CHAPTER 13 The Cost of Capital Sources of capital Component costs WACC.

33

CHAPTER 13 The Cost of Capital Sources of capital Component costs WACC

-

Upload

raymond-hodge -

Category

Documents

-

view

225 -

download

2

Transcript of CHAPTER 13 The Cost of Capital Sources of capital Component costs WACC.

CHAPTER 13The Cost of Capital

Sources of capital Component costs WACC

Cost of Capital

The cost of capital represents the overall cost of financing to the firm

The cost of capital is normally the relevant discount rate to use in analyzing an investment

The overall cost of capital is a weighted average of the various sources, including debt, preferred stock, and common equity:

WACC = Weighted Average Cost of CapitalWACC = After-tax costs x weights

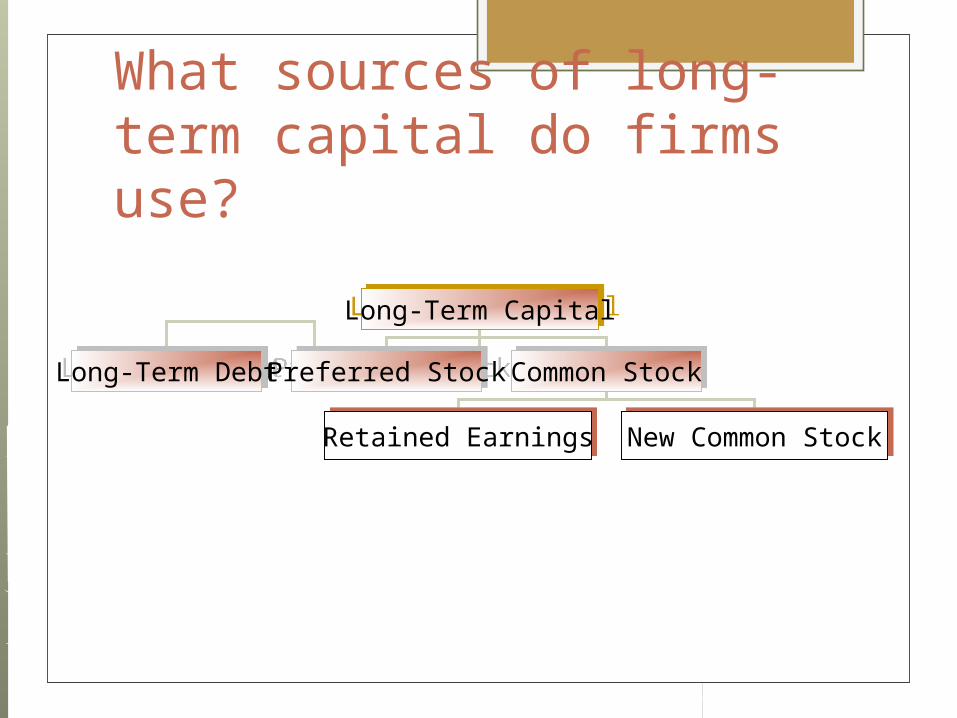

What sources of long-term capital do firms use?

Long-Term CapitalLong-Term Capital

Long-Term DebtLong-Term Debt Preferred StockPreferred Stock Common StockCommon Stock

Retained EarningsRetained Earnings New Common StockNew Common Stock

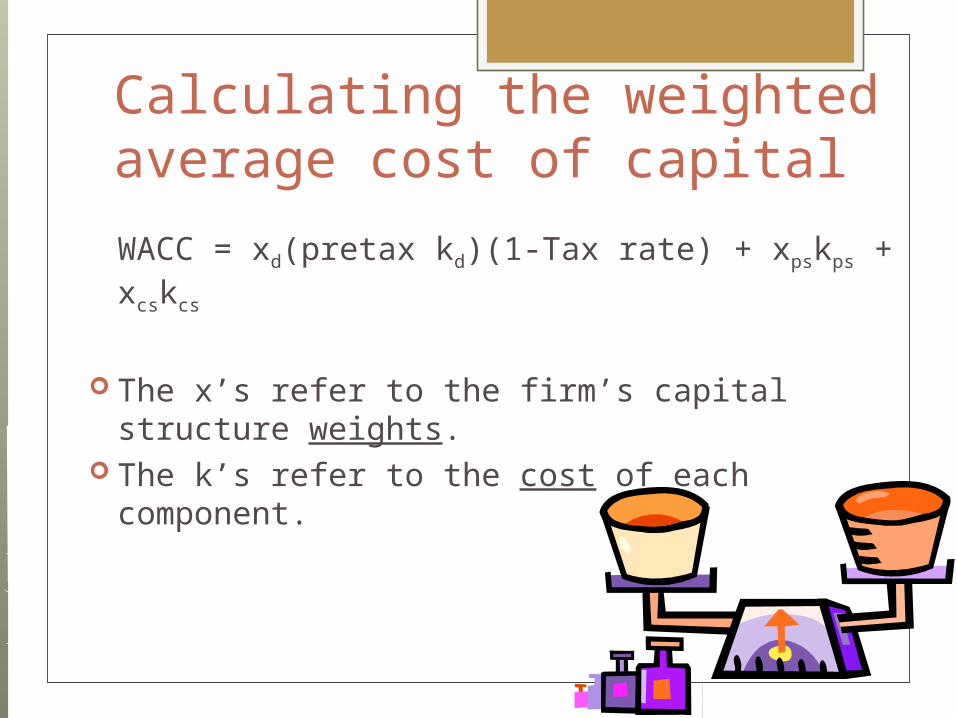

Calculating the weighted average cost of capital

WACC = xd(pretax kd)(1-Tax rate) + xpskps + xcskcs

The x’s refer to the firm’s capital structure weights.

The k’s refer to the cost of each component.

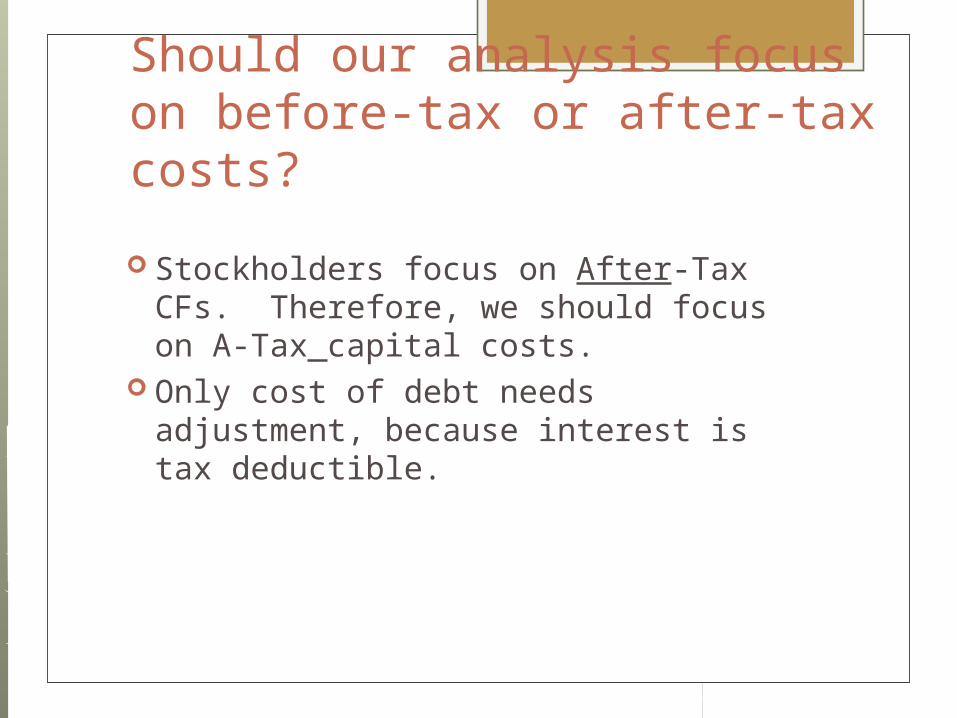

Should our analysis focus on before-tax or after-tax costs?

