CHALLENGES TO HEALTH CARE REFORM Susan A. Channick, J.D., M.P.H. February 16, 2011.

33

CHALLENGES TO HEALTH CARE REFORM Susan A. Channick, J.D., M.P.H. February 16, 2011

-

Upload

cori-gallagher -

Category

Documents

-

view

217 -

download

3

Transcript of CHALLENGES TO HEALTH CARE REFORM Susan A. Channick, J.D., M.P.H. February 16, 2011.

CHALLENGES TO HEALTH CARE REFORMSusan A. Channick, J.D., M.P.H.February 16, 2011

Competing Goals of Health Insurance Schemes: Individualism vs. Solidarity Currently, access and affordability are sacrificed to ensure

excellent care but only for those who can afford Ration by denying access because of inability to pay or

inadequate portals to access (unemployed, health status) Hence, 50M people in the U.S. lack health insurance and more

lack adequate health insurance Under Patient Protection and Affordable Care Act (PPACA),

the primary goal is universal access to adequate, affordable HI ACA creates access for an addit’l 32M people with individual

mandate as linchpin Skewed health care costs (most expensive 5% population =

50% of costs; least expensive 50% = 3% of costs) mitigated by large numbers

ACA prohibits insurers’ behavior to avoid risk pool fragmentation

Exhibit 5. Source of Insurance Coverage Under Current Law and House and Senate Bills, 2019

*CBO estimates 20% of people enrolled in exchange will choose the public plan under the House bill. Employees whose employers provide coverage through the exchange are shown as covered by their employers (9 million in the House bill and 5 million in the Senate bill). Note: ESI is Employer-Sponsored Insurance.Source: Revised Estimate of the Affordable Health Care for America Act, Congressional Budget Office Letter to the Honorable John Dingell, November 20, 2009, http://www.cbo.gov/doc.cfm?index=10741. The Congressional Budget Office Analysis of the Patient Protection and Affordable Care Act, Incorporating the Manager’s Amendment, Dec. 19, 2009, http://cbo.gov/doc.cfm?index=10868.

Among 282 million people under age 65

Current Law

House

18 M (6%)Uninsured

17 M (6%) Exchange

(Private Plans)

4 M (1%) Exchange

(Public Plan)*

16 M (6%)Other

9 M (3%)Nongroup

162 M(57%)

ESI

35 M(12%)

Medicaid

54 M(19%)

Uninsured16 M (6%)

Other

15 M (5%)Nongroup

168 M(60%)

ESI50 M(18%)

Medicaid

158 M(56%)

ESI

50 M(18%)

Medicaid

24 M (9%)Uninsured

26 M (9%)Exchanges

(Private Plans)

16 M (6%)Other

10 M (4%)Nongroup

23 M (8%)Uninsured

Senate

Key Insurance Provisions included in PPACA

Individual mandate; penalty for noncompliance Employer mandate: Pay-or-play choice; Employers

>50 employees who do not play, i.e., offer HI pay a tax to subsidize insurance for employees who purchase from exchanges

Creation of state HI exchanges with federal default Federal subsidies available for individuals and small

businesses (premium tax credit) Income at 133-400% FLP (family of four: $29,327 -

$44,100) Expanded Medicaid to include all under-65

individuals eligible for Medicaid Income eligibility 133% FLP Children, pregnant women, elderly, disabled, adults

Individual Mandate or minimum coverage requirement

All citizens and legal residents must purchase HI Exemptions: Medicare, Medicaid, CHIP, employment,

religious objections, the incarcerated, American Indians, defined financial hardship

HI no longer voluntary Penalty=greater of $695 per year up to a maximum

of $2085 per family; or 2.5% household income Penalty like penalty for failure to pay income taxes;

collected by IRS; the question is whether the penalty is itself a tax

Goals: To achieve (almost) universal coverage To reduce adverse selection

But fear is that the relatively negligible penalty will not force compliance, i.e. will not achieve mandate

Why Mandatory and not Voluntary? Healthy people often choose not to purchase insurance

until they become sick and need care This phenomenon justifies behavior by insurers such as

individual rating, denials for pre-existing conditions, & rescissions when insureds become ill The ACA regulates such conduct by insurers that is tolerable

when HI is voluntary but intolerable when insurers are required to accept everyone regardless of health status

If people could get HI regardless of health status, they would opt out of insurance until they became sick and needed health care

When people who can afford health insurance but choose not to be insured become sick and cannot get insurance, unaffordable costs of care are often shifted to the rest of society

Allowing healthy people to opt out of the insurance pools dilutes the pools with a disproportionate number of unhealthy and raises the cost of premiums

The Social Security Model

Social Security, an income-replacement and welfare system, is funded by a mandatory payroll tax If tax were not mandatory, high-income earners would opt

out and contribute to individual retirement accounts which are purely income-replacement

Contributions to Social Security are regressive (12.4% tax on first $106,800 in earnings in 2011)

Distributions are partly income replacement (progressive) and partly redistributive (cross-subsidization) The contributions from high-wage participants are partly

redistributed to lower wage earners in order to ensure an income safety net

Without redistribution from the wealthy, the floor of the income safety net would be substantially lower and standard of living among the elderly would fall

Is the individual mandate different from Social Security?

