Chapter 3 Deferred Tax

47

Gripping IFRS Deferred taxation Chapter 3 88 Chapter 3 Deferred Taxation Reference: IAS 12 and SIC 21 Contents: Page 1. Definitions 90 2. Normal tax and deferred tax 2.1 Current tax versus deferred tax 2.1.1 A deferred tax asset 2.1.2 A deferred tax liability 2.1.3 Deferred tax balance versus the current tax payable balance 2.1.4 Basic examples Example 1A: creating a deferred tax asset Example 1B: reversing a deferred tax asset Example 2A: creating a deferred tax liability Example 2B: reversing a deferred tax liability 2.2 Calculation of Deferred tax – the two methods 2.2.1 The income statement approach Example 3A: income received in advance (income statement approach) 2.2.2 The balance sheet approach Example 3B: income received in advance (balance sheet approach) Example 3C: income received in advance (journals) Example 3D: income received in advance (disclosure) 2.3 Year-end accruals, provisions and deferred tax 2.3.1 Expenses prepaid Example 4: expenses prepaid 2.3.2 Expenses payable Example 5: expenses payable 2.3.3 Provisions Example 6: provisions 2.3.4 Income receivable Example 7: income receivable 2.4 Depreciable non-current assets and deferred tax 2.4.1 Depreciation versus capital allowances Example 8: depreciable assets 2.5 Rate changes and deferred tax Example 9: rate changes – date of substantive enactment Example 10: rate changes Example 11: rate changes 2.6 Tax losses and deferred tax Example 12: tax losses 3. Disclosure of income tax 3.1 Overview 3.2 Statement of comprehensive income disclosure 3.2.1 Face of the statement of comprehensive income 3.2.2 Tax expense note 91 91 91 91 92 92 92 93 94 95 97 97 98 100 101 102 102 103 104 104 107 107 109 109 112 113 115 115 116 119 120 120 123 124 124 127 127 127 127 128

-

Upload

hammad-ahmad -

Category

Documents

-

view

294 -

download

5

description

uploaded by:-hammad ahmad

Transcript of Chapter 3 Deferred Tax

Gripping IFRS Deferred taxation

Chapter 3

88

Chapter 3 Deferred Taxation

Reference: IAS 12 and SIC 21 Contents:

Page

1. Definitions 90 2. Normal tax and deferred tax

2.1 Current tax versus deferred tax 2.1.1 A deferred tax asset 2.1.2 A deferred tax liability 2.1.3 Deferred tax balance versus the current tax payable balance 2.1.4 Basic examples Example 1A: creating a deferred tax asset Example 1B: reversing a deferred tax asset Example 2A: creating a deferred tax liability Example 2B: reversing a deferred tax liability

2.2 Calculation of Deferred tax – the two methods 2.2.1 The income statement approach Example 3A: income received in advance (income statement approach) 2.2.2 The balance sheet approach Example 3B: income received in advance (balance sheet approach) Example 3C: income received in advance (journals) Example 3D: income received in advance (disclosure)

2.3 Year-end accruals, provisions and deferred tax 2.3.1 Expenses prepaid Example 4: expenses prepaid 2.3.2 Expenses payable Example 5: expenses payable 2.3.3 Provisions Example 6: provisions 2.3.4 Income receivable Example 7: income receivable

2.4 Depreciable non-current assets and deferred tax 2.4.1 Depreciation versus capital allowances Example 8: depreciable assets

2.5 Rate changes and deferred tax Example 9: rate changes – date of substantive enactment Example 10: rate changes Example 11: rate changes

2.6 Tax losses and deferred tax Example 12: tax losses

3. Disclosure of income tax

3.1 Overview 3.2 Statement of comprehensive income disclosure

3.2.1 Face of the statement of comprehensive income 3.2.2 Tax expense note

91 91 91 91 92 92 92 93 94 95 97 97 98

100 101 102 102 103 104 104 107 107 109 109 112 113 115 115 116 119 120 120 123 124 124

127 127 127 127 128

Gripping IFRS Deferred taxation

Chapter 3

89

Contents continued …

3.3 Statement of financial position disclosure 3.3.1 Face of the statement of financial position 3.3.2 Accounting policy note 3.3.3 Deferred tax note

3.3.3.1 Other information needed on deferred tax assets 3.3.3.2 Other information needed on deferred tax liabilities 3.3.3.3 Other information needed on the manner of recovery or

settlement 3.4 Sample disclosure involving tax

Page

129 129 129 129 130 130 130

131

4. Summary 133

Gripping IFRS Deferred taxation

Chapter 3

90

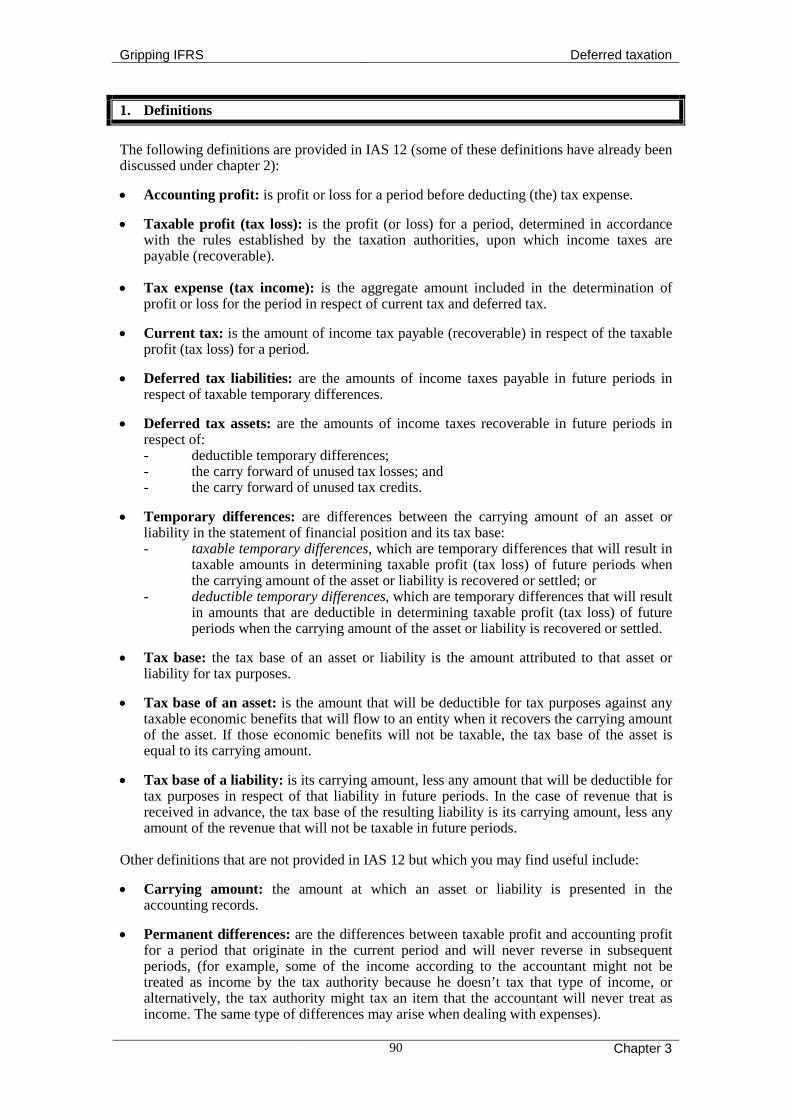

1. Definitions The following definitions are provided in IAS 12 (some of these definitions have already been discussed under chapter 2): • Accounting profit: is profit or loss for a period before deducting (the) tax expense. • Taxable profit (tax loss): is the profit (or loss) for a period, determined in accordance

with the rules established by the taxation authorities, upon which income taxes are payable (recoverable).

• Tax expense (tax income): is the aggregate amount included in the determination of

profit or loss for the period in respect of current tax and deferred tax. • Current tax: is the amount of income tax payable (recoverable) in respect of the taxable

profit (tax loss) for a period. • Deferred tax liabilities: are the amounts of income taxes payable in future periods in

respect of taxable temporary differences. • Deferred tax assets: are the amounts of income taxes recoverable in future periods in

respect of: - deductible temporary differences; - the carry forward of unused tax losses; and - the carry forward of unused tax credits.

• Temporary differences: are differences between the carrying amount of an asset or

liability in the statement of financial position and its tax base: - taxable temporary differences, which are temporary differences that will result in

taxable amounts in determining taxable profit (tax loss) of future periods when the carrying amount of the asset or liability is recovered or settled; or

- deductible temporary differences, which are temporary differences that will result in amounts that are deductible in determining taxable profit (tax loss) of future periods when the carrying amount of the asset or liability is recovered or settled.

• Tax base: the tax base of an asset or liability is the amount attributed to that asset or

liability for tax purposes. • Tax base of an asset: is the amount that will be deductible for tax purposes against any

taxable economic benefits that will flow to an entity when it recovers the carrying amount of the asset. If those economic benefits will not be taxable, the tax base of the asset is equal to its carrying amount.

• Tax base of a liability: is its carrying amount, less any amount that will be deductible for

tax purposes in respect of that liability in future periods. In the case of revenue that is received in advance, the tax base of the resulting liability is its carrying amount, less any amount of the revenue that will not be taxable in future periods.

Other definitions that are not provided in IAS 12 but which you may find useful include: • Carrying amount: the amount at which an asset or liability is presented in the

accounting records. • Permanent differences: are the differences between taxable profit and accounting profit

for a period that originate in the current period and will never reverse in subsequent periods, (for example, some of the income according to the accountant might not be treated as income by the tax authority because he doesn’t tax that type of income, or alternatively, the tax authority might tax an item that the accountant will never treat as income. The same type of differences may arise when dealing with expenses).

Gripping IFRS Deferred taxation

Chapter 3

91

• Comprehensive basis: is the term used to describe the method whereby the tax effects of all temporary differences are recognised.

• Applicable or standard tax rate: is the rate of tax, as determined from time to time by

tax legislation, at which entities pay tax on taxable profits, (a rate of 30% is assumed in this text).

