Chapter 03 working capital 1ce lecture

54

3 Chapte r The Management of Working Capital rsheed Ahmad Bhat artment of Hospital Administration

-

Upload

cma-khursheed-ahmad-bhat -

Category

Documents

-

view

78 -

download

0

Transcript of Chapter 03 working capital 1ce lecture

33Chapt

er

Chapt

er The Management of

Working Capital

Khursheed Ahmad BhatHODDepartment of Hospital Administration

2Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU

Chapter 3 – Outline (1)

• Working Capital Basics Working Capital and the Current Accounts Working Capital and Funding Requirements Objective of Working Capital Management Working Capital Trade-offs Operations—The Cash Conversion Cycle The Operating Cycle and the Cash Conversion Cycle

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU3

Chapter 3 – Outline (2)

Permanent and Temporary Working Capital Maturity Matching Principle Financing Net working Capital Short-Term vs. Long-Term Financing Working Capital Policy

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU4

• Working capital typically means the firm’s holding of current or short-

term assets such as cash, receivables, inventory and marketable

securities.

• These items are also referred to as circulating capital

• Corporate executives devote a considerable amount of attention to the

management of working capital.

Working capital Introduction

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU5

Working Capital Basics

• Working Capital Assets/liabilities required to operate business on day-to-

day basis• Cash• Accounts Receivable• Inventory• Accounts Payable• Accruals

Short-term in nature—turn over regularly

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU6

Concepts of Working Capital

• There are two possible interpretations of working capital concept:

1. Balance sheet concept2. Operating cycle conceptBalance sheet concept

There are two interpretations of working capital under the balance sheet concept. a. Excess of current assets over current liabilities.(CA-CL)

b. Gross or total current assets.(Fixed Assets + Current Assets)

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU7

Working Capital and the Current Accounts

• Gross working capital = Current assets Gross Working Capital (GWC) represents investment in

current assets

• (Net) working capital = Current assets – Current liabilities

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU8

Working Capital and Funding Requirements

• Spontaneous Financing Firm will also always have minimum level of Accounts

Payable—in effect, money you have borrowed• Accounts Payable (and Accruals) are generated spontaneously

• Arise automatically with inventory and expenses • Offset the funding required to support current assets

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU9

Working Capital and Funding Requirements

• Working Capital Requires Funds Maintaining working capital balance requires permanent

commitment of funds• Example: Firm will always have minimum level of Inventory,

Accounts Receivable, and Cash—this requires funding

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU10

Working Capital and Funding Requirements

• Net working capital is Gross Working Capital – Current Liabilities (including spontaneous financing)

Reflects net amount of funds needed to support routine operations

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU11

Concepts Continues 2• Excess of current assets over current liabilities are called the net

working capital or net current assets.

• Working capital is really what a part of long term finance is locked in and used for supporting current activities.

• The balance sheet definition of working capital is meaningful only as an indication of the firm’s current solvency in repaying its creditors.

• When firms speak of shortage of working capital they in fact possibly imply scarcity of cash resources.

• In fund flow analysis an increase in working capital, as conventionally defined, represents employment or application of funds.

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU12

• Operating cycle concept• A company’s operating cycle typically consists of three primary

activities: Purchasing resources, Producing the product and Distributing (selling) the product.

These activities create funds flows that are both unsynchronized and uncertain.Unsynchronized because cash disbursements (for example, payments for resource purchases) usually take place before cash receipts (for example collection of receivables).

They are uncertain because future sales and costs, which generate the respective receipts and disbursements, cannot be forecasted with complete accuracy.

Concepts Continues 3

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU13

“ circulating capital means current assets of a company that are changed in the ordinary course of business from one form to another, as for example, from cash to inventories, inventories to receivables, receivable to cash”

Genestenbreg

Concepts Continues 4

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU14

Objective of Working Capital Management

• To run firm efficiently with as little money as possible tied up in Working Capital Involves trade-offs between easier operation and cost of

carrying short-term assets• Benefit of low working capital

• Money otherwise tied up in current assets can be invested in activities that generate higher payoff