The Adverse Selection Death Spiral: Voluntary HI and Number of Uninsured A rational decision for young, healthy is to forego health insurance

Preference for spending money on something else; Less risk averse than older and sicker for whom the risk of ill health is

much greater and for whom it is rational to purchase health insurance Insurance pools become highly segmented by health status

As members of the pool become sicker and more costly, insurers Raise premiums and more people drop out because of unaffordability; Refuse to sell or renew or cancel the policies of those who are ill. The number of uninsured rises

Conclusion: It is difficult to achieve affordable universal access unless there is very high participation of the populace in the insurance pools which, in a free-market, competitive system, can be achieved only by mandated participation.

Health Insurance Coverage Distribution of the Non-Elderly Urban Institute Health Insurance Policy

Simulation Model (HIPSM) using data from Massachusetts Without Reform (voluntary):18.6% or 50M

uninsured ACA (mandatory): 8.3% or 22M uninsured

2/5 of 22M eligible but unenrolled in Medicaid & CHIP ¼ undocumented immigrants

ACA mandate repealed (voluntary): 14.9% or 39.8M uninsured Decrease from 18.6% to 14.9% due entirely to

expanded Medicaid (additional 12 – 16M Americans)

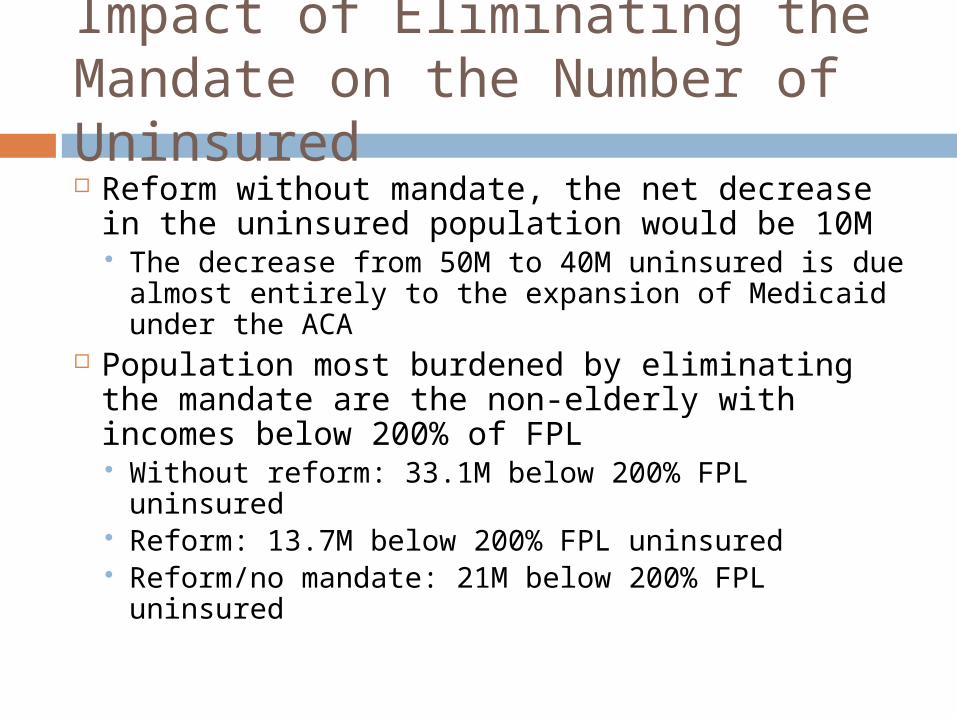

Impact of Eliminating the Mandate on the Number of Uninsured Reform without mandate, the net decrease in

the uninsured population would be 10M The decrease from 50M to 40M uninsured is due

almost entirely to the expansion of Medicaid under the ACA

Population most burdened by eliminating the mandate are the non-elderly with incomes below 200% of FPL Without reform: 33.1M below 200% FPL uninsured Reform: 13.7M below 200% FPL uninsured Reform/no mandate: 21M below 200% FPL

