Chapter 1 RE

62

FIN 338 Real Estate Finance G. Jason Goddard, MBA Fall 2014

Transcript of Chapter 1 RE

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 1/62

FIN 338Real Estate Finance

G. Jason Goddard, MBA

Fall 2014

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 2/62

This is your Book….

Published July 31, 2012

http://www.springer.com/business+%26+management/finance/book/978-3-642-23526-9

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 3/62

Welcome!

You have chosen an interesting and fun

elective in Finance! We will explore the wonderful world of

(investment) real estate finance!

We will discuss the perspectives of the real

estate investor as well as the commerciallender in this course.

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 4/62

Session Plan

Introductions Review of Syllabus Contact Information Laying the Framework Chapter One

– Property rights

– Various forms of estates – Title Assurance – Introducing QQD – Global Housing Boom Case

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 5/62

Introductions

Full Name: George Jason Goddard

Preferred Name: Jason Contact Phone Numbers: See Syllabus

Contact Email Addresses: See Syllabus

Major: Finance Expectations of Course: See Syllabus

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 6/62

My Career at Wachovia/Wells Fargo

Started in 1995, after receiving undergraduatedegree from UNCG, with a finance concentration

Spent 7 years in centralized small business lendinggroup – Commercial loans up to $500,000.00.

Have been a senior commercial lender for

Commercial Real Estate for the past 12 years – Investor real estate loans up to $5,000,000.

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 7/62

Nuts and Bolts of Syllabus

Three Tests – First two tests are MC TF and Problems (20% each)

– Final exam will be an applied exam choosing between realestate investment alternatives using the income approachvaluation model (25%)

One Investment Analysis Paper (20%)

– Either completed individually or in groups (max 3 members)

Class Attendance will affect the outcome of yourassignments & your final grade (15%)

Class Participation Counts (especially for fencesitters) !!

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 8/62

Required Calculator

You will need to begin using a Hewlett Packard 10 Bor 10 B II – Only difference is addition of a key for statistics

Essentially the same calculator

– You can use any other financial calculator with which youare comfortable

You will be required to create your own directcapitalization and DCF spreadsheets in Excel for usein our case studies, investment paper, and finalexam. – Spreadsheets are due after our second exam (for class on Nov. 11)

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 9/62

Exam Dates

Exam I: Sept. 23 (20% of grade) – The first two exams will be multiple choice and problems

– This exam will cover chapters 1-4

Exam II: Nov. 4 (20% of grade) – This exam will cover chapters 5-7, 11 & 12

Final Exam: Dec. 10 (25% of grade)

– This will be an application based exam for chapters 8-10 – You will determine the value of two investment properties and

recommend which is the better investment and why.

– The entire course will culminate with this final exam.

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 10/62

Investment Analysis Paper

Find existing investment property for sale

Use methods discussed in course to analyzeand recommend for purchase

Paper is 20% of grade

Maximum of 5 pages in length

Complete individually or in groups (3 max) Due on Dec. 2

Let me know of any problems…

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 11/62

Class Contribution

This represents 15% of your final grade.

This can be earned via: – Class Attendance

– Participation in Class Discussions

– Participation in Case Study Analysis

– WFU Student Housing Occupancy Study Off-campus options for WFU students

– Discussion of One Current Event Article Duringthe Semester

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 12/62

WFU Student Housing Occupancy

Study

You will be required to complete a worksheet thatpertains to one area off-campus (i.e. not on WFU’scampus) student housing property – Based on interview with property manager – Up to two pages in additional commentary by you on your

perceptions of the property, management ability, etc. – Get a copy of the apartment brochure during your visit

The goal is to better understand the market

occupancy and rental rates for Student Housing nearWFU – Apartments that either fully or partially house WFU students

are eligible for this survey

This is due on Oct. 28

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 13/62

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 14/62

Article Discussion

Dollar Store

Consolidation Ultra-Green Building

Sue those Banks!

http://science.time.com/2012/06/20/silver-bullitt/

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 15/62

Chapter One

Real Estate Defined: – Real: Realty—which is land and improvements

This differs from ―personalty‖ which is moveable thingssuch as cars, stocks, etc.

