CHAPTER 2 LITERATURE REVIEW -...

48

27 CHAPTER 2 LITERATURE REVIEW This literature review is the part of research that endeavors to fill the gap in domain of research by exploring the different variables that covers the nomological network of the study in reference of the financial sector with special emphasis on India. The nomological network for this study contained variables such as Customer expectation, Perceived Service quality, Customer satisfaction and Customer Behavioral intentions. The first three variables above are independently or in association with other variables are assumed as capable of developing behavioral intentions in customer. The scope of the chapter is to introduce the variables of interest in this study and to examine the nature of linkages among the variables identified in previous studies especially in the context of financial sector. The first four sections will narrate the conceptual theories and prevailing practices in measurement the variables of interest in the study. The next section will summarize some of established models linking all the variables including studies related to financial sector with the critical objective of developing a theory for this study. The last section will offer a brief summary of various outputs from the literature review. 2.1 CUSTOMER EXPECTATIONS Expectations are Pre-trial beliefs about a service that functions as a standard against which performance is judged by the customer (Donna J. Hill 1986). Expectation is viewed, as perceived contingencies

Transcript of CHAPTER 2 LITERATURE REVIEW -...

27

CHAPTER 2

LITERATURE REVIEW

This literature review is the part of research that endeavors to fill

the gap in domain of research by exploring the different variables that covers

the nomological network of the study in reference of the financial sector with

special emphasis on India. The nomological network for this study contained

variables such as Customer expectation, Perceived Service quality, Customer

satisfaction and Customer Behavioral intentions. The first three variables

above are independently or in association with other variables are assumed as

capable of developing behavioral intentions in customer. The scope of the

chapter is to introduce the variables of interest in this study and to examine

the nature of linkages among the variables identified in previous studies

especially in the context of financial sector. The first four sections will narrate

the conceptual theories and prevailing practices in measurement the variables

of interest in the study. The next section will summarize some of established

models linking all the variables including studies related to financial sector

with the critical objective of developing a theory for this study. The last

section will offer a brief summary of various outputs from the literature

review.

2.1 CUSTOMER EXPECTATIONS

Expectations are Pre-trial beliefs about a service that functions as a

standard against which performance is judged by the customer

(Donna J. Hill 1986). Expectation is viewed, as perceived contingencies

28

between any two events of human or technical related experiences in a service

context. These events can be contingencies between an action and an outcome

or can be a contingency between two attributes such as high price and

implying high quality (Sheth and Mittal 1996). Word-of-mouth

communication between customers, the personal needs of customers, past

experiences of customers and external communications from service

providers (Parasuraman et al 1991), forms major reasons for customer

expectations.

The needs of the customer provides objective reasons (Martula and

Menon 1995) for expectations whereas past experiences (Lilley and

Usherwood 2000) in many cases become instrumental in developing

expectations. Oliver (1980) identified three factors responsible for

expectations namely the product, the context and the individual

characteristics. Winer (1985) acknowledged the significance of consumer

characteristics as sources of consumer expectation. Carman (1990) opinioned

that expectations are likely to change with familiarity and hence, if possible,

the level of familiarity should be gauged along with the expectations.

Calvert (2001) identified six factors which can have an impact on customer

expectation. Out of these six factors the first four are related to customer, the

fifth factor relates to service provider and the last factor is related to

competitors as mentioned below.

The customer related factors,

Past experience of the customer;

Word-of-mouth from other customers;

Personal needs of the customer; and

National culture of the customer.

29

The service provider related factor,

Communications (direct and indirect) about what the customer

can expect.

Competitors related factor,

Service provided by other providers that acts as a benchmark

Ojasolo (2001) emphasized the importance of understanding and

managing expectations in diagnosing problems related to customer relations

whereby creating sustainable long-term relationships. Various Expectation

standards were proposed by researchers. Woodruff et al (1993) proposed that

customers rely on standards that focal brand provide to meet needs and wants

and form an experience based norms for expectations. Miller (1977) proposed

minimum tolerable expectations and defined it as lower level of expectation

acceptable to the customer reflecting customer’s subjective evaluation of their

own product investment. Prakash ved (1984) proposed a standard called

comparative expectation based on comparing with similar brands

In service quality and customer satisfaction literature, expectations

are interpreted differently. In service quality, expectations have a normative

role and are based on past experience and they provide the consumer's view

of what should happen. In the customer satisfaction literature, expectations

are usually linked to what consumers forecast and therefore have a more

predictive role and they relate to what will happen (Parasuraman et

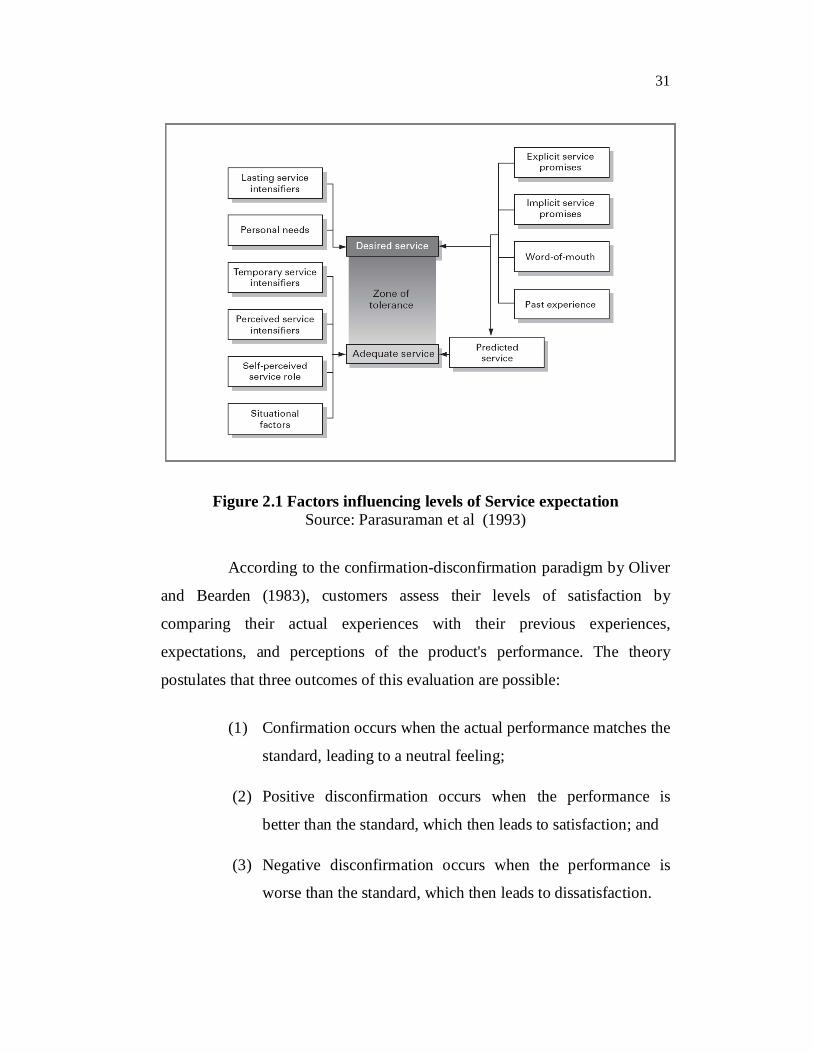

al1993).The concept of Zone of tolerance(ZOT) (Parasuraman et al 1993)

suggested that expectations in service quality has different levels of normative

expectations. Parasuraman et al (1993) defined ‘ZOT’ as the range of

customer perceptions of a service between desired and adequate level of

service. Desired service is defined as the blend of what can and should be

30

provided whereas the 'adequate' service quality level is defined as the

minimum level of service performance customers consider as adequate. The

authors of ‘ZOT’ theory proposed that the desired service level is relatively

stable but that the adequate service level moves up and down according to

consumer circumstances and needs.

