Chapter 06 Risk and Return. Value = + + + FCF 1 FCF 2 FCF ∞ (1 + WACC) 1 (1 + WACC) ∞ (1 + WACC)...

36

Chapter 06 Risk and Return

-

Upload

eugenia-oneal -

Category

Documents

-

view

229 -

download

1

Transcript of Chapter 06 Risk and Return. Value = + + + FCF 1 FCF 2 FCF ∞ (1 + WACC) 1 (1 + WACC) ∞ (1 + WACC)...

Chapter 06Risk and Return

Value = + + +FCF1 FCF2 FCF∞

(1 + WACC)1 (1 + WACC)∞(1 + WACC)2

Free cash flow(FCF)

Market interest rates

Firm’s business riskMarket risk aversion

Firm’s debt/equity mixCost of debt

Cost of equity

Cost of debt

Cost of equity

Weighted averagecost of capital

(WACC)

Net operatingprofit after taxes

Required investmentsin operating capital−

=

Determinants of Intrinsic Value:

The Cost of Equity

...

1. Risk of financial asset is judged by the risk of its cash flow

2. Asset risk: Stand Alone basis vs. Portfolio Context

3. Portfolio context: Diversifiable Risk vs. Market Risk.

4. Investors in general are Risk Averse

Important Notes

Stand alone risk: the risk an investor would face if she or he held only one particular asset.

Investment risk pertains to the probability of actually earning a low or negative return. The greater the chance of low or negative returns, the riskier the investment.

STAND ALONE RISK

.rP = r̂n

1=iii

r = expected rate of return.^

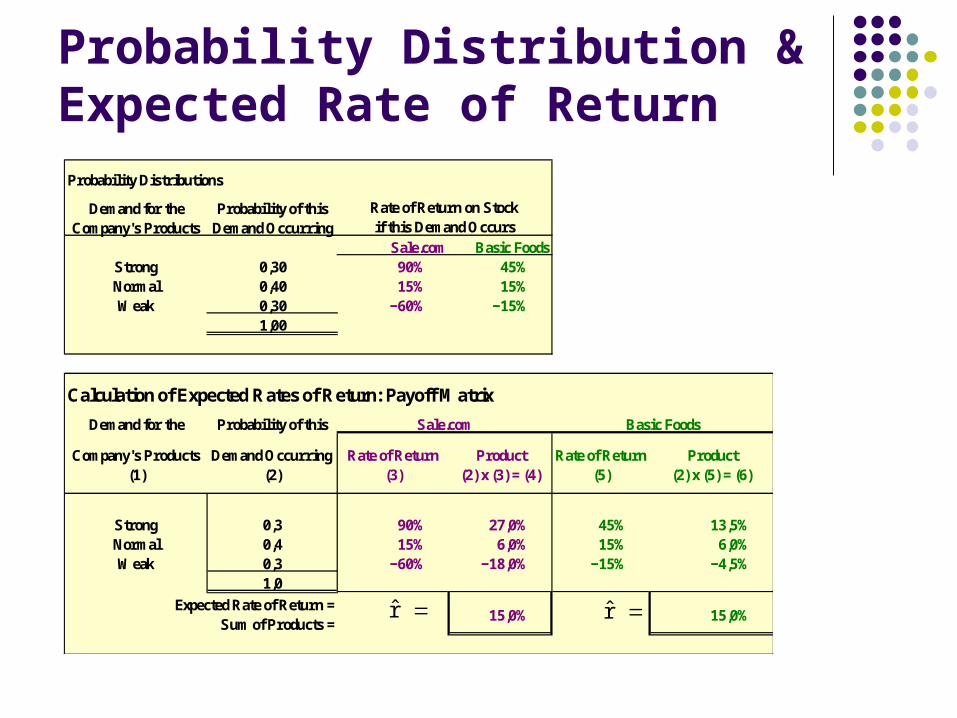

Probability Distribution & Expected Rate of Return

investedAmount

investedAmount - receivedAmount =

investedAmount

ReturnDollar return of rate

Probability Distribution & Expected Rate of Return

Probability Distributions

Demand for the Probability of thisCompany's Products Demand Occurring

Sale.com Basic FoodsStrong 0,30 90% 45%Normal 0,40 15% 15%Weak 0,30 −60% −15%

1,00

Calculation of Expected Rates of Return: Payoff Matrix

Demand for the Probability of this

Company's Products(1)