– Estate: extent to which rights and interests in realestate are owned

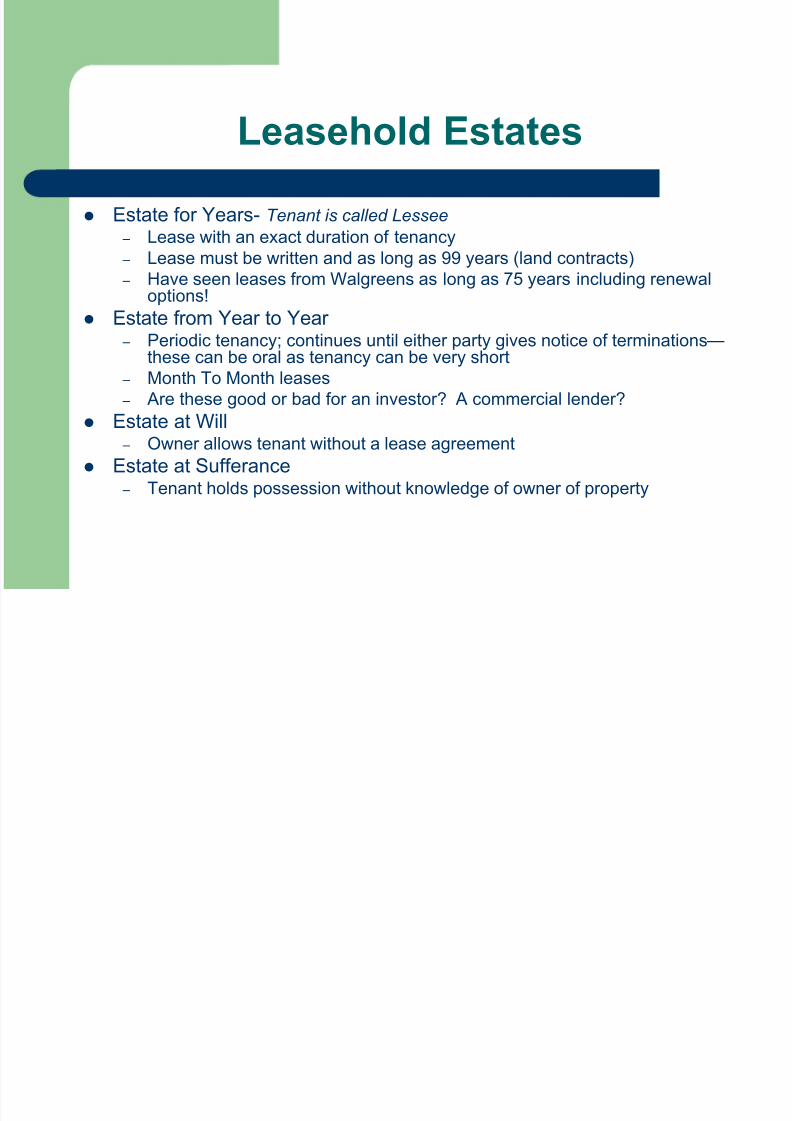

– Two Main Types of Estates: Freehold Estates- Lasts indefinitely

Leasehold Estates- expires on a definite date; right topossess & use (lease) property owned by another

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 16/62

Development of Property Rights

In order for the proper conveyance of a

property from one party to another thereneeds to be:

– A survey system that covers entire U.S.

– A catalogued system of ownership for real estate

– We certainly have these systems now, but back inthe late 1700s, this system did not yet exist. Most legal landholders during this time where individuals

who were deeded land by the British Crown.

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 17/62

Making a System out of Nothing

During the early 1800s, the majority of property ownership wasobtained via illegal methods such as:

Squatter’s Rights – ―any who desired should have right to settle on it‖

Tomahawk Rights – Land was claimed by improvements made by settlers (cutting

trees, planting crops etc.)

Concept of Preemption – Settler could buy land that they improved before it was offered for

sale…the U.S. Government realized that if the young country wasto survive, the majority of ―illegal landholders‖ had to be broughtinto the legal system of real estate ownership

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 18/62

The Importance of Property Rights

―The Mystery of Capital‖ – By Hernando De Soto, Peruvian Economist

Many Third World Nations do not have―legal‖ public ownership of land or haveprocedures for ownership that are verycomplicated

Many poor citizens have ―dead capital‖ – Land cannot be transferred or used as collateral

for obtaining credit

– Land reform is key to economic development

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 19/62

Overly Complicated Systems...

Philippines – 25 years to ―formalize‖ urban property (168 steps)

Egypt – 14 years to access desert land for construction (71 steps, 31

entities)

Haiti

– 12 years to obtain a sales contract following a 5 year landlease (111 steps)

Peru – One year to register a business and 5 stages to form a

legally owned home (207 steps in first stage)

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 20/62

How Much Dead Capital?

