Chapter 17 The Framework for the Implementation of Monetary Policy and the Tools of Monetary Policy.

42

chapter 17 The Framework for the Implementation of Monetary Policy and the Tools of Monetary Policy

-

Upload

archibald-ryan -

Category

Documents

-

view

227 -

download

6

Transcript of Chapter 17 The Framework for the Implementation of Monetary Policy and the Tools of Monetary Policy.

chapter 17

The Framework for the Implementation of Monetary

Policy and the Tools of Monetary Policy

Copyright © 2002 Pearson Education Canada Inc. 17- 2

Overview

So far we derived a multiplicative relation between M and MB

M = m MB

and discussed three monetary policy tools that the Bank of Canada can use to manipulate i and M. These tools are

• open market operations

• Bank of Canada advances, and

• government deposit shifting

In recent years, however, the Bank conducts policy by setting an operating band for the overnight interest rate ior and targeting ior at

the midpoint of the band. In doing so, the Bank permits M to do whatever necessary to keep ior on target.

Copyright © 2002 Pearson Education Canada Inc. 17- 3

The Role of Money

Before we go on, we have to clear up a potential confusion:

Although the Bank of Canada can control both i and M, it would be wrong to view i and M as distinct policy instruments. The reason is that a given i policy has to be supported by a given M policy. That is, the Bank influences i by adjusting M. To put it differently, i is the price of M and the Bank affects the price of M (that is, the interest rate) by controlling the quantity of money.

With this in mind, let’s discuss the institutional framework within which the Bank conducts monetary policy.

Copyright © 2002 Pearson Education Canada Inc. 17- 4

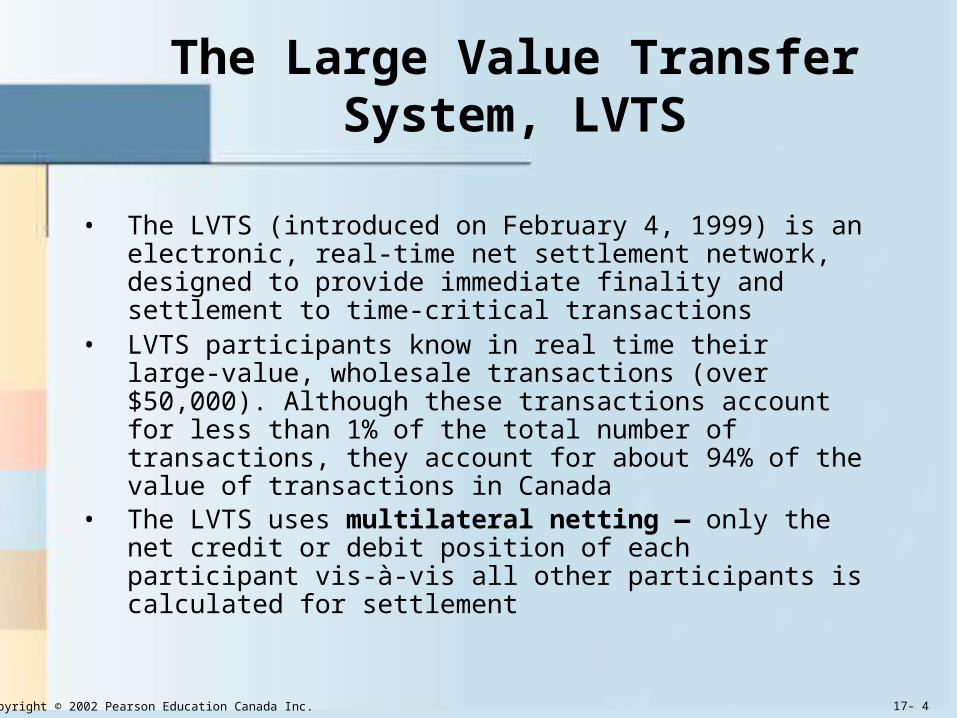

The Large Value Transfer System, LVTS

• The LVTS (introduced on February 4, 1999) is an electronic, real-time net settlement network, designed to provide immediate finality and settlement to time-critical transactions

