Changing industry dynamics - Philips · Changing industry dynamics ... Pioneer, Toshiba,...

25

Changing industry dynamics Rudy Provoost Senior Vice President Royal Philips Electronics CEO Global Sales and Services Philips Consumer Electronics

Transcript of Changing industry dynamics - Philips · Changing industry dynamics ... Pioneer, Toshiba,...

Changing industry dynamics

Rudy ProvoostSenior Vice President Royal Philips Electronics CEO Global Sales and Services Philips Consumer Electronics

2

Changing industry dynamics

• Trends• Threats• Opportunities

3

Changing industry dynamics

• Trends– Convergence – Content revolution– Globalisation

• Threats• Opportunities

4

Digital versus analogue segments* (in billion €), world excl. Japan

As CE markets become digital…

0

50

100

2000 2003 2006

Source: Philips CE World Market Forecast 2003* Philips served segments. Excluding: camcorder, still picture camera, game console, PDA, home PC, PC peripherals

Digital Analogue

in b

illion

€

5

Telecom PC/IT

Gaming CE

…multiple industries are converging

Telecom PC/IT

Gaming CE

6

Convergence drives new consumer solutions

+

+

+

Convergence in the home Portable convergence

7

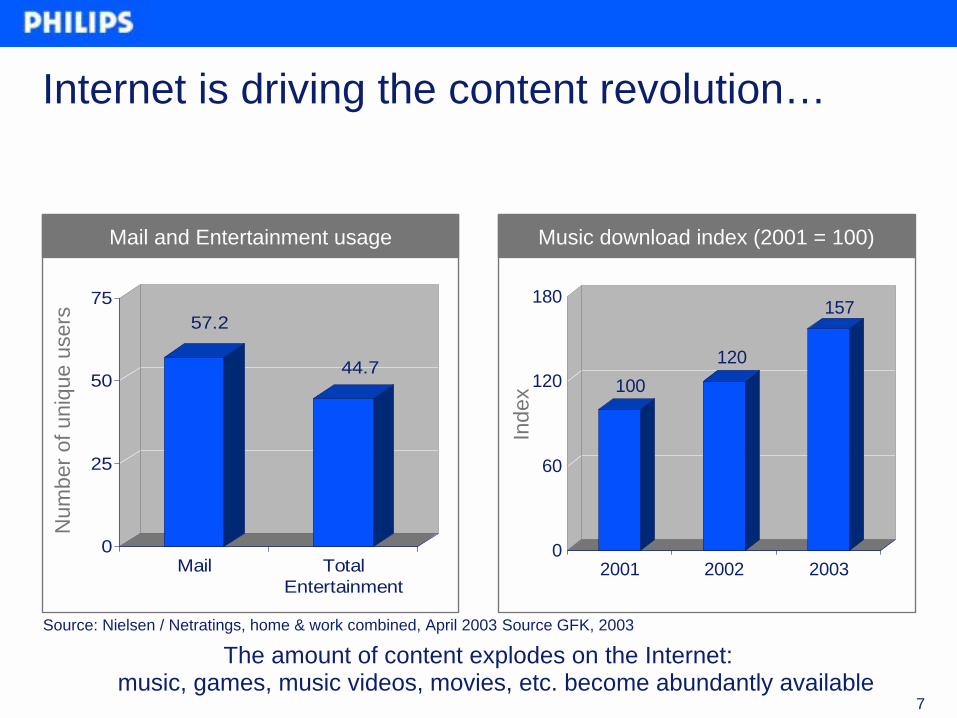

Internet is driving the content revolution…

The amount of content explodes on the Internet: music, games, music videos, movies, etc. become abundantly available

100120

157

0

60

120

180

2001 2002 2003

57.2

44.7

0

25

50

75

Mail TotalEntertainment

Num

ber o

f uni

que

user

s

Inde

x

Source: Nielsen / Netratings, home & work combined, April 2003 Source GFK, 2003

Mail and Entertainment usage Music download index (2001 = 100)

