Annual Financial Report June 30, 2020 and 2019 Sponsored ...

Changes in Financial Management of Sponsored Projects:

- Subrecipient Monitoring

- Institutional Base Salary

Impact of Uniform Guidance

Presentation 212/16 &12/17/2014

Presentation Topics

• New regulations and requirements

• Subawards and Contracts

• Review of subawards vs. contracts

• Components of a subaward agreement

• Subrecipient monitoring

• Calculating Effort

• Institutional Base Salary

• Other things to consider

• Questions?

Uniform Guidance

http://www.gpo.gov/fdsys/pkg/FR-2013-12-26/pdf/2013-30465.pdf

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (“Uniform Guidance”) 2 CFR 200 [may

also be referred to as A-81 or the Omni-Circular]

• Any federal award (new and non-competing segments) after December 26, 2014

• Federal grants, contracts (cooperative agreements, fixed price, etc.), and some aspects of cost reimbursement contracts

• Some aspects of non-federal awards (for consistency)

Applies to

Subawards and Contracts

Definitions of Terms Used in Federal Awards• Subaward – An award provided by a pass-through entity.

[NOTE: This has historically been referred to as a “subcontract” at UAB.]

• Subrecipient – The entity receiving a subaward from a pass-through entity.

• Pass-Through Entity – A non-Federal entity that provides a subaward to a subrecipient.

• Contract – A legal instrument by which property or services. are purchased. [NOTE: This also may be referred to as a “procurement”,

“service”, or “fee-for-service” contract at UAB.]

• Contractor – The entity receiving a contract.

• Cost-reimbursement contract – A Federal award and its subcontracts made under the Federal Acquisition Regulations (FAR).

Recipients, Subrecipients, and Contractors – the flow of federal funds

Recipient

Subrecipient

Recipient

Contractor

and Subrecipient

Remember: A contract, but not a subaward, can be made from a subaward.

Subrecipients vs. Contractors (§200.330)

UAB, when passing Federal awards to a subrecipient “…must make case-by-case determinations whether each agreement it makes for disbursement of Federal program funds casts the party receiving the funds in the role of a subrecipient or a contractor.”

In determining whether funds should be passed as a subaward or contract, “…the substance of the relationship is more important than the form of the agreement.”

