Changing from Accrual to Cash Accounting - LexisNexis · Changing from Accrual to Cash Accounting...

17

Changing from Accrual to Cash Accounting Contents About Changing from Accrual to Cash Accounting Description of Accounting Methods Creating a Client Disb Expense (5010) Account Adjusting GST/Vat and Sales Tax Adjusting Accounts Receivables Adjusting Receive Payments Adjusting Outstanding Accounts Payable Adjusting Payments to Accounts Payable Adjusting Unbilled Disbursements Contacting LexisNexis PCLaw Technical Support About Changing from Accrual to Cash Accounting Changing the accounting method at the start of the fiscal year involves the fewest procedures. Additional procedures are required if there are closed months in the current fiscal year, if the firm implements taxes, uses the Accounts Payable module, or has payment activity in open months of the current fiscal year. This document lists all procedures necessary for changing the accounting method. Each procedure is listed below with a check box so you can mark only the procedures you need to do. The procedures are then described in detail under their own topic heading in the order that they are to be performed. Re-opening closed months in the current fiscal year reduces the number of adjusting entries needed. To do Done Procedure Creating a Client Disb Expense (5010) Account Adjusting GST/VAT and Sales Tax (if applicable) Are there closed months in the current fiscal year? Adjusting Accounts Receivable Is there an A/R balance at the end of the previous fiscal year? Is there billing activity in closed months of the current fiscal year? Adjusting Receive Payments Are there payments in closed months in the current fiscal year? Are there payments in open months of the current fiscal year? Adjusting Accounts Payable Is there an A/P balance at the end of the previous fiscal year? Is there A/P activity in closed months in the current fiscal year? Adjusting Payments to Accounts Payable Are there payments to payables in closed months of the current fiscal year? Are there payments to payables in open months of the current fiscal year? Adjusting Unbilled Disbursements Are there unbilled disbursement at the end of the previous fiscal year? Are there unbilled disbursements in closed months of the current year? Contacting LexisNexis PCLaw Technical Support

Transcript of Changing from Accrual to Cash Accounting - LexisNexis · Changing from Accrual to Cash Accounting...

Changing from Accrual to Cash Accounting

ContentsAbout Changing from Accrual to Cash AccountingDescription of Accounting MethodsCreating a Client Disb Expense (5010) AccountAdjusting GST/Vat and Sales TaxAdjusting Accounts ReceivablesAdjusting Receive PaymentsAdjusting Outstanding Accounts PayableAdjusting Payments to Accounts PayableAdjusting Unbilled DisbursementsContacting LexisNexis PCLaw Technical Support

About Changing from Accrual to Cash AccountingChanging the accounting method at the start of the fiscal year involves the fewest procedures. Additional procedures are required if there are closed months in the current fiscal year, if the firm implements taxes, uses the Accounts Payable module, or has payment activity in open months of the current fiscal year.

This document lists all procedures necessary for changing the accounting method. Each procedure is listed below with a check box so you can mark only the procedures you need to do. The procedures are then described in detail under their own topic heading in the order that they are to be performed.

Re-opening closed months in the current fiscal year reduces the number of adjusting entries needed.

To do Done Procedure

Creating a Client Disb Expense (5010) Account

Adjusting GST/VAT and Sales Tax (if applicable)Are there closed months in the current fiscal year?

Adjusting Accounts ReceivableIs there an A/R balance at the end of the previous fiscal year?Is there billing activity in closed months of the current fiscal year?

Adjusting Receive PaymentsAre there payments in closed months in the current fiscal year?Are there payments in open months of the current fiscal year?

Adjusting Accounts PayableIs there an A/P balance at the end of the previous fiscal year?Is there A/P activity in closed months in the current fiscal year?

Adjusting Payments to Accounts PayableAre there payments to payables in closed months of the current fiscal year?Are there payments to payables in open months of the current fiscal year?

Adjusting Unbilled DisbursementsAre there unbilled disbursement at the end of the previous fiscal year?Are there unbilled disbursements in closed months of the current year?

Contacting LexisNexis PCLaw Technical Support

Changing from Accrual to Cash Accounting Page 2

Description of Accounting MethodsAccrual and Cash systems differ in the way taxes, accounts receivables, receive payments, accounts payable and unbilled disbursements are handled.

Accrual systems post billed fees to Accounts Receivable (1200), taxes to their respective payable accounts, and uses General Liabilities (2000) for the accounts payable.

