CHAPTER 13 Preparing Payroll Records. OBJECTIVES: n Define accounting terms related to payroll...

33

CHAPTER 13 CHAPTER 13 Preparing Payroll Records

-

Upload

jody-hardy -

Category

Documents

-

view

218 -

download

1

Transcript of CHAPTER 13 Preparing Payroll Records. OBJECTIVES: n Define accounting terms related to payroll...

CHAPTER 13CHAPTER 13

Preparing Payroll Records

OBJECTIVES: OBJECTIVES:

Define accounting terms related to payroll records

Identify accounting practices related to payroll records

Complete a payroll time card Calculate payroll taxes Complete payroll register and an employee

earnings record Prepare payroll checks

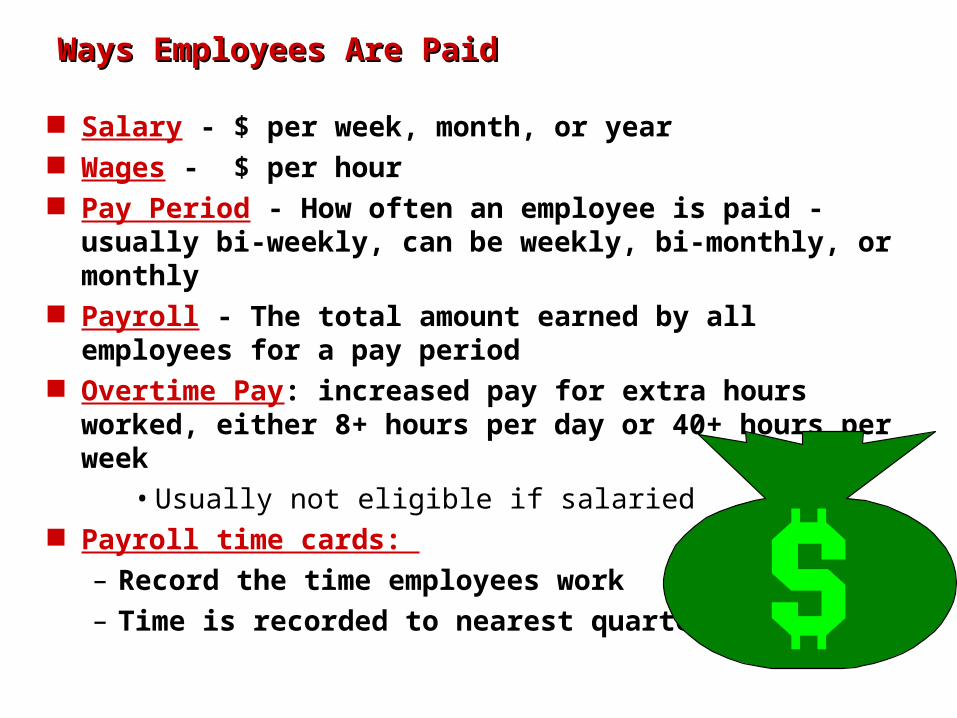

Ways Employees Are PaidWays Employees Are Paid

Salary - $ per week, month, or year Wages - $ per hour Pay Period - How often an employee is paid - usually

bi-weekly, can be weekly, bi-monthly, or monthly Payroll - The total amount earned by all employees for

a pay period Overtime Pay: increased pay for extra hours worked,

either 8+ hours per day or 40+ hours per week• Usually not eligible if salaried

Payroll time cards: – Record the time employees work – Time is recorded to nearest quarter hour

CH 13-1: Preparing Payroll Time CardsCH 13-1: Preparing Payroll Time Cards

Must keep special payroll records to support the recording of payroll transactions in a journal: 1. Employee earnings record – individual2. Payroll register – all employees

Records are used:– To inform employees of their annual

earnings– For business to prepare payroll records for

government

ANALYZING A PAYROLL TIME CARDANALYZING A PAYROLL TIME CARD

CALCULATING EMPLOYEE HOURS WORKEDCALCULATING EMPLOYEE HOURS WORKED

1. Calculate regular hours.

2. Calculate overtime hours.

3. Add Hours Reg and Hours OT columns and enter totals.

4. Add Hours column.

3

4

2

1

Lesson 13-1, page 313Lesson 13-1, page 313

**Round times to nearest quarter hour

Gross Pay (total before deductions)Gross Pay (total before deductions) = Hours X Rate = Hours X Rate

Employee A worked 40 hours and was paid $8.00 an hour.

