Chapter 20 The Fed, Depository Institutions, and the Money Supply Process Copyright ©2006 by...

57

Chapter 20 The Fed, Depository Institutions, and the Money Supply Process Copyright ©2006 by South-Western, a division of Thomson Learning. All rights reserved.

-

date post

21-Dec-2015 -

Category

Documents

-

view

216 -

download

3

Transcript of Chapter 20 The Fed, Depository Institutions, and the Money Supply Process Copyright ©2006 by...

Chapter 20

The Fed, Depository Institutions, and the Money Supply Process

Copyright ©2006 by South-Western, a division of Thomson Learning. All rights reserved.

2

Open Market Operations

• Open market operations are the buying and selling of government securities by the Fed– open market operations affect the supply of

reserves available to depository institutions• the volume of reserves affects the banking

system’s ability to extend loans to expand the money supply

3

The Money Supply Process

Open Market

Operations

Reserves

Credit Availability

Money Supply

Deposit Creation

Interest Rates

Lending

4

Open Market Operations

• When the Fed buys securities, reserves of depository institutions rise

• When the Fed sells securities, reserves of depository institutions fall

5

Open Market Operations

• Suppose the Fed wishes to increases the supply of reserves by $1,000– the trading desk of the New York Fed will buy

$1,000 of Treasury securities• the Fed pays for these securities by writing a

check

– the sellers will deposit these checks into the banking system (assume they use HLT National Bank)

• the Fed will credit the bank’s account at the Fed

6

Open Market Operations

• After the open market purchase– the Fed has $1,000 more in securities and the

dealers have $1,000 less in securities– the public gets $1,000 in checks from the Fed

• these deposits are assts to the public and a liability to the Fed

• After the checks are returned to the Fed– the bank has $1,000 more in its account at

the Fed

7

The Effect of Open Market Operations on Reserves

8

Discount Loans

• The Fed controls the amount of required reserves that depository institutions must hold

• If depository institutions cannot meet their required reserves, they may borrow reserves at the discount window– the interest rate charged by the Fed is called

the discount rate

9

Discount Loans

• Changes in the discount lending also affect the volume of reserves in the banking system– when the Fed makes a discount loan, reserve

assets increase by the amount of the loan• the effect is the same as an open market purchase

– when the loan is repaid, reserve assets fall• the effect is the same as an open market sale

10

The Effect of Discount Loans on the Monetary Base

11

Discount Loans

• The Fed cannot completely control the amount of borrowing from the discount window– can encourage or discourage borrowing by

lowering or raising the discount rate– the Fed can refuse to make a discount loan

12

Factors That Affect the Reserves of Depository Institutions

Factors that increase reserves:

Open Market Purchases

Increases in Discount Loans

Factors that decrease reserves:

Open Market SalesDecreases in

Discount Loans

13

Other Factors that Change Reserves

• Other factors can affect reserves

• The Fed can respond to changes in reserves caused by these other factors with offsetting open market operations

14

Other Factors that Change Reserves

• The check-clearing process can take a few days– deposits and reserves in the banking system

may be temporarily higher than they otherwise would be

– this is called the Federal Reserve float– the Fed can offset this by selling securities if it

wishes

15

Prototype Balance Sheetfor a Bank

Assets

Reserves

Loans

Liabilities

Checkable Deposits

16

Loan and Deposit Expansion

• After the checks from the Fed clear, HLT National bank has $1,000 in new reserves– if the Fed insists that HLT hold required

reserves equal to 10% of checkable deposits, the remaining 90% of reserves are excess reserves

• $100 of the new reserves are required reserves• $900 of the new reserves are excess reserves

– HLT will lend the $900 in excess reserves

17

Loan and Deposit Expansion at HLT National Bank

18

Loan and Deposit Expansion

• HLT’s balance sheet shows a $900 increase in assets (the loan) and a $900 increase in liabilities (new deposit)

• The customer who took out the loan will likely spend the funds– they will become redeposited into the banking

system (assume at Second National Bank)

19

Transactions between HLT National Bank and Second

National Bank

20

Loan and Deposit Expansion

• This transaction reduces HLT’s deposits and liabilities by $900

• The initial deposit at HLT is balanced by a $100 rise in reserves (all required) and a $900 rise in loans– HLT is fully loaned up

• has no excess reserves left to lend

21

Loan and Deposit Expansion

• Second National Bank is not fully loaned up– has $810 in excess reserves to lend– if the loan is made, the funds will likely be

spent and then redeposited in the banking system (assume at Third National Bank)