• Effective tax rate: is the taxation expense charge in the statement of comprehensive

income expressed as a percentage of accounting profits . 2. Normal tax and deferred tax 2.1 Current tax versus deferred tax As mentioned in the previous chapter, the total normal tax for disclosure purposes is broken down into two main components: • current tax; and • deferred tax. Current normal tax is the tax charged by the tax authority in the current period on the current period’s taxable profits. The taxable profits are calculated based on tax legislation (discussed in the previous chapter). Since this tax legislation is not based strictly on the accrual concept, differences may arise such as income being included in taxable profits before it is earned! The total normal tax expense recognised in the statement of comprehensive income is the tax incurred on the accounting profits. Accounting profits are calculated in accordance with the international financial reporting standards, which are based on the concept of accrual. The difference between current normal tax (which is not based on the accrual concept), and the total normal tax in the statement of comprehensive income (which is based on the accrual concept), is an adjustment called deferred tax. The deferred tax adjustment is therefore simply an accrual of tax. In other words: current normal tax (i.e. the amount charged by the tax authority) is adjusted upwards or downwards so that the total normal tax in the statement of comprehensive income is shown at the amount of tax incurred. This results in the creation of a deferred tax asset or liability. 2.1.1 A deferred tax asset (a debit balance) A debit balance on the deferred tax account reflects the accountant’s belief that tax has been charged but which has not yet been incurred. This premature tax charge must be deferred (postponed). In some ways, this treatment is similar to that of a prepaid expense. Debit Credit Deferred tax asset xxx Taxation expense xxx Creating a deferred tax asset 2.1.2 A deferred tax liability (a credit balance) A credit balance reflects the accountant’s belief that tax has been incurred, but which has not yet been charged by the tax authority. It therefore shows the amount that will be charged by the tax authority in the future. This is similar to the treatment of an expense payable. Debit Credit Taxation expense xxx Deferred tax liability xxx Creating a deferred tax liability

Gripping IFRS Deferred taxation

Chapter 3

92

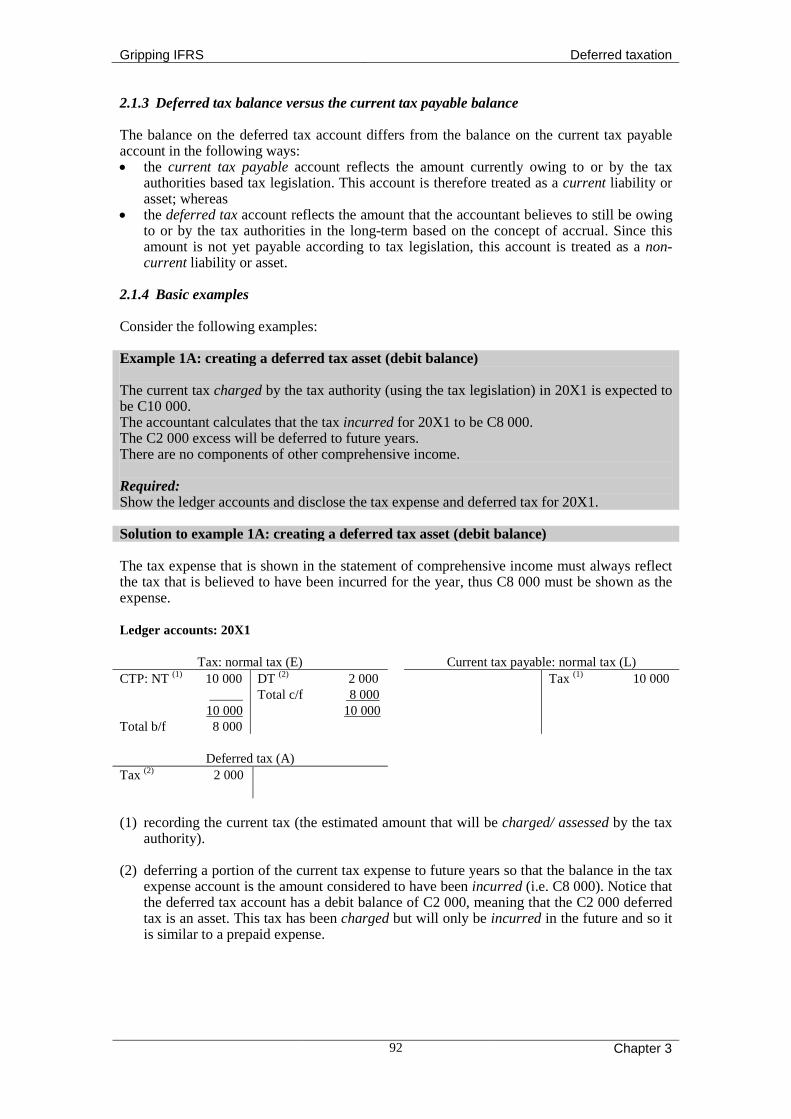

2.1.3 Deferred tax balance versus the current tax payable balance The balance on the deferred tax account differs from the balance on the current tax payable account in the following ways: • the current tax payable account reflects the amount currently owing to or by the tax

authorities based tax legislation. This account is therefore treated as a current liability or asset; whereas

• the deferred tax account reflects the amount that the accountant believes to still be owing to or by the tax authorities in the long-term based on the concept of accrual. Since this amount is not yet payable according to tax legislation, this account is treated as a non-current liability or asset.

2.1.4 Basic examples Consider the following examples: Example 1A: creating a deferred tax asset (debit balance) The current tax charged by the tax authority (using the tax legislation) in 20X1 is expected to be C10 000. The accountant calculates that the tax incurred for 20X1 to be C8 000. The C2 000 excess will be deferred to future years. There are no components of other comprehensive income. Required: Show the ledger accounts and disclose the tax expense and deferred tax for 20X1. Solution to example 1A: creating a deferred tax asset (debit balance) The tax expense that is shown in the statement of comprehensive income must always reflect the tax that is believed to have been incurred for the year, thus C8 000 must be shown as the expense. Ledger accounts: 20X1

Tax: normal tax (E) Current tax payable: normal tax (L) CTP: NT (1) DT (2) 2 000 10 000 Tax (1) 10 000 _____ Total c/f 8 000 10 000 10 000 Total b/f 8 000

Deferred tax (A) Tax (2) 2 000 (1) recording the current tax (the estimated amount that will be charged/ assessed by the tax

authority). (2) deferring a portion of the current tax expense to future years so that the balance in the tax

expense account is the amount considered to have been incurred (i.e. C8 000). Notice that the deferred tax account has a debit balance of C2 000, meaning that the C2 000 deferred tax is an asset. This tax has been charged but will only be incurred in the future and so it is similar to a prepaid expense.

Gripping IFRS Deferred taxation

Chapter 3

93

Disclosure for 20X1: The disclosure will be as follows (the deferred tax asset note will be ignored at this stage): Entity name Statement of comprehensive income For the year ended …20X1

Note 20X1 C

Profit before tax xxx Taxation expense (current tax: 10 000 – deferred tax: 2 000) 3. 8 000 Profit for the period xxx Other comprehensive income 0 Total comprehensive income xxx Entity name Statement of financial position As at …20X1

ASSETS 20X1

C Non-current Assets - Deferred tax: normal tax 2 000 Entity name Notes to the financial statements For the year ended …20X1

3. Taxation expense 20X1

C Normal taxation expense 8 000 - Current 10 000 - Deferred (2 000) Example 1B: reversing a deferred tax asset Use the same information as that given in 1A and the following additional information: The current tax charged by the tax authorities (based on tax legislation) in 20X2 is expected to be C14 000. The accountant calculates the tax incurred for 20X2 to be C16 000 (the ‘excess tax’ charged in 20X1 is now incurred). There are no components of other comprehensive income. Required: Show the ledger accounts and disclose the tax expense and deferred tax in 20X2. Solution to example 1B: reversing a deferred tax asset Ledger accounts: 20X2

Tax: normal tax (E) Current tax payable: normal tax CTP: NT (1) 14 000 Tax (1) 14 000 DT (2) 2 000 16 000

Deferred tax (A) Balance b/d 2 000 Taxation (2) 2 000

Gripping IFRS Deferred taxation

Chapter 3

94

(1) recording the current tax (estimated amount that will be charged by the tax authorities) (2) recording the reversal of the deferred tax asset in the second year. The total tax expense in

20X2 will be the current tax charged for 20X2 plus deferred tax (the portion of the current tax that was not recognised in 20X1, is incurred in 20X2).

Disclosure for 20X2: Entity name Statement of comprehensive income For the year ended …20X2

Note 20X2 C

20X1 C

Profit before tax xxx xxx Taxation expense (20X2: current tax: 14 000 + deferred tax: 2 000)

3. 16 000 8 000

Profit after tax xxx xxx Other comprehensive income 0 0 Total comprehensive income xxx xxx Entity name Statement of financial position As at … 20X2

ASSETS Note 20X2

C 20X1

C Non-current Assets - Deferred tax: normal tax 0 2 000 Entity name Notes to the financial statements For the year ended ……20X2

3. Taxation expense 20X2

C 20X1

C Normal taxation expense 16 000 8 000 - Current 14 000 10 000 - Deferred 2 000 (2 000) It can be seen that over the period of 2 years, the total current tax of C24 000 (10 000 + 14 000) charged by the tax authorities, is recognised as a tax expense in the accounting records: • the tax expense in the first year is C8 000; and • the tax expense in the second year C16 000. Example 2A: creating a deferred tax liability (credit balance) The current tax expected to be charged by the tax authorities (based on tax legislation) is C10 000 in 20X1. The accountant calculates that the tax incurred for 20X1 to be C12 000. There are no components of other comprehensive income. Required: Show the ledger accounts and disclose the tax expense and deferred tax in 20X1. Solution to example 2A: creating a deferred tax liability (credit balance) The tax shown in the statement of comprehensive income must always be the amount incurred for the year rather than the amount charged, thus C12 000 must be shown as the tax expense.

Gripping IFRS Deferred taxation

Chapter 3

95

Ledger accounts: 20X1

Tax: normal tax (E) Current tax payable: normal tax CTP: NT(1) 10 000 Tax (1) 10 000 DT(2) 2 000 12 000

Deferred tax (L) Tax (2) 2 000 (1) Recording the current tax (the estimated amount that will be charged by the tax

authorities). (2) Providing for extra tax that has been incurred but which will only be charged/assessed by

the tax authorities in future years (tax owing to the tax authorities in the long term): we have only been charged C10 000 in the current year, but have incurred C12 000, thus there is an amount of C2 000 that will have to be paid sometime in the future. Notice that the deferred tax account has a credit balance of C2 000, (a deferred tax liability).

Disclosure for 20X1: Entity name Statement of comprehensive income For the year ended …20X1

20X1 C

Profit before tax xxx Taxation expense (current tax: 10 000 + deferred tax: 2 000) 3. 12 000 Profit for the year xxx Other comprehensive income 0 Total comprehensive income xxx Entity name Statement of financial position As at ……..20X1

LIABILITIES 20X1

C Non-current Liabilities - Deferred tax: 2 000 Entity name Notes to the financial statements For the year ended ……20X1

3. Taxation expense 20X1

C Normal taxation expense 12 000 - Current 10 000 - Deferred 2 000 Example 2B: reversing a deferred tax liability Use the same information as that given in example 2A as well as the following information: • The tax authority is expected to charge C14 000 for 20X2 but the tax incurred is

calculated to be C12 000. • There are no components of other comprehensive income. Required:

Gripping IFRS Deferred taxation

Chapter 3

96

Show the ledger accounts and disclose the tax expense and deferred tax in 20X2. Solution to example 2B: reversing a deferred tax liability The deferred tax liability (a non-current liability) will have to be reversed out in 20X2 since the amount will now form part of the current tax payable liability instead (a current liability). Ledger accounts: 20X2

Tax: normal tax (E) Current tax payable: normal tax CTP: NT (1) 14 000 DT (2) 2 000 Tax (1) 14 000 Total 12 000

Deferred tax (L) Tax (2) 2 000 Balance b/f 2 000 (1) recording the current tax (charged by the tax authority) (2) recording the reversal of the deferred tax in the second year. Disclosure for 20X2: Entity name Statement of comprehensive income For the year ended …..20X2

20X2 C

20X1 C

Profit before tax xxx xxx Taxation expense (current tax and deferred tax) 3. 12 000 12 000 Profit for the year xxx xxx Other comprehensive income 0 0 Total comprehensive income xxx xxx Entity name Statement of financial position As at ……..20X2

LIABILITIES 20X2

C 20X1

C Non-current Liabilities - Deferred Tax 0 2 000 Entity name Notes to the financial statements For the year ended …20X2

3. Taxation expense 20X2

C 20X1

C Normal taxation expense 12 000 12 000 - current 14 000 10 000 - deferred (2 000) 2 000 It can be seen that over the period of 2 years, the total current tax of C24 000 (10 000 + 14 000) charged by the tax authority is recognised as a tax expense in the accounting records: • the tax expense in the first year is C12 000 and • the tax expense in the second year is C12 000.