uninsured

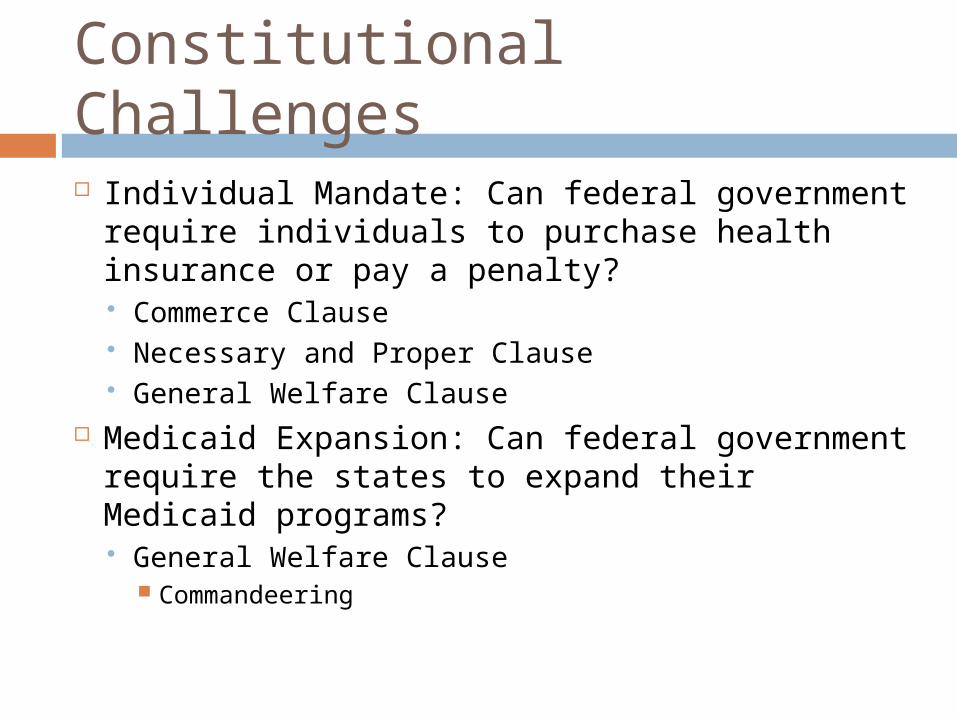

Constitutional Challenges

Individual Mandate: Can federal government require individuals to purchase health insurance or pay a penalty? Commerce Clause Necessary and Proper Clause General Welfare Clause

Medicaid Expansion: Can federal government require the states to expand their Medicaid programs? General Welfare Clause

Commandeering

Federalism: The Allocation of Power Prior to the formation of the United States, there were

thirteen separate and sovereign states The design of authority of the United States is a dual

sovereignty regime that delegates certain powers to the Congress; powers not delegated nor prohibited by the Constitution to the states are reserved to them The federal government is permitted only narrow

authority to regulate in the states (preemption; conditional spending such as Medicaid & EMTALA; Commerce Clause) because it lacks a plenary power to regulate for the general welfare

The individual mandate is a compulsory directive to the states to require their residents to purchase health insurance No language of preemption No conditional spending

Is the Individual Mandate Constitutional? The question is whether the mandate impermissibly

intrudes on the states’ plenary power to regulate for the public’s well-being

The constitutionality of the individual mandate and penalty depends on the USSC’s interpretation of the Commerce Clause which permits Congress to narrowly regulate commerce among the several states under limited conditions: The use of channels of interstate commerce; The instrumentalities of interstate commerce; and Intrastate activities having a substantial economic effect

on interstate commerce Necessary and Proper Clause has been used to implement

the power of Congress over interstate commerce, i.e. where the activity has a substantial economic effect on interstate commerce

Post-New Deal Commerce Clause Jurisprudence The Commerce Clause has historically applied to acts which

directly burden or obstruct interstate commerce Starting in the 1940s (Jones v. Laughlin Steel, Darby, and

Wickard) until the mid-1990s, the USSC broadened its reach to activities, even intrastate activities, that have a “substantial effect” on interstate commerce

In 1995, the Rehnquist Court struck down the federal Gun Free School Zones Act which criminalized the possession of a firearm in a school zone holding it exceeded Congress’s authority under the Commerce Clause because gun possession within 1,000 feet of a school a noneconomic activity (U.S. v. Lopez)

In 2000, the Court reaffirmed the economic/non-economic distinction of Lopez striking down the civil remedy provision of the federal Violence Against Women Act of 1994 which criminalized certain activity against women calling the regulated activity non-economic (U.S. v. Morrison). On behalf of the legislation, the government argued that violence against women deterred women from engaging in interstate commerce thus reducing the productivity of women

