Chapter 131 Chapter 13. Liquidity Risk and Liability Management Learning Objectives: 1. To...

37

Chapter 13 1 Chapter 13. Liquidity Risk and Liability Management Learning Objectives: 1. To understand the importance of liquidity to banks and to the economy 2. To distinguish between core deposits and managed (volatile) liabilities 3. To understand the tradeoff between liquidity and profitability 4. To understand how to measure bank liquidity

-

Upload

jeffery-laurence-hutchinson -

Category

Documents

-

view

217 -

download

1

Transcript of Chapter 131 Chapter 13. Liquidity Risk and Liability Management Learning Objectives: 1. To...

Chapter 13 1

Chapter 13. Liquidity Risk and Liability Management Learning Objectives:

1. To understand the importance of liquidity to banks and to the economy

2. To distinguish between core deposits and managed (volatile) liabilities

3. To understand the tradeoff between liquidity and profitability

4. To understand how to measure bank liquidity

Chapter 13 2

Learning Objectives(cont.) and Chapter Theme 5. To understand securitization as a tool

of liquidity and risk management Chapter Theme

Banks need liquidity to meet deposit withdrawals and to satisfy customer loan demand. This liquidity can be stored in banks’ balance sheets or purchased in the marketplace. Being too liquid, however, is costly and not having enough liquidity is risky. As a tool of risk management, securitization permits banks to remove risk from their balances sheets and generate liquidity.

Chapter 13 3

The Importance of Liquidity Consider these headlines from the

American Banker Viewpoint: Too Many Banks Aren’t

Ready for Looming Liquidity Crisis Spare Change: Liquidity Steering

Group Going in Circles In Focus: Liquidity Rivaling Credit

Quality as Crisis du Jour

Chapter 13 4

LEMAC: The Inverted CAMEL L = Liquidity E = Earnings M = Management A = Asset Quality C = Capital Adequacy

Chapter 13 5

Recent Liquidity Episodes The aftermath of the “Attack on

America” The bailout of LTCM The stock market of 1987 Contrast these events with what

the Fed did after the stock-market crash of 1929

Chapter 13 6

Discussion Topic: Quote from John Reed (1987) We were providing as much liquidity as we

could. Quite a few of the firms went right up to their loan limits. We didn't take physical possession of securities, but we were damn close to our customers. You have a tremendous conflict there. On one hand, there's a need for liquidity in the system. On the other hand, when you're dealing in $100 million lot sizes, you can't afford to be wrong. We can't take a $100 million write-off to save a broker. The stockholders would lynch me and with good reason.

Chapter 13 7

The Role of Confidence A confidence function:

Net worth (+) Stability of earnings (+) Quality of information (+) Government guarantees (+) Liquidity (+)

Chapter 13 8

The Evolution of Liquidity Management Commercial-loan theory or real-bills doctrine

(1920s and earlier) Asset-conversion or shiftability approach (post

World War II through 1940s) Anticipated-income theory (1950s)

Liability management (late 1960s and early 1970s)

Asset-liability management and securitization (mid-1970s to mid-1990s)

Risk management (mid-1990s to present)

Chapter 13 9

The Instruments of Liability Management (LM, see Box 13-1)

Federal funds Repurchase agreements (RPs, repos) Negotiable CDs Consumer CDs Brokered deposits Eurodollar CDs Global CDs

Chapter 13 10

LM Instruments (continued) MMDAs IRAs Commercial paper Notes and debentures Volatile liabilities

Chapter 13 11

Chrysler Financial Corporation:

Case Study of a Liquidity Crisis

Year-end 1989 financial profile: CP outstanding = $10.1 billion Equity capital (E) = $2.8 billion Total assets (A) = $30.1 billion CP/A = 33.5% E/A = 9.3% or EM = 10.75 Note: CP = commercial paper

Chapter 13 12

The Credit Event In 1990, Chrysler’s commercial paper (CP)

was downgraded from P-2 to P-3 and subsequently to N.P. ( Not Prime) and its long-term bond rating was lowered from Baa to Ba

Under these conditions, Chrysler’s CP was not attractive to the money market at rates that Chrysler was willing to pay, that is, it would have to pay a premium to obtain refinancing

Chapter 13 13

CP Background:Orderly Exit and Asset Sales

Bank back-up lines of credit, standby letters of credit, and medium-term note facilities

Asset sales

Chapter 13 14

Lines of Credit vs. Standby Letters of Credit

Since bank line-of-credit (LOC) contracts typically contain material-adverse-change (MAC) clauses, they are not guarantees and they have annual clean-up and rate resets. Strength of customer relation is important.

In contrast, a standby letter of credit virtually guarantees payment, i.e., the bank will pay off the issue if the borrower cannot.

Chapter 13 15

Chrysler’s Strategy

An aggressive program of asset sales and securitization

Chapter 13 16

“The rest of the story ...”