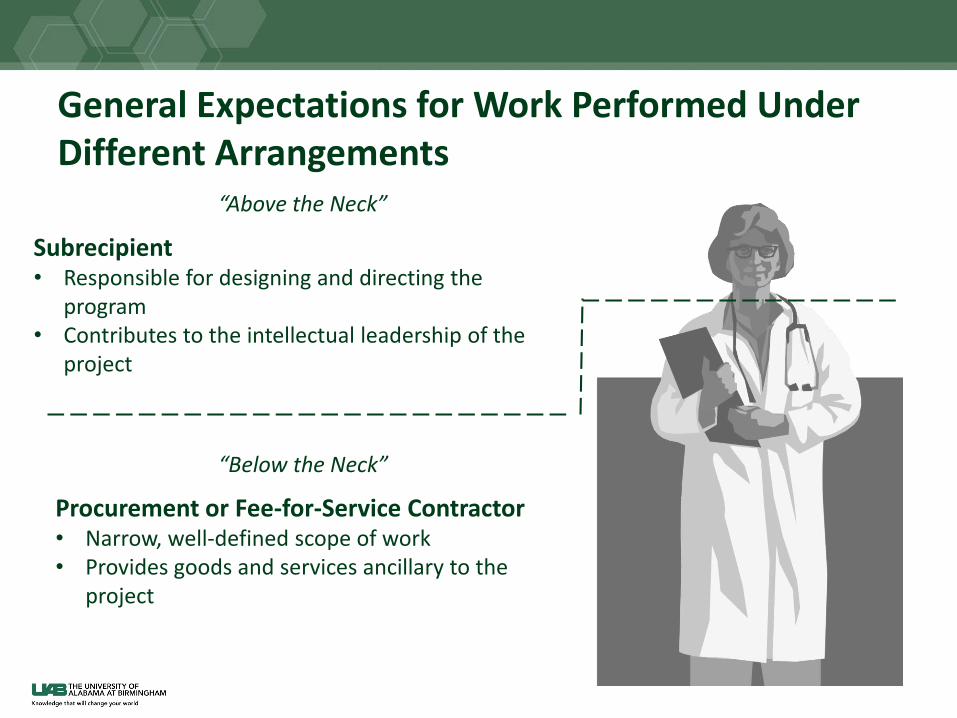

General Expectations for Work Performed Under Different Arrangements

Procurement or Fee-for-Service Contractor• Narrow, well-defined scope of work• Provides goods and services ancillary to the

project

Subrecipient• Responsible for designing and directing the

program• Contributes to the intellectual leadership of the

project

“Above the Neck”

“Below the Neck”

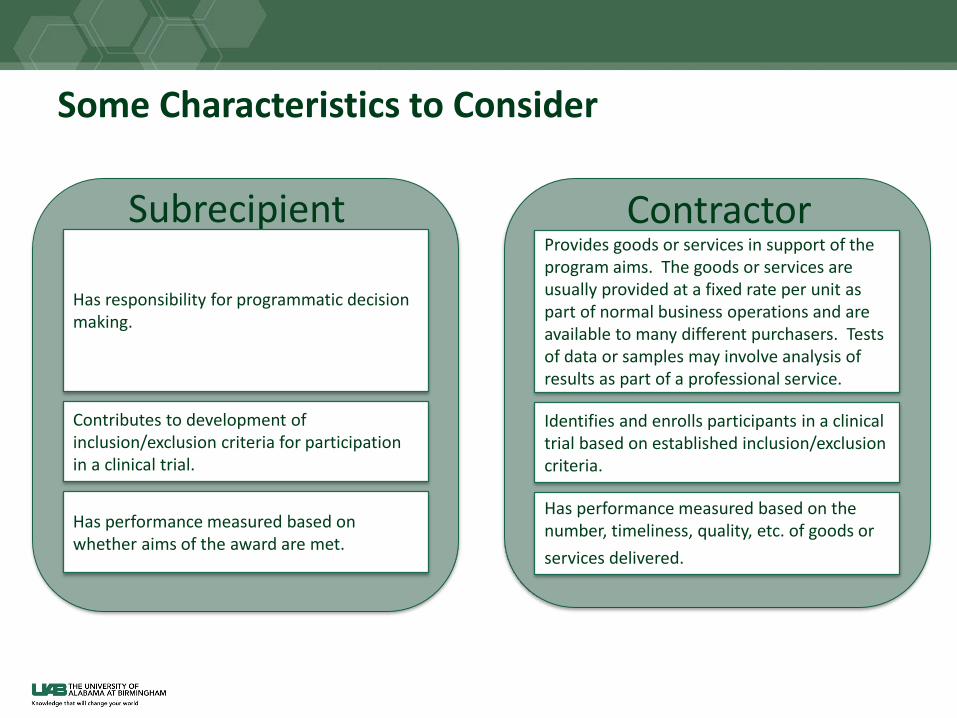

Some Characteristics to Consider

Subrecipient ContractorProvides goods or services in support of the program aims. The goods or services are usually provided at a fixed rate per unit as part of normal business operations and are available to many different purchasers. Tests of data or samples may involve analysis of results as part of a professional service.

Has performance measured based on the number, timeliness, quality, etc. of goods or

services delivered..

Identifies and enrolls participants in a clinical trial based on established inclusion/exclusion criteria.

Has responsibility for programmatic decision making.

Has performance measured based on whether aims of the award are met.

Contributes to development of inclusion/exclusion criteria for participation in a clinical trial.