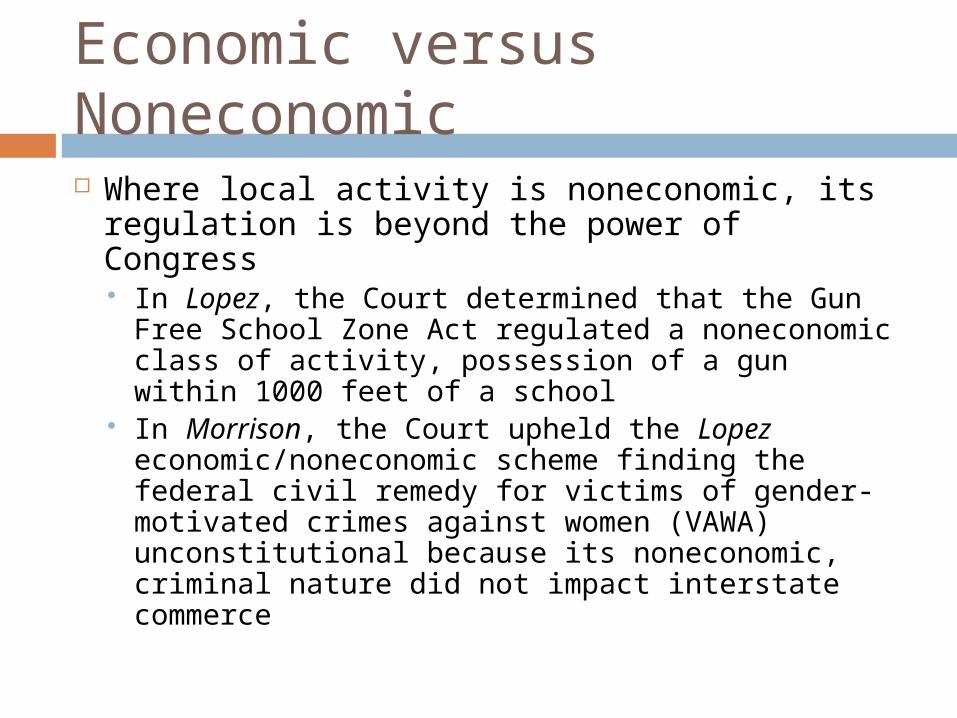

Economic versus Noneconomic Where local activity is noneconomic, its

regulation is beyond the power of Congress In Lopez, the Court determined that the Gun

Free School Zone Act regulated a noneconomic class of activity, possession of a gun within 1000 feet of a school

In Morrison, the Court upheld the Lopez economic/noneconomic scheme finding the federal civil remedy for victims of gender-motivated crimes against women (VAWA) unconstitutional because its noneconomic, criminal nature did not impact interstate commerce

Gonzales v. Raich (2005)

In 2005, the Court again broadened the reach of the Commerce Clause to prohibit, via the federal Controlled Substances Act (to regulate drug trafficking), the local, purely intrastate individual cultivation and use of marijuana permissible under California’s Compassionate Use Act (1996) (Gonzales v. Raich) The CSA regulates the production, distribution, and

consumption of commodities for which there is an established and lucrative interstate market

The Compassionate Use Act creates an exemption from criminal prosecution for physicians as well as patients and primary caregivers who possess or cultivate marijuana for medicinal purposes with the approval of a physician

The 9th Circuit Court of Appeals, relying on Lopez and Morrison, held that purely local cultivation and possession for medicinal purposes was beyond the reach of federal power

Gonzales v. Raich, USSC

The USSC decision relied on the holding of a 1942 case, Wickard v. Filburn, in which the Court upheld a provision of the Agricultural Adjustment Act limiting the quantity of wheat that an individual farmer could grow for his own consumption because of the (aggregate) effect that might have on interstate commerce, i.e. decreasing the demand for wheat in the interstate market

Notwithstanding what seemed to be the purely intrastate nature of the activity, the Court held that Congress can regulate purely intrastate activity if “failure to regulate would undercut regulation of the interstate market in that commodity.” In the case of marijuana, the diversion of homegrown marijuana into the interstate market would frustrate the federal interest in eliminating such commercial transactions, i.e. drug trafficking

The justification for Raich has been attributed to the comprehensiveness of the federal statutory framework for regulating controlled substances

Distinction Between Economic versus Noneconomic Activity In Lopez and Morrison, the Court created an

economic/non-economic scheme Where intrastate economic activity has a

substantial effect on interstate commerce, Congress can regulate In Wickard, the fear was that wheat grown locally

could have been drawn into the interstate market thereby lowering the price of interstate wheat and disrupting the statute’s intent to stabilize that market.

