Ch18_Test Bank Jeter Advanced Accounting 3rd Edition

22

Chapter 18 Introduction to Accounting for State and Local Governmental Units Multiple Choice 1. The highest level of priority of pronouncements that a government entity should look to for accounting and reporting guidance is a. GASB Technical Bulletins. b. GASB Concepts Statements. c. AICPA Industry Accounting Guides. d. GASB Statements. 2. Which of the following funds would account for operations that are financed and operated in a manner similar to private business enterprises? a. Debt Service Fund b. Enterprise Fund c. Internal Service Fund d. Special Revenue Fund 3. All of the following are Governmental (Expendable) Fund Entities except the a. Capital Projects Fund. b. Debt Service Fund. c. Internal Service Fund. d. Special Revenue Fund. 4. The activities of a municipal airport should be accounted for in the a. General Fund. b. Internal Service Fund. c. Special Revenue Fund. d. Enterprise Fund. 5. Fixed assets and noncurrent liabilities are accounted for in the records of a. governmental funds b. expendable funds c. proprietary funds d. both governmental and expendable funds. 6. The liability for general obligation long-term debt is reported in the a. Debt Service Fund. b. Capital Projects Fund. c. Enterprise Fund. d. none of these. 7. The activities of a central computer facility should be accounted for in the a. General Fund. b. Internal Service Fund. c. Enterprise Fund. d. Capital Projects Fund. http://downloadslide.blogspot.com To download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.com To download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.com

-

Upload

abdul-aziz -

Category

Documents

-

view

1.383 -

download

7

Transcript of Ch18_Test Bank Jeter Advanced Accounting 3rd Edition

Chapter 18

Introduction to Accounting for State and Local Governmental Units

Multiple Choice

1. The highest level of priority of pronouncements that a government entity should look to for

accounting and reporting guidance is

a. GASB Technical Bulletins.

b. GASB Concepts Statements.

c. AICPA Industry Accounting Guides.

d. GASB Statements.

2. Which of the following funds would account for operations that are financed and operated in a

manner similar to private business enterprises?

a. Debt Service Fund

b. Enterprise Fund

c. Internal Service Fund

d. Special Revenue Fund

3. All of the following are Governmental (Expendable) Fund Entities except the

a. Capital Projects Fund.

b. Debt Service Fund.

c. Internal Service Fund.

d. Special Revenue Fund.

4. The activities of a municipal airport should be accounted for in the

a. General Fund.

b. Internal Service Fund.

c. Special Revenue Fund.

d. Enterprise Fund.

5. Fixed assets and noncurrent liabilities are accounted for in the records of

a. governmental funds

b. expendable funds

c. proprietary funds

d. both governmental and expendable funds.

6. The liability for general obligation long-term debt is reported in the

a. Debt Service Fund.

b. Capital Projects Fund.

c. Enterprise Fund.

d. none of these.

7. The activities of a central computer facility should be accounted for in the

a. General Fund.

b. Internal Service Fund.

c. Enterprise Fund.

d. Capital Projects Fund.

http://downloadslide.blogspot.com

To download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.comTo download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.com