In essence, ‘ZOT’ represents range of service performance that a

customer considers satisfactory or the range within which customers are

willing to accept variations in service delivery. Performance below the zone is

seen as dissatisfying and performance above the zone is seen as delighting.

The width ‘ZOT’ may vary from customer to customer and from situation to

situation and are likely to be influenced by involvement, individual quality

factors and past experiences (Parasuraman et al 1993).A wider ZOT means

that customers are more tolerant of variations in service levels and

organizations have more scope in managing their service. Parasuraman et al

(1993) in their comprehensive framework of service expectations explained

eleven antecedent factors which can have effect on expectation regarding

levels of service as shown in Figure 21.

Salehi and Rostami (2009) suggested the need to describe

expectation as a difference between anticipation of the facts and reference for

comparison. Expectations as a reference for comparison can be used as a

measure for evaluating satisfaction of customers. However, from the point of

view of the customer, the choice of a product is not only affected by his

expectations, but is also influenced by his needs. In many occasions

expectations may be the reason for acquiring a product or receiving a certain

service rather than needs. Also in most of the occasions customer expectation

and needs may be exactly the same, and even interchangeable. Hence it can

be assumed that expectations may be both what people expect and what they

want, and does not necessarily have to coincide with what they need.

31

Figure 2.1 Factors influencing levels of Service expectationSource: Parasuraman et al (1993)

According to the confirmation-disconfirmation paradigm by Oliver

and Bearden (1983), customers assess their levels of satisfaction by

comparing their actual experiences with their previous experiences,

expectations, and perceptions of the product's performance. The theory

postulates that three outcomes of this evaluation are possible:

(1) Confirmation occurs when the actual performance matches the

standard, leading to a neutral feeling;

(2) Positive disconfirmation occurs when the performance is

better than the standard, which then leads to satisfaction; and

(3) Negative disconfirmation occurs when the performance is

worse than the standard, which then leads to dissatisfaction.

32

The use of expectations as a basis for conceptualizing service

quality has given rise to numerous criticisms. Cronin and Taylor (1992), and

Teas (1993) argue that it is useless to recur to use expectations, in an attempt

to measure service quality, and that only perception should be used. Also

expectations always have a tendency to be high on their own, so the results

they provide when considered alone are not useful (Brown et al 1993). In this

study expectation component is not considered for assessing service quality,

rather the antecedent role of expectations was considered and an attempt was made to analyze customer expectations in a different perspective.

2.2 SERVICE QUALITY

Service quality can be considered as a differentiator that decides

the advantage a service firm enjoys in the competitive environment.

Marketers realized that to retain customers, and to support market growth,

they must provide high quality of service (Dabholkar et al 2000). It is said

that service quality is an important antecedent of consumer assessment of

value, which in turn influences customer satisfaction, which then motivates

loyalty (Babakus and Boller 1992). There has been much debate as to what

constitute service quality and how its measures can be operationalized in

various service industries, yet no consensus has been reached (Chowdary and

Prakash 2007). The following section traces the understanding service quality

to form the basis for the conceptualization of this construct in this study.

The first usage of the word “service quality” was surfaced in when

Anderson et al (1976) recognized importance of it for obtaining and retaining

customers. However substantial research were absent till early 1980s.

Churchill and Suprenant (1982) opinioned that service quality is an attitude.

Gronroos (1982) and Lewis and Booms (1983) identified the significance of

processes and outcomes in defining service quality. Holbrook and Corfman

(1985) concluded perceived service quality as a global value judgment. To

33

compete successfully, a firm must understand the perceptions of consumers

about quality. For achieving consumer satisfaction, expected service and

perceived service should match each other. An exploration of the literature on

service quality revealed the existence of two schools of thought namely

Nordic school of thought based on Gronroos’s (1982) and North American

school of thought based on Parasuraman et al (1984) GAP model. Later,

Cronin and Taylor (1992) questioned the conceptual basis of the SERVQUAL

and found it as confusing and proposed model that accounted only

performance component discarding the expectation component used in

SERVQUAL.

Gronroos (1982) defined the concept of perceived service quality,

as ‘the outcome of an evaluation process, where the consumer compares his

expectations with the service he perceived he has received’. Gronroos (1984),

based his definition on technical quality (the outcome or ‘what’) and

functional quality (the process or ‘how’). The functional quality represents

how the service is delivered; in other words it focuses on the interaction that

takes place during the service delivery. Whereas, the technical quality refers

to what the customer receives in the service encounter. Also corporate image

is introduced as a high order moderating dimension for perceived and

expected quality as illustrated in Figure 2.2.

Figure 2.2 Gronroos model of Service quality

34

Parasuraman et al (1984), proposed that Service quality is a

function of difference between expectations and performance with reference

to quality dimensions as experienced by the Customer. They developed a

service quality model (Figure 2.3) based on gap analysis. The various gaps

visualized in the model are:

Gap 1: Market information, the gap between customer expectations and

what the service provider thinks it is providing;

Gap 2: Service standards, the gap between what the service provider thinks

it is providing and the service provider’s standards;

Gap 3: Service performance, the gap between the service provider’s

standards and actual performance;

Gap 4: Internal communications, the gap between what the service

provider is marketing and what is being delivered; and

Gap 5: Service quality, the gap between the customers’ expectations and

their perception about the service delivery.

Figure 2.3 GAP Model Source: Parasuraman et al.(1984)

35

Parasuraman et al (1984) developed SERQUAL, a scale which asks

customers what they expect from excellent companies in any service sector

and their perception towards the level of service delivered by a specific

company in that sector. The methodology behind the development of the scale

was by capturing the agreement of customers on 22 indicators divided along

five dimensions that are capable of capturing the domain of service quality.

The same indicators were used to capture scores on expectation and

perceptions. The difference in expectation (E) and perception (P) scores gives

the measure of service quality (SQ). If perceived performance is higher than

the expectations, then it indicates high service quality, and the reverse

indicates poor quality. The procedure has got wide acceptance and many

researchers adopted the procedure to assess service quality in different

contexts such as retailing (Barnes and Vidgen 2002), health care

(Carman 1990; Yang et al 2003; Kilbourne et al 2005), banking

(Zhou et al 2002; Al-Hawari et al 2005), education (Ruby 1998; Tan and Kek

2004), information systems (Kettinger et al 1995; Jiang et al 2002), library

(Edwards and Browne 1995; Nitecki 1996; Cook and Thompson 2001;

Landrum and Prybutok 2004) and other areas of service across many

countries. The SERVQUAL was modified in multiple ways as illustrated in

table 2-1.However the classic format containing five dimensions with 22

indicators as illustrated in Table 2.2 is considered popular.

36

Table 2.1. SERVQUAL –Stages in evolution of SERVQUAL

SERVQUAL (Year) Features1985 -10 dimensions such as Reliability,

Responsiveness, Competence, Access, Courtesy, Communication, Credibility, Security, Knowing customer needs, Tangibles

1988 -Reduced to 5 dimensions like Reliability, Assurance, Tangibles, Empathy, Responsiveness, -22 item scale with 2 parts each for expectation and perceptions -sed 7 point scale

1991 -Dropped negative worded - Dropped the normative ‘should’ and replaced it with ‘would’ - Allocated 100 points as weights among the 5 dimensions on a 10 point scale

1993 -Expectation component interpreted in terms of ZOT

1994 -Reformatted 22 items to 21 items on a -9 point Likert-type scale - Included use of ‘no opinion’ - Perception next to desired and adequate separately

1996 -Developed a conceptual framework of both financial and behavioral consequences of service quality

2005 -Modified SERVQUAL to measure e-service quality - Identified 4 dimensions of e-service quality: Efficiency, Fulfillment, System availability, Privacy -Identified 3 dimensions for service recovery: Responsiveness, Compensation, Contact

37

Some major objections relate to use of disconfirmation theory

(Perception minus – Expectations gap scores) (Cronin and Taylor 1992; Teas,

1993, 1994; Buttle 1996), predictive power of the instrument (Babakus and

Boller 1992, Van Dyke et al 1999),validity of the five-dimension structure,

(Dabholkar et al 2000; Wilkins et al 2007; Ladhari 2009;

Saurina Canals 1997; Buttle 1996 and Robbinson 1999) and length of the

questionnaire (Hernon 2002). Subsequently some researchers recommend that

a performance-only measure (or direct-effect model) is superior to the Gap

score (Lee et al 2000; Cronin and Talyor 1992; Roszkowskit et al 2005; Caro

and Gracia 2007; Wilkins et al 2007) because it is more reliable and explains

more variance than the disconfirmation model. Page and Spreng (2002) have

further argued that performance is a much stronger indicator of service

quality than expectations. A new scale called SERVPERF, which measures

only service quality on the basis of perception alone was developed by Cronin

and Taylor (1992). The SERVPERF scale reduced the number of items to be

measured by 50% and is considered more efficient (Jain and Gupta 2004).

