Chapter-3- DATA ANALYSIS AND...

120

67 CHAPTER – 3 Data Analysis and Interpretation Framework of Analysis 1. Financial health a. Profitability Ratios i. Gross Profit Ratio ii. Net Profit Ratio iii. Return on Assets iv. Return on Equity v. Return on Capital employed b. Financial Leverage Ratios i. Debt – Equity Ratio ii. Total Capitalisation c. Capital Market Ratios i. Earning per share ii. Price Earning ratio 2. Synergies a. Financial Synergy Standards i. Current Ratio ii. Quick Ratio iii. Interest Coverage iv. Total assets turnover ratio b. Managerial Synergy Standards i. Investment turnover ratio ii. Fixed assets turn over ratio iii. Total assets turn over ratio c. Operating synergy standards i. Operating Profit Margin 3. Firm Value ( Economic Value Added Model) 4. Value Added / Shortfall ( Economic Value Added Model) 5. Comparative study of overall performance

Transcript of Chapter-3- DATA ANALYSIS AND...

67

CHAPTER – 3

Data Analysis and Interpretation

Framework of Analysis 1. Financial health

a. Profitability Ratios

i. Gross Profit Ratio

ii. Net Profit Ratio

iii. Return on Assets

iv. Return on Equity

v. Return on Capital employed

b. Financial Leverage Ratios

i. Debt – Equity Ratio

ii. Total Capitalisation

c. Capital Market Ratios

i. Earning per share

ii. Price Earning ratio

2. Synergies a. Financial Synergy Standards

i. Current Ratio

ii. Quick Ratio

iii. Interest Coverage

iv. Total assets turnover ratio

b. Managerial Synergy Standards

i. Investment turnover ratio

ii. Fixed assets turn over ratio

iii. Total assets turn over ratio

c. Operating synergy standards

i. Operating Profit Margin

3. Firm Value ( Economic Value Added Model)

4. Value Added / Shortfall ( Economic Value Added Model)

5. Comparative study of overall performance

68

Figure: 3.1 Framework of Analysis

M&A Impact Analysis Model

Financial Health Firm Value

Ratio Analysis Economic Value Added Model

Profitability

Synergies

Leverage

- DER

- Total

Capitalisation

Capital

Market

- EPS

- PER

Financial

- GPR

- NPR

- ROA

- ROE

- ROCE

Managerial

Operational

- CR

- QR

- Interest

Coverage

-Market

Capitalisation

- ITOR

- FATOR

-TATOR

- OPM

- Economic Value Added

- Firm Value

-Value Added / Short Fall

Value added or shortfall

Financial Performance Standards

Synergy Performance Standards

69

This chapter intends to evaluate pre and post performance of select Mergers

and Acquisitions in terms of financial health, synergies, firm value and value addition

or shortfall. The analysis ensures long term survival. In this chapter, an analysis has

been done based on table 4.1. The individual objectives of the study are carried out in

the same order as during the study period. In this context, Mean and Co – efficient of

Variation are used to test volatility in pre and post period performance of the selected

companies.

Analysis of Financial Health

In order to identify the financial health in terms of changes in profitability, leverage

and capital market position after Mergers and Acquisitions studies have been made

separately for each group. However few ratios are used to identify the financial

performance. For convenience, the changes in financial health are identified and

called as financial performance metrics.

Financial performance metrics provide a relative basis for comparing a company over

a time. This analysis is to identify quantitative relations are to diagnose internal

strengths and weakness and help predict future financial performances. There are no

boundaries and hence useful to assessing the company’s performance throughout the

world.

Financial performance metrics considers strategic and economic developments for the

firm’s long-run success. These metrics should quickly provide actionable feedback to

improve the operations of the firm. A company is required to focus on these metrics

and represent the most important drivers of value creation. Long term induced

compensation was tied to attaining reliable levels of performance measured through

financial performance metrics.

Pre and post acquisition period financial performance metrics are computed for the

entire set of selected sample firms. This study involves relevant financial ratios which

are identified and categorised into various groups. Each group of ratios are deals with

important ratios by comparing the pre and post acquisition financial performance and

are shown as follows:

70

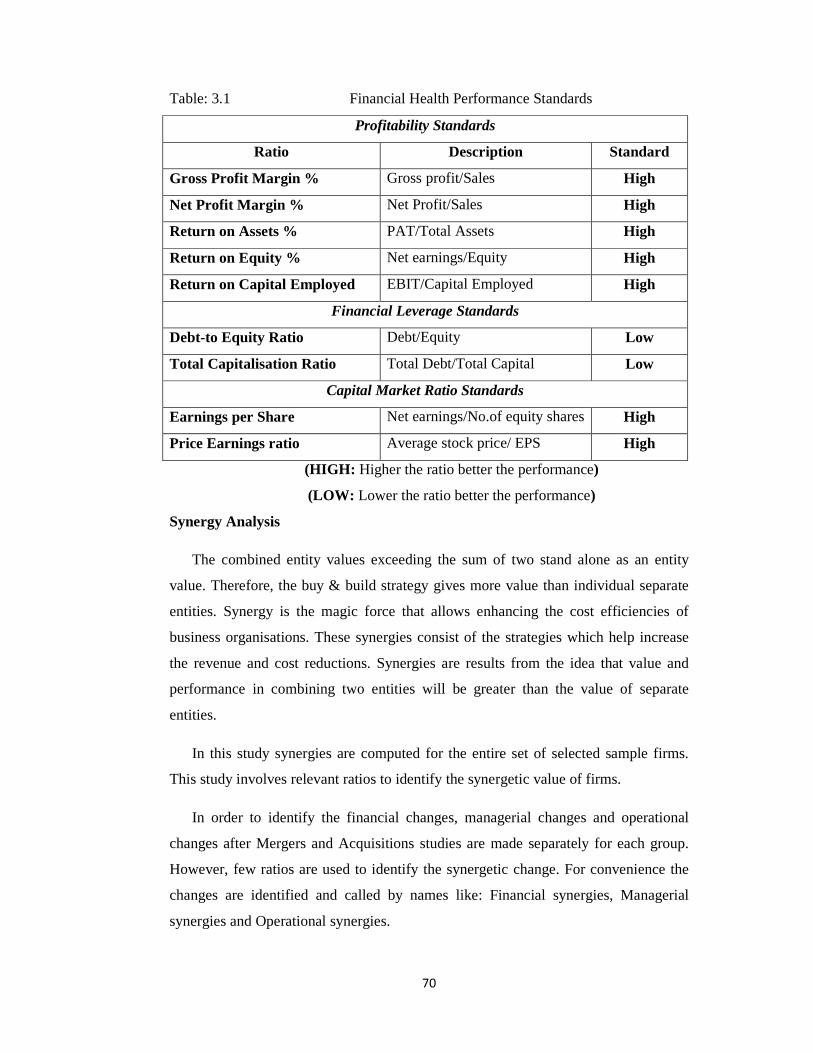

Table: 3.1 Financial Health Performance Standards

Profitability Standards

Ratio Description Standard

Gross Profit Margin % Gross profit/Sales High

Net Profit Margin % Net Profit/Sales High

Return on Assets % PAT/Total Assets High

Return on Equity % Net earnings/Equity High

Return on Capital Employed EBIT/Capital Employed High

Financial Leverage Standards

Debt-to Equity Ratio Debt/Equity Low

Total Capitalisation Ratio Total Debt/Total Capital Low

Capital Market Ratio Standards

Earnings per Share Net earnings/No.of equity shares High

Price Earnings ratio Average stock price/ EPS High

(HIGH: Higher the ratio better the performance)

(LOW: Lower the ratio better the performance)

Synergy Analysis

The combined entity values exceeding the sum of two stand alone as an entity

value. Therefore, the buy & build strategy gives more value than individual separate

entities. Synergy is the magic force that allows enhancing the cost efficiencies of

business organisations. These synergies consist of the strategies which help increase

the revenue and cost reductions. Synergies are results from the idea that value and

performance in combining two entities will be greater than the value of separate

entities.

In this study synergies are computed for the entire set of selected sample firms.

This study involves relevant ratios to identify the synergetic value of firms.

In order to identify the financial changes, managerial changes and operational

changes after Mergers and Acquisitions studies are made separately for each group.

However, few ratios are used to identify the synergetic change. For convenience the

changes are identified and called by names like: Financial synergies, Managerial

synergies and Operational synergies.

71

The below mentioned table indicates the positive changes. The referred ratios are

higher than the pre acquisition ratios of individual firms.

Table: 3.2 Synergy Ratio Standards

Financial Synergy Standards

Ratio Description Standard

Current Ratio Current Assets/Current Liabilities High

Liquid Ratio Liquid Assets/Current Liabilities High

Interest Coverage EBIT/interest Charges High

Market Capitalisation Stock Price x outstanding Shares High

Managerial Synergy Standards

Investment turnover Ratio Sales/ Investment High

Fixed assets turnover ratio Sales/ Fixed Assets High

Total assets turnover ratio Sales/Total Assets High

Operational Synergy Standards

Operating Profit Margin EBIT/Total Sales High

(HIGH: Higher the ratio better the performance)

Economic Value Added (EVA)

Economic Value Added is defined as “the incremental difference in rate of

return over a firms overall cost of capital. In other words, Economic Value Added is

calculated as a sum of excess return made on investment and invested capital.

Economic Value Added may be positive or negative. Negative Economic Value

Added indicates that the firm is destroying the value of funds invested. In case of

Economic Value Added negative means firm is destroying the value of funds

invested. Economic Value Added is a yardstick for an investment to measure the

value addition or shortfall.

Economic Value Added is calculated by using the following formula;

Economic Value Added = (Return on invested capital) – (Cost of Capital) (Capital

invested)

72

Economic Value Added improved measure of the Net Present Value rule. In

calculations of Economic value Added considered the present value of Economic

value Added is considered throughout the project life. The following formula is used

to evaluate the project or investment feasibility.

NPV = EVA t

(1+Kc) t

Where,

EVA t = Economic Value Added of project in year t

K c = Overall Cost of Capital

NPV = Net Present Value

The Economic Value Added and Net Present Value will result in a link

between value of the firm and Economic value Added of the firm. The calculation has

a simple formulation of firm value by the use of value of assets in place and

anticipated growth.

Firm Value = Value of assets in place + Value of expected future growth

There are two types of firm value calculation under Economic Value Added.

1) Discounted cash flow model - in this model both of the assets in place and the

expected future growth are ascertained by the use of Net Present Value created in the

preceding year. The following formula is used to evaluate the firm value by

considering the Net Present Value.

Firm Value = Capital invested Asset in place + Net Present Value Assets in place

+ Net Present Value

2) Economic Value Added model – this model is a substitute for discounted cash flow

model. In this model, instead of Net Present Value results, the calculation considers

Economic Value Added into this equation. The following formula is used to evaluate

firm value by using Economic Value Added.

Firm Value = Capital invested Assets in place +EVA Assets in place + EVA t Future projects

(1+Kc)t (1+Kc)

t

73

Thus, Firm Value is written as the total of following three components. Those are

• Capital investment assets in place

• Present value of Economic Value Added of assets in place

• Expected present value of Economic Value Added from the future investment.

Economic Value Added definitions outlines mainly depend on three basic inputs

that are-1) Invested capital 2) The return on net assets 3) Cost of capital of the firm.

Economic Value Added positive means the management has increased the firm’s total

worth. In other words, the firms profit is higher than that of the creditors and investors

expectations. If, Economic Value Added is negative it means the overall cost of

capital is more than the profit accumulated by the company which a means decline in

the firm value over a period. In other words, the profit of the firm is lower than that of

the Creditors and investors expectations.