Demand Occurring(2)

Rate of Return(3)

Product(2) x (3) = (4)

Rate of Return(5)

Product(2) x (5) = (6)

Strong 0,3 90% 27,0% 45% 13,5%Normal 0,4 15% 6,0% 15% 6,0%Weak 0,3 −60% −18,0% −15% −4,5%

1,0

15,0% 15,0%

Sale.com Basic Foods

Rate of Return on Stockif this Demand Occurs

Expected Rate of Return = Sum of Products =

r̂r̂

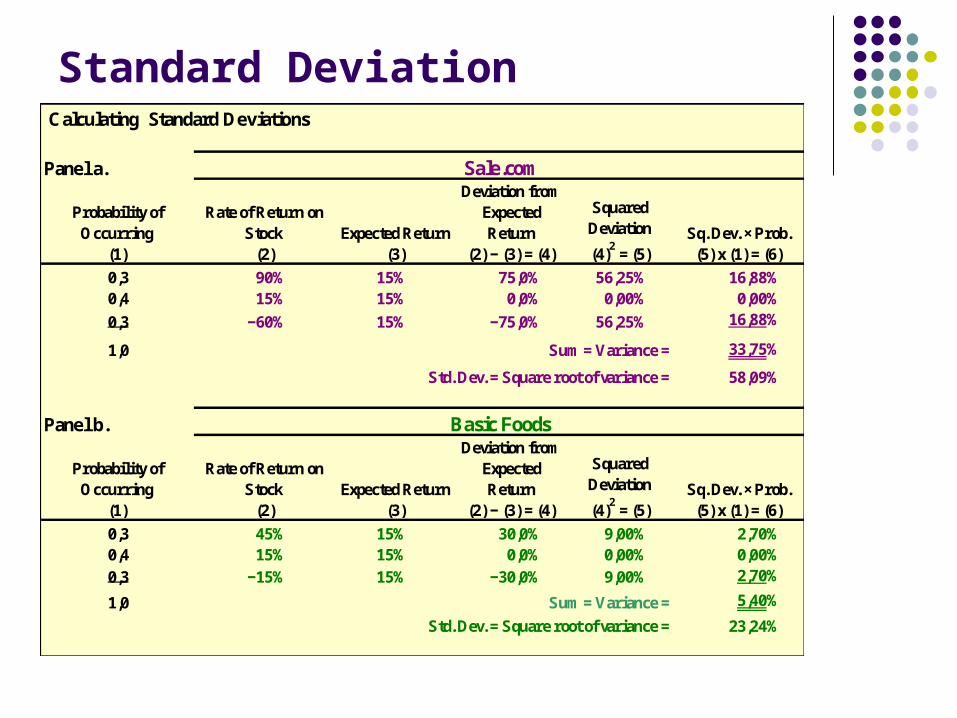

• Standard Deviation: a measure of the tightness of the probability distribution. The tighter the probability distribution, the smaller the Standard Deviation and the less risky the asset.

• Coefficient of Variation: Standard Deviation divided by return. It measures risk per unit of return, thus provides more standardized basis for risk profile comparison between assets with different return.

Stand Alone Risk: Measurements

Standard Deviation

n

1=ii

22 P)r̂(r -i

n

1=ii

2 P)r̂(r -i

Variance

Standard Deviation

Standard Deviation Calculating Standard Deviations

Panel a.

Probability of Occurring

(1)

Rate of Return on Stock

(2)Expected Return

(3)

Deviation from Expected Return

(2) − (3) = (4)

Squared Deviation

(4)2 = (5)

Sq. Dev. × Prob.(5) x (1) = (6)

0,3 90% 15% 75,0% 56,25% 16,88%0,4 15% 15% 0,0% 0,00% 0,00%

0,3 −60% 15% −75,0% 56,25% 16,88%

1,0 Sum = Variance = 33,75%

Std. Dev. = Square root of variance = 58,09%

Panel b.