Even though various criticisms as cited above were coined against

SERVQUAL, the multi-dimensional structure was accepted by majority of

researchers and the structure and contents of the instrument also gathered

much popularity. However the selection of appropriate dimensions that are

relevant to the context of the study emerged as a new area for research. Table

2-3 below was presented to provide a general idea about various dimensions

considered in service quality measurement. In this study, service quality

dimension were identified according to currents trends based on

recommendations of the expert panel. The emerging trends related to

E-banking were also considered during the literature review to identify

possible dimensions to explain the domain of current banking scenario in

India.

38

Table 2.2 SERVQUAL dimensions and indicators

With the advent of technology influence service delivery

possibilities in the banking sector, the relevance of machine related, system

related and connectivity related dimensions also gathered attention in service

quality measurement. Zeithaml et al (2001) identified 11 dimensions for

measuring service quality in the online context after a series of focus group

interviews. These were access, ease of navigation, efficiency, flexibility,

39

reliability, personalization, security, responsiveness, assurance/trust, site

aesthetics, and price knowledge.The service quality perceptions in E-banking

have to be evaluated purely system oriented as possibility of direct interaction

with human involvement is limited. In such a context, service quality will be

decided by system quality, network quality and information quality as

suggested by the expert panel when consulted during the preliminary study.

Therefore this study considered conventional dimensions which are

contemporary as well as technical and system related dimensions which are

more representative of current service delivery options.

Table 2.3 Dimensions used in some important studies

Author Year Context Dimensions Gronroos 1982 bank, insurance,

restaurants, shipping,airline companies,cleaning andmaintenance

technical quality, functional quality & corporate image (3)

Lehthinen and Lehthinen

1982 general physical quality, corporate quality and interactive quality(3)

Parasuraman et al 1984 telephoneco., securitiesbrokerage, insurance co., banks and repair and maintenance

Reliability, responsiveness, tangibility, courtesy, access, credibility, communication, competence, understanding & security (10)

Parasuraman et al 1988 general Reliability, responsiveness, tangibles, assurance & empathy (5)

Gronroos 1990 general attitude and behavior, skills and professionalism, accessibility and flexibility, reliability and trustworthiness, recovery; reputation and credibility (6)

Avkiran 1994 Australian Banking Staff Conduct, Credibility, Communication and Access to Teller Services(4)

Rust and Oliver 1994 general Service product, service delivery and service environment(3)

Johnston 1995 UK banking context Aesthetic, availability, attentiveness, access, care, cleanliness, comfort, commitment, communication, competence, courtesy, friendliness, flexibility, functionality, integrity; reliability, responsiveness &security(18)

Oppewal and Vriens 2000 UK banking accessibility,competence, accuracy and friendliness, and tangibles (4)

40

Table 2.3 (Continued)

Bahia and Nantel 2000 Canada banking Effectiveness and assurance, access, price, tangibles, service portfolio and reliability (6)

Siu and Cheung 2001 Retail format personal interaction; policy; physical appearance; promise; problem solving; and convenience(6)

Othman& Owen 2001 Kuwait banking Compliance with Islamic law, reliability, responsiveness, tangibles, assurance & empathy (6)

Aldlaigan and Buttle 2002 UK banking Service system quality, behavioral service quality, machine service quality and service transactional accuracy (4)

Sureshchander et al 2002 Banking Core service or service product, Human element of service delivery, Systematization of service delivery - non-human element; Servicscapes and Social responsibility(5)

Gounaris et al 2003 Greek Banking employee competence, reliability, the innovativeness of the bank’s products, pricing (value for money), physical evidence and convenience(5)

Karatepe et al 2005 Northern Cyprus banking

service environment, interaction quality, empathy and reliability (4)

Gounaris 2005 B2B context Potential quality, hard processing quality, soft processing quality and output quality (4)

Al-Hawari and Ward 2006 Australia banking ATM, Telephone banking, internet banking, price, core product, customer service and financial performance (8)

Ibrahim et al 2006 UK banking sector provision of convenient/accurate electronic banking operations, the accessibility and reliability of service provision, good queue management, service personalization, the provision of friendly and responsive customer service and the provision of targeted customer service (5)

Nam 2008 US and South Korea Banking

Trustworthiness, functionality, appearance and helpful employees(4)

Guo et al 2008 China Banking Reliability, technology, communication, technical quality and human capital(5)

Kumar et al 2009 Malaysian Banking Tangibility, reliability, convenience and competence (4)

Ravichndran et al 2010 Indian banking Reliability, responsiveness, tangibles, assurance , empathy and price (6)

41

The structure of service quality was conceptualized differently by

researchers. Dabholkar et al (1996) suggested that service quality dimensions

should be viewed as higher-order constructs that have various sub-

dimensions. They identified and tested a hierarchical conceptualization of

retail service quality that proposes three levels: i) customers overall

perception of service quality; ii) primary service quality dimensions and iii)

sub-dimensions of service quality. Philip and Hazlett (1997), proposed a

model that takes the form of a hierarchical structure – based on three main

classes of attributes – pivotal, core and peripheral. According to the model

every service has overlapping of above attributes, where majority of the

dimensions and concepts used to define service quality are contained. The

pivotal attributes, located at the core, are considered collectively to be the

single most determining influence on consumer decision in selecting a

particular organization and exert the greatest influence on the satisfaction

levels. Core attributes, centered on the pivotal attributes, can best be

described as the amalgamation of the people, processes and the service

organizational structure through which consumers must interact and/or

negotiate so that they can achieve/receive the pivotal attribute. The peripheral

attributes which can be defined as the “incidental extras” or frills designed to

add” roundness” to the service encounter and make the whole experience for

the consumer a complete delight. When a consumer makes an evaluation of

any service encounter, he is satisfied if the pivotal attributes are achieved, but

as the service is used more frequently the core and peripheral attributes may

began to gain importance

Brady and Cronin (2001), proposed the hierarchical service quality

model (HSQM) where service quality was conceptualized as a multilevel

construct consisting of three primary dimensions: interaction quality, physical

environment quality, and outcome quality. Each of these three broad

dimensions was composed of various lower-level dimensions. The interaction

42

quality dimension was comprised of attitude, behavior, and expertise of the

service provider. The physical environment quality dimension comprised of

ambient conditions, design, and social factors. The outcome quality

dimension comprised of waiting time, tangibles, and valence (Figure 2-4).

The multilevel-hierarchical structure for service quality proposed by Brady

and Cronin has also been empirically tested in travel services (Ho 2007); B2B

services (Gounaris 2005); electronic services (Fassnacht and Koese 2006) and

hotel services (Wilkins et al 2007).

Figure 2.4 Hierarchical Model for Service Quality

Some researchers approached the concept of service quality in a

different manner and contributed substantially to the body of knowledge. Few

such studies are cited below.