Economic Value Added is performance metric. Economic Value Added is the

most preferable measure to evaluate a firm’s performance. The increase in Economic

Value Added will maximise the firm’s market value. It covers both the capital costs

and the operating costs. Hence it presents the best outcomes of the firms. Economic

Value Added of the firm will evaluate independently identify the feasibility of the

investment.

74

1. Analysis of Financial Health of selected Mergers and Acquisitions

Analysis of financial health measures the ability of the management and a

company’s accomplishments. Capital market performance ensures short term survival.

Profitability and leverage position ensures long term survival. Both are essential for

any company to long run survival. In order to identify the financial health changes

after Mergers and Acquisitions studies are made separately for each group. However,

few ratios are used to measure the financial health. For convenience the changes are

identified and called by names like: profitability ratios, leverage ratios and capital

market ratios. In this heading, an analysis has been done with the help of ratios like

gross profit margin, net profit margin, debt equity ratio, earnings per share and return

on capital employed by using the statistical tools like mean, standard deviation and

co- efficient of variation to examine the financial health of selected Mergers and

Acquisitions during the study period.

Table: 3.1.1 Gross Profit Margin of Selected Companies

Companies Mean Standard Deviation

Co - efficient of Variation

Pre Post Pre Post Pre Post

BAL 28.63 18.12 1.001 4.15 3.50 22.90

HGSL 22.15 12.82 0.60 2.59 2.71 20.20

HZL 63.86 53.19 14.10 2.17 22.08 4.08

LIL 17.10 10.05 3.35 3.29 19.59 32.74

FHL -8.92 -2.53 15.43 4.48 -172.98 -177.08

JSPL 31.17 24.50 2.887 5.475 9.26 22.35

M&ML 10.15 10.95 3.98 1.74 39.21 15.89

TCL 12.04 10.04 1.74 0.300 14.45 2.99

GTLIL -6.58 2.49 9.92 34.16 150.76 1371.89

RPL 0 481.18 0 399.09 0 82.94 (Source: AGM reports of selected companies & moneycontrol.com database)

During the study period, the average Gross Profit Margin from 2007 to 2009 is

considered to be pre-acquisition period whereas 2010 to 2013 to be considered as post

acquisition period. The comparison of the pre and post-acquisition, Gross Profit

Margin of selected companies is shown in table – 3.1.1

75

During pre acquisition period (2007 – 2009) it is observed from the table that the pre

acquisition average Gross Profit Margin ranges between -8.92% and 63.86%. The

highest average of Gross Profit Margin is found in Hindustan Zinc Ltd and the lowest

is found in Fortis Health Care Ltd.

During post acquisition period (2011- 2013) it also observed that the post acquisition

Gross Profit margin ranges between – 2.53% to 481%.The highest average of Gross

Profit Margin is found in Reliance Power Ltd and the lowest is found in Fortis

Healthcare Ltd.

During pre acquisition period (2007 – 2009) the Standard deviation of Gross Profit

Margin ranges between 0 and 15.43. The highest standard deviation is found in Fortis

Healthcare Ltd and the lowest is found in Reliance power Ltd.

During post acquisition period (2011 – 2013) the Standard deviation of Gross Profit

Margin ranges between 0.300 and 399. The highest standard deviation is found in

Reliance Power Ltd and the lowest is found in Tata Chemicals Ltd.

Comparing the Co-efficient of Variation of Selected companies in the pre and post

acquisition period from 2007 to 2013 the post acquisition Co-efficient of Variation is

high with respect to Bharti Airtel, Hinduja Global Solutions Ltd, Lanco Infratech Ltd,

Jindal Steel & Power Ltd, GTL Infrastructure Ltd and Reliance Power Ltd. The study

observed that the Gross Profit Margin Co-efficient of Variation is considerably

increased in the post acquisition.

The analysis of Gross Profit Margin of Selected companies reveals the facts which are

as follows:

• Lower the ratio – while comparing the average of Gross Profit Margin in pre and

post acquisition period Bharti Airtel Ltd, Hinduja Global Solutions Ltd, Hindustan

Zinc Ltd, Lanco Infratech Ltd, Jindal Steel & Power Ltd and Tata Chemicals Ltd

have considerably decrease performance due to high operational and financial

charges in post acquisition.

76

• Higher the ratio – Fortis Healthcare Ltd, Mahindra & Mahindra Ltd, GTL

Infrastructure Ltd and Reliance Power Ltd have considerably increase in Gross

Profit Margin due to low co-efficient of variation in post acquisition period.

Table: 3.1.2 Net Profit Margin of Selected Companies

Companies Mean Standard Deviation

Co - efficient of Variation

Pre Post Pre Post Pre Post

BAL 23.01 14.85 0.85 4.75 3.69 31.99

HGSL 14.38 10.37 1.66 3.18 11.54 30.67

HZL 48.42 45.99 5.73 0.85 11.83 1.85

LIL 10.72 2.10 3.70 2.31 34.51 110.00

FHL -12.44 28.57 19.83 23.43 -159.41 82.01

JSPL 20.68 15.79 1.83 5.36 8.85 33.95

M&ML 8.68 9.40 2.15 1.55 24.77 16.49

TCL 12.98 6.90 8.92 0.43 68.72 6.23

GTLIL -24.87 11.17 22.53 96.01 -90.59 859.53

RPL 60.66 120.46 46.44 75.74 76.56 62.88 (Source: AGM reports of selected companies & moneycontrol.com database)

During the study period, the average Net Profit Margin from 2007 to 2009 is

considered to be pre-acquisition period whereas 2010 to 2013 to be considered as post

acquisition period. The comparison of the pre and post-acquisition, Net Profit Margin

of selected companies is shown in table – 3.1.2

During pre acquisition period (2007 – 2009) it is observed from the table that the pre

acquisition average Net Profit Margin ranges between -24.87% and 60.66%. The

highest average of Net Profit Margin is found in Reliance Power Ltd and the lowest is

found in GTL Infrastructure Ltd.

During post acquisition period (2011- 2013) it also observed that the post acquisition

Net Profit margin ranges between 2.10% to 120.46%.The highest average of Net

77

Profit Margin is found in Reliance Power Ltd and the lowest is found in Lanco

Infratech Ltd.

During pre acquisition period (2007 – 2009) the Standard deviation of Net Profit

Margin ranges between 0.85 and 46.44. The highest standard deviation is found in

Reliance Power Ltd and the lowest is found in Bharti Airtel Ltd.

During post acquisition period (2011 – 2013) the Standard deviation of Net Profit

Margin ranges between 0.43 and 96.01. The highest standard deviation is found in

GTL Infrastructure Ltd and the lowest is found in Tata Chemicals Ltd.

Comparing the Co-efficient of Variation of Selected companies in the pre and post

acquisition period from 2007 to 2013 the post acquisition Co-efficient of Variation is

high with respect to Bharti Airtel, Hinduja Global Solutions Ltd, Lanco Infratech Ltd,

Jindal Steel & Power Ltd, GTL Infrastructure Ltd and Reliance Power Ltd. The study

observed that the Net Profit Margin Co-efficient of Variation is considerably

increased in the post acquisition.

The analysis of Net Profit Margin of Selected companies reveals the facts which are

as follows:

• Lower the ratio – while comparing the average of Net Profit Margin in pre and

post acquisition period Bharti Airtel Ltd, Hinduja Global Solutions Ltd, Hindustan

Zinc Ltd, Lanco Infratech Ltd, Jindal Steel & Power Ltd and Tata Chemicals Ltd

have considerably decrease performance due to high financial charges in post

acquisition.

• Higher the ratio – Fortis Healthcare Ltd, Mahindra & Mahindra Ltd, GTL

Infrastructure Ltd and Reliance Power Ltd have considerably increase in Net

Profit Margin due to low co-efficient of variation in post acquisition period.

78

Table: 3.1.3 Return on Assets of Selected Companies

Companies Mean Standard Deviation

Co - efficient of Variation

Pre Post Pre Post Pre Post

BAL 103 129 42.48 13.22 41.24 10.25

HGSL 294.88 317.20 45.71 5.69 15.50 1.79

HZL 266.91 64.45 80.49 11.55 30.16 17.92

LIL 72.46 14.77 10.87 0.43 15.00 2.91

FHL 29.89 77.48 6.09 2.65 20.37 3.42

JSPL 467.80 113.70 300.85 19.64 64.31 17.27

M&ML 173.94 201.66 22.63 35.50 13.01 17.60

TCL 139.23 196.05 24.39 11.30 17.52 5.76

GTLIL 11.97 12.49 2.70 5.03 22.56 40.27

RPL 42.49 58.02 28.16 1.74 66.27 3.00 (Source: AGM reports of selected companies & moneycontrol.com database)

During the study period, the average Return on Assets from 2007 to 2009 is

considered to be pre-acquisition period whereas 2010 to 2013 to be considered as post

acquisition period. The comparison of the pre and post-acquisition, Return on Assets

of selected companies is shown in table – 3.1.3

During pre acquisition period (2007 – 2009) it is observed from the table that the pre

acquisition average Return on Assets ranges between 11.97% and 467.80%. The

highest average of Return on Assets is found in Jindal Steel and Power Ltd and the

lowest is found in GTL Infrastructure Ltd.

During post acquisition period (2011- 2013) it also observed that the post acquisition

Return on Assets ranges between 12.49% to 317.20%.The highest average of Return

on Assets is found in Hinduja Global Solutions Ltd and the lowest is found in GTL

Infrastructure Ltd.

During pre acquisition period (2007 – 2009) the Standard deviation of Return on

Assets ranges between 2.70 and 300.85. The highest standard deviation is found in

Jindal Steel and Power Ltd and the lowest is found in GTL Infrastructure Ltd.

79

During post acquisition period (2011 – 2013) the Standard deviation of Return on

Assets ranges between 0.43 and 35.50. The highest standard deviation is found in

Mahindra and Mahindra Ltd and the lowest is found in Lanco Infratech Ltd.

Comparing the Co-efficient of Variation of Selected companies in the pre and post

acquisition period from 2007 to 2013 the post acquisition Co-efficient of Variation is

high with respect to GTL Infrastructure Ltd. The study observed that the Return on

Assets Co-efficient of Variation is considerably decreased in the post acquisition.

The analysis of Return on Assets of Selected companies reveals the facts which are as

follows:

• Lower the ratio – while comparing the average of Return on Assets in pre and post

acquisition period Hindustan Zinc Ltd, Lanco Infratech Ltd and Jindal Steel &

Power Ltd have considerably decrease performance due to low utilisation of

available resources.

• Higher the ratio – Bharti Airtel Ltd, Hinduja Global Solutions Ltd,Fortis

Healthcare Ltd, Mahindra & Mahindra Ltd, GTL Infrastructure Ltd, Tata

Chemicals Ltd and Reliance Power Ltd have considerably increase in Return on

Assets due to low co-efficient of variation in post acquisition period.