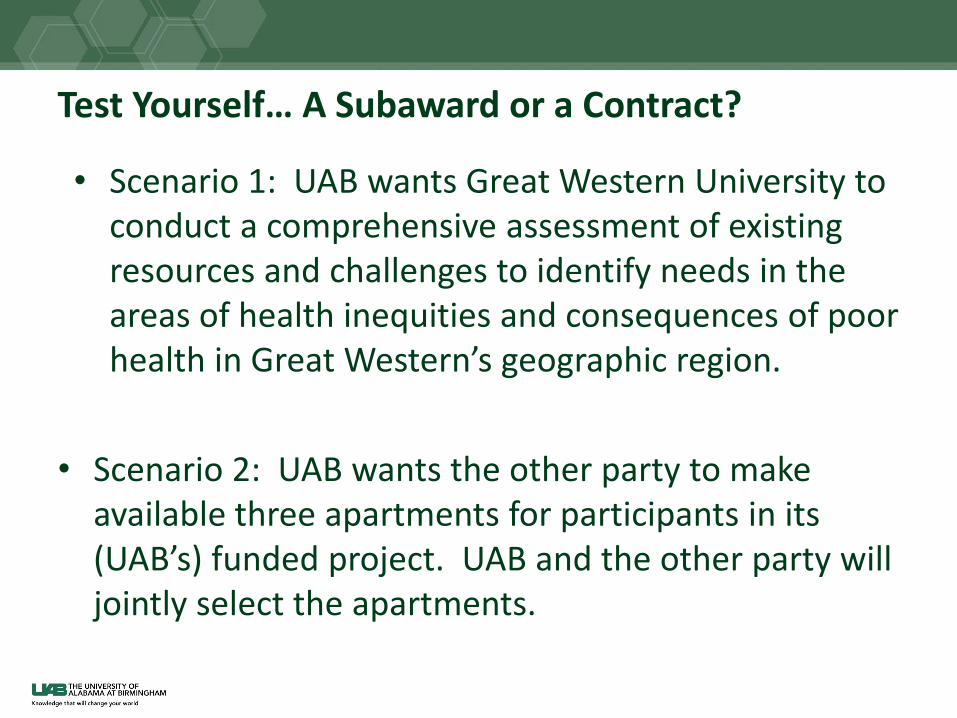

Test Yourself… A Subaward or a Contract?

• Scenario 2: UAB wants the other party to make available three apartments for participants in its (UAB’s) funded project. UAB and the other party will jointly select the apartments.

• Scenario 1: UAB wants Great Western University to conduct a comprehensive assessment of existing resources and challenges to identify needs in the areas of health inequities and consequences of poor health in Great Western’s geographic region.

The Subaward Agreement

Components of a Standard Agreement

• UAB uses (and encourages use of) the templates prepared by the Federal Demonstration Partnership (FDP) for most agreements