Gripping IFRS Deferred taxation

Chapter 3

97

2.2 Calculation of Deferred tax – the two methods Although IAS 12 refers to only one method of calculating deferred tax, (the balance sheet method), there are in fact two methods: • Balance sheet method: a comparison between the carrying amount and the tax base of

each of the entity’s assets and liabilities; and the • Income statement method: a comparison between accounting profits and taxable profits. The method used will not alter the journals or disclosure. You will generally be required to calculate the Deferred tax using the balance sheet method. The income statement method is still useful though since it serves as a tool to check your balance sheet calculations and is useful in that it is easier to explain the concept of deferred tax. If there was deferred tax on a gain or loss that is recognised directly in equity (i.e. not in profit or loss), then the income statement method will need to bear this into account, since the income statement method looks only at the deferred tax caused by items of income and expense recognised in profit or loss. IAS 12 expressly prohibits the discounting (present valuing) of deferred tax balances. 2.2.1 The income statement approach The ‘accountant’ and the ‘tax authorities’ calculate profits in different ways: International Financial Reporting Standards govern the manner in which the accountant calculates accounting profit: • profit or loss for a period before deducting (the) tax expense. Tax legislation governs the manner in which the tax authorities calculate taxable profit: • the profit (or loss) for the period, determined in accordance with the rules established by

the taxation authorities, upon which income taxes are payable or recoverable. In order for the accountant to calculate the estimated current tax for the year, he converts his accounting profits into taxable profits. This is done as follows: Conversion of accounting profits into taxable profits: C Profit before tax (accounting profits) xxx Adjusted for permanent differences: xxx - less exempt income (e.g. certain capital profits and dividend income) - add non-deductible expenses (e.g. certain donations and fines)

(xxx) xxx

Accounting profits that are taxable (A x 30% = tax expense incurred) A Adjusted for movements in temporary differences: xxx - add depreciation - less depreciation for tax purposes (e.g. wear and tear) - add income received in advance (closing balance): if taxed when

received - less income received in advance (opening balance): if taxed when

received - less expenses prepaid (closing balance): if deductible when paid - add expenses prepaid (opening balance): if deductible when paid - add provisions (closing balance): if deductible when paid - less provisions (opening balance): if deductible when paid

xxx (xxx) xxx

(xxx) (xxx) xxx xxx

(xxx)

Taxable profits (B x 30% = current tax charge) B

Gripping IFRS Deferred taxation

Chapter 3

98

As can be seen from the calculation above, the difference between accounting profits and taxable profits may be classified into two main types:

• temporary differences; and • permanent differences.

Accounting

profits

= Profit before tax

+/- Permanent differences

Taxable

accounting profits

=

Portion of the accounting profits that are taxable although not necessarily now

X 30% =

Tax

expense

+/- Temporary differences

X 30% = Deferred tax

expense/ income

Taxable profits

= Profits that are taxable now,

based purely on tax laws X 30% =

Current tax

expense

The difference between total accounting profits and the taxable accounting profits are permanent differences. These differences include, for instance, items of income that will never be taxed as income and yet are recognised as income in the accounting records. The difference between taxable accounting profits (A above) and taxable profits (B above) are caused by the movement in temporary differences. These differences relate to the issue of timing: for instance, when the income is taxed versus when it is recognised as income in the accounting records. A deferred tax adjustment is made for the movement relating to temporary differences only. Example 3A: income received in advance (income statement approach)

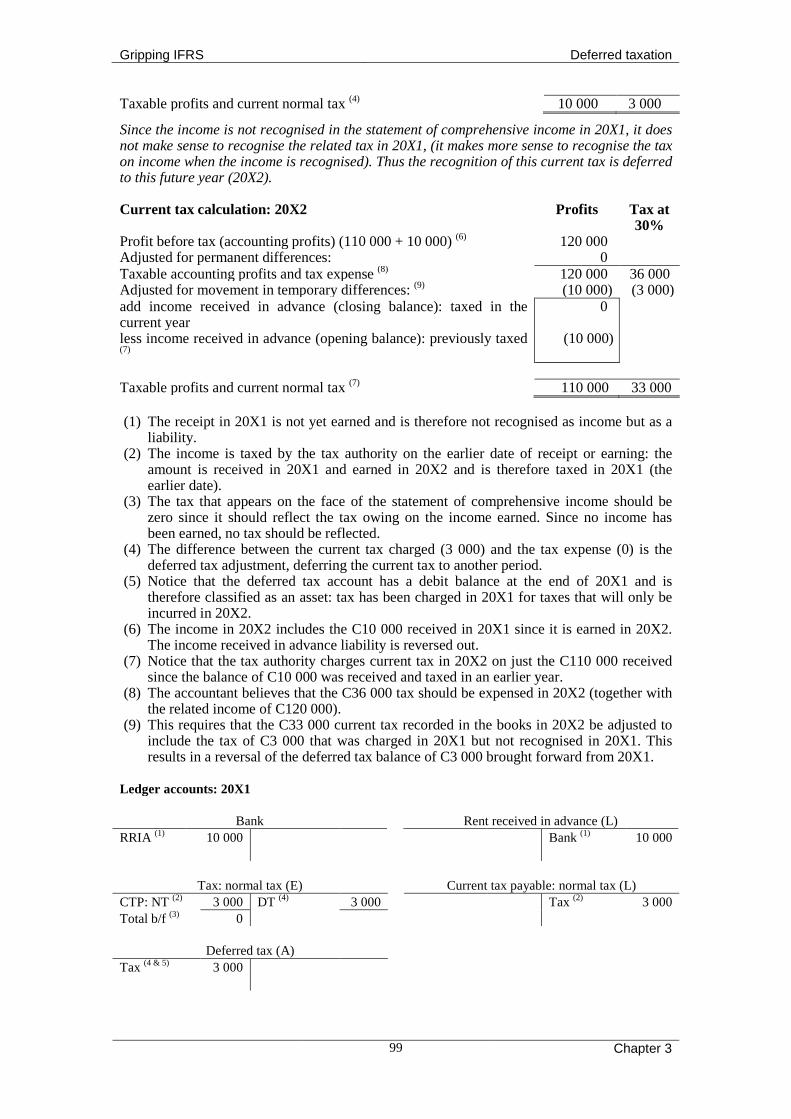

A company receives rent income of C10 000 in 20X1 that relates to rent earned in 20X2 and then receives C110 000 in rent income in 20X2 (all of which was earned in 20X2). The company has no other income. The tax authority taxes income on the earlier of receipt or earning.

Required: Calculate, for 20X1 and 20X2, the current tax expense, the deferred tax adjustment and the final tax expense to appear in the statement of comprehensive income and show the related ledger accounts. Solution to example 3A: income received in advance (income statement approach) Current tax calculation: 20X1 Profits Tax at

30% Profit before tax (accounting profits) (10 000 – 10 000) (1) 0 Adjusted for permanent differences: 0 Taxable accounting profits and tax expense (3) 0 0 Adjusted for movement in temporary differences: (5) 10 000 3 000 add income received in advance (closing balance): taxed in the current year (2)

10 000

less income received in advance (opening balance): previously taxed (0)

Gripping IFRS Deferred taxation

Chapter 3

99

Taxable profits and current normal tax (4) 10 000 3 000 Since the income is not recognised in the statement of comprehensive income in 20X1, it does not make sense to recognise the related tax in 20X1, (it makes more sense to recognise the tax on income when the income is recognised). Thus the recognition of this current tax is deferred to this future year (20X2). Current tax calculation: 20X2 Profits Tax at

30% Profit before tax (accounting profits) (110 000 + 10 000) (6) 120 000 Adjusted for permanent differences: 0 Taxable accounting profits and tax expense (8) 120 000 36 000 Adjusted for movement in temporary differences: (9) (10 000) (3 000) add income received in advance (closing balance): taxed in the current year

0

less income received in advance (opening balance): previously taxed (7)

(10 000)

Taxable profits and current normal tax (7) 110 000 33 000 (1) The receipt in 20X1 is not yet earned and is therefore not recognised as income but as a

liability. (2) The income is taxed by the tax authority on the earlier date of receipt or earning: the

amount is received in 20X1 and earned in 20X2 and is therefore taxed in 20X1 (the earlier date).

(3) The tax that appears on the face of the statement of comprehensive income should be zero since it should reflect the tax owing on the income earned. Since no income has been earned, no tax should be reflected.

(4) The difference between the current tax charged (3 000) and the tax expense (0) is the deferred tax adjustment, deferring the current tax to another period.

(5) Notice that the deferred tax account has a debit balance at the end of 20X1 and is therefore classified as an asset: tax has been charged in 20X1 for taxes that will only be incurred in 20X2.

(6) The income in 20X2 includes the C10 000 received in 20X1 since it is earned in 20X2. The income received in advance liability is reversed out.

(7) Notice that the tax authority charges current tax in 20X2 on just the C110 000 received since the balance of C10 000 was received and taxed in an earlier year.

(8) The accountant believes that the C36 000 tax should be expensed in 20X2 (together with the related income of C120 000).

(9) This requires that the C33 000 current tax recorded in the books in 20X2 be adjusted to include the tax of C3 000 that was charged in 20X1 but not recognised in 20X1. This results in a reversal of the deferred tax balance of C3 000 brought forward from 20X1.

Ledger accounts: 20X1

Bank Rent received in advance (L) RRIA (1) 10 000 Bank (1) 10 000

Tax: normal tax (E) Current tax payable: normal tax (L)

CTP: NT (2) 3 000 DT (4) 3 000 Tax (2) 3 000 Total b/f (3) 0

Deferred tax (A)

Tax (4 & 5) 3 000

Gripping IFRS Deferred taxation

Chapter 3

100

Ledger accounts: 20X2 Bank Rent received in advance (L)

Rent 110 000 Rent (6) 10 000 Balance b/f 10 000

Tax: normal tax (E) Current tax payable: normal tax (L)

CTP:NT (7) 33 000 Balance b/f 3 000 DT (9) 3 000 Tax (7) 33 000 Total (8) 36 000

Deferred tax Rent (I)

Balance b/f 3 000 Tax (9) 3 000 RRIA (6) 10 000 Bank 110 000 120 000 2.2.2 The balance sheet approach When calculating deferred tax using the balance sheet approach, the carrying amount of the assets and liabilities are compared with the tax bases of these assets and liabilities. Any difference between the carrying amount and the tax base of an asset or liability is termed a ‘temporary difference’: • The carrying amounts are the balances of the assets and liabilities as recognised in the

statement of financial position based on International Financial Reporting Standards. • The tax bases are the balances of the assets and liabilities, as they would appear in a

statement of financial position drawn up based on tax law (please read these definitions again – you will find them at the beginning of this chapter).