Stockholders focus on After-Tax CFs. Therefore, we should focus on A-Tax capital costs.

Only cost of debt needs adjustment, because interest is tax deductible.

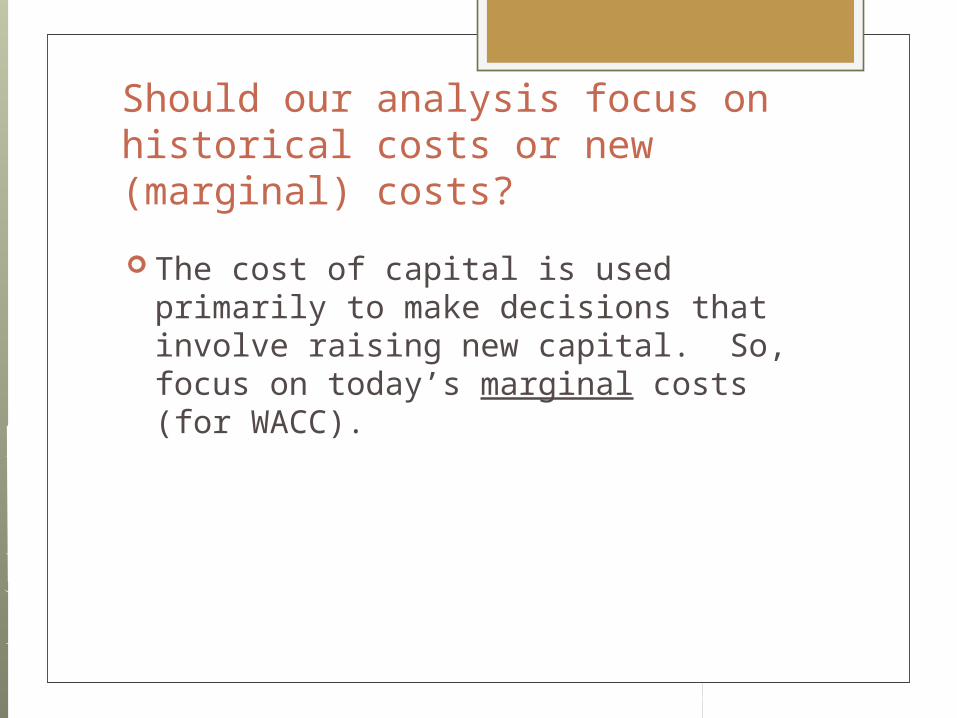

Should our analysis focus on historical costs or new (marginal) costs?

The cost of capital is used primarily to make decisions that involve raising new capital. So, focus on today’s marginal costs (for WACC).

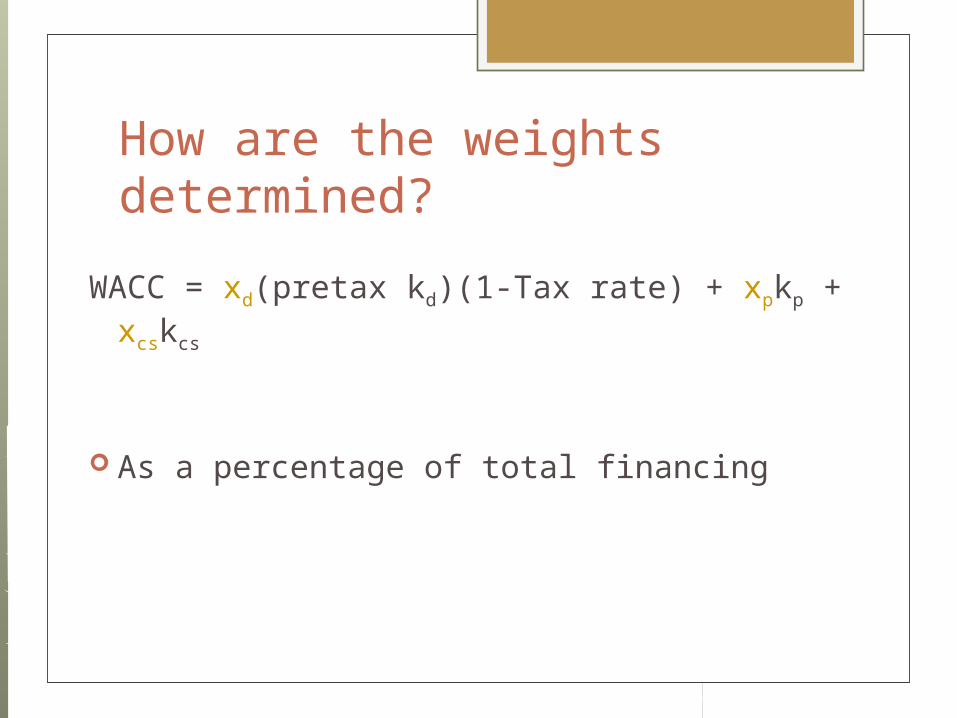

How are the weights determined?

WACC = xd(pretax kd)(1-Tax rate) + xpkp + xcskcs

As a percentage of total financing

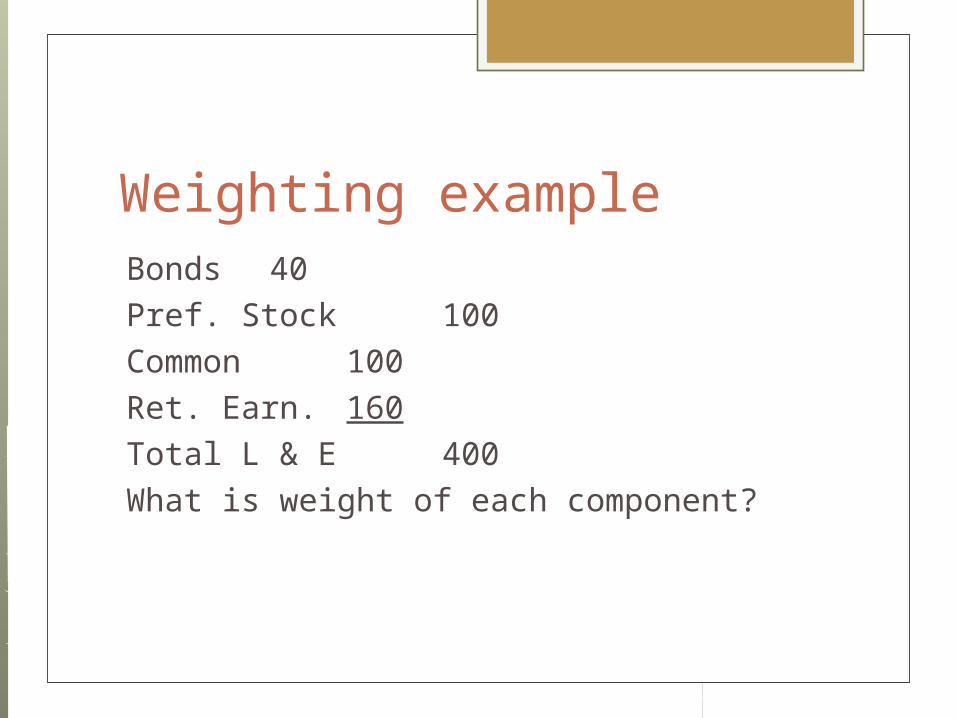

Weighting exampleBonds 40Pref. Stock 100Common 100Ret. Earn. 160Total L & E 400What is weight of each component?