Cash systems do not track accounts receivables, therefore fees do not affect the G/L, disbursements remain in Client Disb Expense (5010), and taxes are not allocated to their respective payable accounts until payment is received. Client disbursements are an expense, not an asset. Accounts payable is allocated directly to an expense account but not until the payable is processed.

An equity account, (3500), is used in many of the following procedures. In a partnership, this account is called Income for Alloc. For a corporation, it is Retained Earnings. For simplicity, this document refers to the account as Income for Alloc (3500).

Creating a Client Disb Expense (5010) Account

Although changing from Accrual to Cash automatically switches Client Disb Recov (1210) to an expense account, it is recommended that a new account, Client Disb Expense (5010), be created for use in the Cash method:

Exhibit 1. The New G/L Account window as it appears when creating a Client Disb Expense (5010) account

1. Type in the Nickname box, 5010

2. Type in the Account box, Client Disb Expense.

3. Select from the Type drop down list, Expense.

4. Click OK to return to the Pop Up Help - G/L Accounts window (or the G/L Accounts window for versions 9.00 to 9.10).

5. For 9.20 and higher: Click Save and Close.

For 9.00 to 9.10: Click OK.

Adjusting GST/VAT and Sales TaxThis section is only applicable for firms collecting GST, VAT and/or sales tax.

Is there GST/VAT/sales tax activity in the previous fiscal year?Tax from the previous fiscal year is included in “Adjusting Accounts Receivable” on page 4. A separate adjusting entry is not required.

Account Nickname Account Type Accrual Cash

1200 Asset Accounts Receivable Does not exist

1210 Asset Client Disb Recov Does not exist

5010 Expense Does not exist Client Disb Exp

2000 Liability General Liabilities Does not exist

Pull-down Menu: Options > Lists > G/L Accounts > Add Item Icon/Add Button

Changing from Accrual to Cash Accounting Page 3

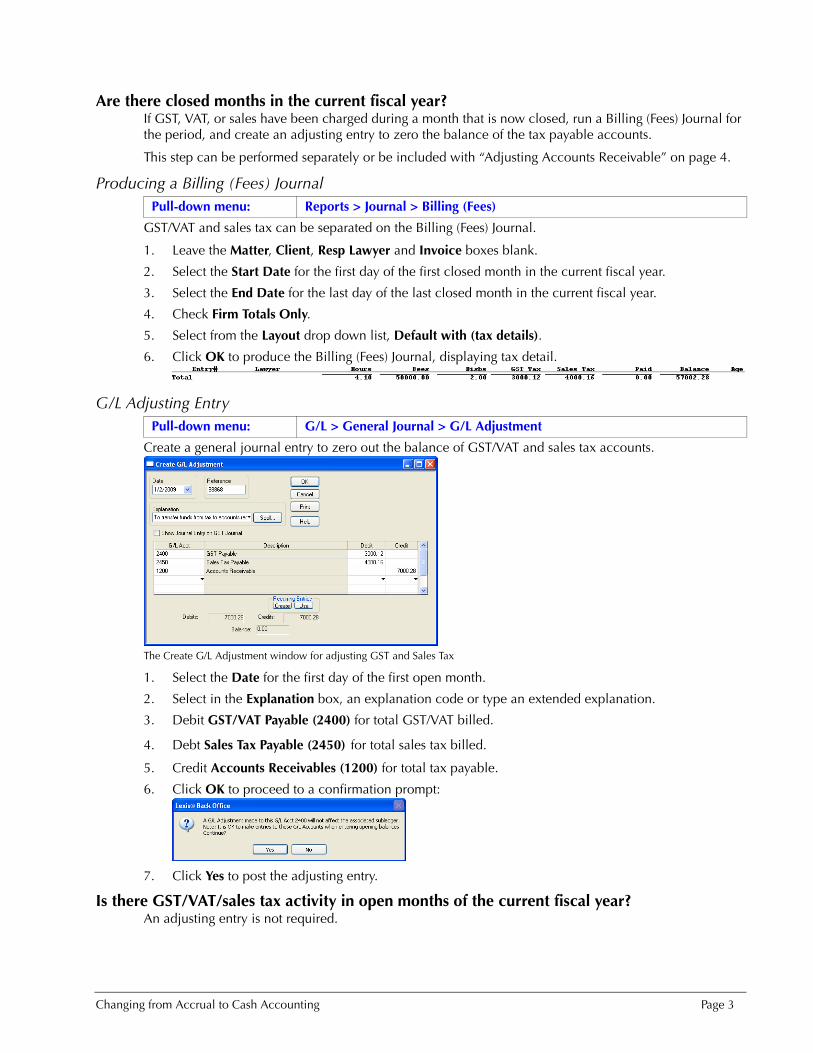

Are there closed months in the current fiscal year?If GST, VAT, or sales have been charged during a month that is now closed, run a Billing (Fees) Journal for the period, and create an adjusting entry to zero the balance of the tax payable accounts.

