Ch_9_Stocks_(pdf)

28

1 1 Bus 170 Debbie Abbott Stocks and Their Valuation Chapter 9 Features of common stock Determining common stock values Preferred stock © Photographer: Scott Rothstein

-

Upload

annie-nguyen -

Category

Documents

-

view

213 -

download

0

description

hgbilkj

Transcript of Ch_9_Stocks_(pdf)

1 1

Bus 170

Debbie Abbott

Stocks and Their Valuation

Chapter 9 Features of common stock Determining common stock values Preferred stock

© Photographer: Scott Rothstein

2

Bus 170

2 Debbie Abbott

Common Stock & Intrinsic Value

Represents ownership

– Ownership implies control

– Stockholders elect directors

– Directors hire management

Management’s goal

– Maximize the stock price

Outside investors, corporate insiders, and analysts use a variety of approaches to estimate a stock’s intrinsic value (P0)

In equilibrium we assume that a stock’s price equals its intrinsic value.

– Outsiders estimate intrinsic value to help determine which stocks are attractive to buy and/or sell.

– Stocks with a price below (above) its intrinsic value are undervalued (overvalued).

3

Bus 170

3 Debbie Abbott

Determinants of Intrinsic Value and Stock Prices Graphic shows that managerial actions, economic environment and political climate influence stock’s intrinsic value and its perceived or market price. When the Market is in equilibrium, Intrinsic value = Stock price

4

Bus 170

4 Debbie Abbott

Ways to Estimate the Intrinsic Value of Stock

Dividend growth model

Corporate value model

5

Bus 170

5 Debbie Abbott

Dividend Growth Model

Key Concept: Value of a stock is the present value of the

future dividends expected to be generated by the stock

∞∞

+++

++

++

+=

)r(1D

... )r(1

D

)r(1D

)r(1

D P

s3

s

32

s

21

s

10

^

6

Bus 170

6 Debbie Abbott

Future Dividends and Their Present Values Graph depicts dividends with a constant growth of g increase every year in a step function. However, the present value of future dividends gets smaller every year. If the value of a stock is the dividends that investors receive over time, then the value of a stock is the sum of PV of its dividends over time.

t0t ) g 1 ( DD +=

tt

t )r 1 (D

PVD+

=

t0 PVDP ∑=

$

0.25

Years (t) 0

7

Bus 170

7 Debbie Abbott

Constant Growth Stock

A stock whose dividends are expected to grow forever at a constant rate, g.

D1 = D0 (1+g)1

D2 = D0 (1+g)2

Dt = D0 (1+g)t

The value of the stock is the sum of the PV of its dividends

If g is constant, the dividend growth formula converges to: P0 =D1 / (rs –g)

g -rD

g -rg)(1D

Ps

1

s

00

^=

+=

∞∞

+++

++

++

+=

)r(1D

... )r(1

D

)r(1D

)r(1

D P

s3

s

32

s

21

s

10

^

8

Bus 170

8 Debbie Abbott

What Happens If g > rs?

If g > rs, the constant growth formula leads to a negative stock price, which does not make sense

The constant growth model can only be used if: –rs > g –g is expected to be constant forever

9

Bus 170

9 Debbie Abbott

To Use Dividend Growth Model, First Need to Find rs

Example: rRF = 7%, rM = 12%, and b = 1.2, what is the required rate of return on the firm’s stock?

Use the CAPM to calculate the required rate of return (rs):

rs = rRF + (rM – rRF)b = 7% + (12% - 7%)1.2 = 13%

10

Bus 170

10 Debbie Abbott

What Is the Stock’s Intrinsic Value?

