Chapter 13 IAS 7 Statement of Cash flows

17

F1 – Financial reporting CH13 – IAS 7 Statement of Cash flows Page 1 Chapter 13 IAS 7 Statement of Cash flows Chapter learning objectives: Lead Component Indicative syllabus content B3. Apply financial reporting standards when preparing basic financial statements Apply financial reporting standards when preparing a: a. Statement of financial position b. Statement of comprehensive income c. Statement of changes in equity d. Statement of cash flows • IAS 1 — Presentation of Financial Statements • IAS 7 — Statement of Cash Flows

Transcript of Chapter 13 IAS 7 Statement of Cash flows

F1 – Financial reporting CH13 – IAS 7 Statement of Cash

flows

Page 1

Chapter 13

IAS 7 Statement of Cash flows

Chapter learning objectives:

Lead Component Indicative syllabus content

B3. Apply financial

reporting standards

when preparing basic

financial statements

Apply financial reporting standards when

preparing a:

a. Statement of financial position

b. Statement of comprehensive income

c. Statement of changes in equity

d. Statement of cash flows

• IAS 1 — Presentation of

Financial Statements

• IAS 7 — Statement of

Cash Flows

F1 – Financial reporting CH13 – IAS 7 Statement of Cash

flows

Page 2

1. The importance of statements of cash flow

The statement of cash flow shows the inflows and outflows of cash for an entity during the

period.

The statement of cash flow adds another layer of information to support the statement of

profit or loss and the statement of financial position.

Profits are not equal to cash flows. As a result, it is essential to present a statement of cash

flow for users in order to base their decisions upon.

It enables an assessment of the liquidity of a business, its financial adaptability and the

utilisation of its cash resources.