• Reduces need for costly financing

• Cost of low working capital• Risk of shortages in cash, inventory

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU15

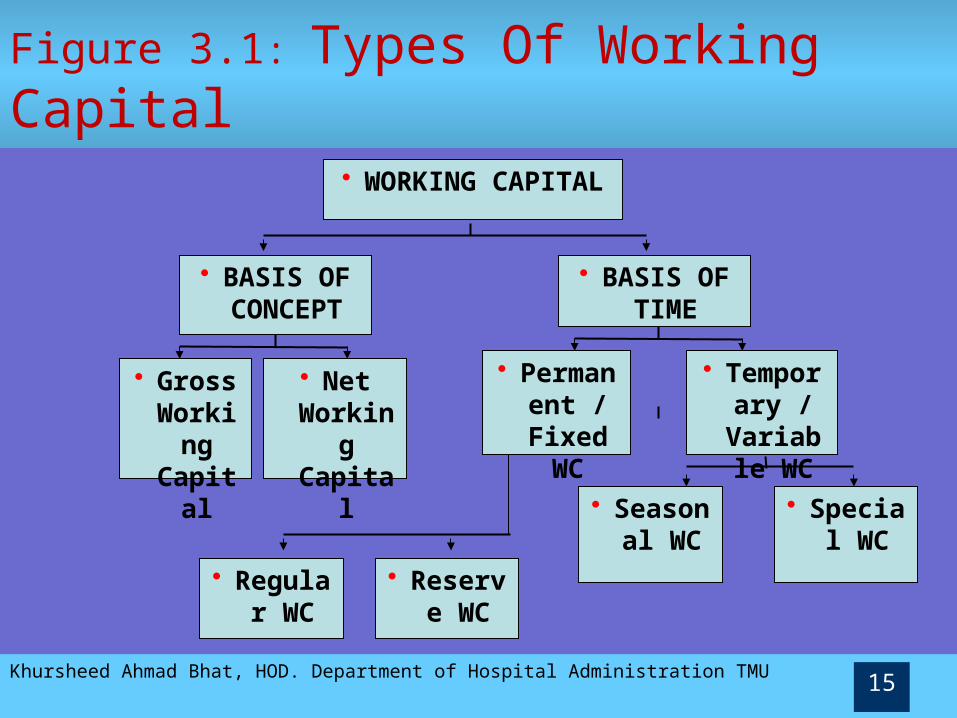

Figure 3.1: Types Of Working Capital

• WORKING CAPITAL

• BASIS OF CONCEPT

• BASIS OF TIME

• Gross Workin

g Capital

• Net Working Capital

• Permanent /

Fixed WC

• Temporary /

Variable WC

• Regular WC

• Reserve WC

• Seasonal WC

• Special WC

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU16

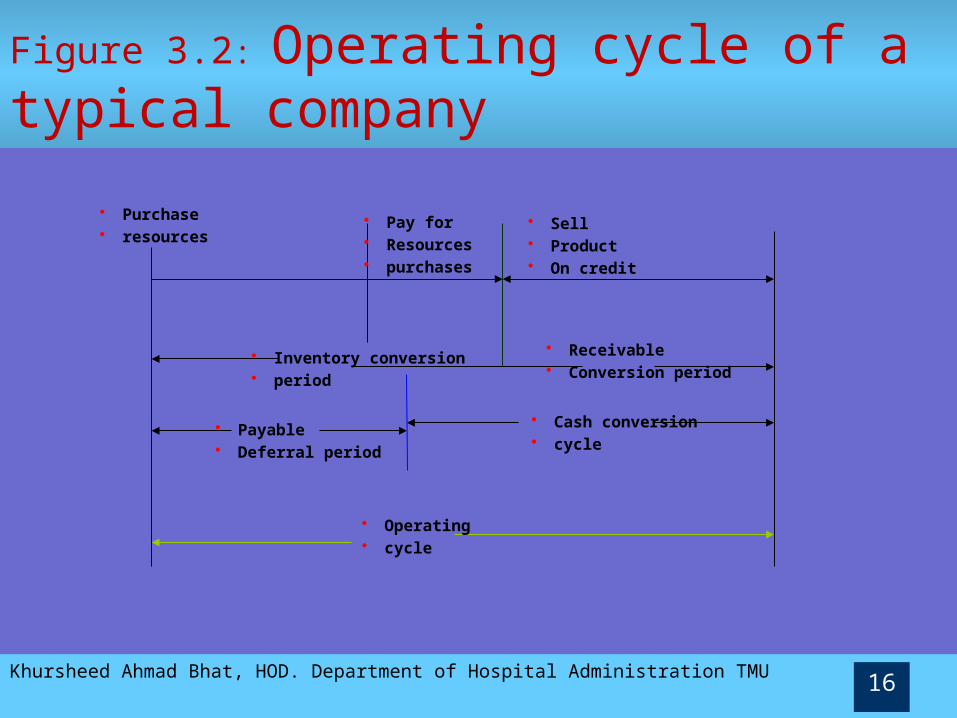

Figure 3.2: Operating cycle of a typical company

• Payable • Deferral period

• Inventory conversion• period

• Cash conversion• cycle

• Operating • cycle

• Pay for• Resources• purchases

• Purchase• resources

• Sell• Product• On credit

• Receivable • Conversion period

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU17

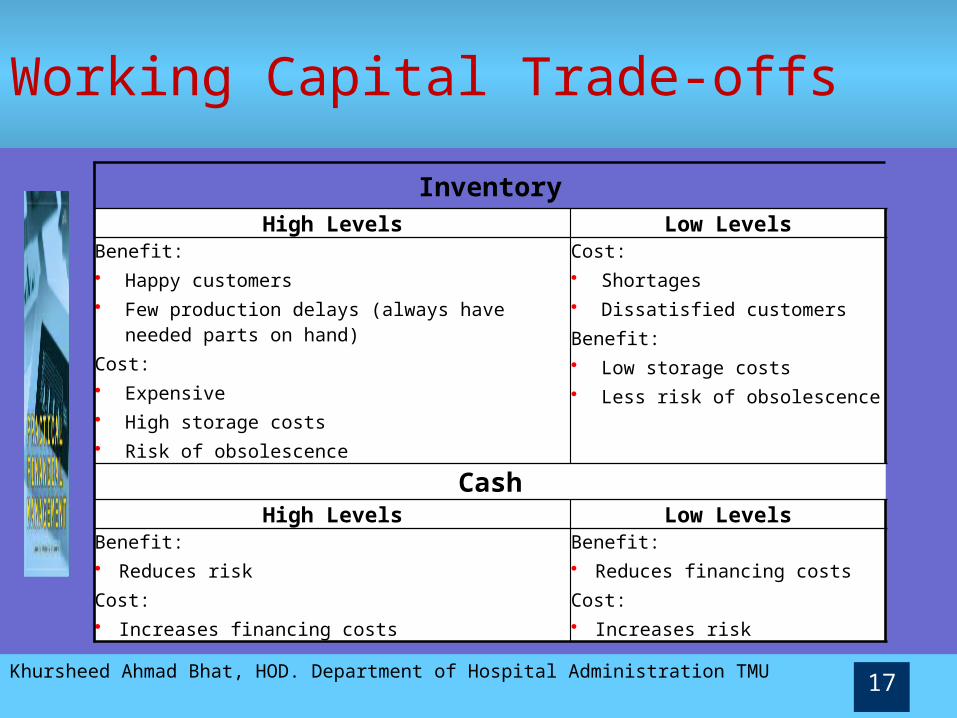

Working Capital Trade-offs

InventoryHigh Levels Low Levels

Benefit: • Happy customers• Few production delays (always have needed

parts on hand)Cost: • Expensive• High storage costs• Risk of obsolescence

Cost: • Shortages• Dissatisfied customersBenefit: • Low storage costs• Less risk of obsolescence

CashHigh Levels Low Levels

Benefit:• Reduces riskCost:• Increases financing costs

Benefit:• Reduces financing costsCost:• Increases risk

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU18

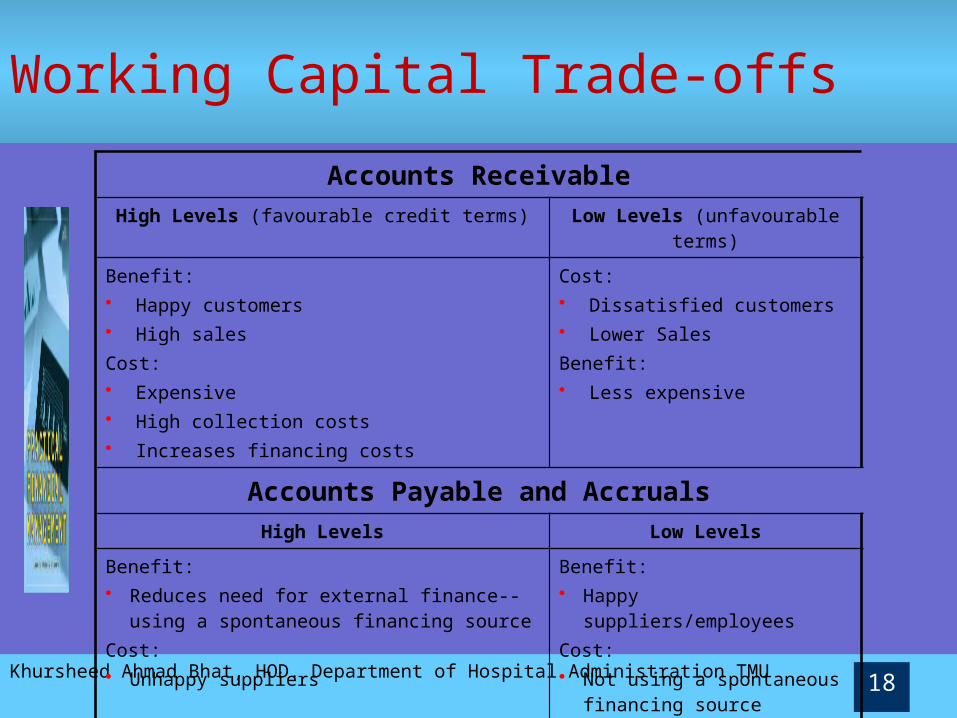

Working Capital Trade-offs

Accounts ReceivableHigh Levels (favourable credit terms) Low Levels (unfavourable

terms)

Benefit: • Happy customers• High salesCost: • Expensive• High collection costs• Increases financing costs

Cost: • Dissatisfied customers• Lower SalesBenefit: • Less expensive

Accounts Payable and AccrualsHigh Levels Low Levels

Benefit:• Reduces need for external finance--using a

spontaneous financing sourceCost:• Unhappy suppliers

Benefit:• Happy suppliers/employeesCost:• Not using a spontaneous

financing source

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU19

Current Assets High Level Low Level

Profitability Lower HigherRisk Lower Higher

Working Capital Trade-offs

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU20

Operations—The Cash Conversion Cycle

• Firm begins with cash which then “becomes” inventory and labour Which then becomes product for sale Eventually this will turn into cash again

• Firm’s operating cycle is time from acquisition of inventory until cash is collected from product sales

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU21

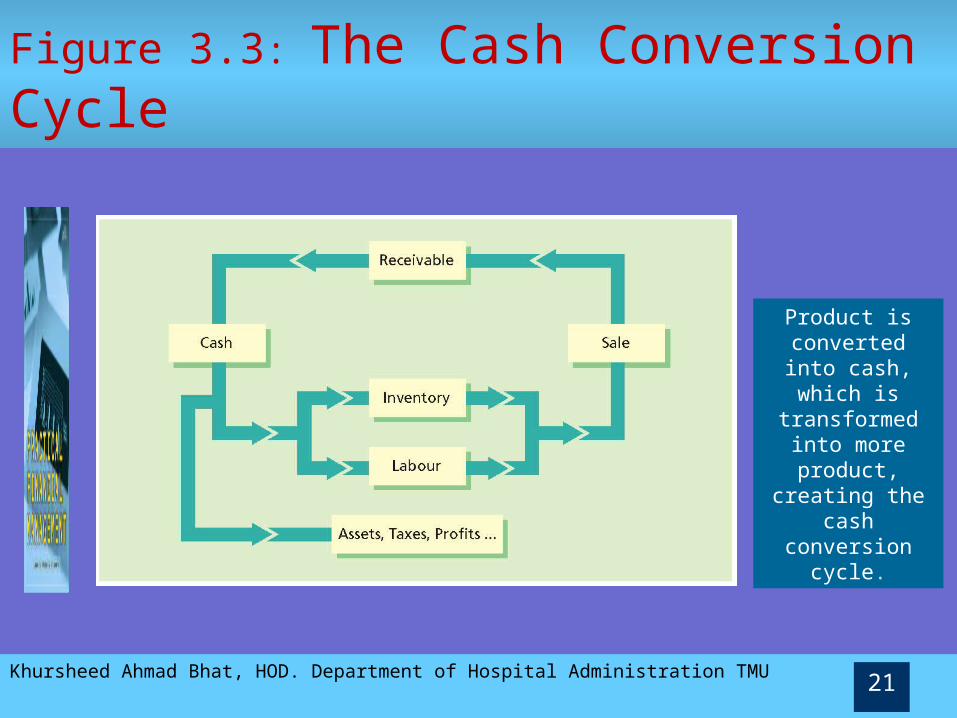

Figure 3.3: The Cash Conversion Cycle

Product is converted into cash,

which is transformed into

more product, creating the cash conversion cycle.

