CHAPTER 1 INTRODUCTIONshodhganga.inflibnet.ac.in/bitstream/10603/27993/6/06...of women, alcohol, the...

29

1 CHAPTER 1 INTRODUCTION Empowering women with economically productive and viable work spaces will enhance their contribution to societal development. Empowerment is a process by which women gain greater control over resources (income, knowledge, information, technology, skill and training), challenge the ideology of patriarchy, and promote in leadership, decision making processes, enhance their self-image, to become active participants in the process of change, and to develop the skills to assert them. Empowerment is a process of awareness and capacity building leading to greater participation, to greater decision-making power and control, and to transformative action. It is “the process of changing the existing power relations and of gaining greater control over the sources of power”. The goals of women empowerment are to change the ideology of patriarchy and to transform the structures of image. At present, Self Help Groups are widely used as an instrument to empower women socially and economically. Once socio economic empowerment is achieved, it would have an impact on the overall development of women. The economic contribution of women has been found to be related to their role and status in the society. Economic independence facilitates bringing about gender equality, and an increase in women's income translates more directly into family wellbeing. Therefore, enhancing job opportunities through the formation of Self Help Groups is a viable path for the empowerment of women.

Transcript of CHAPTER 1 INTRODUCTIONshodhganga.inflibnet.ac.in/bitstream/10603/27993/6/06...of women, alcohol, the...

1

CHAPTER 1

INTRODUCTION

Empowering women with economically productive and viable

work spaces will enhance their contribution to societal development.

Empowerment is a process by which women gain greater control over

resources (income, knowledge, information, technology, skill and training),

challenge the ideology of patriarchy, and promote in leadership, decision

making processes, enhance their self-image, to become active participants in

the process of change, and to develop the skills to assert them. Empowerment

is a process of awareness and capacity building leading to greater

participation, to greater decision-making power and control, and to

transformative action. It is “the process of changing the existing power

relations and of gaining greater control over the sources of power”. The goals

of women empowerment are to change the ideology of patriarchy and to

transform the structures of image.

At present, Self Help Groups are widely used as an instrument to

empower women socially and economically. Once socio economic

empowerment is achieved, it would have an impact on the overall

development of women. The economic contribution of women has been found

to be related to their role and status in the society. Economic independence

facilitates bringing about gender equality, and an increase in women's income

translates more directly into family wellbeing. Therefore, enhancing job

opportunities through the formation of Self Help Groups is a viable path for

the empowerment of women.

2

Self Help Groups are a promising alternative to achieve the

objectives of societal development, especially women’s empowerment.

Through the Self Help Groups, micro credit is disbursed to women for the

purpose of making them enterprising and encouraging them to enter

entrepreneurial activities. The credit needs of Self Help Group women can be

fulfilled totally through Self Help Groups. The group members save a small

amount regularly every month. The group rotates the money to the needy

members for various purposes at a specified interest rate. As the repayment is

100 percent and the recycling is fast, the savings amount increases rapidly

owing to the accumulation of income from interest. The saving habit helps the

members to escape from the clutches of money lenders. It paves the way for

the empowerment of women and builds confidence in them to stand on their

own feet. After the group stabilizes over a period of six months or more in the

management of its own funds, it conducts regular meetings, maintains savings

accounts, and gives loans to members on interest. In India, particularly in

states like Tamilnadu, Andhra Pradesh etc the Self Help Groups are linked

with the banks for external credit, under the projects of rural development.

The banks provide assistance for various entrepreneurial activities, such as

setting up small shops, vegetable shops, tailoring units, charcoal making units,

dairies etc. The borrowers repay the bank loans promptly. The Self Help

Groups repay more than 90 per cent of the loans to the banks on time. Besides

focusing on entrepreneurial development and empowering women, Self Help

Groups concentrate on all-round development of the beneficiaries and their

village as a whole. The groups undertake the responsibility of delivering non-

credit services such as literary, health and environmental issues. The concept

of Self Help Groups moulds women as responsible citizens of the country,

achieving social and economic status.

Self Help Groups are formed and supported by government

agencies or NGOs, and benefit their members economically and socially. The

3

self help group movement is credit linked; it is primarily aimed at addressing

the need for capacity building of women, by organizing them into

homogeneous support groups that pool their resources to engage in micro-

entrepreneurship activities and share the income thus generated. In India,

women who are members of Self Help Groups derive access to low-cost

financial services, with a process of self management and development. Self

Help Groups enable women to grow their savings, and to access the credit

which banks are increasingly willing to lend. Self Help Groups can also be

community platforms for women to become active in village affairs, contest

local elections or take action to address social or community issues (the abuse

of women, alcohol, the dowry system, schools, and water supply). Thus, Self

Help Groups help mobilize women to take social action, accumulate social

capital, display better economic viability, and demonstrate a greater suitability

and sustainability than individual based models for women's empowerment

initiatives.

1.1 SELF HELP GROUPS IN TAMIL NADU

The Government of Tamilnadu spearheaded the Self Help Group

(SHG) concept in the country by forming Self Help Groups in 1989 with the

assistance of the International Fund for Agricultural Development (IFAD).