Definitions

F1 – Financial reporting CH13 – IAS 7 Statement of Cash

flows

Page 3

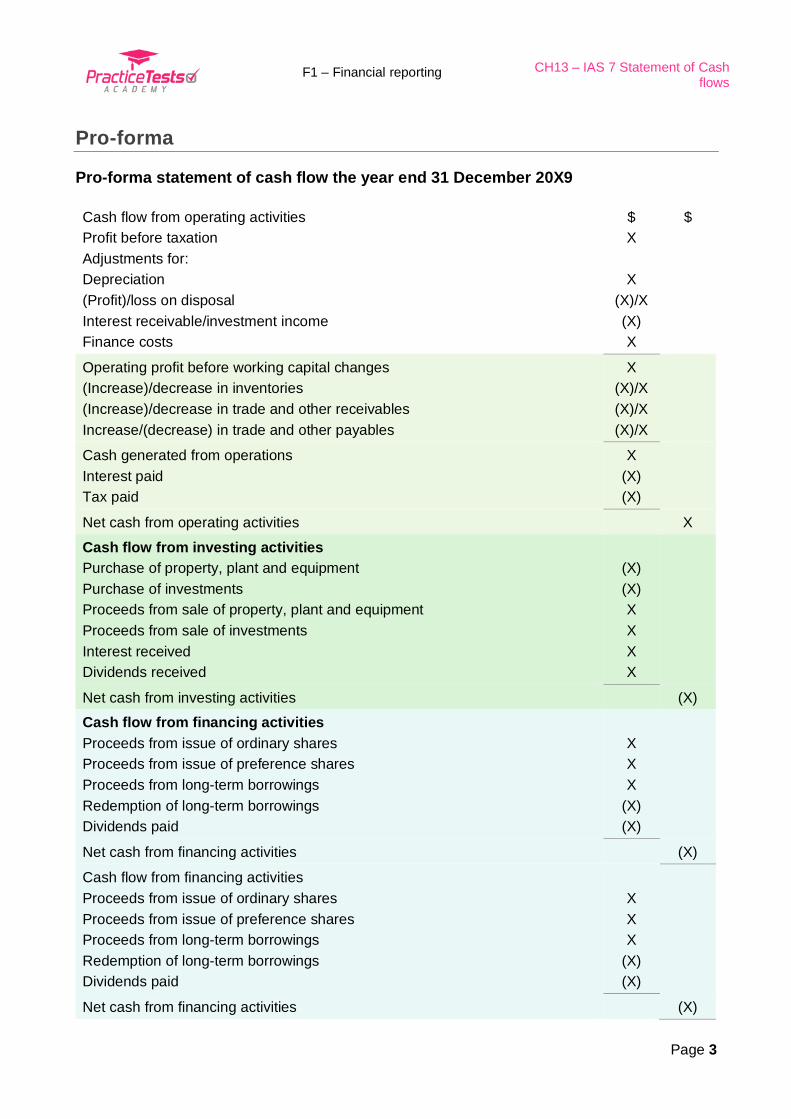

Pro-forma

Pro-forma statement of cash flow the year end 31 December 20X9

Cash flow from operating activities

Profit before taxation

Adjustments for:

Depreciation

(Profit)/loss on disposal

Interest receivable/investment income

Finance costs

$

X

X

(X)/X

(X)

X

$

Operating profit before working capital changes

(Increase)/decrease in inventories

(Increase)/decrease in trade and other receivables

Increase/(decrease) in trade and other payables

X

(X)/X

(X)/X

(X)/X

Cash generated from operations

Interest paid

Tax paid

X

(X)

(X)

Net cash from operating activities X

Cash flow from investing activities

Purchase of property, plant and equipment

Purchase of investments

Proceeds from sale of property, plant and equipment

Proceeds from sale of investments

Interest received

Dividends received

(X)

(X)

X

X

X

X

Net cash from investing activities (X)

Cash flow from financing activities

Proceeds from issue of ordinary shares

Proceeds from issue of preference shares

Proceeds from long-term borrowings

Redemption of long-term borrowings

Dividends paid

X

X

X

(X)

(X)

Net cash from financing activities (X)

Cash flow from financing activities

Proceeds from issue of ordinary shares

Proceeds from issue of preference shares

Proceeds from long-term borrowings

Redemption of long-term borrowings

Dividends paid

X

X

X

(X)

(X)

Net cash from financing activities (X)

F1 – Financial reporting CH13 – IAS 7 Statement of Cash

flows

Page 4

Net increase/(decrease) in cash and cash equivalents

Cash and cash equivalents at beginning of period

X/(X)

X/(X)

Cash and cash equivalents at end of period X/(X)

2. Cash flows from operating activities

Cash flow from operating activities include:

• cash generated from operations

• interest paid

• tax paid (excluded from your F1 knowledge requirements)

Cash generated from operations

• Cash generated from operations includes all day-to-day operating cash flow.

• Numerous cash flows contribute to this figure, for e.g. cash from sales, purchases,

wage payments, receipts from receivables.

The indirect method

(1) Start with profit before tax (PBT) X

(2) Strip out non-cash items from PBT

Depreciation/amortisation/impairments

(Profit)/Loss on disposal

X

(X)/X

(3) Strip out non-operating items from PBT

Interest receivable/investment income

Finance costs

(X)

X

Operating profit before working capital charges X

F1 – Financial reporting CH13 – IAS 7 Statement of Cash

flows

Page 5

(4) Deal with working capital movements

(Increase)/decrease in inventory

(Increase)/decrease in trade receivables

Increase/(decrease) in trade payables

(X)/X

(X)/X

(X)/X

Cash generated from operations X

The direct method

$

Cash receipts from customers

Cash payments to suppliers

Cash payments to employees

Cash payments to expenses

X

(X)

(X)

(X)

Cash generated from operations X/(X)

Comparison of the methods

Test Your Understanding 1: Indirect method

The following information is available for an entity Splatter for the year ended 30 September 20X1:

Statement of Profit or Loss

$000

Revenue 450

Cost of sales (270)

Gross profit 180

Distribution costs (30)

F1 – Financial reporting CH13 – IAS 7 Statement of Cash

flows

Page 6

Administrative expenses (8)

Profit from operations 142

Finance costs (20)

Profit before tax 122

Income tax expense (30)

Profit after tax 92

The total expenses of i.e. cost of sales $270 + distribution costs $30 + administrative expenses $8 can be

analysed as follows:

$000

Wages 75

Auditors remuneration 15

Depreciation 80

Cost of materials used 200

Profit on disposal of non-current assets (50)

Rental income (12)

308

30/09/X1

$000

30/09/X0

$000

Inventories 50 25

Receivables 45 40

Payables (30) (18)

Required:

Produce the section of the statement of cash flows for cash generated from operations using the indirect

method for the year ended 30 September 20X1 in compliance with IAS 7 Statement of Cash Flows.

F1 – Financial reporting CH13 – IAS 7 Statement of Cash

flows

Page 7

Test Your Understanding 2: Direct method

The following information is available for an entity Splatter for the year ended 30 September 20X1:

Statement of Profit or Loss

$000

Revenue 450

Cost of sales (270)

Gross profit 180

Distribution costs (30)

Administrative expenses (8)

Profit from operations 142

Finance costs (20)

Profit before tax 122

Income tax expense (30)

Profit after tax 92

The total expenses of i.e. cost of sales $270 + distribution costs $30 + administrative expenses $8 can be

analysed as follows:

$000

Wages 75

Auditors remuneration 15

Depreciation 80

Cost of materials used 200

Profit on disposal of non-current assets (50)

Rental income (12)

308

30/09/X1 30/09/X0

F1 – Financial reporting CH13 – IAS 7 Statement of Cash

flows

Page 8

$000 $000

Inventories 50 25

Receivables 45 40

Payables (30) (18)

Required:

Using the information for Splatter in the previous illustration, produce the section of the statement of

cash flows for cash generated from operations using the direct method for the year ended 30 September

20X1 in compliance with IAS 7 Statement of Cash Flows.

Other cash flows from operating activities

Other cash flow that is considered as cash flow from operating activities may include:

• Interest paid.

• Income tax paid (accounting for this is not examinable).

F1 – Financial reporting CH13 – IAS 7 Statement of Cash

flows

Page 9

Test Your Understanding 3: Interest paid

Below are extracts from the financial statements of an entity Pincer:

Statement of profit or loss and other comprehensive income for the year ended 31 March 20X1

$m

Profit from operations 140

Interest receivable 80

Finance cost (55)

Profit before tax 165

Statement of financial position 31 March 20X1 31 March 20X0

$m $m

Current liabilities

Interest payable 244 311

Required:

What is the interest paid shown under cash flows from operating activities for Pincer during the year

ended 31 March 20X1?

F1 – Financial reporting CH13 – IAS 7 Statement of Cash

flows

Page 10

3. Cash flows from investing activities

Cash inflows from investing activities may include:

• interest received

• dividends received

• proceeds from the sale of non-current assets

Cash outflows from investing activities may include:

• purchases of non-current assets

Interest/Dividends received

Cash paid to acquire non-current assets

The cash flow for non-current assets should be calculated using the following proforma:

F1 – Financial reporting CH13 – IAS 7 Statement of Cash

flows

Page 11

Cash received on disposal of non-current assets

You may have to calculate the proceeds by working backwards from the profit or loss on

disposal as follows:

Test Your Understanding 4: Cash from investing activities

Below are extracts from the financial statements of an entity Pincer:

Statement of profit or loss and other comprehensive income for the year ended 31 March 20X1:

$m

Profit from operations 140

Statements of financial position 31 March 20X1 31 March 20X0

$m $m

Assets

Non-current assets

Property, plant and equipment 1,050 650

Equity

Capital and reserves

Share capital 30 25

Share premium 450 380

Revaluation reserve 260 0

Retained profit 115 30

F1 – Financial reporting CH13 – IAS 7 Statement of Cash

flows

Page 12

Additional information:

Profit from operations is after charging depreciation on the property, plant and equipment of $22 million.

The revaluation reserve relates wholly to property, plant and equipment.

During the year ended 31 March 20X1, plant and machinery costing $1,464 million, which had a carrying amount

of $424 million, was sold for $250 million.

Required:

What is the amount paid for purchases of property, plant and equipment shown under cash flows from

investing activities for Pincer during the year ended 31 March 20X1?

4. Cash flows from financing activities

Proceeds from new share issues

The proceeds from share issues will be calculated by looking at the movement on the

share capital and share premium accounts in the SOFP.

F1 – Financial reporting CH13 – IAS 7 Statement of Cash

flows

Page 13

Proceeds/repayments from loans and debentures

The proceeds/repayment of loans/debentures will be calculated by looking at the

movements on the loan/debenture accounts in the SOFP.