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU22

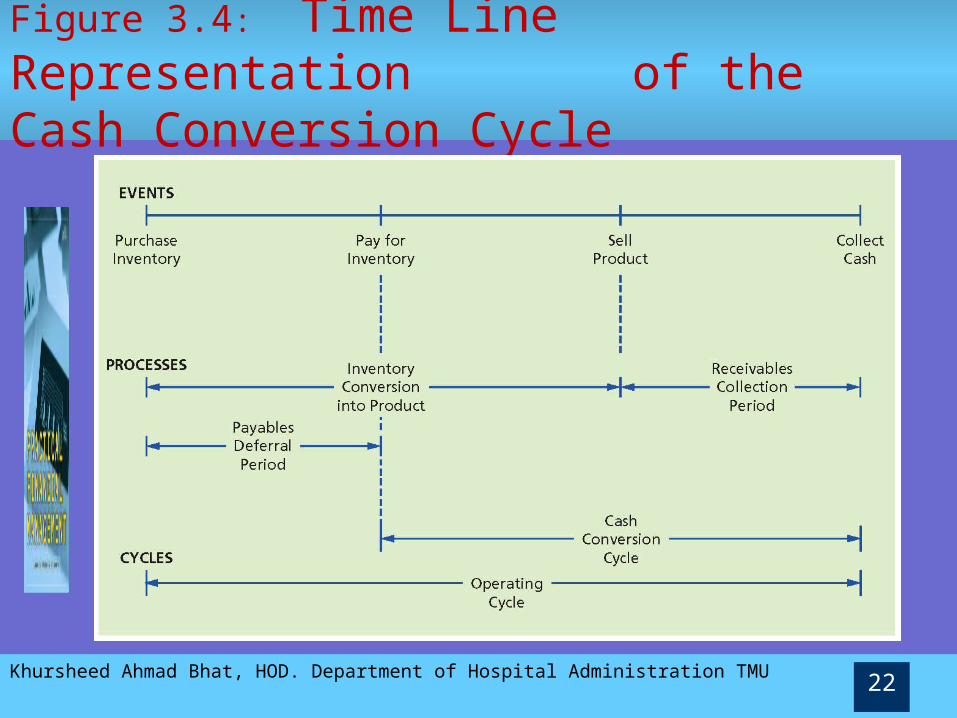

Figure 3.4: Time Line Representation of the Cash Conversion Cycle

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU23

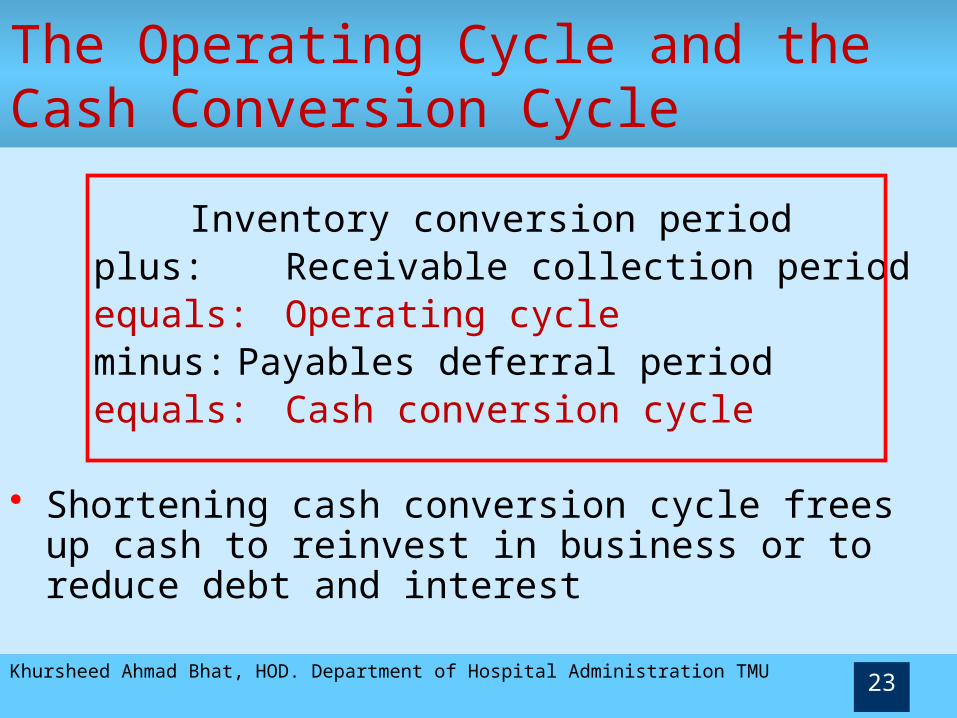

The Operating Cycle and the Cash Conversion Cycle

Inventory conversion periodplus: Receivable collection periodequals: Operating cycleminus: Payables deferral periodequals: Cash conversion cycle

• Shortening cash conversion cycle frees up cash to reinvest in business or to reduce debt and interest

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU24

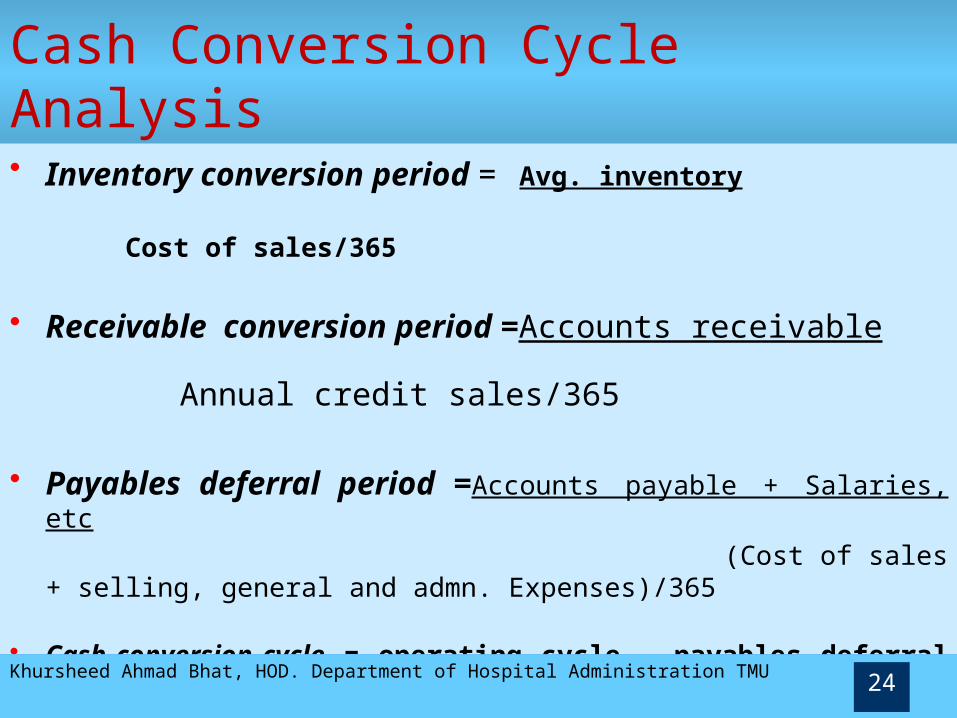

Cash Conversion Cycle Analysis

• Inventory conversion period = Avg. inventory

Cost of sales/365

• Receivable conversion period =Accounts receivable Annual credit sales/365

• Payables deferral period =Accounts payable + Salaries, etc

(Cost of sales + selling, general and admn. Expenses)/365

• Cash conversion cycle = operating cycle – payables deferral period.

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU25

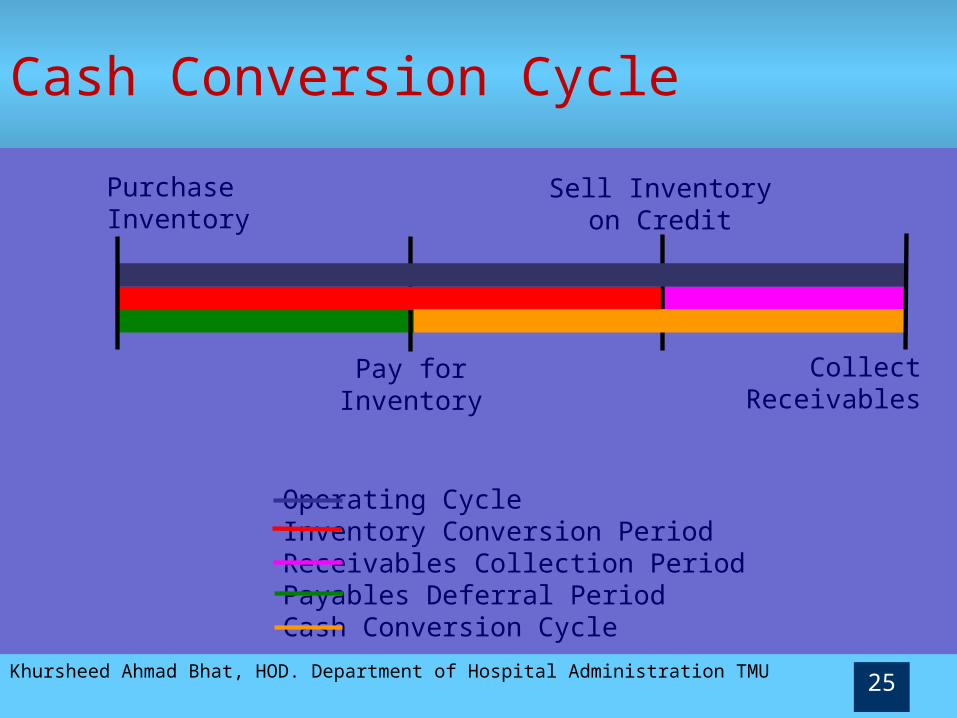

Cash Conversion Cycle

PurchaseInventory

Pay forInventory

Sell Inventoryon Credit

CollectReceivables

Operating CycleInventory Conversion PeriodReceivables Collection PeriodPayables Deferral PeriodCash Conversion Cycle

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU26

Importance of working capital

• Importance of working capital Risk and uncertainty involved in managing the cash flows Uncertainty in demand and supply of goods, escalation in cost both

operating and financing costs.• Strategies to overcome the problem

Manage working capital investment or financing such as

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU27

Importance of working capital

Holding additional cash balances beyond expected needs Holding a reserve of short term marketable securities Arrange for availability of additional short-term borrowing

capacity One of the ways to address the problem of fixed set-up cost may

be to hold inventory. One or combination of the above strategies will target the problem