Table: 3.1.4 Return on Equity of Selected Companies

Companies Mean Standard Deviation Co - efficient of

Variation Pre Post Pre Post Pre Post

BAL 31.47 12.83 3.64 4.18 11.57 32.58

HGSL 8.62 9.81 4.01 1.81 46.52 18.45

HZL 37.81 20.14 20.09 2.52 53.13 12.51

LIL 10.67 3.92 4.73 3.97 44.33 101.28

FHL -3.68 3.84 5.96 2.97 -161.96 77.34

JSPL 29.84 18.70 2.70 5.47 9.05 29.25

M&ML 23.91 24.11 7.21 1.52 30.15 6.30

TCL 19.21 10.80 7.07 1.91 36.80 17.69

GTLIL -4.83 -23.68 4.03 13.66 -83.44 -57.69

RPL 0.0267 2.23 0.046 0.715 172.28 32.06 (Source: AGM reports of selected companies & moneycontrol.com database)

80

During the study period, the average Return on Equity from 2007 to 2009 is

considered to be pre-acquisition period whereas 2010 to 2013 to be considered as post

acquisition period. The comparison of the pre and post-acquisition, Return on Equity

of selected companies is shown in table – 3.1.4

During pre acquisition period (2007 – 2009) it is observed from the table that the pre

acquisition average Return on Equity ranges between -4.83% and 37.81%. The

highest average of Return on Equity is found in Bharti Airtel Ltd and the lowest is

found in GTL Infrastructure Ltd.

During post acquisition period (2011- 2013) it also observed that the post acquisition

Return on Equity ranges between -23.68% to 24.11%.The highest average of Return

on Equity is found in Mahindra and Mahindra Ltd and the lowest is found in GTL

Infrastructure Ltd.

During pre acquisition period (2007 – 2009) the Standard deviation of Return on

Equity ranges between 0.046 and 20.99. The highest standard deviation is found in

Jindal Steel and Power Ltd and the lowest is found in Reliance Power Ltd.

During post acquisition period (2011 – 2013) the Standard deviation of Return on

Equity ranges between 0.715 and 13.66. The highest standard deviation is found in

GTL Infrastructure Ltd and the lowest is found in Reliance Power Ltd.

Comparing the Co-efficient of Variation of Selected companies in the pre and post

acquisition period from 2007 to 2013 the post acquisition Co-efficient of Variation is

high with respect to Lanco Infratech Ltd and Jindal Steel and Power Ltd. The study

observed that the Return on Equity Co-efficient of Variation is considerably

decreased in the post acquisition.

The analysis of Return on Equity of Selected companies reveals the facts which are as

follows:

• Lower the ratio – while comparing the average of Return on Equity in pre and

post acquisition period Bharti Airtel, Hindustan Zinc Ltd, Lanco Infratech Ltd,

Jindal Steel & Power Ltd, Tata Chemicals Ltd have considerably decrease

performance due to decline in profits.

81

• Higher the ratio – Hinduja Global Solutions Ltd,Fortis Healthcare Ltd, Mahindra

& Mahindra Ltd, GTL Infrastructure Ltd, Tata Chemicals Ltd and Reliance Power

Ltd have considerably increase in Return on Equity due to low co-efficient of

variation in post acquisition period.

Table: 3.1.5 Return on Capital Employed of Selected Companies

Companies Mean Standard Deviation

Co - efficient of Variation

Pre Post Pre Post Pre Post

BAL 28.47 13.95 0.558 2.339 1.96 16.77

HGSL 9.93 11.41 5.63 1.81 56.70 15.86

HZL 51.56 24.45 30.56 1.96 59.27 8.02

LIL 13.41 9.02 4.80 1.34 35.79 14.86

FHL 1.59 3.92 1.31 1.14 82.39 29.08

JSPL 22.19 12.69 3.35 2.83 15.10 22.30

M&ML 19.41 25.59 5.91 1.83 30.45 7.15

TCL 14.55 13.38 3.98 3.02 27.35 22.57

GTLIL 0.77 0.66 0.23 3.26 29.87 493.94

RPL 0 1.193 0 0.959 0 80.39 (Source: AGM reports of selected companies & moneycontrol.com database)

During the study period, the average Return on Capital Employed from 2007 to 2009

is considered to be pre-acquisition period whereas 2010 to 2013 to be considered as

post acquisition period. The comparison of the pre and post-acquisition, Return on

Capital Employed of selected companies is shown in table – 3.1.5

During pre acquisition period (2007 – 2009) it is observed from the table that the pre

acquisition average Return on Capital Employed ranges between 0% and 51.56%. The

highest average of Return on Capital Employed is found in Hindustan Zinc Ltd and

the lowest is found in Reliance Power Ltd.

During post acquisition period (2011- 2013) it also observed that the post acquisition

Return on Capital Employed ranges between 0.66% to 25.59%.The highest average of

82

Return on Capital Employed is found in Mahindra and Mahindra Ltd and the lowest is

found in GTL Infrastructure Ltd.

During pre acquisition period (2007 – 2009) the Standard deviation of Return on

Capital Employed ranges between 0 and 30.55. The highest standard deviation is

found in Mahindra and Mahindra Ltd and the lowest is found in Reliance Power Ltd.

During post acquisition period (2011 – 2013) the Standard deviation of Return on

Capital Employed ranges between 0.959 and 2.34. The highest standard deviation is

found in Bharti Airtel Ltd and the lowest is found in Reliance Power Ltd.

Comparing the Co-efficient of Variation of Selected companies in the pre and post

acquisition period from 2007 to 2013 the post acquisition Co-efficient of Variation is

high with respect to Bharti Airtel Ltd, GTL Infrastructure Ltd and Reliance Power

Ltd. The study observed that the Return on Capital Employed Co-efficient of

Variation is considerably decreased in the post acquisition.

The analysis of Return on Capital Employed of Selected companies reveals the facts

which are as follows:

• Lower the ratio – while comparing the average of Return on Capital Employed in

pre and post acquisition period Bharti Airtel, Hindustan Zinc Ltd, Lanco Infratech

Ltd, Jindal Steel & Power Ltd, Tata Chemicals Ltd have considerably decrease

performance due to decline in profits earned and Capital Employed.

• Higher the ratio – Hinduja Global Solutions Ltd,Fortis Healthcare Ltd, Mahindra

& Mahindra Ltd, GTL Infrastructure Ltd, Tata Chemicals Ltd and Reliance Power

Ltd have considerably increase in Return on Capital Employed due to low co-

efficient of variation in post acquisition period.

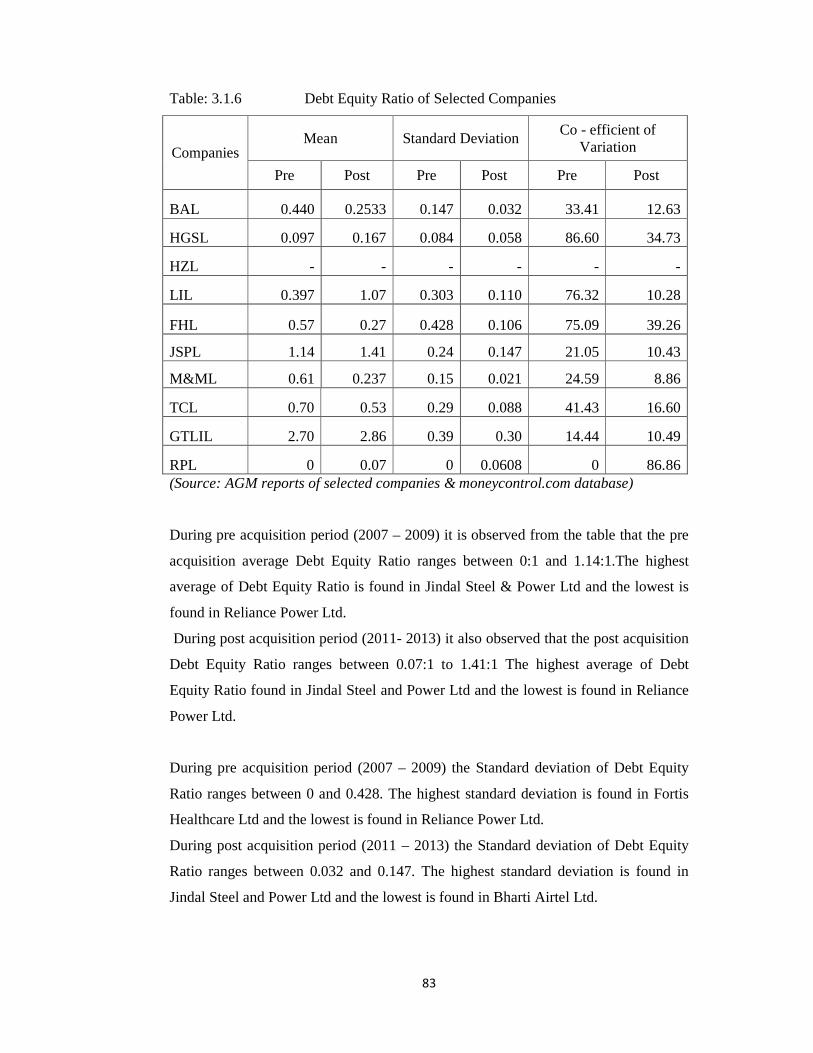

During the study period, the average Debt Equity Ratio from 2007 to 2009 is

considered to be pre-acquisition period whereas 2010 to 2013 to be considered as post

acquisition period. The comparison of the pre and post-acquisition, Debt Equity Ratio

of selected companies is shown in table – 3.1.6

83

Table: 3.1.6 Debt Equity Ratio of Selected Companies

Companies Mean Standard Deviation

Co - efficient of Variation

Pre Post Pre Post Pre Post

BAL 0.440 0.2533 0.147 0.032 33.41 12.63

HGSL 0.097 0.167 0.084 0.058 86.60 34.73

HZL - - - - - -

LIL 0.397 1.07 0.303 0.110 76.32 10.28

FHL 0.57 0.27 0.428 0.106 75.09 39.26

JSPL 1.14 1.41 0.24 0.147 21.05 10.43

M&ML 0.61 0.237 0.15 0.021 24.59 8.86

TCL 0.70 0.53 0.29 0.088 41.43 16.60

GTLIL 2.70 2.86 0.39 0.30 14.44 10.49

RPL 0 0.07 0 0.0608 0 86.86 (Source: AGM reports of selected companies & moneycontrol.com database)

During pre acquisition period (2007 – 2009) it is observed from the table that the pre

acquisition average Debt Equity Ratio ranges between 0:1 and 1.14:1.The highest

average of Debt Equity Ratio is found in Jindal Steel & Power Ltd and the lowest is

found in Reliance Power Ltd.

During post acquisition period (2011- 2013) it also observed that the post acquisition

Debt Equity Ratio ranges between 0.07:1 to 1.41:1 The highest average of Debt

Equity Ratio found in Jindal Steel and Power Ltd and the lowest is found in Reliance

Power Ltd.

During pre acquisition period (2007 – 2009) the Standard deviation of Debt Equity

Ratio ranges between 0 and 0.428. The highest standard deviation is found in Fortis

Healthcare Ltd and the lowest is found in Reliance Power Ltd.

During post acquisition period (2011 – 2013) the Standard deviation of Debt Equity

Ratio ranges between 0.032 and 0.147. The highest standard deviation is found in

Jindal Steel and Power Ltd and the lowest is found in Bharti Airtel Ltd.

84

Comparing the Co-efficient of Variation of Selected companies in the pre and post

acquisition period from 2007 to 2013 the post acquisition Co-efficient of Variation is

high with respect to Reliance Power Ltd. The study observed that the Debt Equity

Ratio Co-efficient of Variation is considerably decreased in the post acquisition.