Test Bank to accompany Jeter and Chaney Advanced Accounting 3rd

Edition

18-2

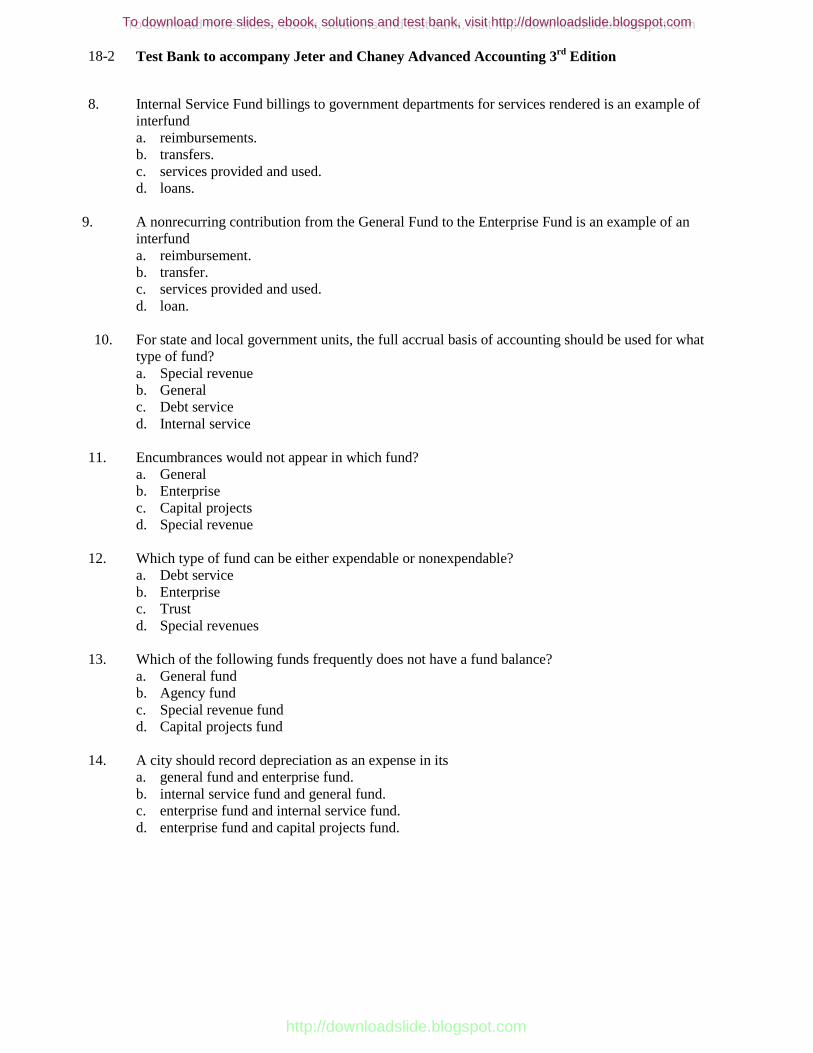

8. Internal Service Fund billings to government departments for services rendered is an example of

interfund

a. reimbursements.

b. transfers.

c. services provided and used.

d. loans.

9. A nonrecurring contribution from the General Fund to the Enterprise Fund is an example of an

interfund

a. reimbursement.

b. transfer.

c. services provided and used.

d. loan.

10. For state and local government units, the full accrual basis of accounting should be used for what

type of fund?

a. Special revenue

b. General

c. Debt service

d. Internal service

11. Encumbrances would not appear in which fund?

a. General

b. Enterprise

c. Capital projects

d. Special revenue

12. Which type of fund can be either expendable or nonexpendable?

a. Debt service

b. Enterprise

c. Trust

d. Special revenues

13. Which of the following funds frequently does not have a fund balance?

a. General fund

b. Agency fund

c. Special revenue fund

d. Capital projects fund

14. A city should record depreciation as an expense in its

a. general fund and enterprise fund.

b. internal service fund and general fund.

c. enterprise fund and internal service fund.

d. enterprise fund and capital projects fund.

http://downloadslide.blogspot.com

To download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.comTo download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.com