In Raich, the fear was that growing marijuana locally could have an adverse effect on even illegal interstate commerce by increasing the supply of marijuana available in that market and frustrating the intent of the Controlled Substances Act

The ACA Cases to Date

Thomas More Law Center v. Obama, 720 F. Supp. 2d 882 (E.D. Mich 2010) and Liberty Univ., Inc., v. Geithner, WL 4860299 (W.D. Va. 2010), both of which were brought by individual plaintiffs, in which the federal district court judges upheld the individual mandate as constitutional;

Virginia v. Sebelius, 728 F. Supp. 2d 768 ( E.D. Va. 2010), brought by the Commonwealth of Virginia, in which federal district court judge Henry Hudson found the individual mandate unconstitutional, and Florida v. HHS, Case No.: 3:10-cv-91-RV/EMT (N.D. Fla 2011), brought by the State of Florida and 25 other states, in which federal district court judge Roger Vinson found the individual mandate unconstitutional and unseverable from the entire health care reform act.

Other cases have been filed, some dismissed procedurally and others still awaiting disposition

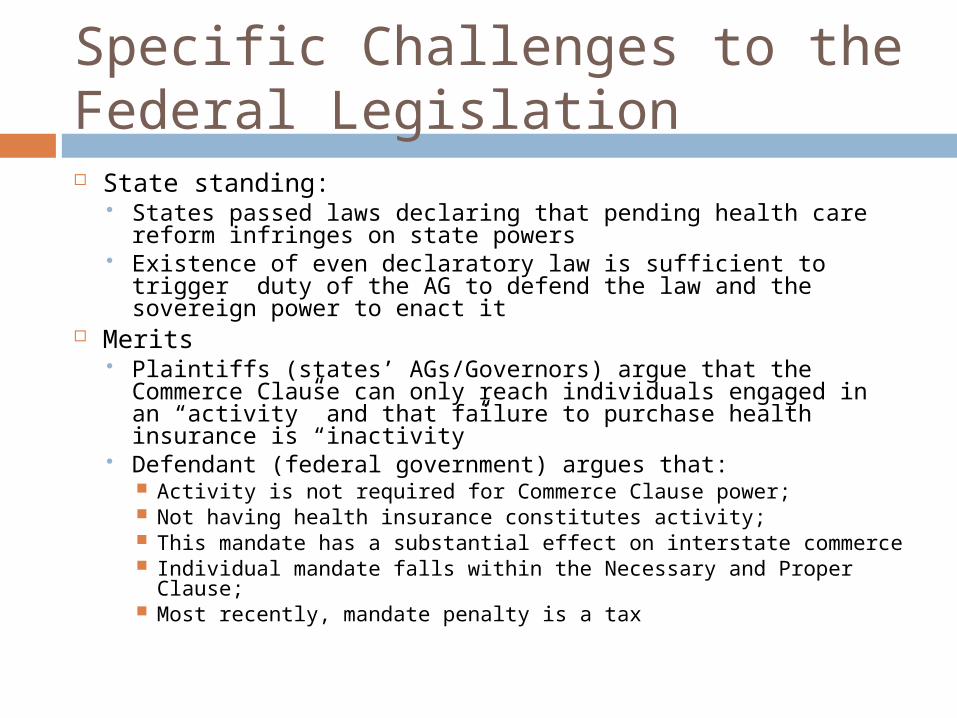

Specific Challenges to the Federal Legislation State standing:

States passed laws declaring that pending health care reform infringes on state powers

Existence of even declaratory law is sufficient to trigger duty of the AG to defend the law and the sovereign power to enact it

Merits Plaintiffs (states’ AGs/Governors) argue that the Commerce

Clause can only reach individuals engaged in an “activity” and that failure to purchase health insurance is “inactivity”

Defendant (federal government) argues that: Activity is not required for Commerce Clause power; Not having health insurance constitutes activity; This mandate has a substantial effect on interstate commerce Individual mandate falls within the Necessary and Proper