Probability of Occurring

(1)

Rate of Return on Stock

(2)Expected Return

(3)

Deviation from Expected Return

(2) − (3) = (4)

Squared Deviation

(4)2 = (5)

Sq. Dev. × Prob.(5) x (1) = (6)

0,3 45% 15% 30,0% 9,00% 2,70%0,4 15% 15% 0,0% 0,00% 0,00%

0,3 −15% 15% −30,0% 9,00% 2,70%

1,0 Sum = Variance = 5,40%

Std. Dev. = Square root of variance = 23,24%

Sale.com

Basic Foods

Probability distribution

Expected Rate of Return

Rate ofreturn (%)

90150-60

Basic Foods

Sale.com

-15 45

The larger the Standard Deviation:•the lower the probability that actual returns will be close to the expected return•hence the larger the risk

Historical Data to Measure Standard Deviation

1

)rr( Estimated

n

1=t

2Avg-t

n

S

Standard Deviation

Standardized measure of dispersionabout the expected value:

Shows risk per unit of return.

CV = ^

r

Coefficient of Variation (CV)

0

A B

A = B , but A is riskier because largerprobability of losses.

= CVA > CVB.^r

rp is a weighted average:^

^ ^rp = wiri

n

i = 1

Risk & Return in Portfolio Context

Return

RiskCorrelation Coefficient to measure the tendency of two variables moving together

Portfolio Return

Stock Portfolio weight Expected ReturnMicrosoft 0,25 12,0%General Electric 0,25 11,5%Pfizer 0,25 10,0%Coca-Cola 0,25 9,5%

Portfolio's Expected Return 10,75%

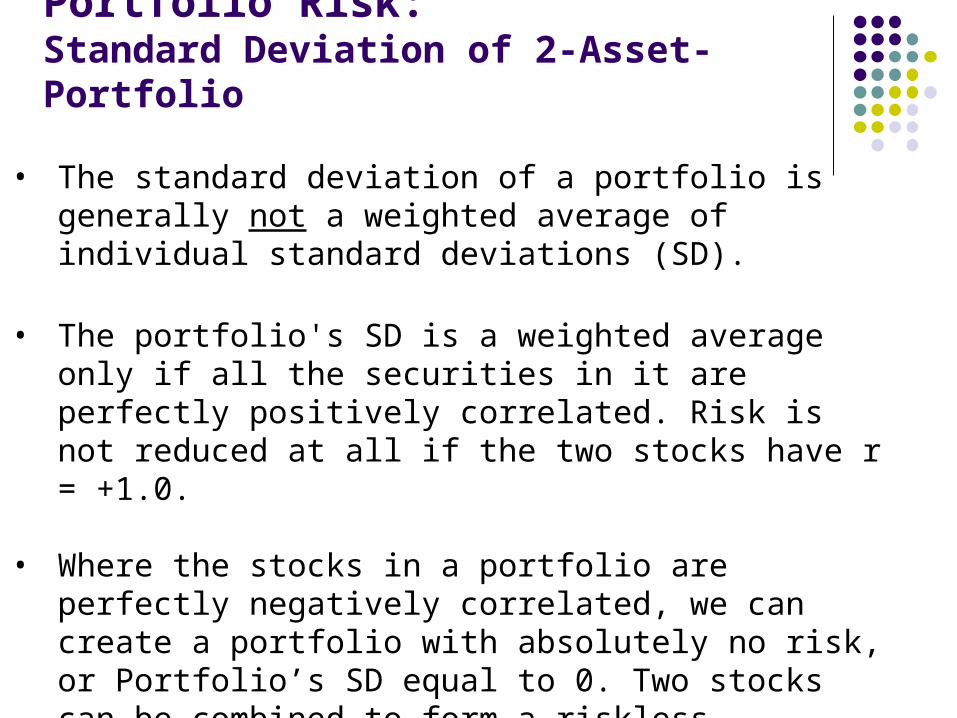

Portfolio Risk:Standard Deviation of 2-Asset-Portfolio

)(2 1221212

22

22

12

12 wwwwp

2pp

12211212 Cov

12Coeficientn Correlatio

Variance

Covariance

Standard Deviation

Portfolio Risk:Standard Deviation of 2-Asset-Portfolio

• The standard deviation of a portfolio is generally not a weighted average of individual standard deviations (SD).

• The portfolio's SD is a weighted average only if all the securities in it are perfectly positively correlated. Risk is not reduced at all if the two stocks have r = +1.0.