22

Transactions of Second National Bank and Third National Bank

23

Loan and Deposit Expansion

• As the loans of one depository institution increase, the use of the loan proceeds by the borrower leads to a deposit inflow at another institution– this increases total deposit liabilities and

reserve assets

24

Loan and Deposit Expansion

• The change in deposits at each depository institution can be represented as the change in required reserves plus the change in excess reserves– the change in required reserves is equal to

10% of the deposit inflow– the change in excess reserves is equal to

90% of the deposit inflow

25

The Simple Multiplier Model

• The process of creating money and credit from increases in reserves will end when all reserves become required reserves– the banking system is fully loaned up

26

The Simple Multiplier Model

• Required reserve assets (RR) are equal to the required reserve ratio (rD) multiplied by the amount of deposit liabilities (D)

RR = rD D

• Excess reserves (ER) are equal to total reserves (TR) minus required reserves

ER = TR – RR

27

The Simple Multiplier Model

• If total reserves are equal to required reserves

TR = RR = rD D

D = TR/rD

D = 1/rD TR

• We shall refer to 1/rD as the simple money multiplier

28

The Simple Multiplier Model

• For any change in total reserves, the change in deposits will equal

D = 1/rD TR

• In our example, the increase in deposits from the $1,000 increase in reserves will be

D = 1/0.10 $1,000 = $10,000

29

The Simple Multiplier Model

• The simple multiplier process is a reflection of what is called the fractional reserve banking system– a depository institution must hold reserve

assets equal to a fraction of deposit liabilities

• The smaller the required reserve ratio is, the larger will be the simple money multiplier

30

The Required Reserve Ratio and the Simple Money Multiplier

31

The Simple Multiplier Model

• The whole process can be viewed as an inverted pyramid– the original injection by the Fed leads to an

increase in reserve assets and liabilities and leaves banks with excess reserves

– the banks respond by extending loans– these loans are deposited in other banks who

then also make loans– the process continues until all banks are

loaned up

32

The Simple Multiplier Model

• As a result, the original injection of reserves can support a multiple expansion in loans and deposits

33

An Inverted Pyramid Representing the Money Supply and the Monetary Base

34

The Multiple Expansion of Deposits and Loans in the Banking System

(Initial Increase in Reserves of $1,000 and a Multiplier of 10)

35

The Multiplier Effect of an Increase in Reserves

36

Policy Implications

• A given dollar change in reserves will lead to a larger change in the money supply

• If the multiplier was as simple as 1/rD, the Fed could control the money supply precisely– in reality, the multiplier is more complicated

and is not under the Fed’s complete control

37

Some Complicating Realities in the Multiplier Model

• In our simple model, we assumed that banks do not hold excess reserves– in fact, banks do choose to hold excess

reserves– these excess reserves are leakages from the

flow of new deposits– this will lower the volume of loans and

deposits created at each stage

38

Some Complicating Realities in the Multiplier Model

• We also ignored the fact that individuals will choose to hold some currency– this means that all loan proceeds may not

become redeposited in the banking system– this will also reduce the flow of reserves and

deposits from bank to bank

39

Modifying the Multiplier Model

• Total reserves are equal to required reserves plus excess reserves

TR = RR + ER

TR = rDD + ER

• Assume that depository institutions hold excess reserve assets equal to a constant proportion of deposit liabilities (eD) where

e = ER/D

40

Modifying the Multiplier Model

• This means that

TR = rDD + eD = (rD + e)D

• This means that, for a given change in total reserves, the change in deposits will be

1

D

D TRr e

41

Modifying the Multiplier Model

• The multiplier is now smaller than before

• The multiplier is not under the complete control of the Fed– the Fed cannot control e

42

Modifying the Multiplier Model

• The public can also affect the money multiplier by its currency-holding behavior

• Assume the public wants to hold currency equal to a constant proportion of its checkable deposits (cD) where

c = C/D

43

Modifying the Multiplier Model

• Thus, the money supply is equal to

M = D + C = D + cD = (1 + c)D

• We define the monetary base (MB) as the sum of reserves and currency in the hands of the public

MB = TR + C

MB = (rD + e)D + cD = (rD + e + c)D

44

Modifying the Multiplier Model

• Rearranging, we get

1

D

D MBr e c

• The money supply is equal to deposits plus currency

1

D

M D C MB Cr e c

45

Modifying the Multiplier Model

• Rearranging, we get

1

D

M MB cDr e c

1 1

D D

M MB c MBr e c r e c

1

D

cM MB

r e c

46

Modifying the Multiplier Model

• In terms of changes in the money supply that result from changes in the monetary base, we get