• LVTS participants know in real time their large-value, wholesale transactions (over $50,000). Although these transactions account for less than 1% of the total number of transactions, they account for about 94% of the value of transactions in Canada

• The LVTS uses multilateral netting — only the net credit or debit position of each participant vis-à-vis all other participants is calculated for settlement

Copyright © 2002 Pearson Education Canada Inc. 17- 5

LVTS Participants

As of January 2001, in addition to the Bank of Canada, there were 13 LVTS participants — members of the CPA who participate in the LVTS and maintain a settlement account at the Bank of Canada. These are:

Big Six Alberta Treasury Branches Bank of America Canada Banque Nationale de Paris Canada La Caisse centrale Desjardins du Québec Credit Union Central of Canada HSBC Bank CanadaLaurentian Bank of Canada

Copyright © 2002 Pearson Education Canada Inc. 17- 6

Systemic Risk

The LVTS has been put in place to eliminate systemic risk. In fact, participants can make a payment only if they have

• positive settlement balances in their accounts with the Bank of Canada,

• posted collateral (such as T-bills and bonds), or

• explicit lines of credit with other LVTS participants

Copyright © 2002 Pearson Education Canada Inc. 17- 7

Real-Time Settlement Systems in Other Countries

Country Year introducedU.S. (Fedwire) 1918Sweden 1986Germany and Switzerland 1987Japan 1988Italy 1989Belgium and U.K. 1996France, Hong Kong, and Netherlands 1997

The LVTS has been put in place in order to eliminate systemic risk — the risk to the entire payments system due to the inability of one bank to fulfill its payment obligations in a timely fashion. Of, course it is not just Canada that is concerned about systemic risk.

Copyright © 2002 Pearson Education Canada Inc. 17- 8

Small Value Transactionsand the ACSS

• These are non-LVTS (paper-based) payment items, such as cheques

• These items are cleared through the Automated Clearing Settlement System (ACSS), an electronic payments system also operated by the CPA

• The ACSS aggregates interbank payments and calculates the net amounts to be transferred from and to each participant's settlement account with the Bank of Canada

• The Bank of Canada completes the settlement retroactively the next day (at midday) through the LVTS

Copyright © 2002 Pearson Education Canada Inc. 17- 9

Direct and Indirect Clearers

Direct Clearers:• The subset of LVTS participants who participate directly in the

ACSS and are known as direct clearers

Indirect Clearers:• These are the deposit-taking financial institutions that are

members of the CPA but do not have a clearing account with the Bank of Canada.

• Indirect clearers hold deposits in direct clearers in exchange for a variety of services, including cheque clearing, foreign exchange transactions, and help with securities purchases

Copyright © 2002 Pearson Education Canada Inc. 17- 10

The Operating Band of 50 Basis Points for the Overnight Interest Rate

The upper limit defines the bank rate — the rate the Bank charges LVTS participants that require an overdraft loan to cover negative settlement balances The lower limit is the rate the Bank pays to LVTS participants with positive settlement balances

Copyright © 2002 Pearson Education Canada Inc. 17- 11

The Bank’s Standing Liquidity Facilities

At the end of each day, each LVTS participant must bring its settlement balance with the Bank close to zero. The Bank therefore stands ready (we call this standing liquidity facilities) to provide or absorb liquidity with an overnight duration to participants facing unforeseen liquidity shocks.

The initiative is on the side of the LVTS participant. A participant may use the Bank’s lending facility to obtain (against eligible collateral) overnight liquidity in case of a shortage, or it may use the deposit facility to make deposits in case of excess liquidity.

Copyright © 2002 Pearson Education Canada Inc. 17- 12

The Bank’s Standing Liquidity Facilities (continued)

Although the Bank’s standing facilities provide an insurance mechanism for banks, they do so at penalty rates:

• Regarding LVTS settlements, the Bank charges ib on LVTS

collateralized advances and pays ib less 50 basis points on LVTS

positive balances.• Regarding ACSS settlements, the Bank charges ib plus 150 basis

points on ACSS collateralized advances and pays ib less 150 basis

points on ACSS positive balances.