8

CAGR ‘03-’07: 246%

… supported by strong growth in broadband penetration and home networking

Source: Yankee Group, base: all Households, June 2003 Source: IDC, March 2003

0

10

20

30

40

50

2002 2003 2004 2005 2006 2007

Broa

dban

d pe

netra

tion

In m

illion

Hou

seho

lds

South KoreaJapanNetherlands

USAUnited KingdomItaly

China Entertainment networksMultimedia networksPC networks

Broadband penetration in selected countries 2002-2007 US Home networking (in million HH)

CAGR ‘03-’07: 77%CAGR ‘03-’07: 19%

0%

20%

40%

60%

80%

2002 2003 2004 2005 2006 2007

9

Hybrid product-service offerings are emerging

Home Entertainment(products and services)

e.g. • Enjoy music • Excited by playing games• Share a movie

All appliancese.g. Game, PC

and CE equipment

TV / AV* e.g. TV and Audio equipment

10

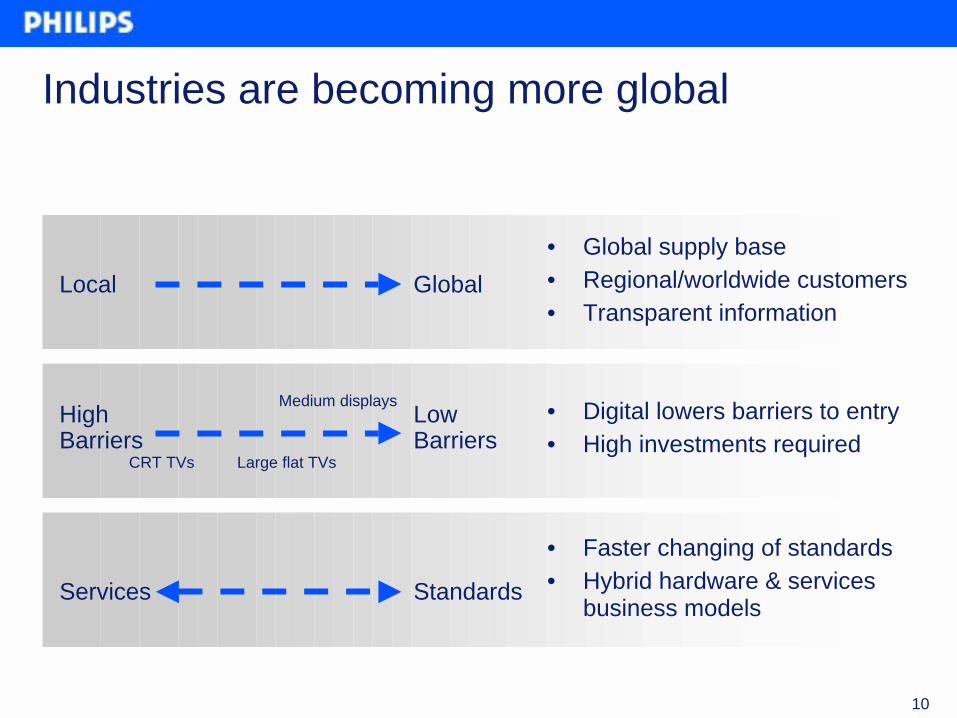

Industries are becoming more global

CRT TVs

Medium displays

Large flat TVs

HighBarriers

Low Barriers

• Digital lowers barriers to entry• High investments required

StandardsServices

• Faster changing of standards• Hybrid hardware & services

business models

Local Global• Global supply base• Regional/worldwide customers• Transparent information

11

International retailers leverage their global presence

0 1 2 3 4 5

Market Share LossesDecline Of National / Local Products

Need For New Layers / RolesFaster Private Label Development

Need For New SkillsNeed For Sophisticated Systems

Downwards Alignment Of Consumer PricesStrategic Vulnerability

Downwards Alignment Of Trade TermsIncreased Retailer 'Muscle'

Challenge Low Challenge High

Source: McKinsey survey of leading FMCG suppliers

Challenges for leading FMCG suppliers

12

Tariffs, duties and trade barriers are still significant

• WTO talks promised tariff cuts/better market access from 2004. Failure at Cancun means delay until ~2005/6

• Europe and USA still willing to lower import duties on CE in exchange for better market access elsewhere.