Clause; Most recently, mandate penalty is a tax

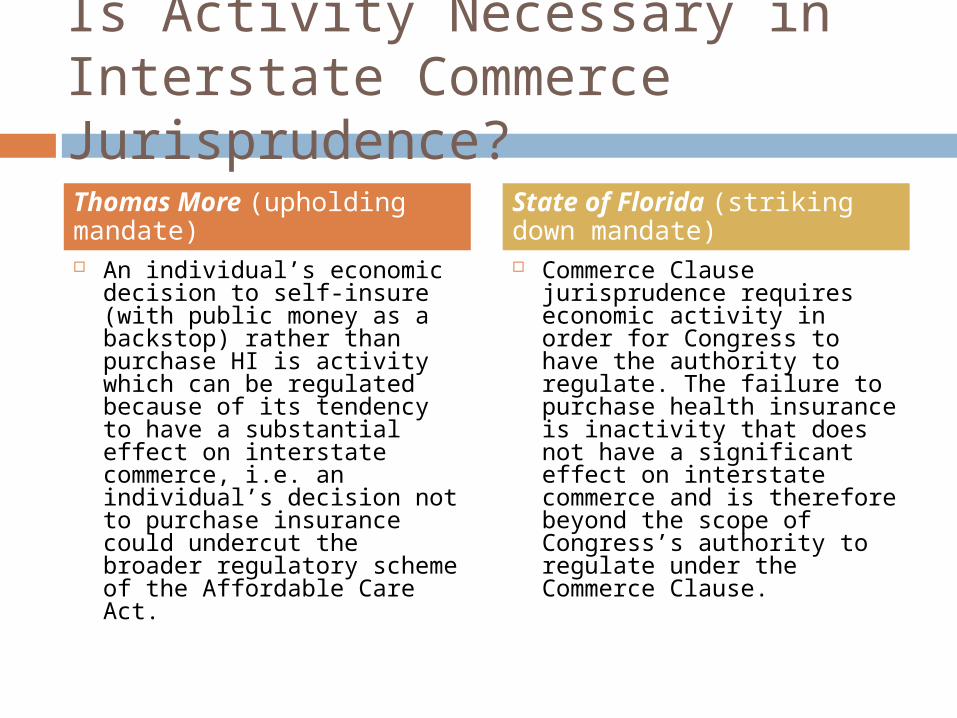

Is Activity Necessary in Interstate Commerce Jurisprudence?

An individual’s economic decision to self-insure (with public money as a backstop) rather than purchase HI is activity which can be regulated because of its tendency to have a substantial effect on interstate commerce, i.e. an individual’s decision not to purchase insurance could undercut the broader regulatory scheme of the Affordable Care Act.

Commerce Clause jurisprudence requires economic activity in order for Congress to have the authority to regulate. The failure to purchase health insurance is inactivity that does not have a significant effect on interstate commerce and is therefore beyond the scope of Congress’s authority to regulate under the Commerce Clause.

Thomas More (upholding mandate)

State of Florida (striking down mandate)

Threshold Commerce Clause Requirement: Activity All prior Commerce Clause jurisprudence has dealt with

regulating an economic activity Economic decision to forego health insurance equals activity

Making an economic decision to forego now and pay for out of pocket later coupled with access to uncompensated care at taxpayer’s expense

Thomas More and Liberty Univ., Inc. One fear of upholding the ACA is the possibility of precedent

Uniqueness of the health insurance market – the limiting principle All human beings are susceptible to illness and injury so no-one can opt

out of the health care market Hospitals required by law to provide care regardless of ability to pay Cost-shifting to third parties; $43B in uncompensated care costs in 2008

But what about the similarities of the food market – can Congress require people to get food insurance?

Predicting the Outcome of the Constitutional Challenges The outcome is difficult to predict for three

reasons: The individual mandate paradigm is so unusual;

Congress has never required individuals to purchase a product from private industry. If Congress can mandate insurance coverage, can it mandate buying and consuming broccoli? Purchasing a GM car should GM become financially unstable? Joining a health club?

Commerce Clause jurisprudence is not compelling either broadly or narrowly (Lopez/Morrison versus Wicker/Raich)

Lack of economic activity has become a new threshold question for courts in determining the constitutionality of the Affordable Care Act Is not having health insurance coverage (1) an activity

versus a non-activity?; (2) one that affects interstate commerce?

Alternative Argument: Necessary and Proper Clause Necessary and Proper Clause

To make all Laws which shall be necessary and proper for carrying into execution the [specifically granted] foregoing Powers

Is the Clause independent or dependent? Can it be used as an independent ground for upholding individual mandate?

Or, alternatively, will it vitiate the enumerated powers doctrine?

