Chapter 17. Sequential Processing Departments T-Account Model of Process Costing Flows.

19

Chapter 17

-

Upload

betty-parker -

Category

Documents

-

view

220 -

download

2

Transcript of Chapter 17. Sequential Processing Departments T-Account Model of Process Costing Flows.

Chapter 17

Sequential Processing Departments

T-Account Model of Process Costing Flows

Process Costing and Direct Labor

Direct labor costsmay be small

in comparison toother product

costs in processcost systems.

Direct labor costsmay be small

in comparison toother product

costs in processcost systems.

DirectMaterials

Type of Product Cost

Do

llar

Am

ou

nt

DirectLabor

Mfg. Ovhd.

Process Costing and Direct Labor

Type of Product Cost

Do

llar

Am

ou

nt Conversion

Direct labor and manufacturing overhead isDirect labor and manufacturing overhead iscombined into one product cost called combined into one product cost called conversionconversion..

Direct labor and manufacturing overhead isDirect labor and manufacturing overhead iscombined into one product cost called combined into one product cost called conversionconversion..

DirectMaterials

Direct labor costsmay be small

in comparison toother product

costs in processcost systems.

Direct labor costsmay be small

in comparison toother product

costs in processcost systems.

Global Defense uses process costing to determine unit costs in its Assembly Department.

Upon completion, units are transferred to the Testing Department.

Direct materials are added at the beginning of the assembly process. Conversion costs are added evenly during assembly.

Global Defense uses process costing to determine unit costs in its Assembly Department.

Upon completion, units are transferred to the Testing Department.

Direct materials are added at the beginning of the assembly process. Conversion costs are added evenly during assembly.

Production Report Example

Process Diagram - Assembly

Conversion costs added evenly during process

Assembly Department

Transfer

Testing Department

Direct materials added at beginning of process

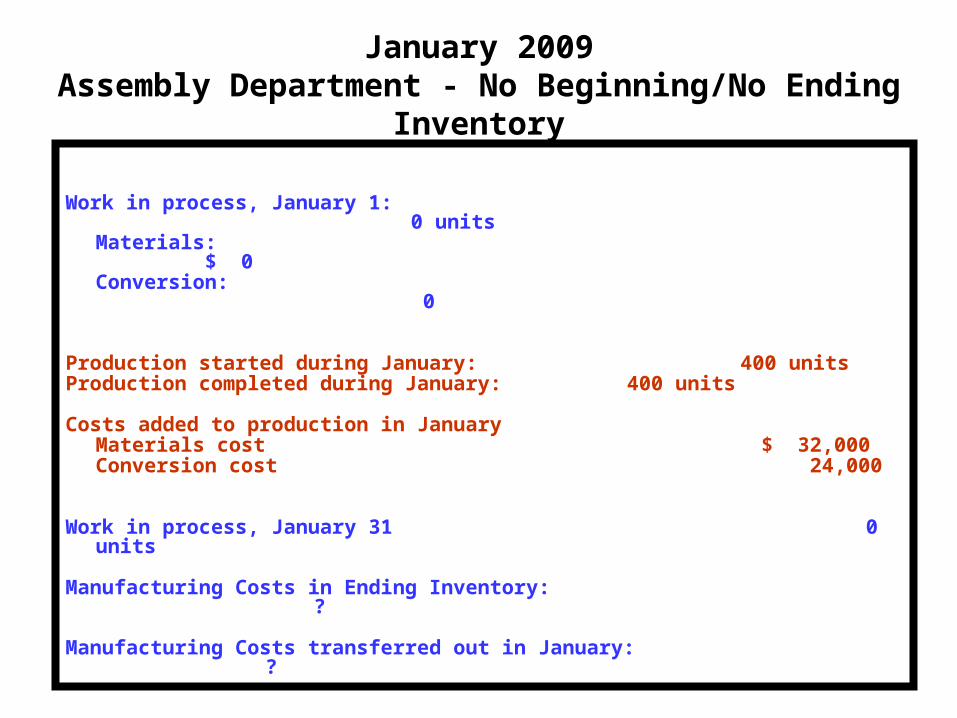

Work in process, January 1: 0 units Materials: $ 0Conversion: 0

Production started during January: 400 unitsProduction completed during January: 400 units

Costs added to production in JanuaryMaterials cost $ 32,000Conversion cost 24,000

Work in process, January 31 0 units

Manufacturing Costs in Ending Inventory: ?

Manufacturing Costs transferred out in January: ?