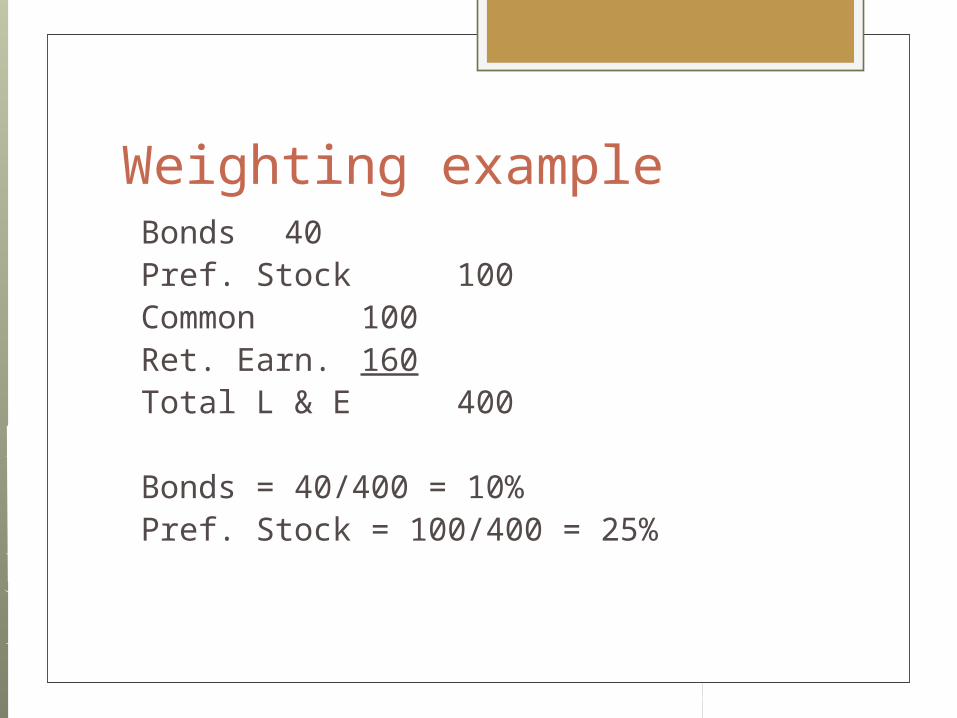

Weighting exampleBonds 40Pref. Stock 100Common 100Ret. Earn. 160Total L & E 400

Bonds = 40/400 = 10%Pref. Stock = 100/400 = 25%

Component cost of debt WACC = xd(pretax kd)(1-T) + xpkp + xcskcs

kd is the marginal cost of debt capital. The yield to maturity on outstanding L-T debt is

often used as a measure of kd.

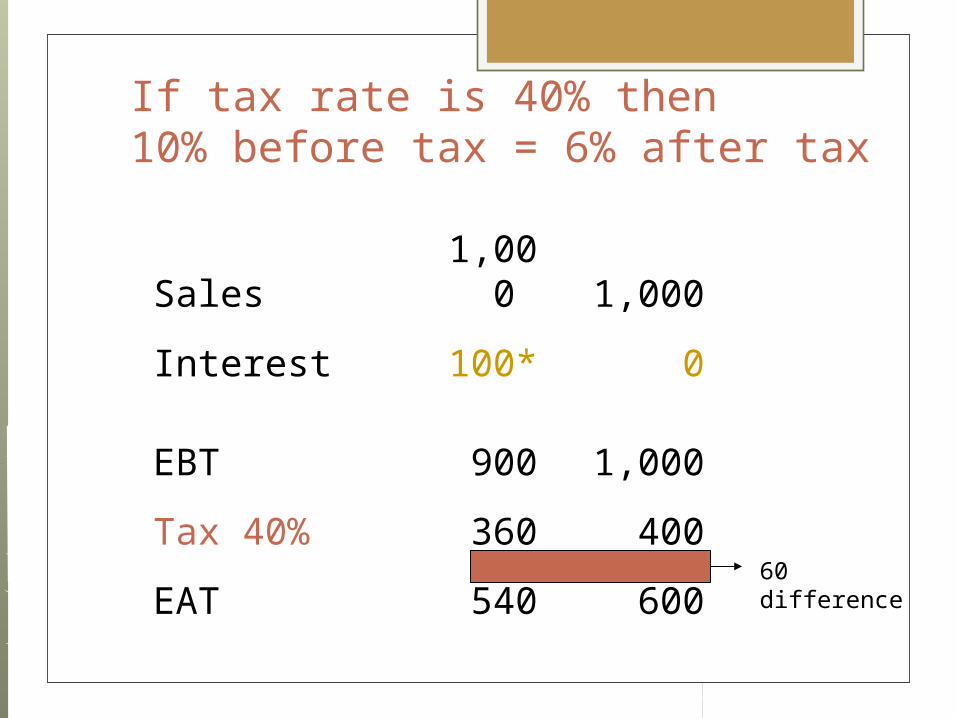

Why tax-adjust, i.e. why kd(1-Tax rate)?

If tax rate is 40% then 10% before tax = 6% after tax

Sales

1,000

1,000

Interest 100* 0

EBT 900

1,000

Tax 40% 360 400

EAT 540 600 60 difference

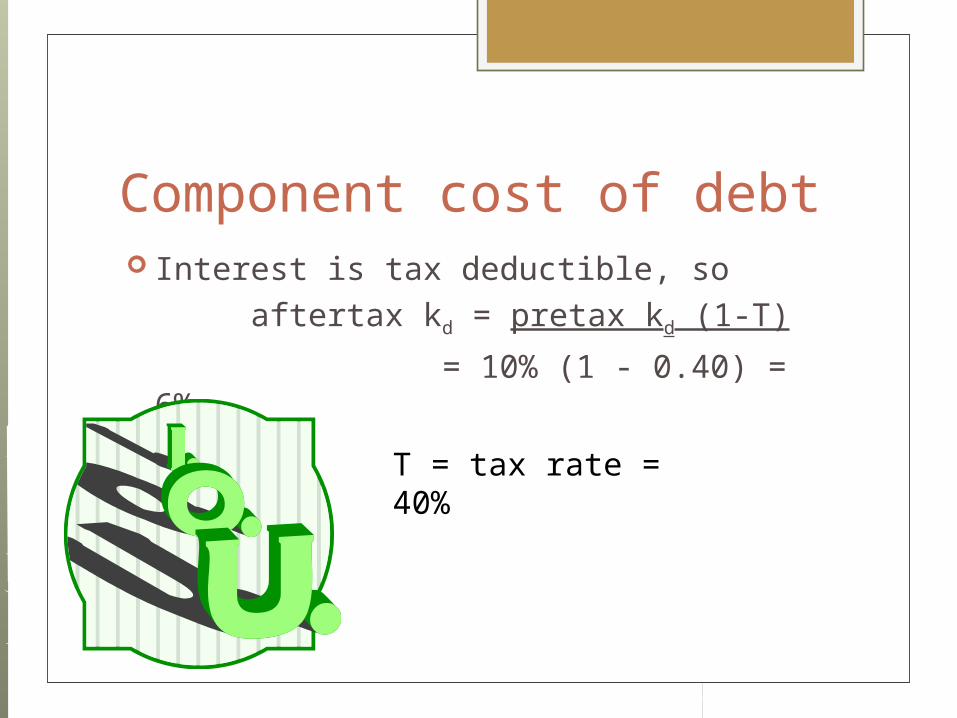

Component cost of debt Interest is tax deductible, so

aftertax kd = pretax kd (1-T)