57%53%

68%

92%

67%

81%

97%

83%

0%

10%

20%

30%

40%

50%

60%

70%80%

90%

100%

Urban Rural

Philippines

Peru

Haiti

Egypt

“The Mystery of Capital” by Hernando DeSoto

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 21/62

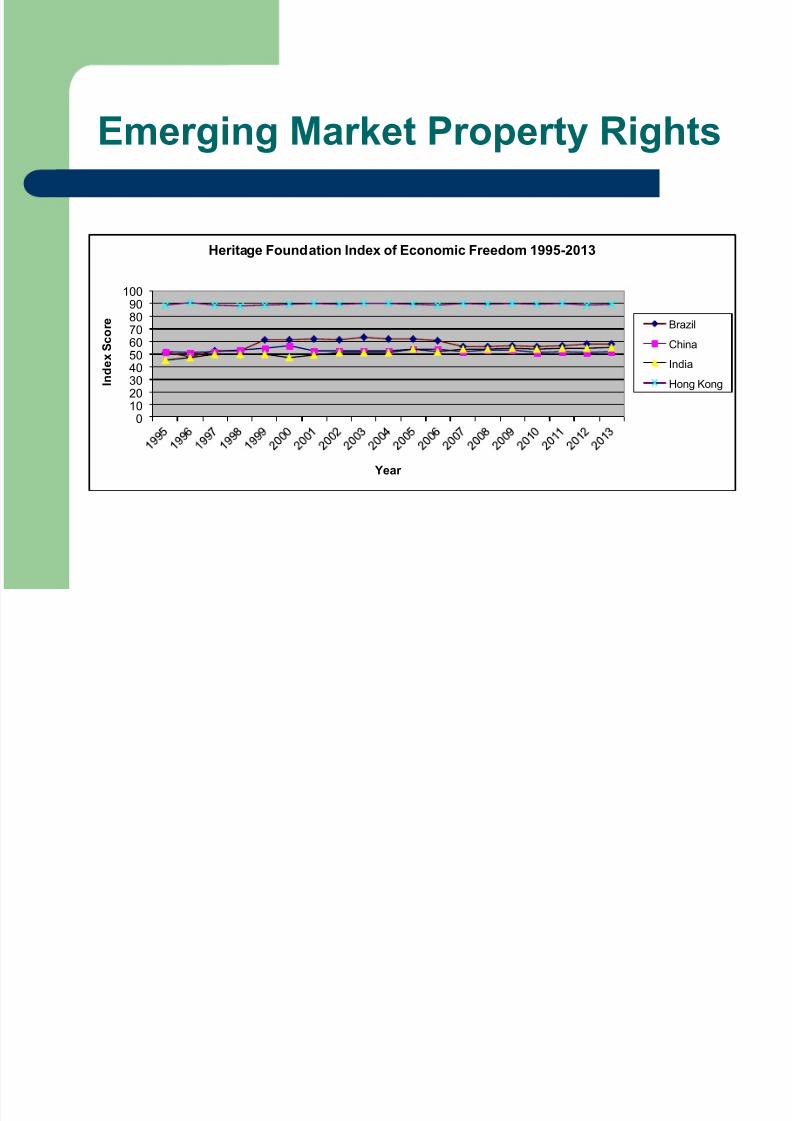

Emerging Market Property Rights

0

102030405060708090

100

I n d e x

S c o r e

Year

Heritage Foundation Index of Economic Freedom 1995-2013

Brazil

China

India

Hong Kong

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 22/62

What are “Property Rights”?

Right to control, occupy, develop, improve, exploit,pledge, lease, and sell property

Lessee: person who leases the land and has a rightto use the land for a specific period of time

Lessor : owner of the land who provides access tothe land for a fee

Lender : mortgagee obtains a secured interest via amortgage. This has value in the event of default bythe land owner. Lender aka mortgagee, borrower

aka mortgagor .