The dividend payment can either be found in the SOCIE or by looking at the movement on

the retained earnings account as follows:

Test Your Understanding 5: Cash flow from financing activities

Below are extracts from the financial statements of an entity Pincer:

Statement of profit or loss and other comprehensive income for the year ended 31 March 20X1

$m

Profit for the year 140

Statements of financial position 31 March 20X1 31 March 20X0

$m $m

Equity

Capital and reserves

Share capital 30 25

Share premium 450 380

Revaluation reserve 260 0

Retained profit 115 30

F1 – Financial reporting CH13 – IAS 7 Statement of Cash

flows

Page 14

Required:

What are the amounts for:

• Cash received from issues of shares, and

• Dividends paid

shown under cash flows from financing activities for Pincer during the year ended 31 March 20X1?

5. Solutions to Test Your Understanding

Test Your Understanding 1: Indirect method

$000

Cash flows from operating activities

Profit before tax 122

Depreciation 80

Profit on disposal of non-current assets (50)

Finance costs 20

Operating profit before working capital changes 172

Increase in inventories (50 – 25) (25)

Increase in trade receivables (45 – 40) (5)

Increase in trade payables (30 – 18) 12

Cash generated from operations 154

Explanation:

Both inventory and receivable balances are increasing, hence a reduction in cash, i.e. the more money tied up

in inventory or the more money owed by receivables the less cash we have available in the bank. Therefore,

this is shown as a decrease in the statement.

Payables also increase but this means we have an increase in cash, i.e. the more money we owe suppliers, the

longer we are keeping the cash in the bank.

F1 – Financial reporting CH13 – IAS 7 Statement of Cash

flows

Page 15

Test Your Understanding 2: Direct method

Splatter Statement of cash flows for the year ended 30 September 20X1

$000

Cash flows from operating activities

Cash receipts from customers (W1) 445

Rental income 12

Cash payments to suppliers (W2) (213)

Cash payments to employees (75)

Cash payments for expenses (15)

Cash generated from operations 161

Working 1:

Cash receipts from customers

$000

Opening receivables 40

Sales revenue 450

Closing receivables (45)

Cash received from customers 445

Working 2:

Cash payment to suppliers

$000

Opening inventory 25

Purchases (bal. fig.) 225

Closing inventory (50)

Cost of materials used 200

F1 – Financial reporting CH13 – IAS 7 Statement of Cash

flows

Page 16

$000

Opening payables 18

Purchases (above) 225

Closing payables (30)

Payments to suppliers 213

Test Your Understanding 3: Interest paid

Interest paid is $122m.

Interest paid ($m)

Bank (bal. fig.) 122 Bal. b/d 311

Bal. c/d (SOFP) 244 Profit or loss (finance costs) 55

366 366

Test Your Understanding 4: Cash from investing activities

Purchases of property, plant and equipment = $586m.

Property, Plant and Equipment ($m)

Bal. b/d 650 Depreciation 22

Bank (bal. fig.) 586 Disposal 424

Revaluation 260 Bal. c/d 1,050

1,496 1,496

Test Your Understanding 5: Cash flow from financing activities

Issue of shares = $75m

Dividend paid = ($55m)

Share capital and share premium ($m)

SC balance b/d 30 SC balance b/d 25

SP balance c/d 450 SP balance b/d 380

Cash from share issue (β) 75

480 480

F1 – Financial reporting CH13 – IAS 7 Statement of Cash

flows

Page 17

Retained earnings ($m)

Dividend paid (β) 55 Balance b/d 30

Balance c/d 115 Profit for the year 140

170

6. Chapter summary

![IAS 7 : STATEMENT OF CASH FLOWS - wirc-icai.org1].pdf · How Statement of Cash Flow is Important ? COMPILED BY: MR. YAGNESH DESAI. ... ELEMENTS OF FINANCING CASH FLOW COVERED IN PARA](https://static.fdocuments.in/doc/165x107/5b14a5fa7f8b9a257c8e3b05/ias-7-statement-of-cash-flows-wirc-icaiorg-1pdf-how-statement-of-cash.jpg)