This step can be performed separately or be included with “Adjusting Accounts Receivable” on page 4.

Producing a Billing (Fees) Journal

GST/VAT and sales tax can be separated on the Billing (Fees) Journal.

1. Leave the Matter, Client, Resp Lawyer and Invoice boxes blank.

2. Select the Start Date for the first day of the first closed month in the current fiscal year.

3. Select the End Date for the last day of the last closed month in the current fiscal year.

4. Check Firm Totals Only.

5. Select from the Layout drop down list, Default with (tax details).

6. Click OK to produce the Billing (Fees) Journal, displaying tax detail.

G/L Adjusting Entry

Create a general journal entry to zero out the balance of GST/VAT and sales tax accounts.

The Create G/L Adjustment window for adjusting GST and Sales Tax

1. Select the Date for the first day of the first open month.

2. Select in the Explanation box, an explanation code or type an extended explanation.

3. Debit GST/VAT Payable (2400) for total GST/VAT billed.

4. Debt Sales Tax Payable (2450) for total sales tax billed.

5. Credit Accounts Receivables (1200) for total tax payable.

6. Click OK to proceed to a confirmation prompt:

7. Click Yes to post the adjusting entry.

Is there GST/VAT/sales tax activity in open months of the current fiscal year?An adjusting entry is not required.

Pull-down menu: Reports > Journal > Billing (Fees)

Pull-down menu: G/L > General Journal > G/L Adjustment

Changing from Accrual to Cash Accounting Page 4

Adjusting Accounts ReceivableThis set of procedures is required if an accounts receivable balance exists at the end of the previous fiscal year, or if there was billing activity within months that are now closed in the current fiscal year. Run a Billing (Fees) Journal to attain the A/R balance, and create adjusting entries to transfer that balance.

Is there an A/R balance at the end of the previous fiscal year? An adjusting entry is required for billed fees, disbursements, and taxes (if applicable) that were unpaid at the end of the previous fiscal year.

Producing a Billing (Fees) Journal

The Billing (Fees) Journal provides the value of outstanding fees, disbursements, and taxes for a specified period.

Exhibit 2. The Billing Fees Journal for adjusting accounts receivables

1. Leave the Matter, Client, Resp Lawyer and Invoice boxes blank.

2. Accept the Start Date of 1/1/82.

3. Select the End Date for the last day of the previous fiscal year.

4. Check Firm Totals Only.

5. Check Include Paid Invoices.

6. Uncheck Show Balances as of End Date.

7. Click OK to produce the Billing (Fees) Journal.

8. Refer to the Total column for the balance of outstanding fees, disbursements and taxes.

G/L Adjusting Entry

Adjust billed fees billed that are outstanding at the end of the previous fiscal year to Income for Alloc (3500). A partnership can also have fees allocated to individual lawyers’ Retained Earnings (3500.xxx) accounts.

Disbursements are adjusted to Income for Alloc (3500), not Client Disb Recov (1210). In the Cash method, Client Disb Expense (5010) zeroes out as part of the End of Year Adjusting Entries. Since Client

Pull-down menu: Reports > Journal > Billing (Fees)

Pull-down menu: G/L > General Journal > G/L Adjustment

Changing from Accrual to Cash Accounting Page 5

Disb Expense (5010) only ever reflects the current year’s balance, disbursements are not carried over as an expense from the previous year.

Taxes, if applicable, are adjusted to Income for Alloc (3500). Outstanding taxes are remitted at the end of the prior fiscal year, and so no further adjustments are required.

Create a general journal entry to transfer the balance from Accounts Receivable (1200) to Income for Alloc (3500).