1

D

cM MB

r e c

• We will refer to this as the money multiplier

47

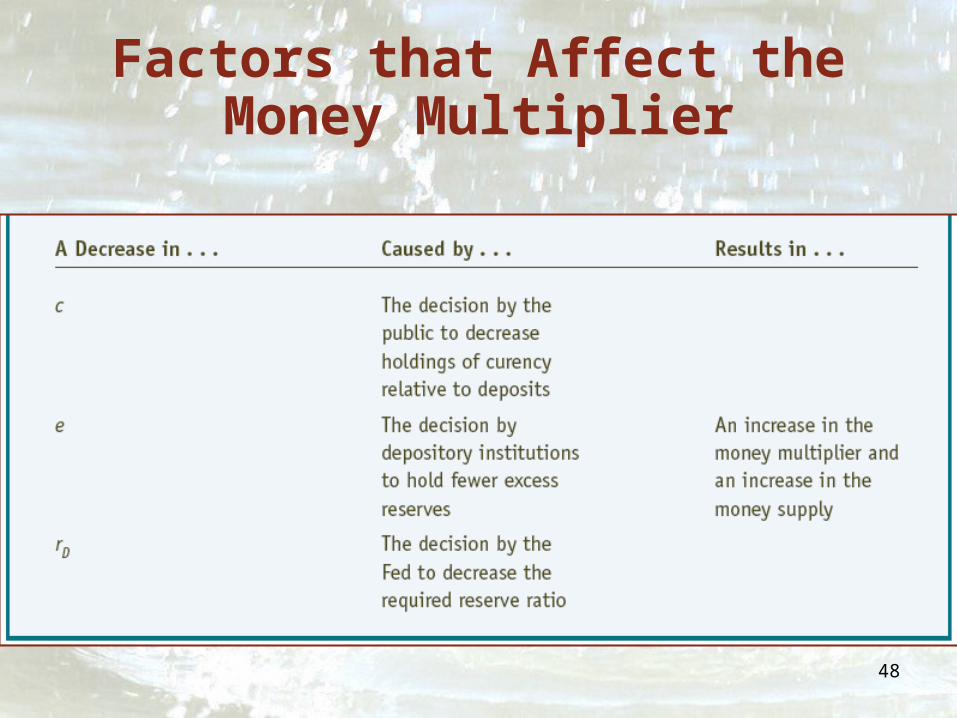

Factors that Affect theMoney Multiplier

48

Factors that Affect theMoney Multiplier

49

The Fed’s Control over the Money Supply

• The Fed’s control of the money supply is not complete– the public controls c (the proportion of

deposits held as currency)– depository institutions control e (the

proportion of deposits held as excess reserves)

50

Summary of Major Points

• The Fed’s open market operations affect the quantity of reserves in the banking system– when the Fed buys securities, reserves of

depository institutions rise– when the Fed sells securities, reserves of

depository institutions fall

51

Summary of Major Points

• Depository institutions must hold reserve assets– reserves in excess of required reserves are

called excess reserves

• When the Fed makes a discount loan or a loan is paid off, reserves are affected

52

Summary of Major Points

• For a depository institution, a deposit inflow will increase total deposit liabilities and total reserve assets– a depository institution can adjust to the inflow

of deposits by expanding its loans and “creating” additional deposits equal to the amount of excess reserves that result from the deposit inflow

53

Summary of Major Points

• As the proceeds of a loan are spent, the lending institution will lose reserves– another institution will gain reserves– this institution can expand loans and create

additional deposits in the amount of excess reserves that flow to it

54

Summary of Major Points

• Following an initial injection of reserves, the total volume of reserves in the banking system does not change– the composition of reserves changes– as deposits expand at each stage, required

reserves rise and excess reserves fall

55

Summary of Major Points

• The total expansion of loans and deposits is a multiple of the initial injection of reserves into the banking system– in the simplest model, the multiplier is 1/rD

• ignores excess reserves and currency• the lower the required reserve ratio, the larger the

multiplier is

56

Summary of Major Points

• The monetary base is reserves plus currency in the hands of the public– in a more elaborate model that takes account

of excess reserves and currency holding s of the public, the multiplier is a multiple of the change in the monetary base

• it is smaller than the simple multiplier• it is influenced by the behavior of the Fed, deposit

institutions, and the public

57

Summary of Major Points

• Even if the Fed can control the monetary base, it may have difficulty controlling the money supply in the short run– over a longer period, the fluctuations in the

multiplier tend to offset one another