So the rate spread at the Bank’s standing facilities for ACSS balances is 250 basis points wider than for LVTS balances.

Copyright © 2002 Pearson Education Canada Inc. 17- 13

Pre-settlement Trading

Participants can reduce the costs of either positive or negative positions by trading with each other in the LVTS pre-settlement period at the end of the day (6:00-6:30 p.m.).

In fact, the typical bid-ask spread on overnight funds in the interbank market has been less than 1/8%, much less than the 50 basis points on LVTS balances and 300 basis points on ACSS balances.

Hence, participants can adjust positions with each other in the overnight market at a better return than can be achieved at the Bank’s standing facilities.

Copyright © 2002 Pearson Education Canada Inc. 17- 14

The Market Timetable

Copyright © 2002 Pearson Education Canada Inc. 17- 15

The Bank’s Implementation of the Operating Band for ior

If ior towards the upper

limit, then the Bank will lend at ib to put a ceiling

on ior

If ior towards the lower

limit, then the Bank will accept deposits at ib less

50 basis points, to put a floor on ior

Copyright © 2002 Pearson Education Canada Inc. 17- 16

The Market for Settlement Balances and ior

Demand Curve for Settlement Balances1. At ib, the demand curve is horizontal, since the demand for negative

settlement balances will be indefinitely large

2. At ib less 50 basis points, the demand curve is also horizontal, since the demand for positive settlement balances would also be indefinitely large

3. At rates within the band, the demand for settlement balances is zero

Supply Curve for Settlement Balances1. Bank normally targets a daily level of settlement balances of zero 2. Supply curve is a vertical line at the zero quantity

Market Equilibrium1. Occurs at the intersection of the vertical supply curve and the vertical

part of the demand curve at the zero quantity

2. Equilibrium ior could be anywhere within the operating band

Copyright © 2002 Pearson Education Canada Inc. 17- 17

Supply and Demand for Settlement Balances

The equilibrium ior is

indeterminate and could be anywhere within the 50-basis-point band.

This means that the actual ior will be

somewhat different from the target ior

indicated at the start of the banking day by the Bank.

Copyright © 2002 Pearson Education Canada Inc. 17- 18

The Bank’s Current Approach to Monetary Policy

In February 1991, the Bank’s governor and the minister of finance announced a series of declining targets. The targets were 3% by the end of 1992, falling to 2% by the end of 1995, to remain within a range of 1%-3% thereafter.

The 1%-3% target range for was renewed in December 1995, in early 1998, and again in May 2001, to apply until the end of 2006.

The goal of the Bank’s current policy is to keep at the midpoint of the target range, 2%.

Copyright © 2002 Pearson Education Canada Inc. 17- 19

How the Bank Keeps From Falling Below the Target Range

The Bank expects the economy to slow down and wishes to ease monetary conditions.

It lowers the operating band for ior, thereby

encouraging banks to borrow R either from each other at ior or from the

Bank at ib

The in i and E lead to an in M, AD, and P, thereby preventing from falling below the target range.

$

euroE

Copyright © 2002 Pearson Education Canada Inc. 17- 20

How the Bank Keeps From Moving Above the Target Range

The Bank expects the economy to be exceeding its capacity in the future and wishes to slow it down.

It raises the operating band for ior in order to

prevent inflationary pressures from building.

The in i and E lead to an in M, AD, and P, thereby preventing from moving above the target range.

$

euroE

Copyright © 2002 Pearson Education Canada Inc. 17- 21

The Bank’s Influence on Long-Term Interest Rates

By changing the operating band for ior the Bank sends a signal regarding

the direction that it would like i and M to take.

•A rise in the band and thus ib is a signal that the Bank would like to see i and M in the economy. •A fall in the band is a signal that the Bank would like i and M.