Now, there is a greater amount of socio-economic emancipation among the

members of the Self Help Groups. Among the various districts of Tamil

Nadu, Kancheepuram and Thiruvallur Districts adjoining Chennai District

occupy a predominant position in starting Self Help Groups. The Self Help

Groups have been formed for meeting the needs of industrial and agricultural

activities. As of November 2011, there are 518519 Self Help Groups in

Tamil Nadu with a membership of 80.40 Lakhs. In Kancheepuram District

alone there are 26993 Self Help Groups, and in Thiruvallur District there are

20047 Self Help Groups.

4

The findings of this study would pave the way for taking certain

policy decisions for strengthening the Self Help Groups relating to ICT usage,

and hence, the study has been undertaken in the Kancheepuram and

Thiruvallur Districts of Tamil Nadu as shown in Table 1.1.

Table 1.1 Details of Self Help Groups in Tamil Nadu as of 2011

Total No. of Self Help Groups 5,18,519

Total No. of Self Help Group Members 80.40 Lakhs

Total No. of Rural Self Help Groups 3,48,753

Total No. of Members in Rural Self Help Groups 54,10,282

Total No. of Urban Self Help Groups 1,69,766

Total No. of Members in Urban Self Help Groups 26,30,312

Total Savings Rs.3085 crores

Source: Tamil Nadu Corporation for Development of Women Ltd.

1.2 DISTRICT-WISE GROUP FORMATION IN TAMIL NADU

AS OF 2011

Self Help Groups (SHGs) have emerged as the most vital

instrument in the process of participatory development and women

empowerment. Women are marginalized in society because of socio-

economic constraints. They remain backward and in the lower rungs of the

social hierarchical ladder. They can lift themselves from the morass of

poverty and stagnation through microfinance, and formation of Self Help

Groups. So credit is a crucial input for the socio-economic development of the

poor, but the institutional sources of credit to the poor are still inadequate. As

a result, moneylenders and landlords provide credit to the needy borrowers,

particularly the depressed sections of society, charging an exorbitant rate of

interest. This non-institutional source of finance has various exploitative

practices. The debtor-creditor relationship gives birth to the master-slave

relationship, as the debtor mortgages his labour with the creditor. Lack of

5

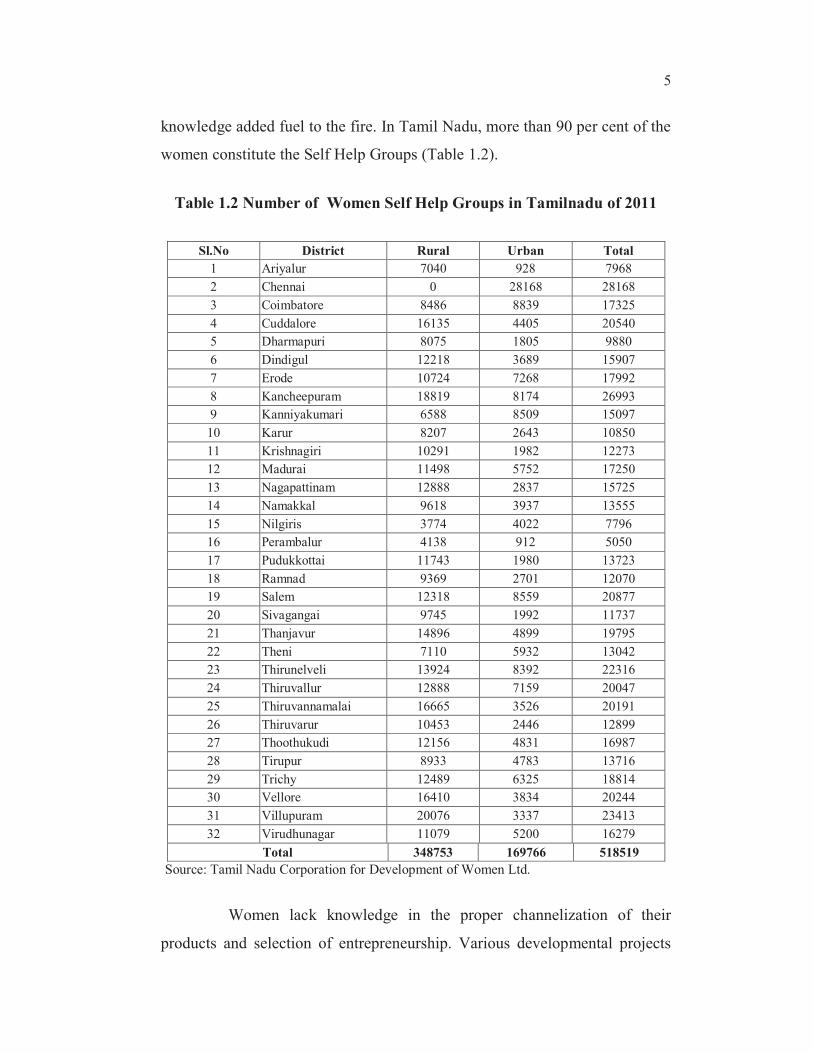

knowledge added fuel to the fire. In Tamil Nadu, more than 90 per cent of the

women constitute the Self Help Groups (Table 1.2).