The analysis of Debt Equity Ratio of Selected companies reveals the facts which are

as follows:

• Lower the ratio – while comparing the average of Debt Equity Ratio in pre and

post acquisition period Bharti Airtel Ltd, Fortis Healthcare Ltd, Ltd, Mahindra and

Mahindra Ltd and Tata Chemicals Ltd have considerably decreased indicating

lower leverage policy by infusing more equity funds in its capital structure.the

raised equity capital was devoted for long term investment purposes and

acquisition of long term assets. Over the years the debt amount decreased on

account of effective borrowing policies. The analysis indicates that the claims of

lenders are less than the shareholders funds or networth.

• Higher the ratio – Hinduja Global Solutions Ltd, Lanco Infratech Ltd, Jindal Steel

& Power Ltd, GTL Infrastructure Ltd and Reliance Power Ltd have considerably

increase in Debt Equity Ratio due to low co-efficient of variation in post

acquisition period.

Table: 3.1.7 Total Capitalisation of Selected Companies

Companies Mean Standard Deviation

Co - efficient of Variation

Pre Post Pre Post Pre Post

BAL 0.2633 0.2000 0.051 0.017 19.37 8.50

HGSL 0.083 0.143 0.072 0.046 86.75 32.17

HZL 0.74 0.42 0.37 0.026 50.00 6.19

LIL 0.26 0.53 0.16 0.04 61.54 7.55

FHL 0.30 0.21 0.16 0.07 53.33 33.33

JSPL 0.52 0.58 0.051 0.023 9.81 3.97

M&ML 0.38 0.19 0.060 0.17 15.79 89.47

TCL 0.40 0.35 0.10 0.038 25.00 10.86

GTLIL 0.72 0.74 0.026 0.017 3.61 2.30

RPL 0 0.063 0 0.055 0 87.30 (Source: AGM reports of selected companies & moneycontrol.com database)

85

During the study period, the average Total Capitalisation from 2007 to 2009 is

considered to be pre-acquisition period whereas 2010 to 2013 to be considered as post

acquisition period. The comparison of the pre and post-acquisition, Total

Capitalisation of selected companies is shown in table – 3.1.7

During pre acquisition period (2007 – 2009) it is observed from the table that the pre

acquisition average Total Capitalisation ranges between 0:1 and 0.74:1.The highest

average of Total Capitalisation is found in Hindustan Zinc Ltd and the lowest is found

in Reliance Power Ltd.

During post acquisition period (2011- 2013) it also observed that the post acquisition

Total Capitalisation ranges between 0.063:1 to 0.74:1 The highest average of Total

Capitalisation found in GTL Infrastructure Ltd and the lowest is found in Reliance

Power Ltd.

During pre acquisition period (2007 – 2009) the Standard deviation of Total

Capitalisation ranges between 0 and 0.37. The highest standard deviation is found in

Hindustan Zinc Ltd and the lowest is found in Reliance Power Ltd.

During post acquisition period (2011 – 2013) the Standard deviation of Total

Capitalisation ranges between 0.017 and 0.17. The highest standard deviation is found

in Mahindra and Mahindra Ltd and the lowest is found in GTL Infrastructure Ltd.

Comparing the Co-efficient of Variation of Selected companies in the pre and post

acquisition period from 2007 to 2013 the post acquisition Co-efficient of Variation is

high with respect to Mahindra and Mahindra Ltd and Reliance Power Ltd. The study

observed that the Total Capitalisation Co-efficient of Variation is considerably

decreased in the post acquisition.

The analysis of Total Capitalisation of Selected companies reveals the facts which are

as follows:

• Lower the ratio – while comparing the average of Total Capitalisation in pre and

post acquisition period Bharti Airtel Ltd, Fortis Healthcare Ltd, Ltd, Mahindra and

Mahindra Ltd and Tata Chemicals Ltd have considerably decreased. It indicates

that the proportion of debt is low compared to equity funds reflecting use under

leveraging to fund the business operation. To fulfil operating and strategic plans

86

above companies depended on equity financing as a result leading to debt trap

where in future earnings are enough to meet obligations.

• Higher the ratio – Hinduja Global Solutions Ltd, Lanco Infratech Ltd, Jindal Steel

& Power Ltd, GTL Infrastructure Ltd and Reliance Power Ltd have considerably

increase in Total Capitalisation due to low co-efficient of variation in post

acquisition period.

Table: 3.1.8 Earnings per Share of Selected Companies

Companies Mean Standard Deviation

Co - efficient of Variation

Pre Post Pre Post Pre Post

BAL 31.65 16.28 9.82 3.59 31.03 22.05

HGSL 47.86 31.05 32 5.17 66.86 16.65

HZL 91.23 13.67 23.12 2.42 25.34 17.70

LIL 8.07 0.57 4.39 0.56 54.40 98.25

FHL -0.92 2.97 1.45 2.32 -157.61 78.11

JSPL 136 20.57 80.50 3.07 59.19 14.92

M&ML 40.57 48.29 8.58 5.75 21.15 11.91

TCL 26.81 21.44 11.93 4.81 44.50 22.43

GTLIL -0.49 -2.77 0.46 1.22 -93.88 -44.04

RPL 0.49 1.30 0.52 0.46 106.12 35.38 (Source: AGM reports of selected companies & moneycontrol.com database)

During the study period, the average Earnings per Share from 2007 to 2009 is

considered to be pre-acquisition period whereas 2010 to 2013 to be considered as post

acquisition period. The comparison of the pre and post-acquisition, Earnings per

Share of selected companies is shown in table – 3.1.8

During pre acquisition period (2007 – 2009) it is observed from the table that the pre

acquisition average Earnings per Share ranges between -0.92 and 136.The highest

87

average of Earnings per Share is found in Jindal Steel and Power Ltd and the lowest is

found in Fortis Healthcare Ltd.

During post acquisition period (2011- 2013) it also observed that the post acquisition

Earnings per Share ranges between -2.77 to 48.29. The highest average of Earnings

per Share found in Mahindra and Mahindra Ltd and the lowest is found in GTL

Infrastructure Ltd.

During pre acquisition period (2007 – 2009) the Standard deviation of Earnings per

Share ranges between 0.46 and 80.50. The highest standard deviation is found in

Jindal Steel and Power Ltd and the lowest is found in GTL Infrastructure Ltd.

During post acquisition period (2011 – 2013) the Standard deviation of Earnings per

Share ranges between 0.46 and 5.75. The highest standard deviation is found in

Mahindra and Mahindra Ltd and the lowest is found in Reliance Power Ltd.

Comparing the Co-efficient of Variation of Selected companies in the pre and post

acquisition period from 2007 to 2013 the post acquisition Co-efficient of Variation is

high with respect to Lanco Infratech Ltd and Fortis Healthcare Ltd. The study

observed that the Earnings per Share Co-efficient of Variation is considerably

decreased in the post acquisition.

The analysis of Earnings per Share of Selected companies reveals the facts which are

as follows:

• Lower the ratio – while comparing the average of Earnings per Share in pre and

post acquisition period Bharti Airtel Ltd, Hinduja Global Solutions Ltd, Lanco

Infratech Ltd, Jindal Steel & Power Ltd, GTL Infrastructure Ltd and Tata

Chemicals Ltd have considerably decreased. It indicates that the decline in

Earning per Share attributed to higher operating expences and proportionate

decrease in sales revenue.

• Higher the ratio – Fortis Healthcare Ltd, Mahindra and Mahindra Ltd and

Reliance Power Ltd have considerably increase in Earnings per Share due to low

co-efficient of variation in post acquisition period.

88

Table: 3.1.9 Price Earning Ratio of Selected Companies

Companies Mean Standard Deviation

Co - efficient of Variation

Pre Post Pre Post Pre Post

BAL 25.56 20.84 19.66 3.86 76.92 18.52

HGSL 9.11 12.26 5.65 5.74 62.02 46.82

HZL 9.95 9.59 7.99 1.28 80.30 13.35

LIL 107.42 2.73 130.11 4.73 121.12 173.26

FHL 21.60 95.23 498.26 124 2306.76 130.21

JSPL 28.62 18.55 33.68 2.82 117.68 15.20

M&ML 20.13 17.63 14.66 2.10 72.83 11.91

TCL 13.61 15.25 8.42 4.31 61.87 28.26

GTLIL -57.53 -2.66 67.67 3.07 -117.63 -115.41

RPL 144.90 65.50 142.85 22.85 98.59 34.89 (Source: AGM reports of selected companies & moneycontrol.com database)

During the study period, the average Price Earning Ratio from 2007 to 2009 is

considered to be pre-acquisition period whereas 2010 to 2013 to be considered as post

acquisition period. The comparison of the pre and post-acquisition, Price Earning

Ratio of selected companies is shown in table – 3.1.9

During pre acquisition period (2007 – 2009) it is observed from the table that the pre

acquisition average Price Earning Ratio ranges between -57.53 and 144.90.The

highest average of Price Earning Ratio is found in Reliance Power Ltd and the lowest

is found in GTL Infrastructure Ltd.

During post acquisition period (2011- 2013) it also observed that the post acquisition

Price Earning Ratio ranges between -2.66 to 95.23. The highest average of Price

Earning Ratio found in Fortis Healthcare Ltd and the lowest is found in GTL

Infrastructure Ltd.

During pre acquisition period (2007 – 2009) the Standard deviation of Price Earning

Ratio ranges between 5.65 and 498.26. The highest standard deviation is found in

Fortis Healthcare Ltd and the lowest is found in Hinduja Global Solutions Ltd.

89

During post acquisition period (2011 – 2013) the Standard deviation of Price Earning

Ratio ranges between 1.28 and 124. The highest standard deviation is found in Fortis

Healthcare Ltd and the lowest is found in Hindustan Zinc Ltd.

Comparing the Co-efficient of Variation of Selected companies in the pre and post

acquisition period from 2007 to 2013 the post acquisition Co-efficient of Variation is

high with respect to Lanco Infratech Ltd. The study observed that the Price Earning

Ratio Co-efficient of Variation is considerably decreased in the post acquisition.

The analysis of Price Earning Ratio of Selected companies reveals the facts which are

as follows:

• Lower the ratio – while comparing the average of Price Earning Ratio in pre and

post acquisition period Bharti Airtel Ltd, Hindustan Zinc Ltd, Lanco Infratech

Ltd, Jindal Steel & Power Ltd, Mahindra and Mahindra Ltd and Reliance Power

Ltd have considerably decreased. It indicates decreasing trend reflects lower

market price was paid by the investors and reported less earning per share during

the post acquisition period. Less dividend payments in post acquisition period

which lead to decrease in investor’s expectation and market appraisal.

• Higher the ratio – Hinduja Global Solutions Ltd, Fortis Healthcare Ltd, Tata

Chemicals Ltd and GTL Infrastructure Ltd have considerably increased in Price

Earning Ratio due to low co-efficient of variation in post acquisition period.

90

2. Analysis of Financial, Managerial and Operational Synergies

Analysis of financial, managerial and operational performance measures the

synergetic value of the firms. Liquidity ensures short term survival and credibility and

marketability ensures long term survival. Both are essential for any company in the

long run. In order to identify the financial changes, managerial changes and

operational changes after Mergers and Acquisitions, studies are made separately for

each group. However, few ratios are used to identify the synergetic change. For

convenience the changes are identified and called by names like: Financial synergies,

Managerial synergies and Operational synergies. Under this heading, an analysis has

been done with the help of ratios like current ratio, liquid ratio, interest coverage,

operating profit margin and investment turn over ratio by using statistical tools like

mean, standard deviation and co- efficient of variance to examine the financial

soundness of selected Mergers and Acquisitions during the study period.