Chapter 18 Introduction to Accounting for State and Local Governmental Units

18-3

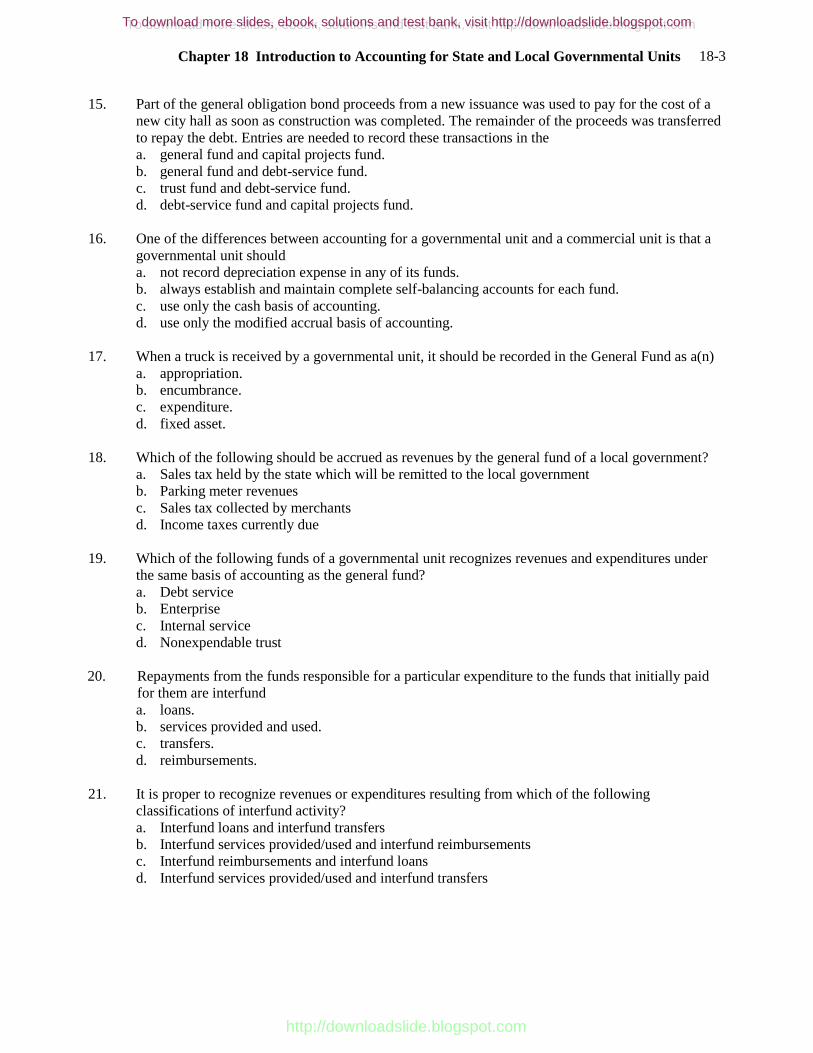

15. Part of the general obligation bond proceeds from a new issuance was used to pay for the cost of a

new city hall as soon as construction was completed. The remainder of the proceeds was transferred

to repay the debt. Entries are needed to record these transactions in the

a. general fund and capital projects fund.

b. general fund and debt-service fund.

c. trust fund and debt-service fund.

d. debt-service fund and capital projects fund.

16. One of the differences between accounting for a governmental unit and a commercial unit is that a

governmental unit should

a. not record depreciation expense in any of its funds.

b. always establish and maintain complete self-balancing accounts for each fund.

c. use only the cash basis of accounting.

d. use only the modified accrual basis of accounting.

17. When a truck is received by a governmental unit, it should be recorded in the General Fund as a(n)

a. appropriation.

b. encumbrance.

c. expenditure.

d. fixed asset.

18. Which of the following should be accrued as revenues by the general fund of a local government?

a. Sales tax held by the state which will be remitted to the local government

b. Parking meter revenues

c. Sales tax collected by merchants

d. Income taxes currently due

19. Which of the following funds of a governmental unit recognizes revenues and expenditures under

the same basis of accounting as the general fund?

a. Debt service

b. Enterprise

c. Internal service

d. Nonexpendable trust

20. Repayments from the funds responsible for a particular expenditure to the funds that initially paid

for them are interfund

a. loans.

b. services provided and used.

c. transfers.

d. reimbursements.

21. It is proper to recognize revenues or expenditures resulting from which of the following

classifications of interfund activity?

a. Interfund loans and interfund transfers

b. Interfund services provided/used and interfund reimbursements

c. Interfund reimbursements and interfund loans

d. Interfund services provided/used and interfund transfers

http://downloadslide.blogspot.com

To download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.comTo download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.com