• Emphasis might shift to sectoral, bilateral or regional trade agreements.

• As tariff barriers fall, standards and non-tariff barriers increase in importance

• Technological convergence blurs distinction between CE (4-30% tariffs) and IT (0% tariffs) products. Planned new system for 2007 of classification

• Chinese competitors become global players

13

Changing industry dynamics

• Trends• Threats

– Increasing retail power– Changing competitive

landscape– Short product lifecycles

and commoditisation• Opportunities

14

29%35%

20%

30%

40%

Top retailers in Europe and the US strengthen their positions in the market

• In Europe Top 5 controls >35%• European retail top 3:

1. MediaMarkt/Saturn2. Dixons Group3. Euronics Buying Group

• In the US Top 5 controls ~45%• US Electrical retail top 3:

1. Best Buy2. Wal-Mart3. Circuit City

Turnover share of Top 5 CE retailers

Source: Mintel 2003

Best Buy CE revenue

Source: Best Buy quarterly report, June 03

Billio

n $

TO s

hare

top

5

1998 2002

2002 20032001

5.26

7.2

3

6

9

15

Retail power of mass merchants increases due to combination of growth and concentration

Both in Europe and the US, mass merchants realise the fastest growth

Source: GFK, July 2003 Source: NPD Intelect, July 2003, excluding Wal Mart

50

100

150

200

2000 2001 200250

100

150

200

2000 2001 2002

Independents Buying groupsMass MerchantChains

Inde

x

Electronic superstore A/V specialtyMass Merchant

Inde

x

CE growth per retail contact Europe 2000 = 100, cumulative

CE growth per retail contact USA 2000 = 100, cumulative

16

0%

20%

40%

60%

80%

100%

Jan'01

May Sep Jan'02

May Sep Jan'03

May

New entrants change the competitive landscape

Source: GFK, July 2003Established brands (global) are: Philips, Sony, Panasonic, Thomson, JVC, Samsung, Pioneer, Toshiba, Goldstar/LG, Grundig, Toshiba, Aiwa, Kenwood, HitachiC-Brands are: all other brands sold in CE retail

0

30

60

90

1999 2000 2001 2002 2003 2004E

EstablishedKorea

TaiwanesePC

Chinese“Established brands” “C-Brands”

Num

ber

Perc

enta

ge

Source: Philips amalgamation based on annual reports, industry studies and press releases 1998-2003

Number of competitors in CE worldwide ‘99-’04E* DVD player unit sales in Germany (units)

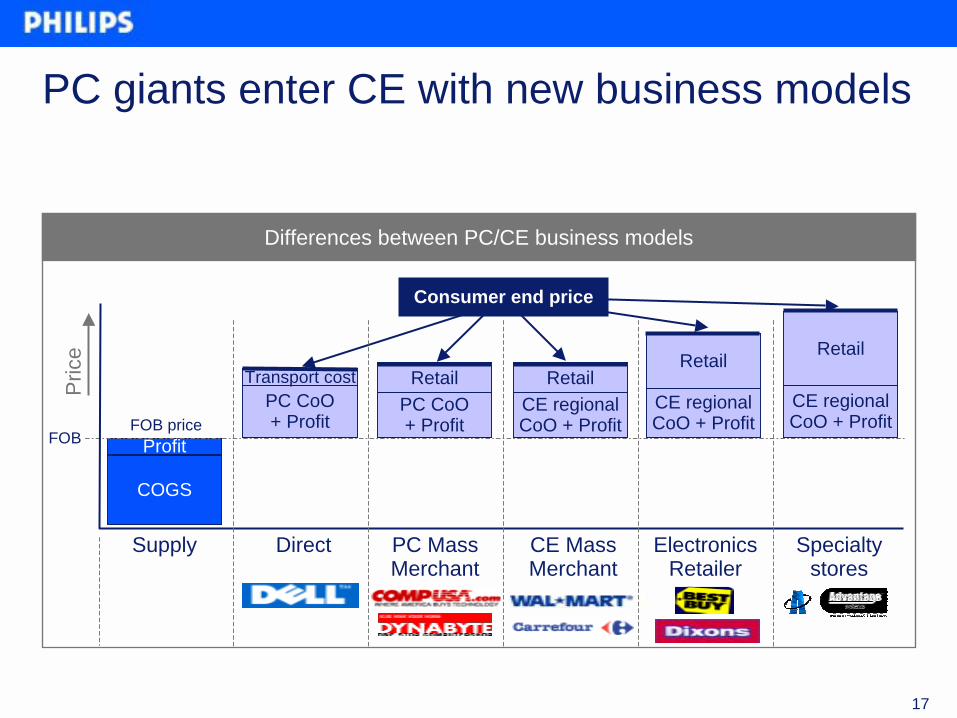

17

PC CoO+ Profit

Transport cost

Direct PC Mass Merchant

PC CoO+ Profit

RetailCE regionalCoO + Profit

Retail

CE Mass Merchant

CE regionalCoO + Profit

Specialtystores

Retail

PC giants enter CE with new business models

Differences between PC/CE business models

Pric

e

COGS

ProfitFOB price

Supply

CE regionalCoO + Profit

Retail

ElectronicsRetailer

Consumer end price

FOB

18

0

10

20

30

40

50

60

1 2 3 4 5 6 7 8 9 10Years after introduction

Mar

ket i

n m

illion

qua

ntiti

esThe pace of new product adoption is increasing…

Source: Philips CE World Market Forecast 2003 and Philips Semiconductor DVD Recorder Market Forecast

DVD Recorder (PH SC) DVD Player (1997) VCR (1971)

Faster adoption of new products

19

0

20

40

60

80

100

120

1975 1985 1995 2005

Mar

ket i

n m

illion

qua

ntiti

es… while lifecycles are shortening significantly

DVD PlayerVCR

Shorter life cycles – world quantities

Source: Philips CE World Market Forecast 2003

20

Changing industry dynamics

• Trends• Threats• Opportunities

– Growth markets– Value added

partnerships– lifecycle management

21

Focus on growth markets

34

1112

3132

4143

0 20 40

Source: Philips CE World Market Forecast 2003 * Broadband household penetration excluding Latin America and Africa

Net

val

ue

-9

-11

-26

-30 -20 -10 0

CRT monitorsAudio Systems & sep.CRT TV

FlatTVDVD-RecorderPersonal Infotainment

Set Top BoxesPDA / OrganiserDigital CamcorderDigital Still Camera

Broadband penetration*

Worldwide growth segments in net value(CAGR: 2003-2006)

Worldwide mature segments in net value (CAGR: 2003-2006)

Net

val

ue

22

Differentiate through value-added partnerships

0 1 2 3 4 5

Harmonised Consumer Pricing PoliciesTrade Terms Aligned Across Borders

Shares Systems With RetailersHarmonised Global Trade Terms SystemSignigificant Presence In All Key Markets

Tailored Responses For Selected PartnersHighly Qualified Multinational Managers

Full Internal Transparency Of Cost To ServeCategory Management Skills

Strong KAM SkillsStrong European / Global Brands

Retailer’s view ofoverall importance

Retailer’s perception of manufacturer’s performance

Retailer’s view of importance and perception of manufacturer’s performance

Source: McKinsey survey of leading FMCG suppliers

23

Create value through IP and market positions

Value shift in analogue and digital era

High value

Low valueBrandDistributionServices

Set makersAssembly

Analogue

Digital

Create valuetechnologyleadership /

licenses

Create valueeffective

go-to market

Intellectual PropertyChips and softwareProcess technology

24

Conclusions

• The CE environment is very dynamic:– converging industries, a content revolution and globalisation

• Threats:– Increasing retail power, a changing competitive landscape,

shortening product lifecycles and commoditisation

• Opportunities– Focus on growth markets, differentiation through value-

added partnerships and appropriately phased lifecycle management