Exhibit 3. The Create G/L Adjustment window for adjusting accounts receivable

1. Select the Date for the first day of the first open month.

2. Select in the Explanation box, an explanation code or type an extended explanation.

3. Debit Income for Alloc (3500) for the value of outstanding billed fees, disbursements and taxes.

4. Credit Accounts Receivable (1200) for the value of outstanding billed fees, disbursements, and taxes.

5. Click OK to proceed to a confirmation prompt:

6. Click Yes to post the adjusting entry.

Is there billing activity in closed months of the current fiscal year?If there is billing within a closed month of the current fiscal year, transfer the value of billed fees and disbursements to Accounts Receivable (1200)If taxes were adjusted in “Adjusting GST/VAT and Sales Tax” on page 2, they do not need to be adjusted in these procedures.

Producing a Billing (Fees) Journal

The Billing (Fees) Journal provides the value of billed fees, disbursements and taxes.

1. Leave the Matter, Client, Resp Lawyer and Invoice boxes blank.

2. Select the Start Date for the first day of the current fiscal year.

3. Select the End Date for the last day of the last closed month in the current fiscal year.

4. Check Firm Totals Only.

5. Check Include Paid Invoices.

6. Uncheck Show Balances as of End Date.

7. Click OK to produce the Billing (Fees) Journal.

8. Refer to the Billed column for the value of billed fees, disbursements and taxes.

Pull-down menu: Reports > Journal > Billing (Fees)

Changing from Accrual to Cash Accounting Page 6

G/L Adjusting Entry

Create a general journal entry to debit fees, disbursements, and taxes and credit A/R.

Exhibit 4. The Create G/L Adjustment window for adjusting Accounts Receivable in the current fiscal year

1. Select the Date for the first day of the first open month.

2. Select in the Explanation box, an explanation code or type an extended explanation.

3. Debit Fees Earned (4000) for total fees billed in all closed months of the current fiscal year.

Note: A partnership may also have individual fee accounts. These accounts can be substituted for (4000), or the balance of (4000) can be reallocated at a later date.

4. Debit Client Disb Recov (1210) for the value of disbursements billed in all closed months of the current fiscal year.

5. If applicable: Debit Sales Tax Payable (2450) and/or GST/VAT Payable (2400) for taxes billed in all closed months of the current fiscal year.

6. Credit Accounts Receivable (1200) for the total of fees, disbursements, and taxes billed in the closed months of the current fiscal year.

7. Click OK to proceed to a confirmation prompt:

8. Click Yes to post the adjusting entry.

Is there billing activity in open months of the current fiscal year?An adjusting entry is not required.

Adjusting Receive PaymentsIf there are payments in the current fiscal year, run a Payment Allocation Listing to show how the payments were applied. Payments may be applied to invoices created in the current or prior fiscal year. Payments made in both closed and open months of the current fiscal year need to be adjusted.

Are there payments in the previous fiscal year?An adjusting entry is not required.

Pull-down menu: G/L > General Journal > G/L Adjustment

Warning: Do not refer to the Paid column of the Billing (Fees) Journal for the value of payments made by clients. The Billing (Fees) Journal value includes only payments made to invoices created with the date range of the produced report.

Changing from Accrual to Cash Accounting Page 7

Are there payments in closed months of the current fiscal year?Payments occurring in any closed month of the current fiscal need to be adjusted. The payments may apply to invoices created in the current or prior fiscal year.

Producing a Payment Allocation Listing

The Payment Allocation Listing presents a record of payments within a specified period.

Exhibit 5. The Payment Allocation Listing for adjusting receive payments

1. Leave the Matter, Client, and Resp Lawyer boxes blank.

2. Select the Start Date for the first day of the current fiscal year.

3. Select the End Date for the last day of the last closed month for the current fiscal year.

4. Check Totals Only.

5. Click OK to produce the Payment Allocation Listing.

6. Refer to the Total Payments and Adjustments line for Fee Tot, Disb, and Tax.

G/L Adjusting Entry

Create a general journal entry to debit Accounts Receivable (1200) and credit fees, disbursements, and taxes.

Exhibit 6. The Create G/L Adjustment window for adjusting receive payments

Pull-down menu: Reports > Accounts Receivables > Payment Allocation Listing

Pull-down menu: G/L > General Journal > G/L Adjustment

Changing from Accrual to Cash Accounting Page 8

1. Select the Date for the first day of the first open month.

2. Select in the Explanation box, an explanation code or type an extended explanation.

3. Debit Accounts Receivable (1200) for the total value of payments in all closed months of the current fiscal year.

4. Credit Fees Earned (4000) for the total of payments applied to fees in all closed months of the current fiscal year.Tip: A partnership may also have individual fee accounts. These accounts can be substituted for (4000) or the balance of (4000) can be reallocated at a later date.