• Working capital cycle is the life-blood of the firm

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU28

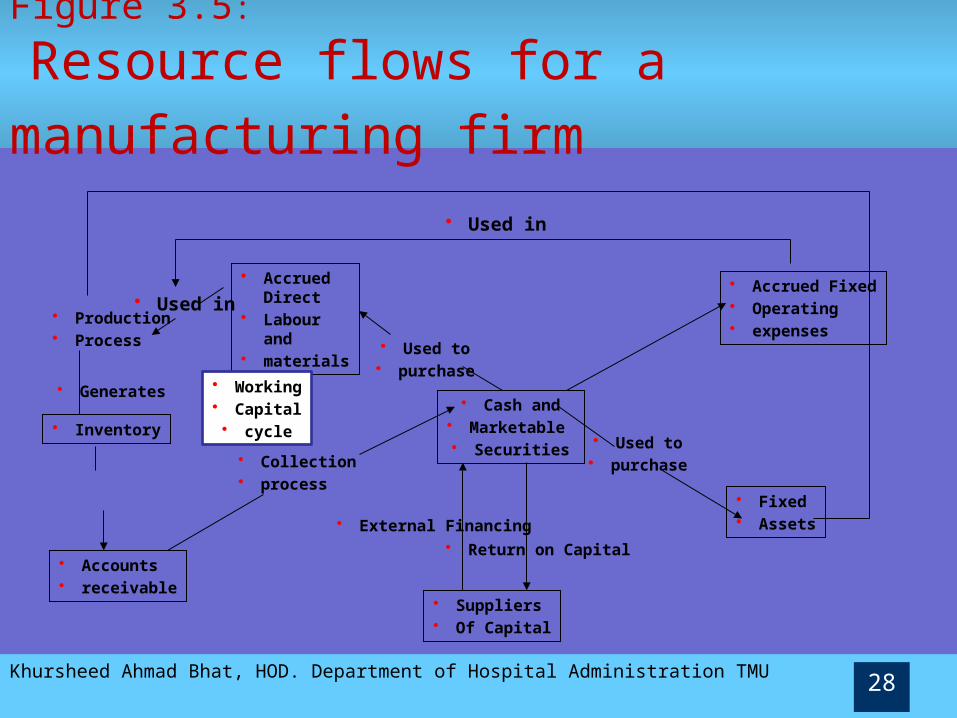

Figure 3.5:

Resource flows for a manufacturing firm

• Fixed • Assets

• Production• Process

• Generates

• Inventory

• Accounts • receivable

• Used in

• Accrued Direct

• Labour and

• materials

• Accrued Fixed• Operating• expenses

• Cash and• Marketable • Securities

• Suppliers• Of Capital

• External Financing • Return on Capital

• Collection • process

• Used to• purchase

• Used to• purchase

• Used in

• Working• Capital• cycle

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU29

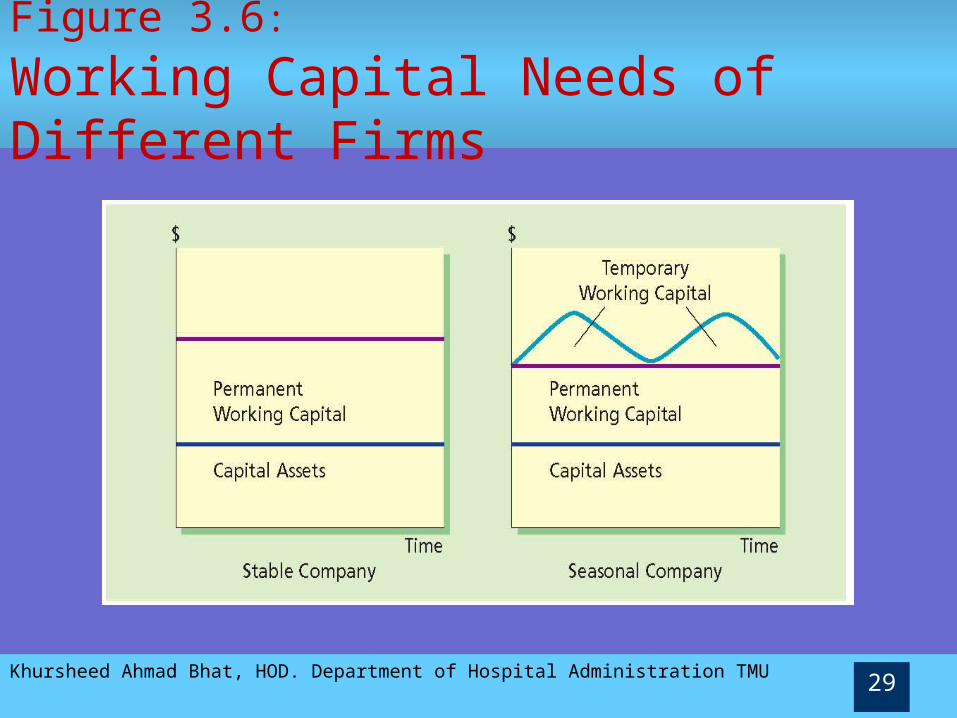

Figure 3.6: Working Capital Needs of Different Firms

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU30

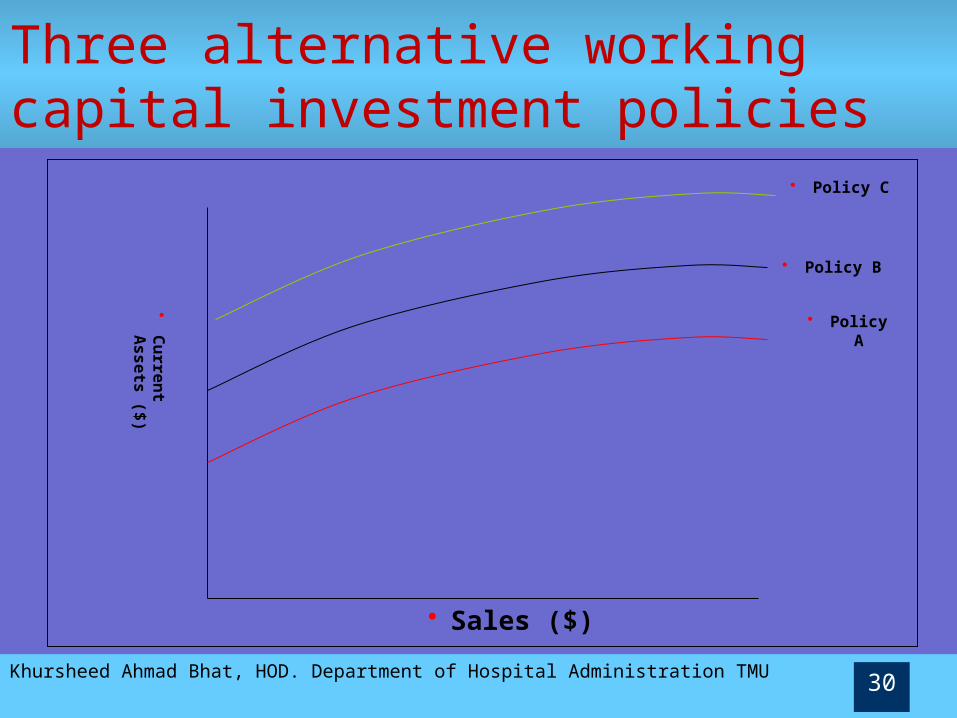

Three alternative working capital investment policies

• Sales ($)

•C

urr

en

t A

ssets

($

)• Policy C

• Policy A

• Policy B

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU31

Three alternative working capital investment policies-2• Policy C represents conservative approach• Policy A represents aggressive approach • Policy B represents a moderate approach

• Optimal level of working capital investment

• Risk of long-term versus short-term debt

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU32

Permanent and Temporary Working Capital

• Working capital is permanent to the extent that it supports constant or minimum level of sales