Table 1.2 Number of Women Self Help Groups in Tamilnadu of 2011

Sl.No District Rural Urban Total

1 Ariyalur 7040 928 7968

2 Chennai 0 28168 28168

3 Coimbatore 8486 8839 17325

4 Cuddalore 16135 4405 20540

5 Dharmapuri 8075 1805 9880

6 Dindigul 12218 3689 15907

7 Erode 10724 7268 17992

8 Kancheepuram 18819 8174 26993

9 Kanniyakumari 6588 8509 15097

10 Karur 8207 2643 10850

11 Krishnagiri 10291 1982 12273

12 Madurai 11498 5752 17250

13 Nagapattinam 12888 2837 15725

14 Namakkal 9618 3937 13555

15 Nilgiris 3774 4022 7796

16 Perambalur 4138 912 5050

17 Pudukkottai 11743 1980 13723

18 Ramnad 9369 2701 12070

19 Salem 12318 8559 20877

20 Sivagangai 9745 1992 11737

21 Thanjavur 14896 4899 19795

22 Theni 7110 5932 13042

23 Thirunelveli 13924 8392 22316

24 Thiruvallur 12888 7159 20047

25 Thiruvannamalai 16665 3526 20191

26 Thiruvarur 10453 2446 12899

27 Thoothukudi 12156 4831 16987

28 Tirupur 8933 4783 13716

29 Trichy 12489 6325 18814

30 Vellore 16410 3834 20244

31 Villupuram 20076 3337 23413

32 Virudhunagar 11079 5200 16279

Total 348753 169766 518519

Source: Tamil Nadu Corporation for Development of Women Ltd.

Women lack knowledge in the proper channelization of their

products and selection of entrepreneurship. Various developmental projects

6

financed by international organizations, banks and the government of India,

have supported their cause. But taking into account their poor knowledge and

literacy level, most of the Self Help Groups failed in the womb before seeing

the light. But in south India, like Andhra Pradesh and Kerala, Self Help

Groups in Tamil Nadu are progressing as per the objectives. To support their

cause, various organizations have started the use of ICT for their further

development.

1.2.1 Self Help Group Movement in India

In a country like India with a population of over 1.27 billion almost

32% people live below the poverty line. A majority of people earn their

livelihood through agriculture and agriculture-related vocations. Most of them

are landless and marginal farmers. They remain engaged in their agriculture-

related activities for not more than six months in a year. To meet their

agricultural and household requirements they need money. Most of them are

either in the fold of agricultural cooperatives or private entrepreneurs/

moneylenders from where they pick up short-term loans. Since the

cooperative institutions are short of funds and the market interest rates are

considerably higher and they do not have any collateral to raise funds, they

find the institution of Self Help Groups as the most convenient to raise funds

for micro-enterprises or to meet their immediate farm and/or off-farm needs.

Self Help Group (SHG) is an unregistered group of micro-

entrepreneurs having homogenous social and economic background;

voluntarily coming together to save regular small sums of money, mutually

agreeing to contribute to a common fund and to meet their emergency needs

on the basis of mutual help. The group members use collective wisdom and

peer pressure to ensure proper end-use of credit and timely repayment. This

system eliminates the need for collateral and is closely related to that of

solidarity lending, widely used by micro-finance institutions. To make the

7

book-keeping simple enough to be handled by the members, flat interest rates

are used for most loan calculations.

Self Help Groups are started by non-profit organizations (NGOs)

that generally have broad anti-poverty agenda. Self Help Groups are seen as

instruments for a variety of goals including empowering women, developing

leadership abilities among poor people, increasing school enrolments, and

improving nutrition and the use of birth control. Financial intermediation is

generally seen more as an entry point to these other goals, rather than as a

primary objective. This can hinder their development as sources of village

capital as well as their efforts to aggregate locally controlled pools of capital

through federation as was historically accomplished by credit unions in the

United States and Canada.

SHG is a social design in which people participate by making

themselves socially and economically accountable to each other. Some

community-based bodies and field level workers of government agencies are

involved in SHG formation as an essential strategic element to fight poverty

in India.

1.2.2 Need for Self Help Groups

Self Help Groups came in to existence as a solution to poverty. The

self help group members with their own collective small savings try to help

the group members. A small group moves forward towards self-

empowerment. The needy persons, the group members, are mostly poorest of

the poor and have determination to strengthen themselves economically and

socially. Usually these people individually have no access to formal banking

system. Moneylenders exploit them in the hours of their needs. To overcome

both these situations there is a felt-need to create Self Help Groups. Members

with their collective resource take up some income-generating activities

8

which will bring additional income to their household. These institutions thus

become powerful tools for poverty alleviation and social cohesion at the

grassroots level.