Assume the company’s last dividend per share was $2.00 and the company has a constant growth rate of 6%

Determine the value per share, using the constant growth model:

P0 = D1 / (rs –g) = $2.12 / (.13 - .06) = $2.12 / .07 = $30.29

11

Bus 170

11 Debbie Abbott

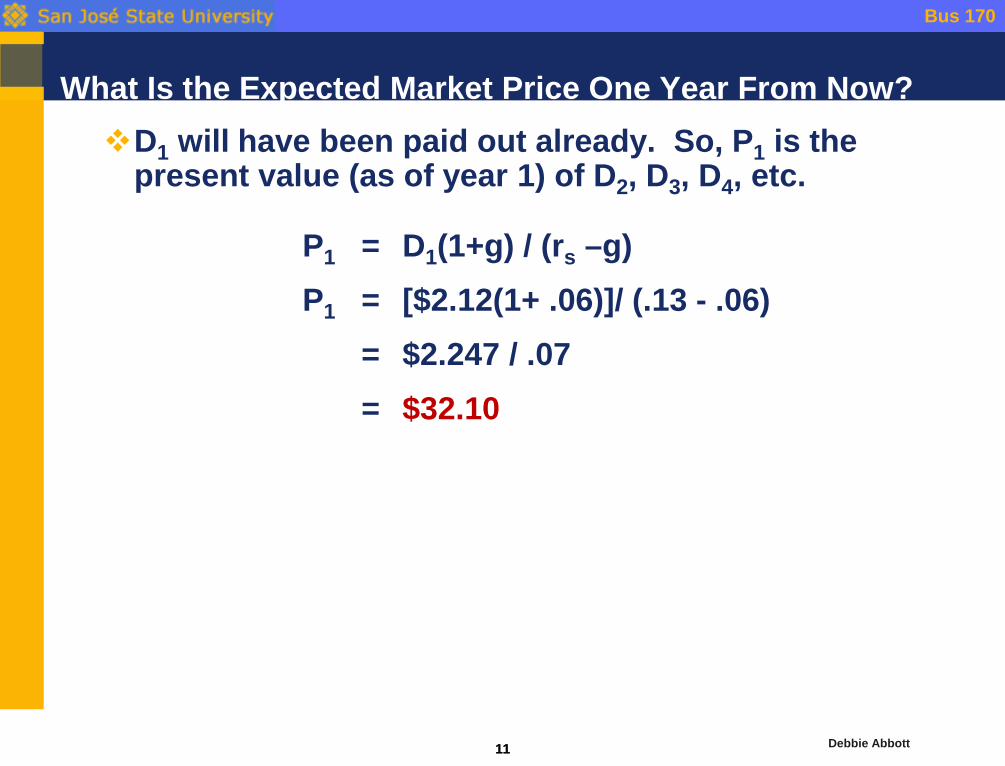

What Is the Expected Market Price One Year From Now? D1 will have been paid out already. So, P1 is the

present value (as of year 1) of D2, D3, D4, etc.

P1 = D1(1+g) / (rs –g) P1 = [$2.12(1+ .06)]/ (.13 - .06) = $2.247 / .07 = $32.10

12

Bus 170

12 Debbie Abbott

Expected Market Price One Year From Now Continued Could also find expected P1 as:

PN = P0 (1+g)N = $30.29 (1+ .06)1

= $32.10

Or by using financial calculator: N = 1 I = 6

PV = -30.29 PMT = 0 FV = ? = 32.10

13

Bus 170

13 Debbie Abbott

First Year Expected Dividend Yield, Capital Gains Yield, and Total Return

Dividend Yield DY = D1 / P0 = $2.12 / $30.29 = 7.0%

Capital Gains Yield CGY = (P1 – P0) / P0 = ($32.10 - $30.29) / $30.29 = 6.0%

Total Return (rS) rS = Dividend Yield + Capital Gains Yield = 7.0% + 6.0% = 13.0%

14

Bus 170

14 Debbie Abbott

What Would the Expected Price Today Be, if g = 0?

The dividend stream would be a perpetuity, with a constant dividend of $2.00

P0 = D0(1+g) / (rs –g) = D0(1+0) / (rs – 0) = D0 / rs

= $2.00 / .13 = $15.38

2.00 2.00 2.00

0 1 2 3 rs = 13% ...