• Temporary working capital supports seasonal peaks in business

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU33

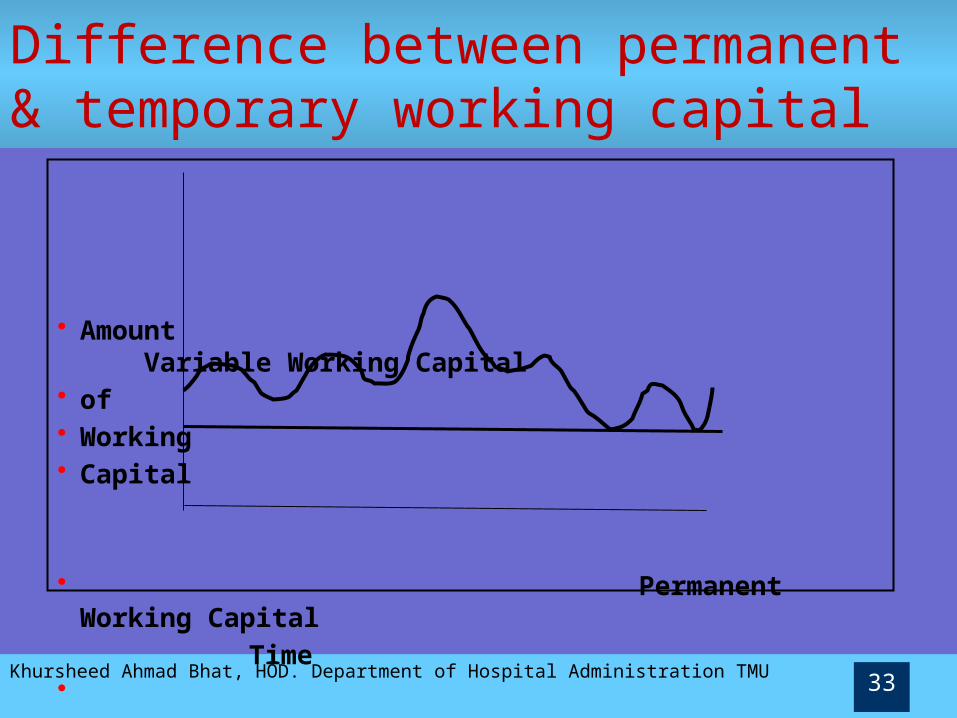

• Amount Variable Working Capital• of • Working• Capital

• Permanent Working Capital

Time•

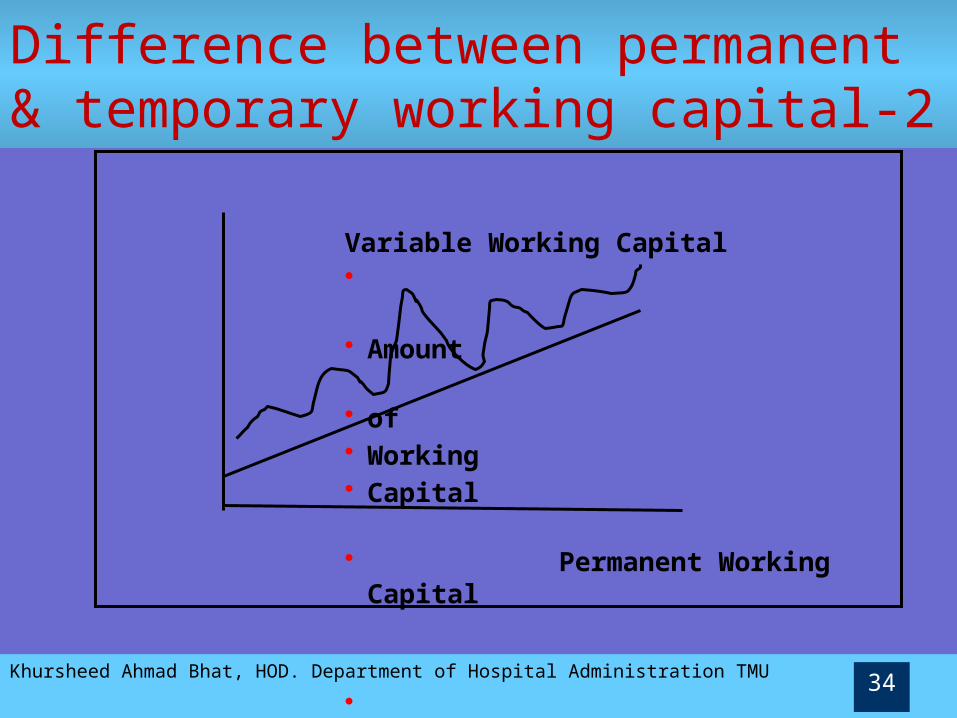

Difference between permanent & temporary working capital

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU34

Difference between permanent & temporary working capital-2

Variable Working Capital• • Amount • of • Working• Capital • Permanent

Working Capital

• • Time•

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU35

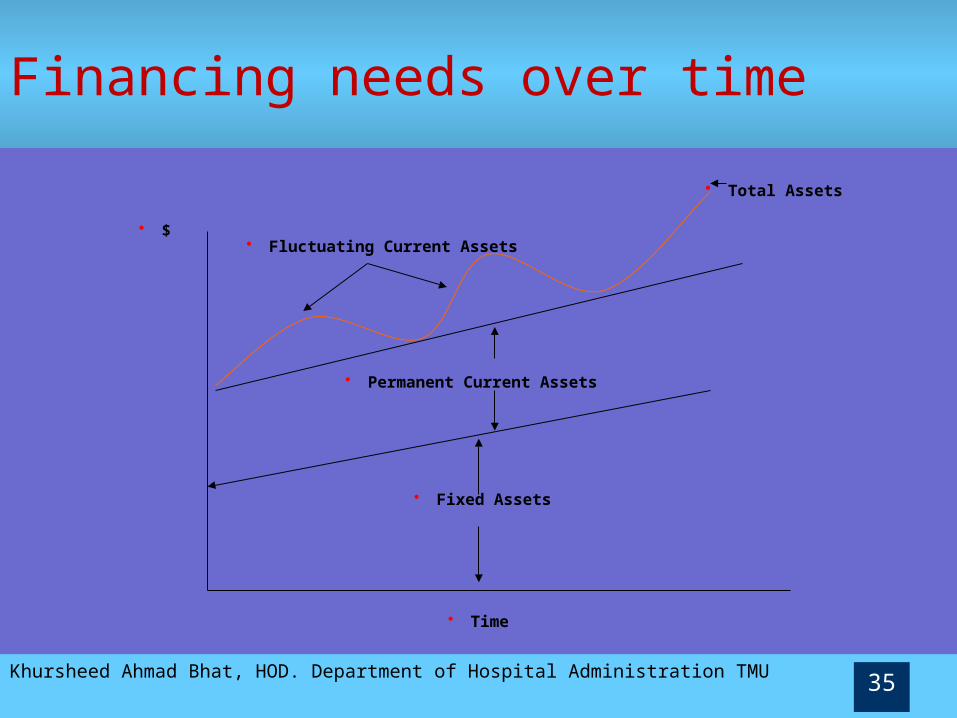

Financing needs over time

• Fixed Assets

• Permanent Current Assets

• Total Assets

• Fluctuating Current Assets

• Time

• $

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU36

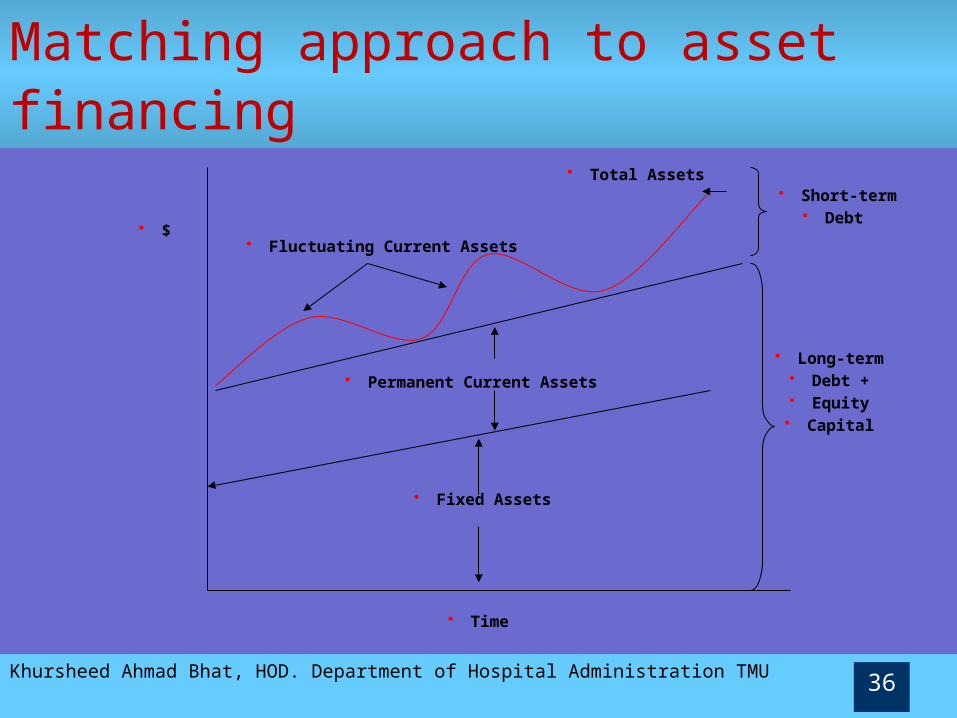

Matching approach to asset financing

• Fixed Assets

• Permanent Current Assets

• Total Assets

• Fluctuating Current Assets

• Time

• $

• Short-term• Debt

• Long-term• Debt +• Equity• Capital

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU37

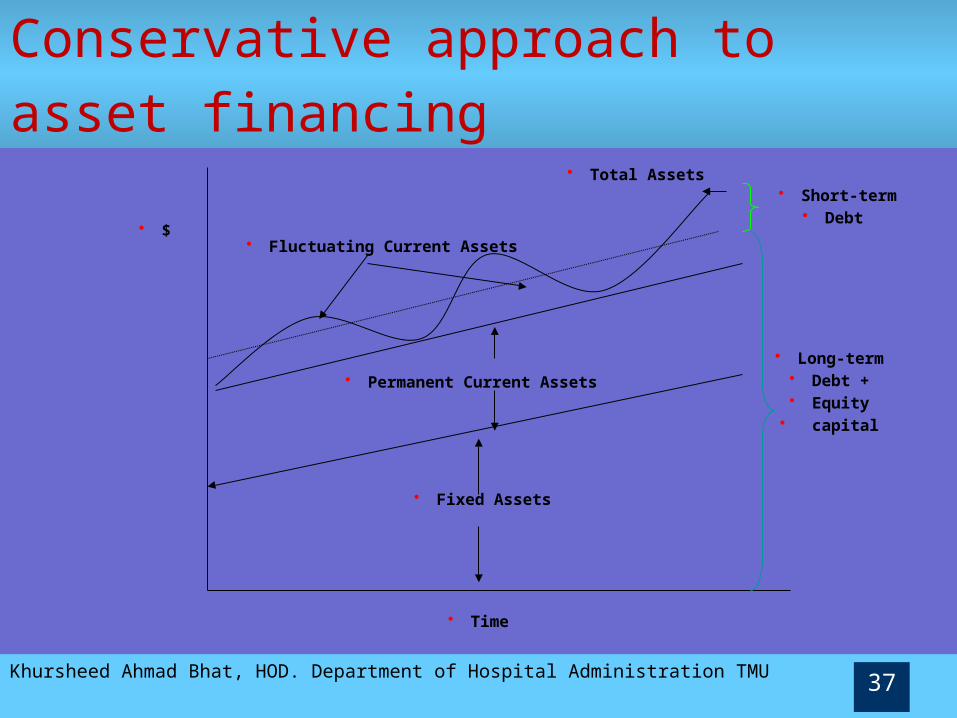

Conservative approach to asset financing

• Fixed Assets

• Permanent Current Assets

• Total Assets

• Fluctuating Current Assets

• Time

• $

• Short-term• Debt

• Long-term• Debt +• Equity• capital

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU38