1.2.3 Functions of Self Help Groups

In order to achieve the main objective, the self help groups

undertake various activities. These activities are:

Savings howsoever small they may be should be made in

order to mobilize financial resource. The idea is to generate

the habit of saving from whatever income is earned in the

household;

Loaning and Repayment in smaller quantities but in time. As

a micro-finance institution the SHG should be able to provide

credit to the members. It is also expected that the members

return the money borrowed in time, in full, and with interest

so that other members also benefit;

Maintaining Books of Account and Records is the most

crucial aspect of management of the SHG as well as of

confidence building among the members. The SHG has to

ensure that all accounts and the books of account are up to

date and maintained to ensure transparency and accuracy.

Good accounts reflect the goodwill of the organization and

ensure its credibility. Properly kept records are not only of

reference value but also useful in future planning and

decision-making;

Member-oriented Action Programmes are conceived and

implemented which are recommended and demanded by the

members. Most of these programmes are social and economic

9

and even cultural. Such programmes are also usually the

agenda of the development projects which promote SHGs.

Programmes can be educational, additional income-

generation, off-farm activities, labour-intensive activities,

watershed-related and public works construction activities,

harnessing water resources for drinking and irrigation, health,

education, vocational training etc. etc. Development

programmes can be directed at women, youth or farmers;

Liaison and Linkages with financial institutions

(FIs)/Government Organisations (GOs) and other agencies.

The SHG considers developing relationship with the financial

institutions e.g., cooperative bank or the rural branch of a

commercial bank, or others, and also relationship with the

governmental organizations and other development agencies;

Training and Capacity Building Activities. Self Help Groups

need constant support, assistance, guidance and advice from

the promoters and other development agencies. They need

constant monitoring, training and education support in order to

help them improve their working capacities and capabilities.

The members might need some exposure and interaction.

They might also need some equipment and technology

support. Self help groups need to continue improve their

capacities.

1.2.4 Income-Generating Activities of SHGs

The following are the some of the income generating activities of

self help group women

Garment shop (tailoring, embroidery, knitting);

10

Soft toys making

Preparing eatables like pickles, snacks, savories etc

Agriculture-related activities.

Small retail businesses/General Store;

Brick-making;

Livestock development (animal husbandry, goatery, poultry,

piggery etc.);

Cattle-feed sales;

Bicycle repair shop;

Milk procurement and processing;

Clay-pot making;

Leaf/Paper plate making;

Flour-mill and grain shop;

Carpentry, Ironsmith, welding;

Raw-sugar (gur/shakkar) making;

Beauty saloon;

Fruit/Vegetable preservation and processing;

Motor winding etc.

Self Help Groups do not thrive and prosper only on one or two

activities. They need to expand the range of their activities by incorporating

new methods and techniques to produce new products. Diversification of

business and up-scaling of activities with the support of SHG association and

cooperative society can further add to the income of members. Self Help

Groups, as members of SHG association, can create more services and

11

products not only for members themselves but also for the market.

Associations, being legal entities, are fully empowered to transact business

with raw material suppliers and end-product consumers and traders. The

associations transact business on behalf of the affiliated Self Help Groups,

and ultimately for the members of SHGs.

1.2.5 Credit Management in Self Help Groups

The poor relate more easily to Self Help Groups than to banks. One

of the important functions of Self Help Groups is credit management, as

discussed below:

The groups foster thrift and promote savings;

The groups encourage women’s groups in fostering thrift and

savings;

Groups contribute a part of their savings earned through group

action. This strengthens the value of group action;

Groups mobilize capital through: (a) Savings, (b) From

interest at rates decided by the group; and (c) From banks and

cooperatives;

The groups interlink with other groups with similar functions.

1.2.6 Characteristics of SHGs

The working of Self Help groups is real and truly contributory to

the general social and economic welfare of the local communities.

Mutual trust and mutual support;

Each individual is equal and responsible;

12

Each individual is committed to the cause of the group;

Decisions are based on the principle of consensus.

Self help group characteristics are:

Bottom-up approach;

Homogeneous membership;

Self-management; and

Need-based activities.

1.2.7 Functional Features of Self Help Groups

The Self Help Group is a voluntary association of poor people

whose needs are limited and are not engaged in speculative business. The

composition of the group is of the members who belong to similar socio-

economic status or category, which are bound by affinity, similarity of

interests and who are willing to work together. Self help groups should be

separate groups since their requirements and style of work is different. They

do not work under the direction or control of any external agency or official.

The characteristic of the group is completely independent and highly

participatory.

1.2.8 Financial Management in Self Help Groups

The self help groups important activities are savings and loaning.

Members are expected to regularly save small amounts and use the savings

for internal loaning among the members. The group manages the process of

thrift and credit by itself. In case the loan requirement of members is higher,

the group can borrow from the lead bank.

13

It is viewed that provision of micro-finance may be seen more as

logical extension of the managerial and pragmatic approach to poverty

reduction but with regard to financial perspective credit is an effective tool

which helps the poor to tackle the problem of deprivation, improve their

welfare and social acceptance and credibility. Thus, micro-finance institutions

including Self Help Groups are those which provide thrift, credit and other

financial services and products of very small amounts mainly to the poor in

rural, semi-urban and urban areas for enabling them to raise their income

level and improve living standards.