However, the Bank’s direct influence on long-term rates diminishes as the time period . Long-term rates can be either higher or lower than short-term rates depending on expectations about and the level of short-term rates in the future, the relative balance between the demand for and supply of loanable funds, the level of i in the U. S., and the relative stance of monetary policies in the two countries.

Copyright © 2002 Pearson Education Canada Inc. 17- 22

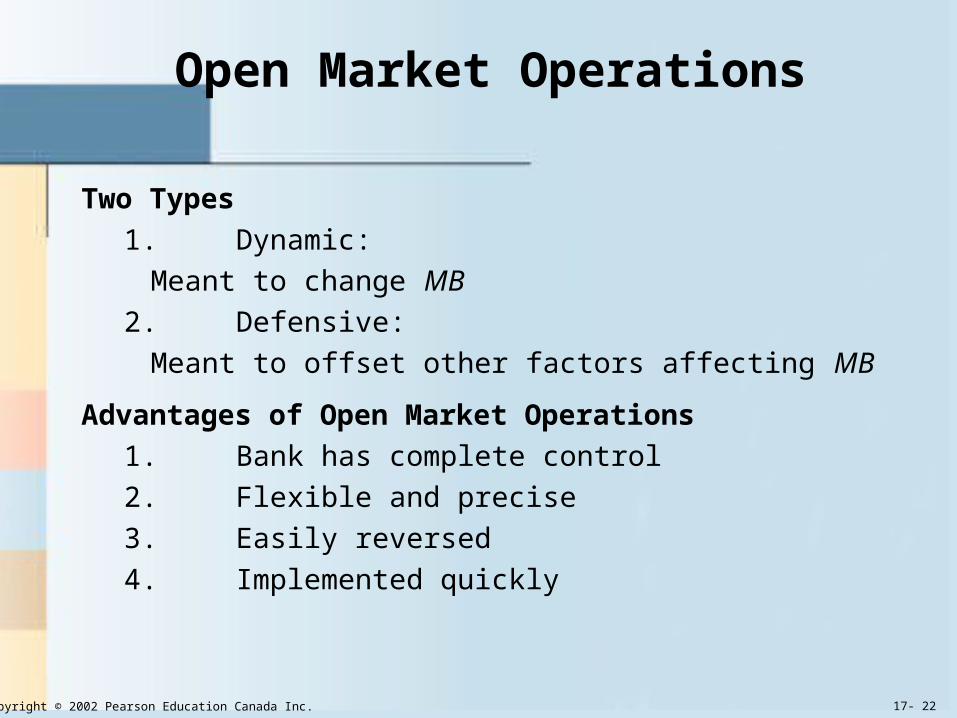

Open Market Operations

Two Types

1. Dynamic:

Meant to change MB

2. Defensive:

Meant to offset other factors affecting MB

Advantages of Open Market Operations

1. Bank has complete control

2. Flexible and precise

3. Easily reversed

4. Implemented quickly

Copyright © 2002 Pearson Education Canada Inc. 17- 23

SPRAs and SRAs

Over the years, the Bank introduced additional tools in its conduct of monetary policy.

1. In 1985, the Bank introduced repos, which in Canada are known as Special Purchase and Resale Agreements (SPRAs)

2. In 1986, the Bank introduced reverse repos, known in Canada as Sale and Repurchase Agreements (SRAs)

By 1994, the Bank stopped conducting open market operations in government of Canada T-bills and bonds and its most common operations since then have been repurchase transactions, either SPRAs of SRAs.

SPRAs and SRAs, are conducted with primary dealers (formerly known as jobbers) — the Big Six and the major investment dealers.

Copyright © 2002 Pearson Education Canada Inc. 17- 24

The Bank’s Use of SPRAs to Reinforce the Target ior

If overnight funds are traded at a rate higher than the target ior, the Bank enters into SPRAs at a price that works out to the target ior.