• Templates are available for Cost Reimbursement and Fixed Price agreements

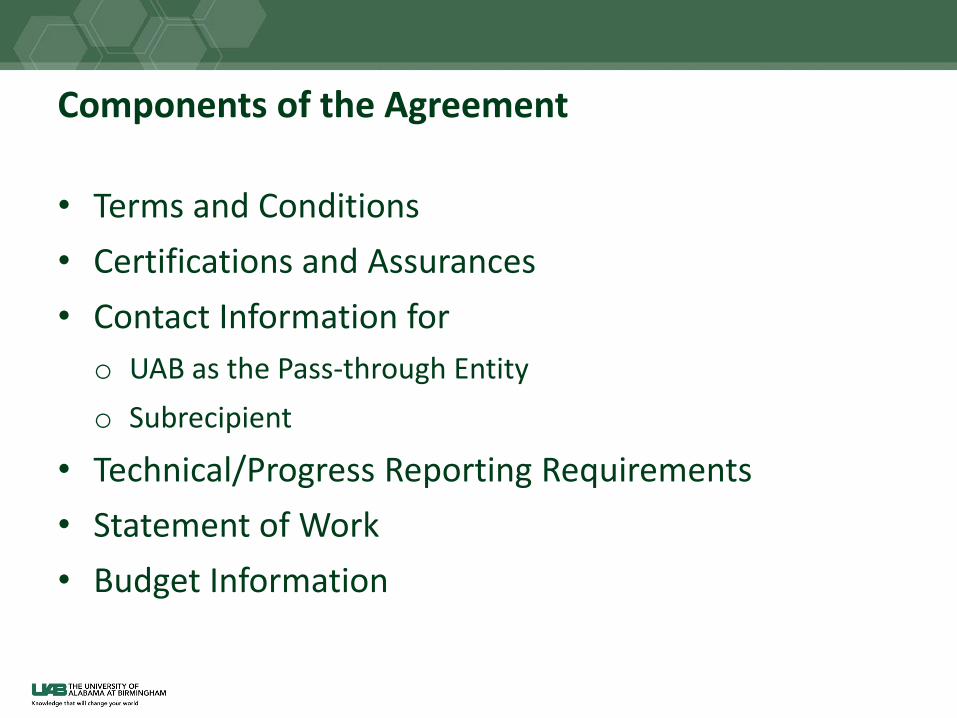

Components of the Agreement

• Terms and Conditions

• Certifications and Assurances

• Contact Information for

o UAB as the Pass-through Entity

o Subrecipient

• Technical/Progress Reporting Requirements

• Statement of Work

• Budget Information

Subrecipient Monitoring

Subrecipient Monitoring (§200.331)

• When UAB passes Federal award funds through to a subrecipient it (UAB) is responsible for ensuring that the subaward

o Is used for authorized purposes;

o Is in compliance with Federal statutes, regulations, and the terms and conditions of the subaward; and

o Achieves performance goals.

With Uniform Guidance, the Federal Government is passing greater responsibility to recipients to monitor performance and use of funds.

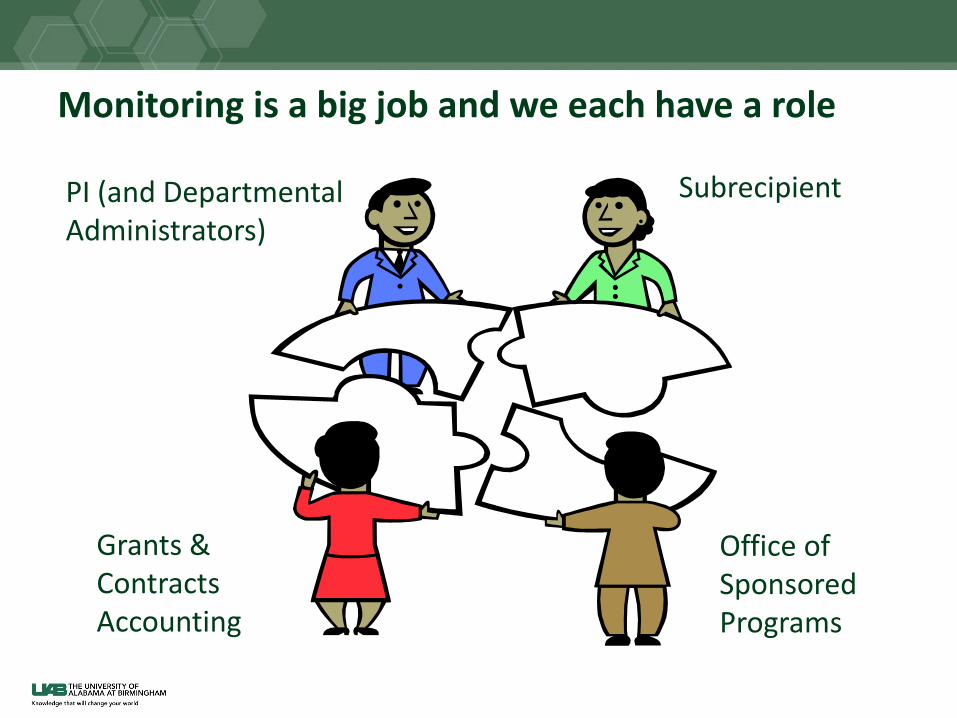

Monitoring is a big job and we each have a role

PI (and Departmental Administrators)