1.2.9 Funds of the Self Help Groups

The funds of the Self Help Group consist of:

i) Membership Fee – Generally Rs 10 per member;

ii) Membership Fee is payable only once at the time of

admission;

iii) Minimum regular deposits every month;

iv) Interest earned;

v) Grants from promoters and government;

vi) Project funds provided by promoters to carry out specific

activities;

vii) Donations and Gifts;

viii) Development Fund etc.;

ix) Fines and Penalties due to defaults.

14

1.2.10 Regular Savings

Every member of the group has to accept to make a minimum

saving every month. The decision as to the amount to be saved depends on the

capacity of the member itself. Members will save a specific amount on

fortnightly or monthly basis. This amount is decided by the group members.

Once the amount has been fixed then that amount must be paid in every

month regularly.

The defaulting member is required to pay a penalty if the fixed

amount is not paid in time. All incoming funds should be distributed among

the members who have applied for loans and the remaining amount should be

promptly deposited into the bank as soon as possible.

1.2.11 Self Help Group Funds Management

The members shall abide by the rules and regulations of the group.

The self help group women shall be jointly and severally liable for all the

debts contracted by the group. All assets and goods acquired by them shall be

in the joint ownership of all the members. The self help group members shall

elect and appoint a certain person to look after and manage the day-to-day

affairs of the group. The person shall be made responsible to manage all

affairs of the group with the bank e.g., filling in loan applications, receiving

the cheques from the bank, loan disbursements to the members, securing

repayments for the bank etc. The appointed person can be removed at any

time by a majority vote of the members and a new person to be elected or

appointed. In the event of the death of any members of the SHG all

entitlements shall be handed over to the next kin of the person.

Since the SHG is based on the principle of mutual trust,

cooperation and mutual benefit, the loans must be returned in time. It has

15

been observed that members of SHG do not default simply because they know

that they would not get the loan next time if they do not realize the

importance of this principle. Regular repayment has been a special feature of

a SHG. In more than 90% cases, members do return their loans.

However, in a situation where the member finds it difficult to repay

in time, a special request with a specific explanation can be given to the SHG

at its half-monthly meeting. The member must be present in person and must

explain the reason for the default. If the reason submitted is reasonable and

acceptable to the rest of the members, the repayment can be rescheduled, and

the member has to pay a penalty for the default.

Recovery of loans is expected to be 100% in order to make the

funds available to other members. Default in repayment is a serious matter as

in the long run the financial situation of the group gets worse.

The group can receive the repayment either in cash or in kind.

Repayment of loan in kind should be acceptable only in case the group has

ventured in marketing and storage of the product.

1.2.12 Books Maintained by Self Help Groups

The Self Help Group is an organization, it is necessary to maintain

certain books to keep track of membership, decisions and accounts. The

NABARD has suggested that the following books need to be maintained by

all Self Help Groups:

Simple and clear books for all transactions to be maintained;

If the group is not able to maintain the books on its own,

someone from outside can be engaged by the group for the

purpose;

16

Minutes Books. This book should contain the proceedings of

meetings, the rules and regulations of the group, names and

full addresses of the members, and details of deposits received

and loans given, details and comments of the visitors and

major happenings in the village etc.;

Savings and Loan Register. It should contain information on

the savings of the members separately and of the group as a

whole. Details of individual loans repayments, interest

collected, balance etc. are to be entered in this book;

Members’ Passbooks. Individual members’ passbooks

encourage regular savings;

A regular correspondence file to be maintained which should

have all the correspondence of the group with the bank,

members and other agencies.

1.2.13 Capacity Building in Self Help Groups

Self Help Groups are to be strengthened socially, economically and

professionally. Since the members are from the group which had limited

capacity to manage themselves and to promote their profession it becomes

essential to impart training to them on various aspects of social mobilization,

financial management and vocational upliftment. This kind of training

provides enough information which will facilitate smooth functioning of

SHGs. However, the need for different vocational training and resource

mobilization should continue to persist for achieving higher tier of progress .

17

1.2.14 Capacity Building of Members

Members will need constant education in the following:

Maintaining SHG records;

Vocational training;

Health and Hygiene;

Organizing groups and associations;

Banking procedures;

Participation including group dynamics.

Motivators/facilitators and professionals in different vocations will

become the trainers for this purpose.

1.2.15 Functions of Motivators

In the organisation and management of Self Help Group there is a

need for someone who could provide motivational and organisational support.

This person is an extension agent who interacts with the prospective members

and motivates them to become members of SHGs. This person should be fully

conversant with the methods and techniques of operating Self Help Groups.

This person need not be a full-time employee of the group. This person can be

given a small remuneration. This person can look after 10-15 or more groups

in the locality.