January 2009Assembly Department - No Beginning/No Ending Inventory

Work in process, February 1: 0 units Materials: $ 0Conversion: 0

Production started during February: 400 unitsProduction completed during February: 175 units

Costs added to production in FebruaryMaterials cost $ 32,000Conversion cost 18,600

Work in process, February 29 225 units Materials 100% complete

Conversion 60% complete

Manufacturing Costs in Ending Inventory: ?

Manufacturing Costs transferred out in February: ?

February 2009Assembly Department - No Beginning/Some Ending Inventory

Equivalent Units of Production

Equivalent units are partially complete and are part of work in process inventory.

Partially completed products are expressed in terms of a smaller number

of fully completed units.

Equivalent Units of ProductionTwo half completed products are

equivalent to one completed product.

So, 10,000 units 70 percent completeare equivalent to 7,000 complete units.

So, 10,000 units 70 percent completeare equivalent to 7,000 complete units.

+ = 1

For the current period, Jones started 15,000 units and completed 10,000 units, leaving 5,000 units in process that were 30 percent complete for conversion costs. How many equivalent units of production did Jones have for the period?

a. 10,000

b. 11,500

c. 13,500

d. 15,000

For the current period, Jones started 15,000 units and completed 10,000 units, leaving 5,000 units in process that were 30 percent complete for conversion costs. How many equivalent units of production did Jones have for the period?

a. 10,000

b. 11,500

c. 13,500

d. 15,000

Quick Check

Calculating and Using Equivalent Units of ProductionTo calculate the cost per

equivalent unit for the period:

Cost perequivalent

unit

=Costs for the period

Equivalent units of productionfor the period

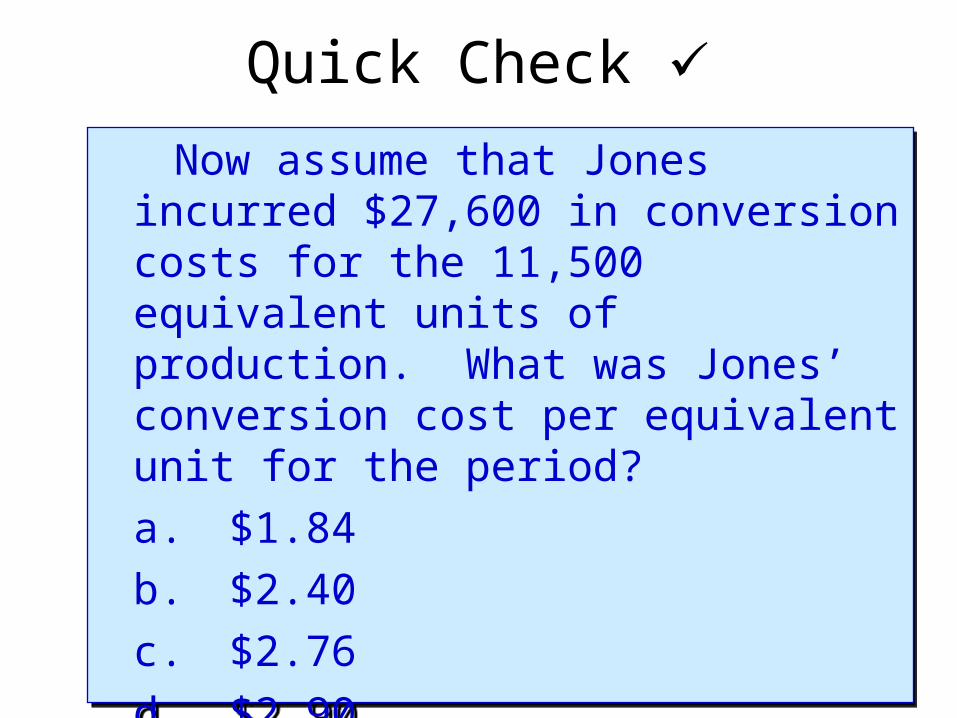

Now assume that Jones incurred $27,600 in conversion costs for the 11,500 equivalent units of production. What was Jones’ conversion cost per equivalent unit for the period?

a. $1.84

b. $2.40

c. $2.76

d. $2.90

Now assume that Jones incurred $27,600 in conversion costs for the 11,500 equivalent units of production. What was Jones’ conversion cost per equivalent unit for the period?

a. $1.84

b. $2.40

c. $2.76

d. $2.90

Quick Check

Now assume that Jones incurred $27,600 in production costs for the 11,500 equivalent units of production. What was Jones’ cost per equivalent unit for the period?