Subrecipient

Office of Sponsored Programs

Grants & Contracts Accounting

Proposal Development – The PI should:

• Complete Subrecipient Determination Form

• Collect subrecipient application information:

Subrecipient Assurance form (replaces and expands on the Letter of Intent currently requested)

Statement of Work (SOW)*

Budget and justification*

Subrecipient contact information*

*Although requested at time of proposal often are not received until

time for subaward issuance

A SOW Should Address -• Who – the subrecipient institution, PI, and personnel

• What – the subaward objectives in the context of those of the overall project, a description of the work to be performed

• When – the period of performance and the timing/frequency of reports (phone conferences, written reports, etc.)

• Where – where the work will be conducted

• How – how objectives will be achieved (the deliverables/milestones)

• Why – the reason this particular subrecipient should perform the work

Upon Receipt of the Subrecipient Application Information, the PI should:

• Assess subrecipient’s expertise and financial viability

• Determine that proposed costs are

• Reasonable,

• Necessary, and

• Allocable

• Integrate subrecipient’s SOW and budget information into the proposal per RFA/RFP format

Submit Funding Application to OSP

• Forward the draft proposal to OSP including the Subrecipient Application Information and Subrecipient Determination Form

Prior to Submission to Funding Agency

OSP notifies PI of any changes required

OSP reviews (in addition to usual review)• Subrecipient Determination Form and SOW for proper

classification as a subaward• Confirms that budget contains subrecipient’s federally negotiated

F&A rate (or 10% if there is no federally negotiated rate)

PI submits revised/final application

Application submitted to funding agency

At Notice of Award

PI sends to OSP• Request for New Subaward• Any revisions to

Subrecipient Application Information

OSP conducts subrecipient risk assessment based on• Request for New Subaward• Subrecipient Application Information (and

any revisions)• Audit findings

o Single audit (A-133) reporto Supplemental financial questionnaire

(if not subject to Single audit)

OSP drafts agreement and sends to PI for review

PI reviews and okays or works with OSP on revisions

Subrecipient receives agreement (may wish to negotiate) and work begins

Schedule Options for Subrecipient Technical/Progress Reports and Invoicing (Addressed on Request for New Subaward Form)• Ongoing

o Quarterly for technical/progress reports and invoices*

o Based on defined milestones/deliverables or other schedule (as needed to provide adequate oversight)

• Closeout

o Final invoice and technical/progress report within 60 days after project end date*

o Other – 15, 30, 45 – as requested by PI (as long as allows timely closeout) and consistent with funding agency requirements

* Recommended

During the Project

Subrecipient sends the PI• Technical/progress reports • Invoice(s) and Subrecipient’s

Request for Payment Certificate

If okay, PI • Enters payment request

into Oracle• Scans invoice(s),

Subrecipient’s Request for Payment Certificate, andPI’s Request for Payment Certificate into Optidoc

PI• Reviews reports and

invoices• Returns to Subrecipient

if problems

GCA • Conducts

secondary review• Makes payment if

no problems

Monitoring Subrecipient Performance – The PI’s role

• Communicates regularly with Sub PI

• Reviews progress/technical reports and invoices

• Determines if changes in SOW are needed

• Identifies and works to resolve any noncompliance

• Certifies work on each authorization to pay each subrecipient

Reviewing Invoices – Things to consider

• Are they arriving as scheduled?

• Are they detailed enough to allow adequate review?

• Are costs reasonable, necessary, allowable, and allocable?

• Are expenses aligned with program progress?

