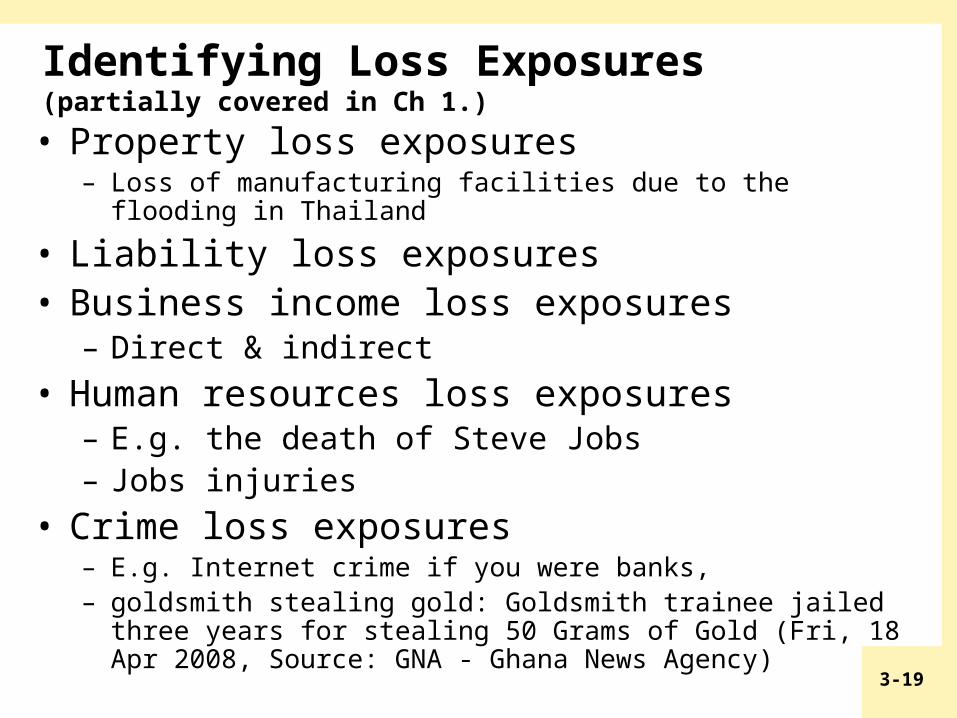

Identifying Loss Exposures (partially covered in Ch 1.)

• Property loss exposures – Loss of manufacturing facilities due to the flooding in

Thailand

• Liability loss exposures• Business income loss exposures

– Direct & indirect

• Human resources loss exposures– E.g. the death of Steve Jobs– Jobs injuries

• Crime loss exposures– E.g. Internet crime if you were banks, – goldsmith stealing gold: Goldsmith trainee jailed three years

for stealing 50 Grams of Gold (Fri, 18 Apr 2008, Source: GNA - Ghana News Agency)

3-20

Identifying Loss Exposures cont’d• Employee benefit loss exposures

– E.g. Failure to contribute to MPF– Retirement plan exposures like large corps. not

enough fund for pension• Foreign loss exposures

– Exchange rate risks– Kidnapping of key personnel (Chinese

engineers)– Political risks or terrorism

• Intangible property loss exposures– Damages to intellectual property; software or

movie industry– Damages of company image (Milk powder

producer in the mainland)Boeing reported strong fourth-quarter results on Wednesday but forecast lower-than-expected profits for 2012 because of rising pension costs and… January 25, 2012, The New York Times

3-21

Types of Risk Exposure in practice

• Have a quick look at

“Industry risk report auto manufacturing Risk & Insurance.htm”

3-22

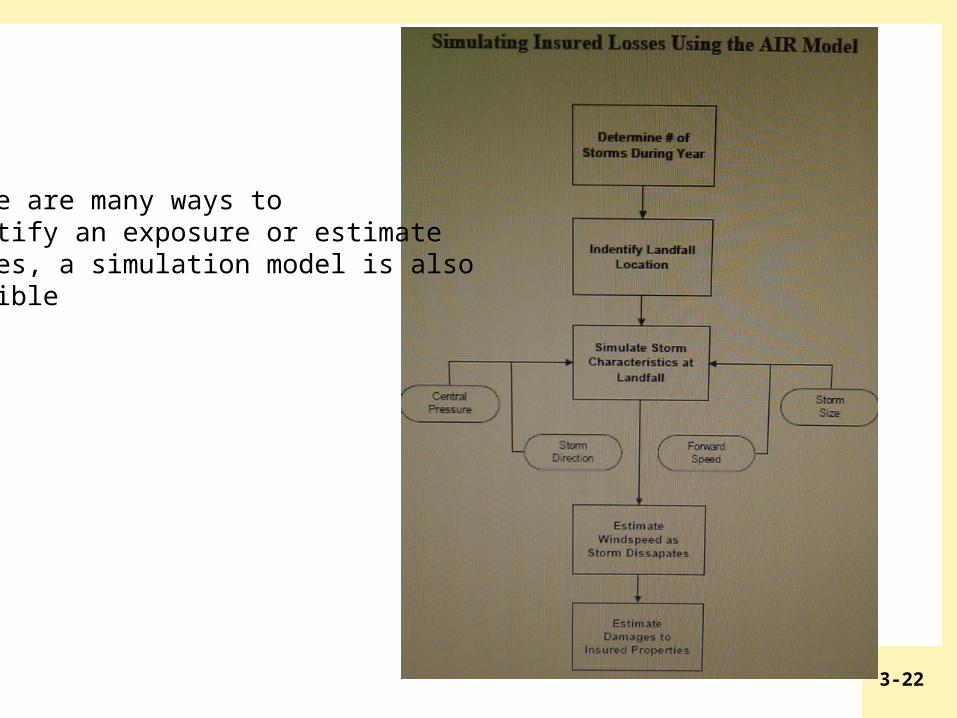

There are many ways to identify an exposure or estimate losses, a simulation model is also possible