5. Credit Client Disb Recov (1210) for the total of payments applied to disbursements in all closed months of the current fiscal year.

6. If applicable: Credit Sales Tax Payable (2450) and/or GST/Vat Payable (2400) for payments applied to taxes in all closed months of the current fiscal year.

7. Click OK to proceed to a confirmation prompt:

8. Click Yes to post the adjusting entry.

Are there payments in open months of the current fiscal year?Payments received in an open month need to be adjusted on the last day of that month. A separate adjusting entry should be made for each open month for which there are payments.

Producing a Payment Allocation Listing

The Payment Allocation Listing provides a record of payments for a specific period.

1. Leave the Matter, Client, and Resp Lawyer boxes blank.

2. Select the Start Date for the first day of the first open month.

3. Select the End Date for the last day of the first open month.

4. Check Totals Only.

5. Click OK to produce the Payment Allocation Listing.

6. Repeat this procedure for each open month where payments were received.

7. Refer to the Total Payments and Adjustments line for Fee Tot, Disb, and Tax.

G/L Adjusting Entries

Create a general journal entry to reallocate payments. Make a separate entry for each open month, dated on the last day of the particular month.

1. Select the Date for the last day of the first open month.

2. Select in the Explanation box, an explanation code or type an extended explanation.

3. Debit Accounts Receivable (1200) for the value of payments in the month.

4. Credit Client Disb Recov (1210) for the value of payments applied to disbursements in the month.

5. Credit Fees Earned (4000) for the value of payments applied to fees in the month.

Tip: A partnership may also have individual fee accounts. These accounts can be substituted for (4000) or the balance of (4000) can be reallocated at a later date.

Pull-down menu: Reports > Accounts Receivables > Payment Allocation Listing

Pull-down menu: G/L > General Journal > G/L Adjustment

Changing from Accrual to Cash Accounting Page 9

6. If applicable: Credit Sales Tax Payable (2450) and/or GST/Vat Payable (2400) for the value of payments applied to taxes in the month.

7. Click OK to proceed to a confirmation prompt.

8. Click Yes to post the adjusting entry.

9. Repeat this procedure for each subsequent open month where there are payments. Substitute the date of the last day of the particular month.

Adjusting Outstanding Accounts PayableThis step is for firms using the Accounts Payable module.

Accrual system, incur liabilities through accounts payable as soon as the payable is created. The liability is continued until the payable is processed.

Cash systems allocates a payable directly to an expense account but not until the payable is processed. The balance of an expensed payable is not carried over to the next year.

Is there an A/P balance at the end of the previous fiscal year?Payables outstanding at the end of the previous fiscal year need to be adjusted to equity so the expense is not carried over to the current year.