The total temporary differences multiplied by the tax rate will give: • the deferred tax balance in the statement of financial position. The difference between the opening and closing deferred tax balance in the statement of financial position will give you: • the deferred tax journal adjustment.

Carrying amount:

Tax base:

Opening balance

Opening balance

Carrying amount:

Tax base:

Closing balance Closing balance

Temporary difference X 30% =

Deferred tax balance: beginning of year

Temporary difference X 30% =

Deferred tax balance: end of year

Movement: Deferred tax

journal adjustment

Gripping IFRS Deferred taxation

Chapter 3

101

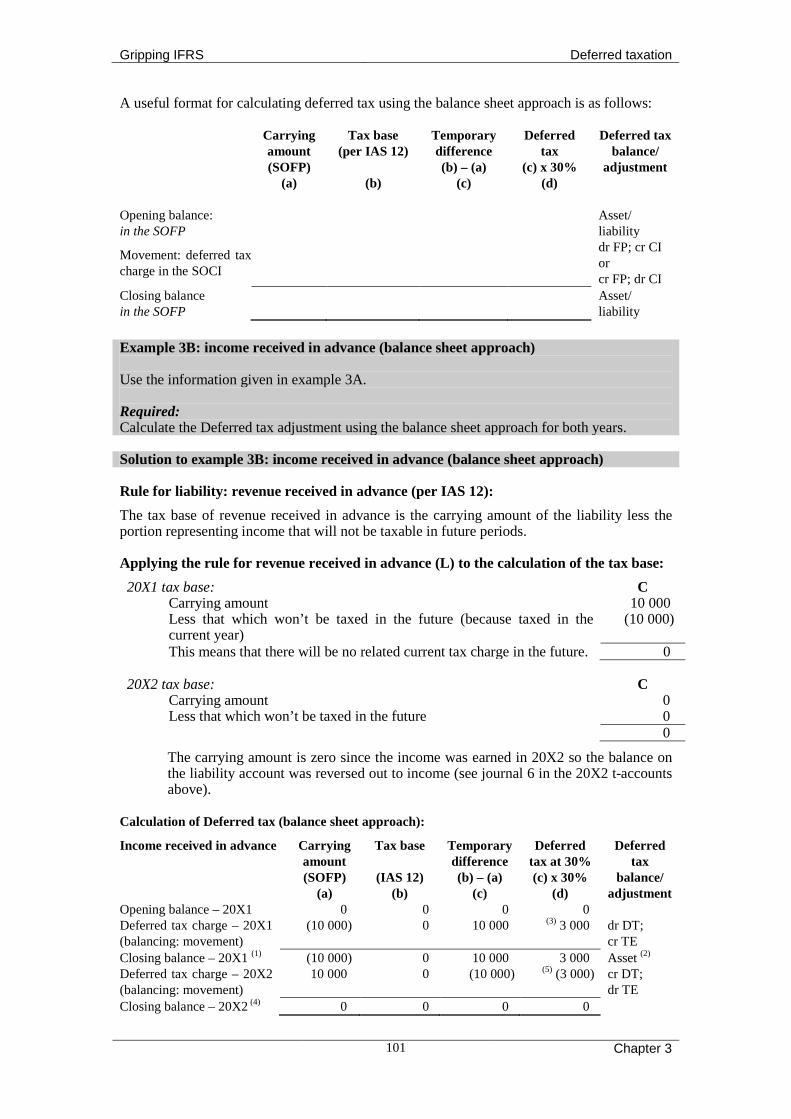

A useful format for calculating deferred tax using the balance sheet approach is as follows: Carrying

amount (SOFP)

(a)

Tax base (per IAS 12)

(b)

Temporary difference (b) – (a)

(c)

Deferred tax

(c) x 30% (d)

Deferred tax balance/

adjustment

Opening balance: in the SOFP

Asset/ liability

Movement: deferred tax charge in the SOCI

dr FP; cr CI or cr FP; dr CI

Closing balance in the SOFP

Asset/ liability

Example 3B: income received in advance (balance sheet approach) Use the information given in example 3A. Required: Calculate the Deferred tax adjustment using the balance sheet approach for both years. Solution to example 3B: income received in advance (balance sheet approach) Rule for liability: revenue received in advance (per IAS 12): The tax base of revenue received in advance is the carrying amount of the liability less the portion representing income that will not be taxable in future periods. Applying the rule for revenue received in advance (L) to the calculation of the tax base: 20X1 tax base: C

Carrying amount 10 000 Less that which won’t be taxed in the future (because taxed in the current year)

(10 000)

This means that there will be no related current tax charge in the future. 0 20X2 tax base: C

Carrying amount 0 Less that which won’t be taxed in the future 0 0

The carrying amount is zero since the income was earned in 20X2 so the balance on the liability account was reversed out to income (see journal 6 in the 20X2 t-accounts above).

Calculation of Deferred tax (balance sheet approach): Income received in advance Carrying

amount (SOFP)

(a)

Tax base

(IAS 12) (b)

Temporary difference (b) – (a)

(c)

Deferred tax at 30% (c) x 30%

(d)

Deferred tax

balance/ adjustment

Opening balance – 20X1 0 0 0 0 Deferred tax charge – 20X1 (balancing: movement)

(10 000) 0 10 000 (3) 3 000 dr DT; cr TE

Closing balance – 20X1 (1) (10 000) 0 10 000 3 000 Asset (2) Deferred tax charge – 20X2 (balancing: movement)

10 000 0 (10 000) (5) (3 000) cr DT; dr TE

Closing balance – 20X2 (4) 0 0 0 0

Gripping IFRS Deferred taxation

Chapter 3

102

Explanation of the above: 1) During 20X1, the C10 000 rent is received in advance. The accountant treats this as a

liability whereas the tax authority treats it as income. Thus the carrying amount of the income received in advance account is C10 000 whereas the tax authority has no such liability: the tax base is therefore zero. This results in a temporary difference of C10 000 and therefore a deferred tax balance of C3 000.

2) The tax base of a liability that represents income, is that portion of the liability that will be taxed in the future. The difference between the carrying amount and the tax base represents the portion of the liability that won’t be taxed in the future with the result that the deferred tax balance is an asset to the company: the tax that has been ‘prepaid’.

3) The deferred tax charge in 20X1 will be a credit to the statement of comprehensive income.

4) During 20X2, the C10 000 rent that was received in advance in 20X1 is now recognised as income (the accountant will debit the liability and credit income) with the result that the accountant’s liability reverses out to zero. As mentioned above, the tax authority had no such liability since he treated the receipt as income in 20X1. The carrying amount and the tax base are now both zero, with the result that the temporary difference is now zero and the deferred tax is zero.

5) The deferred tax charge in 20X2 is a debit to the statement of comprehensive income. Example 3C: income received in advance (journals) Use the current tax calculation done in example 3A and the deferred tax calculation done in 3B. Required: Show the related tax journal entries. Solution to example 3C: income received in advance (journals) 20X1 Debit Credit Taxation expense: normal tax (SOCI) 3 000 Current tax payable: normal tax (SOFP) 3 000 Current tax payable per tax law (see calculation in 3A)

Deferred tax: normal tax (SOFP) 3 000 Taxation expense: normal tax (SOCI) 3 000 Deferred tax adjustment (see calculation in 3B) 20X2 Taxation expense: normal tax (SOCI) 33 000 Current tax payable: normal tax (SOFP) 33 000 Current tax payable per tax law (see calculation in 3A)

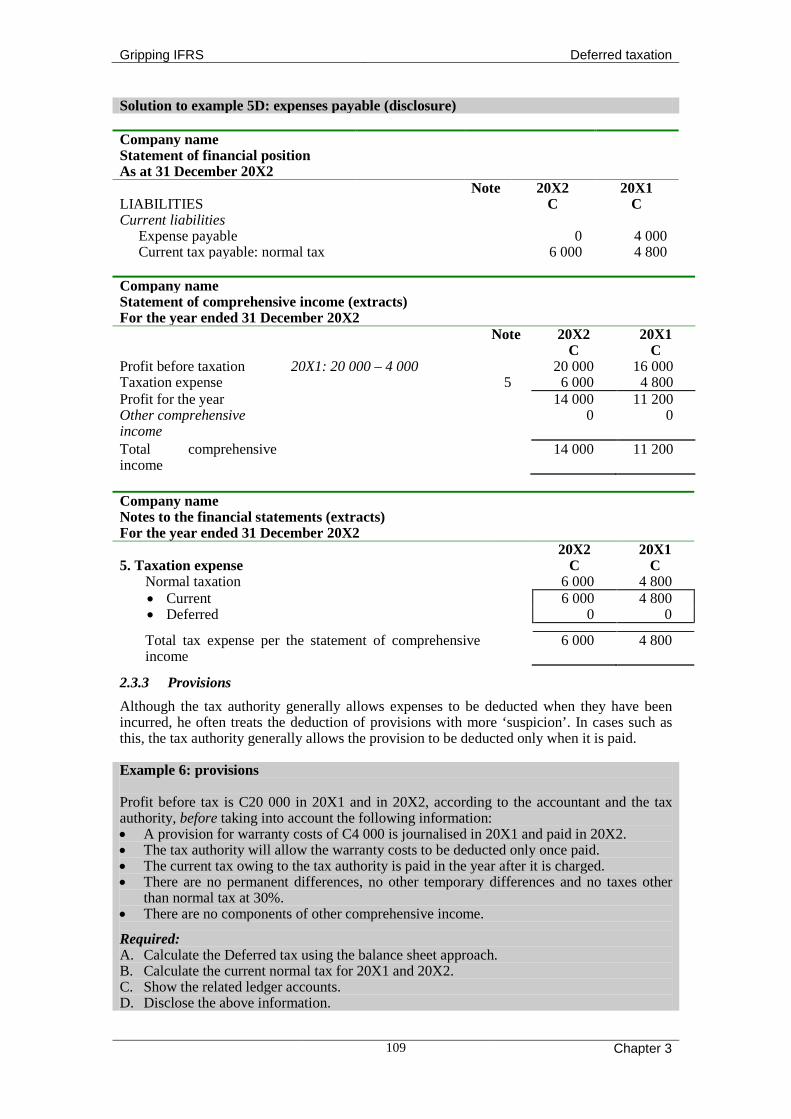

Taxation expense: normal tax (SOCI) 3 000 Deferred tax: normal tax (SOFP) 3 000 Deferred tax adjustment (see calculation in 3B) Example 3D: income received in advance (disclosure) Use the information given in example 3A, 3B or 3C. The current tax for 20X1 is paid in 20X2 and that the current tax for 20X2 is paid in 20X3. There are no components of other comprehensive income. Required: Disclose all information in the financial statements.