Bank of CanadaAssets LiabilitiesSPRAs +100 Settlement Balances +100

Direct ClearersAssets LiabilitiesSettlement Balances +100 SPRAs +100

Hence, SPRAs relieve undesired upward pressure on ior

Copyright © 2002 Pearson Education Canada Inc. 17- 25

The Bank’s Use of SRAs to Reinforce the Target ior

If overnight funds are traded at a rate below the target rate, the Bank enters into SRAs, at a price that works out to the target ior

Bank of CanadaAssets Liabilities

Settlement Balances - 100 SRAs +100

Direct ClearersAssets LiabilitiesSettlement Balances -100 SRAs +100

Hence, SRAs alleviate undesired downward pressure on ior

Copyright © 2002 Pearson Education Canada Inc. 17- 26

Bank of Canada Lending (Advances)

Two Types1. Standing Liquidity Facility, to reinforce the operating band

for ior

2. Last Resort Lending

Lender of Last Resort Function1. To prevent banking panics

CDIC fund not big enough

Examples: Canadian Commercial Bank and Northland Bank

2. To prevent nonbank financial panics

Examples: 1987 ‘Black Monday’ stock market crash

Announcement Effect1. Problem: False signals

Copyright © 2002 Pearson Education Canada Inc. 17- 27

Bank of Canada Advances to Members of the CPA

With the failure of the Canadian Commercial and Northland banks in 1985, rumours of trouble led to large deposit withdrawals from the Bank of British Columbia, Mercantile Bank, and Continental Bank.

By the time Mercantile was acquired by the National Bank of Canada, Bank of British Columbia by the Hong Kong Bank of Canada, and Continental by Lloyds Bank of Canada, the Bank of Canada lent over $5 billion.

Copyright © 2002 Pearson Education Canada Inc. 17- 28

Lending Policy

Advantages1. Lender of Last Resort Role

Disadvantages1. Confusion interpreting bank rate changes2. Fluctuations in advances cause unintended fluctuations in money supply3. Not fully controlled by Bank

Proposed Reforms1. Abolish central bank lending (Milton Friedman)

A. Eliminates fluctuations in Ms

B. However, lose lender of last resort role2. Tie bank rate to market rate

A. i – ib = constant, so fewer fluctuations of A and Ms

B. Easier administrationC. No false announcement signals

Copyright © 2002 Pearson Education Canada Inc. 17- 29

Should ib be Tied to a Market Interest Rate?

For most of the last two decades, the Bank of Canada operated under a floating bank rate regime. That is, ib was tied to a specific market interest rate. For example, from March 1980 to February 1996, ib was set each week at 25 basis points above the average 3-month T-bill rate.

In February 1996 the Bank switched to a fixed bank rate regime, with ib being the upper limit of the operating band for ior. Moreover, in December 2000, the Bank introduced a system of eight fixed dates throughout the year for announcing changes (if any) to ib, keeping the option to act between the fixed dates in extraordinary circumstances.

Figure 17-7 shows the spread between ib and ior since 1975.

Copyright © 2002 Pearson Education Canada Inc. 17- 30

Spread Between ib and ior

Copyright © 2002 Pearson Education Canada Inc. 17- 31

The U.S. Fed’s Discount Rate id

In contrast to the Bank of Canada, the U.S. Federal Reserve does not tie the discount rate to a market rate of interest, although it pursues a policy that is consistent with a floating bank rate regime.

That is, the Fed does not let id move too far from market rates because it does not want discount loans to get out of control.

Moreover, unlike the Bank, the Fed operates under a system of ten fixed dates throughout the year for announcing changes (if any) to id.

There is no correlation between the Bank of Canada’s eight pre-set announcement dates for ib changes with those of the Fed’s for id changes.

Copyright © 2002 Pearson Education Canada Inc. 17- 32

Advantages of a Flexible ib Regime

Many economists support a floating bank rate regime. They argue that by tying ib to a market interest rate (such as the 3-month T-bill rate):

• the Bank of Canada can continue to perform its role as lender of last resort.