Main functions of the agent (Motivator/Facilitator/Assistant) are:

Explaining the purpose and objective of a Self Help Group to

the target group;

18

Explaining group linkages (among themselves, with other

groups and with bank etc.);

Motivating prospective members to come forward to seek the

membership;

Holding preliminary meetings with prospective members;

Rights and duties of members;

Office-bearers of SHGs and their responsibilities and duties;

Importance of savings;

Identifying the functions which the group are to undertake;

Develop a business plan for the group;

Collect initial shares from members;

Recording the collections made;

Assistance in holding meetings;

Management of books of accounts and other registers;

Procedures of lending and repayment of loans;

Establishing contacts with lead banks etc.

The group decides who should be the motivator/facilitator, and also

takes decision on the continuity or removal of the person.

1.2.16 Sustainable Livelihoods of Women Self Help Groups

Sustainable livelihood approaches are people centered, recognizing

the capital assets of the poor and the influence of policies and institutions on

their livelihood strategies. In order to improve the decision-making of the

poor, it is necessary for those attempting to assist them to recognize the

19

heterogeneity of their local contexts. In this way, one-size fits-all

development solutions become less important, paving the way for more

pluralistic approaches. Rural livelihoods in particular are increasingly

understood to involve a diverse range of strategies, both within and outside

the agricultural sector. The role of women and youth in household income

generation must also be considered to be one of growing complexity,

including non-farm incomes such as remittances and wages from rural urban

migration of family members. It is clear that for information and

communication to benefit the rural poor, it needs to be relevant in the context

of the choices available to them and to assist them, to make decisions that

lead to improved livelihood options.

1.2.17 ICT and Women Self Help Groups in Tamil Nadu

A study carried out in Tamil Nadu, found that several Self Help

Groups have been formed and involved in various types of work, but the sole

aim is income generation. These Self Help Groups have opened various

centers which focus on the use of computer and significant media linkages of

different types. For example, firstly the presence of peripheral

equipment/particularly digital cameras, telephones, and printer/scanner/

photocopier have gradually made an impact comparable to the computer

itself, particularly in most rural groups, that have had the least access to

modern paraphernalia so far. The experiences of answering the phone for the

first time or using it to make a call, a technician at the local technical partner,

cannot be separated from the experience of using the computer themselves.

The use of the printer was a significant technical achievement for

some users, and it became a technical and social focus in its own right, not

just an adjunct to the computer. In Tamil Nadu, there is considerable

excitement about visual multimedia – computer drawing, digital photographs

and use of the power point. It can be argued that some Self Help Groups

20

divide the computer itself into multiple technologies: it is both a tool for

learning essential modern skills and at the same time, a visual medium for

personal expression and enjoyment through activities, such as drawing and

watching DVDs.

1.2.18 Role of Self Help Groups in the Application of the ICT

Since the ICT revolution took place in the early 1990s in India,

along with the literate and urban people, the middle and high class groups and

people in the rural areas were also highly benefited from it. During the initial

years, ICT’s application was only limited to a select few, but with the

intervention of International agencies along with the birth of liberalized

economy by the then Finance Minister, Dr. Manmohan Singh, the ICT spread

its avenues to the rural areas. To alleviate poverty which was prevailing

among the rural masses, the central government with some planned economy

started various rural developmental schemes to benefit the rural poor people.

One among them, created by the central government was the Sampoorna

Grameen Rojgar Yojana (SGSY), meant for women, though created by men.

Following the model from Bangladesh, this scheme worked well in the initial

years in states like Tamil Nadu, Kerala and Andhra Pradesh, while it failed

totally failed in the north India. However, this model also got stereotyped in

south India without further knowledge. The Self Help Group-bank linkage

programme was not sufficient for the Self Help Group members to run the

entrepreneurship for a long time. To overcome the various shortcoming

associated with the running of Self Help Groups, further knowledge was

required to smoothen the process. During that time the ICT intervened in the

Self Help Group sector and helped them to gain more knowledge in the area.

Through the successful strategies of the government of India and

the state governments along with the intervention of Self Help Groups, now

women (poor and illiterate) have been highly benefited by the ICT. VAPS

21

field researchers were able to evaluate some of the Self Help Groups,

composed mainly of women in five districts of Tamil Nadu, namely, Chennai,

Coimbatore, Madurai, Tiruchirapalli and Tirunelveli, and the benefit they

received from the application of the ICT.

1.2.19 ICT and Women Self Help Groups

Information and Communication Technologies (ICT) are for

everyone and women have to be equal beneficiaries to the advantages offered

by technology, and the products and processes which emerge from their use.

The benefits accrued from the synergy of knowledge and ICT need not be

restricted to the upper strata of the society but have to flow freely to all

segments of the female population. The gamut of areas in which a ICT can

bestow greater control in the hands of women is wide and continuously

expanding; namely, from managing water distribution at the village-level to

standing for local elections and having access to lifelong learning

opportunities. In convergence with other forms of communication the ICT has

the potential to reach those women who hitherto have not been reached by

any other media, thereby empowering them to participate in economic and

social progress, and make informed decisions on issues that affect them.

Like the urban-rural disparity, women are also divided on the basis

of economic and social positions in rural society, to understand their

information needs. Elite women in the rural sector are mainly from the landed

gentry class or from the highly sophisticated politically important families.