3-23

Identifying Loss Exposures cont’d

• Failure to comply with government rules and regulations– A Russian court convicted Mikhail B. Khodorkovsky, the

embattled tycoon and founder of the Yukos oil company, of criminal charges today and sentenced him to nine years in a prison camp

– Mr. Khodorkovsky, 41, who had been the wealthiest man in Russia until he publicly challenged President Vladimir V. Putin, was found guilty of six charges, including fraud and tax evasion. (C.J. Chivers and Erin Arvedlund , New York Times May 31st, 2005 http://www.corpwatch.org )

Or should this be under political risks?

3-24

Identifying Loss Exposures• Risk Managers have several sources of information to

identify loss exposures:– Questionnaires– Physical inspection– Flowcharts

• show production flow to identify potential loss exposure e.g. the IC chips of mobile phone may of high demand (see the case next slide)

– Financial statements• E.g. Huge capital expenditure leads to collapse of

FuJi(1175), see 1175FujiFinancialStatement 06-08.xls– Historical loss data

• Industry trends and market changes can create new loss exposures.– e.g., exposure to acts of terrorism

How about the UBS case?

3-25

Your Leadership Approach Must Anticipate CrisisFeb 10, 2009

• Early Recognition Can Keep Crisis From Becoming Chaos

• As reported in the Wall Street Journal, the reversal of fortunes started with a lightning strike at a semiconductor plan owned by Philips Electronics. The resulting fire was out in ten minutes, but its market-changing disruptive consequences to Nokia and Ericsson were not apparent for weeks to come. Both Nokia and Ericsson depended on the same chip produced by the plant, but Nokia prospered while Ericsson suffered tremendously. In fact, Ericsson ended up permanently shuttering its cell phone manufacturing and relying upon subcontractors.

http://garybclayton.com/leadership/2009/02/crisis-chaos-leadership-approach-2/

3-26

Your Leadership Approach Must Anticipate Crisis cont’d• The difference in business outcome can be attributed to

the leadership culture differences between the two companies. Nokia’s culture promoted flexibility through open and rapid communication inside and outside the company. Ericsson’s culture fostered complacency and rigidity.

• Nokia was alert for emerging problems, with a philosophy of “We encourage bad news to travel fast. We don’t want to hide problems.” Nokia noticed changes to its supply stream within 72 hours of the fire and quickly elevated its awareness to the head of the division. When the enormity of the disruption became apparent just two weeks later (chip production disrupted for an unknown time into the future), Nokia assembled a crisis management team and immediately swung into action. The team created alternative designs to eliminate the part in some products and worked actively with Philips to create emergency sourcing for the component.

3-27

Measure and Analyze Loss Exposures

• Estimate the frequency and severity of loss for each type of loss exposure – Loss frequency refers to the probable number of losses that

may occur during some given time period– Loss severity refers to the probable size of the losses that

may occur

• Once loss exposures are analyzed, they can be ranked according to their relative importance

• Loss severity is more important than loss frequency:– The maximum possible loss is the worst loss that could

happen to the firm during its lifetime– The probable maximum loss is the worst loss that is likely