Test Bank to accompany Jeter and Chaney Advanced Accounting 3rd

Edition

18-4

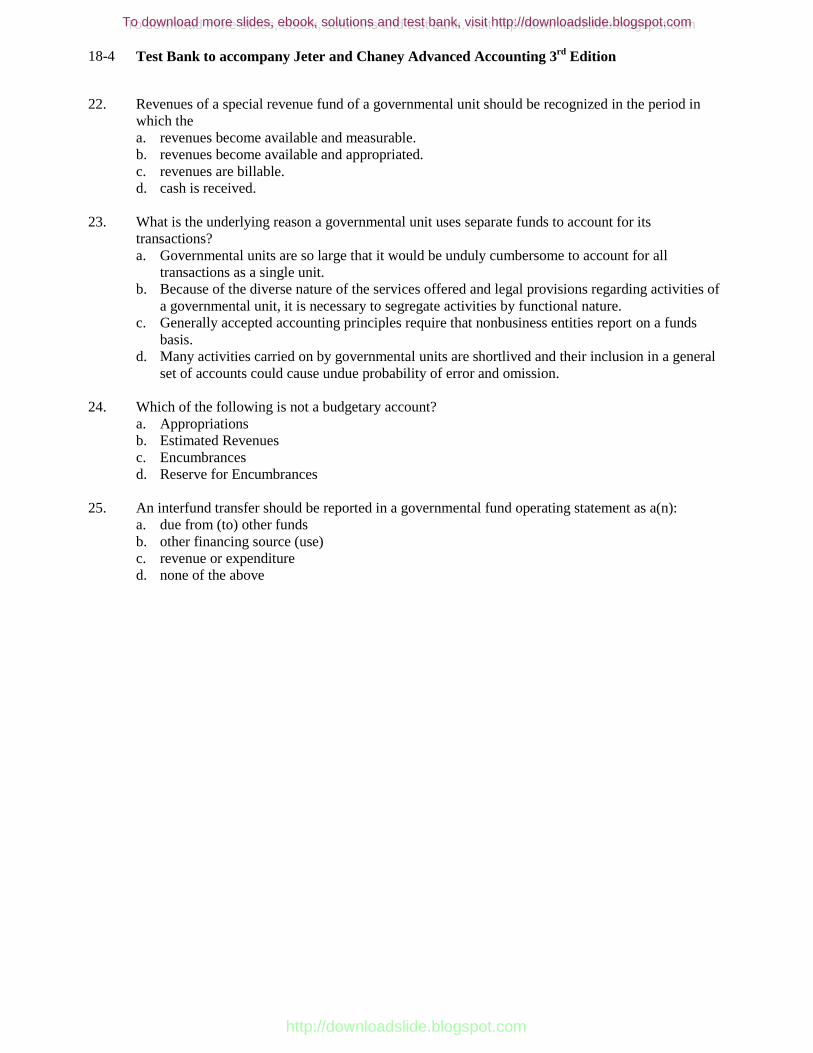

22. Revenues of a special revenue fund of a governmental unit should be recognized in the period in

which the

a. revenues become available and measurable.

b. revenues become available and appropriated.

c. revenues are billable.

d. cash is received.

23. What is the underlying reason a governmental unit uses separate funds to account for its

transactions?

a. Governmental units are so large that it would be unduly cumbersome to account for all

transactions as a single unit.

b. Because of the diverse nature of the services offered and legal provisions regarding activities of

a governmental unit, it is necessary to segregate activities by functional nature.

c. Generally accepted accounting principles require that nonbusiness entities report on a funds

basis.

d. Many activities carried on by governmental units are shortlived and their inclusion in a general

set of accounts could cause undue probability of error and omission.

24. Which of the following is not a budgetary account?

a. Appropriations

b. Estimated Revenues

c. Encumbrances

d. Reserve for Encumbrances

25. An interfund transfer should be reported in a governmental fund operating statement as a(n):

a. due from (to) other funds

b. other financing source (use)

c. revenue or expenditure

d. none of the above

http://downloadslide.blogspot.com

To download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.comTo download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.com

Chapter 18 Introduction to Accounting for State and Local Governmental Units

18-5

Problems

18-1 During 2010, the City of Lebo started a street paving project. The project is being financed by the

proceeds from the issue of five-year, 6% special assessment bonds payable at a face value of

$3,000,000. The bonds were issued July 1, 2010 at their par value. One-fifth of the principal plus

interest is payable on June 30 of each year beginning June 30, 2011. Property owners are assessed to

provide the funds to pay the principal and interest on the debt.

The following transactions occurred during 2010 and 2011:

1. The bonds for the paving of the streets were issued.

2. The street paving was completed at a cost of $3,000,000.

3. Property owners were assessed and billed for the first installment of principal and interest on the

special assessment debt.

4. Assessments for the first installment of principal and interest on the special assessment debt

were collected. The June 30, 2011, payment of principal and interest was made.

Required:

Prepare all journal entries for the preceding transactions that are necessary for the City of Lebo

assuming:

A. The City of Lebo has not obligated itself in any manner to the holders of the special

assessment bonds.

B. The City of Lebo has made a commitment to the holders of the special assessment bonds to

assure the full payment of principal and interest on the due dates.

18-2 The following activities and transactions are typical of those which may affect the various funds

used by a municipal government.

Required:

Prepare journal entries to record each transaction and identify the fund in which each entry is

recorded.

1. The Zola City Council passed a resolution approving a general operating budget of $6,800,000

for the fiscal year. Total revenues are estimated at $5,800,000.

2. The Zola City Council passed an ordinance providing a property tax levy of $3.50 per $100 of

assessed valuation for the fiscal year. Total property valuation in Zola City is $320,000,000.

Property is assessed at 30% of current property valuation. Property tax bills are mailed to

property owners. An estimated 5% will be uncollectible.