15

Bus 170

15 Debbie Abbott

Value of a Stock with Negative Growth?

Assume D0 = 2.00, = -6% rs = 13%

P0 = D0(1+g) / (rs –g ) = $2.00(1 - .06) / .13 – (.06) = $1.88 / .19 = $9.89

The firm still has earnings and pays dividends, even though they may be declining, they still have value

16

Bus 170

16 Debbie Abbott

Supernormal Growth

What if g = 30% for 3 years before achieving long-run growth of 6%?

Can no longer use just the constant growth model to find stock value

However, the growth does become constant after 3 years

17

Bus 170

17 Debbie Abbott

Approach: Sum PV of Cash Flows + Terminal Value

Assume D0 = 2.00, g= 30% for 3 years, then 6% thereafter, rs = 13% First find Dividends DN+1 = DN (1+g) D1=2.00(1+.3) = 2.60, D2=2.60(1+.3) = 3.38, D3=3.38(1+.3) = 4.394, D4

=4.394(1+.06) = 4.658 Next calculate TV3 TV3 = D3(1+g) / (rs –g) TV3 = 4.658 / (.13 – .06) TV3 = $66.542 PV = FV /(1+rs) PVD1 = 2.6/(1.13)1 =2.301 PVD2 = 3.38/(1.13)2 =2.647 PVD3+TV3 = (4.394 + 66.542)/(1.13)3 = 70.936 P0 = ∑PV = 54.110 Next find PV of each of the cash flows: PV = FV /(1+rs) PVD1 = 2.6/(1.13)1 =2.301 PVD2 = 3.38/(1.13)2 =2.647 PVD3+TV3 = (4.394 + 66.542)/(1.13)3 = 70.936 P0 = ∑PV = 54.110

Supernormal Then Constant Growth – Sum of PVs

rs = 13%

g = 30% g = 30% g = 30% g = 6%

0

4 0 1 2 3 ...

4.658

= 0.06

P

3

4.394(1.06)

0.13 − $66.542 =

4.394

70.936

2.301

2.647

54.110 = P0 ^

49.162

2.600 3.380 4.394

18

Bus 170

18 Debbie Abbott

Approach: Calculate Dividends + TV; then find NPV

Assume D0 = 2.00, g= 30% for 3 years, then 6% thereafter, rs = 13% Find Dividends and TV as you did in previous example Next find NPV of cash flows, using your financial calculator: I = 13% CF0 = 0 CF1 = 2.6 CF2 = 3.38

CF3 = D3+TV3 =(4.394 + 66.542) = 70.936 NPV = 54.110

Supernormal Then Constant Growth – NPV on calculator

rs = 13%

g = 30% g = 30% g = 30% g = 6%

CF0= 0 CF1= 2.600

I = 13 NPV = 54.11

CF2= 3.380 CF3= 70.936

= 0.06

P

3

4.394(1.06)

0.13 − $66.542 =

4.394

70.936

4 0 1 2 3 ...

4.658 2.600 3.380 4.394

19

Bus 170

19 Debbie Abbott

Assume D0 = 2.00, g= 0% for 3 years, then 6% thereafter, rs = 13% First find Dividends

DN+1 = DN (1+g)

D1=2.00, D2= 2.00, D, D4 =2.00(1+.06) = 2.18

Next calculate TV3

TV3 = D3(1+g) / (rs –g)

TV3 = 2.12 / (.13 – .06) TV3 = $30.29 Next find NPV of cash flows, using your financial calculator: I = 13% CF0 = 0 CF1 = 2.00 CF2 = 2.00 CF3 = D3+TV3 =(2.00 + 30.29) = 32.29 NPV = 25.71

Non-constant Growth: No Growth Then Constant Growth

rs = 13%

g = 0% g = 0% g = 0% g = 6%

CF0= 0 CF1= 2.00

I = 13 NPV = 25.71

CF2= 2.00 CF3= 32.29

= 0.06

P

3

2.00(1.06)

0.13 − $30.29 =

2.00

32.29

4 0 1 2 3 ...