Table: 3.2.1 Current Ratio of Selected Companies

Companies Mean Standard Deviation

Co - efficient of Variation

Pre Post Pre Post Pre Post

BAL 0.568 0.767 0.11 0.22 19.37 28.68

HGSL 0.88 1.13 0.26 0.30 29.55 26.55

HZL 1.90 3.18 0.55 0.33 28.95 10.38

LIL 1.09 0.68 0.21 0.050 19.27 7.35

FHL 2.03 8.06 0.593 9.27 29.21 115.01

JSPL 0.99 0.73 0.29 0.038 29.29 5.21

M&ML 1.02 0.99 0.25 0.025 24.51 2.53

TCL 0.78 1.18 0.28 0.17 35.90 14.41

GTLIL 3.49 1.02 2.55 1.13 73.07 110.78

RPL 63.40 20.13 90.36 15.85 142.52 78.74 (Source: AGM reports of selected companies & moneycontrol.com database)

During the study period, the average Current Ratio from 2007 to 2009 is considered

as pre-acquisition period and 2010 to 2013 is considered as post acquisition period.

91

The comparison of the pre and post-acquisition Current Ratio of selected companies is

shown in table – 3.2.1

During pre acquisition period (2007 – 2009) it is observed from the table that the pre

acquisition average Current Ratio ranges between 0.57:1 and 63.4:1. The highest

average of Current Ratio is found in Reliance Power Ltd., and the lowest average of

Current Ratio is found in Bharti Airtel Ltd.

During post acquisition period (2011- 2013) it is observed that the post acquisition

Current Ratio ranges between 0.68:1 to 20.13:1.The highest average of Current Ratio

is found in Reliance Power Ltd and the lowest average of Current Ratio is found in

Lanco Infratech Ltd.

During pre acquisition period (2007 – 2009) the Standard deviation of Current Ratio

ranges between 0.11 and 90.36. The highest standard deviation is found in Reliance

Power Ltd. The lowest standard deviation is found in Bharti Airtel Ltd.

During post acquisition period (2011 – 2013) the Standard deviation of Current Ratio

ranges between 0.025 and 15.85. The highest standard deviation is found in Reliance

Power Ltd. The lowest standard deviation is found in Mahindra & Mahindra Ltd.

Comparing the Co-efficient of Variation of Selected companies in the pre and post

acquisition period from 2007 to 2013 the post acquisition Co-efficient of Variation is

more in Bharti Airtel, Fortis Healthcare Ltd and GTL Infrastructure Ltd. The study

observed that Current Ratio Co-efficient of Variation considerably decreased in the

post acquisition. It indicates infuse of resources to pay its debt over the short term

period and easy to meet short term obligations. Over the years percentage increase in

current liabilities is greater than percentage increase in current assets.

The analysis of Current Ratio of Selected companies reveals the following facts:

• Lower the ratio – while comparing the average of Current Ratio in pre and post

acquisition period Lanco Infratech Ltd, Jindal Steel & Power Ltd, Mahindra &

Mahindra Ltd, GTL Infrastructure Ltd and Reliance Power Ltd have considerable

decrease performance due to high variation in post acquisition. It indicates infuse

of resources to pay its debt over the short term period and easy to meet short term

92

obligations. Over the years percentage increase in current liabilities is greater than

percentage increase in current assets.

• Higher the ratio – Bharti Airtel Ltd, Hinduja Global Solutions Ltd, Hindustan Zinc

Ltd, Fortis Healthcare Ltd and Tata Chemicals Ltd have considerable increase in

Current Ratio due to low co-efficient of variation in post acquisition period.

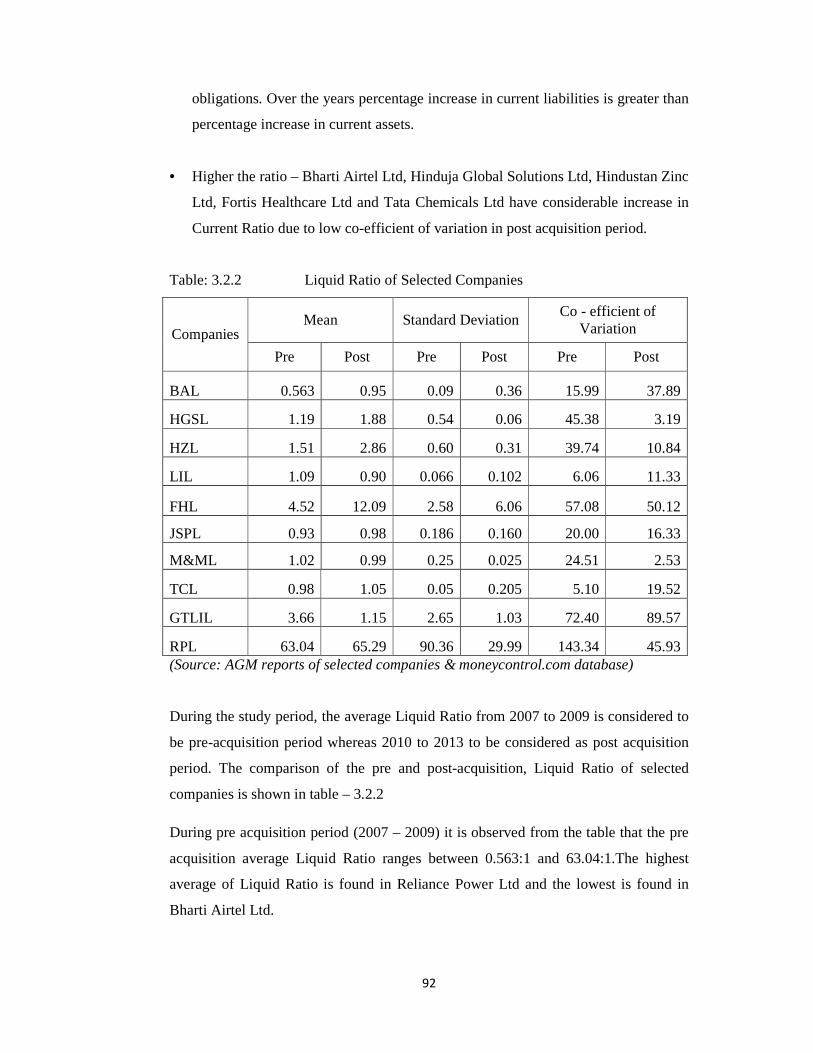

Table: 3.2.2 Liquid Ratio of Selected Companies

Companies Mean Standard Deviation

Co - efficient of Variation

Pre Post Pre Post Pre Post

BAL 0.563 0.95 0.09 0.36 15.99 37.89

HGSL 1.19 1.88 0.54 0.06 45.38 3.19

HZL 1.51 2.86 0.60 0.31 39.74 10.84

LIL 1.09 0.90 0.066 0.102 6.06 11.33

FHL 4.52 12.09 2.58 6.06 57.08 50.12

JSPL 0.93 0.98 0.186 0.160 20.00 16.33

M&ML 1.02 0.99 0.25 0.025 24.51 2.53

TCL 0.98 1.05 0.05 0.205 5.10 19.52

GTLIL 3.66 1.15 2.65 1.03 72.40 89.57

RPL 63.04 65.29 90.36 29.99 143.34 45.93 (Source: AGM reports of selected companies & moneycontrol.com database)

During the study period, the average Liquid Ratio from 2007 to 2009 is considered to

be pre-acquisition period whereas 2010 to 2013 to be considered as post acquisition

period. The comparison of the pre and post-acquisition, Liquid Ratio of selected

companies is shown in table – 3.2.2

During pre acquisition period (2007 – 2009) it is observed from the table that the pre

acquisition average Liquid Ratio ranges between 0.563:1 and 63.04:1.The highest

average of Liquid Ratio is found in Reliance Power Ltd and the lowest is found in

Bharti Airtel Ltd.

93

During post acquisition period (2011- 2013) it also observed that the post acquisition

Price Earning Ratio ranges between 0.90:1 to 65.29:1 The highest average of Liquid

Ratio found in Reliance Power Ltd and the lowest is found in Lanco Infratech Ltd.

During pre acquisition period (2007 – 2009) the Standard deviation of Liquid Ratio

ranges between 0.05 and 90.36. The highest standard deviation is found in Reliance

Power Ltd and the lowest is found in Tata Chemicals Ltd.

During post acquisition period (2011 – 2013) the Standard deviation of Liquid Ratio

ranges between 0.06 and 29.99. The highest standard deviation is found in Fortis

Healthcare Ltd and the lowest is found in Hindustan Zinc Ltd.

Comparing the Co-efficient of Variation of Selected companies in the pre and post

acquisition period from 2007 to 2013 the post acquisition Co-efficient of Variation is

high with respect to Bharti Airtel Ltd, Tata Chemicals Ltd and GTL Infrastructure

Ltd. The study observed that the Liquid Ratio Co-efficient of Variation is

considerably decreased in the post acquisition.

The analysis of Liquid Ratio of Selected companies reveals the facts which are as

follows:

• Lower the ratio – while comparing the average of Liquid Ratio in pre and post

acquisition period Lanco Infratech Ltd, Mahindra and Mahindra Ltd and GTL

Infrastructure Ltd have considerably decreased. It indicates lower liquidity

positions and inability to meet immediate current liabilities. The results show less

than the standards in the post acquisition. It is also observed that Current Ratio is

much greater than the Quick Ratio. It suggests current assets are not highly

dependent on inventory and sundry creditors.

• Higher the ratio – Bharti Airtel Ltd, Hinduja Global Solutions Ltd, Hindustan Zinc

Ltd, Fortis Healthcare Ltd, Jindal Steel and Power Ltd, Tata Chemical Ltd and

GTL Infrastructure Ltd have considerably increased in Liquid Ratio due to low

co-efficient of variation in post acquisition period.