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 23/62

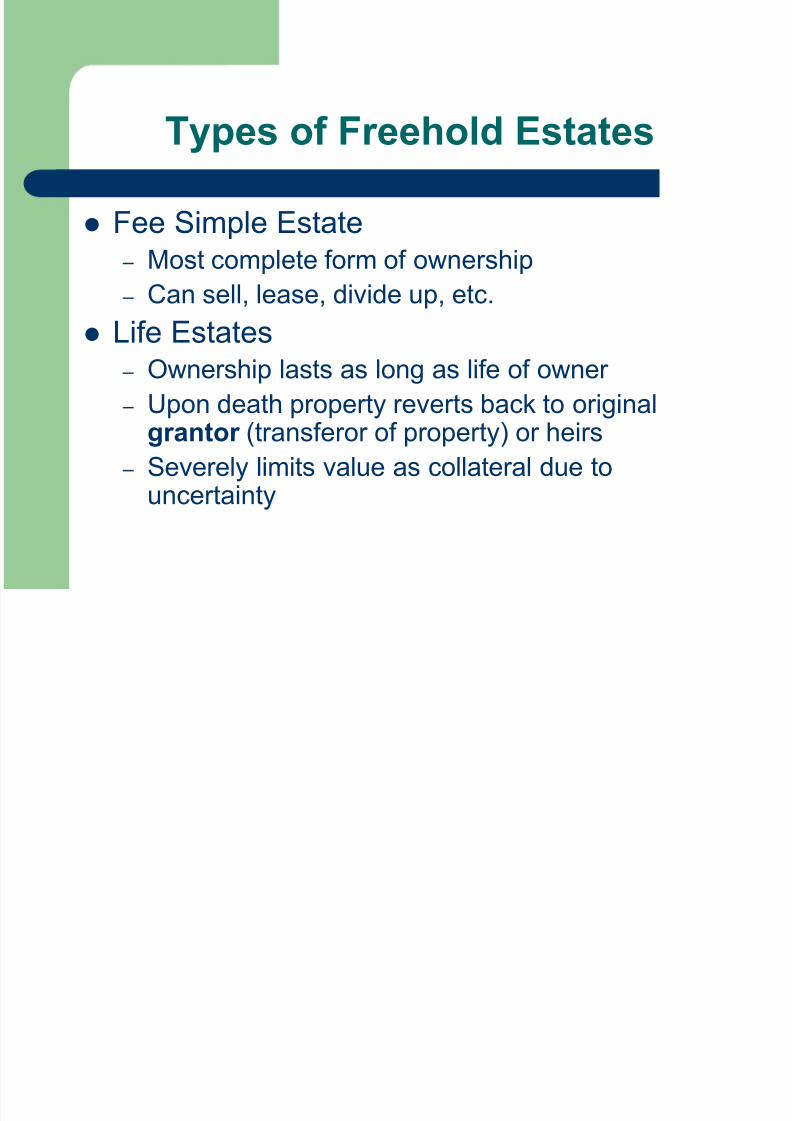

Types of Freehold Estates

Fee Simple Estate – Most complete form of ownership

– Can sell, lease, divide up, etc.

Life Estates – Ownership lasts as long as life of owner

–

Upon death property reverts back to originalgrantor (transferor of property) or heirs

– Severely limits value as collateral due touncertainty

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 24/62

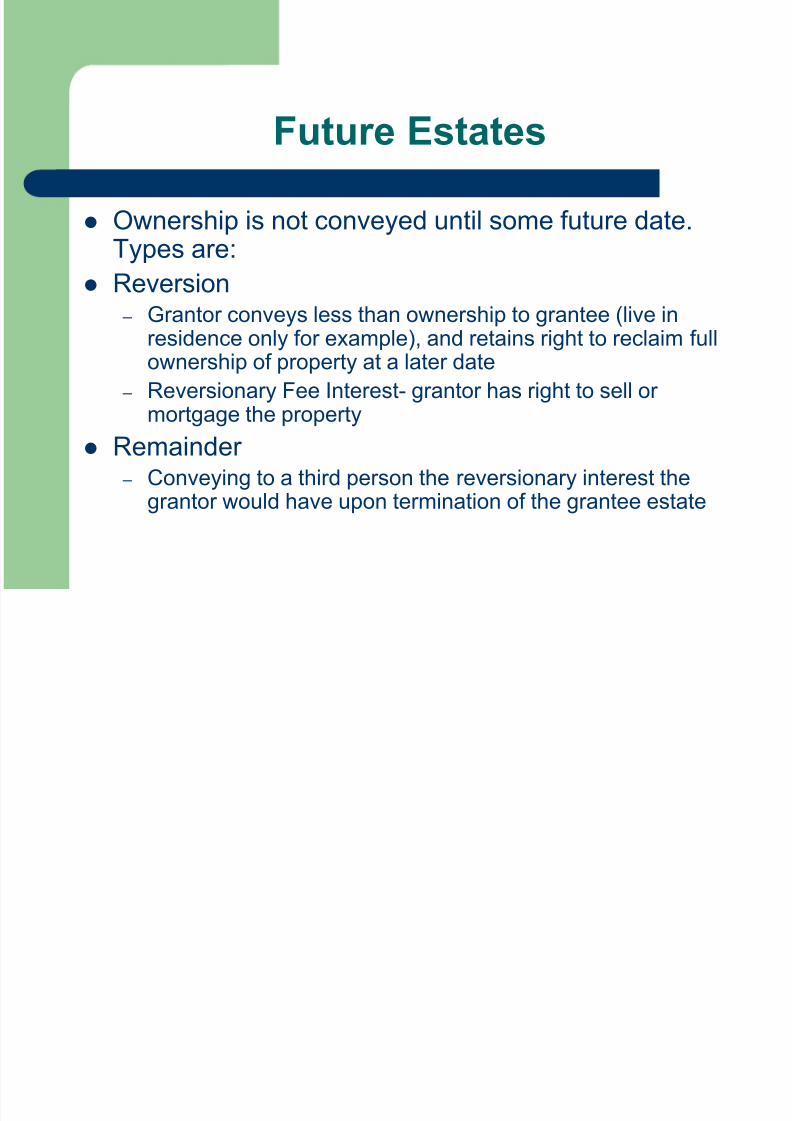

Future Estates

Ownership is not conveyed until some future date.Types are:

Reversion – Grantor conveys less than ownership to grantee (live in

residence only for example), and retains right to reclaim fullownership of property at a later date

– Reversionary Fee Interest- grantor has right to sell or

mortgage the property Remainder

– Conveying to a third person the reversionary interest thegrantor would have upon termination of the grantee estate