to happen

3-28

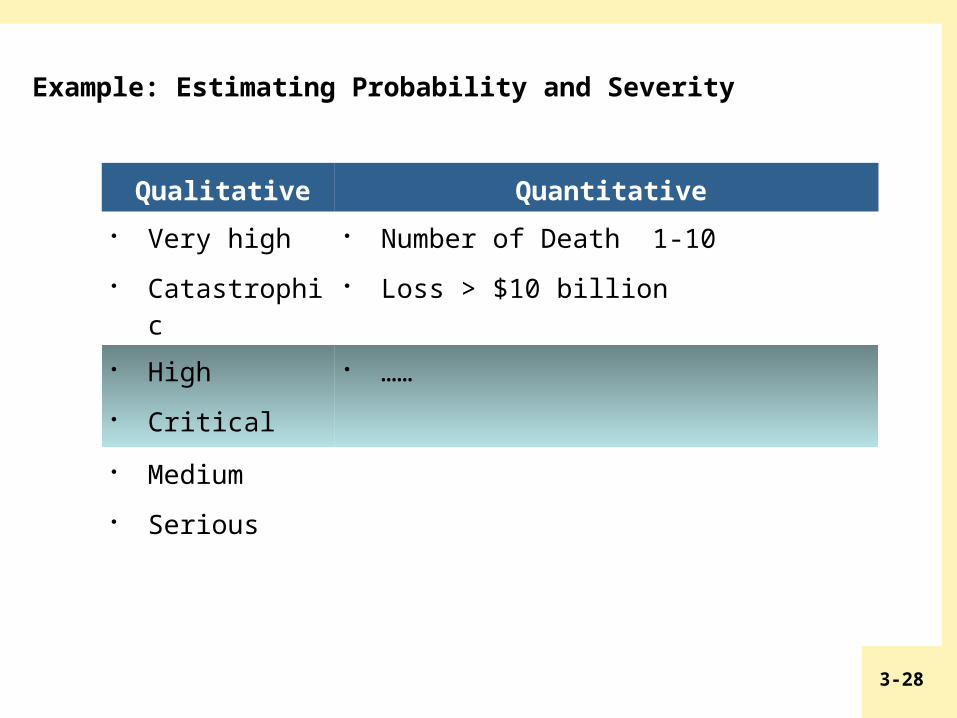

Qualitative Quantitative

Very high

Catastrophic

Number of Death 1-10

Loss > $10 billion

High

Critical

……

Medium

Serious

Example: Estimating Probability and Severity

3-29

Select the Appropriate Combination of Techniques for Treating the Loss Exposures Covered in Ch.1

• Risk control refers to techniques that reduce the frequency and severity of losses

• Methods of risk control include:– Avoidance– Loss prevention– Loss reduction

• Avoidance means a certain loss exposure is never acquired, or an existing loss exposure is abandoned– The chance of loss is reduced to zero– It is not always possible, or practical, to avoid all losses

3-30

Select the Appropriate Combination of Techniques for Treating the Loss Exposures

– Loss prevention refers to measures that reduce the frequency of a particular loss• e.g., installing safety features on

hazardous products– Loss reduction refers to measures that reduce

the severity of a loss after is occurs• e.g., installing an automatic sprinkler

system

Covered in Ch.1

3-31

Select the Appropriate Risk Management Technique

• Risk financing refers to techniques that provide for the funding of losses

• Methods of risk financing include:– Retention– Non-insurance Transfers– Commercial Insurance

Partially covered in Ch.1

3-32

Risk Financing Methods: Retention• Retention means that the firm retains part or all of

the losses that can result from a given loss– Retention is effectively used when:

• No other method of treatment is available• The worst possible loss is not serious (BP violated it?)• Losses are highly predictable

– The retention level is the dollar amount of losses that the firm will retain

• A financially strong firm can have a higher retention level than a financially weak firm

• The maximum retention may be calculated as a percentage of the firm’s net working capital

The loss of BP is estimated to be in billions. It can onlyreceive at most millions from its captive, BP “keeps” most of thelosses to herself.

3-33

Risk Financing Methods: Retention

– A risk manager has several methods for paying retained losses:

• Current net income: losses are treated as current expenses

• Unfunded reserve: losses are deducted from a bookkeeping account

• Funded reserve: losses are deducted from a liquid fund

• Credit line: funds are borrowed to pay losses as they occur

3-34

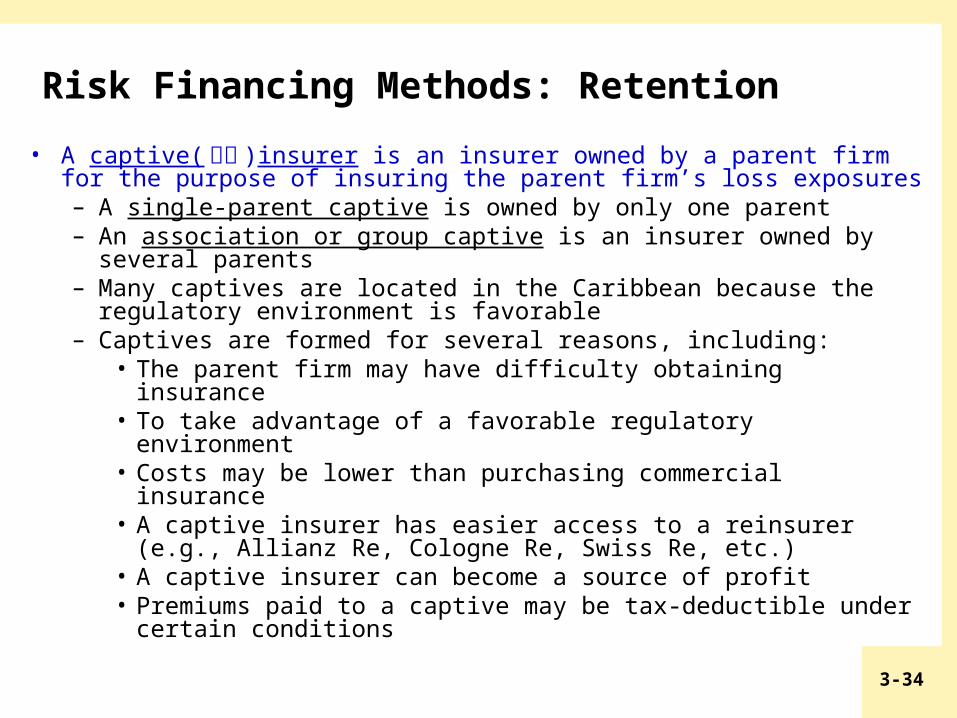

Risk Financing Methods: Retention

• A captive(自保 )insurer is an insurer owned by a parent firm for the purpose of insuring the parent firm’s loss exposures– A single-parent captive is owned by only one parent– An association or group captive is an insurer owned by

several parents– Many captives are located in the Caribbean because the

regulatory environment is favorable– Captives are formed for several reasons, including:

• The parent firm may have difficulty obtaining insurance• To take advantage of a favorable regulatory environment• Costs may be lower than purchasing commercial

insurance• A captive insurer has easier access to a reinsurer (e.g.,

Allianz Re, Cologne Re, Swiss Re, etc.)• A captive insurer can become a source of profit • Premiums paid to a captive may be tax-deductible under

certain conditions

3-35

PetroChina (00857) to invest $3B in captive insurance JV 05 Jan 2012 Infocast

• PetroChina (00857) announced that it has agreed with its controlling shareholder, China National Petroleum Corporation (CNPC), on the establishment of CNPC Captive Insurance Company Limited, a captive insurance company, that has a registered capital of RMB5 billion (HK$6.135 billion).