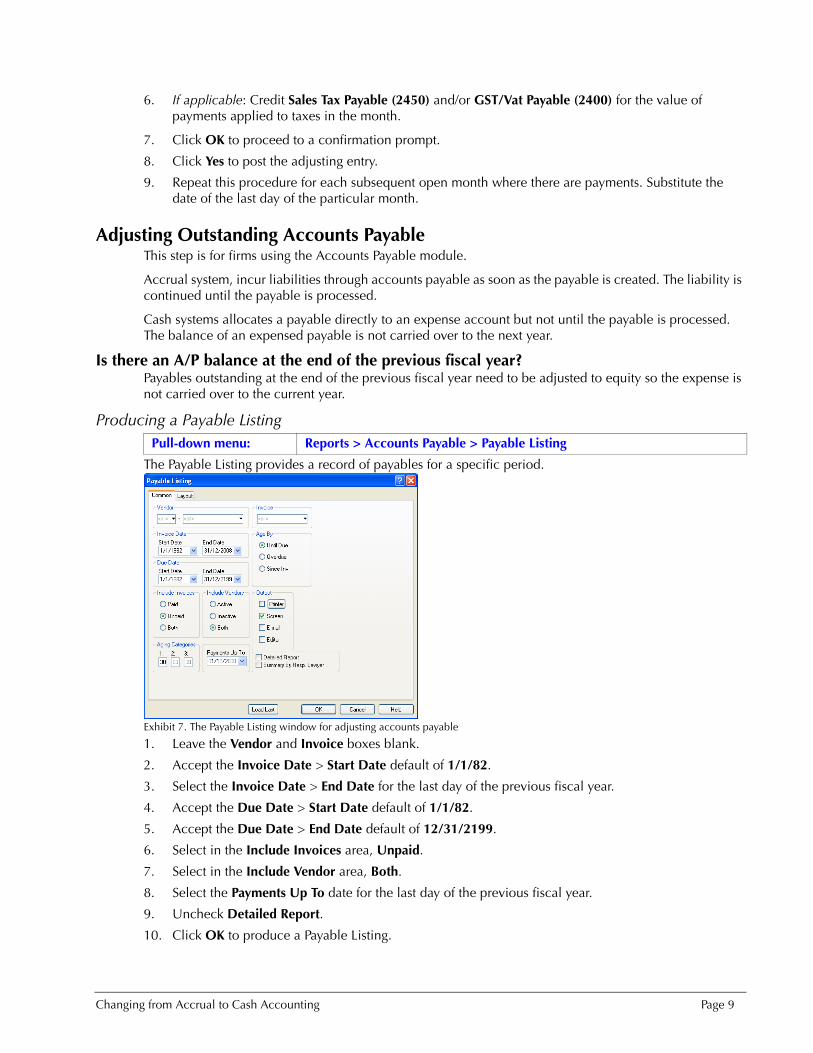

Producing a Payable Listing

The Payable Listing provides a record of payables for a specific period.

Exhibit 7. The Payable Listing window for adjusting accounts payable

1. Leave the Vendor and Invoice boxes blank.

2. Accept the Invoice Date > Start Date default of 1/1/82.

3. Select the Invoice Date > End Date for the last day of the previous fiscal year.

4. Accept the Due Date > Start Date default of 1/1/82.

5. Accept the Due Date > End Date default of 12/31/2199.

6. Select in the Include Invoices area, Unpaid.

7. Select in the Include Vendor area, Both.

8. Select the Payments Up To date for the last day of the previous fiscal year.

9. Uncheck Detailed Report.

10. Click OK to produce a Payable Listing.

Pull-down menu: Reports > Accounts Payable > Payable Listing

Changing from Accrual to Cash Accounting Page 10

11. Refer to the breakdown of expenses in the AP Allocations Summary section of the report.

G/L Adjusting Entry

Create a general journal entry to debit General Liabilities (2000) and credit the individual expense accounts.

Exhibit 8. The Create G/L Adjustment window for adjusting Accounts Payable

1. Select the Date for the first day of the first open month.

2. Select in the Explanation box, an explanation code or type an extended explanation.

3. Debit General Liabilities (2000) for the Allocation Totals value displayed on the Payable Listing - AP Allocation Summary.

4. Credit the individual expense accounts as shown for the Allocation Totals on the Payable Listing - AP Allocations Summary.

5. Click OK to proceed to a confirmation prompt:

6. Click Yes to post the adjusting entry.

Is there A/P activity in closed months of the current fiscal year?Payables created in closed months of the current fiscal year need to be adjusted to their respective expense accounts.

Producing a Payable Listing

The Payable Listing provides a record of payables for a specified period.

1. Leave the Vendor and Invoice boxes blank.

2. Select the Invoice Date > Start Date for the first day of the first closed month.

3. Select the Invoice Date > End Date for the last day of the last closed month.

4. Accept the Due Date > Start Date default of 1/1/82.

5. Accept the Due Date > End Date default of 12/31/2199.

Pull-down menu: G/L > General Journal > G/L Adjustment

Pull-down menu: Reports > Accounts Payable > Payable Listing

Changing from Accrual to Cash Accounting Page 11

6. Select in the Include Invoices area, Both.

7. Select the Include Vendors area, Both.

8. Uncheck Detailed Report.

9. Click OK to produce the Payable Listing.

10. Refer to the breakdown of expenses in the AP Allocations Summary section of the report.

G/L Adjusting Entry

Create a general journal entry to debit General Liabilities (2000) and credit the individual expense accounts.

1. Select the Date for the first day of the first open month.

2. Select in the Explanation box, an explanation code or type an expanded explanation

3. Debit General Liabilities (2000) for the Allocation Totals value displayed in the AP Allocation Summary.

4. Credit the individual expense accounts as shown in the AP Allocations Summary.

5. Click OK to proceed to a confirmation prompt.

6. Click Yes to post the adjusting entry.

Is there A/P activity in open months of the current fiscal year?An adjusting entry is not required.