• most fluctuations between ib and market rates are eliminated. In fact, i – ib = constant, so fewer fluctuations of A and M.

• there is easier administration of the discount window, there are no false signals about the intentions of the central bank, and hence any possible announcement effects disappear.

Copyright © 2002 Pearson Education Canada Inc. 17- 33

Advantages of a Fixed ib Regime

Other economists oppose a flexible ib because they think that keeping ib fixed when market rates change would fluctuations in market rates. For example, keeping ib fixed when market rates would A and M, possibly countering some of the in market interest rates.

The most important advantage, however, of a fixed ib regime is that the Bank of Canada can signal its intentions about future monetary policy. For example, if the Bank wants to slow the expansion of the economy by the target ior, it can amplify the announcement by also ib.

The problem is that ib changes can be subject to misinterpretation.

Copyright © 2002 Pearson Education Canada Inc. 17- 34

False Signals and Announcement Effects

If, for example, ior above the target ior, A will . In such a case, the Bank might have no intention of ib but to keep A from becoming excessive it may ib to keep it more in line with market rates.

When ib the market may interpret this as a signal that the Bank of Canada is moving to a more contractionary policy, even if this is not the case. The announcement effect may be a hindrance rather than a help.

Copyright © 2002 Pearson Education Canada Inc. 17- 35

Government Deposit Shifting

Prior to the introduction of the LVTS, the management of settlement balances (cash setting) was the main mechanism by which the Bank of Canada implemented monetary policy. In particular, using drawdowns (transfers of government deposits from the direct clearers to the Bank of Canada) and redeposits (transfers of government deposits from the Bank of Canada to the direct clearers), the Bank was essentially implementing its target band for the overnight interest rate.In the LVTS environment, however, the Bank uses twice-daily auctions of government term deposits (the first at 9:15 a.m. and the second at 4:15 p.m.) to effect the shifting of government funds and neutralize certain government flows.

Copyright © 2002 Pearson Education Canada Inc. 17- 36

… Neutralizing a Net Government Receipt

Consider a net government receipt of $100 (i.e., the government’s receipts from the public exceed its payments to the public by $100). To prevent a in settlement balances and an in ior, the Bank neutralizes the net government receipt by morning (9:15 a.m.) and afternoon (4:00 p.m.) auctions of government term deposits, as follows:

Bank of CanadaAssets Liabilities

Government Deposits - 100 Settlement Balances +100

Direct ClearersAssets LiabilitiesSettlement Balances +100 Government Deposits +100

Copyright © 2002 Pearson Education Canada Inc. 17- 37

… Neutralizing a Net Government Disbursement

If there were a net government disbursement of $100 (i.e., the government's payments to the public exceed its receipts from the public by $100), then settlement balances would by the same amount. To prevent a in ior, the Bank neutralizes the net government disbursement by a transfer of $100 from the government's accounts at the LVTS participants to the government's account at the Bank:

Bank of CanadaAssets Liabilities

Government Deposits + 100 Settlement Balances -100

Direct ClearersAssets LiabilitiesSettlement Balances -100 Government Deposits -100