ACA Regulatory Reform insurers now must take all comers regardless of health

status and with little differential in rating These reforms incentivize delay in purchase of HI If healthy young people stay out of the pools, less

opportunity to cross-subsidize care of the ill

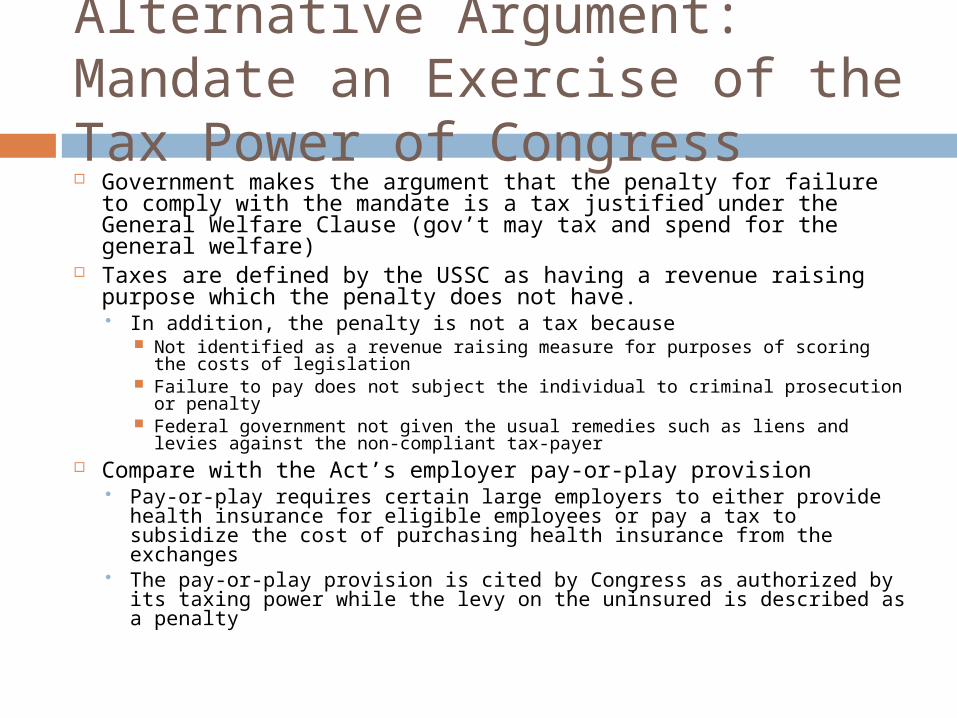

Alternative Argument: Mandate an Exercise of the Tax Power of Congress Government makes the argument that the penalty for failure to

comply with the mandate is a tax justified under the General Welfare Clause (gov’t may tax and spend for the general welfare)

Taxes are defined by the USSC as having a revenue raising purpose which the penalty does not have. In addition, the penalty is not a tax because

Not identified as a revenue raising measure for purposes of scoring the costs of legislation

Failure to pay does not subject the individual to criminal prosecution or penalty

Federal government not given the usual remedies such as liens and levies against the non-compliant tax-payer

Compare with the Act’s employer pay-or-play provision Pay-or-play requires certain large employers to either provide health

insurance for eligible employees or pay a tax to subsidize the cost of purchasing health insurance from the exchanges

The pay-or-play provision is cited by Congress as authorized by its taxing power while the levy on the uninsured is described as a penalty

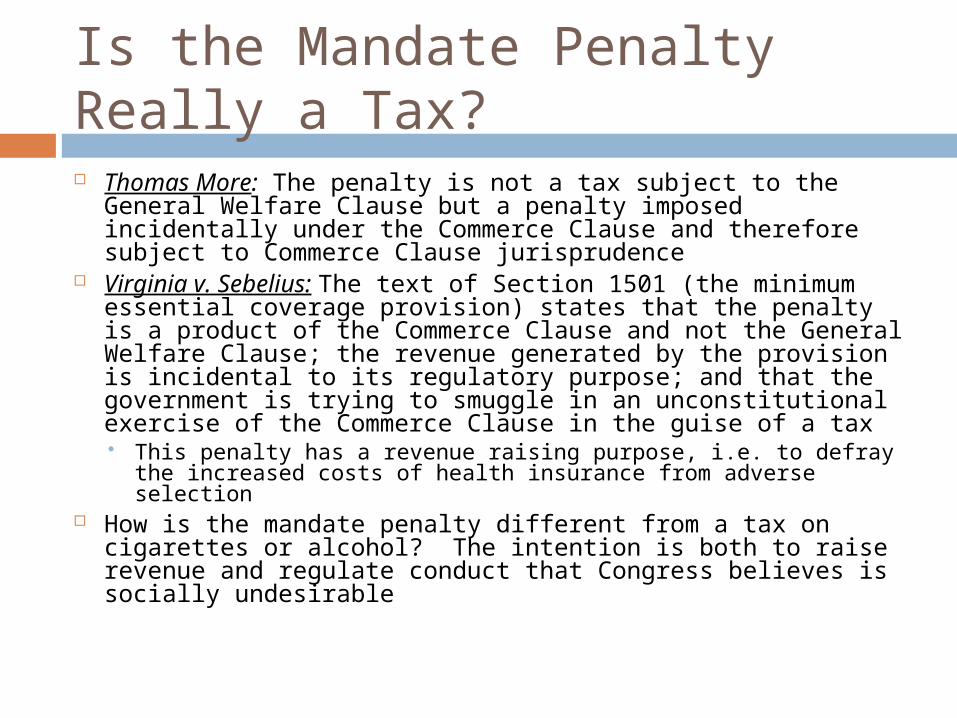

Is the Mandate Penalty Really a Tax? Thomas More: The penalty is not a tax subject to the