94

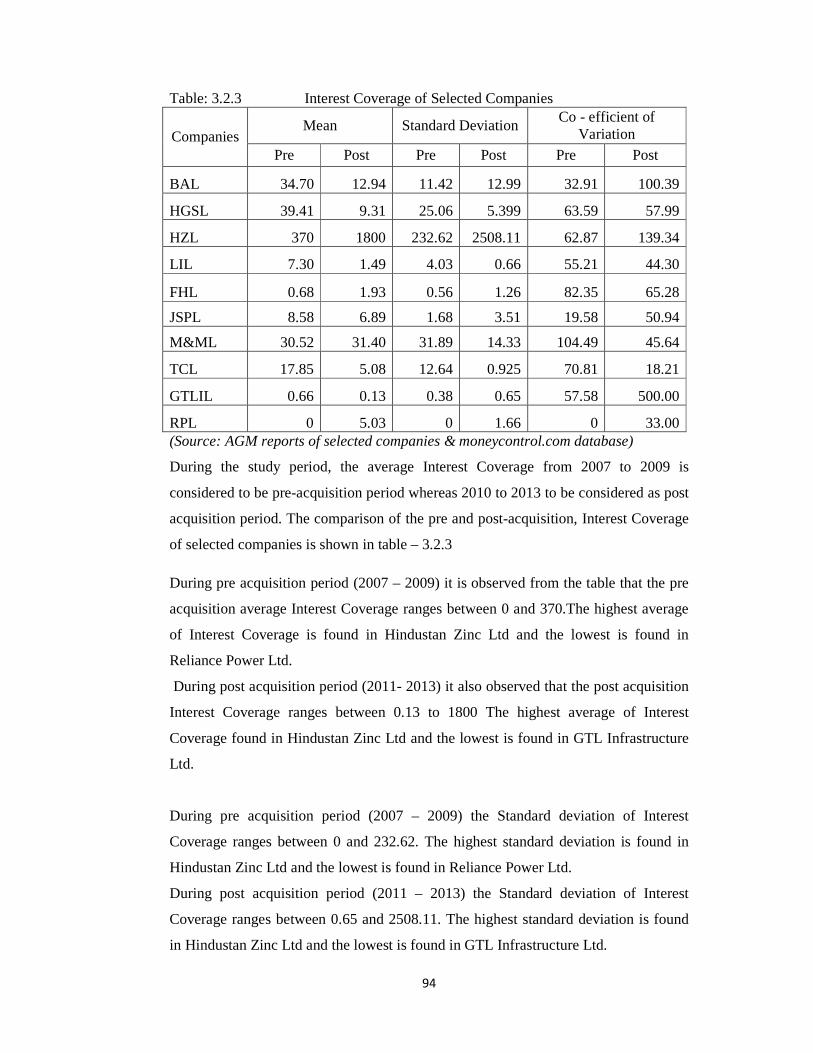

Table: 3.2.3 Interest Coverage of Selected Companies

Companies Mean Standard Deviation

Co - efficient of Variation

Pre Post Pre Post Pre Post

BAL 34.70 12.94 11.42 12.99 32.91 100.39

HGSL 39.41 9.31 25.06 5.399 63.59 57.99

HZL 370 1800 232.62 2508.11 62.87 139.34

LIL 7.30 1.49 4.03 0.66 55.21 44.30

FHL 0.68 1.93 0.56 1.26 82.35 65.28

JSPL 8.58 6.89 1.68 3.51 19.58 50.94

M&ML 30.52 31.40 31.89 14.33 104.49 45.64

TCL 17.85 5.08 12.64 0.925 70.81 18.21

GTLIL 0.66 0.13 0.38 0.65 57.58 500.00

RPL 0 5.03 0 1.66 0 33.00 (Source: AGM reports of selected companies & moneycontrol.com database)

During the study period, the average Interest Coverage from 2007 to 2009 is

considered to be pre-acquisition period whereas 2010 to 2013 to be considered as post

acquisition period. The comparison of the pre and post-acquisition, Interest Coverage

of selected companies is shown in table – 3.2.3

During pre acquisition period (2007 – 2009) it is observed from the table that the pre

acquisition average Interest Coverage ranges between 0 and 370.The highest average

of Interest Coverage is found in Hindustan Zinc Ltd and the lowest is found in

Reliance Power Ltd.

During post acquisition period (2011- 2013) it also observed that the post acquisition

Interest Coverage ranges between 0.13 to 1800 The highest average of Interest

Coverage found in Hindustan Zinc Ltd and the lowest is found in GTL Infrastructure

Ltd.

During pre acquisition period (2007 – 2009) the Standard deviation of Interest

Coverage ranges between 0 and 232.62. The highest standard deviation is found in

Hindustan Zinc Ltd and the lowest is found in Reliance Power Ltd.

During post acquisition period (2011 – 2013) the Standard deviation of Interest

Coverage ranges between 0.65 and 2508.11. The highest standard deviation is found

in Hindustan Zinc Ltd and the lowest is found in GTL Infrastructure Ltd.

95

Comparing the Co-efficient of Variation of Selected companies in the pre and post

acquisition period from 2007 to 2013 the post acquisition Co-efficient of Variation is

high with respect to Bharti Airtel Ltd, Hindustan Zinc Ltd, Jindal Steel and Power

Ltd, GTL Infrastructure Ltd and Reliance Power Ltd. The study observed that the

Interest Coverage Co-efficient of Variation is considerably increased in the post

acquisition.

The analysis of Interest Coverage of Selected companies reveals the facts which are

as follows:

• Lower the ratio – while comparing the average of Interest Coverage in pre and

post acquisition period Bharti Airtel Ltd, Hinduja Global Solutions Ltd, Lanco

Infratech Ltd, Jindal Steel and Power Ltd, Tata Chemicals Ltd and GTL

Infrastructure Ltd have considerably decreased. It indicates inability to honour its

debt payments due to less profit margin reported over the post three years. Post

acquisition Interest Coverage was low indicating possibility of default to creditors.

• Higher the ratio – Hindustan Zinc Ltd, Fortis Healthcare Ltd, Mahindra and

Mahindra Ltd and Reliance Power Ltd have considerably increased in Interest

Coverage due to low co-efficient of variation in post acquisition period.

Table: 3.2.4 Market Capitalisation of Selected Companies

Companies Mean Standard Deviation

Co - efficient of Variation

Pre Post Pre Post Pre Post

BAL 129100.2 125426.1 63423.78 5012.75 49.13 4.00

HGSL 470.39 747.89 436.99 232.22 92.90 31.05

HZL 33422.28 54584.08 18511.22 3785.22 55.39 6.93

LIL 11682.90 2463.99 7721.61 726.58 66.09 29.49

FHL 2189.83 4074.64 826.68 627.20 37.75 15.39

JSPL 24103.58 36200.70 20240.49 10223.13 83.97 28.24

M&ML 18848.50 52343.83 11542.41 9088.81 61.24 17.36

TCL 6773.50 7994.67 2601.88 1007.95 38.41 12.61

GTLIL 2752.65 563.20 467.24 260.91 16.97 46.33

RPL 23548.11 22207.25 15712.10 3459.99 66.72 15.58 (Source: AGM reports of selected companies & moneycontrol.com database)

96

During pre acquisition period (2007 – 2009) it is observed from the table that the pre

acquisition average Market Capitalisation ranges between 470.39Crores and

1,29,100.20Crores.The highest average of Market Capitalisation is found in Bharti

Airtel Ltd and the lowest is found in Hinduja Global Solutions Ltd.

During post acquisition period (2011- 2013) it also observed that the post acquisition

Market Capitalisation ranges between 563.20Crores to 1,25,426.10Crores. The

highest average of Market Capitalisation found in Bharti Airtel Ltd and the lowest is

found in GTL Infrastructure Ltd.

During pre acquisition period (2007 – 2009) the Standard deviation of Market

Capitalisation ranges between 436.99 and 63,423.78. The highest standard deviation

is found in Bharti Airtel Ltd and the lowest is found in Hinduja Global Solutions Ltd.

During post acquisition period (2011 – 2013) the Standard deviation of Market

Capitalisation ranges between 232.22 and 10.223.13. The highest standard deviation

is found in Jindal Steel and Power Ltd and the lowest is found in Hinduja Global

Solutions Ltd.

Comparing the Co-efficient of Variation of Selected companies in the pre and post

acquisition period from 2007 to 2013 the post acquisition Co-efficient of Variation is

high with respect to GTL Infrastructure Ltd. The study observed that the Market

Capitalisation Co-efficient of Variation is considerably decreased in the post

acquisition.

The analysis of Market Capitalisation of Selected companies reveals the facts which

are as follows:

• Lower the ratio – while comparing the average of Market Capitalisation in pre and

post acquisition period Bharti Airtel Ltd, Lanco Infratech Ltd, GTL Infrastructure

Ltd and Reliance Power Ltd have considerably decreased. It reflects on investors

by way of quoting lower prices to outstanding equity shares in the capital market.

Future growth prospects are uncertain on account of intense competition and

decrease in equity funds in the capital structure.

97

• Higher the ratio – Hinduja Global Solutions Ltd, Hindustan Zinc Ltd, Fortis

Healthcare Ltd, Jindal Steel and Power Ltd, Mahindra and Mahindra Ltd and Tata

Chemicals Ltd have considerably increased in Market Capitalisation due to low

co-efficient of variation in post acquisition period.

Table: 3.2.5 Investment Turnover Ratio of Selected Companies

Companies Mean Standard Deviation

Co - efficient of Variation

Pre Post Pre Post Pre Post

BAL 0.997 0.68 0.064 0.025 6.42 3.68

HGSL 0.520 0.823 0.197 0.051 37.88 6.20

HZL 0.73 0.42 0.364 0.025 49.86 5.95

LIL 0.78 0.89 0.46 0.32 58.97 35.96

FHL 0.15 0.073 0.010 0.006 6.67 8.22

JSPL 0.69 0.49 0.076 0.032 11.01 6.53

M&ML 1.65 2.07 0.25 0.20 15.15 9.66

TCL 0.99 0.993 0.271 0.159 27.37 16.01

GTLIL 0.047 0.10 0.0057 0.036 12.13 36.00

RPL 0.013 0.033 0.006 0.006 46.15 18.18 (Source: AGM reports of selected companies & moneycontrol.com database)

During the study period, the average Investment Turnover Ratio from 2007 to 2009 is

considered to be pre-acquisition period whereas 2010 to 2013 to be considered as post

acquisition period. The comparison of the pre and post-acquisition, Investment

Turnover Ratio of selected companies is shown in table – 3.2.5

During pre acquisition period (2007 – 2009) it is observed from the table that the pre

acquisition average Investment Turnover Ratio ranges between 0.013times and

1.65times. The highest average of Investment Turnover Ratio is found in Mahindra

and Mahindra Ltd and the lowest is found in Reliance Power Ltd.

During post acquisition period (2011- 2013) it also observed that the post acquisition

Investment Turnover Ratio ranges between 0.033times to 2.07times. The highest

98

average of Investment Turnover Ratio found in Mahindra and Mahindra Ltd and the

lowest is found in Reliance Power Ltd.

During pre acquisition period (2007 – 2009) the Standard deviation of Investment

Turnover Ratio ranges between 0.0057 and 0.46. The highest standard deviation is

found in Lanco Infratech Ltd and the lowest is found in GTL Infrastructure Ltd.

During post acquisition period (2011 – 2013) the Standard deviation of Investment

Turnover Ratio ranges between 0.006 and 0.32. The highest standard deviation is

found in Lanco Infratech Ltd and the lowest is found in Reliance Power Ltd.

Comparing the Co-efficient of Variation of Selected companies in the pre and post

acquisition period from 2007 to 2013 the post acquisition Co-efficient of Variation is

high with respect to GTL Infrastructure Ltd. The study observed that the Investment

Turnover Ratio Co-efficient of Variation is considerably decreased in the post

acquisition.

The analysis of Investment Turnover Ratio of Selected companies reveals the facts

which are as follows:

• Lower the ratio – while comparing the average of Investment Turnover Ratio in

pre and post acquisition period Bharti Airtel Ltd, Hindustan Zinc Ltd, Fortis

Healthcare Ltd and Jindal Steel and Power Ltd have considerably decreased. It

indicates that there is an inefficiency to utilise the investment to improving the

turnover.

• Higher the ratio – Hinduja Global Solutions Ltd, Lanco Infratech Ltd, Mahindra

and Mahindra Ltd, Tata Chemicals Ltd, GTL Infrastructure Ltd and Reliance

Power Ltd have considerably increased in Investment Turnover Ratio due to low

co-efficient of variation in post acquisition period.