Mukjerjee and Nath (2005) conducted a study to empirically

compare alternate approaches like TOPSIS from decision sciences, and Loss

function from operations research and engineering with SERVQUAL for

measuring service quality. The empirical evidence was provided by large

sample consumer data on the service quality for leading Indian commercial

banks. Findings revealed that the rankings obtained from different methods

43

are statistically in agreement, suggesting that the alternative approaches can

provide equally good measurement of service quality.

Ugur Yavas and Martin Benkenstein (2007) conducted a study to

determine the underlying configurations of service quality perceptions

between Turkish and German bank customers by ascertaining the extent of

cross-cultural congruence and found that underlying configurations of service

quality items decompose into three factors for both groups and the extent of

congruence between the two groups were strong.

Dash et al (2009), conducted a study to find the effect of power

distance and individualism on service quality expectations in banking among

Indian and Canadian banking customers. The results showed that the

importance of various SERVQUAL dimensions was related to Hofstede's

power distance and individualism cultural dimensions both at the individual

and national levels. Also consumers low on power distance expects highly

responsive and reliable service. High power distance customers attached

higher importance to tangible service attributes. Consumers high on

individualism expect lower empathy and assurance from service providers.

Furthermore, Indian consumers attached higher importance to tangible

attributes, whereas Canadian consumers found service reliability more

important. However, differences in overall service quality expectations were

not significantly different across the two countries.

Tigineh Mersha and Veena Adlakha (1992), identified the attributes

for good and poor quality of five selected types of services such as physician

service, retail banking, auto maintenance, college/university, and fast food.

The findings indicated that consumers had well-conceived ideas about service

quality, and that certain quality attributes were emerged important for most

types of services. This study found that some attributes seem to have effects

44

similar to Herzberg's hygiene factors, i.e. the absence of certain attributes may

lead consumers to perceive service quality as poor. However, the presence of

these attributes may not substantially improve the perceived quality of the

service. Also suggested that most customers would be willing to trade some

convenience for a price break, and that the behaviour, skill level and

performance of service employees are key determinants of perceived quality

of services.

Nitin Seth et al (2004),conducted a study with the objective of

critically appraising various service quality models and revealed that the

service quality outcome and measurement were dependent on type of service

setting, situation, time and need factors. In addition to this even the

customer’s expectations towards particular services were also found changing

with respect to factors like time, increase in the number of encounters with a

particular service, competitive environment, etc.

Malhotra et al (1994), identified that economic and socio-cultural

differences will affect customer perceptions of service quality. Service quality

dimensions of courtesy, credibility, and communication were related to

cultural dimensions of individualism/collectivism and power distance.

Similarly service quality dimensions such as reliability, access and the

understanding of the customer were related to factors of economic

development such as affluence, competition, education, infrastructure, and

technology.

According to Johnson (1996), non-personal-contact (e.g. bank

statements) dimensions are expected to be less related to personal-contact

(teller service) dimensions. Seeking information, service training and support,

service rewards and recognition were the service climate themes that were

most predictive of specific facets of customer satisfaction and overall

45

satisfaction with service. These three dimensions were probably highly

related because they all had an informational component. It was expected that

all service climate dimensions would be related to customer service

satisfaction. This was generally supported, as all dimensions were

significantly related to at least some facets of customer satisfaction except

bank statements. It was also expected that the customer dimensions of bank

statements and convenience would tend to be less related to service climate

dimensions, because these are non-personal-contact facets of customer

satisfaction.

2.3 SERVICE QUALITY IN BANKING SECTOR

Extensive research has been undergone to understand service

quality perceptions in the banking sector. Many of such studies used

SERVQUAL (Angur et al 1999; Arasli et al 2005; Lam 2002; Zhou 2004;

Nam 2008; Ravichandran et al 2010) whereas application of alternative

measures (Bahia and Nantel 2000; Aldlaigan and Buttle 2002; Jabnoun and

Al-Tamimi 2003; Karapte et al 2005; Guo et al 2008) also cherish the

literature.

Ravichandran et al (2010),conducted a study in India banking

context to identify the Influence of Service Quality on Customer Satisfaction

using SERVQUAL Model and found out that Customers are satisfied with the

quality of banks’ services ( all the 5 dimensions) but in varying degrees. It

was further identified that with regards to overall satisfaction of banks

services, responsiveness was the only significant dimension. Three

dimensions such as tangibles, reliability and a combination of empathy and

responsiveness were identified as important in Cyprus banking context

(Arasli et al 2005) whereas reliability and assurance decided service quality

of US customers (Zhou 2004).The Chinese customers offered two sub

46

dimensions such as “understanding of needs” and “convenient operating

hours” for the empathy dimension while identifying all other dimensions

significant (Lam 2002).An earlier study conducted in the Indian Banking

context identified responsiveness and reliability seem to be the most

important dimensions followed by the empathy and tangible dimensions;

whereas, assurance appears to be the least important dimension

(Angur et al1999)

Jabnoun and Al-Tamimi (2003) examined perceived services

quality in commercial banks in the United Arab Emirates and emphasized the

importance of service quality to maintain market share, the study identified

human skills as the most significant dimension in service quality. Guo et al

(2008) conducted a study to measure Service Quality in the Chinese

Corporate Banking and concluded that service quality contained two higher-

order constructs (Functional Quality and technical quality) and four lower-

order dimensions (reliability, human capital, technology and communication).

Aldlaigan and Buttle (2002), based on the technical and functional

service quality model proposed by Gronroos (1984), developed a scale to

measure service quality perceptions of bank customers. Their study resulted

in SYSTRA-SQ, which consisted of service system quality, behavioral

service quality, service transactional accuracy, and machine service quality. A

21-item scale comprising four dimensions: service system quality,

behavioural service quality, service transactional accuracy, and machine

service quality was developed and validated. It was found that that customer

evaluates SQ at two levels: organizational and transactional. The parsimony,

reliability and validity of the scale suggested high utility of this scale to the

banking industry.

47

Bahia and Nantel (2000) developed a new measurement called

Bank Service Quality (BSQ) for perceived service quality in Retail Banking.

This scale includes 31 items classified across six dimensions - effectiveness

and assurance, access, price, tangibles, range of services offered and accuracy

and reliability. They argued that the dimensions of BSQ are more reliable

than the dimensions of SERVQUAL and are fit for all retail banking of the

world.

Tsoukatos and Mastrojianni (2010) developed a 27-item

BANQUAL-R scale consists of 12 SERVQUAL, seven BSQ, two common in

SERVQUAL and BSQ and six items specific to the context of Greece

banking. Avkiran (1999) developed an instrument BANKSEV which had

identified the following four discriminating factors of service quality in the

banking sector.

Staff Conduct: Responsiveness, civilised conduct and

presentation of branch staff that will project a professional

image to the customers.

Credibility: maintaining bank staff-customer trust by rectifying

mistakes and keeping customers informed.

Communication: Fulfilling banking needs to customers by

successfully communicating financial advice and serving

notices timely.

Access to Teller Services: The adequacy of number of branch

staff

48

2.4 E- BANKING SERVICE QUALITY

The emergence of internet and its widespread popularity resulted in

the introduction of virtual market place instead of traditional physical ones.

The banks also employed the Internet as an alternative service delivery

channel. It has been pointed out that the introduction of e-banking services

could offer both bankers and customers diverse benefits (Broderick and

Vachirapornpuk 2002). The interaction between the customer, and the bank’s

Web site or employees over the Internet enabled the bank to lower its

operating and fixed costs by reducing the number of employees, branch

offices, and other physical facilities while maintaining a high quality level of

customer service. These cost benefits could make favorable conditions for the

bank to provide customer services at lower fees. E-service quality can be

defined as overall consumer evaluations and opinions about the excellence of

e-service delivery in the virtual marketplace (Santos 2003). Colier and

Bienstock (2006) describe e-service quality as user’s perceptions of the

outcome of the service delivery along with service recovery perceptions, if

service failures happened. It was widely accepted that certain dimensions

relating to technical aspects and website characteristics need to be

incorporated to fully capture the service quality perception in e-context

(Zeithaml 2002).The following Table 2.4 narrates few of the prominent

dimensions considered by researcher’s to measure e-service quality applicable

to multiple contexts.