They are also usually from the upper castes. Their information needs are akin

to those of the urban elite women, except for the fact, that they are often

passive viewers in the changing socioeconomic scenario, because they are

bound by the upper caste traditions where patriarchy rules supreme. The rural

educated middle class women are more prone to change. They are in the

process of gradually breaking the caste and class barriers, and are working

22

towards better education and economic independence. They are in urgent

need of information regarding their new entitlements:

Educational opportunities outside the village

Job opportunities in both the formal and informal sectors

Government assistance programs for career advancement

within the bounds of tradition

Health services including sexual reproductive health

Modern child care facilities

Legal provisions to counter sexual harassment, domestic

violence and social injustice.

The largest group, which has been marginalized from getting any

need based information, is the rural poor. Though this is the most active group

of women in the rural sector, these women have never been specially

considered for information dissemination. An information system specially

designed for the rural poor, has to be need based, because this group has been

worst affected by the process of globalization. Their information needs will

encompass their economic, social and familial roles. Focusing on the

improved use of information and communication technologies, women can

broaden the scope of their actions and address issues, which were previously

beyond their capacity. For example, knowledge networking for influencing

decision-making strengthens the democratic processes, and brings recognition

to the power of women, as it enables the decision-making mechanism to

percolate right below to involve women at the grassroots level without being

concerned with the bureaucratic straitjacketed approach of the more formal

institutions (Nath 2000).

Across the globe, countries have recognized Information and

Communication Technology (ICT) as an effective tool in catalyzing the

23

economic activity in efficient governance, and in developing human

resources. There is a growing recognition of the newer and wider possibilities

that technology presents society in modern times. IT, together with

Communication Technologies has brought about unprecedented changes in

the way people communicate, and conduct business, pleasure and social

interaction. The evolution of new forms of technologies, and imaginative

forms of applications of the new and older technologies, makes the lives of

people better and more comfortable in several ways.

ICTs generally refer to an expanding assembly of technologies that

are used to handle information and aid communication. These include

hardware, software, media for collection, storage, processing, transmission

and presentation of information in any format (i.e., voice, data, text and

image), computers, the Internet, CD-ROMs, email, telephone, radio,

television, video, digital cameras etc. While the radio, television and print

media were primarily used to perform these tasks earlier, with the advent of

the new ICTs, these have now been considered as traditional ICTs. However,

many of these traditional ICTs are more effective than web-based solutions,

as they can resolve issues related to language, literacy or access to the

Internet.

The importance of Information and Communication Technologies

(ICT) in stimulating socio-economic development is widely recognized. The

ICT can create new types of economic activity, employment opportunities and

the improvements in the delivery of healthcare and other services. Universal

access to ICT can lead to a more capable work force and increase economic

efficiency. It can also enhance networking, participation and advocacy within

society, improve Government-Citizen interface and foster transparency and

accountability in governance. The digital divide constitutes a major barrier to

24

equitable and sustainable development, and bridging it can promote a nation's

growth.

With the shift towards a ‘knowledge society’, the role of

Information and communication technologies (ICTs), such as email and the

Internet in sustainable community and economic development is becoming

increasingly important (Mansell and Wehn 1998). It is well recognized that

ICT facilities can help to bridge the gender divide. In fact, women represent

an important part of the 'have-nots' within the digital divide, which bears a

mutually reinforcing or chicken and egg relationship with the gender divide.

Access to ICT can empower rural women by promoting basic literacy and

education, providing access to knowledge, employment opportunities,

banking services, government services and markets, and by facilitating their

health and safety. The ICT is an especially powerful tool as it can achieve

these desirable outcomes in a culturally acceptable manner, making pertinent

information, services and assistance available to women within their

homes/villages. ICTs have improved rural women’s access to new

information. However, many women don’t have the required support (human

networks and financial support) and access to complementary set of

knowledge and services to make use of this information. New information is

necessary but not sufficient to bring about women’s empowerment.

The “digital divide” threatens to exacerbate wide gaps between the

rich and poor, within and among countries. The stakes are indeed high.

Timely access to news and information can promote trade, education,

employment, health and wealth. One of the hallmarks of the information

society openness is a crucial ingredient of democracy and good governance.

Information and knowledge are at the heart of the efforts to strengthen

tolerance, mutual understanding and respect for diversity. To bridge the

digital divide, the only sustainable route is to reduce poverty. In the long run,

25

governments need to do much by enhancing access to education and health

care through distance learning and telemedicine. ICT can improve the quality

of life for poor rural communities who do not have access to these facilities.

Most of the ICT initiatives are related to disseminating new

information and knowledge useful for women, many of whom are not able to

make use of them, due to the lack of access to complementary sources of

support and services. Among the varied tools, knowledge centres and the

community radio were found to have the greatest potential, in reaching

women with locally relevant content. There is immense potential for the ICTs

to create new employment opportunities for rural women, and to contribute to

significant gains in efficiency and effectiveness in rural women enterprises.