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 25/62

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 26/62

Other Definitions

Easement – Non-possessory interest in land

– A right of Way or another specific purpose Easement Examples

– Duke Power to create access point for public utilities

– Driveway for a property that does not have frontage on road

– Development Projects requiring access to road or otherdesirable characteristics New Housing Development that is positioned behind land

May pay land owner a fee for access from this property to thenew development

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 27/62

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 28/62

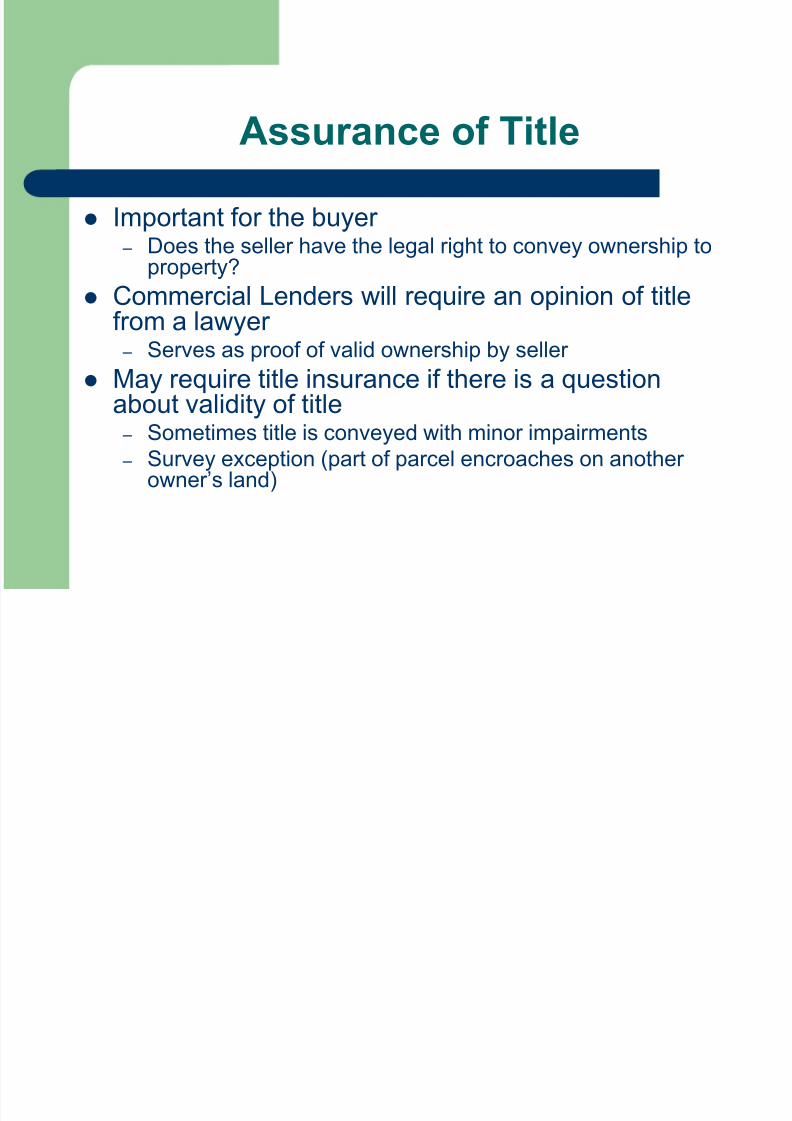

Assurance of Title

Abstract of Title – Historical summary of documents affecting title

– Deed: written instrument to convey title fromgrantor to grantee

Adverse Possession – Lack of sufficient documentation but is in

possession of property (i.e. squatter’s rights)

Marketable Title – Free from reasonable doubt & litigation

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 29/62

Methods of Title Assurance

General Warranty Deed

Special Warranty Deed Quit Claim Deed

Abstract & Opinion Method

Title Insurance

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 30/62

Methods of Title Assurance…

General Warranty Deed – Grantor warrants that title conveyed is free and clear of all

encumbrances other than those specifically listed

– This offers buyer the most protection Special Warranty Deed

– Similar to above but limits warrant to period that seller held theproperty prior to conveyance

Quit Claim Deed – Simply conveys grantor’s rights in property—whatever they might

be – No warranties are made, grantor quits claim (sometimes used in

divorce situations or when one partner wants to exit partnership) – Offers grantee/buyer the least protection

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 31/62

Methods of Title Insurance

Abstract & Opinion Method – Lawyer’s opinion of title

– Search title records & public records & offers opinion – Opinion is limited to the existing records on file

– If title is clouded, attorney will offer steps to clear theexception(s)

Title Insurance – Eliminates title risks & is typically required by lenders – One time insurance payment to ensure that title is clean &

marketable

– Protects policyholder from loss due to title defects

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 32/62

Other Issues with Title

Recording Acts

– Once legal paperwork is completed & filed, noticeis given to the world of ownership