49

Table 2.4 E-Service quality Dimensions

Author Year Dimensions Zeithaml et al. 2001 access, ease of navigation, efficiency, flexibility,

reliability, personalization, security/privacy, responsiveness, trust/assurance, site aesthetics, and price knowledge(11)

Broderick and Vachirapornpuk

2002 Expectations of customer, the image and reputation of the service provider, aspects of the service setting, service encounter, and customer participation (5)

Wolfinbarger and Gilly

2002 customer service, privacy/security, reliability, and Web site design (4)

Madu and Madu 2002 performance, features, structure, aesthetics, reliability, storage capacity, serviceability, security and system integrity, trust, responsiveness, product differentiation and customization, web store policies, reputation, assurance, and empathy (15)

Zeithaml et al 2002 efficiency, reliability, fulfillment, privacy, responsiveness, compensation, and contact(7)

Santos 2003 Incubative dimensions (web site design, easy access, understanding and attractions of a web site) and active dimensions (good support, fast speed, and attentive maintenance )(6)

Siu and Mou 2005 credibility, efficiency, security, and problem handling(4)

Parasuraman et al 2005 e-core service quality dimensions (efficiency, fulfillment, system availability and privacy) and e-recovery service quality dimensions ( responsiveness, compensation and contact

Pikkarainen et al 2006 content, ease of use and accuracy(3)Maenpaa 2006 Convenience, security, status, auxiliary features,

personal finances, investment, and explorationpotential (7).

Nusair and Kandampully

2008 Navigability, playfulness, information quality, trust, personalization, and responsiveness (6).

Herington and Weaven

2008 personal needs, site organization, user-friendliness and efficiency (4)

50

A web site that acts as an interface between customer and service

provider is an essential component that can bring more quality perceptions in

e- context. Hence many researchers have attempted to identify dimensions for

measuring web-site quality. Yoo and Donthu (2001) proposed a scale called

SITEQUAL for measuring web site quality based on four factors namely ease

of use, aesthetic design, processing speed, and security. Cox and Dale (2001)

claimed that traditional service quality dimensions such as competence,

comfort, cleanliness and courtesy were not suitable for online environment,

whereas dimensions such as accessibility, communication, credibility,

understanding, appearance, and availability were very significant for online

environment. A scale called WebQual has been developed by Loiacono et al

(2002) to evaluate web site quality, which is composed of 12 dimensions:

informational fit-to-task, tailored communications, trust, response time, ease

of understanding, intuitive operations, visual appeal, innovativeness,

emotional appeal, consistent image, online completeness, and relative

advantage. Barnes and Vidgen (2002) developed WebQual scale for

measuring web site quality based on three factors: usability, information

quality, and service interaction quality.

The hierarchical structure of e-service quality was considered idea

by Collier and Bienstock (2006) in his study on e-retailing. The study

identified three dimensions: process quality, outcome quality, and recovery

quality. Each of these dimensions has sub dimensions such as functionality,

information accuracy, design, privacy, and ease of use to determine process

quality. Whereas the outcome quality is determined by order accuracy, order

condition, and timeliness; and recovery quality is determined by interactive

fairness, procedural fairness, and outcome fairness. Table 2.5 lists down

certain dimensions considered by researchers as relevant to e-banking

context.

51

Table 2.5 E-banking Dimensions

Dimension Author

Website designs/ Web site appears/ Aesthetic design

Jun and Cai (2001), Kim and Stoel (2004), Kim et al (2009)

Reliability Madu and Madu(2002), Yang and Jun (2002)

Ease of use Yang et al (2003), Sukasame (2004), Yang et al (2004), Sohn and Tadisina (2008), Obi (2009)

Responsiveness Zeithaml et al (2002), Madu and Madu (2002)

Communication Sohn andTadisina (2008), Surjadaja et al(2003), Kim et al (2009)

Information Jun and Cai (2001), Yang (2001), Zeithaml et al (2002)

Courtesy Jun and Cai (2001), Yang et al (2003)

Customization Sohn andTadisina (2008), Surjadaja et al(2003), Kim et al (2009)

2.5 CUSTOMER SATISFACTION

Zeithaml et al (2009), defined Customer satisfaction as “the

customer’s evaluation of a product or service in terms of whether that product

or service has met the customer needs and expectations”. Gustafsson (2005)

defined Customer satisfaction as a “customer’s overall evaluation of the

performance of an offering to date”. Kotler (2000) defined satisfaction as a

“person’s feeling of pleasure or disappointment resulting from comparing a

product’s perceived performance/outcome from his/her expectations”.

Yi (1990) defined customer satisfaction as “collective outcome of perception,

evaluation and psychological reaction to consumption-experience with a

product or service”. Zairi (1996), mentioned the importance of asking

52

customers about their needs and expectations and collecting feedback

regularly about the level of service they have received in order to serve them

better. Satisfaction is a function of perceived performance and expectations.

If the performance falls short of expectations, the customer will be

dissatisfied. If the performance matches the expectations, the customer will

be satisfied. If the performance exceeds expectations, the customer is highly

satisfied or delighted. Thus satisfaction formed as a result of post-

consumption evaluative judgment (Westbrook and Oliver 1991).

Most studies on satisfaction were based on the theory that the

confirmation or disconfirmation of pre-consumption product standards

essentially determines satisfaction. So, in a service context, it was argued that

customers have certain service standards in mind prior to consumption (their

expectations) which are observed and compared with their standards during

service encounter and then satisfaction judgments are formed. The resulting

judgment is labeled negative disconfirmation if the service is worse than

expected, which results in customer dissatisfaction and may lead to negative

word of mouth publicity and/or customer defection. In contrast, a positive

disconfirmation exists if service is better than expected, thereby resulting in

customer satisfaction, positive word of mouth publicity and customer

retention (Hoffman and Bateson 1997). A simple confirmation occurs if

service turns to be as expected. Positive disconfirmation along with pleasure

and an element of surprise develops customer delight.

Most of the retail banks set their strategies towards increasing satisfaction and loyalty of customers through the quality of service. Devlin, (2001), pointed out that “customers perceive very little difference in the services offered by retail banks and any new offering is quickly matched by competitors.” Ability of SERVQUAL dimensions to develop customer satisfaction is identified as different in prior studies. Zaim et al (2010), observed that tangibility, reliability and empathy are important factor for

53

customer satisfaction, whereas Mengi (2009), founded that responsiveness and assurance are important factors. Kumar et al (2010), and Lai (2004), found that assurance, empathy and tangibles are the important factors, and on the other hand, Baumann et al (2007), found that tangibles are not related to customer satisfaction and Ahmed et al (2010), find out that empathy is negatively related to customer satisfaction. Kirti and Dutta (2009) explored the gulf between customer expectations and perceptions of service quality factors throughout public, private and foreign banks in India based on the SERVEQUEL model and found that tangibles, assurance, empathy and reliability dimensions explain customer satisfaction in Indian banks

Researchers have identified various determinants of customer satisfaction in the retail banking sector. Arasli et al (2005), pointed out that reliability dimension of SERVQUAL has the highest impact on customer satisfaction in Greek Cypriot banking industry. Chaniotakis and Lymperopoulos (2009), observed that reliability was not related to customer satisfaction. According to Levesque and McDougall (1996), competitive interest rate was one of the important determinants of customer satisfaction in retail banking sector. They also found out that a good “employee customer” relationship can increase the satisfaction level and pointed out that problem-recovery is important to maintain the customer satisfaction. They concluded that competitiveness and convenience of the banks are the two important determinants of customer satisfaction. On the other hand, Jamal and Naser(2003), found that convenience and competitiveness are not the critical factors for all gender, age and income groups. Johnston (1995) opined that attentiveness, responsiveness, care, and friendliness are the main source of satisfaction in banking services, and integrity, reliability, responsiveness, availability, and functionality are the main source of dissatisfaction. Yang and Fang (2004) identified that dimensions of responsiveness, competence, service reliability, and ease of use as key determinants of both satisfaction and dissatisfaction in online banking context.