Radio (All India Radio) and Television disseminate a wide range of

information relevant to socio-economic development, including agriculture,

health, rural employment, environment, e-governance etc. Women who have

access to these media have mostly benefited as passive recipients of generic

information and advice. However, with the addition of new programme

formats, such as phone-in-programmes, these media are now becoming more

interactive. Over the past few years, the Government of India, has invested

heavily in strengthening the ICT infrastructure, and has taken several policy

initiatives, to attract private sector investments in the ICT infrastructure and

service delivery. In response to this, access to ICTs has been growing at a

higher rate. Consequently, the digital divide, in terms of access to mobile

subscribers, fixed telephone lines, and the internet is getting smaller. Studies

have shown that some of these initiatives have also contributed to the

empowerment of women (Nath 2001, Gurumurthy 2006), even though,

Indian women still face huge imbalances in the ownership and access to many

of these technologies.

26

1.2.20 Research Background

The promotion of women's Self Help Groups is seen as an effective

means to empower poor women and enable them to participate in and drive

their own development. Self Help Groups are now recognized as a key

transmission belt for developmental efforts by the state and civil society. Such

village level collectives are a preferred institutional mechanism, because they

are gender sensitive, participatory, cost-effective and grassroots organizations.

1.3 SCOPE OF THE STUDY

Women have to be equal beneficiaries to the advantages offered by

technology, and its products and processes. However, it should not be

confined to an elite group of society, but flow to the other segments of women

in Indian society. This study wanted to know about the infrastructure (social,

economical, educational, etc) available to Self Help Groups, and the social

freedom and opportunities in rural areas. The applicability may invite

government intervention to narrow the digital divide among women, and also

to increase the empowerment of women with ICT usage. Everywhere the

potential exists for the media to make a far greater contribution to the

advancement of women. There are numerous possibilities for ICTs to improve

women’s economic activities in the field of trade, governance, education,

health, crafts, employment in the formal as well as the informal sectors. ICTs

bring a lot of opportunities to women in their work situations and small

business.

The present study attempts to examine the growth of women’s

Self Help Groups when information and communication technology are used

27

as supports for their development. The present study is from the standpoint of

the Self Help Group members.

1.4 OBJECTIVES OF THE STUDY

i) To study the impact of the training provided to Self Help

Groups on information and communication technology.

ii) To know the level of knowledge of information and

communication technology among Self Help Group women.

iii) To study the difficulties faced by them in using information

and communication technology, and find out the medium to

create awareness among Self Help Group women.

iv) To develop a model to overcome the digital divide.

1.5 RESEARCH QUESTIONS

i) To what extent do the Self Help Group women seek to use a

computer, mobile, or any other ICT tool?

ii) What is the relationship between the education levels of the

Self Help Group women and the use of ICT tools?

iii) What exactly is new about the access to and use of ICT as

compared to other sources of information?

iv) What is the level of ICT knowledge, and how has it benefited

the Self Help Group women? Is there a need for the Media to

bridge the gap?

v) What are the barriers for the Self Help Group women in

accessing ICT tools?

28

1.6 LIMITATIONS OF THE STUDY

i) The study was confined to women Self Help Groups belong to

only two districts of Tamil Nadu.

ii) The study relates to the period 2008 to 2011, and the

perception of the respondents, which may not be free from

their individual biases, in spite of the efforts to get them as

objectively as possible.

iii) The study focuses on the women Self Help Groups and their

development when they use ICT; other factors were not

considered.

1.7 ORGANISATION OF THESIS

Chapter 1 deals with the introduction, the background of the

emergence of Self Help Groups, their composition, methods of working and

their linkages with the financial institutions, and their empowerment for their

sustainability, research objectives, research questions, limitations of the study

and chapterization of the entire study.

Chapter 2, the Review of literature consists of the history of Self

Help Groups, their functions, the working of the Self Help Groups, the

importance of training, changing social norms and perceptions, and how the

Self Help Groups increase the woman’s influence over economic resources,

woman’s participation in social, community and political activities, and

unveiling empowerment of the Self Help Group, the role of ICT in the

development of Self Help Groups women.

Chapter 3 the primary data collected during the pre test and post

test while training the self help group women in 30 districts and on

establishing an information kiosk and its impacts is compiled. It also explains

29

the research methodology adopted in the study. The sampling method, size

and distribution, and the various statistical techniques adopted.

Chapter 4 discusses data analysis and interpretation. It includes the

tabulation of data, results of the various analyse, and the relevant, charts and

diagrams etc.

Chapter 5 gives the summary of the research findings, conclusion

and suggestions. It also includes the areas for further research.

![CHAPTER - 1 INTRODUCTIONshodhganga.inflibnet.ac.in/bitstream/10603/3456/8/08_chapter 1.pdf · 1 CHAPTER - 1 INTRODUCTION Analytical methods development, identification [1], characterization](https://static.fdocuments.in/doc/165x107/5ac6eb937f8b9acb688b4f32/chapter-1-in-1pdf1-chapter-1-introduction-analytical-methods-development-identification.jpg)