The JV company would be held as to 51% by CNPC and 49% by PetroChina and its registered capital will be contributed as to RMB2.55 billion (HK$3.129 billion) by CNPC and RMB2.45 billion (HK$3.006 billion) by PetroChina.

3-36

PetroChina (00857) to invest $3B in captive insurance JV 05 Jan 2012 Infocast cont’d

• It is proposed that the JV company should principally engage in property insurance, liability insurance, credit insurance, guarantee insurance, short term health insurance, accident insurance, the reinsurance of those insurance businesses and the use of insurance funds.

PetroChina said that it decided to set up the JV company for the purpose of satisfying its risk management requirements of highly risky and overseas projects, reasonably mitigating its operational risks, balancing the business insurance costs, improving its ability to withstand the risks, and ensuring the insurance enforcement effect after the occurrence of certain covered incidents.

3-37

REASONS FOR THE FORMATION OF THE JOINT VENTURE COMPANY (read it in your spare time)Due to the feature of high risks and speciality in the petroleum industry, the normal business insurance cannot cover all business operations of the Company at the current stage. For the purpose of satisfying its risk management requirements of highly risky and overseas projects, reasonably mitigating its operational risks, balancing the business insurance costs, improving its ability to withstand the risks, and ensuring the insurance enforcement effect after the occurrence of certain covered incidents, the Company decides to set up the Joint Venture Company and the detailed reasons are as follows:(a) the formation of the Joint Venture Company is helpful to provide more comprehensive,safer and more efficient insurance services for the Company and its subsidiaries;(b) the formation of the Joint Venture Company is able to steadily support the segmentaloperations and overseas businesses of the Company which increases its overallcapabilities to react to risks;(c) the formation of the Joint Venture Company is able to save the total insurance costs of the Company which will decrease operation costs; and(d) the formation of the Joint Venture Company is helpful for the Company to accumulateexperiences to withstand the risks, to broaden the channel of reinsurance, and to upgradeits specialised risk management operations which will finally maximise the shareholders'interests of the Company as a whole.

http://www.hkexnews.hk/listedco/listconews/sehk/2012/0104/LTN201201041173.pdf

3-38

Captive Insurance Domiciles Worldwide

Domiciles Number

Bermuda 1150

Cayman Islands 694

Vermont 524

Guernsey 410

British Virgin Islands 350

Barbados 257

Luxembourg 219

Dublin 214

Total 4842

Source: Business Insurance - 2005 captive spotlight

3-39

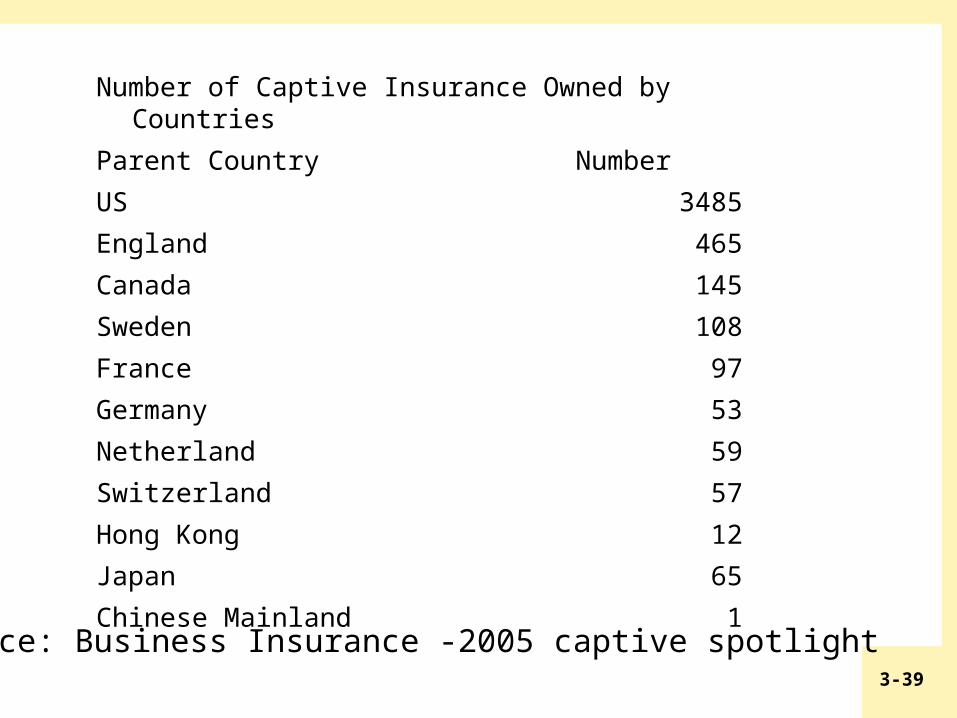

Number of Captive Insurance Owned by Countries

Parent Country Number

US 3485

England 465

Canada 145

Sweden 108

France 97

Germany 53

Netherland 59

Switzerland 57

Hong Kong 12

Japan 65

Chinese Mainland 1Source: Business Insurance -2005 captive spotlight

3-40

Captive

• In 2010, global captive numbers reaching 6000

• new formations totaled 345 in 2009

• Singapore and Hong Kong, the minimum registered capital of establishing a captive is S$0.4m and HK$2m respectively