During the study period, the average Fixed Assets Turnover Ratio from 2007 to 2009

is considered to be pre-acquisition period whereas 2010 to 2013 to be considered as

post acquisition period. The comparison of the pre and post-acquisition, Fixed Assets

Turnover Ratio of selected companies is shown in table – 3.2.6

99

Table: 3.2.6 Fixed Assets Turnover Ratio of Selected Companies

Companies Mean Standard Deviation

Co - efficient of Variation

Pre Post Pre Post Pre Post

BAL 1.21 1.00 0.25 0.064 20.66 6.40

HGSL 2.027 3.21 0.592 0.406 29.21 12.65

HZL 2.09 1.02 1.44 0.025 68.90 2.45

LIL 10.21 6.55 2.12 3.66 20.76 55.88

FHL 1.28 2.29 0.081 1.04 6.33 45.41

JSPL 0.89 0.81 0.17 0.066 19.10 8.15

M&ML 3.98 4.44 1.66 0.36 41.71 8.11

TCL 1.59 1.77 0.629 0.162 39.56 9.15

GTLIL 0.107 0.147 0.012 0.006 11.21 4.08

RPL 2.13 6.46 2.17 1.21 101.88 18.73 (Source: AGM reports of selected companies & moneycontrol.com database)

During pre acquisition period (2007 – 2009) it is observed from the table that the pre

acquisition average Fixed Assets Turnover Ratio ranges between 0.107times and

10.21times. The highest average of Fixed Assets Turnover Ratio is found in Lanco

Infratech Ltd and the lowest is found in GTL Infrastructure Ltd.

During post acquisition period (2011- 2013) it also observed that the post acquisition

Fixed Assets Turnover Ratio ranges between 0.147times to 6.55times. The highest

average of Fixed Assets Turnover Ratio found in Lanco Infratech Ltd and the lowest

is found in GTL Infrastructure Ltd.

During pre acquisition period (2007 – 2009) the Standard deviation of Fixed Assets

Turnover Ratio ranges between 0.012 and 2.17. The highest standard deviation is

found in Reliance Power Ltd and the lowest is found in GTL Infrastructure Ltd.

During post acquisition period (2011 – 2013) the Standard deviation of Fixed Assets

Turnover Ratio ranges between 0.006 and 3.66. The highest standard deviation is

found in Lanco Infratech Ltd and the lowest is found in GTL Infrastructure Ltd.

100

Comparing the Co-efficient of Variation of Selected companies in the pre and post

acquisition period from 2007 to 2013 the post acquisition Co-efficient of Variation is

high with respect to Lanco Infratech Ltd and Fortis Healthcare Ltd. The study

observed that the Fixed Assets Turnover Ratio Co-efficient of Variation is

considerably decreased in the post acquisition.

The analysis of Fixed Assets Turnover Ratio of Selected companies reveals the facts

which are as follows:

• Lower the ratio – while comparing the average of Fixed Assets Turnover Ratio in

pre and post acquisition period Bharti Airtel Ltd, Hindustan Zinc Ltd, Lanco

Infratech Ltd and Jindal Steel and Power Ltd have considerably decreased. It

indicates that lack of operational efficiency and revenue generating activities.

• Higher the ratio – Hinduja Global Solutions Ltd, Fortis Healthcare Ltd, Mahindra

and Mahindra Ltd, Tata Chemicals Ltd, GTL Infrastructure Ltd and Reliance

Power Ltd have considerably increased in Fixed Assets Turnover Ratio due to low

co-efficient of variation in post acquisition period.

Table: 3.2.7 Total Assets Turnover Ratio of Selected Companies

Companies Mean Standard Deviation

Co - efficient of Variation

Pre Post Pre Post Pre Post

BAL 1.14 0.77 0.136 0.127 11.93 16.49

HGSL 0.434 0.682 0.186 0.043 42.86 6.30

HZL 0.74 0.42 0.37 0.027 50.00 6.43

LIL 0.78 0.89 0.462 0.321 59.23 36.07

FHL 0.15 0.073 0.010 0.006 6.67 8.22

JSPL 0.68 0.49 0.077 0.032 11.32 6.53

M&ML 1.66 2.09 .25 0.205 15.06 9.81

TCL 0.993 0.993 0.271 0.159 27.29 16.01

GTLIL 0.05 0.10 0.010 0.036 20.00 36.00

RPL 0.013 0.033 0.006 0.006 46.15 18.18 (Source: AGM reports of selected companies & moneycontrol.com database)

101

During the study period, the average Total Assets Turnover Ratio from 2007 to 2009

is considered to be pre-acquisition period whereas 2010 to 2013 to be considered as

post acquisition period. The comparison of the pre and post-acquisition, Total Assets

Turnover Ratio of selected companies is shown in table – 3.2.7

During pre acquisition period (2007 – 2009) it is observed from the table that the pre

acquisition average Total Assets Turnover Ratio ranges between 0.013times and

1.66times. The highest average of Total Assets Turnover Ratio is found in Mahindra

and Mahindra Ltd and the lowest is found in Reliance Power Ltd.

During post acquisition period (2011- 2013) it also observed that the post acquisition

Total Assets Turnover Ratio ranges between 0.033times to 2.09times. The highest

average of Total Assets Turnover Ratio found in Mahindra and Mahindra Ltd and the

lowest is found in Reliance Power Ltd.

During pre acquisition period (2007 – 2009) the Standard deviation of Total Assets

Turnover Ratio ranges between 0.006 and 0.462. The highest standard deviation is

found in Lanco Infratech Ltd and the lowest is found in Reliance Power Ltd.

During post acquisition period (2011 – 2013) the Standard deviation of Total Assets

Turnover Ratio ranges between 0.006 and 0.321. The highest standard deviation is

found in Lanco Infratech Ltd and the lowest is found in Reliance Power Ltd.

Comparing the Co-efficient of Variation of Selected companies in the pre and post

acquisition period from 2007 to 2013 the post acquisition Co-efficient of Variation is

high with respect to Bharti Airtel Ltd, Fortis Healthcare Ltd and GTL Infrastructure

Ltd. The study observed that the Total Assets Turnover Ratio Co-efficient of

Variation is considerably decreased in the post acquisition.

The analysis of Total Assets Turnover Ratio of Selected companies reveals the facts

which are as follows:

• Lower the ratio – while comparing the average of Total Assets Turnover Ratio in

pre and post acquisition period Bharti Airtel Ltd, Hindustan Zinc Ltd, Fortis

Healthcare Ltd and Jindal Steel and Power Ltd have considerably decreased. It

102

indicates lower sales revenue. The notion of low profit margin tends to have

negative impact on assets turnover.

• Higher the ratio – Hinduja Global Solutions Ltd, Lanco Infratech Ltd, Mahindra

and Mahindra Ltd, Tata Chemicals Ltd, GTL Infrastructure Ltd and Reliance

Power Ltd have considerably increased in Total Assets Turnover Ratio due to low

co-efficient of variation in post acquisition period.

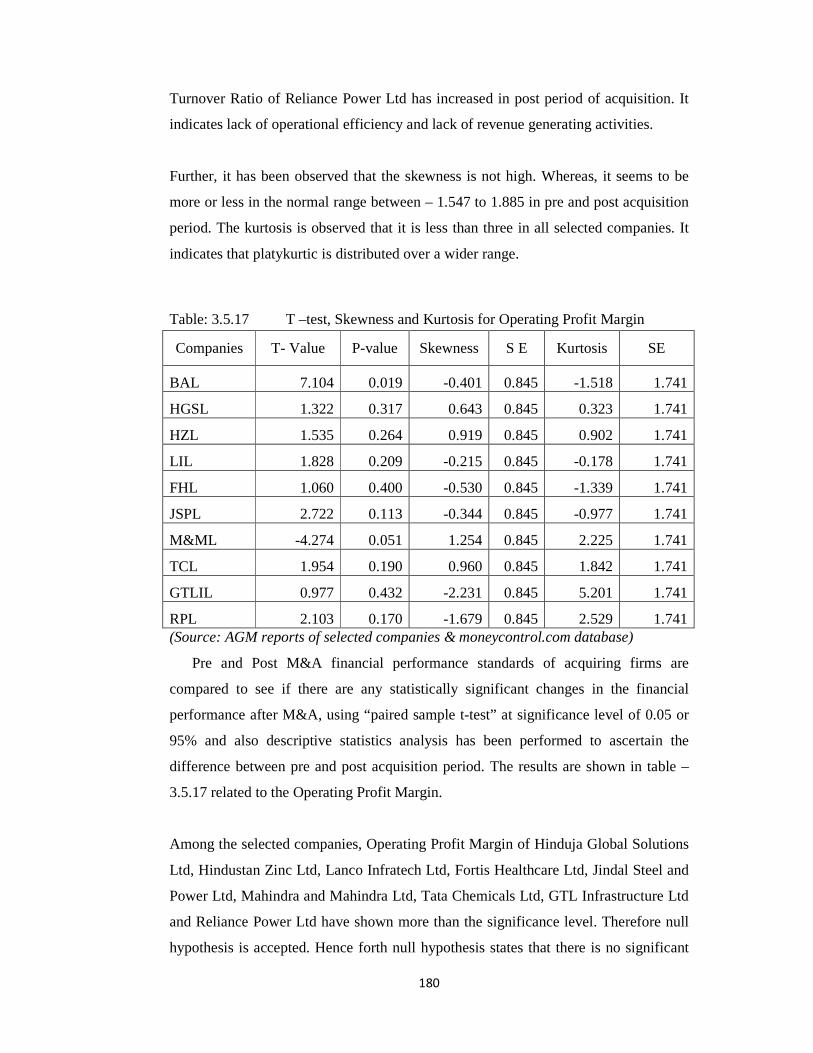

Table: 3.2.8 Operating Profit Margin of Selected Companies

Companies Mean Standard Deviation

Co - efficient of Variation

Pre Post Pre Post Pre Post

BAL 40.25 32.52 1.359 2.70 3.38 8.30

HGSL 24.02 18.89 4.06 3.38 16.90 17.89

HZL 63.86 53.19 14.10 2.17 22.08 4.08

LIL 18.30 11.74 3.86 3.65 21.09 31.09

FHL 5.50 2.47 1.94 3.25 35.27 131.58

JSPL 39.04 31.40 4.29 5.60 10.99 17.83

M&ML 10.50 12.73 0.85 1.73 8.10 13.59

TCL 23.91 12.91 10.31 0.57 43.12 4.42

GTLIL 59.06 29.99 11.03 57.95 18.68 193.23

RPL 0 -469 0 386.99 0 -82.51 (Source: AGM reports of selected companies & moneycontrol.com database)

During the study period, the average Operating Profit Margin from 2007 to 2009 is

considered to be pre-acquisition period whereas 2010 to 2013 to be considered as post

acquisition period. The comparison of the pre and post-acquisition, Operating Profit

Margin of selected companies is shown in table – 3.2.8

During pre acquisition period (2007 – 2009) it is observed from the table that the pre

acquisition average Operating Profit Margin ranges between 0% and 63.86%. The

highest average of Operating Profit Margin is found in Hindustan Zinc Ltd and the

lowest is found in Reliance Power Ltd.

103

During post acquisition period (2011- 2013) it also observed that the post acquisition

Operating Profit Margin ranges between -469% to 53.19% . The highest average of

Operating Profit Margin found in Hindustan Zinc Ltd and the lowest is found in

Reliance Power Ltd.

During pre acquisition period (2007 – 2009) the Standard deviation of Operating

Profit Margin ranges between 0and 14.10. The highest standard deviation is found in

Hindustan Zinc Ltd and the lowest is found in Reliance Power Ltd.

During post acquisition period (2011 – 2013) the Standard deviation of Operating

Profit Margin ranges between 0.57 and 386.99. The highest standard deviation is

found in Reliance Power Ltd and the lowest is found in Tata Chemicals Ltd.

Comparing the Co-efficient of Variation of Selected companies in the pre and post

acquisition period from 2007 to 2013 the post acquisition Co-efficient of Variation is

high with respect to Bharti Airtel Ltd, Hinduja Global Solutions Ltd, Lanco Infratech

Ltd, Fortis Healthcare Ltd, Jindal Steel and Power Ltd, Mahindra and Mahindra Ltd

and GTL Infrastructure Ltd. The study observed that the Operating Profit Margin Co-

efficient of Variation is considerably increased in the post acquisition.