3. Kansas City sold a general obligation term bond issue for $1,000,000 at 104 to a major

brokerage firm. The stated interest rate is 10%. Construction of a new Municipal Courts

Building will be financed by the bond issue proceeds.

4. The premium on bond sale in (3) above is transferred to the Debt Service Fund.

5. At the end of fiscal year, the Zola City Council approves the write-off of $55,000 of uncollected

taxes because of inability to locate the property owners.

http://downloadslide.blogspot.com

To download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.comTo download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.com

Test Bank to accompany Jeter and Chaney Advanced Accounting 3rd

Edition

18-6

6. The Kansas City Municipal Courts Building (3 above) is completed. Contracts and expenses

total $1,190,000, and all have been paid and recorded in the Capital Projects Fund. Prepare

entries to close this project and record the completion of the project in all other funds and/or

account groups affected. Any balance in the Capital Projects Fund is to be applied to payment

of interest and principal of the bond issue.

7. On March 1, Webb City issued 10% serial bonds at par to finance streetlights in an area recently

incorporated in the city limits. The face amount of the bonds is $900,000; interest is payable

annually, and bonds are to be retired in equal amounts over 6 years from collections from

assessments against property affected. In case of default by the property owners, the bond

principal will be paid by the city.

a. Record the issuance of the bonds on March 1 of the current year.

b. Record the payment to bondholders on March 1 of the next year.

8. The street lighting project in (7) above was completed on September 30 at a total cost of

$840,000. Record summary entries for expenditure transactions from March 1 - September 30,

and on completion of the project.

18-3 Prepare entries, in general journal form, to record the following transactions in the proper fund(s)

and/or account group(s). Designate the fund or account group in which each entry is recorded.

1. Bond proceeds of $2,000,000 were received to be used in constructing a new City Jail. An

equal amount is contributed from general revenues.

2. Serial bonds in the amount of $300,000 matured. Interest of $75,000 was paid on these and

other serial bonds outstanding.

3. Insurance proceeds amounting to $19,000 were received as a result of the accidental destruction

of a garbage truck costing $33,000. Accumulated depreciation on the truck was $21,000.

4. The City Parks Endowment Fund transferred $160,000 in expendable funds to the City Parks

Special Revenue Fund.

5. Proceeds of $21,000 were received from the sale of equipment which had been purchased from

general revenues at a cost of $100,000. Accumulated depreciation on the equipment was

$75,000.

6. The City Power Company (an enterprise fund) issued a bill for $400,000 for electricity provided

to municipal government buildings.

7. The City Power Company transferred excess funds of $90,000 to the General Fund.

8. A central data processing center was established by a contribution of $400,000 from the General

Fund, a long-term loan of $130,000 from the City Parks Special Revenue Fund, and general

obligation bond proceeds of $180,000.

9. The Data Processing Fund billed the General Fund $20,000 and the City Parks Special Revenue

Fund $8,500 for data processing services.

http://downloadslide.blogspot.com

To download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.comTo download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.com

Chapter 18 Introduction to Accounting for State and Local Governmental Units

18-7

10. The City Power Company received $7,000 as customer deposits during the year. The monies

are to be held in trust until customers request that their services be discontinued and final bills

are collected.

11. In order to retire general obligation term bonds when they become due, it is determined that the

Debt Service Fund will require annual contributions of $40,000 and earnings in the current year

of $3,000.

18-4 The general fund trial balance for Shawnee City held the following balances at June 30, 2011, just

before closing entries were made:

Unreserved Fund Balance $ 2,000

Estimated Revenues 33,000

Revenues 27,250

Appropriations 28,000

Expenditures 26,200

Expenditures-Prior Year 1,200

Encumbrances 3,000

Operating Transfers In 6,000

Reserve for Encumbrances 3,000

Reserve for Encumbrances – Prior Year 1,500

Required:

Prepare the necessary closing entries.

18-5 The following schedule of capital assets was prepared for Pratt County.

Government Activities Beg. Balance Additions Retirements Ending Balance

Total Capital Assets $850,000 250,000 (185,000) $915,000

Less: Accumulated ( 500,000) ( 50,000) 150,000 ( 400,000)

Depreciation

Net Capital Assets $350,000 $200,000 ( 35,000) $515,000

All capital asset acquisitions were made in the capital projects fund and paid in cash. An asset was sold by

the general fund for $40,000 cash.

Required:

Determine how the above information will be reflected on each of the following statements for the

year 2011.