Gripping IFRS Deferred taxation

Chapter 3

103

Solution to example 3D: income received in advance (disclosure) Company name Statement of financial position As at 31 December 20X2

ASSETS Non-Current Assets

Note 20X2 C

20X1 C

Deferred tax: normal tax 6 0 3 000 LIABILITIES Current Liabilities

Current tax payable: normal tax 33 000 3 000 Income received in advance 0 10 000

Company name Statement of comprehensive income (extracts) For the year ended 31 December 20X2

Note 20X2 C

20X1 C

Profit before taxation 120 000 0 Taxation expense 5 36 000 0 Profit for the year 84 000 0 Other comprehensive income 0 0 Total comprehensive income 84 000 0 Company name Notes to the financial statements (extracts) For the year ended 31 December 20X2 20X2

C 20X1

C 5. Taxation expense

Normal taxation 36 000 0 • Current 33 000 3 000 • Deferred 3 000 (3 000) Total tax expense per the statement of comprehensive income

36 000 0

6. Deferred tax asset

The closing balance is constituted by the effects of: • Year-end accruals 0 3 000

It can be seen that the deferred tax effect on profits is nil over the period of the two years.

2.3 Year-end accruals, provisions and deferred tax Five statement of financial position accounts resulting directly from the use of the accrual system include: • income received in advance; • expenses prepaid; • expenses payable; • provisions; and • income receivable. Income received in advance has already been covered in example 3 above. The deferred tax effect of each of the remaining four examples will now be discussed. Since IAS 12 refers only to the use of the balance sheet approach, this is the only approach shown in this text.

Gripping IFRS Deferred taxation

Chapter 3

104

2.3.1 Expenses prepaid Remember that, although the tax authority normally allows a deduction of expenses when the expenses are incurred, he may, however, allow a deduction of a prepaid expense depending on criteria in the tax legislation. If this happens, deferred tax will result. Example 4: expenses prepaid Profit before tax is C20 000 in 20X1 and in 20X2, according to the accountant and the tax authority, before taking into account the following information: • An amount of C8 000 in respect of electricity for January 20X2 is paid in December 20X1. • The Receiver allows the payment of C8 000 as a deduction against taxable profits in 20X1. • The company paid the current tax owing to the tax authorities for 20X1, in 20X2. • There are no permanent differences, no other temporary differences and no taxes other

than normal tax at 30%. • There are no components of other comprehensive income. Required: A. Calculate the Deferred tax for 20X1 and 20X2 using the balance sheet approach. B. Calculate the current normal tax for 20X1 and 20X2. C. Show the related journal entries in ledger account format. D. Disclose the tax adjustments for the 20X2 financial year. Solution to example 4A: expenses prepaid (deferred tax)

Rule for assets: expenses prepaid (IAS 12): The tax base of an asset (that represents an expense) is the amount that will be deducted for tax purposes against any taxable economic benefits that will flow to an entity when it recovers the carrying amount of the asset. If those economic benefits will not be taxable, the tax base of the asset is equal to its carrying amount (e.g. an investment that renders dividend income). Applying the rule to the calculation of the tax base (expenses prepaid): 20X1 tax base: C

Carrying amount 8 000 Less amount already deducted from taxable profits (deducted in current year: 20X1) (8 000) Deduction from taxable profits in the future 0

20X2 tax base:

Carrying amount 0 Less that which won’t be deducted for tax purposes in the future 0 0

The carrying amount will now be zero since the expense was incurred in 20X2 with the asset balance transferred to an expense account (see journal 1 in the 20X2 t-accounts).

Calculation of Deferred tax (balance sheet approach): Expenses prepaid Carrying

amount (per SOFP)

(a)

Tax base

(IAS 12) (b)

Temporary difference (b) – (a)

(c)

Deferred tax at 30% (c) x 30%

(d)

Deferred tax balance/

adjustment

Opening balance: 20X1 0 0 0 0 Movement (balancing) 8 000 0 (8 000) (2 400) cr FP; dr CI (3) Closing balance: 20X1 (1) 8 000 0 (8 000) (2 400) Liability (2)

Gripping IFRS Deferred taxation

Chapter 3

105

Solution to example 4B: expenses prepaid (current tax) Calculation of current normal tax: 20X1 The prepayment of C8 000 is allowed as a deduction by the tax authority in 20X1 but the accountant recognises the C8 000 as a prepaid expense, (an asset), thus causing a temporary difference. Profits Tax at 30% Profit before tax (accounting profits) (1) 20 000 Adjusted for permanent differences: 0 Taxable accounting profits and tax expense (1) 20 000 6 000 Adjusted for movement in temporary differences: (3) (8 000) (3) (2 400) Less expense prepaid (closing balance): deductible in current year 20X1 (8 000) Taxable profits and current normal tax (6) 12 000 3 600 Calculation of current normal tax: 20X2 The accountant recognises (deducts) the C8 000 as an expense in 20X2 since this is the period in which the expense is incurred but the tax authority, having already allowed the deduction of the expense in 20X1, will not deduct it again in 20X2. The difference in 20X2 reverses the difference in 20X1. Profits Tax at 30% Profit before tax (accounting profits) (20 000 – 8 000) (4) 12 000 Adjusted for permanent differences: 0 Taxable accounting profits and tax expense (4) 12 000 3 600 Adjusted for movement in temporary differences: (5) 8 000 (5) 2 400 Add expense prepaid (opening balance): deducted in prior year 20X1 8 000 Taxable profits and current normal tax (7) 20 000 6 000 Solution to example 4C: expenses prepaid (ledger accounts) Ledger accounts: 20X1

Bank Expenses prepaid (A) Exp Prepaid(1) 8 000 Bank (1) 8 000

Tax: normal tax (E) Current tax payable: normal tax (L) CTP: NT(6) 3 600 Tax (6) 3 600 DT (3) 2 400 Total 6 000

Deferred tax (L) Tax (3) 2 400 T-accounts: 20X2

Electricity and water Expenses prepaid (A) EP(4) 8 000 Balance b/f 8 000 E&W (4) 8 000

Tax: normal tax (E) Current tax payable: normal tax (L) CTP: NT(7) 6 000 DT (5) 2 400 Bank (8) 3 600 Balance 3 600 _____ Total c/f 3 600 Tax (7) 6 000 6 000 6 000 Total b/f 3 600

Deferred tax (L) Bank Tax (5) 2 400 Balance b/d 2 400 CTP: NT (8) 3 600

Gripping IFRS Deferred taxation

Chapter 3

106

Comments on example 4 A, B and C 1) The accountant treats the payment as an asset since the expense has not yet been incurred

whereas the tax authority treats the payment as an expense and therefore has no asset account.

2) This represents a deferred tax liability since it represents a premature tax saving (received before the related expense is incurred).

3) In order to create a deferred tax credit balance, the deferred tax liability must be credited and the tax expense debited.

4) The expense is incurred in 20X2, so the expense prepaid (asset) is reversed out to electricity expense (reducing profits). Now both accountant and tax authority have zero balances on the expense prepaid (asset) account and so there is no longer a temporary difference and thus a zero deferred tax balance.

5) In order to adjust a deferred tax credit balance to a zero balance, the liability must be debited and the tax expense credited.

6) Current tax charged by the tax authority in 20X1. 7) Current tax charged by the tax authority in 20X2. 8) Payment of the balance owing to the tax authority for 20X1 (the prior year).

It can be seen that over 2 years: • the accountant recognises tax expense of C9 600 (6 000 + 3 600) as incurred; and this equals • the actual tax charged by the tax authority over 2 years is C9 600 (3 600 + 6 000). The difference relates purely to when the tax is incurred versus when the tax is charged, thus the difference reverses out once the tax has both been charged and incurred. Solution to example 4D: expenses prepaid (disclosure)

Company name Statement of financial position As at 31 December 20X2

ASSETS Note 20X2

C 20X1

C Current assets

Expense prepaid 0 8 000 LIABILITIES Non-current liabilities

Deferred tax: normal tax 6 0 2 400 Current liabilities

Current tax payable: normal tax 6 000 3 600

Company name Statement of comprehensive income (extracts) For the year ended 31 December 20X2

Note 20X2 C

20X1 C

Profit before taxation 20X2: 20 000 – 8 000 12 000 20 000 Taxation expense 5 3 600 6 000 Profit for the year 8 400 14 000 Other comprehensive income 0 0 Total comprehensive income 8 400 14 000

Company name Notes to the financial statements (extracts) For the year ended 31 December 20X2

5. Taxation expense 20X2

C 20X1

C Normal taxation 3 600 6 000 • current 6 000 3 600 • deferred (2 400) 2 400 Total tax expense per the statement of comprehensive income 3 600 6 000

Gripping IFRS Deferred taxation

Chapter 3

107

6. Deferred tax asset/ (liability) The closing balance is constituted by the effects of: • Year-end accruals 0 (2 400)

It can be seen that the deferred tax effect on profits is nil over the period of the two years.

2.3.2 Expenses payable The tax authority generally allows expenses to be deducted when they have been incurred irrespective of whether or not the amount incurred has been paid. This is the accrual system and therefore there will be no deferred tax on an expense payable balance. Example 5: expenses payable Profit before tax is C20 000 in 20X1 and in 20X2, according to the accountant and the tax authority, before taking into account the following information: • A telephone expense of C4 000, incurred in 20X1, is paid in 20X2. • The Receiver will allow the expense of C4 000 to be deducted from the 20X1 taxable

profits. • The current tax owing to the tax authorities is paid in the year after it is charged. • There are no permanent or other temporary differences and no taxes other than normal tax

at 30%. • There are no components of other comprehensive income Required: A. Calculate the Deferred tax for 20X1 and 20X2 using the balance sheet approach. B. Calculate the current normal tax for 20X1 and 20X2. C. Show the related journal entries in ledger account format. D. Disclose the tax adjustments for the 20X2 financial year. Solution to example 5A: expenses payable (deferred tax) Rule for liabilities: expenses payable (IAS 12 adapted): The tax base of a liability (representing expenses) is its carrying amount less any amount that will be deductible for tax purposes in respect of that liability in future periods. Applying the rule to the example (expenses payable):

20X1 tax base: C Carrying amount 4 000 Less deductible in the future (all deducted in the current year) 0 4 000

20X2 tax base: Carrying amount 0 Less deductible in the future (already deducted in 20X1) 0 0 The carrying amount will now be zero since the expense was paid in 20X2 with the balance on the liability account being reversed.

Calculation of Deferred tax (balance sheet approach):

Expenses payable

Carrying amount

(per SOFP) (a)

Tax base

(IAS 12) (b)

Temporary difference (b) – (a)

(c)

Deferred tax at 30% (c) x 30%

(d)

Deferred tax balance/ adjustment

Opening balance: 20X1 0 0 0 0 N/A Movement (balancing) (4 000) (4 000) 0 0 N/A Closing balance:20X1 (3) (4 000) (4 000) 0 0 N/A Movement (balancing) 4 000 4 000 0 0 N/A Closing balance: 20X2(5) 0 0 0 0 N/A

Gripping IFRS Deferred taxation

Chapter 3

108

Solution to example 5B: expenses payable (current tax) Calculation of current normal tax: 20X1 Since the telephone expense is recognised as an expense and is also deducted for tax purposes in 20X1, the effect on accounting profits and taxable profits is identical. There is, therefore, no deferred tax. Profits Tax at

30% Profit before tax (accounting profits) (20 000 – 4 000) (1) 16 000 Adjusted for permanent differences: 0 Taxable accounting profits and tax expense (1) 16 000 4 800 Adjusted for temporary differences: (3) 0 0 Taxable profits and current normal tax (2) 16 000 4 800 Calculation of current normal tax: 20X2 Since the telephone expense is recognised as an expense in the statement of comprehensive income in 20X1, it will have no impact on the statement of comprehensive income in 20X2. Similarly, since the telephone expense is deducted for tax purposes in 20X1, it will not be deducted for tax purposes in 20X2. Since the effect on accounting profits and taxable profit is the same, there is no deferred tax.

Profits Tax at 30% Profit before tax (accounting profits) (4) 20 000 Adjusted for permanent differences: 0 Taxable accounting profits and tax expense 20 000 6 000 Adjusted for movement in temporary differences: (6) 0 0 Taxable profits and current normal tax (5) 20 000 6 000 Solution to example 5C: expenses payable (ledger accounts) Ledger accounts - 20X1

Telephone Expenses payable (L) EP(1) 4 000 Tel (1) 4 000

Tax: normal tax (E) Current tax payable: normal tax (L) CTP: NT(2) 4 800 Tax (2) 4 800 Ledger accounts – 20X2

Bank Expenses payable (L) EP(4) 4 000 Bank(4) 4 000 Balance b/f 4 000 CTP: NT (7) 4 800

Tax: normal tax (E) Current tax payable: normal tax (L) CTP: NT(5) 6 000 Bank (7) 4 800 Balance 4 800 Tax (5) 6 000 Comments on example 5A, B and C (1) The telephone expense is incurred but not paid in 20X1 and is therefore recognised as an expense

and expense payable in 20X1. (2) Current tax charged by the tax authority in 20X1. (3) Since the accountant and tax authority both treat the expense payable as an expense in the

calculation of profits, there is no temporary difference and therefore no deferred tax adjustment. (4) Notice that although the telephone expense is paid in 20X2, the payment is not taken into account

in the calculation of the profits for 20X2. The payment of the expense in 20X2 simply results in the reversal of the expense payable account.

(5) Current tax charged by the tax authority in 20X2. (6) Since the tax authority has treated the expense in the same manner as the accountant, there is no

temporary difference and therefore no deferred tax adjustment. (7) The balance owing to the tax authority at the end of 20X1 is paid in 20X2.

Gripping IFRS Deferred taxation

Chapter 3

109

Solution to example 5D: expenses payable (disclosure) Company name Statement of financial position As at 31 December 20X2

LIABILITIES Note 20X2

C 20X1

C Current liabilities

Expense payable 0 4 000 Current tax payable: normal tax 6 000 4 800

Company name Statement of comprehensive income (extracts) For the year ended 31 December 20X2

Note 20X2 C

20X1 C

Profit before taxation 20X1: 20 000 – 4 000 20 000 16 000 Taxation expense 5 6 000 4 800 Profit for the year 14 000 11 200 Other comprehensive income

0 0

Total comprehensive income

14 000 11 200

Company name Notes to the financial statements (extracts) For the year ended 31 December 20X2

5. Taxation expense 20X2

C 20X1

C Normal taxation 6 000 4 800 • Current 6 000 4 800 • Deferred 0 0 Total tax expense per the statement of comprehensive income

6 000 4 800

2.3.3 Provisions

Although the tax authority generally allows expenses to be deducted when they have been incurred, he often treats the deduction of provisions with more ‘suspicion’. In cases such as this, the tax authority generally allows the provision to be deducted only when it is paid. Example 6: provisions Profit before tax is C20 000 in 20X1 and in 20X2, according to the accountant and the tax authority, before taking into account the following information: • A provision for warranty costs of C4 000 is journalised in 20X1 and paid in 20X2. • The tax authority will allow the warranty costs to be deducted only once paid. • The current tax owing to the tax authority is paid in the year after it is charged. • There are no permanent differences, no other temporary differences and no taxes other

than normal tax at 30%. • There are no components of other comprehensive income.

Required: A. Calculate the Deferred tax using the balance sheet approach. B. Calculate the current normal tax for 20X1 and 20X2. C. Show the related ledger accounts. D. Disclose the above information.

Gripping IFRS Deferred taxation

Chapter 3

110

Solution to example 6A provisions (deferred tax) Rule for liabilities: provisions (IAS 12 adapted) The tax base of a liability (representing expenses) is its carrying amount less any amount that will be deductible for tax purposes in respect of that liability in future periods. Applying the rule to the calculation of the tax base (provisions)

20X1 tax base: C Carrying amount 4 000 Less deductible in the future (all will be deducted in the future: 20X2) 4 000 0

20X2 tax base: Carrying amount 0 Less deductible in the future (all deducted in 20X2 since now paid) 0 0

The carrying amount will now be zero since the expense was paid in 20X2 with the balance on the liability account being reversed.

Calculation of Deferred tax (balance sheet approach)

Provision for warranty costs

Carrying amount

(per SOFP) (a)

Tax base

(IAS 12) (b)

Temporary difference (b) – (a)

(c)

Deferred tax at 30% (c) x 30%

(d)

Deferred tax

balance/ adjustment

Opening balance – 20X1 0 0 0 0 Movement (balancing) (4 000) 0 4 000 1 200 dr FP; cr CI (3) Closing balance – 20X1 (1) (4 000) 0 4 000 1 200 Asset (2) Movement (balancing) 4 000 0 (4 000) (1 200) cr FP; dr CI (7) Closing balance – 20X2 (5) 0 0 0 0 Solution to example 6B: provisions (current tax) Calculation of current normal tax: 20X1 Since in 20X1 the tax authority disallows the provision and the accountant recognises the provision, the accounting profits will be less than the taxable profits in 20X1. Profits Tax at

30% Profit before tax (accounting profits) (20 000 – 4 000) (1) 16 000 Adjusted for permanent differences: 0 Taxable accounting profits and tax expense 16 000 4 800 Adjusted for movement in temporary differences: (3) 4 000 1 200 • Add back provision for an expense disallowed in 20X1 4 000 Taxable profits and current normal tax (4) 20 000 6 000 Calculation of current normal tax: 20X2 The difference that arose in 20X1 will reverse in 20X2 when the tax authority allows the deduction of the provision since the taxable profits will now be less than the accounting profits (the provision will not affect the statement of comprehensive income again in 20X2). 20X2 Profits Tax at 30% Profit before tax (accounting profits) 20 000 Adjusted for permanent differences: 0 Taxable accounting profits and tax expense 20 000 6 000 Adjusted for movement in temporary differences: (7) (4 000) (1 200) - provision for warranty cost allowed in 20X2 (4 000) Taxable profits and current normal tax (6) 16 000 4 800

Gripping IFRS Deferred taxation

Chapter 3

111

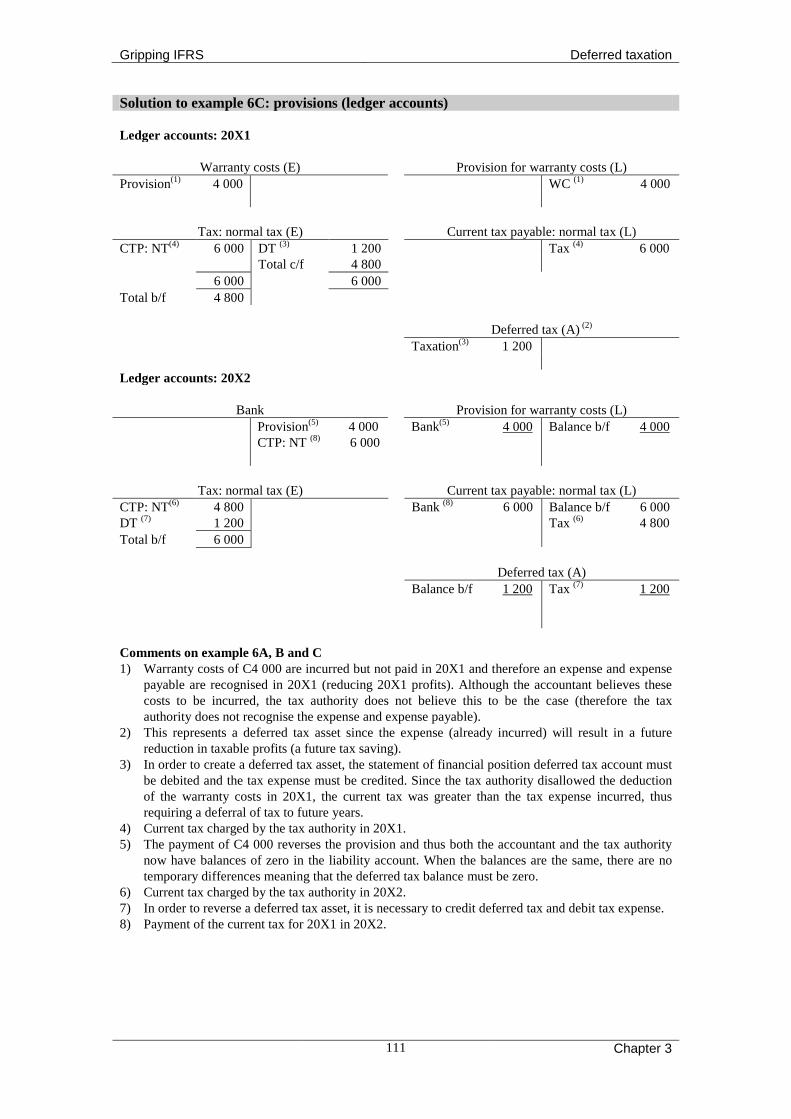

Solution to example 6C: provisions (ledger accounts) Ledger accounts: 20X1

Warranty costs (E) Provision for warranty costs (L) Provision(1) 4 000 WC (1) 4 000

Tax: normal tax (E) Current tax payable: normal tax (L) CTP: NT(4) 6 000 DT (3) 1 200 Tax (4) 6 000 Total c/f 4 800

6 000 6 000 Total b/f 4 800 Deferred tax (A) (2) Taxation(3) 1 200 Ledger accounts: 20X2

Bank Provision for warranty costs (L) Provision(5) 4 000 Bank(5) 4 000 Balance b/f 4 000 CTP: NT (8) 6 000

Tax: normal tax (E) Current tax payable: normal tax (L) CTP: NT(6) 4 800 Bank (8) 6 000 Balance b/f 6 000 DT (7) 1 200 Tax (6) 4 800 Total b/f 6 000

Deferred tax (A)

Balance b/f 1 200 Tax (7) 1 200 Comments on example 6A, B and C 1) Warranty costs of C4 000 are incurred but not paid in 20X1 and therefore an expense and expense

payable are recognised in 20X1 (reducing 20X1 profits). Although the accountant believes these costs to be incurred, the tax authority does not believe this to be the case (therefore the tax authority does not recognise the expense and expense payable).

2) This represents a deferred tax asset since the expense (already incurred) will result in a future reduction in taxable profits (a future tax saving).

3) In order to create a deferred tax asset, the statement of financial position deferred tax account must be debited and the tax expense must be credited. Since the tax authority disallowed the deduction of the warranty costs in 20X1, the current tax was greater than the tax expense incurred, thus requiring a deferral of tax to future years.

4) Current tax charged by the tax authority in 20X1. 5) The payment of C4 000 reverses the provision and thus both the accountant and the tax authority

now have balances of zero in the liability account. When the balances are the same, there are no temporary differences meaning that the deferred tax balance must be zero.

6) Current tax charged by the tax authority in 20X2. 7) In order to reverse a deferred tax asset, it is necessary to credit deferred tax and debit tax expense. 8) Payment of the current tax for 20X1 in 20X2.

Gripping IFRS Deferred taxation

Chapter 3

112

Solution to example 6D: provisions (disclosure) Company name Statement of financial position As at 31 December 20X2

ASSETS Note 20X2

C 20X1

C Non-current assets

Deferred tax: normal tax 6 0 1 200 LIABILITIES Current liabilities

Provision for warranty costs 0 4 000 Current tax payable: normal tax 4 800 6 000

Company name Statement of comprehensive income (extracts) For the year ended 31 December 20X2

Note 20X2 C

20X1 C

Profit before taxation (20X1: 20 000 – 4 000) 20 000 16 000 Taxation expense 5 6 000 4 800 Profit for the year 14 000 11 200 Other comprehensive income 0 0 Total comprehensive income 14 000 11 200 Company name Notes to the financial statements (extracts) For the year ended 31 December 20X2

5. Taxation expense 20X2

C 20X1

C

Normal taxation 6 000 4 800 • Current 4 800 6 000 • Deferred 1 200 (1 200) Total tax expense per the statement of comprehensive income

6 000 4 800

6. Deferred tax asset/ (liability)

The closing balance is constituted by the effects of: • Year-end accruals 0 1 200

It can be seen that the deferred tax effect on profits is nil over the period of the two years.

2.3.4 Income receivable The tax authority generally taxes income on the earlier of the date the income is earned or the date it is received. Therefore the taxable income will equal the accounting income if the income is received on time or is receivable (as opposed to received in advance) and therefore there will be no deferred tax on an income receivable balance.

Gripping IFRS Deferred taxation

Chapter 3

113

Example 7: income receivable Profit before tax is C20 000 in 20X1 and in 20X2, according to the accountant and the tax authority, before taking into account the following information: • Interest income of C6 000 is earned in 20X1 but only received in 20X2. • The tax authority will tax the interest income when earned. • The current tax owing to the tax authorities is paid in the year after it is charged. • There are no permanent or other temporary differences and no taxes other than normal tax

at 30%. • There are no components of other comprehensive income. Required: A. Calculate the Deferred tax using the balance sheet approach. B. Calculate the current normal tax for 20X1 and 20X2. C. Show the related ledger accounts. D. Disclose the above information. Solution to example 7A: income receivable (deferred tax) Rule for assets: income receivable: The tax base of an asset (that represents an income) is the carrying amount less that portion that will be taxed in the future. Applying the rule to the calculation of the tax base (income receivable):

20X1 tax base: C Carrying amount 6 000 Less portion that will be taxed in the future (all taxed in current year: 20X1) 0 6 000

20X2 tax base: Carrying amount 0 Less portion that will be taxed in the future (all taxed in 20X1) 0 0 The carrying amount will now be zero since the income receivable was received in 20X2 (see journal 1 in the 20X2 ledger accounts).

Calculation of Deferred tax (balance sheet approach): Income receivable

Carrying amount

(per SOFP) (a)

Tax base

(IAS 12) (b)

Temporary difference (b) – (a)

(c)

Deferred tax at 30% (c) x 30%

(d)

Deferred tax

balance/ adjustment

Opening balance – 20X1 0 0 0 0 N/A Movement (balancing) 6 000 6 000 0 0 N/A Closing balance – 20X1 (1) 6 000 6 000 0 0 N/A Movement (balancing) (6 000) (6 000) 0 0 N/A Closing balance – 20X2 (3) 0 0 0 0 N/A Solution to example 7B: income receivable (current tax) Since the tax authority taxes income either on the date it is received or on the date it is earned, whichever is earlier, the interest income will be taxable in 20X1. The accountant records income when it is earned and since the interest income is earned in 20X1, the accountant will record the income in 20X1. The accountant and tax authority therefore treat the interest income in the same way with the result that there are no deferred tax consequences.

Gripping IFRS Deferred taxation

Chapter 3

114

Calculation of current normal tax: 20X1 Profits Tax at 30% Profit before tax (accounting profits) (20 000 + 6 000) (1) 26 000 Adjusted for permanent differences: 0 Taxable accounting profits and tax expense 26 000 7 800 Adjusted for movement in temporary differences: (1) 0 0 Taxable profits and current normal tax (2) 26 000 7 800

Calculation of current normal tax: 20X2 Profits Tax at

30% Profit before tax (accounting profits) (3) 20 000 Adjusted for permanent differences: 0 Taxable accounting profits and tax expense 20 000 6 000 Adjusted for movement in temporary differences: (3) 0 0 Taxable profits and current normal tax (4) 20 000 6 000 Solution to example 7C: income receivable (ledger accounts) 20X1

Income receivable (A) Interest income (I) Int income(1) 6 000 Inc receivable(1) 6 000

Tax: normal tax (E) Current tax payable: normal tax (L) CTP: NT(2) 7 800 Tax (2) 7 800 20X2

Income receivable (A) Bank Balance b/d 6 000 Bank (3) 6 000 Int receivable (3) 6 000 CTP (5) 7 800

Tax: normal tax (E) Current tax payable: normal tax (L) CTP: NT(4) 6 000 Bank (5) 7 800 Balance b/d 7 800 Tax (4) 6 000 Comments on example 7A, B and C 1) Since the income is treated as income by both the accountant and the tax authority in

20X1 and yet it hasn’t been received, both the accountant and the tax authority have the same income receivable account. There are therefore no temporary differences or deferred tax.

2) Current tax for 20X1. 3) Since the income is received, the receipt reverses the income receivable account to zero

(in both the accountant’s and tax authority’s books). There are therefore still no temporary differences or deferred tax.

4) Current tax for 20X2. 5) Payment of current tax for 20X1 in 20X2.

Gripping IFRS Deferred taxation

Chapter 3

115

Solution to example 7D: income receivable (disclosure) Company name Statement of financial position As at 31 December 20X2

ASSETS Note 20X2

C 20X1

C Current assets

Income receivable 0 6 000 LIABILITIES Current liabilities

Current tax payable: normal tax 6 000 7 800 Company name Statement of comprehensive income (extracts) For the year ended 31 December 20X2

Note 20X2 C

20X1 C

Profit before taxation (20X1: 20 000 + 6 000) 20 000 26 000 Taxation expense 5 6 000 7 800 Profit for the year 14 000 18 200 Other comprehensive income 0 0 Total comprehensive income 14 000 18 200 Company name Notes to the financial statements (extracts) For the year ended 31 December 20X2

5. Taxation expense 20X2

C 20X1

C Normal taxation 6 000 7 800 • Current 6 000 7 800 • Deferred 0 0 Total tax expense per the statement of comprehensive income

6 000 7 800

2.4 Depreciable non-current assets and deferred tax 2.4.1 Depreciation versus capital allowances The accountant expenses (deducts from income) the cost of non-current assets through the use of depreciation and the tax authority allows (deducts from income) the cost of non-current assets through the use of depreciation for tax purposes. Depreciation in the tax records may be referred to in many different ways, for example it may be referred to as wear and tear, capital allowances or depreciation for tax purposes. For ease of reference, this text will generally refer to the depreciation for tax purposes as capital allowances. The difference between depreciation in the accounting records and capital allowances (depreciation in the tax records) is generally a result of the differences in the rate or method of depreciation. For example, the rate of depreciation in the accounting records may be 15% using the reducing balance method, whereas the rate of capital allowance may be 10% using the straight-line method. Another difference may arise when depreciation is apportioned for a period that is less than one year, if the capital allowance in the tax records is not apportioned for part of the year. Over a period of time, however, the accountant and the tax authority will generally expense the cost of the asset, meaning that any difference arising between the depreciation and capital allowance in any one year is just a temporary difference.

Gripping IFRS Deferred taxation

Chapter 3

116

Example 8: depreciable assets

Profit before tax is C20 000, according to both the accountant and the tax authority, in each of the years 20X1, 20X2 and 20X3, before taking into account the following information: • A plant was purchased on 1 January 20X1 for C30 000 • The plant is depreciated by the accountant at 50% p.a. straight-line. • The tax authority allows a capital allowance thereon at 33 1/3 % straight-line. • This company paid the tax authority the current tax owing in the year after it was charged. • The normal income tax rate is 30%. • There are no components of other comprehensive income.

Required: A. Calculate the Deferred tax using the balance sheet approach. B. Calculate the current normal tax for 20X1, 20X2 and 20X3. C. Show the related ledger accounts. D. Disclose the above in as much detail as is possible for all three years. Solution to example 8A: depreciable assets (deferred tax) Rule for assets: depreciable assets (per IAS 12): The tax base of an asset is the amount that will be deducted for tax purposes against any taxable economic benefits that will flow to an entity when it recovers the carrying amount of the asset. If those economic benefits will not be taxable, the tax base of the asset is equal to its carrying amount (e.g. an investment that renders dividend income). Applying the rule to the calculation of the tax base (depreciable assets): 20X1: Tax base: C

Original cost 30 000 Less accumulated capital allowances (30 000 x 33 1/3 % x 1year) 10 000 Deductions still to be made (decrease in taxable profits in the future) 20 000

Carrying amount: C

Original cost 30 000 Less accumulated depreciation (30 000 x 50%) 15 000 Expenses still to be incurred (decrease in accounting profits in the future) 15 000

20X2: Tax base: C

Original cost 30 000 Less accumulated capital allowances (10 000 x 2 years) 20 000 Deductions still to be made 10 000

Carrying amount: C

Original cost 30 000 Less accumulated depreciation (15 000 x 2 years) 30 000 Expenses still to be incurred 0

20X3: Tax base: C

Original cost 30 000 Less accumulated capital allowances (10 000 x 3 years) 30 000 Deductions still to be made 0

Carrying amount: C

Original cost 30 000 Less accumulated depreciation (15 000 x 2yrs) (fully depreciated at

31/12/20X2) 30 000

Expenses still to be incurred 0

Gripping IFRS Deferred taxation

Chapter 3

117

Calculation of Deferred tax (balance sheet approach): Depreciable assets Carrying

amount (per SOFP)