• China: RMB200m

3-41

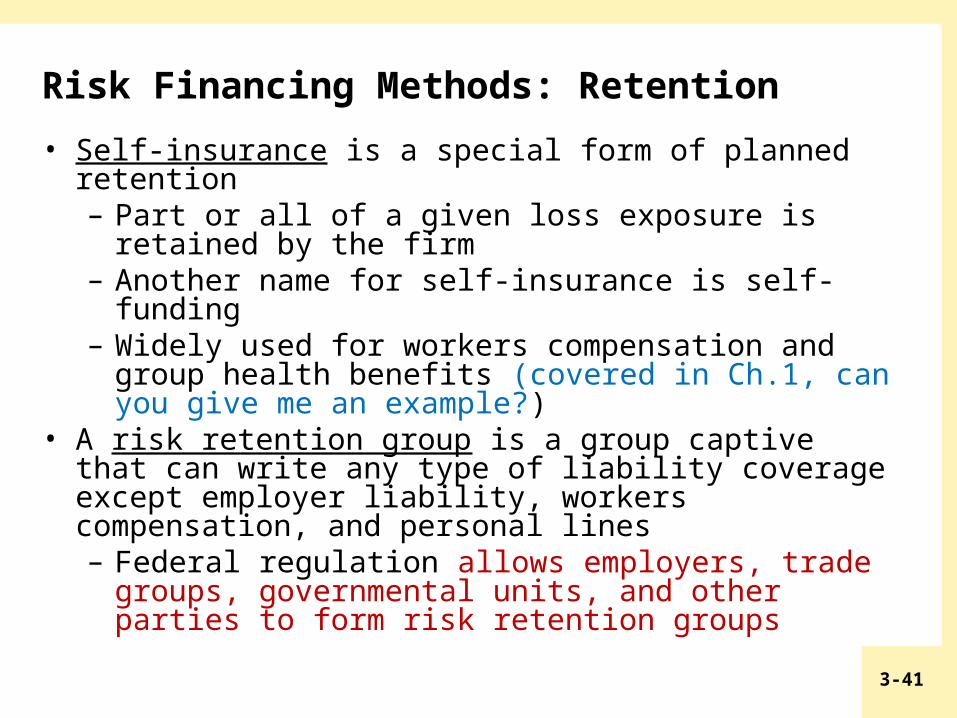

Risk Financing Methods: Retention

• Self-insurance is a special form of planned retention – Part or all of a given loss exposure is retained

by the firm– Another name for self-insurance is self-funding– Widely used for workers compensation and

group health benefits (covered in Ch.1, can you give me an example?)

• A risk retention group is a group captive that can write any type of liability coverage except employer liability, workers compensation, and personal lines– Federal regulation allows employers, trade

groups, governmental units, and other parties to form risk retention groups

3-42

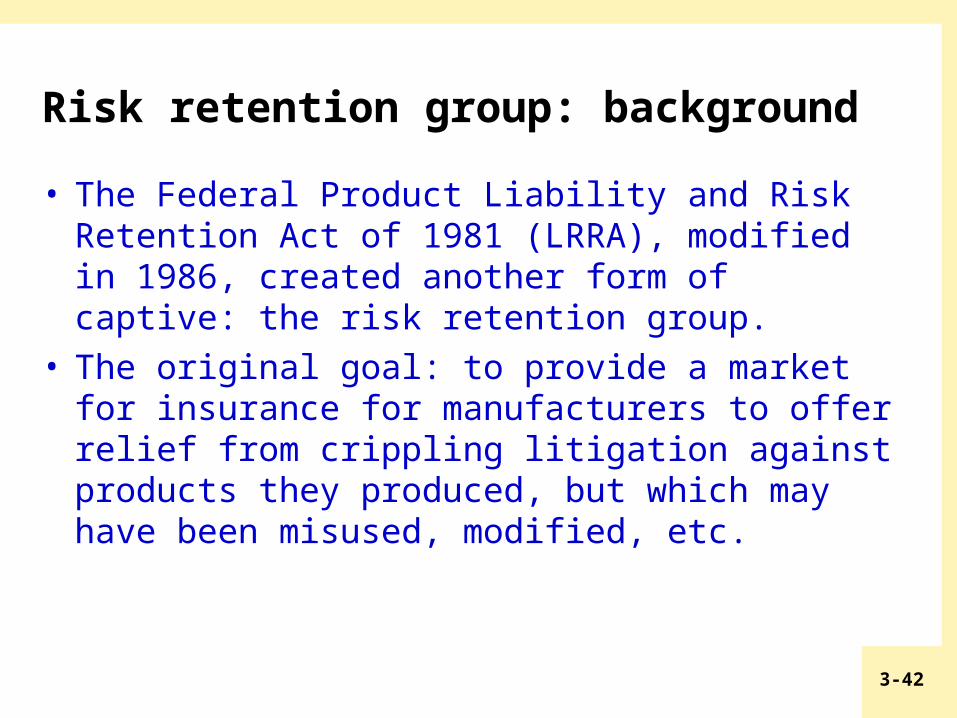

Risk retention group: background

• The Federal Product Liability and Risk Retention Act of 1981 (LRRA), modified in 1986, created another form of captive: the risk retention group.