• Where the stocks in a portfolio are perfectly negatively correlated, we can create a portfolio with absolutely no risk, or Portfolio’s SD equal to 0. Two stocks can be combined to form a riskless portfolio if r = -1.0.

Portfolio Risk:Perfectly Negative Correlation

Portfolio WMYear Stock W returns Stock M returns (Equally weighted avg.)2000 40% -10% 15%2001 -10% 40% 15%2002 35% -5% 15%2003 -5% 35% 15%2004 15% 15% 15%

Average return 15% 15% 15%

Standard deviation 22.64% 22.64% 0.00%Correlation Coefficient -1.00

Returns Distribution for Two Perfectly Negatively Correlated Stocks (ρ = -1.0) and for Portfolio WM

40

15

0

-10 -10 -10

0 0

15 15

40 40

Stock W Stock M Portfolio WM

..

. .

.

.

..

.. . . . .

Portfolio Risk:Perfectly Positive Correlation

Year Stock M returns Stock M' returns Portfolio MM'2000 -10% -10% -10%2001 40% 40% 40%2002 -5% -5% -5%2003 35% 35% 35%2004 15% 15% 15%

Average return 15% 15% 15%

Standard deviation 22,64% 22,64% 22,64%Correlation Coefficient 1,00

Returns Distributions for Two Perfectly Positively Correlated Stocks (ρ= +1.0) and for Portfolio MM’

Stock M

0

15

40

-10

Stock M’

0

15

40

-10

Portfolio MM’

0

15

40

-10

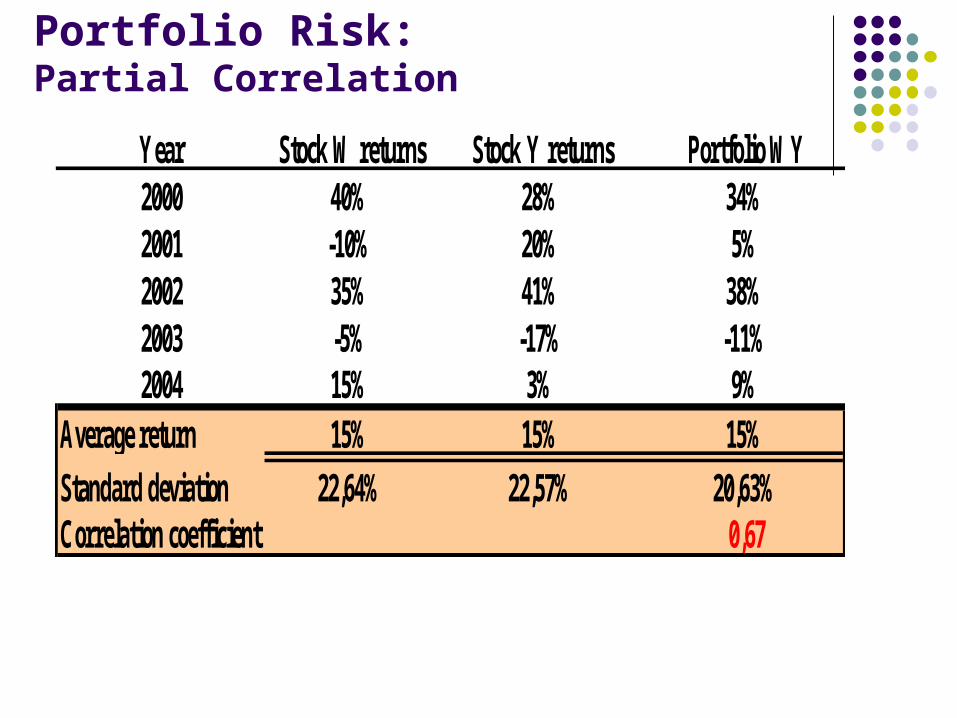

Portfolio Risk:Partial Correlation

Year Stock W returns Stock Y returns Portfolio WY2000 40% 28% 34%2001 -10% 20% 5%2002 35% 41% 38%2003 -5% -17% -11%2004 15% 3% 9%

Average return 15% 15% 15%

Standard deviation 22,64% 22,57% 20,63%Correlation coefficient 0,67

23

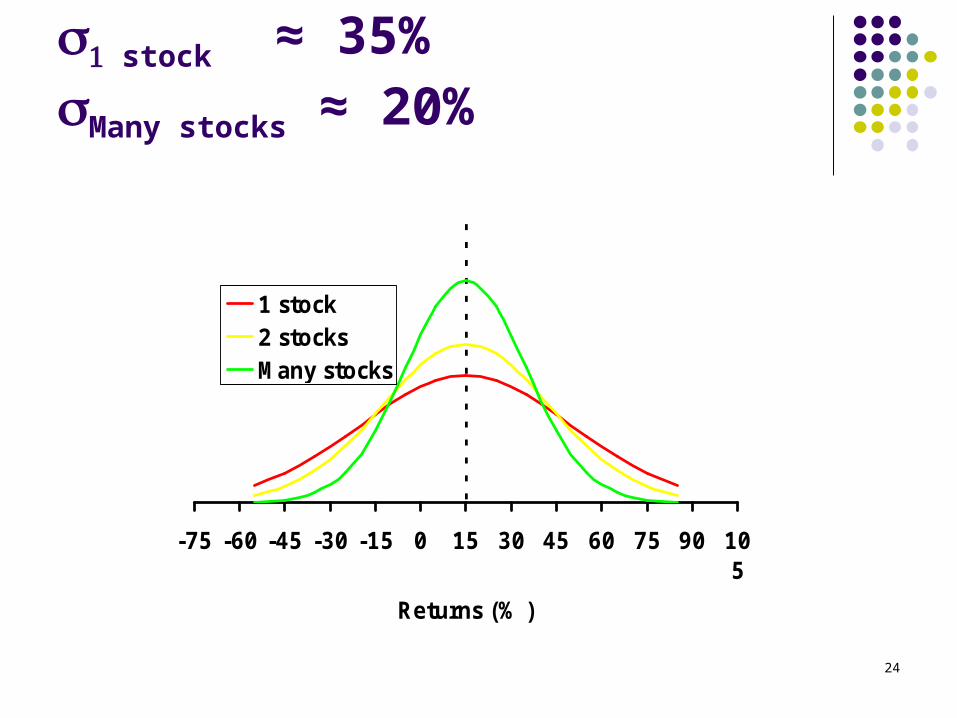

Adding Stocks to a Portfolio

What would happen to the risk of an average 1-stock portfolio as more randomly selected stocks were added?

p would decrease because the added stocks would not be perfectly correlated, but the expected portfolio return would remain relatively constant.

24

stock ≈ 35%Many stocks ≈ 20%

-75 -60 -45 -30 -15 0 15 30 45 60 75 90 105

Returns (% )

1 stock2 stocksMany stocks

# Stocks in Portfolio10 20 30 40 2,000+

Company Specific Risk

Market Risk

20

0

Stand-Alone Risk, p

p (%)

35

Effects of Portfolio Size on Portfolio Risk

Market risk is that part of a security’s stand-alone risk that cannot be eliminated by diversification, and is measured by beta.

Firm-specific risk is that part of a security’s stand-alone risk that can be eliminated by proper diversification.

Capital Asset Pricing Model (CAPM): relevant risk of individual stock is the amount of risk that the stock contributes to well-diversified stock portfolio, or the market portfolio.

Market risk, which is relevant for stocks held in well-diversified portfolios, is defined as the contribution of a security to the overall riskiness of the portfolio. It is measured by a stock’s beta coefficient.

Beta measures a stock’s market risk. It shows a stock’s volatility relative to the market. Beta shows how risky a stock is if the stock is held in a well-diversified portfolio. Beta can be calculated by running a regression of past returns on Stock i versus

returns on the market. The slope of the regression line is defined as the beta coefficient.

If beta > 1.0, stock is riskier than the market. If beta < 1.0, stock less risky than the market.

Capital Asset Pricing Model & The Concept of Beta

MiM

iib ,

28

Using a Regression to Estimate Beta

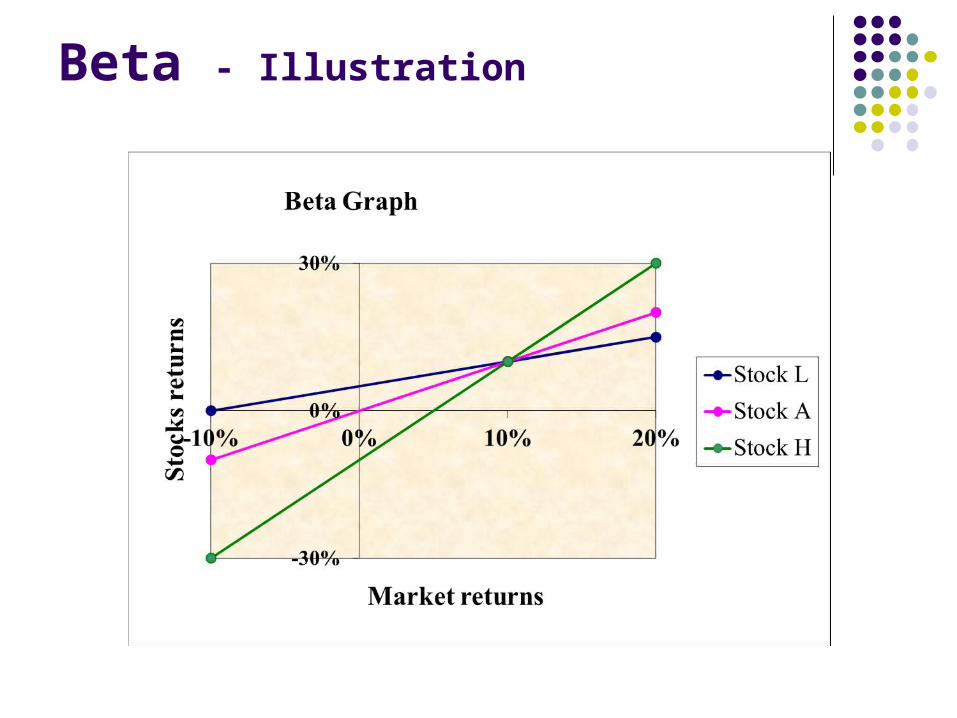

Run a regression with returns on the stock in question plotted on the Y axis and returns on the market portfolio plotted on the X axis.

The slope of the regression line, which measures relative volatility, is defined as the stock’s beta coefficient, or b.

Beta - Illustration

30

Calculating Beta in Practice

Many analysts use the S&P 500 to find the market return.

Analysts typically use four or five years’ of monthly returns to establish the regression line.

Some analysts use 52 weeks of weekly returns.

Beta - Calculation

CALCULATING THE BETA COEFFICIENT FOR AN ACTUAL COMPANYNow we show how to calculate beta for an actual company, General Electric.

Step 1. Acquire DataStep 2. Calculate Returns

DateMarket Level

(S&P 500 Index) Market ReturnGE Adjusted Stock

Price GE ReturnMaret 2003 848,18 0,8% 25,50 6,0%Februari 2003 841,15 -1,7% 24,05 4,7%Maret 1999 1.286,37 NA 34,42 NA

Average return (annual) -8,8% -3,4%Standard deviation (annual) 17,6% 29,2%Correlation between GE and the market. 66,0%Beta (using the SLOPE function) 1,09

32

How is beta interpreted?

If b = 1.0, stock has average risk. If b > 1.0, stock is riskier than average. If b < 1.0, stock is less risky than average. Most stocks have betas in the range of 0.5 to

1.5.

ri = Required return on Stock i rRF = Risk-free return (rM-rRF) = Market risk premium bi = Beta of Stock i

ri = rRF + (rM – rRF)bi .

^

Security Market Line (SML)Relationship between required rate of return and risk

ri = rRF + RPMbi .

34

Use the SML to calculate eachalternative’s required return.

The Security Market Line (SML) is part of the Capital Asset Pricing Model (CAPM).

SML: ri = rRF + (RPM)bi .

Assume rRF = 8%; rM = rM = 15%.

RPM = (rM - rRF) = 15% - 8% = 7%.

35

SML1

Original situation

r (%)

SML2

0 0.5 1.0 1.5 Risk, bi

1815

11 8

New SML I = 3%

Impact of Inflation Change on SML

36

SML1

Original situation

r (%)SML2

After change

Risk, bi

18

15

8

1.0

RPM = 3%

Impact of Risk Aversion Change