54

In marketing literature, Service Quality and Customer Satisfaction have been conceptualized as a distinct, but closely related constructs. There is a positive relationship between the two constructs (Beerli et al 2004). Some researchers argued that service quality is the antecedent of customer satisfaction, while others argued the opposite relationship. Jamal and Naser(2003), stated that service quality is the antecedent of customer satisfaction. Figure 2.4a explains the summary of debate by various researchers regarding the Causal Relationships between Satisfaction and Service Quality.

Figure 2.4a Summary of the Causal Relationships between Satisfaction and Service Quality

Source: Gonzalez et al (2007)

The most popular method to measure customer satisfaction was by way of surveys that capture customer perceptions on selected attributes that are relevant to conclude about satisfaction level of customers. The Customer satisfaction Index is considered as the most popular method that directly captures customer satisfaction level. The CSI model consists of a number of latent factors, each of which is operationalised by multiple indicators. Customer satisfaction can be defined as an overall evaluation of a firm’s post-

55

purchase performance or utilization of a service. The antecedent of overall customer satisfaction considered in the framework includes expectations, image, perceived quality, value, customer loyalty and customer complaints(Adela Poliakova 2010). The American Customer Satisfaction Index (ACSI), developed in the mid-1990s, has provided a basic framework for many other index models created elsewhere in the world (Fornell et al 1996). Thecustomer satisfaction Index in simple words is a weighted average score of all attributes that are believed to contribute to customer satisfaction on a scale from 1 to 10. Since different attributes can contribute differently to the overall customer satisfaction, the individual attributes are awarded proper weights. The following Table 2.6 list down various studies based on customer satisfaction index

Table 2.6 Prior studies on customer satisfaction index models

Model Author Dimensions American Customer Satisfaction Index(ACSI)

Fornell et al 1996

Perceived quality, customer expectations, perceived value, overall customer satisfaction, customer complaints, customer loyalty

European Customer Satisfaction Index(ECSI)

O’Loughlin and Coenders

1998

Image, customer expectations, perceived hardware quality/perceived software quality, perceived value, customer satisfaction, customer loyalty

ECSI for Portal Services

O’Loughlin and Coenders

2004

Image, customer expectations, product hardware quality, customer service human ware quality, perceived value, customer satisfaction, customer loyalty

Swiss CSI Bruhn and Grund 2000

Customer satisfaction, customer dialogue, customer loyalty

Canadian CSI for Mobile Services

Turel and Serenko 2006

Perceived quality, customer expectations, perceived value, customer satisfaction, customer complaints, price tolerance, repurchase likelihood

African Banking KPMG 2013 Convenience, customer care, transactions, methods &systems, pricing and products and services

56

A model of customer satisfaction was introduced by Kano et al

(1984), distinguishing between three types of product requirements which

influence customer satisfaction in different ways was accepted by various

scholars as an approach to measure satisfaction in both products and services.

KANO model defines three types of customer needs: The basic needs,

expected needs, excited needs. Basic needs are fundamental functions of

products in the view of customers. They are basic requirements to the

product. If the product doesn’t satisfy these basic needs, customers would be

extremely dissatisfied; on the contrary, when the product fully satisfies the

basic needs, consumers will not show a particular satisfaction either as they

think it’s the fundamental function of products. The more Expected needs are

achieved in the product, the more satisfied customers are; while the product

does not meet these requirements, customers will also be dissatisfied. Excited

needs are referred to unexpected product features. If the product does not

provide this type of demand, customers will not be dissatisfied, because they

often do not think about these requirements, on the contrary, when the

products provide such demands; the customer would be very satisfied with

the products.

Kano has developed a two-dimensional questionnaire positive

(functional) and negative (disfunctional) version of the attribute that evaluates

satisfaction. The responses were collected on a five point scale containing

options “like, must-be, neutral, live with and dislike”. The combinations

scores of responses are classified into six categories and are evaluated as per

the tables developed for the purpose of the model. The six categories were

Attractive (A): An Attractive attribute leads to a better

satisfaction, whereas it is not expected to be in the product.

One-dimensional (O): A One-dimensional attribute

fulfillment helps enhance the satisfaction and vice versa.

57

Must-be(M) : A Must-be attribute absence produces absolute

dissatisfaction and its presence does not increase satisfaction

Indifferent (I): An Indifferent attribute, that result neither in

satisfaction nor dissatisfaction, whether fulfilled or not.

Reverse (R): A Reverse attribute presence causes

dissatisfaction and its absence causes satisfaction.

Questionable (Q): contradictory responses

All possible combinations of customer answers and the

corresponding classification of attribute are evaluated using the Table 2.7

below. Two scores between 0 and 1 are calculated after the classification

based on the formulae to evaluate the satisfaction on various attributes

considered.

Better values close to 1 suggests satisfying attributes and worst

values close to1 indicates that the attributes causes dissatisfaction.

Table 2.7 Kano evaluation

58

This study has attempted to explore and measure customer

satisfaction in a different perspective as elaborated in the theoretical frame

work. The outcomes of customer satisfaction are reflected in various

behavioral intentions displayed by the customer. The behavioral intentions

can be favorable or unfavorable which in turn can give rise to a “remain”

behavior or a “defect” behavior. Dimensions of “loyalty” and “pay more”

describe a favorable behavior whereas “switch” represents an unfavorable

behavior. External response and internal response can be favorable or

unfavorable depending upon the level of satisfaction of the customer. Nuri

Calik and Figen Balta (2006), identified “Loyalty” as a major behavioral

intention, believed to be resulting from customer satisfaction. To have

favorable behavioral intentions the need to satisfy the customer was found

essential. Retaining satisfied customers lead to word of mouth

recommendations to a new customer. The next section attempts to explore

research undertaken to understand the scope of behavioral intentions in the

banking context.

2.6 BEHAVIORAL INTENTIONS

Behavioral intentions are assumed to be the immediate antecedent

of a specific behavior by the customer. Intentions are explicit decisions to act

in a certain way, and they concentrate on a person’s motivation towards a

goal in terms of direction and intensity (Sheeran 2002). Triandis (1980)

defined Behavioral intention as "instructions that people give to themselves to

behave in a certain way". Ajzen (2002) defined Behavioral intention as “ an

indication of an individual's readiness to perform a given behavior”. Warshaw

and Davis (1985) defined behavioral intention as, “the degree to which a

person has formulated conscious plans to perform some specified future

behavior”. As immediate predictors of behavior, intentions have been at the

59

centre of research for many years, for instance in the theories of planned

behavior and reasoned action (Ajzen and Madden 1991).

According to the theory of reasoned action, behavioral intention

explains the most immediate determinant of any social behavior but only

under conditions where the behavior in question remains under volitional

control and behavioral intention remains unchanged. The theory proposes that

an individual’s intention is determined by attitudes and subjective norm

regarding the performance of the behavior. Furthermore, attitude to the

behavior accounts for beliefs about the outcomes of the behavior and

evaluations of those outcomes. Subjective norm is determined by perceived

pressure from specified significant others to carry out the behavior and

motivation to comply with the wishes of those significant others.