40 x 8 = $320.00 Gross Pay Employee B worked 40 regular hours and 2

overtime hours at $8.00 an hour.

40 x 8 = $320.00 Regular

2 x 12 = 24.00 Overtime (OT = $8 x 1.5 = $12)

$344.00 Gross Pay

Net Pay = Gross Pay – Deductions

CALCULATING EMPLOYEE TOTAL EARNINGSCALCULATING EMPLOYEE TOTAL EARNINGS

Lesson 13-1, page 314Lesson 13-1, page 3145

1 2

43

3. Enter the rate for overtime.

1. Enter the rate for regular time.

4. Calculate overtime earnings.

OT hours * OT Rate

2. Calculate regular earnings.

Reg hours * Reg rate

5. Calculate Total Earnings.

***AKA***

Gross Pay or Gross Earnings

TTERMS REVIEWERMS REVIEWsalary

pay period

payroll

total earnings

TO DO:

Work Together, pg 315

On your own, pg 315

CHAPTER 13-2: Determining Payroll Tax WithholdingsCHAPTER 13-2: Determining Payroll Tax Withholdings

Payroll taxes: taxes based on payroll of the business Business is required by law to withhold certain

payroll taxes from employee salaries

All are based on employee total earnings must keep accurate and detailed records

– Errors incorrect tax payments state and federal government penalties

Liability for the employer until paid to government

Employee Income Tax:Employee Income Tax:

Must withhold federal income taxes from total earnings

Forwarded periodically to federal government Many states also require state income taxes

withheld

Employer must keep payroll records for:– Federal Government– State Government– County Government– Local Government

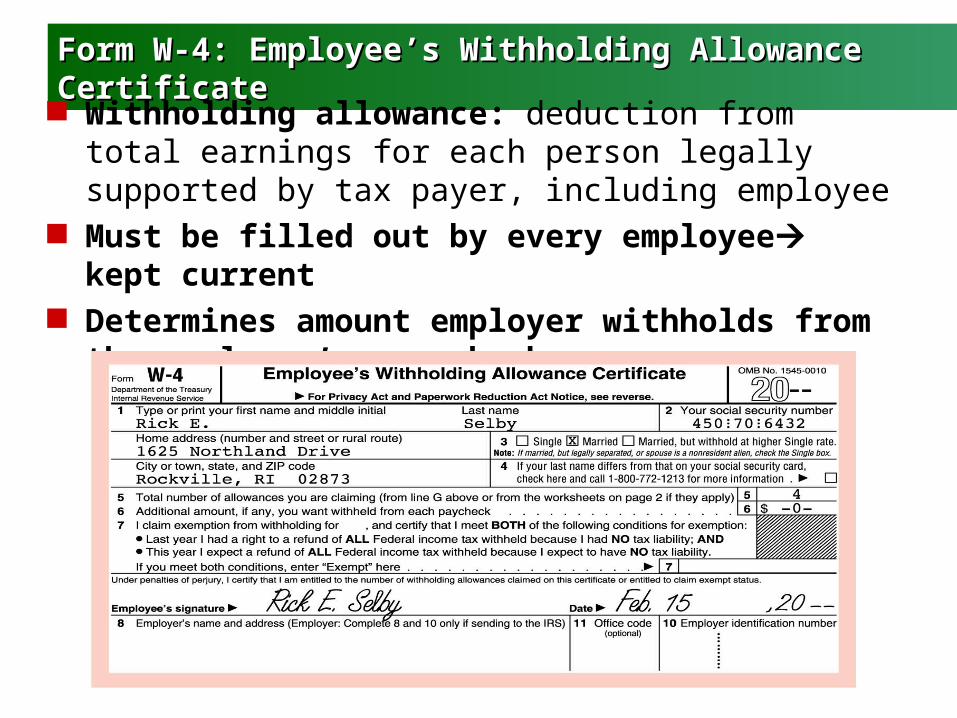

Form W-4: Employee’s Withholding Allowance CertificateForm W-4: Employee’s Withholding Allowance Certificate

Withholding allowance: deduction from total earnings for each person legally supported by tax payer, including employee

Must be filled out by every employee kept current Determines amount employer withholds from the

employee’s pay check.

Five Filing Statuses – to determine amount of tax Five Filing Statuses – to determine amount of tax withheldwithheld

Single Married Married Filing Separately Widow/Widower Head of Household

ITEM 7 on W-4ITEM 7 on W-4 Claiming Exemption from Withholding for certain low-

income, part-time employees Employer would not withhold income tax because you

would owe none at the end of the year. Must STILL fill out W-4 TO qualify:

1. Cannot earn over $7002. Cannot have earned any interest or dividends3. Cannot be claimed by another person4. International student / foreign employee from temporary visa

EMPLOYEE’S WITHHOLDING ALLOWANCE EMPLOYEE’S WITHHOLDING ALLOWANCE CERTIFICATECERTIFICATE

5

1 34

2

3. Marital Status

1. Name and Address 4. Withholding Allowances

2. Social Security Number 5. Signature and Date

EMPLOYEE’S INCOME TAX WITHHOLDING—SINGLE EMPLOYEE’S INCOME TAX WITHHOLDING—SINGLE PERSONSPERSONS

EMPLOYEE’S INCOME TAX WITHHOLDING—MARRIED EMPLOYEE’S INCOME TAX WITHHOLDING—MARRIED PERSONSPERSONS

Lesson 13-2, page 319Lesson 13-2, page 319

63At least But Less than

1,120 1,140

Selby:

Married

$1137.00

4

Payroll Taxes Paid by EmployeePayroll Taxes Paid by Employee

FICA (Federal Insurance Contributions Act)– Social Security 6.5% (old-age, survivors, disability)– Medicare 1.5% (hospital insurance)– Total 8% (paid by both employee AND employer)

Tax Base for 1997 is $65,400 (used for book)2007 - $97,5002008 - $102,000

Medicare – proportional at all levels (no tax base)

Federal Income Tax – Rates are from 15% to 38.6 %– Amount Paid depends on:

• Exemptions claimed• Filing Status • Gross Pay

State Income Tax - PA 2.8% Local Income Tax – Upper Saucon 1% - Lower Saucon 2%

Taxes Paid by EmployerTaxes Paid by Employer

Social Security and Medicare - Same rate as employee

Federal Unemployment – 0.8% (first $7000)

State Unemployment – 5.4% (first $7000)

– (more details later)

EMPLOYEE SOCIAL SECURITY AND MEDICARE TAXEMPLOYEE SOCIAL SECURITY AND MEDICARE TAX

Total Social Security Social SecurityEarnings Tax Rate = Tax Deduction

Total Medicare MedicareEarnings Tax Rate = Tax Deduction

Calculate Social Security Tax Deduction

Calculate Medicare Tax Deduction

$1,137.00 6.5% = $73.91

$1,137.00 1.5% = $17.06

TTERMS REVIEWERMS REVIEWpayroll taxes

withholding allowance

social security tax

Medicare tax

tax base

***************************

TO DO:

Work Together, 321

On your own, 321

Application Problems 13-1, 13-2, pg 331

Chapter 13-3: Preparing Payroll RecordsChapter 13-3: Preparing Payroll Records

Payroll Register: Summarizes Gross & Net Pay and

deductions for all employees for 1 payroll period. Remember: Partners are not employees and are

not paid salaries – how are they paid????

*****Payroll is an expense of the business*****

PAYROLL REGISTERPAYROLL REGISTER

5

1

3

4

2

3. Employee Personal Data

1. Pay Period Date

4. Earnings

2. Payment Date

5. Federal Income Tax

106 8 97

6. Social Security Tax

11 13

12

10. Total Deductions

8. Health Insurance

11. Net Pay

9. Other Deductions

12. Total, Prove, and Rule

7. Medicare Tax

13. Check Number

Voluntary/Other Deductions – Column 8Voluntary/Other Deductions – Column 8

Union dues - U Savings /Retirement – S or R Insurance – Life - L United Way - UW US Savings Bonds - B Company Stock options Health, Travel fund, etc. Anything employer and employee agree upon.

Employee Earnings RecordEmployee Earnings Record

Business form used to record details affecting payments made to each employee

New record prepared each quarter for each employee

Info needed to prepare it is taken from the payroll register

Must send quarterly reports to government agencies showing: – Employee taxable earnings– Taxes withheld

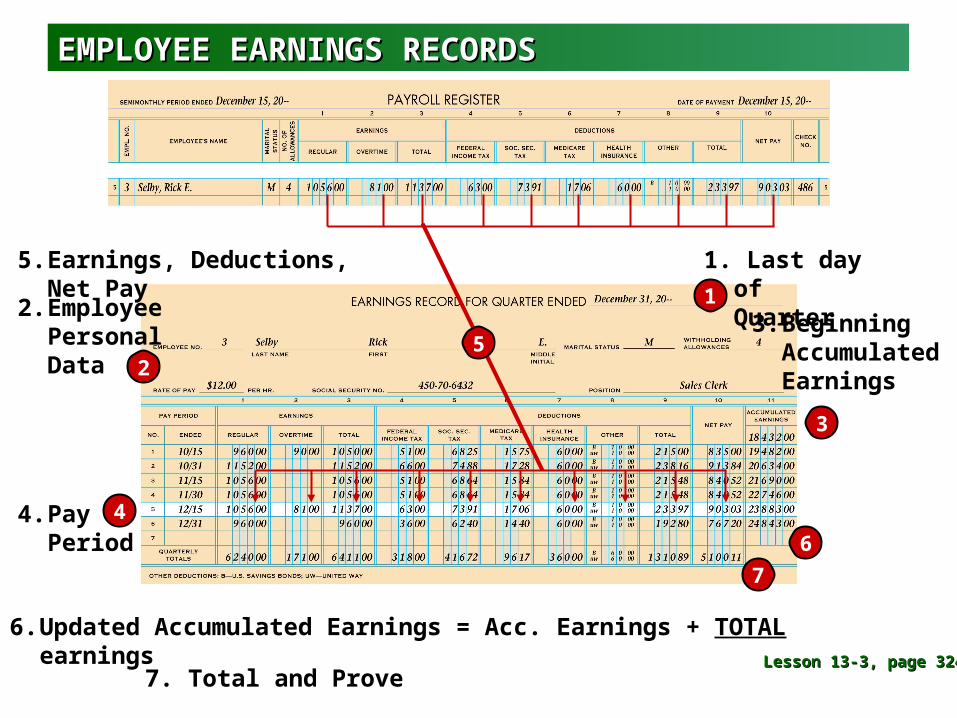

EMPLOYEE EARNINGS RECORDSEMPLOYEE EARNINGS RECORDS

Lesson 13-3, page 324Lesson 13-3, page 324

1

3

4

2

3. Beginning Accumulated Earnings

1. Last day of Quarter

4. Pay Period

5. Earnings, Deductions, Net Pay

6

7

6. Updated Accumulated Earnings = Acc. Earnings + TOTAL earnings

7. Total and Prove

2. Employee Personal Data

5

TTERMS REVIEWERMS REVIEWpayroll register

net pay

employee earnings record

TO DO:

Work Together, pg 326

On your own, pg 326

Lesson 13-3, page 326Lesson 13-3, page 326

Chapter 13-4: Preparing Payroll ChecksChapter 13-4: Preparing Payroll Checks

A separate checking account is set up for payroll.

One check is made out for the TOTAL net wages and deposited into the payroll checking account.

Then individual checks are made to each employee from this account.

Helps to protect and control payroll payments

INFO is taken from payroll register

PAYROLL BANK ACCOUNTPAYROLL BANK ACCOUNT

1

1. Prepare the check stub.

2

2. Prepare the check.

Lesson 13-4, page 327Lesson 13-4, page 327

Voucher checkVoucher check

This is a check with a description of the attached check.

An employer must give an employee a voucher check for his wages.– It must show gross pay (regular and overtime),

deductions, and net pay. Employee's Earnings Record:

– This is a record of one employee’s pay for the entire quarter.

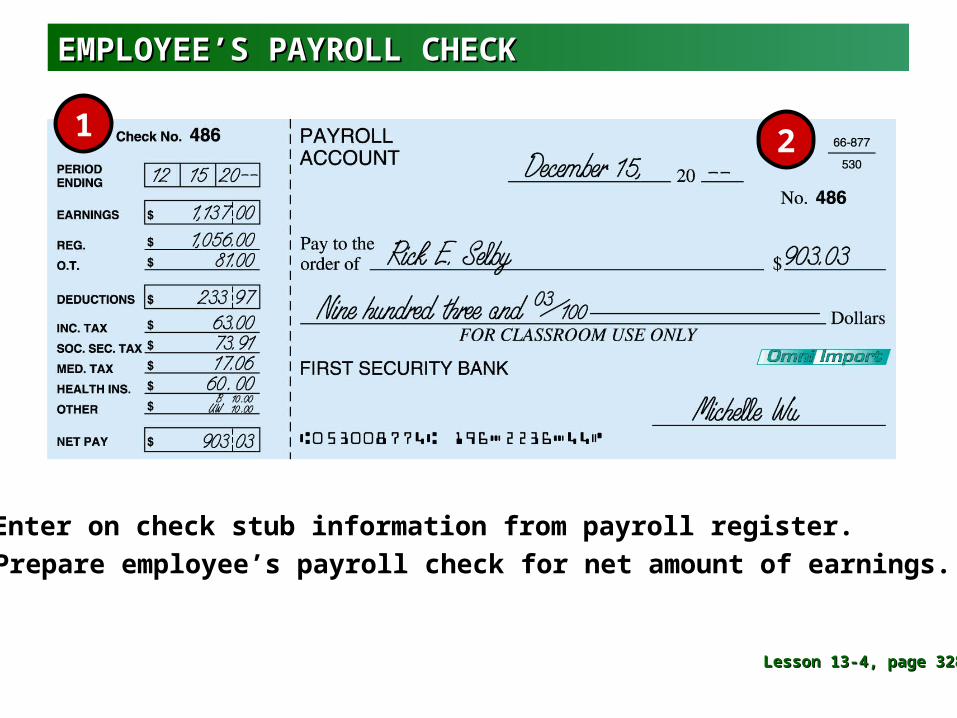

EMPLOYEE’S PAYROLL CHECKEMPLOYEE’S PAYROLL CHECK

1

1. Enter on check stub information from payroll register.

2

2. Prepare employee’s payroll check for net amount of earnings.

Lesson 13-4, page 328Lesson 13-4, page 328

Automatic Check DepositAutomatic Check Deposit

The employee authorizes the employer to deposit his payroll check into a particular checking or savings account.

EFT: Electronic Fund Transfer

A check is never made out; it is a computer transaction.

The employee receives a check stub with payroll information.

TO DO: Work Together, pg 329 On your own, pg 329 Application Problems 13-3, 13-4, pg 331-332