(a)

Tax base

(IAS 12) (b)

Temporary difference (b) – (a)

(c)

Deferred tax at 30% (c) x 30%

(d)

Deferred tax

balance/ adjustment

Opening balance: 20X1 Purchase 30 000 30 000 Depreciation/ capital allowances (1)

(15 000) (10 000) 5 000 1 500 dr FP; cr CI

Closing balance: 20X1 (2) 15 000 20 000 5 000 1 500 Asset (2) Depreciation/ capital allowances (1)

(15 000) (10 000) 5 000 1 500 dr FP; cr CI

Closing balance: 20X2 (2) 0 10 000 10 000 3 000 Asset (2) Depreciation/ capital allowances (4)

0 (10 000) (10 000) (3 000) cr FP; dr CI

Closing balance: 20X3 (5) Solution to example 8B: depreciable assets (current tax) Calculation of current normal tax: 20X1 Profits Tax at 30% Profit before tax (accounting profits) (20 000 - 15 000) (1) 5 000 Adjusted for permanent differences: 0 Taxable accounting profits and tax expense 5 000 1 500 Adjusted for movement in temporary differences: (1) 5 000 1 500 - add back depreciation (30 000 x 50%) 15 000 - less capital allowances (30 000 x 33 1/3%) (10 000) Taxable profits and current normal tax (3) 10 000 3 000 Calculation of current normal tax: 20X2 Profits Tax at 30% Profit before tax (accounting profits) (20 000 - 15 000) (1) 5 000 Adjusted for permanent differences: 0 Taxable accounting profits and tax expense 5 000 1 500 Adjusted for movement in temporary differences: (1) 5 000 1 500 - add back depreciation (30 000 x 50%) 15 000 - less capital allowances (30 000 x 33 1/3%) (10 000) Taxable profits and current normal tax (3) 10 000 3 000 Calculation of current normal tax: 20X3 Profits Tax at 30% Profit before tax (accounting profits) (asset fully depreciated) (4) 20 000 Adjusted for permanent differences: 0 Taxable accounting profits and tax expense 20 000 6 000 Adjusted for movement in temporary differences: (4) (10 000) (3 000) - add back depreciation (the asset is fully depreciated) 0 - less capital allowances (30 000 x 33 1/3%) (10 000) Taxable profits and current normal tax (6) 10 000 3 000

Gripping IFRS Deferred taxation

Chapter 3

118

Solution to example 8C: depreciable assets (ledger accounts)

Tax: normal tax (E) Current tax payable: normal tax (L) 20X1 20X1 Tax (3) 3 000 CTP: NT (3) 3 000 DT (2) 1 500 Balance c/f 3 000 Total 1 500 P & L 1 500 3 000 3 000 20X2 20X2 Bank 3 000 Balance b/f 3 000 CTP: NT (3) 3 000 DT (2) 1 500 Balance c/f 3 000 20X2 Tax (3) 3 000 Total 1 500 P & L 1 500 6 000 6 000 20X3 20X3 Bank 3 000 Balance b/f 3 000 CTP: NT (6) 3 000 20X3 Tax (6) 3 000 DT (5) 3 000 Balance c/f 6 000 6 000 Total 6 000 P & L 6 000 Balance b/f 3 000

Deferred tax (A) 20X1 Tax (2) 1 500 20X2 Tax (2) 1 500 20X3 Tax (5) 3 000 3 000 3 000

Depreciation (E) Plant: cost (A) 20X1 20X1 Bank 30 000 Plant: AD (1) 15 000 P & L 15 000 20X2 Plant: AD (1) 15 000 P & L 15 000

Plant: accumulated depreciation (A) 20X1 Depr(1) 15 000 20X2 Depr(1) 15 000 Balance 30 000 Comments on example 8A, B and C (1) The tax authority allows a capital allowance at 33 1/3% of the cost per year whereas the accountant

allows depreciation at 50% of the cost per year in 20X1 and 20X2. (2) The fact that the depreciation and capital allowance are not the same amount results in temporary

differences and deferred tax. This represents a deferred tax asset since the future tax deductions (20X1: C20 000 and 20X2: C10 000) are greater than the tax effect of the future economic benefits recognised in the statement of financial position (20X1: C15 000 and 20X2: C0). This asset is therefore similar to an expense prepaid since the current tax has been greater than the tax incurred in 20X1 and 20X2.

(3) Current tax of C3 000 is recorded in 20X1 and 20X2. (4) The tax authority allows a capital allowance at 33 1/3% of the cost per year whereas the accountant

allows depreciation at 50% of the cost per year. Notice that the accountant did not write off depreciation in 20X3 since the asset was fully depreciated at the end of 20X2.

(5) At the end of 20X3, both the carrying amount and tax base of the asset are zero. The deferred tax

balance of C3 000 must therefore be reversed. (6) Current tax of C6 000 is recorded in 20X3.

Gripping IFRS Deferred taxation

Chapter 3

119

Solution to example 8D: depreciable assets (disclosure) Entity name Statement of comprehensive income For the year ended 20X3

Note 20X3 C

20X2 C

20X1 C

Profit before tax 20 000 5 000 5 000 Taxation expense 3 6 000 1 500 1 500 Profit for the period 14 000 3 500 3 500 Other comprehensive income 0 0 0 Total comprehensive income 14 000 3 500 3 500 Entity name Statement of financial position As at …20X3

ASSETS Note 20X3

C 20X2

C 20X1

C Non-current assets Deferred tax: normal tax 4 0 3 000 1 500 Property, plant and equipment 0 0 15 000 LIABILITIES Current liabilities Current tax payable: normal tax 3 000 3 000 3 000 Entity name Notes to the financial statements For the year ended …20X3

20X3 20X2 20X1 3. Taxation expense C C C

Normal taxation expense 6 000 1 500 1 500 • Current 3 000 3 000 3 000 • Deferred 3 000 (1 500) (1 500)

4. Deferred tax asset The closing balance is constituted by the effects of:

• Property, plant and equipment 0 3 000 1 500 Notice that over the three years, the capital allowances (10 000 x 3 years = 30 000) equals the depreciation (15 000 x 2 years = 30 000). Similarly, the current tax charged by the tax authority (3 000 x 3 years = 9 000) equals the tax expense (1 500 + 1 500 + 6 000 = 9 000). 2.5 Rate changes and deferred tax A deferred tax balance is simply an estimate of the tax owing to the tax authority in the long-term or the tax savings expected from the tax authority in the long-term. The estimate is made based on the temporary differences multiplied by the applicable tax rate. If this tax rate changes, so does the estimate of the amount of tax owing by or owing to the tax authority in the future. Therefore, if a company has a deferred tax balance at the beginning of a year during which the rate of tax changes, the opening balance of the deferred tax account will need to be re-estimated. This is effectively a change in accounting estimate, the adjustment for which is processed in the current year’s accounting records. Since the tax expense account in the current year will include an adjustment to the deferred tax balance from a prior year, the effective rate of tax in the current year will not equal the applicable tax rate. The difference between the effective and the applicable rate of tax results in the need for a tax rate reconciliation in the tax note.

Gripping IFRS Deferred taxation

Chapter 3

120

Example 9: rate changes – date of substantive enactment A change in the corporate normal tax rate from 30% to 29% is announced on 20 January 20X1. No significant changes were announced to other forms of tax. The new tax rate will apply to tax assessments ending on or after 1 March 20X1. Required: State at what rate the current and deferred tax balances should be calculated assuming: A. The company’s year of assessment ends on 31 December 20X0. B. The company’s year of assessment ends on 28 February 20X1. C. The company’s year of assessment ends on or after 31 March 20X1. Solution to example 9: rate changes – date of substantive enactment • The date of substantive enactment is 20 January 20X1 (no significant changes to other

taxes were announced at the time). • The effective date is 1 March 20X1

A B C Year end:

31 December 20X0

Year end: 28 February

20X1

Year end: 31 March

20X1 Current tax payable/ receivable 30% 30% 29% Deferred tax liability/ asset 30% 29% 29% Explanations: (1) (2) (3) Explanations: 1) Since the year ends before the effective date of the rate change, the current tax payable

will still be based on the old rate. Since the year ends before the date of substantive enactment, the deferred tax balance must still be estimated based on the old rate although a subsequent event note should be included to explain that the deferred tax balances will be reduced in the future due to a rate change that occurred after the end of the reporting period.

2) Since the year ends before the effective date of the rate change, the current tax payable will still be based on the old rate. Since the year ends after the date of substantive enactment, the deferred tax balance must be estimated using the new rate.

3) Since the year ends after the effective date of the rate change, the current tax payable will be based on the new rate. For the same reason, the deferred tax balance will be based on the new rate.

Example 10: rate changes The opening balance of deferred tax at the beginning of 20X2 is C45 000, credit and is due purely to temporary differences caused by capital allowances on the property, plant and equipment. • The tax rate in 20X1 was 45% but changed to 35% in 20X2. • The profit before tax in 20X2 is C200 000, all of which is taxable in 20X2. • No balance was owing to or from the tax authority at 31 December 20X1 and no

payments were made to or from the tax authority during 20X2. • There are no other temporary differences or permanent differences. • There are no components of other comprehensive income. Required: A. Calculate the effect of the rate change. B. Show the Calculation of Deferred tax using the balance sheet approach. C. Calculate the current normal tax for 20X2. D. Post the related journal in the ledger accounts. E. Disclose the above in the financial statements for the year ended 31 December 20X2.

Gripping IFRS Deferred taxation

Chapter 3

121

Solution to example 10A: rate change The opening balance in 20X2 (closing balance in 20X1) was calculated by multiplying the total temporary differences at the end of 20X1 by 45%. Therefore, the temporary differences (TD) provided for at the end of 20X1 are as follows:

Deferred tax balance = Temporary difference x applicable tax rate C45 000 = Temporary difference x 45% Temporary difference = C45 000/ 45% Temporary difference = C100 000

The credit balance means that the company is expecting the tax authority to charge them tax on the temporary difference of C100 000 in the future. If the tax rate is now 35%, the estimate of the tax we expect to pay on this C100 000 needs to be changed to:

Deferred tax balance = Temporary difference x applicable tax rate Deferred tax balance = C100 000 x 35% Deferred tax balance = C35 000

An adjustment to the deferred tax balance must be processed:

Deferred tax balance was 45 000 Balance: credit Deferred tax balance should now be

35 000 Balance: credit

Adjustment needed 10 000 Adjustment: debit deferred tax, credit tax expense

Solution to example 10B: rate change (deferred tax) Depreciable assets Carrying

amount (per FP)

(a)

Tax base

(IAS 12) (b)

Temporary difference (b) – (a)

(c)

Deferred tax at 30%

(c) x % (d)

Deferred tax balance/

adjustment

Opening balance @ 45% xxx xxx 100 000 45 000 Liability Rate change (100 000 x 10%) (10 000) dr FP; cr CI Opening balance @ 35% 100 000 35 000 Movement (there are no temporary differences in 20X2)

0 0 0 0