• The original goal: to provide a market for insurance for manufacturers to offer relief from crippling litigation against products they produced, but which may have been misused, modified, etc.

3-43

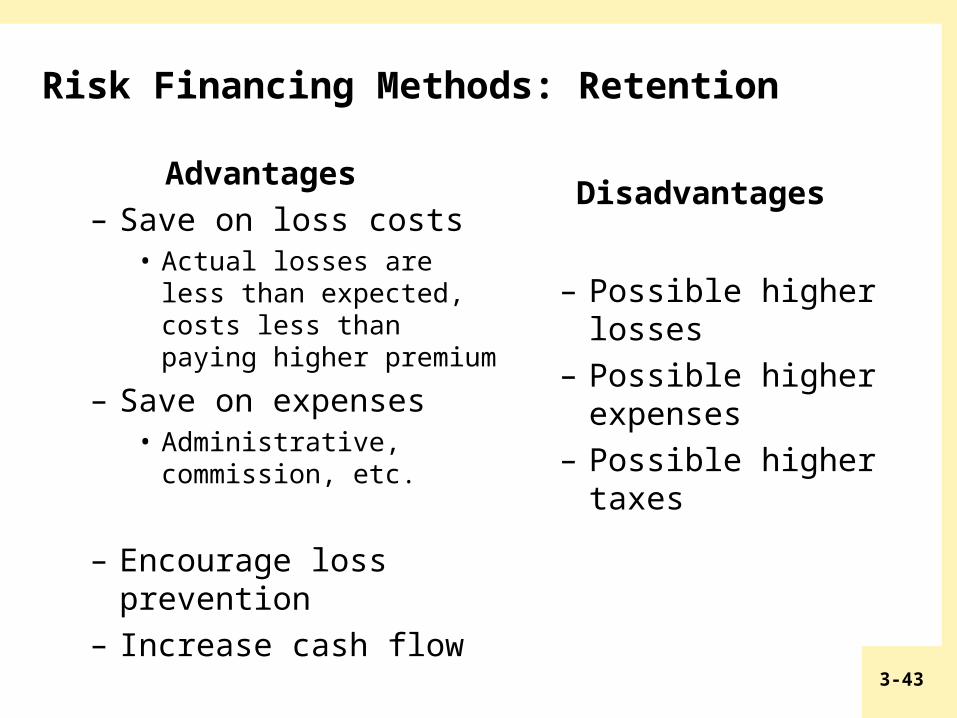

Risk Financing Methods: Retention

Advantages – Save on loss costs

• Actual losses are less than expected, costs less than paying higher premium

– Save on expenses• Administrative,

commission, etc.

– Encourage loss prevention

– Increase cash flow

Disadvantages

– Possible higher losses

– Possible higher expenses

– Possible higher taxes

3-44

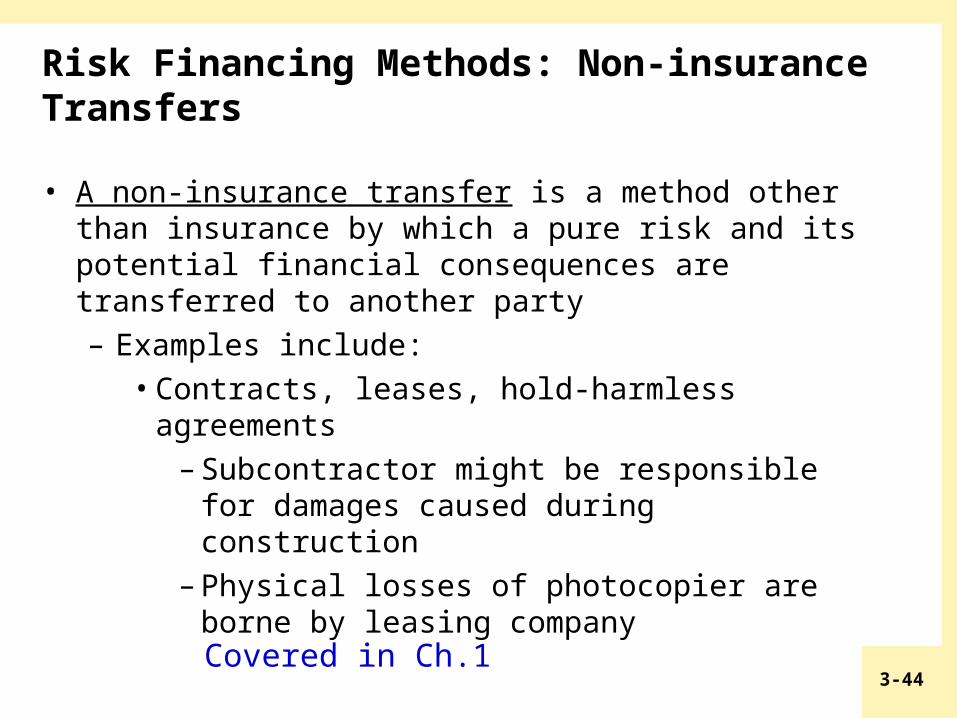

Risk Financing Methods: Non-insurance Transfers

• A non-insurance transfer is a method other than insurance by which a pure risk and its potential financial consequences are transferred to another party – Examples include:

• Contracts, leases, hold-harmless agreements– Subcontractor might be responsible for

damages caused during construction– Physical losses of photocopier are borne

by leasing company

Covered in Ch.1

3-45

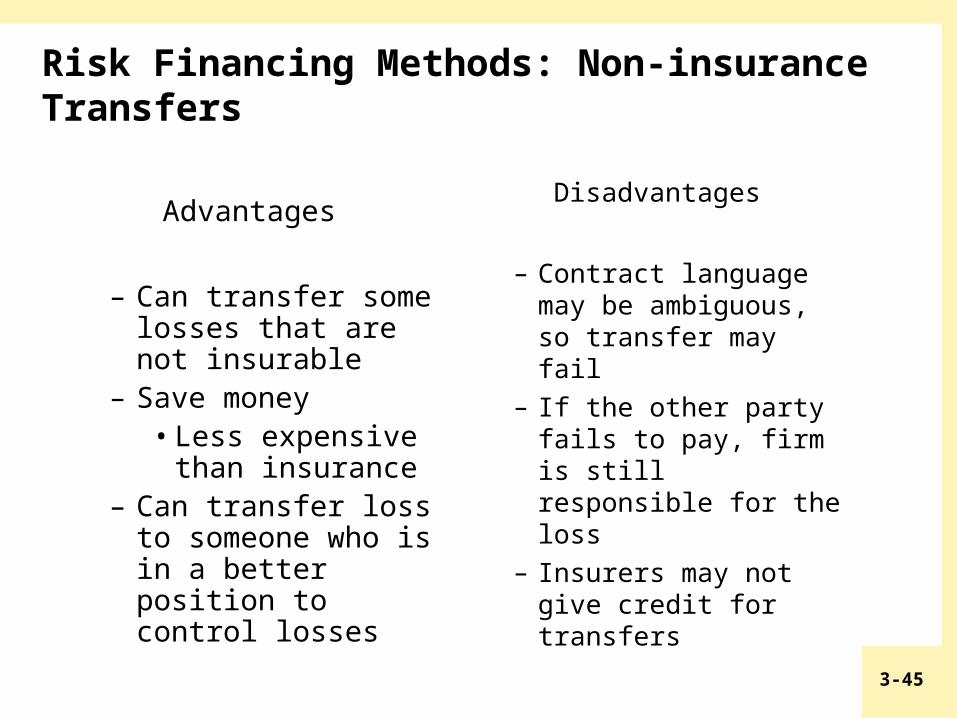

Risk Financing Methods: Non-insurance Transfers

Advantages

– Can transfer some losses that are not insurable

– Save money• Less expensive

than insurance– Can transfer loss

to someone who is in a better position to control losses

Disadvantages

– Contract language may be ambiguous, so transfer may fail

– If the other party fails to pay, firm is still responsible for the loss

– Insurers may not give credit for transfers

3-46

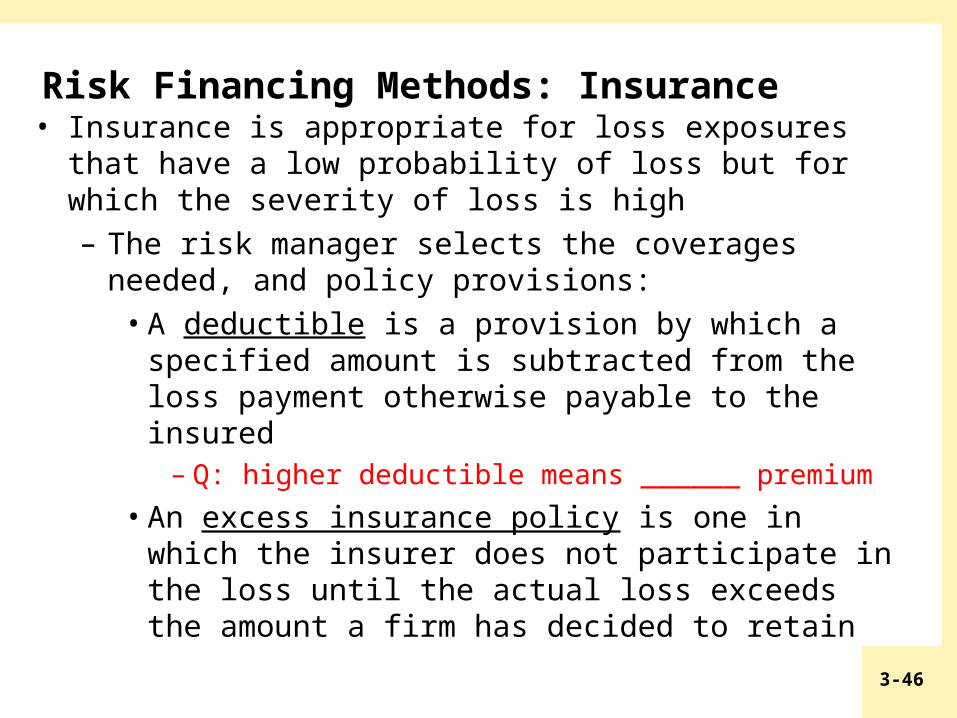

Risk Financing Methods: Insurance• Insurance is appropriate for loss exposures that

have a low probability of loss but for which the severity of loss is high– The risk manager selects the coverages needed,

and policy provisions:• A deductible is a provision by which a

specified amount is subtracted from the loss payment otherwise payable to the insured