Copyright © 2002 Pearson Education Canada Inc. 17- 38

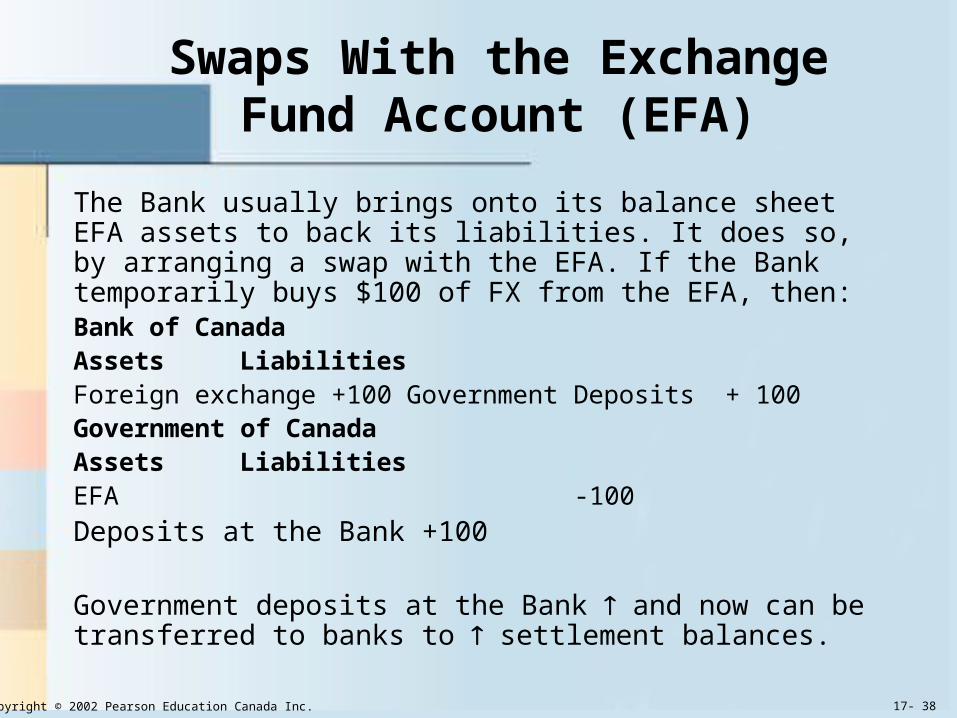

Swaps With the Exchange Fund Account (EFA)

The Bank usually brings onto its balance sheet EFA assets to back its liabilities. It does so, by arranging a swap with the EFA. If the Bank temporarily buys $100 of FX from the EFA, then: Bank of CanadaAssets LiabilitiesForeign exchange +100 Government Deposits + 100 Government of CanadaAssets LiabilitiesEFA -100

Deposits at the Bank +100

Government deposits at the Bank and now can be transferred to banks to settlement balances.

Copyright © 2002 Pearson Education Canada Inc. 17- 39

An Example of Monetary Control

• Suppose that the operating band is 4.5% to 5% and the Bank wishes to tighten policy by raising the band by 25 basis points

• In one of the eight fixed days for announcing changes to the band for ior, the Bank announces, at 9:00 a.m., that it is adjusting the band up from 4.5% to 5% to 4.75% to 5.25%

• From this announcement, LVTS participants know that the ib shifts from 5% to 5.25%, the rate on positive settlement balances shifts from 4.5% to 4.75%, and that the Bank’s new target ior, the midpoint of the operating band, shifts from 4.75% to 5%

• If later in the day overnight funds are trading below the target ior, the Bank enters into SRAs to enforce the new target for ior

Copyright © 2002 Pearson Education Canada Inc. 17- 40

An Example of Monetary Control(continued)

Assuming that the Bank enters into SRAs in the amount of $100, theT-accounts of the Bank and the direct clearers will be:

Bank of CanadaAssets Liabilities

Settlement Balances -100SRAs +100

Direct ClearersAssets LiabilitiesSettlement Balances -100 SRAs +100

Copyright © 2002 Pearson Education Canada Inc. 17- 41

An Example of Monetary Control(continued)

Because settlement balances the Bank neutralizes the effect on settlement balances of its issue of SRAs, by auctioning off $100 of government deposits :

Bank of CanadaAssets Liabilities

Settlement Balances +100Government Deposits -100

Direct ClearersAssets LiabilitiesSettlement Balances +100 Government Deposits +100

Copyright © 2002 Pearson Education Canada Inc. 17- 42

An Example of Monetary Control(continued)

The end-of-day effect on the balance sheets of the Bank and the direct clearers is as follows:Bank of CanadaAssets Liabilities

SRAs +100Government Deposits -100

Direct ClearersAssets LiabilitiesSRAs +100 Government Deposits +100

The Bank’s monetary tightening has been effected through the management of settlement balances, during the course of the day, with no change in the aggregate settlement balances