Ajzen and Madden (1991) extended the theory of reasoned action

to better account for behaviors which are not fully under volitional control by

introducing the theory of planned behavior. The theory of planned behavior

incorporates the original components of the reasoned action model, but also

includes a perceived behavioral control variable, defined as, “the perceived

ease or difficulty of performing the behavior”. According to Ajzen where

behaviors are not fully under volitional control, perceived behavioral control

and behavioral intention will together account for behavior, at least when

perceptions of control are accurate reflections of actual control over a

behavior. The theory of planned behavior also proposes that, along with

attitude and subjective norm, perceived behavioral control is a determinant of

behavioral intention.

Minami and Dawson (2008), suggested that importance should be

given to behavioral intentions of the customer as it contributes to profitability

of the firm. Boulding et al (1993) reported that the overall service quality

60

perception were positively related with willingness to recommend

and negatively related with switching and complaining behavior

(Kelley et al1993). Lee et al (2006), reported that customers are more likely

to spread out negative word of mouth than positive word of mouth. Empirical

evidences are available to claim that a direct positive relationship exist

between customer satisfaction and active engaging in more word-of-mouth

(Brown et al 2005; Babin et al 2005).Also researchers observed the existence

of positive association between satisfaction and repurchase intention

(Bitner et al 1990; Jones and Suh 2000; Cronin and Taylor 1992). Both

Parasuraman et al (1988) and Zeithaml et al (1996) have reported that a

positive relationship exists between perceived service quality and behavioural

intentions. In particular, positive word-of-mouth has been clearly associated

with superior service quality. Bitner (1990) also found that perceived service

quality influence behavioural intentions in terms of word-of-mouth and

repurchase intention. Similarly, Dabholkar et al (1996) reported a positive

association between perceptions of service quality and the likelihood of

recommending a product or service.

Many empirical studies have investigated the relationships among

the constructs of service quality, customer satisfaction, and behavioural

intentions in a variety of industries and cultures. These include studies of the

lodging industry in the USA (Olorunniwo et al 2006), audit industry in

Malaysia (Ismail et al 2006), banking industry in Taiwan (Lee and Hwan,

2005), recreation industry in the USA (Tian-Cole et al 2002; Lee et al 2004),

health-care industry in South Africa (Boshoff and Gray, 2004), and airline

industry in Korea (Park et al 2004).

61

Several studies show that merely satisfied customers don’t suffice

to service companies and the assumption that satisfaction comes with loyalty

is incorrect (Deming 1986; Jones and Sasser 1995). The evidence from Bain

and Company showed that around 65 to85 percent of the satisfied customers

will defect from the company (Oliver 1999). The result from automobile

industry also showed that among the 85 to 95 percent of the satisfied

customer, only 30 to 40 percent return (Oliver 1999). The relationship

between customer retention and profits has been estimated by many

researchers (Anderson and Sullivan 1993; Fomell and Wemerfelt 1987;

Reichheld and Sasser 1990) and found positive.

Zeithaml et al (1996), identified five dimensions to behavioral

intentions such as loyalty to company (loyalty), propensity to switch (switch),

willingness to pay more (pay more), external response to problem (external

response), and internal response to problem (internal response). To measure

the above dimensions an instrument with 13 items divided among 5

dimensions is used. The loyalty (with five items) and pay more (with two

items), Switch (with two items) and external response (with three items),

internal response, contains just one item are used to measure behavioral

intentions. Bloemer et al (1999) raised a number of conceptual and empirical

criticisms of the Behavioral-Intentions Battery that inter-dimensional overlap

is occurring among “external response to a problem” and “internal response

to a problem” as well as “propensity to switch” and “willingness to pay more.

Empirically, they claimed that the use of a single-item measure, “internal

response to a problem”, should be avoided.

Bloemer et al (1999) developed a scale to measure service loyalty

using the dimensions Word-of-mouth, Purchase intentions, Price sensitivity,

and Complaining behavior. Ravichandran et al (2010) used a 13 item scale

under four dimensions namely Attitudinal Loyalty, Switching propensity, Pay

62

more Sum and External and Internal response and measured behavioral

intentions in the Indian banking context.

The measurement behavioral intentions are commonly done in the

qualitative manner seeking responses from the customer regarding indicators

that are capable of extracting various intentions of the customer. The scope of

measurement with regard to behavioral intentions is to limited actions such as

loyalty, switch over, positive word of mouth and complaint nature. In this

study set of validated questions were used to measure this construct.

2.7 PREVIOUS STUDIES ON CUSTOMER EXPECTATION,

SERVICE QUALITY, CUSTOMER SATISFACTION AND

BEHAVIORAL INTENTIONS

Dabholkar et al (2000), presented a comprehensive model of

service quality which attempted to examine antecedents, consequences, and

mediators of service quality for better understanding of concepts. This model

analyzed some of the relevant factors related to service quality as components

or antecedents and the relationship of customer satisfaction with behavioral

intentions (Figure 2.5).

Figure 2.5 Antecedents and mediator model

63

Christopher White and Yi-Ting Yu (2005), conducted a study to

develop and refine the theoretical framework behind consumer satisfaction

emotions. The study suggested that satisfaction emotions were best

conceptualized as a three-dimensional construct that included positive,

negative and “bi-directional” emotions. Moreover, a positive statistically

significant relationship between “bi-directional” emotions and consumer

complaining behavior was established through correlation analysis. The study

indicated that satisfaction emotions can be conceptualized as a three-

dimensional construct of: positive emotions (hopeful, happy, positively

surprised); negative emotions (guilty, humiliated, depressed); and bi-

directional emotions (angry, disappointed). The researchers used the term “bi-

directional” to accommodate the position when customers exhibit angry and

disappointment with themselves for consuming the service, and at the same

time be angry and disappointed with the service provider for failing to satisfy

their needs.

Festus Olorunniwo et al (2006), conducted a study to investigate,

through the development of an operationalized service quality construct in the

context of a service factory, whether the typology to which a service belongs

may explain the nature of the service quality (SQ) construct and its

relationship to customer satisfaction (SAT) and behavioral intentions (BI).

The study revealed that the dominant dimensions of SQ construct in the

service factory were found to be: Tangibles, Recovery, Responsiveness, and

Knowledge. Further results indicate that, although the direct effect of SQ on

BI is significant, the indirect effect (with SAT playing a mediating role) was

stronger driver for BI in the context of the service factory.

Birgit Leisen Pollack (2009), had attempted to study the linking of

hierarchical service quality model developed by Brady and Cronin (2001),

64

to customer satisfaction and loyalty. A conceptual model was developed

where service quality was antecedent to customer satisfaction and loyalty

(Figure 2.6). The results confirmed the ability of HSQM to generate

satisfaction and loyalty.

Fomell and Wemerfelt (1987), developed the concept of offensive

effects (capturing new customers) and defensive effects (retaining customers)

for the analysis of financial impact on service quality. Determining the

offensive impact of service quality was found similar to advertising-sales

relation. Service quality's effect’s— similar to advertising's effects—was

cumulative, and therefore evidence of the link developed slowly. And, similar

to advertising, service quality, pricing, advertising, efficiency, and image

simultaneously influenced profits. Furthermore, spending on service quality

alone does not guarantee results, because strategy and execution must both be

considered. On the other hand, evaluating the defensive impact of service

quality through customer retention had impact on service quality.

However, the results suggested that the significance of various

service quality dimensions differs depending on the type of service. The

services considered for the study were Local telephone services being more

equipment-based and hairdresser/barber services being people-based. The

findings suggested that the importance (significance) of sub dimensions and

primary dimensions were service dependent. For instance, the main drivers of

interaction quality for the phone service were attitude and behavior while

attitude and expertise were important for the hairdresser/barber service.

Interaction quality, physical environment quality and outcome quality were

the primary dimensions of overall service quality for both services. Outcome

quality emerged as the most important dimension.

65

Figure 2.6 Service quality as antecedent to customer satisfaction and

loyalty

Source: Birgit Leisen Pollack (2009)

Le Blanc and Nguyen, (1988), developed a model where, Service

quality was related to the degree of customer satisfaction derived from the

service offering (Figure 2.7). Customer service was the most important factor

in explaining service quality in financial institutions. Service quality depends

on the tangible characteristics (contact personnel, the internal organization

and physical environment) associated with the service offering or on the

performance of the service provider.

66

Figure 2.7 Model developed by Le Blanc and Nguyen

Source: Le Blanc and Nguyen (1988)

Oh (1999), proposed an integral model for service quality,

customer value and customer satisfaction focusing on post purchase decision

process. The key variables such as perceptions, service quality, consumer

satisfaction, customer value and intentions to repurchase were incorporated in

the model. Finally word of mouth communication was conceptualized as a

direct, combined function of perceptions, value, and satisfaction and

repurchase intentions. The model provided evidence that customer value has a

significant role in customer’s post-purchase decision-making process and

formed an immediate antecedent to customer satisfaction and re-purchase

intentions. Results also indicated that perceived price has a negative influence

on perceived customer value and no relationship with perceived service

quality.

Ugur Yavas et al (1997), conducted a study to investigate the effect

of service quality on customer satisfaction, complaint behavior and

67

commitment. The study was conducted in Turkish banking sector.

SERVQUAL instrument covering conventional five dimensions with seven-

point scales ranging from “Much worse than I expected” to “Much better than

I expected”, was used to evaluate the performances of bank. Satisfaction was

operationalized by a five item measure. These items related to the five

dimensions of SERVQUAL. After defining each dimension, respondents

were asked to rate their level of satisfaction on that dimension on a five-point

scale ranging from “very satisfied” to “very dissatisfied”. Respondents’

complaint behaviour was operationalized by two questions relating to two

forms of complaint, private response and voice response. Specifically, on

five-point balanced scales ranging from “very likely” to “very unlikely”,

respondents were asked to indicate the likelihood with which they would

complain to a bank’s employees and other consumers when experiencing a

problem with their bank’s services. Two questions were used to

operationalize commitment (e.g. consumers’ intentions to continue to do

business with their bank).The results of the study indicated that tangibles,

responsiveness and empathy are significant predictors of consumer

satisfaction. Of those three attributes, tangibles and responsiveness are also

significant antecedents of commitment. Empathy was the only attribute with a

significant relationship with complaint behaviour.

Gour C. Saha and Theingi (2009), examined the relationships

among the constructs of service quality, satisfaction, and behavioural

intentions in passengers of three low-cost carriers (LCCs) offering airline

services in Thailand. The study revealed that the order of importance of the

dimensions of service quality tested were flight schedules, flight attendants,

tangibles and ground staff. Passenger satisfaction with these service-quality

dimensions were found to be very important in explaining behavioural

intentions. Satisfied passengers are mostly influenced by the schedule. Such

customers engage in positive word-of-mouth communication and have high

68

repurchase intentions. Dissatisfied passengers prefer to change airlines, rather

than provide feedback to the LCCs. Analysis of the relationships among

service quality, satisfaction, and behavioural intention revealed that

satisfaction plays a direct role in enhancing passengers’ intentions to become

involved in word-of-mouth activities and repurchase. However, satisfaction

had a weaker correlation with the provision of feedback; unsatisfied

customers tended to move to other airlines. Passengers who engaged in word-

of-mouth activities were found to become loyal customers subsequently.

Having satisfied passengers was thus shown to be important in developing

loyal passengers.

Huseyin Arasli et al (2005) conducted a study to measure the

service quality perceptions of Greek Cypriot bank customers and to examine

the relationship between service quality, customer satisfaction and positive

word of mouth. The study revealed that SERVQUAL scale proved to be of a

three-dimensional structure. Results revealed that the expectations of bank

customers were not met and the largest gap was obtained in the

responsiveness-empathy dimension. Reliability items had the highest effect

on customer satisfaction, which in turn had a statistically significant impact

on the positive word of mouth

Wen-Bao Lin (2009), studied the effect of the difference between

the consumer’s expectation and perception of service quality on post-

purchase behavior intentions and the effect of the consumer’s personality

traits and the enterprise’s service recovery strategy as intervening variables on

post-purchase behavior intentions of consumers. The study was conducted

among customers of various banks in Taiwan. The result indicated that the

smaller the difference between expectation and perception of service quality,

the more the consumers will show their loyalty in post-purchase behavior; the

bigger the difference between expectation and perception of service quality,

69

the more the customers will make complaints and convert to other brands.

When the difference between customer expectation and perception of service

quality increases, then the personality trait of external control orientation may

prevail over the personality trait of internal control orientation. The following

model was developed for the purpose of the study (Figure 2.8).

Figure 2.8 model developed by Wen-Bao Lin

Source: Wen-Bao Lin (2009)

The conclusions from the above study were found to have

significance in developing strategies for customer loyalty. It was observed

that when banks narrow the gap between the expected and perceived service

quality level by promotion activities and other methods, consumers show

more loyalty and other positive behavior intentions. Service providers should

motivate positive behavior of consumers by favorable deployment of various

marketing mixes. As for the influence of personality traits, consumers with

external-control character tend to manifest negative behavior when the

70

difference in expected and perceived service quality was more prominent.

However, when the difference in expected and perceived service quality was

narrow, personality traits had no significant intervening effects on behavior

intentions, but some other factors, such as goodwill and purchase habit had

greater intervening effect.

Uppal and Bishnupriya Mishra (2011) conducted a study to

analyze the widening gap between desirability and availability regarding

reliability, accuracy, confidentiality, flexibility, e-channels, high attention to

customers, low service charges and overall satisfaction of customers in three

bank groups i.e. public sector banks, Indian private sector banks and foreign

banks. The study concluded that desirability regarding reliability, accuracy,

confidentiality, flexibility, e-channels, high attention to customers, low

service charges and overall satisfaction is much higher than the availability.

This gap causes dissatisfaction among the customers and to some extent the

customers are shifting from one bank to another due this reason.

Riadh Ladhari (2009), attempted to develop and test a conceptual

model of the relationships among the constructs of “service quality”,

“emotional satisfaction”, and “behavioural intention” in the hospitality

industry. The study proposed a conceptual model (Figure 2.9) with service

quality positively related to consumers’ emotions, behavioural intentions.

Also consumers’ emotions were positively related to behavioural intentions.

Moreover, the model postulated that emotional satisfaction partially mediates

the effect of service quality on behavioural intentions. The results confirmed

that service quality exerts both direct and indirect effects (through emotional

satisfaction) on behavioural intentions. In this study, satisfaction was posited

as having both a cognitive component and an affective component. The

cognitive component (referred to as “perceived service quality”) refered to a

customer’s evaluation of a series of service attributes that constitute a service

71

performance. The emotional component (referred to as “emotional

satisfaction”) consisted of such emotions as anger, contentment, happiness,

pleasure, irritation, and disappointment.

Sang-Lin Han and Seung Baek (2004) conducted a study to

investigate the usefulness and applicability of SERVQUAL in measuring

online service quality and its relationships to customer satisfaction and

customer retention. The results of the study confirmed that service quality had

positive impact on customer satisfaction and, the level of customer

satisfaction influenced the level of customer retention and that service quality

emerged as antecedent to customer satisfaction and retention

Figure 2.9 Model developed by Riadh Ladhari

Source: Riadh Ladhari, 2009

72

A review of all the models linking critical variable in the

framework concluded that perceived quality significantly develops customer

satisfaction and leads to loyalty intentions. In most of the studies perceived

service quality is conceptualized as multi dimensional one with distinct

dimensions.

2.8 SUMMARY

The observations from the literature revealed that there exists a

recognized importance for better service quality in the banking industry,