– Q: higher deductible means ______ premium

• An excess insurance policy is one in which the insurer does not participate in the loss until the actual loss exceeds the amount a firm has decided to retain

3-47

Risk Financing Methods: Insurance

– The risk manager selects the insurer, or insurers, to provide the coverages • Costs, services, financial strength, etc. to be

considered

– The risk manager negotiates the terms of the insurance contract

– The risk manager must periodically review the insurance program

3-48

Risk Financing Methods: Insurance

Advantages

– Firm is indemnified for losses

– Uncertainty is reduced

– Insurers may provide other risk management services

– Premiums are tax-deductible

Disadvantages

– Premiums may be costly

• Opportunity cost should be considered

– Negotiation of contracts takes time and effort

– The risk manager may become lax in exercising loss control

3-49

Exhibit 2 Risk Management Matrix

You might want to compare the techniques mentioned abovewith those employed by BP.

3-50

Market Conditions and the Selection of Risk Management Techniques

• Risk managers may have to modify their choice of techniques depending on market conditions in the insurance markets

• The insurance market experiences an underwriting cycle– In a “hard” market, when profitability is

declining, underwriting standards are tightened, premiums increase, and insurance becomes more difficult to obtain

– In a “soft” market, when profitability is improving, standards are loosened, premiums decline, and insurance become easier to obtain

3-51

Implement and Monitor the Risk Management Program

• Implementation of a risk management program begins with a risk management policy statement that:– Outlines the firm’s risk management objectives – Outlines the firm’s policy on loss control– Educates top-level executives in regard to the risk

management process– Gives the risk manager greater authority

• He/she has to work with other departments – Provides standards for judging the risk manager’s

performance• A risk management manual may be used to:

– Describe the risk management program– Train new employees

3-52

Implement and Monitor the Risk Management Program

• A successful risk management program requires active cooperation from other departments in the firm

• The risk management program should be periodically reviewed and evaluated to determine whether the objectives are being attained– The risk manager should compare the costs and

benefits of all risk management activities

3-53

Benefits of Risk Management

• RM program: more easy to attain Pre-loss and post-loss objectives

• A risk management program can reduce a firm’s cost of risk– The cost of risk includes premiums paid, retained losses,

outside risk management services, financial guarantees, internal administrative costs, taxes, fees, and other expenses

• Reduction in pure loss exposures (may have big impact on the firm financially) allows a firm to enact an enterprise risk management program to treat both pure and speculative loss exposures

• Society benefits because both direct and indirect losses are reduced

3-54

Insight Show Me the Money–Risk Manager Salaries Rise

3-55

Personal Risk Management

• Personal risk management refers to the identification of pure risks faced by an individual or family, and to the selection of the most appropriate technique for treating such risks

• The same principles applied to corporate risk management apply to personal risk management

3-56

Example in Risk Management (ref.)• RISK MANAGEMENT• The Group (“We”) are developing an improved framework for

the management and control of risk in the Group. • Risks are in the process of being more formally identified and

recorded in the Risk Register for key operations, and we are evaluating the inherent risks and residual risks after mitigating controls are considered. The Risk Register will be updated regularly and used to plan the Group’s audit and risk strategy. Specific risks that we proactively manage are detailed below:

• STRATEGIC RISK• We differentiate our products primarily through technology and

innovation, and by being the safe choice for our customers.• We actively focus on innovation in technology and product

design. This leads to competitive advantage in markets which are characterized by constant developments in technology, changes in industry standards and continuing demand for product and service enhancements.

Source: Annual Report 2010, Johnson Electric Holdings Limited

3-57

Example in Risk Management

• OPERATIONAL RISK• We continue to develop high quality

engineering and manufacturing processes across our operations which enable us to minimize the risk of warranty claims.

• We actively seek to attract and retain high calibre management and key personnel by building effective networks of key employees and partners to safeguard our ongoing business success.

Source: Annual Report 2010, Johnson Electric Holdings Limited

3-58

Example in Risk Management

• MANAGEMENT’S DISCUSSION AND ANALYSIS FINANCIAL RISK

• We control working capital and the risk of bad debts by carefully evaluating credit risk with our customers and a low tolerance for delinquent payment. We continue to monitor our receivables carefully as the economic recovery continues.

• COMPLIANCE RISK• We manage compliance with taxation regulations

world-wide through our Corporate Tax department which also ensures that our legal and tax structure optimizes tax liabilities within the constraints set by tax regulations and laws.

Source: Annual Report 2010, Johnson Electric Holdings Limited

3-59

Risk Register or risk log

Risk Category

Risk Name

Risk Number

Probability Impact Risk Score

Mitigation ContingencyAction

By

Nature FireUse inventory in the store

Contact 2nd supplier