Adjusting Payments to Accounts PayableThese procedures are for firms using the Accounts Payable module.

Cash systems allocate payables to specific expense accounts when the payable is processed.

Accrual systems credits General Liabilities (2000) when payment is received. Since payments are posted to General Liabilities (2000), it is not possible to determine the specific expense account the payment is applied to unless payables are referenced in the Purchases Journal.

Are there payments to payables in the previous fiscal year?An adjusting entry is not required.

Are there payments to payables in closed months in the current fiscal year?Payments occurring in any closed month of the current fiscal need to be adjusted. The payments may apply to payables created in the current or prior fiscal year.

Pull-down menu: G/L > General Journal > G/L Adjustment

Warning: Do not refer to the Paid column of the Payable Listing created in “Adjusting Outstanding Accounts Payable” on page 9. These values include only payments made to payables that match the date range of the report.

Changing from Accrual to Cash Accounting Page 12

Producing a Payment Listing

The Payment Listing provides a record of payments within a specified period.

Exhibit 9. The Payment Listing for adjusting payments to accounts payable

1. Leave the Vendor and G/L Account boxes blank.

2. Select in the Include Vendors area, Both.

3. Accept the Invoice Date > Start Date default of 1/1/82.

4. Select the End Date for the last day of the last closed month.

5. Select the Payment Date > Start Date for the first day of the current fiscal year.

6. Select the Payment Date > End Date for the last day of the last closed month.

7. Check Include Unpaid Invoices.

8. Click OK to produce the Payment Listing.

9. Refer to the G/L Account Summary for the value of payments made in all closed months of the current fiscal year.

Pull-down menu: Reports > Accounts Payable > Payment Listing

Changing from Accrual to Cash Accounting Page 13

G/L Adjusting Entry

Create a general journal entry to debit a generic or individual expense account and credit General Liabilities (2000) for the value of the payments.

Exhibit 10. The Create G/L Adjustment window for adjusting payments to accounts payable

1. Select the Date for the first day of the first open month.

2. Select in the Explanation box, an explanation code or type an extended explanation code.

3. Debit an expense account(s) for the payment value as displayed on the Payment Listing.

4. Credit General Liabilities (2000) for the payment value as displayed on the Payment Listing.

5. Click OK to proceed to a confirmation prompt:

6. Click Yes to post the adjusting entry.

Are there payments to payables in open months of the current fiscal year?Payments applied to payables in an open month need to be adjusted on the last day of that month. Make a separate adjusting entry for each open month where payables were processed.

Producing a Payment Listing

Run a Payment Listing for each open month where payables were processed.

1. Leave the Vendor and G/L Account boxes blank.

2. Accept the Invoice Date > Start Date default of 1/1/82.

3. Select the Invoice Date > End Date for the last day of the first open month.

4. Select the Payment Date > Start Date for the first day of the first open month.

5. Select the Payment Date > End Date for the last day of the first open month.

6. Check Include Unpaid Invoices.

7. Click OK to produce the Payment Listing.

8. Repeat this procedure for all open months where payables were processed.

9. Refer to the G/L Account Summary for the value of payments made in each open month of the current fiscal year.

Pull-down menu: G/L > General Journal > G/L Adjustment

Pull-down menu: Reports > Accounts Payable > Payment Listing

Changing from Accrual to Cash Accounting Page 14

G/L Adjusting Entries

Create general journal entries to debit a generic or individual expense account and credit General Liabilities (2000) for the value of the payments. Make a separate entry for each month, on the last day of that particular month.

1. Select the Date for the last day of the first open month.

2. Select in the Explanation box, an explanation code or type an extended explanation.

3. Debit a generic expense account(s) for the value of payable payments made in the month.

4. Credit General Liabilities (2000) for the value of payable payments made in the month.

5. Click OK to proceed to a confirmation prompt.

6. Click Yes to post the adjusting entry.

7. Repeat this procedure for each subsequent open month where payments were processed. Substitute the date of the last day of the particular month.

Adjusting Unbilled DisbursementsClient Disb Recov (1210) does not exist as an asset account in a Cash system. Client Disb Expense (5010) closes out as part of the End of Year Adjusting Entries. Therefore, for the previous fiscal year, the balance of Client Disb Recov (1210) is transferred to Income for Alloc (3500). For closed months of the current fiscal year, the balance of Client Disb Recov (1210) is transferred to Client Disb Expense (5010).