Mechanics Liens

– Title is sometimes clouded due to placement of a

lien by contractor or other worker associated witha property (if they are not paid for their services)

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 33/62

Limits on Property Rights

Environmental Restrictions – State controls water (riparian) rights, mineral rights,

pollution, environmental restrictions Fair Housing

– Pertains to investments for 1-4 family dwellings andapartments

– Cannot discriminate against tenants due to race, religion,

national origin, handicap, or other such characteristics. Eminent Domain

– Government may purchase property for their purposes butmust provide fair market value for the property conveyed

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 34/62

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 35/62

Alternatives to Foreclosure

Most lenders will also attempt a Workout Loan scenario rather than moving toforeclosure

– Foreclosure is expensive for the lender, and oftentimes the sales price obtained at foreclosure is farbelow the fair market value of the property

– This is due to the perception that the foreclosurewas property specific. It could have been simplyrelated to the borrower’s financial condition.

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 36/62

Workout Loan Scenarios

Restructuring the Mortgage – Extend maturity (via an extension agreement),

additional collateral, recourse (or additionalguarantors)

Transfer of Mortgage – To a new owner (original owner still liable)

– Lender might accept this solution if the balanceon the mortgage is less than the perceived valueof the property

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 37/62

More Workout Loan Scenarios

Voluntary Conveyance – Borrower sells equity to mortgagee (lender)

– Title transferred via Quit Claim Deed or warranty – Provide ―Deed in Lieu of Foreclosure‖ – Lender must make arrangements with all other creditors

Friendly Foreclosure – Borrower agrees to cooperate in court with lender –

AKA a ―quick foreclosure‖ Prepackaged Bankruptcy

– Borrower agrees to terms with creditors on which to turnover assets

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 38/62

Foreclosure

Once all workout loan scenarios have beenconsidered, the next option is to seek foreclosure

against the mortgage. Judicial foreclosure

– Sue on debt, attach a judgment against subject propertyand anything else bank can legally obtain

IRAs are not eligible for this process (ask O.J. Simpson!) Lender then sells the property…

– Via public auction, foreclosure sale, etc.

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 39/62

Foreclosure Icon

Late night infomercial iconCharlton Sheets has made aname for himself bypurchasing ―distressedproperties‖

Or was it by getting others topurchase his videos?

There are many other

―gurus‖ out there who saythat foreclosures represent atrue opportunity to ―buy lowand sell high‖

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 40/62

Foreclosure

Redemption

– Represents borrower’s last chance to

cancel/annul the title conveyed by the foreclosuresale

– This is done by paying the full amount of debt,interest, and costs due the lender

– Cannot do this once foreclosure is confirmed

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 41/62

The Race at Foreclosure

Redeem up, but foreclose down – If sell at foreclosure for $110M

$90M mortgage balance first mortgage is paid out $20M second mortgage is paid out

Any remaining balances will be left unpaid

Any unpaid creditors can still seek funds from the borrower – What if you are lending to a holding company?

Taxes in Default take precedence over any credit debt

Deficiency Judgment – Left over balance after foreclosure proceeds have paid out

credits, it is now an unsecured position

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 42/62

Classification of Real Estate Uses

Single Family – Either as primary residence or investment property – Banks have a hard time financing investment single family residences due to the lack

of comparables in the market

Multi-Family – Apartments, Duplexes, etc.

Office Retail Industrial/Warehouse/Self Storage Recreation

– Marinas, country clubs, sports complexes Institutional

– Specialty use, Hospitals, Universities, etc.

Mixed Use – Could combine apartments with retail, retail with office, etc. – Not all combinations are good ones

How would you feel about living in an apartment unit located above a drug rehabilitation clinic?

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 43/62

Risk by Property Types

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 44/62

Risk by Property Types

Relative Risk*

Apartments Warehouse/Industrial

Office

AnchoredRetail

UnanchoredRetail

Mini-storageFacilities

Hotels

Restaurants

Conveniencestores

CondosSingle-purposefacilities

Land

Lowest Excessive

*Subject to change and may vary by market!

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 45/62

Why are Some Property Types Better

Than Others?

Availability of Comparables in the Market – Can better ascertain vacancy and market rental and

expense rates

Availability of Investor/Secondary Financing in theMarket – Serve as Source of financing for buyers

Higher Probability of Finding Replacement Tenants – The more special the purpose of a property, the more likely

it is to remain vacant if the tenant vacates the property – Think about restaurants in your neighborhood and compare

with five years ago. How many have been there over thatentire period of time?

Not all Net Operating Income is the Same…

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 46/62

Cash Flow Fundamentals

Quantity How much lease income per month (historical/projected)?

Comparison to market rental rates per square foot for similarproperties.

Quality Diversification (number of tenants)

Tenant financial strength (internal information or BusinessCredit Report when applicable)

Durability Length of leases relative to term of loan.