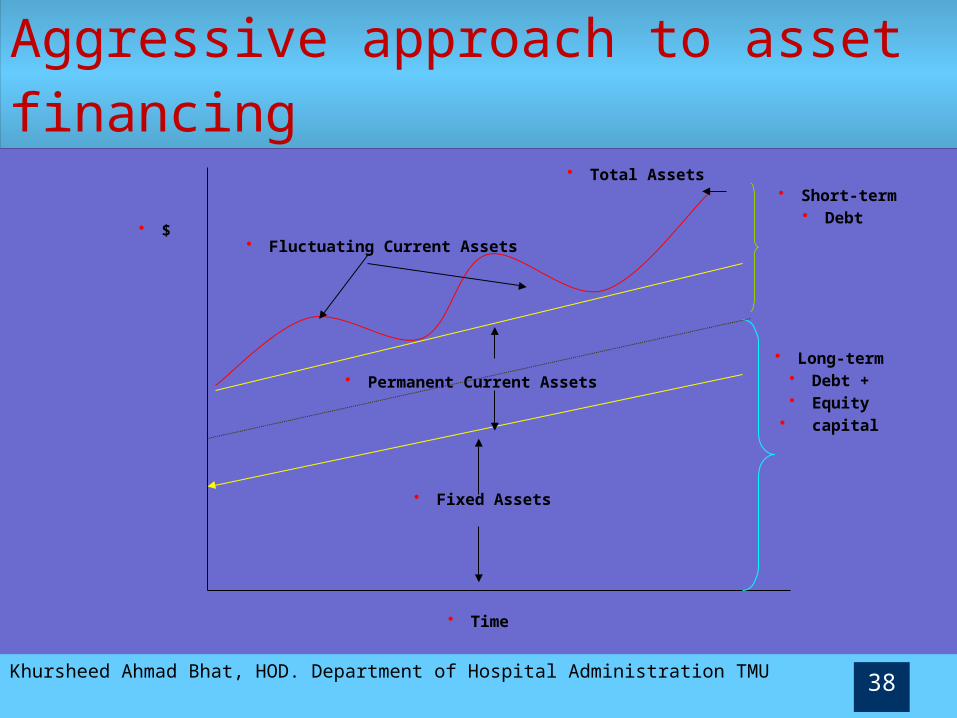

• Fixed Assets

• Permanent Current Assets

• Total Assets

• Fluctuating Current Assets

• Time

• $

• Short-term• Debt

• Long-term• Debt +• Equity• capital

Aggressive approach to asset financing

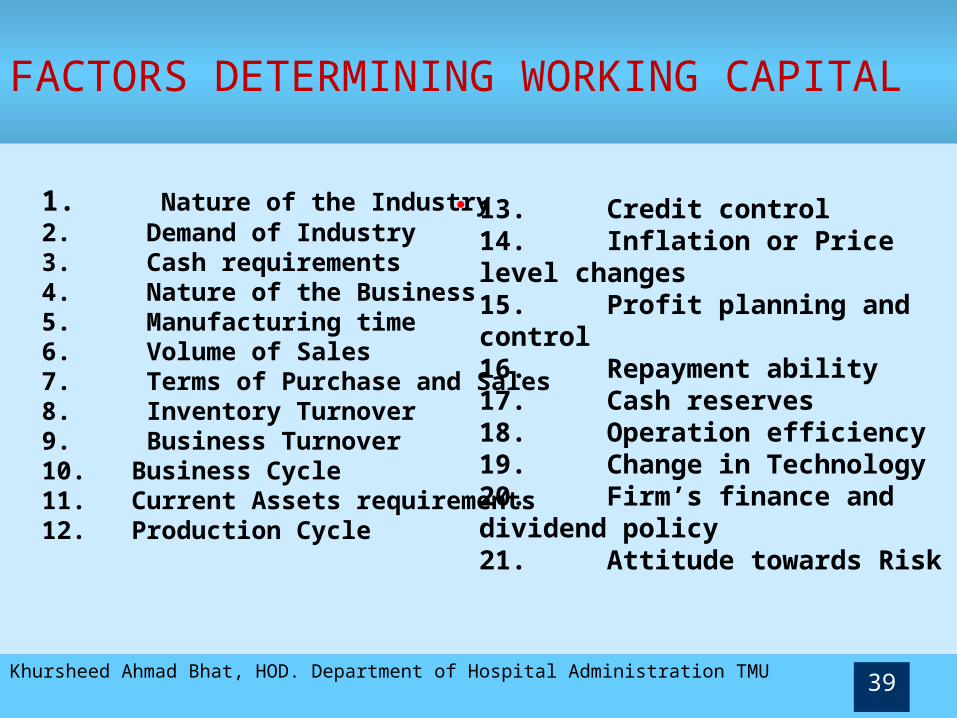

FACTORS DETERMINING WORKING CAPITAL

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU39

1. Nature of the Industry2. Demand of Industry3. Cash requirements4. Nature of the Business5. Manufacturing time6. Volume of Sales7. Terms of Purchase and Sales8. Inventory Turnover9. Business Turnover10. Business Cycle11. Current Assets requirements12. Production Cycle

• 13. Credit control14. Inflation or Price level changes15. Profit planning and control16. Repayment ability17. Cash reserves18. Operation efficiency19. Change in Technology20. Firm’s finance and dividend policy

21. Attitude towards Risk

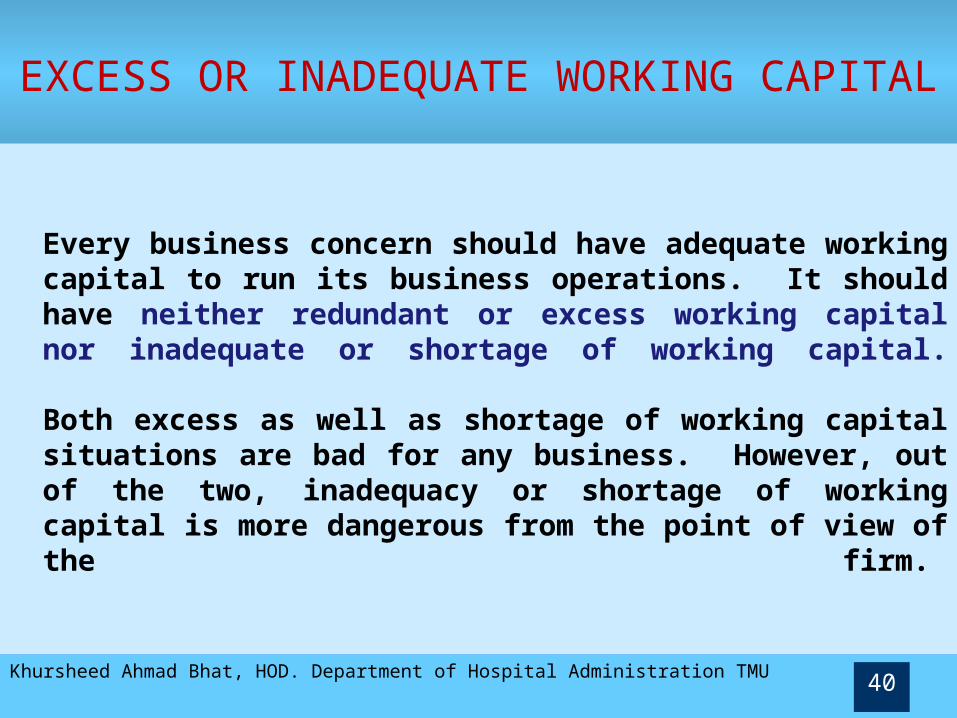

EXCESS OR INADEQUATE WORKING CAPITAL

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU40

Every business concern should have adequate working capital to run its business operations. It should have neither redundant or excess working capital nor inadequate or shortage of working capital.

Both excess as well as shortage of working capital situations are bad for any business. However, out of the two, inadequacy or shortage of working capital is more dangerous from the point of view of the firm.