Are there unbilled disbursements at the end of the previous fiscal year?The balance of Client Disb Recov (1210) at the end of the previous fiscal year is transferred to Income for Alloc (3500).

Producing a General Ledger

To find the value of unbilled disbursements, run a general ledger for Client Disb Recov (1210).

Exhibit 11. The G/L Statements window for accustomed unbilled disbursements

1. Check General Ledger.

2. Select from the G/L Account Selection > Start drop down list, 1210 - Client Disb Recov.

3. Select from the G/L Account Selection > End drop down list, 1210 - Client Disb Recov.

4. Select in the Current Report Period section, the beginning and ending date of the last closed month of the previous fiscal year.

Pull-down menu: G/L > General Journal > G/L Adjustment

Pull-down menu: G/L > G/L Statements

Changing from Accrual to Cash Accounting Page 15

5. Click OK to produce a general ledger for Client Disb Recov (1210).

6. Refer to the Closing balance - Client Disb Recov value.

G/L Adjusting Entry

Create a general journal entry to move billed disbursements at the end of the prior fiscal year.

Exhibit 12. The Create G/L Adjustment window for adjusting unbilled disbursements

1. Select the Date for the first day of the first open month.

2. Select in the Explanation box, an explanation code or type an extended explanation.

3. Debit Income for Alloc (3500) for the balance of unbilled disbursements.

4. Credit Client Disb Recov (1210) for the balance of unbilled disbursements.

5. Click OK to proceed to a confirmation prompt:

6. Click Yes to post the adjusting entry.

Are there unbilled disbursements in closed months of the current fiscal year?The value of unbilled disbursements from closed months in the current fiscal year are moved to Client Disb Expense (5010).

Producing a General Ledger

To find the balance of unbilled disbursements at the end of the last closed month, run a general ledger statement for Client Disb Recov (1210).

1. Check General Ledger.

2. Select from the G/L Account Selection > Start drop down list, 1210 - Client Disb Recov.

3. Select from the G/L Account Selection > End drop down list, 1210 - Client Disb Recov.

4. Select in the Current Report Period area, in the first date box, the date of the first day of the current fiscal year.

Pull-down menu: G/L > General Journal > G/L Adjustment

Pull-down menu: G/L > G/L Statements

Changing from Accrual to Cash Accounting Page 16

5. Select in the Current Report Period area, in the second date box, the date of the last day of the last closed month for the current fiscal year.

6. Click OK to produce a general ledger for Client Disb Recov (1210).

7. Subtract the Closing Balance - Client Disb Recov value from the opening balance value. Using the example below: 2234.58 - 617.29 = 1617.29 .

G/L Adjusting Entry

Create a general journal entry to move the balance from Client Disb Recov (1210) to Client Disb Expense (5010).

Exhibit 13. The Create G/L Adjustment window for unbilled disbursements in closed months of the current fiscal year

1. Select the Date for the first day of the first open month.

2. Select in the Explanation box, an explanation code or type an extended explanation.

3. Debit Client Disb Expense (5010) for the net balance (closing balance minus opening balance) of unbilled disbursements incurred during all closed months of the current fiscal year.

4. Credit Client Disb Recov (1210) for the net balance (closing balance minus opening balance) of unbilled disbursements incurred during all closed months of the current fiscal year.

5. Click OK to proceed to a confirmation prompt:

6. Click Yes to post the adjusting entry.

Are there unbilled disbursements for any open month of the current fiscal yearSince transactions are not formally posted to the general ledger until months are closed, an adjusting entry is not required.

Warning: Although an adjusting entry was made to transfer the unbilled disbursement value for the previous fiscal year from Client Disb Recov (1210), that entry is not reflected on this statement since the entry was dated for the first day of the first open month.

Pull-down menu: G/L > General Journal > G/L Adjustment

Changing from Accrual to Cash Accounting Page 17

Contacting LexisNexis PCLaw Technical Support

Contact LexisNexis PCLaw Technical Support to change the accounting method within PCLaw. A Technical Support Representative is required to perform this change.

1. Click the Tech Support button to display the Technical Support window.

2. Call the technical support number for your location.

Note to support personnel: Refer to Technical Support Appendix Accrual to Modified to Cash.

Pull-down menu Help > About LexisNexis Back Office Powered by PCLaw