Mgmt Experience with property (or similar properties)

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 47/62

Some Definitions

Net Operating Income (NOI):

Income from property after operating expenses and vacancy factors have been

deducted, but before deducting income taxes and financing expenses (interest and principal payments). This represents the primary source of repayment for

definition real estate loans.

Debt Service Coverage Ratio (DSCR):

The relationship between net operating income (NOI) and the annual debt service

(ADS).

The Formula is DSCR = NOI

ADS

This is a typical covenant contained in most definition real estate loans (i.e. minimumDSCR of 1.25x)

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 48/62

Supportable Loan Amount

Supportable Loan Amount (SLA):

The net operating income of the property (NOI) divided by the desired debt service

coverage ratio, then divided by the loan constant. This is in effect how much of a loan

amount that the NOI of the property will support, given a desired coverage ratio, and a

specific loan constant (which considers interest rate, loan amount, and amortization

period).

The formula is: (NOI/Desired DSCR)/Loan Constant

Depending on the underwriting rate and assumptions used in determining the

property’s NOI, the SLA is a range of values.

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 49/62

Other Assumptions

Vacancy Factor to correspond withguidelines, market, or actual rates

5% Management Fee

Do not include officer salaries, non-cashexpenses, or other non-real estate relatedexpenses

Either Flat % of EGI for Structural Reservesor based on cost per square foot.

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 50/62

General Guidelines for a Commercial Bank

Property Type Max. Amort.

DSC LTV Equity Expenses Vacancy

Apartments & Age: Class A

New to <3yr >3 to <10 yrs

>10 to <20 yrs

>20 yrs

30

25

25

20

15

1.20

1.20

1.25

1.30

1.35

75%

75%

75%

70%

65%

20%

20%

20%

20%

25%

Greater of35% of PGI

or actual

Greater of7% or actual

Office & Quality*

Class A Class B

Class C

25

Up to 25

15

1.25

1.35

1.35

75%

75%

70%

20%

20%

25%

Greater ofactual ormarket

Greater of10% or actual

Retail Type*

Neighborhood S/C

Single Credit Tenant Unanchored/Other

25 = lease

Up to 25

1.25 1.10

1.30

75% 80%

70%

20% 10 -20%

25%

Greater ofactual ormarket

Greater of 10- 15% or

actual

Flex/Warehouse*

Bulk (>24’ height) Service (>18’ ht)

Flex

Self-storage

25

20 – 25

Up to 25

15 – 20

1.25

1.30

1.35

1.35-1.4

75%

70 –75%

65-70%

65-70%

20%

20%

20%

25%

Greater ofactual ormarket

Greater of10% or actual

* “Arms Length” term leases required. Equity relates to the cash selling price, Loan to Value relates to the appraisal

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 51/62

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 52/62

Global Housing Boom Case

Explain the changes thattook place during the

―Yes Era‖ at La VistaBank

What were theunderlying flaws in their

operation model? Class experiences

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 53/62

Flip That House!The Cause and Effect of the Sub-Prime

Housing Crisis

Sub-Prime Borrowers: Those that would nottypically be approved for financing in traditional

underwriting. Needed easy credit, teaser rates toqualify.

– Ninja Loans: ―No Income, No Job, No Assets‖

– Typically have poor credit or no credit histories

– Sub-prime represented 5% of total residentialmortgages in 1994, 20% by 2007.

– Pricing in segment fell from 280 basis points in2001 to 130 basis points in 2007.

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 54/62

Sub-Prime Continued

Housing prices rose in US by 124% between 1997and 2006

US Home ownership went from 64% in 1994 to 69%in 2004

22% of homes purchased as investment and 14% asvacation homes in 2006 (All-time high for both)!

Some ―house flippers‖ had as many as 12 housespurchased at a time, on interest only payments. – The fix it up and sell it for a big profit mentality

– Once the sales market dried up, these borrowers couldn’tpay their payments.

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 55/62

Sub-Prime: Role of ARM’s

Many sub-prime borrowers were attracted by the lowinterest rates and payments associated with

Adjustable Rate Mortgages. – These are variable rate mortgages tied to an index that

neither the borrower nor lender controls 10 Year Treasury, T-Bills, Prime, LIBOR, etc.

As an example, assume that a borrower was approved

for a 30-year ARM for $100,000 in 2006. The initialinterest rate was 4%, but it resets every 12 months,depending on the value of the index plus the originalloan spread.

ARM % Pmt

Year 1 4% $477.42

Year 2 6% $596.32Year 3 9% $791.33

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 56/62

Sub-Prime Mortgage Crisis Cont…

Once the assumed appreciation of housing did not continue(especially in CA, FL, AZ), the amount of mortgage foreclosuresescalated. This was accompanied by stricter lending criteria at

commercial banks, but the value of the decline of their assetsoccurred much more quickly than their reaction time.