• Is cost sharing, if applicable, reflected?

Review should be conducted by someone familiar enough with the project to make a meaningful assessment!

Request for Payment of Subrecipient Invoice(s)

• Certification (by both PI and Subrecipient)

• Appropriateness of charges (as budgeted, during period of performance, reasonable, etc.)

• Subrecipient has submitted all technical/progress reports and other data as required and has performed all obligations covered by the invoice

• Not aware

• of anything that would prevent subrecipient from continuing work

• that subrecipient has been debarred

Forms available on Financial Affairs webpage under Forms

Prompt Payment Requirement (§200.305(b)(3))

• “…pass-through entity must make payment within 30 calendar days after receipt of the billing unless the Federal awarding agency or pass-through entity reasonably believes the request to be improper.”

If Subrecipient is not compliant with Terms and Conditions of Agreement or SOW – First steps

• PI

o Follows up with subrecipient

o Notifies OSP if issues are resolvable by

Amending SOW and budget

Revising agreement to provide better monitoring

If Subrecipient is not compliant with Terms and Conditions of Agreement or SOW

• If situation cannot be easily remedied, the PI should

o Promptly notify the CFO/Associate VP for Financial Affairs and the Senior Associate VP for Research Administration

o Be prepared to provide documentation of compliance issues and efforts to resolve

DO NOT simply ignore an invoice!

Examples of monitoring tools to ensure proper accountability and compliance with program and performance requirements

• Providing training and technical assistance on program-related matters

• Performing on-site reviews of program operations, policies, systems, record retention, procurement procedures, etc.

Possible Remedies for Noncompliance

• UAB can

• Withhold payment pending correction of deficiency

• Disallow part or all of the cost of the activity/action not in compliance with T&C and SOW

• Wholly or partly suspend or terminate agreement

Subaward CloseoutPI• Reviews reports and invoices• Returns to Subrecipient if

problems

GCA • Conducts secondary review• Sends Subrecipient

payment if no problems

Subrecipient sends PI• Final invoice Marked Final• Subrecipient’s Request for

Payment Certificate• Final technical/progress

report If okay, PI • Enters payment request

into Oracle• Scans invoice(s),

Subrecipient’s Request for Payment Certificate, andPI’s Request for Payment Certificate into Optidoc

Calculating Effort

Institutional Base Salary (§200.430 (h)(2))

• For salaries and wages earned beginning January 1, 2015, a UAB employee’s IBS will be the same as that utilized for the Teachers’ Retirement System of Alabama (TRS).

• The following pay elements that have been excluded for effort reporting but included for TRS purposes will change to be included for effort reporting:

o On Call Hours

o On Call Amount

o Extra Duty Hours (formerly called Moonlighting)

Activities Comprising UAB Effort

UAB Effort

Research

Clinical

(not HSF)

Public Service

Admin

Teaching

Compensation for activities considered UAB Effort are the basis for Alabama Teachers Retirement System (TRS) calculations and make up the Institutional Base Salary (IBS).

Time spent for activities considered UAB Effort does not require the employee to take vacation or leave without pay although the time away should be documented through eLAS or other acceptable system.

Questions?

What happens if I can’t/don’t provide all the requested information about the potential subrecipient to the OSP with my application?

• OSP will process the application; however, the information must be provided before the agreement can be issued.

may cause significant delays in processing while the required information is being obtained. Also, it may be determined that the agreement should be a fee-for-service rather than a subaward and therefore require funding agency approval and budget changes .

Waiting until the agreement is being drafted:

reduces stress during proposal development. Besides, we may not get the award so doing all that work would be a waste of time.

What if the Final Invoice isn’t submitted timely?

• If funding agency has closed award

• Subrecipient will not be paid

• UAB Department pays from voluntary cost share (VCS) account

How can I find out more about these changes?

• Links on Research or Accounting websites

• Notices distributed via listserves

• Town Halls and requested presentations

• Send questions to [email protected]