General Welfare Clause but a penalty imposed incidentally under the Commerce Clause and therefore subject to Commerce Clause jurisprudence

Virginia v. Sebelius: The text of Section 1501 (the minimum essential coverage provision) states that the penalty is a product of the Commerce Clause and not the General Welfare Clause; the revenue generated by the provision is incidental to its regulatory purpose; and that the government is trying to smuggle in an unconstitutional exercise of the Commerce Clause in the guise of a tax This penalty has a revenue raising purpose, i.e. to defray the

increased costs of health insurance from adverse selection How is the mandate penalty different from a tax on

cigarettes or alcohol? The intention is both to raise revenue and regulate conduct that Congress believes is socially undesirable

Medicaid and Health Care Reform Medicaid is a conditional spending program; federal assistance

depends on states’ voluntary opt in and compliance Currently FMAP is from 50% - 75% of costs

One way the ACA expands coverage is to expand Medicaid eligibility to all adults whose income does not exceed 133% of FLP ($14,404) Presently, deserving poor (pregnant women, children until 19, aged,

disabled, adults with dependent children at varying levels of income) Individuals above 133% FLP and 400% of FLP entitled to federal HI

premium subsidies Expands Medicaid by 16M Federal government to pick up approximately 95% of the cost of

additional Medicaid beneficiaries from 2014 - 2019 with states picking up the balance

Congress projects that over time Medicaid expansion will save the states money such as uncompensated care costs and costs of coverage of beneficiaries who will shift to HI exchanges and premium subsidies

Challenges to Expansion of Medicaid In Florida vs. HHS, the state plaintiffs claim that the Act

violates the Spending Clause of the Constitution by expanding and altering the Medicaid program to such an extent they cannot afford the newly-imposed costs and burdens

They allege that Medicaid expansion violates the Spending Clause because it is coercive and effectively commandeers the states The states argue that because they have no choice but to

participate in the Medicaid program, the lack of choice transforms the spending provision from pressure into compulsion

The Hobson’s Choice the states are put to is (1) to accept the new costs and obligations of the Medicaid expansion; or (2) exit the Medicaid program altogether and lose FMAP

Judge Vinson, in Florida vs. HHS, ruled in favor of the government that the states’ claim of commandeering did not survive a motion for summary judgment

Can Congress Make You Buy a Broccoli? A GM car? The individual mandate penalizes individuals who do

not purchase a product from a private company The requirement of the purchase of health insurance is

necessary because Congress chose to solve the universal health insurance problem by preserving the private insurance market instead of adopting a single-payer solution like “Medicare For All”

If Congress can force individuals to purchase HI, can it make you buy broccoli? Can it make you buy a GM car if GM is again on the verge of insolvency?

The irony of the challenges to the mandate is that preservation of the private insurance market was a conservative shield against the single-payer option, and is now being used, after the fact, as a sword against the constitutionality of the ACA.

Is Constitutionality of the Mandate Really a Political Issue? Constitutionality issue arises because Congress

insisted and the administration acquiesced on preserving private insurance market Individual mandate necessary to stabilize private

insurance market in light of regulatory reforms Reforms make it possible for individuals to opt out If the healthy opt out, adverse selection spiral causes

prices to rise forcing out more and . . . . . . . . . . . . . . . The federal district court cases to date have fallen out

along party lines, i.e. depending on the political affinity of the judges Is this because conservative judges simply don’t like

health care reform (or Barack Obama) or because they believe that Congress has really overstepped the scope of its Commerce Clause power?

It’s a Long Way to the Supreme Court Eventually, the USSC will no doubt opine on

whether the PPACA will survive constitutional muster but, on the way, a number of circuit courts of appeal will opine as well The federal bench is populated with judges who

believe there is too much government regulation of economic affairs

Can this be true after the cataclysmic financial meltdown?

Once it gets to the USSC, the question is whether the Court will divide on political lines (Roberts, Scalia, Thomas and Alito vs. Ginsburg, Breyer, Sotomayor, and Kagan with Kennedy havingf the swing vote) Larry Tribe’s February 7 op-ed piece in the NYTimes