a. $1.84

b. $2.40

c. $2.76

d. $2.90

Now assume that Jones incurred $27,600 in production costs for the 11,500 equivalent units of production. What was Jones’ cost per equivalent unit for the period?

a. $1.84

b. $2.40

c. $2.76

d. $2.90

$27,600 ÷ 11,500 equivalent units

= $2.40 per equivalent unit

$27,600 ÷ 11,500 equivalent units

= $2.40 per equivalent unit

Quick Check

Work in process, March 1: 225 units Materials: 100% complete $ 18,000Conversion: 60% complete 8,100

Production started during March: 275 unitsProduction completed during March: 400 units

Costs added to production in March:Materials cost $ 19,800Conversion cost 16,380

Work in process, March 31: 100 units Materials 100% complete

Conversion 50% complete

Manufacturing Costs in Ending Inventory: ?

Manufacturing Costs transferred out in March: ?

March 2009Assembly Department - Some Beginning/Some Ending Inventory

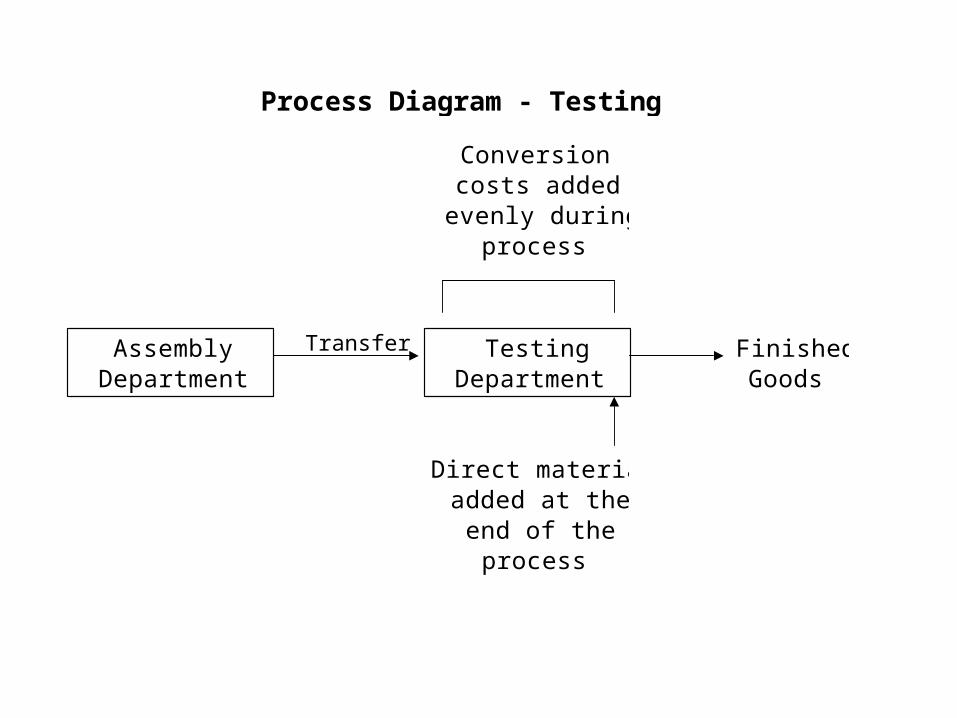

Transfer

Conversion costs added

evenly during process

Process Diagram - Testing

Direct materials added at the end of the

process

Finished Goods

Assembly Department

Testing Department

Work in process, March 1: 240 units Transferred-in 100% complete $ 33,600Materials: 0% complete 0Conversion: 62.5% complete 18,000

Transferred-in during March: 400 unitsProduction completed during March: 440 units

Costs added to production in March:Transferred-in cost $ 52,000Materials cost 13,200Conversion cost 48,600

Work in process, March 31: 200 units Transferred-in 100% complete

Materials 0% completeConversion 80% complete

Manufacturing Costs in Ending Inventory: ?

Manufacturing Costs transferred out in March: ?

March 2009Testing Department with Transferred-in Costs – W.A.Method

Work in process, March 1: 240 units Transferred-in 100% complete $ 33,600Materials: 0% complete 0Conversion: 62.5% complete 18,000

Transferred-in during March: 400 unitsProduction completed during March: 440 units

Costs added to production in March:Transferred-in cost $ 52,480Materials cost 13,200Conversion cost 48,600

Work in process, March 31: 200 units Transferred-in 100% complete

Materials 0% completeConversion 80% complete

Manufacturing Costs in Ending Inventory: ?

Manufacturing Costs transferred out in March: ?

March 2009Testing Department with Transferred-in Costs – FIFO Method