= 10% (1 - 0.40) = 6%

T = tax rate = 40%

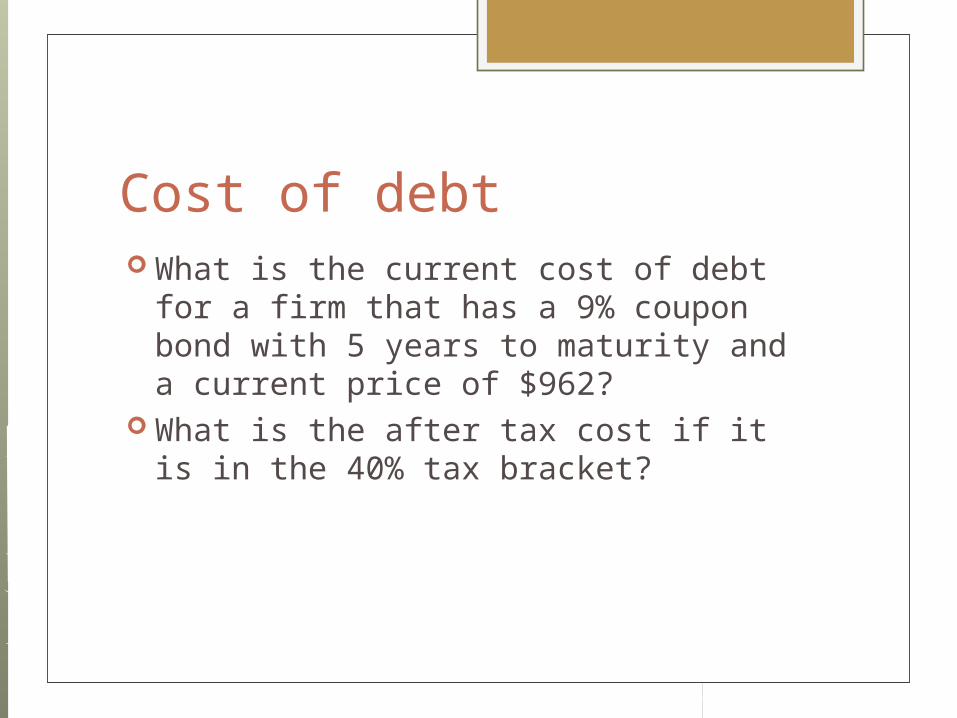

Cost of debt What is the current cost of debt for a

firm that has a 9% coupon bond with 5 years to maturity and a current price of $962?

What is the after tax cost if it is in the 40% tax bracket?

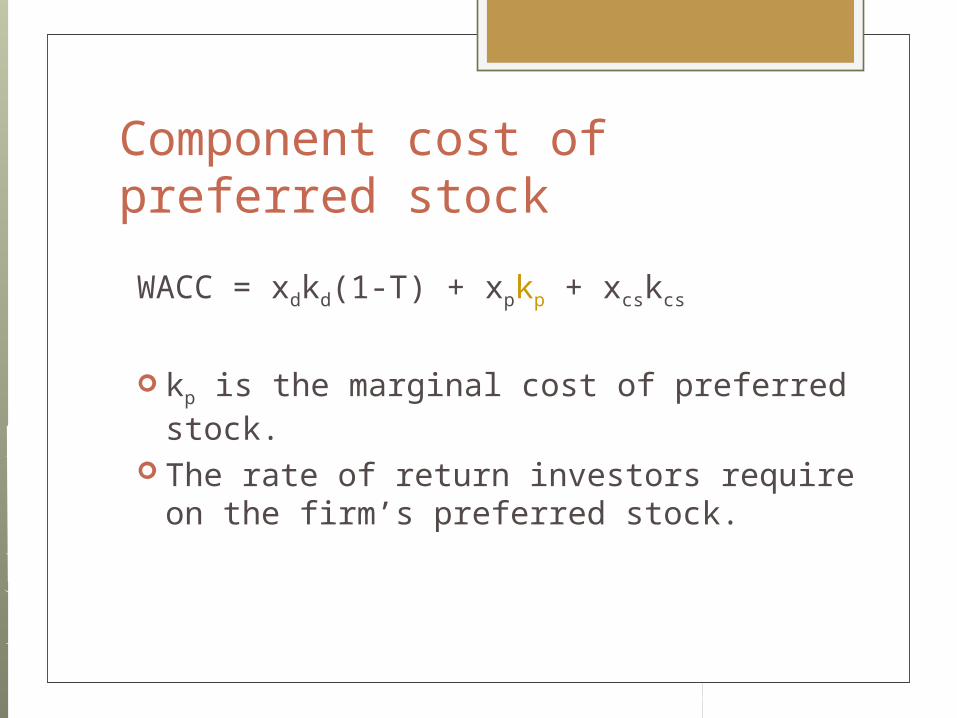

Component cost of preferred stock

WACC = xdkd(1-T) + xpkp + xcskcs

kp is the marginal cost of preferred stock. The rate of return investors require on the

firm’s preferred stock.

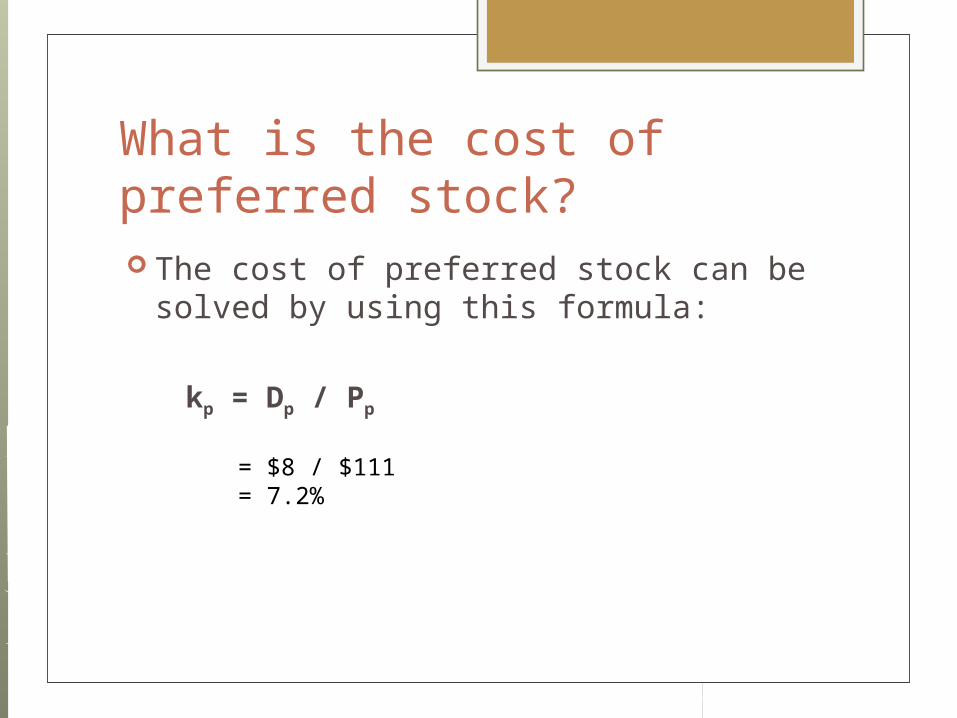

What is the cost of preferred stock? The cost of preferred stock can be

solved by using this formula:

kp = Dp / Pp

= $8 / $111= 7.2%

Component cost of preferred stock Preferred dividends are not

tax-deductible, so no tax adjustments necessary.

Component cost of equity WACC = xd(pretax kd)(1-T) + xpkp + xcskcs

kcs is the marginal cost of common equity

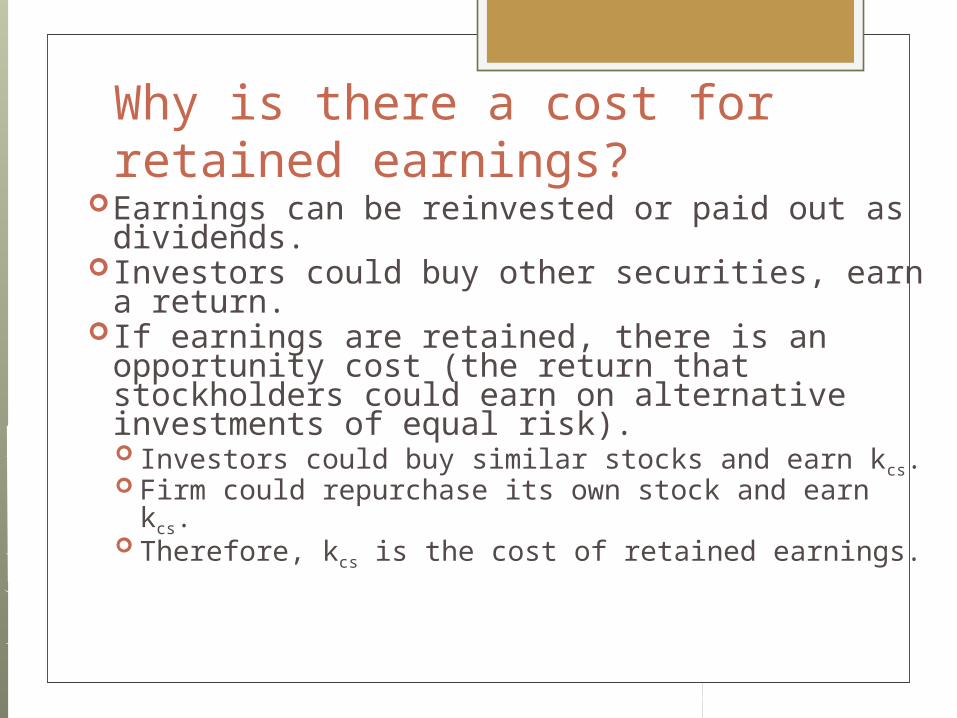

Why is there a cost for retained earnings?

Earnings can be reinvested or paid out as dividends.

Investors could buy other securities, earn a return.

If earnings are retained, there is an opportunity cost (the return that stockholders could earn on alternative investments of equal risk). Investors could buy similar stocks and earn kcs. Firm could repurchase its own stock and earn

kcs. Therefore, kcs is the cost of retained earnings.

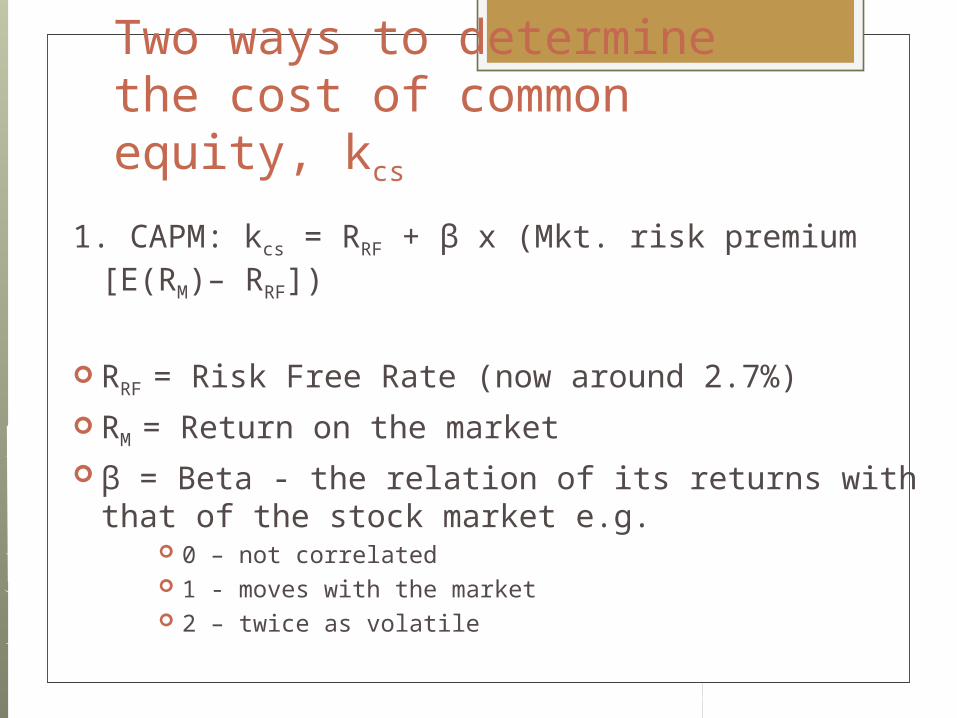

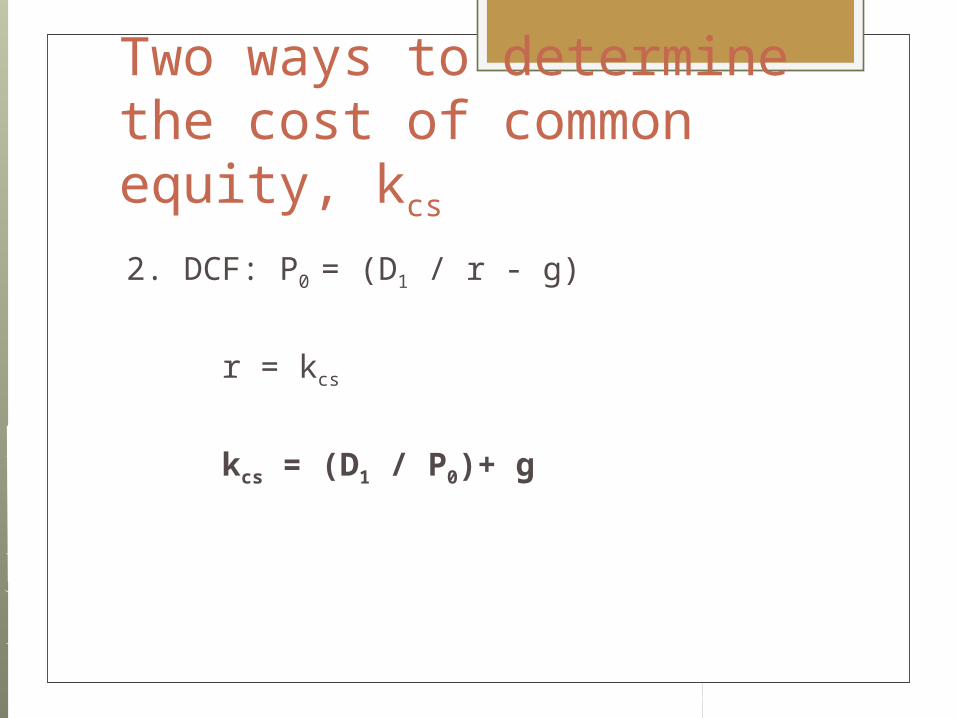

Two ways to determine the cost of common equity, kcs

1. CAPM: kcs = RRF + β x (Mkt. risk premium [E(RM)– RRF])

RRF = Risk Free Rate (now around 2.7%)

RM = Return on the market β = Beta - the relation of its returns with that of

the stock market e.g. 0 – not correlated 1 - moves with the market 2 – twice as volatile

Two ways to determine the cost of common equity, kcs

2. DCF: P0 = (D1 / r - g)

r = kcs

kcs = (D1 / P0)+ g

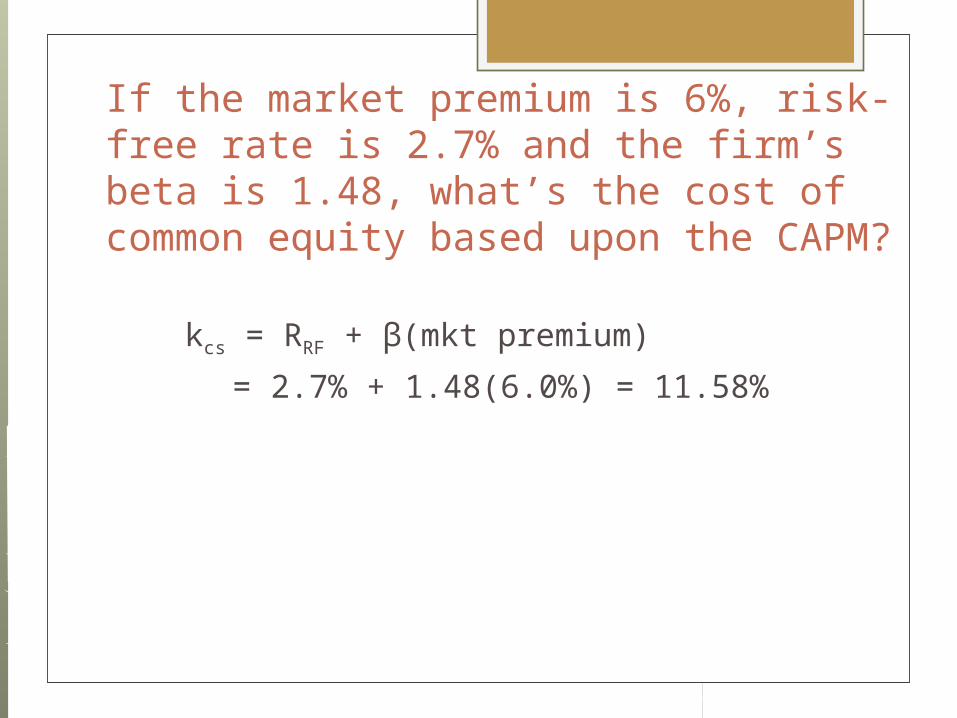

If the market premium is 6%, risk-free rate is 2.7% and the firm’s beta is 1.48, what’s the cost of common equity based upon the CAPM?

kcs = RRF + β(mkt premium)

= 2.7% + 1.48(6.0%) = 11.58%

If D0 = $1.72, P0 = $43, and g = 5%, what’s the cost of common equity based upon the DCF approach?

D1 = D0 (1+g)

D1 = $1.72 (1 + .05)

D1 = $1.81

kcs = (D1 / P0)+ g

= ($1.81 / $43) + 0.05= 9.2%

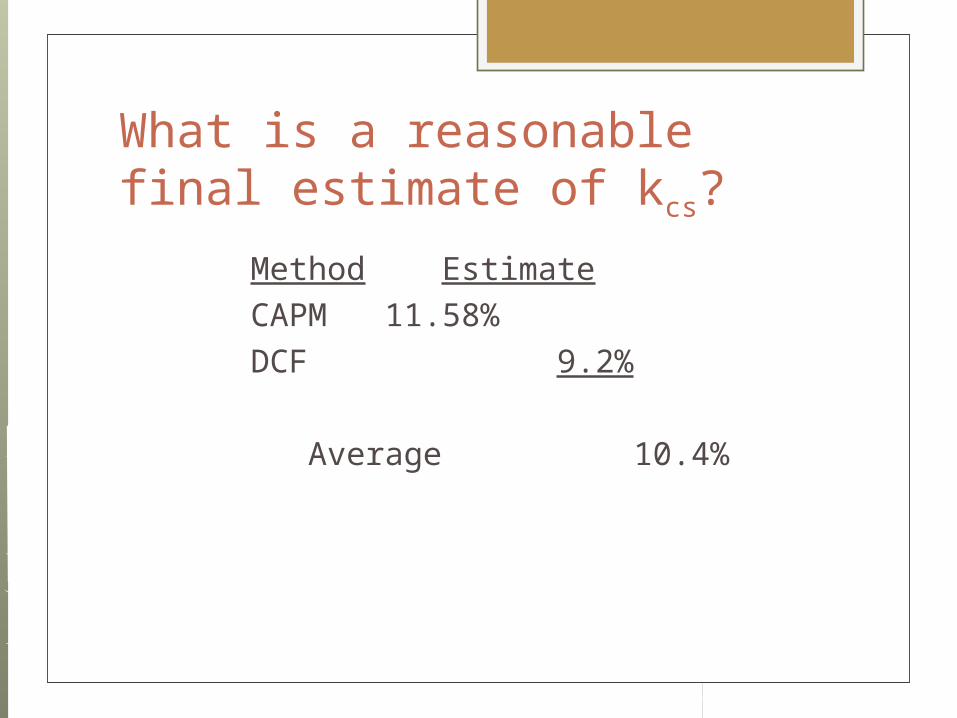

What is a reasonable final estimate of kcs?

Method EstimateCAPM 11.58%DCF 9.2%

Average 10.4%

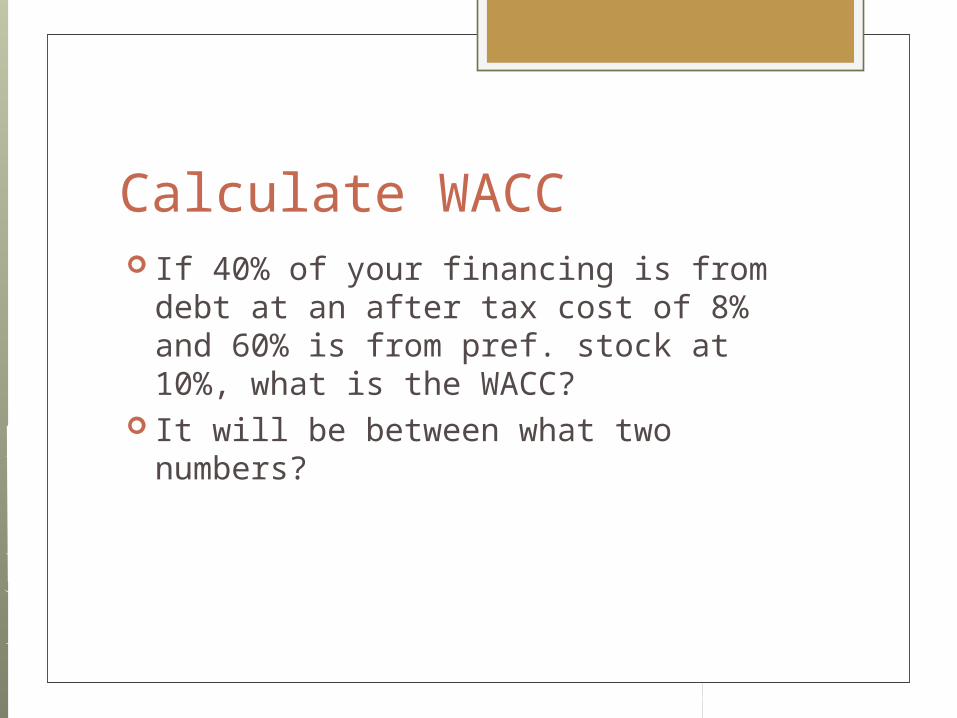

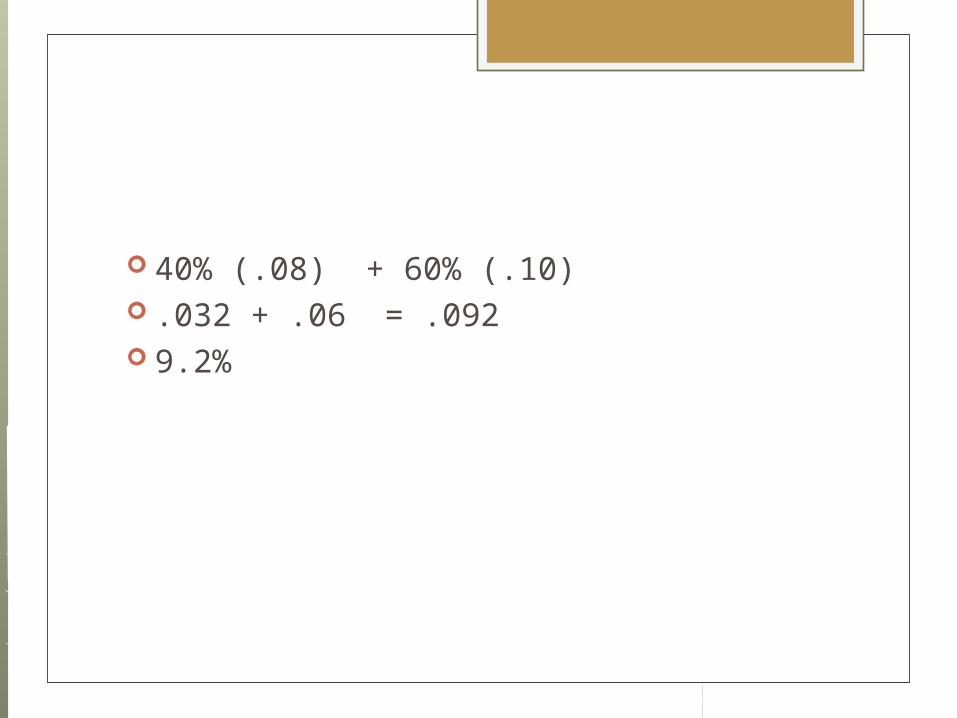

Calculate WACC If 40% of your financing is from debt at

an after tax cost of 8% and 60% is from pref. stock at 10%, what is the WACC?

It will be between what two numbers?

40% (.08) + 60% (.10) .032 + .06 = .092 9.2%

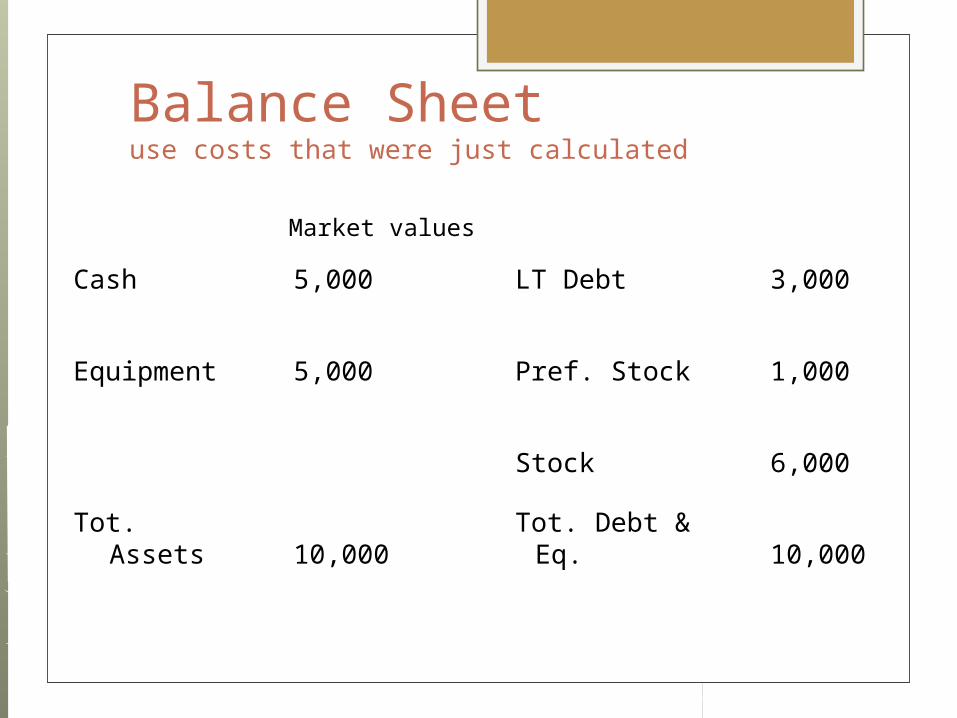

Balance Sheetuse costs that were just calculated

Cash 5,000 LT Debt 3,000

Equipment 5,000 Pref. Stock 1,000

Stock 6,000

Tot. Assets 10,000 Tot. Debt & Eq. 10,000

Market values

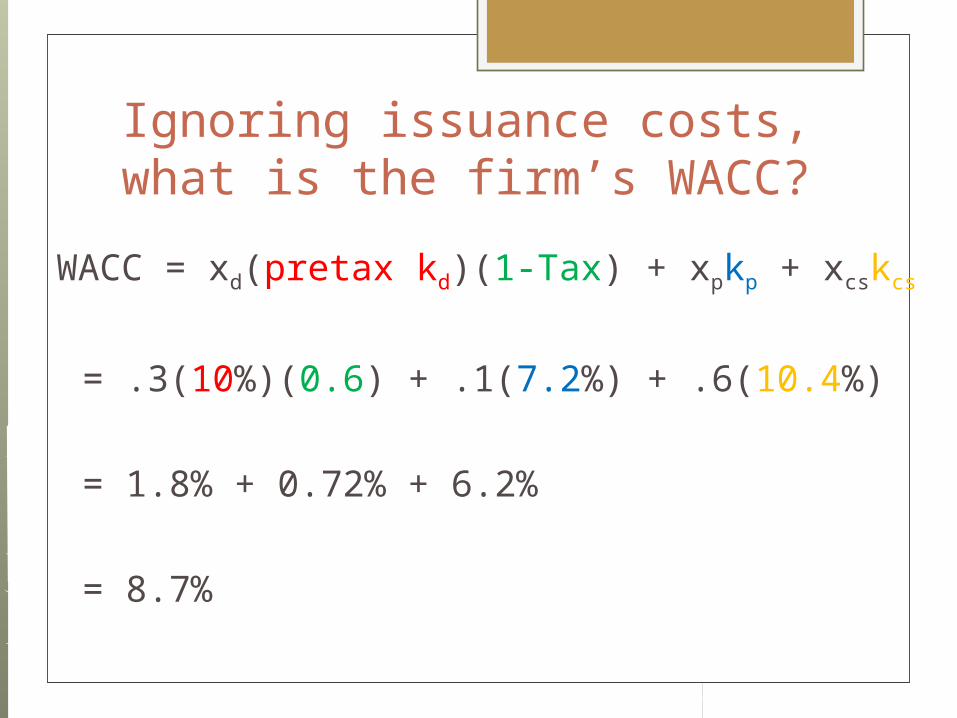

Ignoring issuance costs, what is the firm’s WACC?

WACC = xd(pretax kd)(1-Tax) + xpkp + xcskcs

= .3(10%)(0.6) + .1(7.2%)

+ .6(10.4%)

= 1.8% + 0.72% + 6.2%

= 8.7%

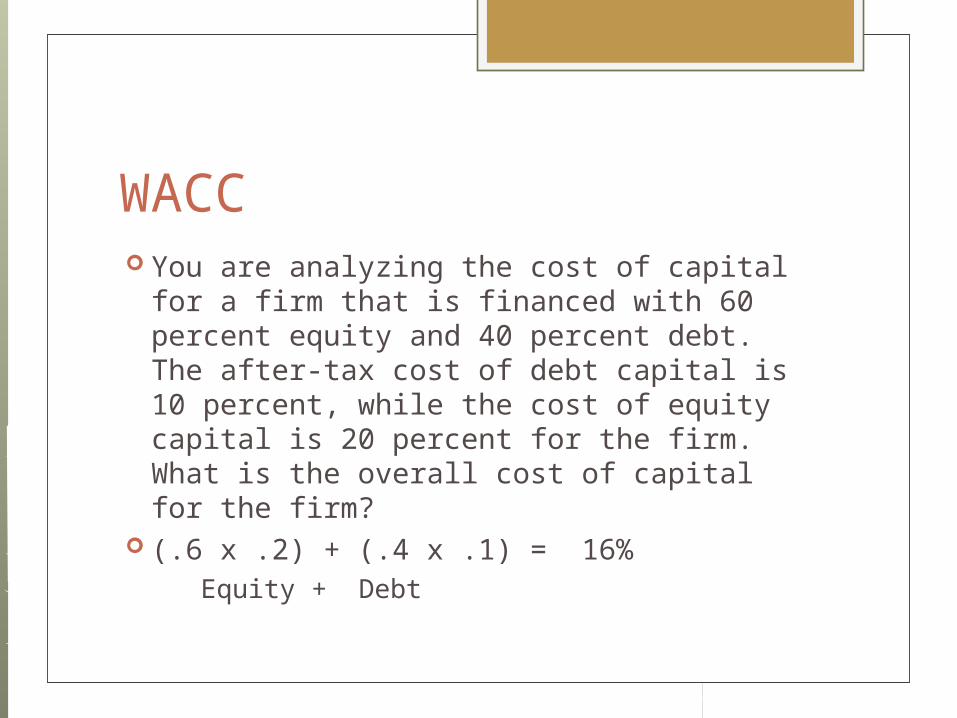

WACC You are analyzing the cost of capital for

a firm that is financed with 60 percent equity and 40 percent debt. The after-tax cost of debt capital is 10 percent, while the cost of equity capital is 20 percent for the firm. What is the overall cost of capital for the firm?

(.6 x .2) + (.4 x .1) = 16% Equity + Debt

Cardinal Health has bonds outstanding with 15 years to maturity and are currently priced at $800. If the bonds have a coupon rate of 8.5 percent, then what is the after-tax cost of debt for Beckham if its marginal tax rate is 30%?

7.9%

Should the company use the composite WACC as the hurdle rate for each of its projects?

NO! The composite WACC reflects the risk of an average project undertaken by the firm. Therefore, the WACC only represents the “hurdle rate” for a typical project with average risk.

Different projects have different risks. The project’s WACC should be adjusted to reflect the project’s risk.

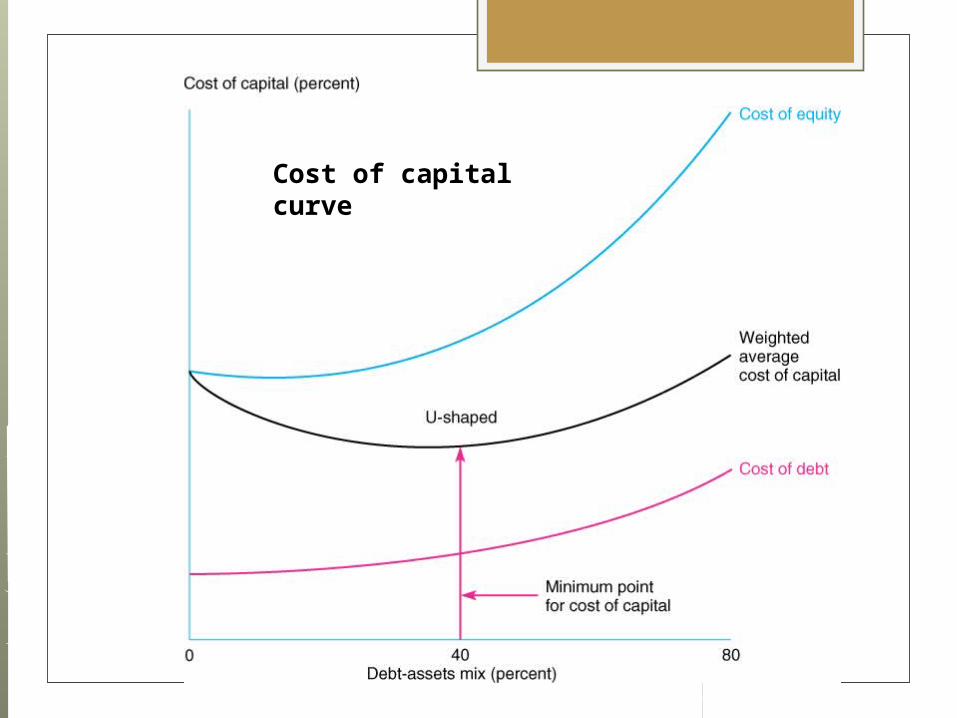

Optimum Capital Structure

The optimal (best) situation is associated with the minimum overall cost of capital: Optimum capital structure means the lowest WACC

Usually occurs with 30-50% debt in a firm’s capital structure

WACC is also referred to as the required rate of return or the discount rate

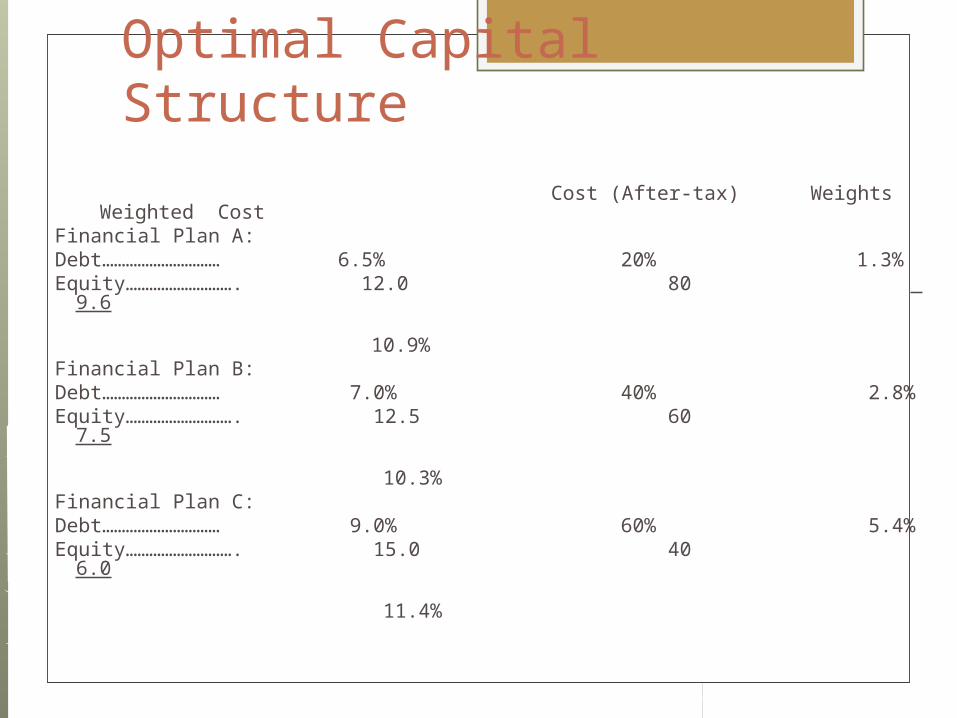

Optimal Capital Structure

Cost (After-tax) Weights Weighted Cost

Financial Plan A:Debt………………………… 6.5% 20% 1.3%Equity………………………. 12.0 80 9.6

10.9%Financial Plan B:Debt………………………… 7.0% 40% 2.8%Equity………………………. 12.5 60 7.5

10.3%Financial Plan C:Debt………………………… 9.0% 60% 5.4%Equity………………………. 15.0 40 6.0

11.4%

Cost of capital curve