2.12 2.00 2.00 2.00

20

Bus 170

20 Debbie Abbott

Corporate Value Model

Corporate Value Model – Suggests the value of the entire firm equals

the present value of the firm’s free cash flows

FCF = EBIT(1-T) + D&A – CapEx - ∆NOWC

– A good way to evaluate firms that don’t pay dividends (technology companies, start-ups)

– Also called the free cash flow method

21

Bus 170

21 Debbie Abbott

Corporate Value Model

3 Steps: 1. Find the ValueFIRM today by finding the NPV

of the firm’s future FCFs If at constant growth now: VFIRM_0 = FCF1 / (WACC – g) If at constant growth at year N: VFIRM_0 = Sum of NPV of FCF1 through N

+ VFIRM_N

22

Bus 170

22 Debbie Abbott

Corporate Value Model Continued

2. Find Value of Equity VFIRM_0 - Debt = VEQUITY

3. Find the Expected Stock Price today VEQUITY / Shares = P0

23

Bus 170

23 Debbie Abbott

Step 1 – Value of Firm

If the FCF’s shown below grow at a constant rate of 6% starting in year 3 and WACC is 10%, what is the value of the firm today? FCF0 = 0, FCF1 = -5, FCF2 = 10, FCF3 = 20; TV3 = FCF3(1+g) / WACC- g TV3 = 20(1+.06) / (.10 - .06) = 21.20 / .04 = 530 Solve for NPV, by entering CF’s and I, then press NPV CF0 = 0, CF1 = -5, CF2 = 10, CF3 = FCF3 + TV3 = 20 + 530 = 550 I = 10 NPV = ValueFIRM = $416.94

CF0= 0 CF1= -5

I = 10 NPV = ValueFIRM_0 = $416.94

0 1 2 3 4

0 -5 10 20

...

21.20

= 0.06

$ 530 TV

3

20.00(1.06)

0.10 − =

20

$ 550

CF2= 10

CF3= 550

g = 6%

r = 10%

24

Bus 170

24 Debbie Abbott

Step 2: Value of Equity and Step 3: Expected Stock Price, P0

If the firm has $40 million in debt and has 10 million shares of stock, what is the firm’s value per share?

ValueEQUITY = ValueFIRM_0 – Debt = $416.94 - $40 = $376.94 million

Value /Share = P0

= ValueEQUITY / Shares = $376.94 million / 10 million = $37.69

25

Bus 170

25 Debbie Abbott

What Is Market Equilibrium?

In equilibrium, stock prices are stable and there is no general tendency for people to buy versus to sell

In equilibrium, two conditions hold: – The current market stock price equals its intrinsic value – Expected returns must equal required returns

Expected returns are determined by estimating dividends and expected capital gains

– r^ = (D1 / P0) + g

Required returns are determined by estimating risk and applying the CAPM

– r = rRF + (rM – rRF)b

In equilibrium, r^ = r − (D1 / P0) + g = rRF + (rM – rRF)b

26

Bus 170

26 Debbie Abbott

How Market Equilibrium Works

Equilibrium levels are based on the market’s estimate of intrinsic value and the market’s required rate of return, which are both dependent upon the attitudes of the marginal investor

If price is below intrinsic value … – The current price (P0) is “too low” and offers a bargain – Buy orders will be greater than sell orders – P0 will be bid up until expected return equals required

return

If price is above intrinsic value, the opposite is true

27

Bus 170

27 Debbie Abbott

Preferred Stock

Hybrid security

Like bonds, preferred stockholders receive a fixed dividend that must be paid before dividends are paid to common stockholders

However, companies can omit preferred dividend payments without fear of pushing the firm into bankruptcy

28

Bus 170

28 Debbie Abbott

Expected Return on Preferred Stock

If preferred stock with an annual dividend of $5 sells for $50, what is the preferred stock’s expected return?

Vp = Dp / rp $50 = $5 / rp rp = $5 / $50 = 0.10 = 10%