Immediate cash shortfall is met by borrowing $1.3 billion under its parent company’s banks’ lines of credit

By year-end 1990, CP outstanding is $1.1B, a decrease of $9B

Sales of receivables in 1990 generates $18.3B

Year-end 1990 assets total $24.7B with equity of $2.8B (capital ratio of 11.3%)

Chapter 13 17

The story continues ...

To repay maturing debt of $3.6B in 1991 and $3B in 1992, Chrysler continued its asset-sales strategy.

Chapter 13 18

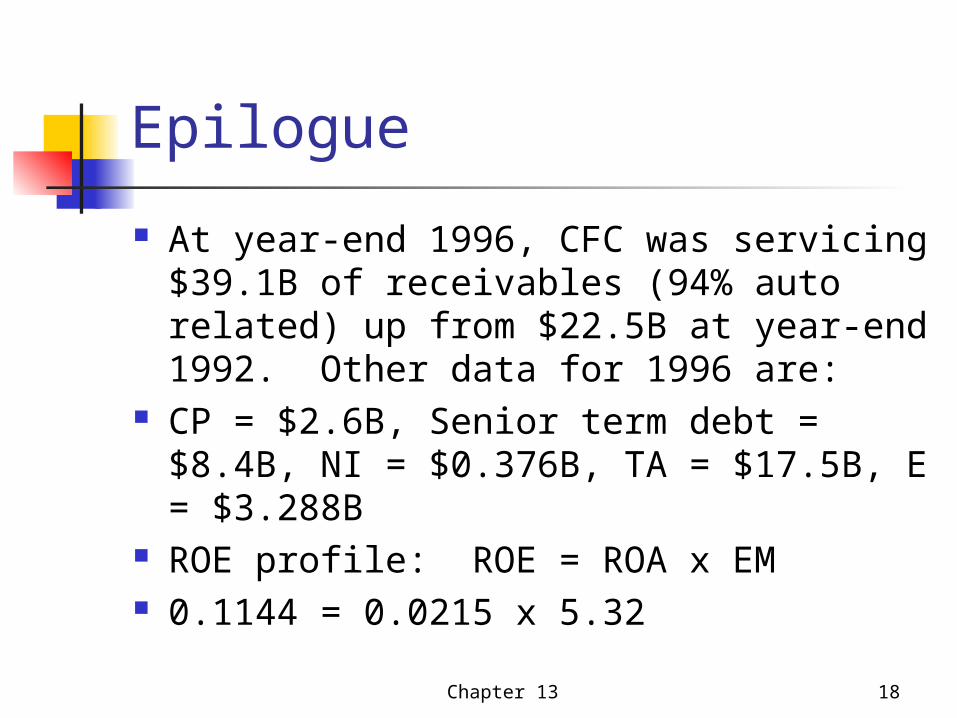

Epilogue

At year-end 1996, CFC was servicing $39.1B of receivables (94% auto related) up from $22.5B at year-end 1992. Other data for 1996 are:

CP = $2.6B, Senior term debt = $8.4B, NI = $0.376B, TA = $17.5B, E = $3.288B

ROE profile: ROE = ROA x EM 0.1144 = 0.0215 x 5.32

Chapter 13 19

Discussion of other Cases First National Bank of Browning,

Montana (1980) Continental Illinois (Chicago, 1984) Bank of New England (1991) REBs and FHLB Advances

Chapter 13 20

Liquidity Versus Profitability Given a positively sloped yield curve,

short-term rates < long-term rates Short-term assets are safer while

longer-term assets are riskier When the yield curve is inverted,

safer assets have higher returns but such rates are expected to decline based on the expectations theory

Chapter 13 21

Discussion Questions Explain the basic yield-curve

shapes and the embodied tradeoffs Over the interest-rate/business

cycle, how does the yield curve move? How do bank loan and deposit flows move?

Distinguish between stored liquidity and purchased liquidity

Chapter 13 22

Effective Liquidity Management Confidence Maintaining relationships Avoiding “fire sales” Cost of capital and default-risk

premiums Avoiding the Fed’s discount

window

Chapter 13 23

Core Deposits Versus Managed Liabilities Core = sum of interest-bearing

deposits in domestic offices minus large time deposits in domestic offices plus domestic demand deposits

Core deposits are relatively stable funds gather in local markets

They vary inversely with bank size

Chapter 13 24

Managed Liabilities Managed liabilities have four

components: Interest-bearing deposits in foreign

offices Large time deposits in domestic offices FF purchased/Repos Other interest-bearing liabilities

“Hot money” is volatile and use of it varies directly with bank size

Chapter 13 25

Types of Interest-Bearing Liabilities Savings accounts Small time deposits Large time deposits Deposits in foreign offices FF purchases and RPs Discuss use of these funds by

banks of various sizes

Chapter 13 26

Noninterest-Bearing Liabilities Why do banks hold such funds? How have these funds varied over

time? What forces have been driving

these trends?

Chapter 13 27

The Cost of Bank Funds Distinguish and discuss the following

pairs of terms with respect to cost: Foreign vs. domestic Core vs. managed liabilties Explicit vs. implicit interest Eras of interest-bearing checking

accounts: Pre-1933 1933-1980 Post 1980

Chapter 13 28

A Bank’s Weighted Average Marginal Cost of Funds Source of funds (as a % of balance

sheet) Interest cost Operating cost Total cost Weighted cost Weighted average

Chapter 13 29

Example (no operating costs) Source Amt Cost

Weighted cost Deposits .85 5% 4.25% Nondep.debt 0.057% 0.35% Equity* .10 14%1.40% Weighted 1.00 6.00% *Shareholder required return

Chapter 13 30

Market Discipline and Cost of Funds Since riskier banks will have to pay more for

funds than safer banks, bank should want to signal/demonstrate to money and capital markets that they are safe (e.g., have adequate capital – the K in TRICK)

To the extent that banks engage in cost plus pricing, they might just ignore this discipline with respect to the costs of deposits and nondeposit debt; however, higher shareholder required returns and lower stock values should get managers’ attention

Chapter 13 31

Measures of Bank Liquidity Sources and uses of funds Large-liability dependence Various ratios (to assets)

Core deposits Loans Temporary investments

Other ratios: Loans to deposits, pledged securities, brokered deposits, market to book (of securities)

Chapter 13 32

The Dynamics of Liquidity Management Role of expectations Properties of time series data Forecasting techniques

Chapter 13 33

The Three Faces of Liability Management Minimize interest expense

Segment markets Meeting loan demand to enhance

customer relationships Desire to reduce regulatory burdens

associated with reserve requirements and deposit-insurance fees (and Reg Q when it existed)

Chapter 13 34

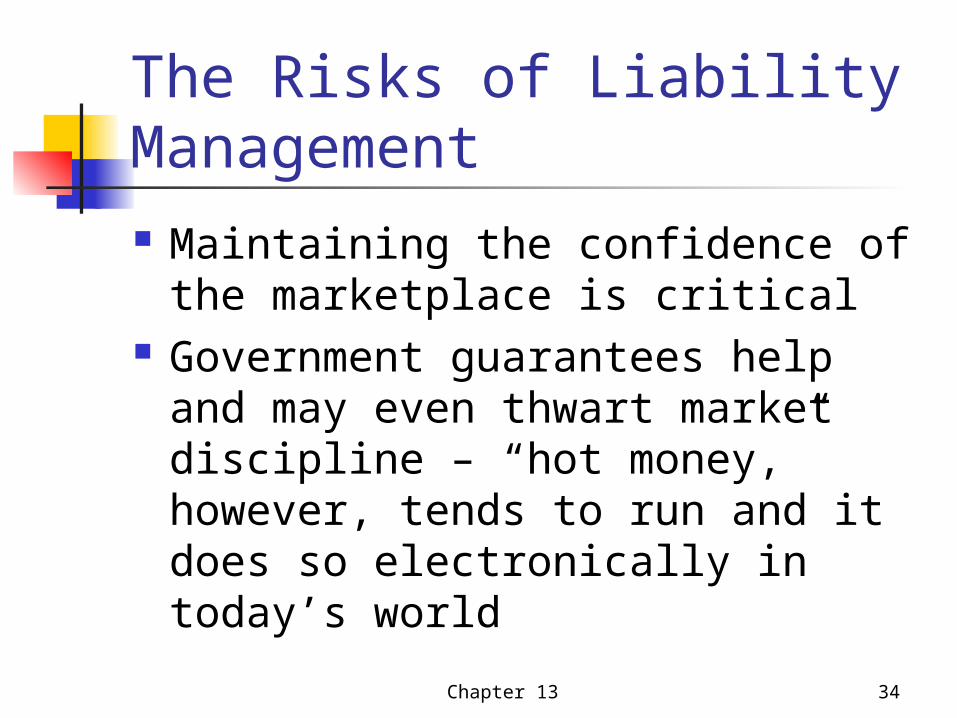

The Risks of Liability Management Maintaining the confidence of the

marketplace is critical Government guarantees help and

may even thwart market discipline – “hot money,” however, tends to run and it does so electronically in today’s world

Chapter 13 35

Chapter Summary The importance and interaction of

liquidity and confidence are captured by the following statements: "Liquidity always comes first; without it

a bank doesn't open its doors; with it, a bank may have time to solve its basic problems" (Donald Howard, Chief Financial Officer, Citicorp).

Chapter 13 36

Summary (continued) "Our whole financial system runs

on confidence and not much else when you get down to it. What we've learned is that when confidence erodes, it erodes very quickly" (L. William Seidman, former Chairman, FDIC).

Chapter 13 37

Summary (continued) On the topic of liquidity and the

availability of capital, also consider, this by David Ruder, former chairman of the SEC, following the stock market crash of October 1987 : "I personally regard that question is

probably the most important one to come out of the market decline.