A. The governmental funds’ statement of revenues, expenditures, and changes in fund

balances. List the governmental fund and then list the dollar amount within the appropriate

heading on the statement (such as Revenues, Expenditures, or Other Financing Sources

(Uses)).

B. The government-wide statement of net assets.

C. The government-wide statement of activities.

http://downloadslide.blogspot.com

To download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.comTo download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.com

Test Bank to accompany Jeter and Chaney Advanced Accounting 3rd

Edition

18-8

18-6 The following events take place:

1. Interest payments in the amount of $20,000 that are the responsibility of the Debt Service

Fund are paid by the General Fund.

2. The Internal Service Fund bills the Special Revenue Fund $25,000 for services performed.

3. The Special Revenue Fund transfers $10,000 to the Internal Service Fund as a temporary loan.

4. The General Fund transfers $150,000 to start an Internal Service Fund.

Required:

Identify the interfund activity as a loan, services provided and used, interfund transfer, or interfund

reimbursement and prepare entries in general journal form to record the transactions on the records

of the fund involved.

18-7 The following transactions take place:

1. On January 1, the city issued 9% general obligation bonds with a face value of $4,000,000

payable in 10 years to finance the construction of city offices. Total proceeds were

$4,500,000.

2. On December 20, construction was completed and occupancy taken of the city offices. The

full cost of $3,900,000 was paid to the contractor, and appropriate closing entries were made

with regard to the project.

3. The General Fund repaid the Special Revenue Fund a loan of $15,000 plus $900 in interest on

the loan.

Required:

Prepare entries in general journal form to record these transactions in the proper fund(s). Designate

the fund in which each entry is recorded.

Short Answer

1. There are eleven categories of government fund entities that fall under three subheadings. Describe

the subheadings of government fund entities.

2. GASB Statement No. 34 specifies how governments report capital assets and long-term obligations.

Describe where capital assets and long-term obligations are reported in government financial

statements.

Short Answer Questions from the Textbook

1. Eleven funds are recommended to account for the various activities and resources of a govern-

mental unit. Identify these funds by title and type and briefly state (in two sentences or less) the

basic purpose of each fund.

2. Why are governments required to prepare financial statements on a government-wide basis using

full accrual accounting?

3. What is the difference between a governmental fund and a proprietary fund?

4. Are fiduciary funds governmental funds or proprietary funds? Explain.

http://downloadslide.blogspot.com

To download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.comTo download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.com

Chapter 18 Introduction to Accounting for State and Local Governmental Units

18-9

5. A disbursement by the general fund to another fund may be recorded as a receivable, an

expenditure, or a fund transfer. Explain the circum-stances that would result in each of these

different treatments.

6. In what funds would you expect bonds payable to be included?

7. In what funds might property and other non financial resources be recorded?

8. Why are budgeted revenues and expenditures formally recorded in the records of the general fund

but not in the records of a capital projects fund?

9. Are all major capital facilities acquisitions ac-counted for in a capital projects fund? Explain.

10. What exception to the normal expenditure recognition criteria is associated with debt ser-vice funds

and what is the justification for this exception?

11. Identify and describe four types of interfund activities.

12. The following funds and account groups are recommended for use in accounting for state and

municipal governmental financial operations:

A. General Fund.

B. Special Revenue Fund.

C. Debt Service Fund.

D. Capital Projects Fund.

E. Agency Fund.

F. Enterprise Fund.

G. Internal Service Fund.

H. Trust Fund.

I. Government-wide Statement of Activities.

J. Government-wide Statement of Net Assets.

Identify, by the letters given above, the funds and account groups in which each of the ac-count

titles below might properly appear.

(1) Bonds Payable.

(2) Reserve for Encumbrances.

(3) Equipment.

(4) Appropriations.

(5) Estimated Revenue.

(6) Property Taxes Receivable.

(7) Construction Work in Progress.

(8) Accumulated Depreciation.

(9) Depreciation Expense.

(10)Required Earnings.

13. Describe some of the major reconciling items between a government fund and the government-

wide financial statements.

Business Ethics Question from the Textbook

GASB 45requires that the expected future costs of retiree health costs be recognized in the current period.

Prior to this, governments used a pay-as-you-go plan in which only the current year’s actual payments

http://downloadslide.blogspot.com

To download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.comTo download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.com

Test Bank to accompany Jeter and Chaney Advanced Accounting 3rd

Edition

18-10

affected the financial statements. Suppose you are working for a government prior to the issuance of GASB

45. As part of the collective bar-gaining agreement, the government offers employees increased health

benefits.

