Chapter 12 International Financing and National Capital Markets.

24

Chapter 12 International Financing and National Capital Markets

-

Upload

erik-tyler -

Category

Documents

-

view

233 -

download

5

Transcript of Chapter 12 International Financing and National Capital Markets.

Chapter 12

International Financing and National Capital Markets

Chapter 12: International Financing and National Capital Markets 2

Chapter 12 Outline

A. Corporate Sources and Uses of Funds

B. National Capital Markets as International Financial Centers

C. Eurocurrency Market

D. Eurobonds

E. Asiacurrency Market

F. Project Finance

Chapter 12: International Financing and National Capital Markets 3

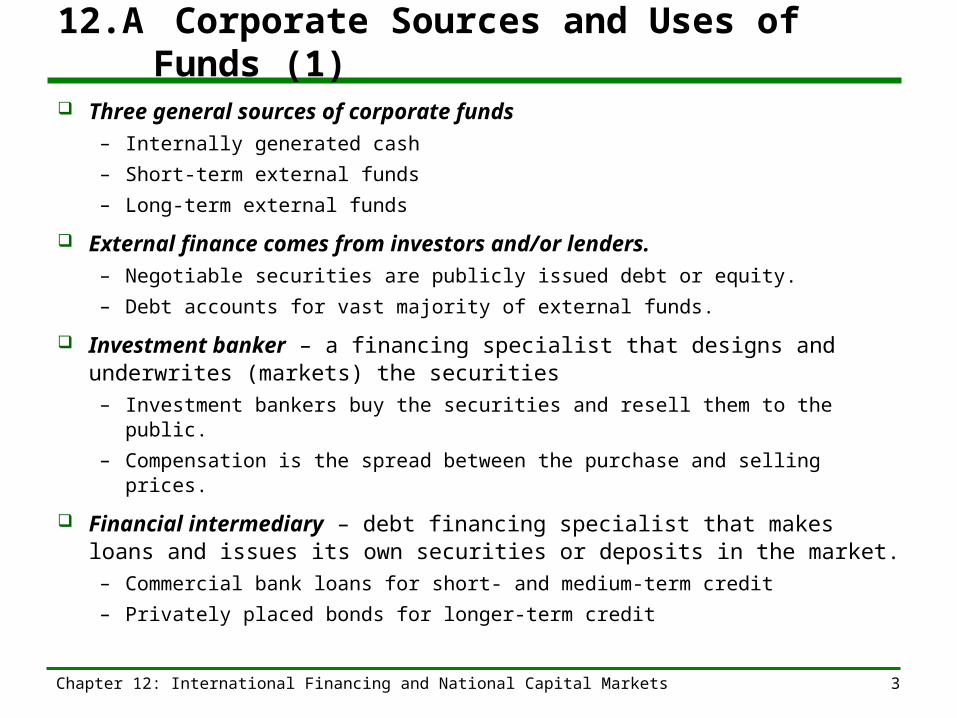

12.A Corporate Sources and Uses of Funds (1)

Three general sources of corporate funds– Internally generated cash

– Short-term external funds

– Long-term external funds

External finance comes from investors and/or lenders.– Negotiable securities are publicly issued debt or equity.

– Debt accounts for vast majority of external funds.

Investment banker – a financing specialist that designs and underwrites (markets) the securities– Investment bankers buy the securities and resell them to the public.

– Compensation is the spread between the purchase and selling prices.

Financial intermediary – debt financing specialist that makes loans and issues its own securities or deposits in the market.– Commercial bank loans for short- and medium-term credit

– Privately placed bonds for longer-term credit

Chapter 12: International Financing and National Capital Markets 4

12.A Corporate Sources and Uses of Funds (2)

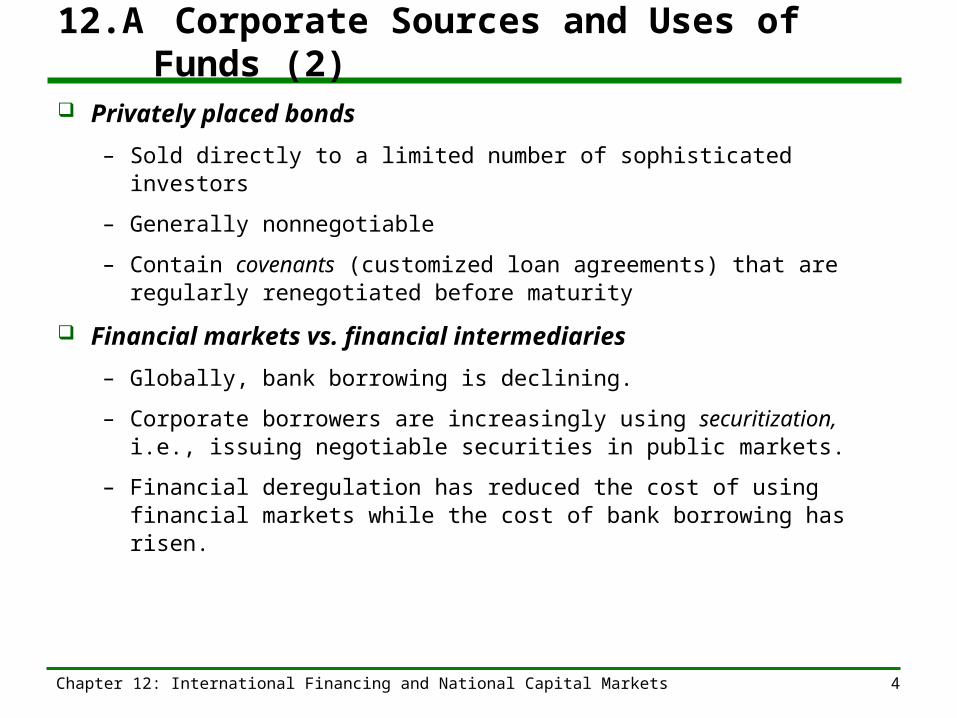

Privately placed bonds

– Sold directly to a limited number of sophisticated investors

– Generally nonnegotiable

– Contain covenants (customized loan agreements) that are regularly renegotiated before maturity

Financial markets vs. financial intermediaries

– Globally, bank borrowing is declining.

– Corporate borrowers are increasingly using securitization, i.e., issuing negotiable securities in public markets.

– Financial deregulation has reduced the cost of using financial markets while the cost of bank borrowing has risen.

Chapter 12: International Financing and National Capital Markets 5

12.A Corporate Sources and Uses of Funds (4)

Corporate governance – two general models

– Anglo-Saxon (“AS” or market-oriented) model used in U.S. and U.K.

• Institutional investors play a critical role and exert a high level of corporate control.

• Equity finance is important.

• Corporate objective: maximize shareholder value

• High return on capital is stressed

– Continental European and Japanese (“CEJ”) model

• Banks play a critical role.

• Share ownership and control are concentrated in banks and other firms.

• Corporate decision-making is influenced heavily by close personal relationships between corporate leaders who sit on each other’s boards of directors.

• Less focus on return on capital

Chapter 12: International Financing and National Capital Markets 6

12.A Corporate Sources and Uses of Funds (5)

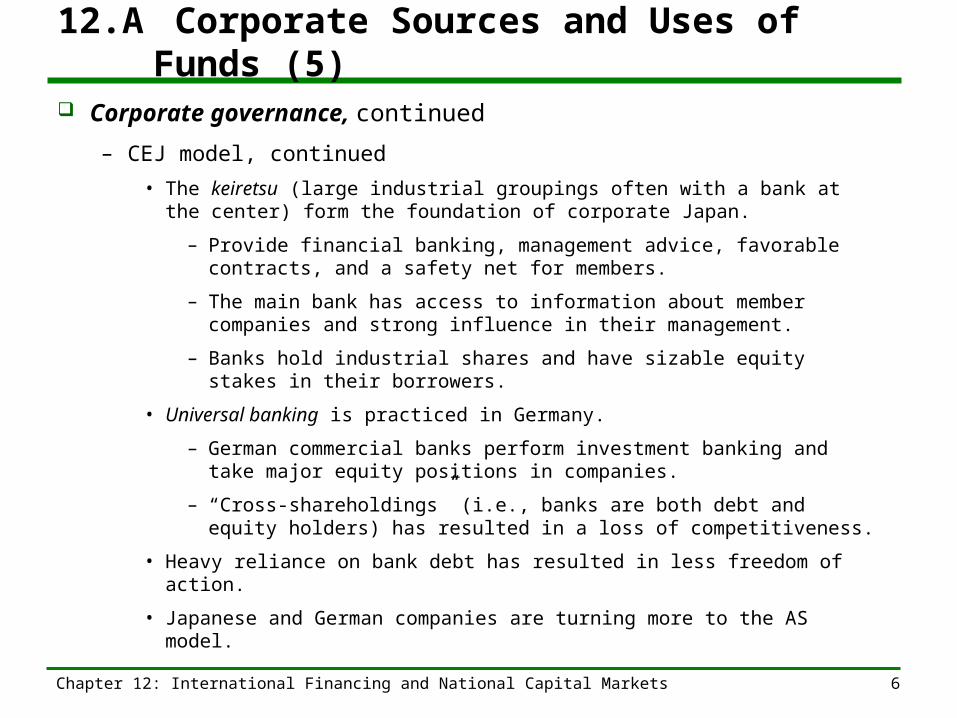

Corporate governance, continued

– CEJ model, continued

• The keiretsu (large industrial groupings often with a bank at the center) form the foundation of corporate Japan.

– Provide financial banking, management advice, favorable contracts, and a safety net for members.

– The main bank has access to information about member companies and strong influence in their management.

– Banks hold industrial shares and have sizable equity stakes in their borrowers.

• Universal banking is practiced in Germany.

– German commercial banks perform investment banking and take major equity positions in companies.

– “Cross-shareholdings” (i.e., banks are both debt and equity holders) has resulted in a loss of competitiveness.

• Heavy reliance on bank debt has resulted in less freedom of action.

• Japanese and German companies are turning more to the AS model.

Chapter 12: International Financing and National Capital Markets 7

12.A Corporate Sources and Uses of Funds (6)

Globalization of financial markets

– Advances in communications and technology combined with deregulation have reduced transaction costs and created a global financial market.

– Competition among key financial centers and institutions has skyrocketed and further reduced the cost of issuing new securities.

– Regulatory arbitrage draws users of capital markets to the financial centers with the lowest regulatory standards and thus the lowest costs.

Financial innovation

– Enables companies to tap previously inaccessible markets and permits investors and issuers to optimize tax loopholes.

– To the extent that a firm can design a security that appeals to a capital market niche, it can attract funds at a lower cost than the market’s required return on securities of comparable risk.

Chapter 12: International Financing and National Capital Markets 8

International financial markets

– Political stability and minimal government intervention are necessary to become a major international financial center.

– The most important global financial centers are in London, Tokyo, and New York.

– The domestic markets in Switzerland, Luxembourg, Hong Kong, the Bahamas, and Bahrain serve as financial entrepôts (channels through which foreign funds pass).

Foreign access to domestic markets

– MNCs have greater latitude in accessing a variety of local money markets than domestic firms.

– Money raised in local markets is often limited to local uses through exchange controls.

– However, MNCs can transfer funds using a variety of financial channels.

12.B National Capital Markets as International Financial Centers (2)

Chapter 12: International Financing and National Capital Markets 9

Foreign access to domestic markets, continued

– Foreign equity market, continued

• Companies must meet often-stringent accounting and disclosure practices (such as in the U.S.) to be listed on a foreign exchange.

• Rule 144A allows qualified institutional investors to trade in unregistered private placements (equity and debt), attracting foreign companies that would not enter the U.S. market given the reporting requirements.

– Global shares

• Shares of a non-U.S. company listed and traded in the same form on any market in the world

• Tracked in a single global registry

• Traded in the home currency of each market

12.B National Capital Markets as International Financial Centers (5)

Chapter 12: International Financing and National Capital Markets 10

Eurocurrency – a dollar (Eurodollar) or other freely convertible currency deposited in a bank outside its country of origin. (The prefix euro is not related to the euro currency.)

Eurobank – a foreign bank or foreign branch of a domestic U.S. bank that accepts deposits and makes loans in foreign countries.

The Eurocurrency market enables investors to hold short-term claims on commercial banks, which then act as intermediaries to transform deposits into long-term claims on final borrowers.

By operating in Eurocurrencies, banks and suppliers of funds avoid certain regulatory costs and restrictions, including

– Reserve requirements that lower a bank’s earning asset base;

– Special charges and taxes on domestic banking transactions; e.g.,FDIC fees;

– Requirements to lend money to certain borrowers at concessionary rates;

– Interest rate ceilings on deposits or loans that inhibit competition for funds;

– Rules or regulations that restrict competition among banks.

12.C Eurocurrency Market (1)

Chapter 12: International Financing and National Capital Markets 11

Eurocurrency market versus domestic banking operations

– The Eurocurrency market involves a chain of deposits and a chain of borrowers and lenders.

• There is a chain of ownership between the original dollar depositor and the U.S. bank.

• There is a changing control over the deposit and the use to which the funds are put.

– Domestic banking operations are typically characterized by an owner of dollars depositing the dollars in a bank, with the bank controlling the use of the funds until they are withdrawn.

– The majority of Eurocurrency transactions involve transferring control of deposits from one Eurobank to another.

12.C Eurocurrency Market (3)

Chapter 12: International Financing and National Capital Markets 12

Eurocurrency loans

– Loans are made on a floating-rate basis, typically set at a fixed margin above LIBOR.

– The bank’s spread is based on the borrower’s perceived riskiness and can range from 15 to 300 basis points.

– Maturity ranges from 3 to 10 years.

– If a loan is made by a syndicate of banks, a syndication fee of 0.25% to 2% of the loan value is charged.

– The drawdown period and repayment period vary by the borrower’s needs.

– Borrowers are mainly concerned about the effective interest rate (all-in cost) on their loans.

12.C Eurocurrency Market (4)

Chapter 12: International Financing and National Capital Markets 13

Eurocurrency loans, continued

– Example: compute the loan proceeds, first semiannual payment, and effective annual cost of a Eurocurrency loan

• Loan = €250 million, five-year, euro-denominated Eurocurrency loan with a syndicate of banks and a syndication fee of 2.0% and interest rate of LIBOR6 (initially 5.5%) + 1.75%.

• Proceeds = €250 million – (€250 million * 0.02) = €245 million

• First semiannual payment = [(0.055 + 0.0175) / 2] * €250 million = €9,062,500

• Effective annual interest rate for first six months =€9,062,500 / €245,000,000 * 2 * 100 = 7.4%

– Multicurrency clauses – the borrower has the right to switch from one currency to another on any rollover or reset date, enabling the borrower to match currencies on cash inflows and outflows based on expected exchange rate changes.

12.C Eurocurrency Market (5)

Chapter 12: International Financing and National Capital Markets 14

Relationship between domestic and Eurocurrency money markets

– The presence of arbitrage activities ensures a close relationship between interest rates in national and international (Eurocurrency) money markets.

– Currency controls or risk explain any substantial differences between domestic and external interest rates.

• If exchange controls are effective, the national money market can be isolated or segmented from its international counterpart.

• If future exchange controls are expected, creating the possibility that the lender or borrower will not be able to transfer funds across a border, interest rate differentials may result.

12.C Eurocurrency Market (6)

Chapter 12: International Financing and National Capital Markets 15

Relationship between domestic and Eurocurrency money markets

– Eurocurrency spreads are generally narrower and lower than those in domestic money markets.

• Lending rates can be lower because

– Regulatory expenses that raise costs and lower returns on domestic transactions do not exist in the Eurocurrency market;

– Most borrowers are well known, reducing the cost of information-gathering and credit analysis;

– Eurocurrency lending is characterized by high volumes, resulting in lower margins and transaction costs; and

– Eurocurrency lending often takes place out of tax-haven countries, providing higher after-tax returns.

• Deposit rates can be higher because

– They must be to attract domestic deposits;

– Eurobanks can afford to pay higher rates based on lower regulatory costs;

– Eurobanks are not subject to the interest rate ceilings present in many countries; and

– A larger percentage of deposits can be loaned out.

12.C Eurocurrency Market (7)

Chapter 12: International Financing and National Capital Markets 16

Eurobonds are similar to public debt sold in domestic markets.

– Consist largely of fixed-rate, floating-rate, and equity-related debt.

– Self-regulated by the Association of International Bond Dealers.

70% of Eurobonds are swaps

The growing presence of sophisticated investors willing to arbitrage between the domestic dollar and Eurodollar bond markets has eliminated most interest disparity that once existed between domestic bonds and Eurobonds.

Issues are arranged through an underwriting group and often involve more than a hundred banks for an issue as small as $25 million.

About 75% of Eurobonds are dollar denominated.

12.D Eurobonds (1)

Chapter 12: International Financing and National Capital Markets 17

Fixed-rate Eurobonds

– Coupons are typically paid annually.

– The interest rate is the internal rate of return on the bond (the discount rate that equates the present value of future interest and principal payments to the net proceeds received).

– Conversion of annual yield to semiannual yield

12.D Eurobonds (2)

Semiannual yield = (1 + annual yield)1/2 - 1

Annual yield = (1 + semiannual yield)2 - 1

– Conversion of semiannual yield to annual yield

Chapter 12: International Financing and National Capital Markets 18

12.D Eurobonds (3)

Floating-rate Eurobonds (FRNs)

– The interest rate is a fixed amount above a floating reference rate, typically LIBOR (e.g., LIBOR3 + 0.5%), and is reset at regular intervals equaling the maturity of LIBOR used (e.g., if LIBOR3 is used, interest is reset every 3 months).

– Inverse floaters – FRNs with coupons that move in the opposite direction of the reference rate (e.g., 12% - LIBOR3).

Eurobond retirement

– Sinking fund – requires the borrower to retire a fixed amount of bonds annually after a specified number of years.

– Purchase fund – the bonds are retired only if the market price is below the issue price.

– Call provisions give the borrower the option to retire the bonds before maturity if interest rates decline sufficiently. Eurobonds with call provisions typically require a call premium and higher interest rates.

Chapter 12: International Financing and National Capital Markets 19

12.D Eurobonds (4)

Why the Eurobond market exists

– The Eurobond market is largely unregulated and untaxed.

• A relatively free flow of capital among countries attracts international investors.

• MNCs can raise funds more quickly and flexibly than at home.

– Eurobonds are issued in bearer, or unregistered, form, meaning the bond owners are anonymous.

The cost advantage of Eurobonds has eroded somewhat since regulatory relaxation in the U.S., Japan, and England.

– In the U.S., the shelf registration procedure enables certain companies to bypass some complex securities laws when issuing new securities.

– Rule 144A enables companies to issue bonds simultaneously in Europe and the U.S., blurring the distinction between the U.S. bond market and its Eurobond equivalent.

Chapter 12: International Financing and National Capital Markets 20

Eurobonds versus Eurocurrency loans

– Cost of borrowing

• Eurobonds are issued in both fixed- and floating-rate forms. Fixed-rate bonds are useful for exposure management because long-term currency inflows can be offset with known long-term outflows in the same currency.

• Eurocurrency loan interest rates are variable. When rates decline, borrower costs decline; when rates increase, borrower costs increase.

– Maturity – Eurobonds have longer maturities.

– Size of issue – the volume of Eurobond offerings exceeds that of global bank lending; sizes and prices of Eurobond financings are expanding.

12.D Eurobonds (5)

Chapter 12: International Financing and National Capital Markets 21

Eurobonds versus Eurocurrency loans, continued

– Flexibility

• Eurobonds

– Funds are drawn down in one sum on a fixed date and repaid on a fixed schedule unless the borrower pays a prepayment penalty.

– Switching the denomination involves a costly refunding and reissuing process.

• Eurocurrency loan

– The drawdown can be staggered to fit the borrower’s needs with a fee of about 0.5% per annum paid on the unused portion and can be prepaid without penalty.

– A Eurocurrency loan with a multicurrency clause enables the borrower to switch currencies on any rollover date.

– Speed

• Eurocurrency market – funds can be raised in as little as two to three weeks.

• Eurobonds – financing takes more time, but the difference is becoming less significant.

12.D Eurobonds (6)

Chapter 12: International Financing and National Capital Markets 22

Euronotes

– Note issuance facility (NIF) – a low-cost substitute for syndicated credits that allows borrowers to issue their own short-term Euronotes.

– NIFs have features of both the U.S. commercial paper market and U.S. commercial lines of credit.

• Like commercial paper, notes under NIFs are unsecured, short-term debt (also known as Euro-commercial paper or Euro-CP) generally issued by MNCs with excellent credit ratings.

• Like lines of credit, NIFs generally include multiple pricing components for various contract features, including a market-based interest rate and participation, facility, and underwriting fees.

– Revolving underwriting facility (RUF) – a NIF that includes underwriting services and gives borrowers long-term continuous access to short-term money underwritten by banks at a fixed rate.

12.D Eurobonds (7)

Chapter 12: International Financing and National Capital Markets 23

Euronotes, continued

– Euronote pricing

• In lieu of a coupon rate, Euronotes are sold at a discount from face value.

• The yield is usually quoted on a discount basis from its face value.

– Euro-medium term notes (Euro-MTNs)

• Can be offered in small amounts; in different maturities, currencies, seniority, and security; and on a daily basis.

• Issuers can thus take advantage of changes in the yield curve and of changing investor needs.

• Maturities are typically from 5 to 30 years. However, increasing issues with maturities of less than one year are negatively impacting the Euro-CP market.

• Euro-MTNs are typically underwritten in batches of more than $50 million.

12.D Eurobonds (8)

Chapter 12: International Financing and National Capital Markets 24

Located in Singapore due to relaxed financial controls and taxes.

Primary economic functions

– Channel investment dollars to rapidly growing Southeast Asian countries

– Provide deposit facilities for investors with excess funds

Dragon bond – Asiabond counterpart to the Asiadollar market.

– Denominated in a foreign currency, usually dollars, but launched, priced, and traded in Asia.

– The market has slumped because Asian borrowers with good international credit ratings can raise funds with longer maturities and at lower cost in Europe or the U.S.

12.E Asiacurrency (Asiadollar) Market