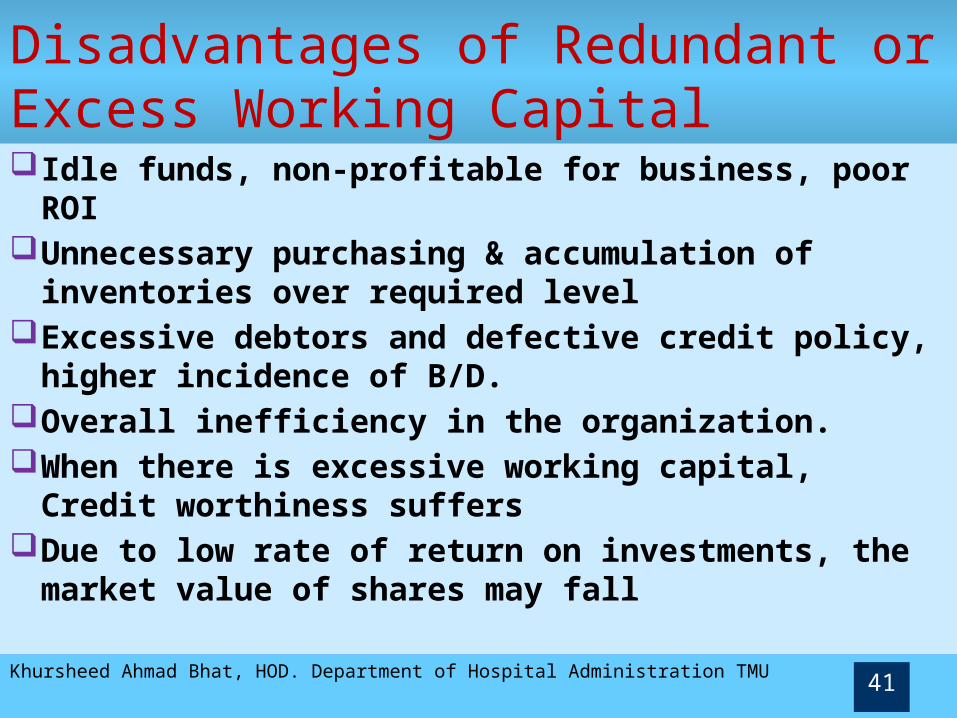

Disadvantages of Redundant or Excess Working Capital

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU41

Idle funds, non-profitable for business, poor ROIUnnecessary purchasing & accumulation of inventories

over required level Excessive debtors and defective credit policy, higher

incidence of B/D.Overall inefficiency in the organization.When there is excessive working capital, Credit

worthiness suffersDue to low rate of return on investments, the market

value of shares may fall

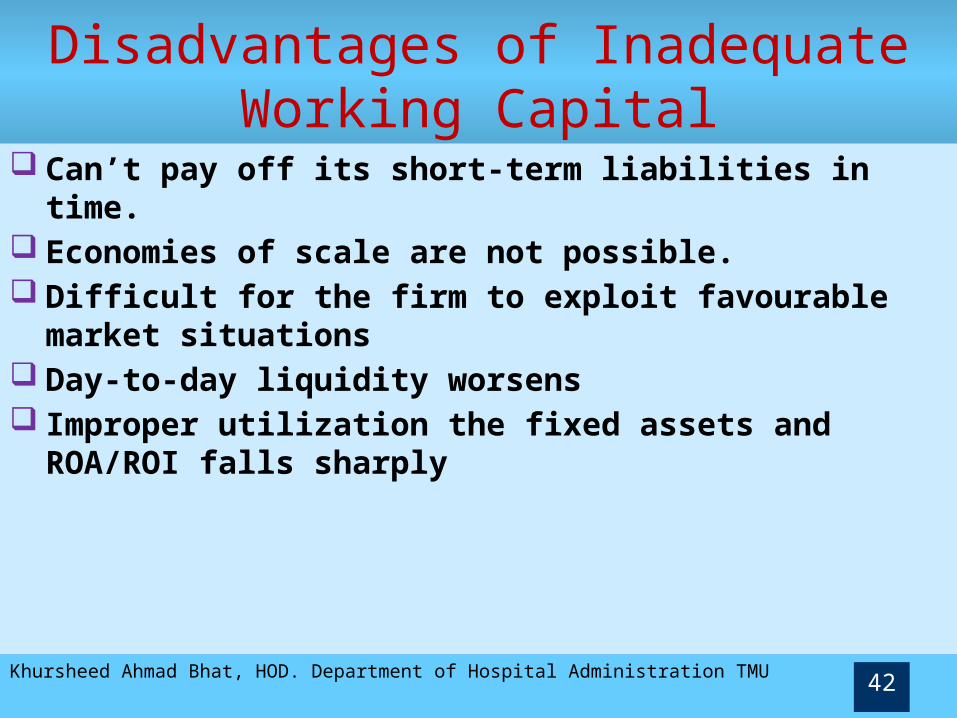

Disadvantages of Inadequate Working Capital

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU42

Can’t pay off its short-term liabilities in time. Economies of scale are not possible. Difficult for the firm to exploit favourable market situations Day-to-day liquidity worsens Improper utilization the fixed assets and ROA/ROI falls sharply

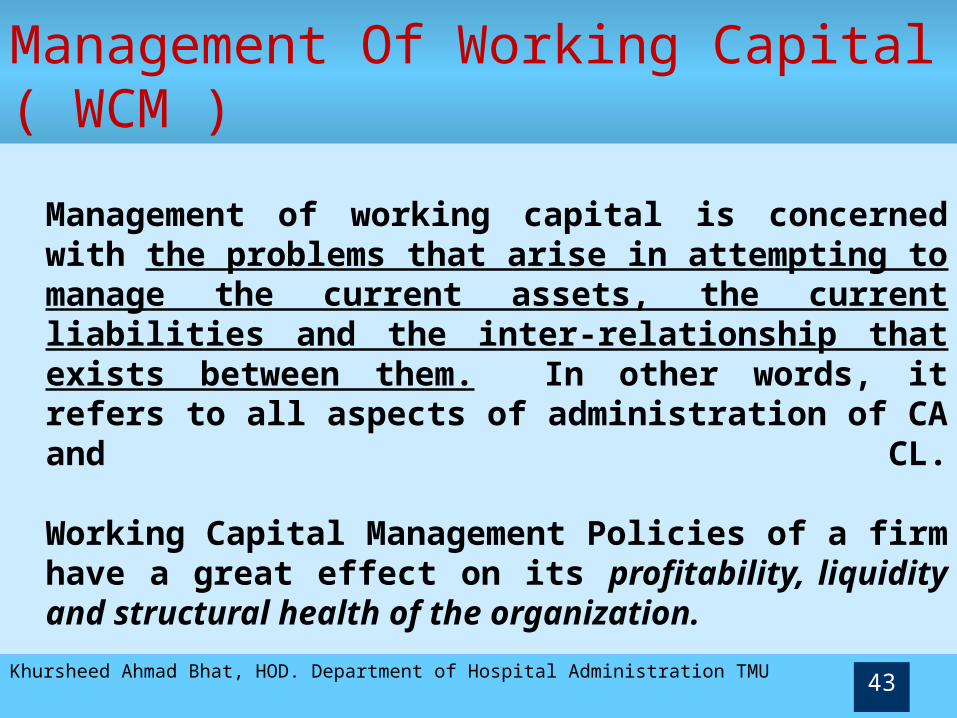

Management Of Working Capital ( WCM )

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU43

Management of working capital is concerned with the problems that arise in attempting to manage the current assets, the current liabilities and the inter-relationship that exists between them. In other words, it refers to all aspects of administration of CA and CL.

Working Capital Management Policies of a firm have a great effect on its profitability, liquidity and structural health of the organization.

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU44

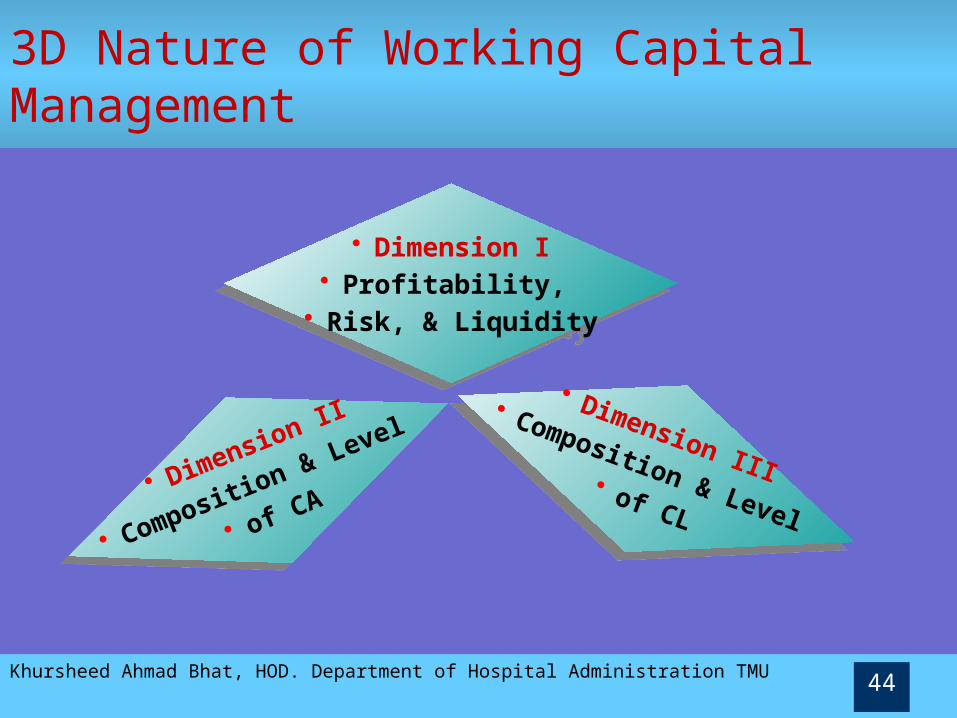

3D Nature of Working Capital Management

• Dimension I• Profitability,

• Risk, & Liquidity

• Dimension I• Profitability,

• Risk, & Liquidity

• Dimension II

• Composition & Level

• of CA

• Dimension II

• Composition & Level

• of CA

• Dimension III

• Composition & Level • of CL

• Dimension III

• Composition & Level • of CL

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU45

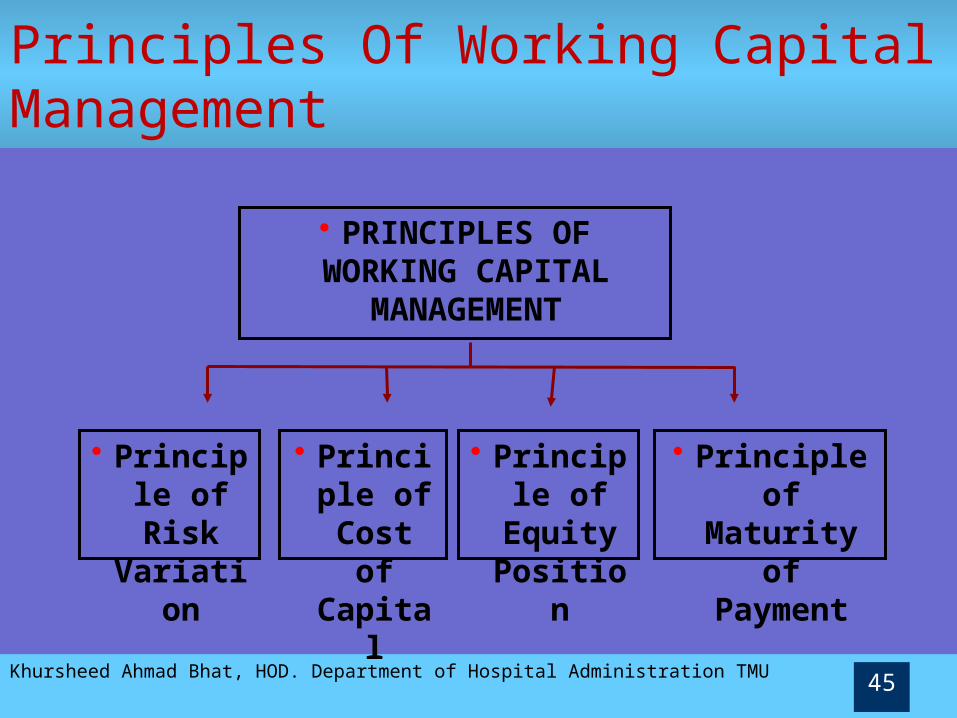

Principles Of Working Capital Management

• PRINCIPLES OF WORKING CAPITAL

MANAGEMENT

• Principle of Risk

Variation

• Principle of Cost

of Capital

• Principle of Equity Position

• Principle of Maturity of

Payment

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU46

Maturity Matching Principle

• Maturity (due date) of financing should roughly match duration (life) of asset being financed Then financing /asset combination becomes self-

liquidating• Cash inflows from asset can be used to pay off loan

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU47

Financing Net Working Capital

• According to maturity matching principle Temporary (seasonal) should be financed with short-

term borrowing Permanent working capital should be financed with

long-term sources, such as long-term debt and/or equity

• In practice, firms may use more or less short-term funds to finance working capital

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU48

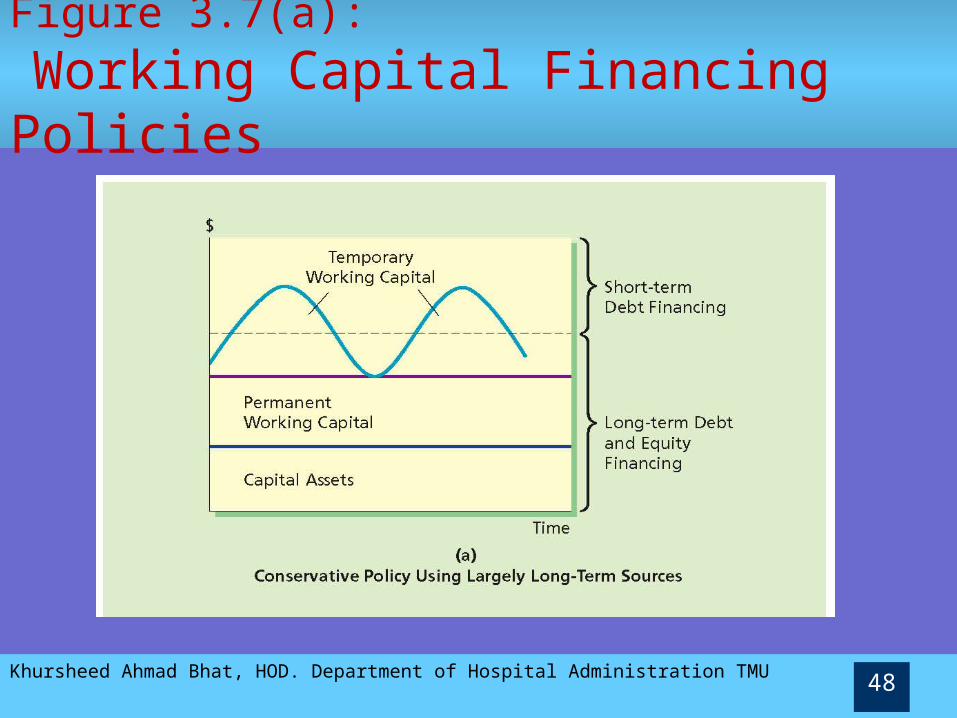

Figure 3.7(a):

Working Capital Financing Policies

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU49

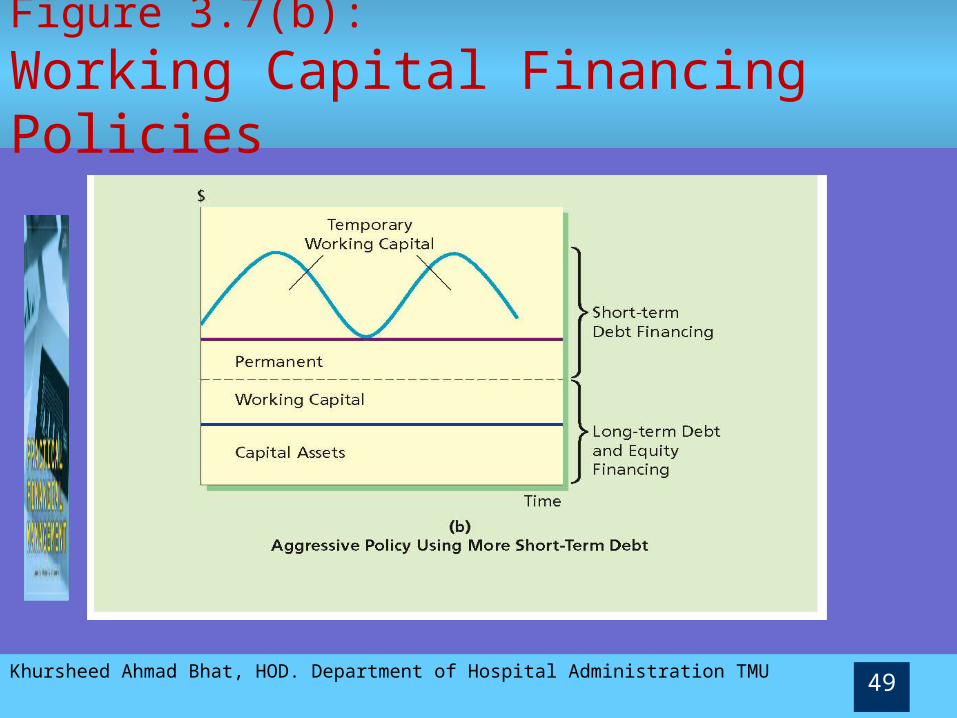

Figure 3.7(b):

Working Capital Financing Policies

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU50

Short-Term vs. Long-Term Financing

• The mix of short- or long-term working capital financing is a matter of policy

Use of long-term funds is a conservative policy Use of short-term funds is an aggressive policy

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU51

Short-Term vs. Long-Term Financing

• Short-term financing Cheap but risky

• Cheap—short-term rates generally lower than long-term rates

• Risky—because you are continually entering marketplace to borrow

• Borrower will face changing conditions (ex; higher interest rates and tight money)

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU52

Short-Term vs. Long-Term Financing

• Long-term financing Safe but expensive

• Safe—you can secure the required capital

• Expensive—long-term rates generally higher than short-term rates

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU53

Working Capital Policy

• Firm must set policy on following issues: How much working capital is used Extent to which working capital is supported by short-

vs. long-term financing How each component of working capital is managed The nature/source of any short-term financing used

Thank You

Khursheed Ahmad Bhat, HOD. Department of Hospital Administration TMU54