The analysis of Operating Profit Margin of Selected companies reveals the facts

which are as follows:

• Lower the ratio – while comparing the average of Operating Profit Margin in pre

and post acquisition period overall selected firms have considerably decreased

however, Mahindra and Mahindra Ltd was the exception. It indicates worsened on

account of lower cash flow streams generated by operating activities.

• Higher the ratio –Mahindra and Mahindra Ltd has considerably increased in

Operating Profit Margin due to low co-efficient of variation in post acquisition

period.

104

3. Examine the impact of Mergers and Acquisitions on value of the firms.

On analysis of examining the firm value measures, the total networth of the firms

in long run is explained herewith. Value added / shortfall ensures the percentage of

value addition and firm value ensures long term survival. In order to identify the

changes in Value added/Shortfall, economic value added and firm value after Mergers

and Acquisitions studies are made separately for each group. However, economic

value added model is used to identify the firm value. In this heading, an analysis has

been done with the help of Value added/Shortfall, economic value added and firm

value by using statistical tools like mean, standard deviation and co- efficient of

variance to examine the firm value of selected Mergers and Acquisitions during the

study period.

Table: 3.3.1 Value Addition/Shortfall of Selected Companies

Companies Mean Standard Deviation

Co - efficient of Variation

Pre Post Pre Post Pre Post

BAL 16.65 2.97 1.74 5.55 10.45 186.87

HGSL 4.79 1.60 7.39 3.63 154.28 226.88

HZL 30.58 14.77 18.70 1.18 61.15 7.99

LIL 3.30 -0.52 5.06 0.16 153.33 -30.77

FHL -7.72 -2.88 1.50 2.96 -19.43 -102.78

JSPL 14.22 4.75 6.44 2.00 45.29 42.11

M&ML 52.40 47.16 43.06 12.51 82.18 26.53

TCL 9.51 0.35 6.47 0.765 68.03 218.57

GTLIL -2.73 -8.42 0.75 4.23 -27.47 -50.24

RPL -0.793 -2.87 4.61 0.48 -581.34 -16.72 (Source: AGM reports of selected companies & moneycontrol.com database)

During the study period, the average Value Addition/Shortfall from 2007 to 2009 is

considered to be pre-acquisition period whereas 2010 to 2013 is to be considered as

post acquisition period. The comparison of the pre and post-acquisition, Value

Addition/Shortfall of selected companies is shown in table – 3.3.1

105

During pre acquisition period (2007 – 2009) it is observed from the table that the pre

acquisition average Value Addition/Shortfall ranges between (7.72%) and 52.40%.

The highest average of Value Addition is found in Mahindra & Mahindra Ltd and the

highest average of shortfall is found in Fortis Healthcare Ltd.

During post acquisition period (2011- 2013) it also observed that the post acquisition

Value Addition/Shortfall ranges between (8.42%) and 47.16%.The highest average of

Value Addition is found in Mahindra & Mahindra Ltd and the Highest average of

Shortfall is found in GTL Infrastructure Ltd.

During pre acquisition period (2007 – 2009) the Standard deviation of Value

Addition/Shortfall ranges between 0.75 and 43.06. The highest standard deviation is

found in Mahindra & Mahindra Ltd. The lowest standard deviation is found in GTL

Infrastructure Ltd.

During post acquisition period (2011 – 2013) the Standard deviation of Value

Addition ranges between 0.16 and 12.51. The highest standard deviation is found in

Mahindra & Mahindra Ltd. The lowest standard deviation is found in Lanco Infratech

Ltd.

Comparing the Co-efficient of Variation of Selected companies in the pre and post

acquisition period from 2007 to 2013 the post acquisition Co-efficient of Variation is

high with respect to Bharti Airtel, Hinduja Global Solutions Ltd and Tata Chemicals

Ltd. The study observed that the Value Addition Co-efficient of Variation is

considerably decreased in the post acquisition.

The analysis of Value Addition / Shortfall of Selected companies reveals the facts

which are as follows:

Lower the ratio – while comparing the average of Value Addition in pre and post

acquisition period overall selected companies have considerably decrease

performance due to high cost of capital in post acquisition. It indicates that

acceleration of the funds failed to increase its value addition.

106

Table: 3.3.2 Economic Value Added of Selected Companies

Companies Mean Standard Deviation

Co - efficient of Variation

Pre Post Pre Post Pre Post

BAL 4974.96 1737.72 2079.52 3564.20 41.80 205.11

HGSL 31.18 11.79 46.50 28.42 149.13 241.05

HZL 3084.70 4099.19 951.03 767.36 30.83 18.72

LIL 81.84 -37.94 104.15 10.55 127.26 -27.81

FHL -77.08 -118.80 5.79 127.73 -7.51 -107.52

JSPL 1236.45 1182.04 652.87 276.11 52.80 23.36

M&ML 876.44 2909.13 253.29 646.01 28.90 22.21

TCL 524.56 23.76 411.03 60.34 78.36 253.96

GTLIL -83.25 -329.51 82.69 99.92 -99.33 -30.32

RPL -170.24 -501.95 155.32 98.90 -91.24 -19.70 (Source: AGM reports of selected companies & moneycontrol.com database)

During the study period, the average Economic Value Added from 2007 to 2009 is

considered to be pre-acquisition period whereas 2010 to 2013 is to be considered as

post acquisition period. The comparison of the pre and post-acquisition, Economic

Value Added of selected companies is shown in table – 3.3.2

During pre acquisition period (2007 – 2009) it is observed from the table that the pre

acquisition average Economic Value Added ranges between (170.24)Crores and

4,974.96Crores. The highest average of Economic Value Added is found in Bharti

Airtel Ltd and the lowest average is found in Reliance Power Ltd.

During post acquisition period (2011- 2013) it also observed that the post acquisition

Economic Value Added ranges between (501.95)Crores and 4099.19Crores.The

highest average of Economic Value Added is found in Hindustan Zinc Ltd and the

Lowest average is found in Reliance Power Ltd.

During pre acquisition period (2007 – 2009) the Standard deviation of Economic

Value Added ranges between 5.79 and 2079.52. The highest standard deviation is

107

found in Bharti Airtel Ltd. The lowest standard deviation is found in Fortis Healthcare

Ltd.

During post acquisition period (2011 – 2013) the Standard deviation of Economic

Value Added ranges between 10.55 and 3564.20. The highest standard deviation is

found in Bharti Airtel Ltd. The lowest standard deviation is found in Lanco Infratech

Ltd.

Comparing the Co-efficient of Variation of Selected companies in the pre and post

acquisition period from 2007 to 2013 the post acquisition Co-efficient of Variation is

high with respect to Bharti Airtel, Hinduja Global Solutions Ltd and Tata Chemicals

Ltd. The study observed that the Economic Value Added Co-efficient of Variation is

considerably decreased in the post acquisition.

The analysis of Economic Value Added of Selected companies reveals the facts which

are as follows:

• Lower the ratio – while comparing the average of Economic Value Added in pre

and post acquisition period overall selected firms have considerably decreased

however, Hindustan Zinc Ltd and Mahindra & Mahindra Ltd was the exception. It

indicates worsened on account of lower cash flow streams generated by operating

activities.

• Higher the ratio – Hindustan Zinc Ltd and Mahindra and Mahindra Ltd has

considerably increased in Economic Value Added due to low co-efficient of

variation in post acquisition period.

108

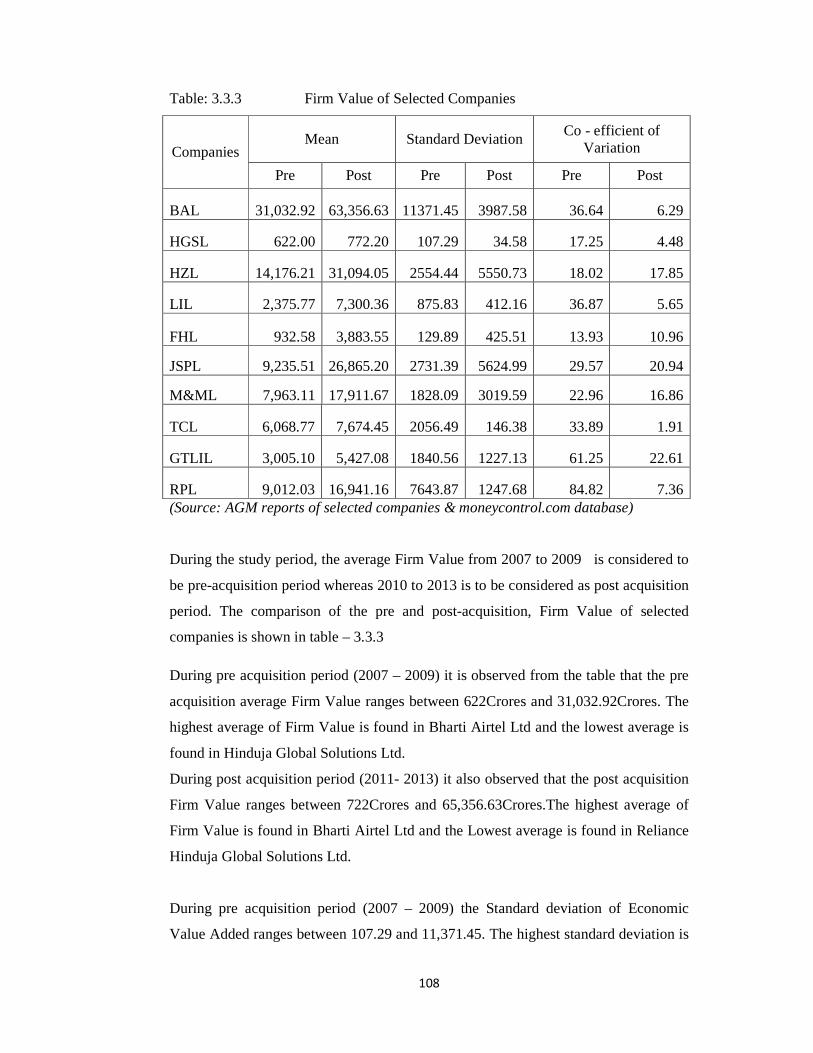

Table: 3.3.3 Firm Value of Selected Companies

Companies Mean Standard Deviation

Co - efficient of Variation

Pre Post Pre Post Pre Post

BAL 31,032.92 63,356.63 11371.45 3987.58 36.64 6.29

HGSL 622.00 772.20 107.29 34.58 17.25 4.48

HZL 14,176.21 31,094.05 2554.44 5550.73 18.02 17.85

LIL 2,375.77 7,300.36 875.83 412.16 36.87 5.65

FHL 932.58 3,883.55 129.89 425.51 13.93 10.96

JSPL 9,235.51 26,865.20 2731.39 5624.99 29.57 20.94

M&ML 7,963.11 17,911.67 1828.09 3019.59 22.96 16.86

TCL 6,068.77 7,674.45 2056.49 146.38 33.89 1.91

GTLIL 3,005.10 5,427.08 1840.56 1227.13 61.25 22.61

RPL 9,012.03 16,941.16 7643.87 1247.68 84.82 7.36 (Source: AGM reports of selected companies & moneycontrol.com database)

During the study period, the average Firm Value from 2007 to 2009 is considered to

be pre-acquisition period whereas 2010 to 2013 is to be considered as post acquisition