1. Prior to the issuance of GASB 45, what would be the impact on the government’s financial

statements?

2. Under GASB 45, what are the financial statement implications?

3. Why might the current governmental leaders agree to offer such a benefit?4.What are the ethical

issues involved in this decision?

http://downloadslide.blogspot.com

To download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.comTo download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.com

Chapter 18 Introduction to Accounting for State and Local Governmental Units

18-11

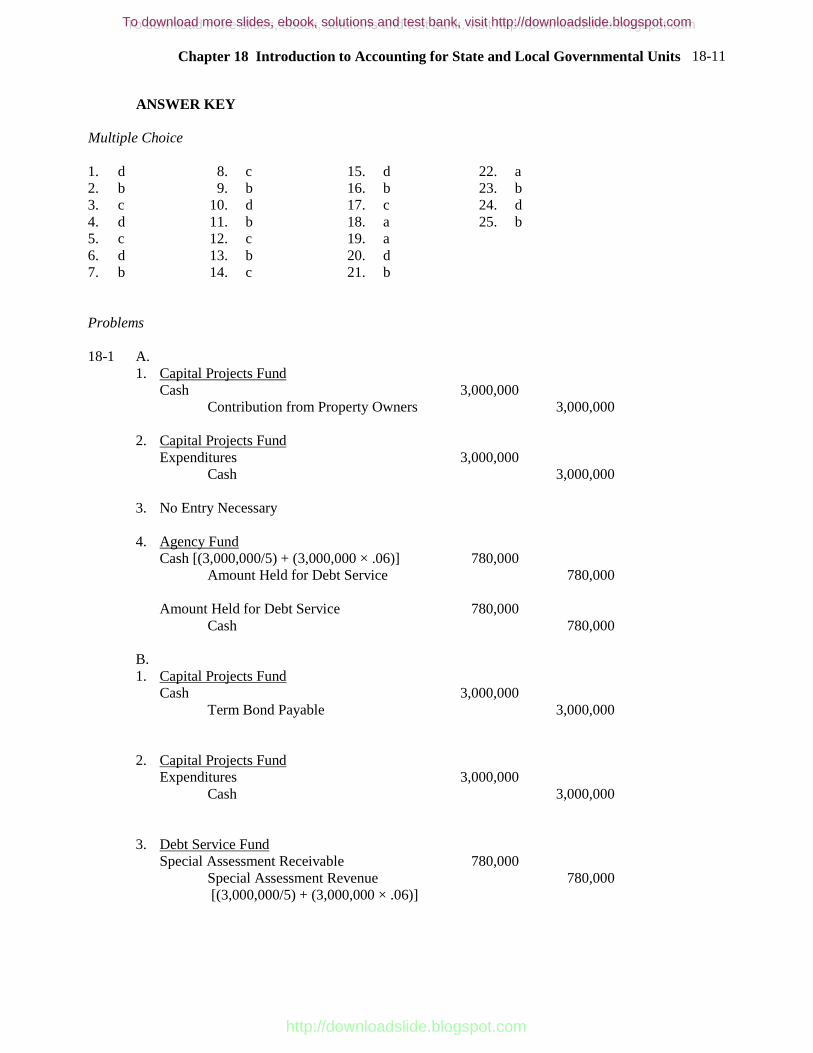

ANSWER KEY

Multiple Choice

1. d

2. b

3. c

4. d

5. c

6. d

7. b

8. c

9. b

10. d

11. b

12. c

13. b

14. c

15. d

16. b

17. c

18. a

19. a

20. d

21. b

22. a

23. b

24. d

25. b

Problems

18-1 A.

1. Capital Projects Fund

Cash 3,000,000

Contribution from Property Owners 3,000,000

2. Capital Projects Fund

Expenditures 3,000,000

Cash 3,000,000

3. No Entry Necessary

4. Agency Fund

Cash [(3,000,000/5) + (3,000,000 × .06)] 780,000

Amount Held for Debt Service 780,000

Amount Held for Debt Service 780,000

Cash 780,000

B.

1. Capital Projects Fund

Cash 3,000,000

Term Bond Payable 3,000,000

2. Capital Projects Fund

Expenditures 3,000,000

Cash 3,000,000

3. Debt Service Fund

Special Assessment Receivable 780,000

Special Assessment Revenue 780,000

[(3,000,000/5) + (3,000,000 × .06)]

http://downloadslide.blogspot.com

To download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.comTo download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.com

Test Bank to accompany Jeter and Chaney Advanced Accounting 3rd

Edition

18-12

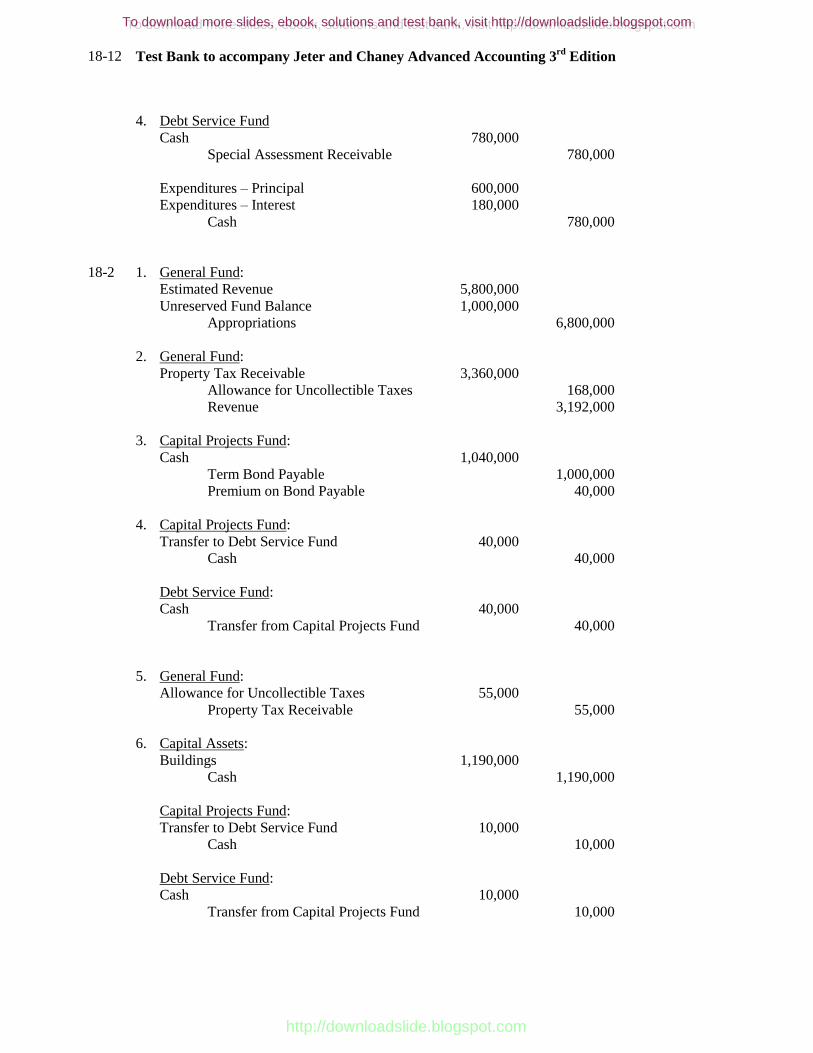

4. Debt Service Fund

Cash 780,000

Special Assessment Receivable 780,000

Expenditures – Principal 600,000

Expenditures – Interest 180,000

Cash 780,000

18-2 1. General Fund:

Estimated Revenue 5,800,000

Unreserved Fund Balance 1,000,000

Appropriations 6,800,000

2. General Fund:

Property Tax Receivable 3,360,000

Allowance for Uncollectible Taxes 168,000

Revenue 3,192,000

3. Capital Projects Fund:

Cash 1,040,000

Term Bond Payable 1,000,000

Premium on Bond Payable 40,000

4. Capital Projects Fund:

Transfer to Debt Service Fund 40,000

Cash 40,000

Debt Service Fund:

Cash 40,000

Transfer from Capital Projects Fund 40,000

5. General Fund:

Allowance for Uncollectible Taxes 55,000

Property Tax Receivable 55,000

6. Capital Assets:

Buildings 1,190,000

Cash 1,190,000

Capital Projects Fund:

Transfer to Debt Service Fund 10,000

Cash 10,000

Debt Service Fund:

Cash 10,000

Transfer from Capital Projects Fund 10,000

http://downloadslide.blogspot.com

To download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.comTo download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.com

Chapter 18 Introduction to Accounting for State and Local Governmental Units

18-13

7. Capital Projects Fund:

Cash 900,000

Term Bond Payable 900,000

Debt Service Fund:

Expenditures – Principal 150,000

Expenditures – