Chairman’s Statement - Cagamas Berhad Report/ar02corp_part3... · Laporan Tahunan 2002 Annual...

39

52 CAGAMAS BERHAD 157931-A In 2002, the Company diversified more aggresively into hire purchase and leasing debts and Islamic hire purchase debts. This strategy yielded positive results as evidenced by the achievement of a higher volume of purchases of loans and debts and higher profitability in 2002.

Transcript of Chairman’s Statement - Cagamas Berhad Report/ar02corp_part3... · Laporan Tahunan 2002 Annual...

52 CAGAMAS BERHAD 157931-A

In 2002, the Company diversified moreaggresively into hire purchase and leasingdebts and Islamic hire purchase debts. Thisstrategy yielded positive results as evidencedby the achievement of a higher volume ofpurchases of loans and debts and higherprofitability in 2002.

Laporan Tahunan 2002 Annual Report 53

Chairman’s Statement

Ooi Sang KuangChairman

On behalf of the Board of Directors, I am pleased topresent the Sixteenth Annual Report and the FinancialStatements of Cagamas Berhad, the NationalMortgage Corporation, for the financial year ended31 December 2002.

The year 2002 presented a challenging environmentof excess liquidity in the banking system and lowinterest rates. The commercial banks were generallyless forthcoming in selling their housing loans toCagamas. However, to hedge their fixed rateportfolio, the finance companies took advantage ofthe low fixed Cagamas rates to sell their hirepurchase and leasing debts, which accounted for62.8% of total purchases by Cagamas during they e a r.

In the face of a more challenging environment,Cagamas embarked on an aggressive marketingstrategy to promote its products. In addition, the

Company began to diversify more aggresively intohire purchase and leasing debts and Islamic hirepurchase debts. This strategy yielded positive resultsas evidenced by the achievement of a higher volumeof purchases of loans and debts and higherprofitability in 2002. The diversification strategy hasfurther enhanced the resilience of Cagamas.

H i g h l i g h t s

During the year, the Company recorded purchases ofloans and debts amounting to RM10,992 million, thehighest volume of purchases in any single year. Byend 2002, Cagamas had purchased 15.9% of thehousing loans and 18.6% of the hire purchase andleasing debts outstanding in the banking system.To d a y, Cagamas is well-positioned to continue itslead and prominent role in providing competitivelypriced funds to the banking system.

54 CAGAMAS BERHAD 157931-A

The Company will continue to support Bank NegaraMalaysia’s promotion of a dual banking system, withan Islamic banking system operating parallel with theconventional banking system. During the year,Cagamas purchased RM610 million of Islamic assets,RM500 million of which consisted of Islamic hirepurchase debts. This represented the highest volume ofpurchases of Islamic assets since the introduction ofIslamic products in 1994.

Outstanding Cagamas bonds as at end of December2002 stood at RM22,595 million which accounted for16.5% of the private debt securities or 7.9% of thetotal bonds (including public sector securities)outstanding in the capital market.

Reflecting the financial strength of the Company andits prudent risk management practices, bonds andnotes issued by Cagamas in 2002 continued to beassigned the highest ratings of AAA and P1 by RatingAgency Malaysia Berhad and AAA and MARC-1 byMalaysian Rating Corporation Berhad.

Financial Performance

During the year 2002, Cagamas achieved a pre-taxprofit of RM208 million, a sharp improvement of26.1% over the previous year’s pre-tax profit ofRM165 million. This is a significant achievement asthe Company was able to reverse the declining trendin profit over the past three years. The rise in profitwas attributed to the higher volume of loans and debtspurchased during the year, with a significant portionof the total purchases amounting to 64.1% made inthe first half of 2002.

The after-tax return per share increased from 79 sen in2001 to 100 sen in 2002, providing an after-taxreturn of 13.6% on average shareholders’ funds,compared with 11.9% in the previous year.Correspondingly, the Company’s shareholders’ fundsincreased by 12.4% from RM1,036 million in 2001 toRM1,164 million in 2002, while net tangible assetsper share increased from RM6.91 at the end of 2001to RM7.76 at the end of 2002. The larger volume ofnew purchases in 2002 also contributed to anincrease in the Company’s total assets fromRM22,812 million as at the end of 2001 toRM26,383 million as at the end of 2002.

Dividend

For the half-year ended 30 June 2002, the Board ofDirectors had declared an interim dividend paymentof 10 sen per share less income tax. To reflect thehealthy financial performance of the Company, theBoard recommended a final dividend payment of 15sen per share less income tax. In view of the largereserves totalling RM1,014.3 million and the high risk-weighted capital ratio of 22.3% as at the end of 2002as well as to commemorate the Fifteenth Anniversaryof the Company, the Board also recommended aspecial dividend of 93 sen per share tax exempt,bringing the total dividend for the financial yearended 31 December 2002 to 25 sen per share lessincome tax and 93 sen per share tax exempt, asagainst 20 sen per share less income tax in 2001. Thetotal dividend proposed for the financial year 2002represented a dividend cover of 0.9 times.

Initiatives in 2002

Applying and leveraging on state-of-the-art technologywill continue to be a challenge for the Company,particularly in integrating such technology intomainstream business. Towards this end, the Companyhas embarked on the first phase of the implementationof a 3-year Information and CommunicationsTechnology (ICT) Master Plan. During the year, theLoans Processing System and Treasury ManagementSystem were implemented to enhance productivity,ensure efficient work processes, deliver new productsand services more effectively and undertake effectiverisk management.

Mindful of the need to be prepared for any unforeseendevelopments, a comprehensive Business ContinuityPlan (BCP) to minimise the impact from any potentialdisruptions arising from internal and external disasterswas put in place. The BCP will be regularly updatedand tested to ensure that the Company is able tomobilise its resources speedily to undertake recoveryoperations.

The Company observes high standards oft r a n s p a r e n c y, accountability and integrity in itsbusiness dealings, operations and corporatedisclosure. Cagamas is committed to adhering andapplying the relevant principles and best practices of

Laporan Tahunan 2002 Annual Report 55

the Malaysian Code on Corporate Governance in itspolicies and procedures. During the year, theCompany also put in place a risk managementframework to effectively evaluate risk while achievingmaximisation of shareholders’ value and sustainabilityof business performance.

Prospects

The ongoing financial and economic liberalisation willbring forth new opportunities as well as challenges forCagamas. The continued success of the Company willhinge on the strength of its professionalism,leadership, financial creativity and innovation indeveloping new products in response to the rapidlychanging demands of the capital market in anincreasingly competitive environment.

The Company will be increasing its product offeringwith the introduction of the purchase of credit cardreceivables from financial institutions on with recoursebasis in January 2003. Going forward, the Companywould continue to step up its efforts in enhancing itsexisting products, developing new products andexploring new business opportunities in order tosustain its growth and meet the increasinglysophisticated needs of the market.

In order to improve the competitiveness and enhancethe attractiveness of its products, efficient deliverychannels via ICT will be emphasised to better serveand extend its services directly to its customers,especially with the use of Internet and web-basedapplications. The Company will continue to leverageon technology to introduce new products, streamlineoperations and expand business opportunities.

With the risk management framework already inplace, the Company plans to develop and implementan enterprise-wide risk management strategy forquantifying the various risks inherent in the Company’sbusiness. This involves aligning business strategieswith the corporate risk management policy,developing risk models, systems and datamanagement capabilities and the use of multi-disciplinary teams and committees as a mechanism tofacilitate risk management processes.

Over the years, Cagamas has gained internationalrecognition as a model for developing countriesconsidering the establishment of a secondarymortgage market. As testimony to this, in 2002,Cagamas received representatives from a number ofcountries interested to study the set-up and operationsof Cagamas. The World Bank also invited Cagamasto present its model and experience at conferencesheld in Bangladesh and Pakistan.

Acknowledgement

On behalf of the Board of Directors, I would like totake this opportunity to record my appreciation to ourcustomers and shareholders for their continuedsupport towards our commendable performance in2002. The Board also wishes to extend its sincereappreciation to the regulatory authorities, inparticular, the Ministry of Finance, the SecuritiesCommission, Bank Negara Malaysia and theCompanies Commission of Malaysia for theircontinuous and invaluable support and contributionstowards enabling the Company to successfully achieveits goal as a premier secondary market institution.

On behalf of the Board, I am pleased to welcomeEncik Michael Andrew Hague who joined the Board inJuly 2002. I would like to express the Board’sgratitude to Y. Bhg. Tan Sri Dato’ Sri Dr. Zeti AkhtarAziz, Governor, Bank Negara Malaysia, whorelinquished her post as Chairman and Director of theCompany in October 2002. Cagamas is muchindebted to Y. Bhg. Tan Sri Dato’ Sri Dr. Zeti AkhtarAziz for her stewardship in leading the Companytowards greater heights and rapid and sustainablegrowth. I would also like to record the Board’sappreciation of the contributions made by PuanYvonne Chia, Dato’ Huang Sin Cheng and Encik LeeKam Chuen who resigned from the Board in March,June and December 2002 respectively.

Ooi Sang KuangChairman

56 CAGAMAS BERHAD 157931-A

Cagamas was established in December 1986 for thepurpose of serving as a special vehicle to mobiliselow-cost funds to support the national home ownershippolicy and to spearhead the development of theprivate debt securities market in Malaysia. T h eCompany has been in operation for 15 years sincecommencement of business in October 1987. As atend December 2002, total volume of outstandinghousing loans purchased by Cagamas amounted toRM14,823 million, while total Cagamas debtsecurities outstanding amounted to RM24,970 million.

The Malaysian Mortgage and Debt SecuritiesMarket Prior to the Establishment ofCagamas

Since the 1970s, the Malaysian Government has beenactively promoting widespread ownership of housing,especially amongst the low and middle-incomegroups. This national objective can only be realised ifthese groups have ready access to credit facilities.Such access is only possible if there are willing lendersand the cost of paying the interest and principal iswithin the means of the borrowers. However, theprincipal providers of housing loans would only bewilling lenders if they were able to secure thenecessary funds at an economical cost, and sell someof the existing housing loans so that such long-termloans do not constitute an excessive proportion of theirtotal assets.

In the early 1980s, the financial institutions wereexperiencing a tight liquidity situation as reflected bytheir loans to deposits ratio which deteriorated to98.0% as at 30 September 1986, from 89.0% as atthe end of 1980. Hence, the financial institutions werereluctant to give out housing loans which areconsidered to be long-term illiquid assets.

In addition, as the financial institutions borrow short-term (largely in the form of deposits of 12 months orless) and housing loans were long-term (10 to 15years), the financial institutions were subject toliquidity risk arising from the mismatch of maturities ofthe funds and the housing loans. The financialinstitutions also faced financial risk if their source offunds became more expensive than the rate of returnon their housing loans, especially in view of the factthat the interest rates on the loans for low and medium-cost houses costing RM100,000 and below werefixed at controlled levels.

Moreover, the private debt securities market wasvirtually absent until the creation of Cagamas. Up tothe 1980s, the debt securities market was dominatedby Malaysian Government Securities.

Characteristics of Housing Loans in Malaysia

P r e s e n t l y, housing loans in Malaysia have thefollowing characteristics:

(a) Housing loans have maturities ranging from 15 to30 years, as against the deposits of the financialinstitutions (where maturities are primarily 12months or less), thus exposing the banks tointerest rate risk; and

(b) Housing loans have low default rates andforeclosure losses are minimal. Hence, thefinancial institutions are reluctant to sell themoutright.

The Cagamas Model: A Unique Secondary Mortgage MarketConduit for Emerging Economies

The scheme to purchase mortgages formulated byCagamas was designed to suit domestic conditionsand to overcome barriers that could prevent thescheme from taking off.

The following are some of the special features ofCagamas’ model that has been accepted in thefinancial market:

(a) Purchase with Recourse

Under this scheme, Cagamas purchases housingloans with recourse to the primary lender i.e. thelatter is responsible for any loss arising from thedefault of the borrower. As there was a lack ofinformation regarding the credit risks involved ina housing loan, it was prudent for the Companyto purchase loans without taking the credit risk.Although Cagamas introduced the purchase ofhousing loans without recourse in 1999, thefinancial institutions have not sold any of theirhousing loans under this scheme. The reluctanceto sell is due to the concern that their non-performing loans ratio would deteriorate if goodquality loans are taken off from their balancesheet.

Evolution of Cagamas

Laporan Tahunan 2002 Annual Report 57

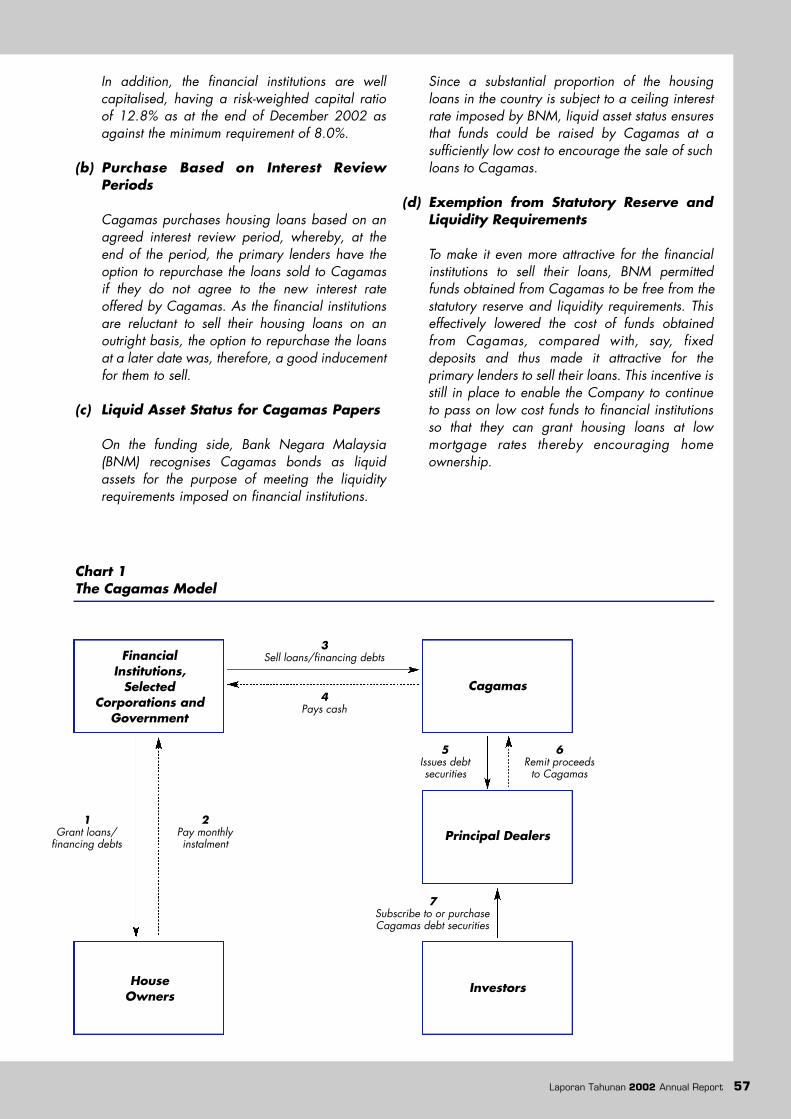

In addition, the financial institutions are wellcapitalised, having a risk-weighted capital ratioof 12.8% as at the end of December 2002 asagainst the minimum requirement of 8.0%.

(b) P u rchase Based on Interest ReviewPeriods

Cagamas purchases housing loans based on anagreed interest review period, whereby, at theend of the period, the primary lenders have theoption to repurchase the loans sold to Cagamasif they do not agree to the new interest rateoffered by Cagamas. As the financial institutionsare reluctant to sell their housing loans on anoutright basis, the option to repurchase the loansat a later date was, therefore, a good inducementfor them to sell.

(c) Liquid Asset Status for Cagamas Papers

On the funding side, Bank Negara Malaysia(BNM) recognises Cagamas bonds as liquidassets for the purpose of meeting the liquidityrequirements imposed on financial institutions.

Since a substantial proportion of the housingloans in the country is subject to a ceiling interestrate imposed by BNM, liquid asset status ensuresthat funds could be raised by Cagamas at asufficiently low cost to encourage the sale of suchloans to Cagamas.

(d) Exemption from Statutory Reserve andLiquidity Requirements

To make it even more attractive for the financialinstitutions to sell their loans, BNM permittedfunds obtained from Cagamas to be free from thestatutory reserve and liquidity requirements. Thiseffectively lowered the cost of funds obtainedfrom Cagamas, compared with, say, fixeddeposits and thus made it attractive for theprimary lenders to sell their loans. This incentive isstill in place to enable the Company to continueto pass on low cost funds to financial institutionsso that they can grant housing loans at lowmortgage rates thereby encouraging homeownership.

Chart 1The Cagamas Model

1Grant loans/

financing debts

2Pay monthlyinstalment

3Sell loans/financing debts

4Pays cash

5Issues debtsecurities

7Subscribe to or purchaseCagamas debt securities

6Remit proceeds

to Cagamas

Principal Dealers

InvestorsHouse Owners

Financial Institutions,

SelectedCorporations and

Government

Cagamas

58 CAGAMAS BERHAD 157931-A

Cagamas purchases housing loans from theinstitutions which originate the loans at the primarylevel and issues Cagamas debt securities to financethe purchases. In effect, Cagamas turns the housingloans into debt securities at the secondary levelthrough a process, which is tailored to suit theMalaysian market environment.

The process is shown in Chart 1. The originators,n a m e l y, the commercial banks and the financecompanies, grant housing loans to the house buyers.They subsequently sell these loans to Cagamas withrecourse. Cagamas then raises funds from the marketto finance these purchases by issuing debt securities,in the form of Cagamas bonds and short-termCagamas notes, to investors.

Investors include financial institutions, insurancecompanies, pension funds, non-resident companiesand others who are interested in investing in short- andmedium-term papers to obtain an income either at afixed or adjustable interest rate. In essence, this is theway the secondary mortgage market currentlyoperates in Malaysia.

The Cagamas Model: Its Success Story

In its unique way, the Cagamas model can beconsidered a success as it has benefited both housebuyers and institutional players involved in its operations.

(a) House Buyers

The competitively-priced funds made available tothe primary lenders through Cagamas’ schemehave enabled house buyers to obtain easy accessto housing loans at a reasonable cost. This has inturn encouraged home ownership and helped thedevelopment of the housing industry.

(b) Financial Institutions

By selling their housing loans to Cagamas, thefinancial institutions are able to obtain thenecessary liquidity at a competitive cost to enablethem to further originate housing loans andenhance their lending operations. This can beseen from the increase in housing loans approvedby the commercial banks and finance companies,by more than a thousand-fold from RM1.8 billionin 1987 to RM29.2 billion as at 31 December2002, as shown in Chart 2. The only exceptionwas 1998 where the amount of housing loansapproved dropped sharply as a result of theeconomic contraction.

Chart 2Total Housing Loans Approved by the Financial Institutions

Source: BNM Annual Reports and Monthly Statistical Bulletins

RM million

30,000

25,000

20,000

15,000

10,000

5,000

01987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Year

Laporan Tahunan 2002 Annual Report 59

The competitively-priced funds obtained fromCagamas also enabled the financial institutions toprice their loan products competitively and thisprovided them with an edge in their businessoperations. By selling their housing loans toCagamas, the primary lenders were also able tohedge their interest rate risks, particularly if theyhad granted fixed rate loans.

(c) Investors

Cagamas securities have been given the highestrating by the two domestic rating agencies inMalaysia. This reflects the high quality ofCagamas papers which provide investors a safeand reasonable return on their investments.Pension and provident funds, insurancecompanies and commercial banks with largesurplus funds find Cagamas securities anattractive investment.

(d) Government and the Economy

The secondary mortgage market has helped theGovernment to achieve its policy of encouraginghome ownership, particularly amongst the lowand middle-income groups. This is because inMalaysia, loans to finance the purchase of housescosting RM100,000 or less are subject to aninterest rate ceiling of 9.0% per annum imposedby BNM. Cagamas funds, which arecompetitively priced, enable the financialinstitutions to meet the policy objective of BNM tomake housing loans more affordable to the lowerincome group without any interest subsidy beingincurred by the authorities.

The Cagamas Model: Initial Obstacles and Challenges

The initial years of Cagamas were not withoutdifficulties. The unfamiliarity of its operations and itslimited product line were obstacles to its development.It was only after a slow start-up phase of five years thatthe Company has been able to establish its marketniche.

(a) Start-up Phase (1987 - 1991)

When Cagamas commenced operations inOctober 1987, it only purchased one product,namely housing loans on fixed rate basis for a 5-year period. In 1988, Cagamas began topurchase housing loans from the Government ofMalaysia. In 1989 and 1990, Cagamas alsoextended the purchases on fixed rates for 3- and7-year periods. The first five years werecharacterised by low volumes of housing loansbeing sold to Cagamas. This was due to thefollowing reasons:

(i) The financial institutions were not familiarwith Cagamas’ operations and theadvantages of selling their housing loans toCagamas; and

(ii) Cagamas only purchased on fixed ratebasis. Hence, the financial institutions werenot prepared to sell their loans, particularlyin 1991 when interest rates were decliningrapidly.

As at the end of December 1991, outstandinghousing loans with Cagamas amounted to onlyRM2 billion.

(b) Take-off and Growth Phase (1992 - to date)

This take-off phase which started in 1992 wascharacterised by active marketing of its productsto the financial institutions and the innovation ofnew products to suit the needs of the market. In1992, in response to the continued downwardtrend in interest rates, Cagamas introducedfloating rate purchases. In 1993, Cagamasintroduced the convertible rate purchaseswhereby the sellers were given the option toswitch from fixed rate to floating rate or vice-versahalf way through their purchase period. Inaddition, Cagamas also started to widen its clientbase by purchasing housing loans from selectedcorporations in 1994, in addition to purchasesfrom the financial institutions and theGovernment.

60 CAGAMAS BERHAD 157931-A

From its initial product of purchasing housing loans, the Company has extended its range of products as shownin Table 1 below:

Conclusion

Malaysia was the first country in the region and oneof the earliest amongst the developing economies, toestablish a secondary mortgage market. At the time ofthe establishment of the market, the business andfinancial community in Malaysia was not familiar withthe concept of a secondary mortgage market and thebond market was still under-developed. To d a y,Cagamas has established the foundation andframework for other institutions to further develop themortgage market and to enhance the private debtsecurities market. Its success today has beenrecognised by other countries such as Indonesia,Thailand, Kazakhstan, Ghana and Jordan as well asthe World Bank and the Asian Development Bank.

With rapidly rising income levels and increasedurbanisation, demand for housing will continue toincrease. Thus, the availability of housing finance atreasonable mortgage rates will continue to play animportant role in ensuring home affordability. In linewith its mission to promote home ownership,Cagamas on its part, will continually refine, modifyand introduce new products to meet the challenges ofensuring easy accessibility to housing loans at anaffordable cost. In addition, the Company will alsocontinue to refine and enhance its existing non-housing loans products to cater to the needs of itscustomers.

Table 1Range of Cagamas’ Products (1992 - to date)

Year Product PurposeIntroduced

Purchase With Recourse:

1994 Islamic house financing debts • provides liquidity to the Islamic institutions • promotes the creation of more Islamic house financing debts

1996 Industrial property loans • encourages the development of the manufacturing sector,especially the small and medium-scale enterprises

• provides the financial institutions an additional avenue to lock-in their funding position in order to hedge their longer term fixed rate loans

1998 Hire purchase and leasing debts • provided the finance companies with a much needed source of medium-term financing during the 1997-98 economic crisis

• serves as a hedging mechanism for such debts which are granted on a fixed rate basis

• eventually enables the finance companies to lower the rates charged to their customers

• alleviates the funding mismatch problem and provides the finance companies an avenue to minimise their interest rate risks

2002 Islamic hire purchase debts • provides Islamic institutions with an avenue to raise fixed rate funds at low cost to hedge their fixed rate assets

2003 Credit card receivables • provides liquidity to financial institutions which generate credit card receivables

• allows the financial institutions to diversify their funding sources

Purchase Without Recourse:

1999 Housing loans • introduced in tandem with the thrust towards asset-backed securitisation

• improves the risk-weighted capital adequacy ratio of the financial institutions as Cagamas will bear the credit risk on the housing loans sold to the Company for the remaining life of the loans

Laporan Tahunan 2002 Annual Report 61

The Company purchased a record volume ofhousing loans and hire purchase and leasingdebts in 2002, which is by far the largestvolume ever purchased in a single year.

62 CAGAMAS BERHAD 157931-A

Purchase Activities

The Company purchased a record volume of housingloans and hire purchase and leasing (HP&L) debtsamounting to RM10,992 million in 2002. This was50.1% higher than the volume of RM7,321 million ofhousing loans, HP&L debts and industrial propertyloans (collectively known as loans and debts)purchased in 2001 and by far the largest volumeever purchased in a single year. The recordpurchases in 2002 were achieved in spite of theexcess liquidity in the banking system and lowinterest rates. This reflects the success of concertede fforts made to market the Company’s facilities.

The financial institutions, especially the financecompanies, capitalised on the low fixed Cagamasrate to hedge their fixed rate portfolio, leading to asignificant increase in the purchase of HP&L debts by75.3% from RM3,940 million in 2001 to RM6,907million in 2002. Purchases of housing loans increasedby 22.0% from RM3,349 million in 2001 to RM4,085million in 2002. As in the previous year, financialinstitutions continued to lock in for longer tenures totake advantage of the low Cagamas rates. Of the totalpurchases, 74.8% or RM8,225 million were forlonger tenures of four to 10 years as compared with59.6% in 2001.

Following the introduction of the scheme to purchaseIslamic hire purchase (IHP) debts in December 2001,the Company made its maiden purchase of IHP debtsamounting to RM500 million in April 2002. In

addition, the Company also purchased RM110 millionof Islamic house financing (IHF) debts for tenuresranging from five to seven years. The RM610 millionof Islamic assets acquired by Cagamas in 2002represents the single largest volume of purchases ofIslamic assets since Cagamas introduced its Islamicproduct in 1994.

Table 2 shows the Company’s purchases ofconventional housing loans and IHF debts fromfinancial institutions in 2002 by geographicaldistribution. About three-quarters of the total numberand value of conventional housing loans and IHFdebts purchased from the financial institutions wereoriginated in Kuala Lumpur, Johor, Selangor andPenang.

During the year under review, a total of RM4,196million of loans and debts were repurchased byfinancial institutions and selected corporations. Of thisamount, RM3,711 million represented housing loansand industrial property loans, whilst another RM485million consisted of HP&L debts. Under the terms forthe sale of loans and debts, the selling institutionsundertake to repurchase the loans and debts inC a g a m a s ’ portfolio if the loans and debts areredeemed by the borrowers or are found to bedefective. In addition, the selling institutions are alsorequired to repurchase the loans and debts sold toCagamas at the price review date if they do not agreeto the revised price offered by Cagamas for therollover of the purchase contract.

Operations

Table 2Purchases of Conventional Housing Loans and IHF Debts by Geographical Distribution

Purchase Value Number of State RM million % Loans %

Kuala Lumpur 1,753 45.5 22,334 38.1Johor 701 18.2 10,794 18.4Selangor 431 11.2 6,572 11.3Penang 186 4.8 3,870 6.6Kedah 184 4.8 3,909 6.7Negeri Sembilan 119 3.1 2,050 3.5Perlis 109 2.8 2,860 4.9Melaka 94 2.4 1,519 2.6Sarawak 77 2.0 1,005 1.7Perak 76 2.0 1,704 2.9Sabah 53 1.4 658 1.1Pahang 38 1.0 778 1.3Kelantan 18 0.5 296 0.5Terengganu 11 0.3 243 0.4Labuan 0 0.0 1 0.0

Total 3,850 100.0 58,593 100.0

Laporan Tahunan 2002 Annual Report 63

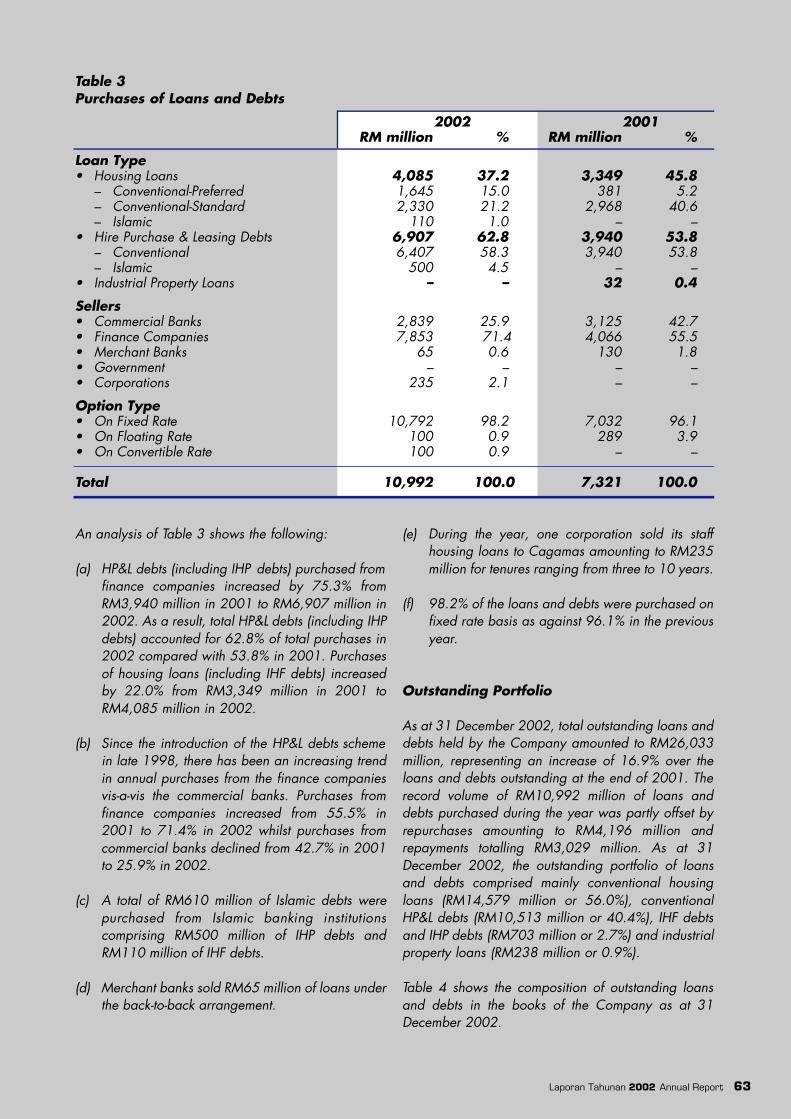

An analysis of Table 3 shows the following:

(a) HP&L debts (including IHP debts) purchased fromfinance companies increased by 75.3% fromRM3,940 million in 2001 to RM6,907 million in2002. As a result, total HP&L debts (including IHPdebts) accounted for 62.8% of total purchases in2002 compared with 53.8% in 2001. Purchasesof housing loans (including IHF debts) increasedby 22.0% from RM3,349 million in 2001 toRM4,085 million in 2002.

(b) Since the introduction of the HP&L debts schemein late 1998, there has been an increasing trendin annual purchases from the finance companiesvis-a-vis the commercial banks. Purchases fromfinance companies increased from 55.5% in2001 to 71.4% in 2002 whilst purchases fromcommercial banks declined from 42.7% in 2001to 25.9% in 2002.

(c) A total of RM610 million of Islamic debts werepurchased from Islamic banking institutionscomprising RM500 million of IHP debts andRM110 million of IHF debts.

(d) Merchant banks sold RM65 million of loans underthe back-to-back arrangement.

(e) During the year, one corporation sold its staffhousing loans to Cagamas amounting to RM235million for tenures ranging from three to 10 years.

(f) 98.2% of the loans and debts were purchased onfixed rate basis as against 96.1% in the previousyear.

Outstanding Portfolio

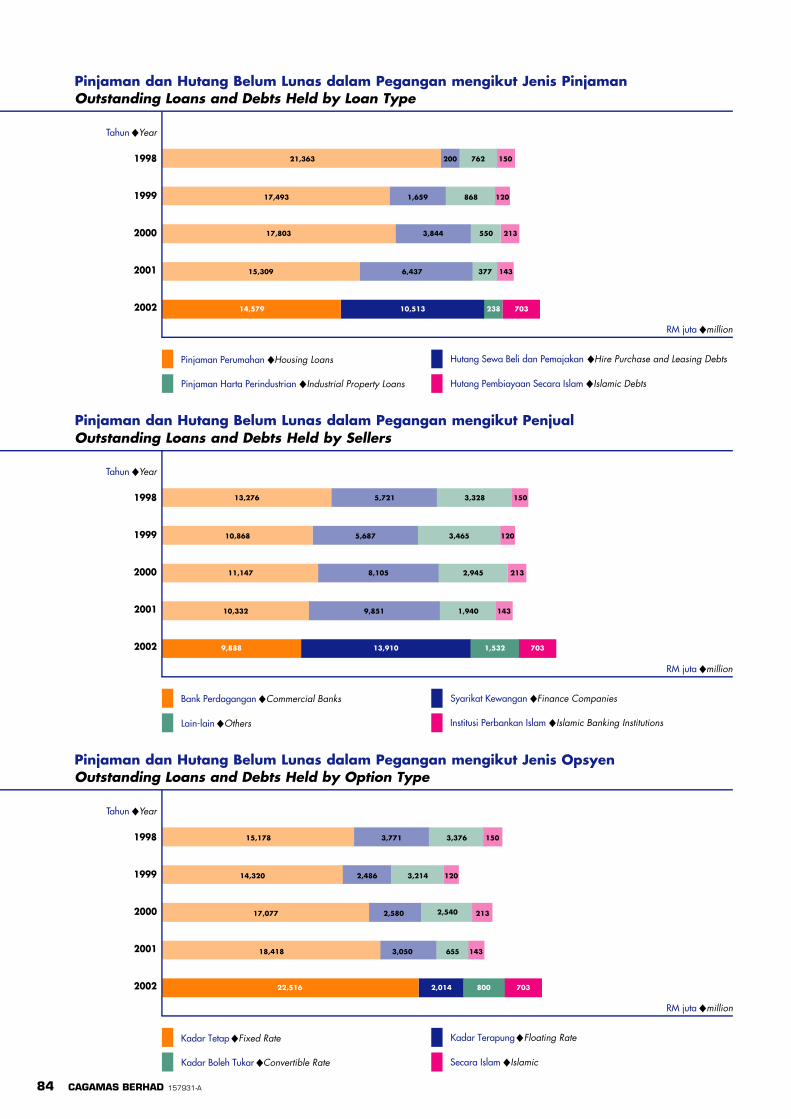

As at 31 December 2002, total outstanding loans anddebts held by the Company amounted to RM26,033million, representing an increase of 16.9% over theloans and debts outstanding at the end of 2001. Therecord volume of RM10,992 million of loans anddebts purchased during the year was partly offset byrepurchases amounting to RM4,196 million andrepayments totalling RM3,029 million. As at 31December 2002, the outstanding portfolio of loansand debts comprised mainly conventional housingloans (RM14,579 million or 56.0%), conventionalHP&L debts (RM10,513 million or 40.4%), IHF debtsand IHP debts (RM703 million or 2.7%) and industrialproperty loans (RM238 million or 0.9%).

Table 4 shows the composition of outstanding loansand debts in the books of the Company as at 31December 2002.

Table 3Purchases of Loans and Debts

2002 2001RM million % RM million %

Loan Type• Housing Loans 4,085 37.2 3,349 45.8

– Conventional-Preferred 1,645 15.0 381 5.2– Conventional-Standard 2,330 21.2 2,968 40.6– Islamic 110 1.0 – –

• Hire Purchase & Leasing Debts 6,907 62.8 3,940 53.8– Conventional 6,407 58.3 3,940 53.8 – Islamic 500 4.5 – –

• Industrial Property Loans – – 32 0.4

Sellers• Commercial Banks 2,839 25.9 3,125 42.7 • Finance Companies 7,853 71.4 4,066 55.5• Merchant Banks 65 0.6 130 1.8• Government – – – –• Corporations 235 2.1 – –

Option Type• On Fixed Rate 10,792 98.2 7,032 96.1• On Floating Rate 100 0.9 289 3.9• On Convertible Rate 100 0.9 – –

Total 10,992 100.0 7,321 100.0

64 CAGAMAS BERHAD 157931-A

Table 4Outstanding Loans and Debts Portfolio

As at As at31 December 2002 31 December 2001

Types RM million % RM million %

Housing Loans 14,823 56.9 15,452 69.4– Conventional 14,579 56.0 15,309 68.8– Islamic 244 0.9 143 0.6Hire Purchase & Leasing Debts 10,972 42.2 6,437 28.9– Conventional 10,513 40.4 6,437 28.9– Islamic 459 1.8 – –Industrial Property Loans 238 0.9 377 1.7

Total 26,033 100.0 22,266 100.0

Table 53-year Cagamas Fixed Rate for Purchase with Recourse

Preferred StandardRate Rate

Effective Date % p.a. % p.a.

10 December 2001 3.65 3.7012 January 2002 4.00 4.0517 January 2002 4.00 4.0526 January 2002 4.30 4.354 February 2002 4.00 4.0521 February 2002 3.90 3.9520 March 2002 3.90 3.951 April 2002 3.90 3.9521 May 2002 3.80 3.853 June 2002 3.70 3.7519 June 2002 3.60 3.653 July 2002 3.55 3.6018 July 2002 3.45 3.505 September 2002 3.45 3.501 October 2002 3.40 3.4516 October 2002 3.40 3.4520 November 2002 3.35 3.403 December 2002 3.30 3.35

Initiatives in 2002

The Company continued to broaden its customer baseto include new business opportunities with thedevelopment financial institutions (DFI) which havesince 15 February 2002 come under the directsupervision of Bank Negara Malaysia. During thesecond half of 2002, Board approval was obtained topurchase IHF debts from a DFI. The Company alsowidened its product base by introducing a scheme forthe purchase of credit card receivables in January2003 to meet the needs of the financial institutions.

Cagamas Rates

Through a large part of the year, Cagamas was ableto fund its operations at relatively stable and low bondyields. Overall, during the period January to

December 2002, there were 17 revisions to theCagamas Rate as compared with 12 revisions in2001.

Table 5 shows the revisions to the benchmark 3-yearCagamas Fixed Rate.

The 3-year Preferred Cagamas Rate was at its highestin January 2002 when it was raised by 30 basispoints to 4.30% p.a. in response to the firming ofbond yields in the secondary market. Since then, the3-year Preferred Cagamas Rate was steadily reducedto 3.30% p.a. by 3 December 2002, in tandem withthe reduction in yields of Cagamas debts securities.

Laporan Tahunan 2002 Annual Report 65

The Scheme

Cagamas introduced a scheme for the purchase ofcredit card receivables from financial institutions onwith recourse basis in January 2003.

Under this scheme, Cagamas will purchase credit cardreceivables from eligible accounts. Financialinstitutions that originate these accounts will retain fullcontrol and ownership of the accounts to enable thefinancial institutions to change the terms andconditions of the credit card agreement, whenevernecessary.

The credit card receivables are purchased on a fixedrate basis for price review periods ranging from threeto five years. The purchase price is based on the bookvalue of the receivables less finance charges and anyother charges incurred.

After the sale, the financial institutions will continue toadminister the receivables on behalf of Cagamas,including collection of outstanding receivables andfollow-up actions on delinquent accounts. Credit cardreceivables that become defective will be repurchasedand an equivalent amount of receivables from newaccounts will be offered for sale to Cagamas asreplacements for the repurchased receivables on aperiodic basis.

The financial institutions will remit to Cagamas on amonthly basis, the Cagamas instalment whichcomprises interest only until the price review date. Atthe end of the price review date, the financialinstitutions have the option to roll-over the contract fora further review period at the then prevailingCagamas rate or to repurchase the credit cardreceivables sold to Cagamas.

Special Features of the Scheme

• As credit card accounts are revolving in nature, thefinancial institutions are required to automaticallyadd new receivables from designated accounts ornewly designated accounts, as the case may be,on a periodic basis. This is to ensure that theprincipal outstanding of the credit card receivablessold to Cagamas be maintained at the purchasevalue throughout the tenure of the contract.

• The financial institutions will hold all payments,both principal and interest made by their customersin a collection account held in trust for Cagamas.

• The monthly principal collections from thedesignated accounts will not be remitted toCagamas but will be used to purchase newreceivables until the price review date.

Eligibility Criteria of Credit Card Accounts

Cagamas purchases receivables generated only fromeligible credit card accounts. To be eligible theaccounts should:

• be related to receivables in connection with theutilisation of credit or charge cards.

• be serviced for at least 12 months.• not be more than 60 days past the due date at the

time of sale.• not be closed, terminated or written off.• not be assigned, pledged or sold to any other

parties.• comply with all other criteria specified in the

Cagamas Credit Card Receivables Guide.

Regulatory Treatment

• The proceeds from the sale of credit cardreceivables are subject to the statutory reserverequirement.

• Unsecured debt securities issued by Cagamas tofund the purchase of credit card receivables areaccorded the following status:– Class 1 liquefiable asset status;– 10% risk weight under the Risk-We i g h t e d

Capital Requirement framework; and– Low risk asset status for insurance companies.

Benefits of the Scheme to the FinancialInstitutions

• Illiquid credit card receivables become liquidassets as the receivables can be sold to Cagamas.

• Low cost funds obtained from Cagamas can beused to lower the financial institutions’ weightedaverage cost of funds.

• The financial institutions may diversify their fundingsources.

• The sale of credit card receivables to Cagamas isexempted from ad valorem stamp duty, therebyproviding substantial savings.

Credit Card Receivables on With Recourse Basis

66 CAGAMAS BERHAD 157931-A

Chart 3Purchase of Credit Card Receivables on With Recourse Basis

CARDHOLDERS

1Pay monthly payment

3(i)Issues unsecureddebt securities

3(ii)Pay cash

2(iii)Enters into servicing

agreement

2(ii)Pay cash

2(i)Sell their credit

card receivables

RM million

Period

Purchase Date Purchase Period

RevolvingPeriod

Price Review Date

Purchase Value

4Enters into Trust Deed

INVESTORS

TRUSTEE

CAGAMASBERHAD

FINANCIALINSTITUTIONS

Laporan Tahunan 2002 Annual Report 67

In 2002, Cagamas issued the largest amountof fixed rate bonds to fund its conventionalpurchases and a record amount of SanadatMudharabah Cagamas to fund its purchasesof Islamic debts.

68 CAGAMAS BERHAD 157931-A

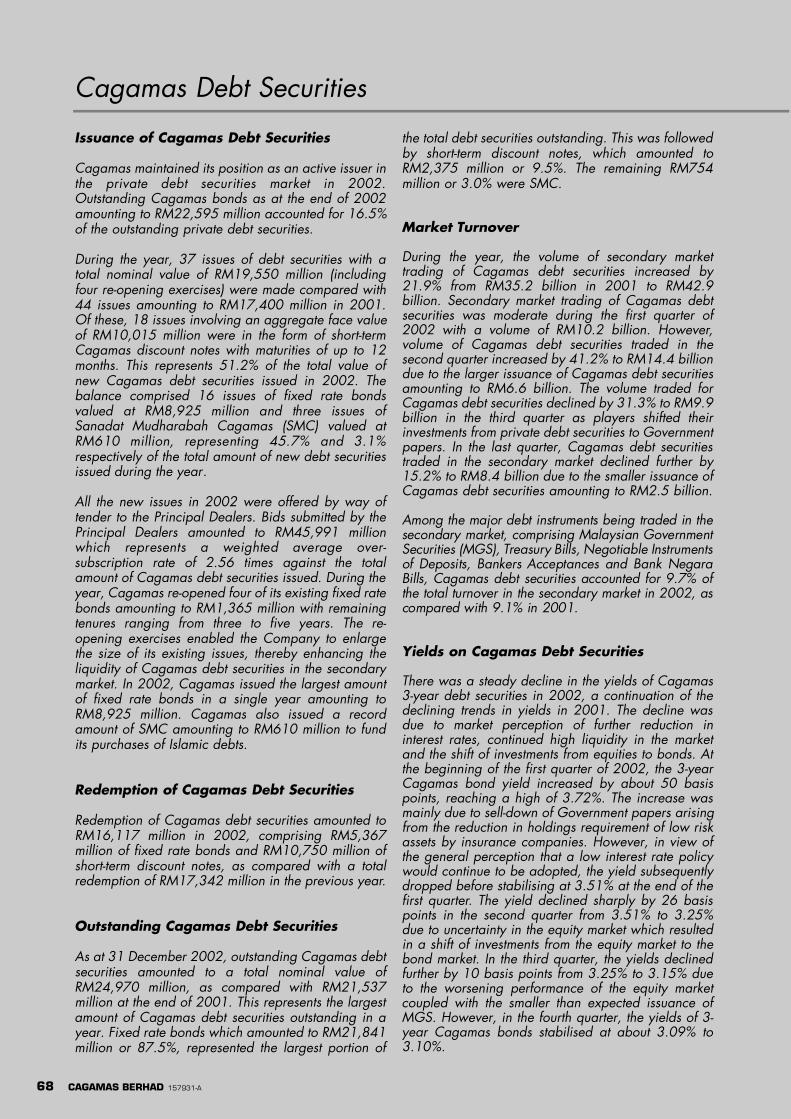

Issuance of Cagamas Debt Securities

Cagamas maintained its position as an active issuer inthe private debt securities market in 2002.Outstanding Cagamas bonds as at the end of 2002amounting to RM22,595 million accounted for 16.5%of the outstanding private debt securities.

During the year, 37 issues of debt securities with atotal nominal value of RM19,550 million (includingfour re-opening exercises) were made compared with44 issues amounting to RM17,400 million in 2001.Of these, 18 issues involving an aggregate face valueof RM10,015 million were in the form of short-termCagamas discount notes with maturities of up to 12months. This represents 51.2% of the total value ofnew Cagamas debt securities issued in 2002. Thebalance comprised 16 issues of fixed rate bondsvalued at RM8,925 million and three issues ofSanadat Mudharabah Cagamas (SMC) valued atRM610 million, representing 45.7% and 3.1%respectively of the total amount of new debt securitiesissued during the year.

All the new issues in 2002 were offered by way oftender to the Principal Dealers. Bids submitted by thePrincipal Dealers amounted to RM45,991 millionwhich represents a weighted average over-subscription rate of 2.56 times against the totalamount of Cagamas debt securities issued. During theyear, Cagamas re-opened four of its existing fixed ratebonds amounting to RM1,365 million with remainingtenures ranging from three to five years. The re-opening exercises enabled the Company to enlargethe size of its existing issues, thereby enhancing theliquidity of Cagamas debt securities in the secondarymarket. In 2002, Cagamas issued the largest amountof fixed rate bonds in a single year amounting toRM8,925 million. Cagamas also issued a recordamount of SMC amounting to RM610 million to fundits purchases of Islamic debts.

Redemption of Cagamas Debt Securities

Redemption of Cagamas debt securities amounted toRM16,117 million in 2002, comprising RM5,367million of fixed rate bonds and RM10,750 million ofshort-term discount notes, as compared with a totalredemption of RM17,342 million in the previous year.

Outstanding Cagamas Debt Securities

As at 31 December 2002, outstanding Cagamas debtsecurities amounted to a total nominal value ofRM24,970 million, as compared with RM21,537million at the end of 2001. This represents the largestamount of Cagamas debt securities outstanding in ayear. Fixed rate bonds which amounted to RM21,841million or 87.5%, represented the largest portion of

the total debt securities outstanding. This was followedby short-term discount notes, which amounted toRM2,375 million or 9.5%. The remaining RM754million or 3.0% were SMC.

Market Turnover

During the year, the volume of secondary markettrading of Cagamas debt securities increased by21.9% from RM35.2 billion in 2001 to RM42.9billion. Secondary market trading of Cagamas debtsecurities was moderate during the first quarter of2002 with a volume of RM10.2 billion. However,volume of Cagamas debt securities traded in thesecond quarter increased by 41.2% to RM14.4 billiondue to the larger issuance of Cagamas debt securitiesamounting to RM6.6 billion. The volume traded forCagamas debt securities declined by 31.3% to RM9.9billion in the third quarter as players shifted theirinvestments from private debt securities to Governmentpapers. In the last quarter, Cagamas debt securitiestraded in the secondary market declined further by15.2% to RM8.4 billion due to the smaller issuance ofCagamas debt securities amounting to RM2.5 billion.

Among the major debt instruments being traded in thesecondary market, comprising Malaysian GovernmentSecurities (MGS), Treasury Bills, Negotiable Instrumentsof Deposits, Bankers Acceptances and Bank NegaraBills, Cagamas debt securities accounted for 9.7% ofthe total turnover in the secondary market in 2002, ascompared with 9.1% in 2001.

Yields on Cagamas Debt Securities

There was a steady decline in the yields of Cagamas3-year debt securities in 2002, a continuation of thedeclining trends in yields in 2001. The decline wasdue to market perception of further reduction ininterest rates, continued high liquidity in the marketand the shift of investments from equities to bonds. Atthe beginning of the first quarter of 2002, the 3-yearCagamas bond yield increased by about 50 basispoints, reaching a high of 3.72%. The increase wasmainly due to sell-down of Government papers arisingfrom the reduction in holdings requirement of low riskassets by insurance companies. However, in view ofthe general perception that a low interest rate policywould continue to be adopted, the yield subsequentlydropped before stabilising at 3.51% at the end of thefirst quarter. The yield declined sharply by 26 basispoints in the second quarter from 3.51% to 3.25%due to uncertainty in the equity market which resultedin a shift of investments from the equity market to thebond market. In the third quarter, the yields declinedfurther by 10 basis points from 3.25% to 3.15% dueto the worsening performance of the equity marketcoupled with the smaller than expected issuance ofMGS. However, in the fourth quarter, the yields of 3-year Cagamas bonds stabilised at about 3.09% to3.10%.

Cagamas Debt Securities

Differential MGS Cagamas Bonds

2001 2002

Jan Feb Mar Apr Jun Jul Aug Sep Oct Nov DecMay Jan Feb Mar Apr Jun Jul Aug Sep Oct Nov DecMay

Laporan Tahunan 2002 Annual Report 69

The yield differential between Cagamas bonds andMGS in the secondary market during the year asshown in Chart 4, was between 5 to 22 basis points.In the first quarter of the year, the yield differential wasrelatively volatile as compared with the yielddifferential in 2001, reaching a high of 22 basispoints before settling at 17 basis points. This was dueto uncertainty on the impact of a reduction in theholdings requirement of low risk assets by insurancecompanies from 20.0% to 10.0%. The differential wasbetween 11 to 17 basis points as a result of thelacklustre equity market in the second quarter. In thethird quarter, the differential narrowed to 7 basispoints due to an increase in demand for high qualityliquid asset papers such as Cagamas debt securitiesfollowing the lower than expected volume of issuanceof MGS during the same period. The spread betweenCagamas bonds and MGS further narrowed to 5basis points in the fourth quarter due to the lack ofissuance of MGS during the same period.

Holders of Cagamas Debt Securities

Holders of Cagamas debt securities as at end ofDecember 2002 are shown in Table 6.

Holdings of Cagamas debt securities by bankinginstitutions as at 31 December 2002 increased to50.8% of the total holdings from 50.3% as at the endof 2001. Conversely, the holdings of Cagamas debtsecurities by the non-banking institutions declined from49.7% in 2001 to 49.2% as at 31 December 2002.However, there was an increase of holdings bypension and provident funds, whose holdings ofCagamas papers increased from 25.3% of the totalholdings as at the end of December 2001 to 35.7%as at the end of December 2002. This reflects theincrease in demand for high quality investment papersby the pension and provident funds.

General Outlook

Cagamas continued to receive strong demand for itsprimary market issues in 2002 as evidenced by theweighted average over-subscription rates of 1.94 and3.33 times for Cagamas notes and bonds respectively.The yield differential between Cagamas bonds andMGS which narrowed substantially during the yearhas enabled the Company to continue to play its rolein providing low cost funds to the financial institutions.

Chart 4Yield Differential between 3-year Cagamas Bonds and Malaysian Government Securities

2002 2001Holders RM million % RM million %

Banking Institutions 12,697 50.8 10,828 50.3

Insurance Companies 2,172 8.7 2,596 12.1

Pension and Provident Funds 8,902 35.7 5,457 25.3

Other Investors 1,199 4.8 2,656 12.3

Total 24,970 100.0 21,537 100.0

Table 6Distribution of Cagamas Debt Securities Holders

30 –

20 –

10 –

0 –

– 4.00

– 3.50

– 3.00

– 2.50

– 2.00

70 CAGAMAS BERHAD 157931-A

Introduction

Cagamas implemented a Business Continuity Plan(BCP) in 2002 to minimise the impact from potentialinternal and external disaster disruptions to theCompany’s operations. In this respect, the Companyhas formulated a comprehensive plan that will coverall actions to be taken before, during and after adisaster. The Company will achieve this through acombination of efforts, which are:

• Advance preparation and preventive controls;• Early detection and impact minimisation

procedures;• Effective organisation and communication;• Operational business recovery procedures and

minimisation of operational downtime;• Specific operational Contingency Procedures and

Recovery Actions (CPRA) for key processes;• Mobilisation of human and information resources;

and• Working towards restoring full processing

capabilities as soon as possible.

Scope of the BCP

This BCP which incorporates the CPRA has beendesigned to manage Cagamas’ risks based on the

Business Risk Assessment for each department andCagamas as a whole. These include the followingkey areas:

• Key business processes;• IT-related systems and infrastructure used; and• Facilities, utilities and external party

dependencies.

Disaster Situation

The Company may declare a disaster under thefollowing circumstances:

• Prolonged interruption of power supply atCagamas’ premises;

• Prolonged breakdown of communication to hostsystem;

• Hardware failure or other equipment becominginaccessible; and

• Fire, flood and other natural disasters toCagamas’ premises.

Business Recovery Teams

In the event of a disaster, the various BusinessRecovery Teams will be activated. The OrganisationChart for Business Recovery is set out below:

Business Recovery Organisation

Business Continuity Plan

EmergencyManagement

Team

BusinessRecovery

Coordinators

CagamasStaff

BusinessRecovery

Team

A d m i n i s t r a t i v eS u p p o rt Te a m

Laporan Tahunan 2002 Annual Report 71

The various teams that will be activated to expeditebusiness recovery are as follows:

(a) Emergency Management Team (EMT)A disaster can only be authorised and declaredby the EMT and its primary tasks are:

(i) to review the extent of the impact to thebusiness arising from the damage to theCompany’s operations including computerfacilities;

(ii) to issue directives to activate the recoverysite; and

(iii) to provide a channel for key decisions duringthe recovery operations.

The EMT is only activated when the situationrenders an inoperative status or total destructionin the primary business premises.

(b) Business Recovery Coordinators (BRC)The BRC are responsible for executing,coordinating and monitoring the BCP when adisaster is declared by the EMT.

(c) Business Recovery Team (BRT)The BRT is responsible for carrying out the variousCPRA established by the Company.

(d) Administrative Support Team (AST)The A S T is responsible for arrangingtransportation and accommodation (if necessary),dealings with financial matters, security, publicrelations, insurance and other corporate matters.

(e) Cagamas StaffAll Cagamas staff in general are responsible toassist in the execution of the BCP.

Business Recovery Site

The Business Recovery Site will be activated upondeclaration of a disaster for the specific purpose ofmanaging the BCP for Cagamas. The recovery site willalso serve as the Command Centre for business andrecovery operations. Besides business work area, theCompany will be able to recover the use of keycomputer systems for operations, treasury andpayments.

Other Areas of BCP

In addition to the above, the BCP also covers thefollowing areas:

• Immediate activities to be performed during adisaster such as evacuation procedures,declaration of disaster/full business shutdown,alert/activate recovery centre and alert/activatedisaster recovery teams;

• Setting up a working environment at the recoverycentre;

• Retrieval of files and documents;• Resumption of operations;• Migration to Cagamas’ premises; and• Return to normal operations.

Testing and Updating of BCP

All the above-mentioned critical systems recoveryprocedures will be tested on a periodic basis. The BRCare responsible for updating the BCP on a regularbasis to ensure that the BCP remains relevant. The BCPwill continuously be updated to be in line with theimplementation of the Company’s Information andCommunications Technology Master Plan and businessoperations.

72 CAGAMAS BERHAD 157931-A

The Board of Directors (the Board) of Cagamas iscommitted to ensuring that the Company practises thehighest standards of corporate governance so that itsa ffairs are conducted with integrity andprofessionalism with the objectives of safeguardingshareholders’ value and the financial performance ofthe Company.

The Board is pleased to report that the Company hasapplied the principles and best practices of theMalaysian Code on Corporate Governance (theCode), as set out below.

1. The Board of Directors

1.1 CompositionAs at 31 December 2002, the Boardcomprised 11 Non-Executive Directors,which consisted of senior officers from BankNegara Malaysia (BNM) and ChiefExecutives or Directors of selected financialinstitutions nominated by The Association ofBanks in Malaysia, the Association ofFinance Companies of Malaysia and theAssociation of Merchant Banks in Malaysia(collectively referred to as the Associations).

Based on the Code’s broad description,C a g a m a s ’ Directors are consideredindependent as they are independent ofmanagement and do not participate in theday-to-day running of the Company’sbusiness. The Directors do not hold shares intheir personal capacity and are notinfluenced by any significant shareholder ofthe Company. There is no one group ofDirectors or any individual Director todominate the Board’s discussions or itsdecision-making process. The Directors bringan objective and independent view to theBoard’s deliberations.

The Board is effective in leading andcontrolling the Company as the Directorshave varied and in-depth experience in thefinancial sector which the Company isinvolved in. The Directors bring to the Boarda diverse set of skills and knowledge inbanking, accounting, economics, informationtechnology and general management.Cagamas was set up to promote the

secondary mortgage market and to broadenand deepen the domestic debt securitiesmarket. A combination of nominees fromBNM and financial institutions ensures thatthe Company’s national and socialobjectives are met and at the same time, theCompany remains profit-motivated to gainmarket credibility amongst its investors andshareholders.

The Board has developed positiondescriptions for the Board, the BoardCommittees and the Chief Executive Officerincluding the delegation of authority andassignment of limits on the scope andresponsibilities of the Board Committees andthe Chief Executive Officer. The Chairmanheads the Board and during meetings, leadsthe discussions on overall strategies, policiesand the conduct of the Company’s businesswhile the Chief Executive Officer isresponsible for the implementation of thesestrategies and policies as well as the day-to-day running of the business.

1.2 Duties and ResponsibilitiesThe Board oversees the conduct andperformance of the Company’s business byreviewing and approving the Company’sannual strategic business plan as well as theannual budget. Updates on the keyoperations of the Company are provided tothe Board for review at every Board meeting.

The Board has the overall responsibility toensure that there is proper oversight of themanagement of risks in the Company. Duringthe year, the Board has approved a RiskManagement Framework which sets out theCompany’s overall approach to managingrisks, including the identification of relevantrisks, the risk methodology used by theCompany and responsibilities and reportingstructures of parties involved in themanagement of risks.

The Board, based on the recommendationsof the Board Staff Compensation andOrganisation Committee, also approves theappointment and replacement of SeniorManagement staff and reviews theirperformance and compensation.

Statement on Corporate Governance

Laporan Tahunan 2002 Annual Report 73

In carrying out its duties and responsibilities,the Board is committed to transparency andseeks to avoid any conflict of interestsituations arising from transactions that mayraise questions as to the integrity of itsdecisions.

2. Board Meetings

During the financial year ended 31 December2002, the Board met four times to deliberate ona wide range of matters, including theCompany’s business performance, business plansand other strategic issues that affect theC o m p a n y ’s business. Details of Directors’attendance at Board meetings held during theyear 2002 are set out on page 5 of this AnnualReport.

The Board meetings are structured with a pre-setagenda. Board papers providing updates onoperational, financial and corporatedevelopments are sent to the Directors prior toeach meeting to provide them adequate time tostudy the matters to be discussed at the meeting.

In furtherance of their duties, the Directors, in theirindividual capacity and as members of thevarious Board Committees, are empowered toseek independent professional advice at theC o m p a n y ’s expense, as and when deemednecessary.

All Directors have direct access to the advice ofSenior Management and the services of theCompany Secretary, who is responsible forensuring that Board procedures are followed andthat all applicable rules and regulations arecomplied with.

3. Appointment and Re-election of Directors

The Directors are nominated by BNM and theAssociations to be members of the Board. Thesenominations are then presented to the Board forits approval. In view of the independent decisionsof BNM and the Associations and the adequacyof the present procedure, the Board is of the viewthat a nomination committee to nominateDirectors to the Board is not necessary.

A separate annual assessment of Directors on theBoard is not conducted by Cagamas since theDirectors representing the Associations are eitherChief Executives or Directors of financialinstitutions and are subject to supervision andperiodic review by BNM.

In accordance with the Company’s Articles ofAssociation, at least one-third of the Directorsshall retire from office at each Annual GeneralMeeting of the Company and they can offerthemselves for re-election. The Articles also statethat Directors appointed by the Board during aparticular year are subject to election by theshareholders at the next Annual General Meetingheld following their appointments.

4. Directors’ Training

Most of the Directors are Directors of public-listedcompanies and have attended the Kuala LumpurStock Exchange (KLSE) accredited trainingprogramme as required under the KLSE’sguidelines on training for Directors.Notwithstanding this, the Directors are regularlyupdated on the relevant new laws and regulationsat Board meetings.

5. Directors’ Remuneration

The Board, as a whole, determines theremuneration of each Director based on therecommendation of the Board FinanceCommittee. The level of the Directors’remuneration is determined based on their roleassumed in the Board. The Chairman abstainsduring discussions on the Chairman’s fee.

During the year 2002, a review of the Directors’fees was carried out and subject to thes h a r e h o l d e r s ’ approval, the Directors’ f e e sproposed are RM7,000 per annum for eachDirector and RM10,000 per annum for theChairman. In addition, the Directors are paid ameeting allowance of RM500 for each meetingthat they attend. The aggregate remunerationpayable to the Directors is RM125,500,comprising Directors’ fees of RM90,000 andmeeting allowances of RM35,500.

74 CAGAMAS BERHAD 157931-A

6. Board Committees

In discharging its duties, the Board is assisted byfour Committees, which operate within specifiedterms of reference. The Committees comprise theBoard Executive Committee, Board FinanceCommittee, Board Audit Committee and BoardS t a ff Compensation and OrganisationCommittee. The Board Executive Committee hasthe authority to decide and act on behalf of theBoard on all matters in between Board meetings.The other Committees are assigned to examineparticular issues and are empowered by theBoard to either approve or report back to theBoard with their recommendations. The finaldecision on all matters, however, rests with theentire Board.

7. Investor Relations and Share h o l d e r s ’Communication

The Board recognises the importance of effectiveand timely communication with all itsshareholders and investors. The Company’sstrategies, plans, financial information and newproducts are communicated to the shareholdersand investors through the Annual Report sent tothem. For Cagamas, the principal forum fordialogue with shareholders continues to be at theAnnual General Meeting. At this Meeting, theChairman highlights the performance of theCompany and provides the shareholders everyopportunity to raise questions and seekclarifications on the business and performance ofthe Company.

As all the Company’s shareholders arerepresented through the Associations whichnominate Directors to the Board, the Board is ofthe view that the identification of a seniorindependent non-executive Director is notnecessary since shareholders’ concerns can beraised through the Associations.

The Company also publishes half-yearly andyearly financial results and disseminates pressreleases on its debt securities issuance activities inmajor newspapers and wired services. Inaddition, the Company also maintains a websiteat www.cagamas.com.my which providescomprehensive up-to-date information on theCompany’s products, rates and operations.

8. Accountability and Audit

8.1 Financial ReportingThe Board aims to present a balanced andunderstandable assessment of theCompany’s financial position and prospectsin its annual financial statements toshareholders and investors.

The Companies Act, 1965, requires theDirectors to prepare financial statements foreach financial year, which give a true andfair view of the state of affairs of theCompany. Following discussions with theExternal Auditors, the Directors consider thatin preparing the financial statements, theCompany has used appropriate accountingpolicies which are consistently applied andsupported by reasonable judgements andestimates and that all accounting standardswhich they consider applicable have beenfollowed.

8.2 Internal ControlThe Company’s Statement on Internal Controlis set out on page 78 of this Annual Report.

8.3 Relationship with AuditorsThe Report on the role of the Board AuditCommittee in relation to the Internal andExternal Auditors is described on pages 75to 77 of this Annual Report.

Through the Board Audit Committee, theCompany has established transparent andprofessional relationship with the Company’sInternal and External Auditors. T h eCompany’s External Auditors attended twomeetings during the year to report on theaudits for financial year ended 31 December2001 and half-year ended 30 June 2002and to present the Audit Plan for 2002.

Auditors’ remuneration is as shown on page145 of this Annual Report.

Laporan Tahunan 2002 Annual Report 75

1. Members

The Board Audit Committee (the Committee)comprises:

• Dato’ Tan Teong Hean (Chairman)• Encik Mohamed Azmi Mahmood• Encik Michael Andrew Hague

Based on the Malaysian Code on CorporateGovernance’s broad description, all the membersare considered independent Non-ExecutiveDirectors as they do not participate in the day-to-day running of the Company’s business and areindependent of Management. The Directors donot hold shares in their personal capacity and arenot influenced by any significant shareholder ofthe Company. There is no one group of Directorsor any individual Director to dominate theCommittee’s discussions or decision-making. TheDirectors bring an independent view to theCommittee’s deliberations.

2. Terms of Reference

2.1 Authority(a) The Committee shall have unlimited

access to all information and documentsrelevant to its activities, to the Internaland External Auditors, and toManagement of the Company.

(b) The Committee is authorised by theBoard to obtain outside legal or otherindependent professional advice and tosecure the attendance of outsiders withrelevant experience and expertise toattend meetings whenever it deemsnecessary.

(c) The Committee is authorised by theBoard to investigate any activity withinits purview and members of theCommittee shall direct all employees toco-operate as they may deem necessary.

2.2 Size and Composition(a) The Committee shall be appointed by

the Board from amongst the Non-Executive Directors and shall comprise aminimum of three members, a majorityof whom shall be independent Directors.

(b) If for any reason the number of membersis reduced to below three, the Boardmust fill the vacancies within threemonths.

(c) The members of the Committee shallelect a Chairman from amongst theirmembers who shall be an independentDirector.

(d) At least one member of the Committee:

(i) must be a member of the MalaysianInstitute of Accountants (MIA); or

(ii) if he is not a member of the MIA, hemust have at least 3 years’ workingexperience and:• he must have passed the

examinations specified in Part Iof the 1st Schedule of theAccountants Act, 1967; or

• he must be a member of one ofthe associations of accountantsspecified in Part II of the 1stSchedule of the AccountantsAct, 1967.

(e) No member of the Committee shall havea relationship, which in the opinion ofthe Board will interfere with the exerciseof independent judgement in carryingout the functions of the Committee.

2.3 Meetings(a) Meetings will be held once a quarter or

at a frequency to be decided by theChairman and the Committee may inviteany person to be in attendance to assistin its deliberations.

(b) The Chief Executive Officer, the ChiefOperating Off i c e r, the CompanySecretary and the Head of Internal Auditshall normally attend the meetings. Atleast once a year, the Committee shallmeet with the External Auditors.

(c) The quorum shall be two members.

(d) The Secretary to the Committee shall bethe Head of Internal Audit.

Report of the Board Audit Committee

76 CAGAMAS BERHAD 157931-A

2.4 Duties and Responsibilities(a) Review the half-yearly and annual

financial statements of the Companyprior to submission to the Board, toensure compliance with disclosurerequirements and the adjustmentssuggested by the External A u d i t o r s .These include:

(i) Review of the auditors’ report andqualifications (if any) which mustbe properly discussed and actedupon to remove the auditors’concerns in future audits;

(ii) Significant changes andadjustments in the presentation offinancial statements;

(iii) Major changes in accountingpolicies and principles;

(iv) Compliance with accountingstandards and other legalrequirements;

(v) Material fluctuations in statementof balances;

(vi) Interim financial reports andpreliminary announcements;

(vii) Significant variations in auditscope; and

(viii) Significant commitments orcontingent liabilities.

(b) Review the scope and results of InternalAudit procedures including:

(i) Compliance with internal auditingstandards, the Company’s internalcontrols, policies and other legalrequirements;

(ii) Adequacy of established policiesand procedures and internalcontrols;

(iii) Co-ordination between the Internaland External Auditors;

(iv) Exercising independence andprofessionalism in carrying outInternal Audit work;

(v) Restrictions placed on InternalAudit by Management;

(vi) Reporting of results;(vii) Recommending changes in

accounting policies to the Board;and

(viii) Recommending and ensuring theimplementation of appropriateremedial and corrective actionsregularly.

(c) Responsible for the establishment of theInternal Audit functions which include:

(i) Approval of the Internal A u d i tCharter;

(ii) Approval of the Internal Audit Plan;(iii) Reviewing the performance of the

Head of Internal Audit, inconsultation with Management;

(iv) Approval of the appointment ortermination of the Head of InternalAudit;

(v) Notification of resignation ofInternal Audit staff and to provideopportunity for such staff to submitreasons for resigning;

(vi) Reviewing the adequacy of thescope and functions of InternalAudit;

(vii) Ensuring that the Internal A u d i tfunctions have appropriatestanding within the Company;

(viii) Alignment of goals and objectivesof the Internal Audit functions withthe Company’s overall goals;

(ix) Placing Internal Audit under thedirect authority and supervision ofthe Committee; and

(x) Reviewing the assistance given bythe Company’s officers to theAuditors.

(d) Recommend to the Board theappointment of External Auditors, theaudit fee and any question ofresignation and dismissal of the ExternalAuditors.

(e) Discuss matters arising from the previousyear’s audit, review with the ExternalAuditors the scope of their current year’saudit plan, their evaluation of theaccounts and internal control systems,including their findings andrecommended actions.

(f) Review changes in statutoryrequirements and any significant auditproblems that can be foreseen as aresult of previous year’s experience orbecause of new developments.

(g) Evaluate and review the role of Internaland External Auditors from time to time.

(h) Review any significant related partytransactions or conflict of interestsituation that may arise within theCompany.

Laporan Tahunan 2002 Annual Report 77

(i) Review any significant transactions,which are not a normal part of theCompany’s business.

(j) Perform any other functions as may bedelegated by the Board from time totime.

3. Meetings

The Committee held four meetings during thefinancial year ended 31 December 2002 with theChief Executive Officer, the Chief OperatingOfficer, the Company Secretary and the Head ofInternal Audit in attendance. The attendance ofthe members was as follows:

Member Attendance

• Dato’ Tan Teong Hean 4/4• Encik Mohamed Azmi Mahmood 2/4• Encik Michael Andrew Hague 2/2

(appointed on 24.7.2002) • Puan Yvonne Chia 1/1

(resigned on 23.3.2002)• Encik Lee Kam Chuen 4/4

(resigned on 16.12.2002)• Dato’ Mohd Razif Abdul Kadir 3/4

(resigned on 23.1.2003)

The Company’s External Auditors attended twomeetings during the year to report on the auditsfor financial year ended 31 December 2001 andhalf-year ended 30 June 2002 and to present theAudit Plan for 2002.

4. Summary of Activities

During the financial year, the Committee carriedout its duties, as set out in the terms of reference.Summary of its main activities is as follows:

(a) Reviewed and approved the Internal AuditPlan for 2003;

(b) Reviewed Internal Audit methodology inassessing and rating risks of the auditableareas with emphasis on critical risk areas;

(c) Reviewed the results of the internal auditprocedures, i.e. the Internal Auditor’s auditfindings and recommendations andM a n a g e m e n t ’s responses to the auditfindings and recommendations;

(d) Monitored the progress of the Internal AuditPlan and the implementation of the auditrecommendations in order to ensure thatappropriate actions have been taken or arebeing taken on the audit recommendations;

(e) Reviewed the performance of Head ofInternal Audit, in consultation withManagement;

(f) Reviewed the scope of the audit by theExternal Auditors and Audit Plan for 2002;

(g) Reviewed the results of the half-yearly andyear-end audits by the External Auditors anddiscussed the findings and other concerns ofthe External Auditors;

(h) Reviewed the audited half-yearly and theyear-end financial statements and ensuredcompliance with disclosure requirements ofrelevant authorities; and

(i) Reviewed the audit programmes (for theExternal Auditors) on loans and debts sold toCagamas.

5. Internal Audit Function

The Company has a well-established InternalAudit Department, which reports to the Committeeand assists the Board in discharging itsresponsibilities to ensure that the Companymanages its risks and maintains a sound andeffective system of internal control.

The Internal Audit Department undertakes theinternal audit functions of the Company inaccordance with the approved Audit Charter andthe annual Audit Plan approved by theCommittee.

The Audit Plan was derived from the results of thesystematic risk assessment process, whereby theCompany’s risks are identified, prioritised andlinked to the key processes and auditable areas.

Overall, the audits conducted during the financialyear emphasised on the review of the adequacyof the Company’s system of internal controls, riskmanagement, financial reporting and compliancewith laws and regulations. The internal auditreports are presented to the Committee for itsconsideration and to the Board for its information.

78 CAGAMAS BERHAD 157931-A

Statement on Internal Control

The Board of Directors has overall responsibility forensuring that the Company maintains a sound andeffective system of internal control and for reviewingits adequacy and integrity. The system on internalcontrol cover, inter alia, risk management, financial,organisational, operational and compliance controls.The Board however, recognises that such a systemcannot eliminate the risk of failure to achieve businessobjectives, rather, it is designed to manage andcontrol the risks to acceptable levels. Accordingly, itcan only provide reasonable, but not absoluteassurance, against material misstatement or loss.

The Directors and Senior Management of theCompany are committed to maintaining a culture ofcorporate risk awareness in all areas of operations.During the year, a Risk Management Unit was set upto formulate, review and implement sound riskmanagement policies, strategies and procedureswithin the Company. In September 2002, the Boardof Directors approved the Risk ManagementFramework for the Company, which amongst others,defines the sources of key business risks, outlines theroles and responsibilities of the Board of Directors andthe key committees in managing specific areas of risksand sets out the Company’s overall approach tomanaging risks. Further details on risk managementare set out in pages 79 to 81 of this Annual Report.

The Internal Audit Department provides assurance tothe Board by conducting an independent review onthe adequacy, effectiveness and integrity of theCompany’s system of internal control. It adopts a risk-based approach in accordance with the annual auditplan approved by the Board Audit Committee. Theresults of the audits are submitted to the Board AuditCommittee, which meets four times a year. The auditplan and audit reports are also submitted to the Boardto keep the Board informed of any weaknesses in theC o m p a n y ’s internal control system. Whereweaknesses are identified, new procedures have beenor are being put in place to strengthen controls. Duringthe financial year, none of the weaknesses highlightedhave resulted in any material losses, contingencies oruncertainties that would require disclosure in theCompany’s Annual Report.

Other key elements of the Company’s system ofinternal control are:

• Clearly defined lines of responsibility anddelegation of authority to Committees of theBoard, Management and staff of the Company;

• Clearly documented internal policies andprocedure manuals such as Tr e a s u r yManagement Policy. These manuals are reviewedat least once every quarter;

• An annual business plan and detailed budgetwhich are approved by the Board. The Companyalso monitors monthly actual results against thebudget, with major variances being followed up;

• Regular reporting to the Board. Reports on theCompany’s financial position, status of loans anddebts purchased, bonds and notes issued andinterest rate swap transactions are provided to theBoard at least once a quarter. Where necessary,other issues such as legal, accounting or strategicmatters will also be reported to the Board; and

• Regular and comprehensive information isprovided to Management, covering financial andoperational reports, at least once a month.

Laporan Tahunan 2002 Annual Report 79

Risk Management

The volatile and rapidly changing environment hasmade it imperative for Cagamas to review its pastpractices and implement sound risk managementstrategies not only to protect the Company’sprofitability but also to sharpen its competitive edge toremain resilient.

Towards this end, in September 2002, the Board ofDirectors had formalised the Company’s RiskManagement Framework which sets out theC o m p a n y ’s overall approach to managing risks,including the identification of relevant risks, the riskmanagement methodology used by the Company andresponsibilities and reporting structures of partiesinvolved in the management of risks.

The Company’s primary objective of risk managementis to effectively manage and link risks with reward inorder to maximise the Company’s shareholders’ valueas well as to ensure that the Company is able tosustain its performance.

To achieve its objective, the Company’s plan is todevelop and implement an enterprise-wide riskmanagement strategy. This strategy entails:

• aligning business strategy with the corporate riskmanagement policy;

• establishing a risk assessment and audit plan;• developing risk models, systems and data

management capabilities to support themanagement of risks on a consistent basis;

• inculcating a corporate risk awareness culture;and

• improving risk transparency to stakeholders.

Risks Faced by the Company

The Company faces the following risks:

• Market risk;• Liquidity risk; • Credit risk; and• Operational risk.

Market RiskMarket risk is the exposure of the Company’s financialposition to adverse movements in market interest ratesor prices. The principal risk faced by the Company inits operations is mainly due to interest rate movements.The types of market risks related to the Company’soperations are pipeline risk, funding mismatch risk,reinvestment risk, basis risk, price risk andovercrowding risk.

To facilitate the control of these risks, the Companymonitors closely the secondary market trading ofbonds and prevailing market expectations on interestrates and bond yields. The Company has the ability toissue debt securities within the shortest possible time.To minimise the impact of repurchases on its cash flow,the Company has also incorporated compulsoryreplacement of all repurchased loans and debts, withthe exception of housing loans, where it remainsoptional.