Governmental Sponsored Enterprises Fannie Mae (FederalNational Mortgage Assoc, 1938) and Freddie Mac (Federal HomeLoan Mortgage Corp, 1968) have $95 billion in capital, but hold

over $5 trillion in mortgages! – These entities are ―too big to fail‖ per Treasury Secretary HankPaulson in July 2008. Thus, he allowed them to borrow from theFed’s discount window at the primary rate.

– Fannie Mae and Freddie Mac provide a huge amount of liquidity tothe market; without them, rates would be much higher.

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 57/62

Housing and Economic Recovery Act of 2008

Strengthens regulation of Fannie Mae & Freddie Mac byestablishing capital standards, prudent management standards,restricting asset growth, and reviewing and approving all newproduct offerings before they are offered to the public.

Creates Housing Trust Fund and Capital Magnet Fund,financed by annual contributions, to construct affordablehousing.

Restricts asset growth and capital distributions forundercapitalized institutions

Now has authority to remove officers and directors

Increases loan limit in high cost areas, to expand coverage ofthe number of families helped by Fannie Mae & Freddie Mac.

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 58/62

Hope for Homeowners Act of 2008

Provides voluntary refinance for distressed loans at significant discountfor owner occupants (not investors!) at risk of losing their homes – In exchange, homeowners will share future appreciation with the Federal

Housing Admin (FHA). – Owner-occupants only with mortgage debt to income ratio above 31%. – Must verify income and not had fraud for last 10 years (Madoff free zone) – Loans are 30 year fixed rate loans only at lesser of what the borrower can

afford to pay or 90% of the current value of the home. – Higher risk loans require ―seasoning‖ before they are insured under the

program. Program is authorized to insure up to $300 billion in mortgages,or 400,000 homeowners

– Program was from 10/01/2008 until 09/30/2011 Expected to net $250 million for tax payers

– Program is paid for by using part of the Affordable Housing Trust Fund,and establishes a reserve fund at the Treasury over ten years (expected tobe $2 billion over that time)

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 59/62

Foreclosure Prevention Act of 2008

Increase FHA loan limit to reach more homeowners Assists communities devastated by foreclosures

– Use Community Development Block Grant Funds to purchase foreclosed homes at a discount,rehab/redevelop homes to stabilize neighborhoods, & stem significant losses in house values of

neighboring homes Provides Pre-Foreclosure Counseling for Families in Need

– $150 million for additional funding for housing counseling – $30 million to help provide legal services to distressed borrowers

Enhancing Mortgage Disclosure – Inform borrowers of maximum loan payments at least 7 days before closing, & expands types of

loans subject to early disclosures (within 3 days of application)

Additional Help for US Veterans – Lengthens time to start foreclosure from 3 to 9 months after soldier returns home from service – Returning soldiers have one year relief from increases in mortgage interest rates – Increases Veteran’s Admin (VA) loan guarantee amount, to help more veterans – Provides moving benefit to veterans who are forced to move out of rental housing due to

foreclosure – Provides improvements and structural alterations to homes of veterans with service-connected

disabilities

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 60/62

Casualties of the Crisis

Lehman Brothers, Bear Stearns, Countrywide Financial, NewCentury Mortgage, Indy Mac failed, Wachovia & Merrill Lynchwere purchased, and Northern Rock (England), had an old

fashioned bank run in 2008. Large write-downs by Citi Group, Wachovia, JP Morgan Chase,

Bank of America, UBS, etc. – More write-downs & casualties are expected

– Bank of China holds $9.7 billion in sub-prime debt

Homebuilding at an all-time low, lending criteria the most strictin decades, bottom of housing market in US was not predicteduntil late 2011 or early 2012 , with meaningful housing recoverybeing years away.

Sources: Wachovia Economics, Economist,Mortgage Bankers Assoc., & US Government.

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 61/62

Nietzsche on the Housing Bubble

“For he wanted to determine what

had happened to man meanwhile;whether he had become greater

or sm aller . And once he saw a rowof new houses ; then he wasamazed and said:

What do these hous es mean? Verily no great soul put them up asits likeness. Might an idiotic childhave taken them out of his toy box?

Would that another child might putthem back into his box! And theserooms and chambers—can men goin and out of them? They look tome as if made for si lken dol ls , orfor steal thy nibb lers wh oprobably also let themselves benibbled stealthily.”

―Thus Spoke Zarathustra‖, pg. 167 On Virtue That Makes Small

8/11/2019 Chapter 1 RE

http://slidepdf.com/reader/full/chapter-1-re 62/62

End of Session

Next week we will next discuss chapter 2 andthe various forms of mortgages.

Read chapters 1 and 2, and Rent Roll Mini-Case

This is a Madoff Free Zone!

![CHAPTER 4 [RE] RESIDENTIAL ENERGY EFFICIENCY](https://static.fdocuments.in/doc/165x107/61688a33d394e9041f70624e/chapter-4-re-residential-energy-efficiency.jpg)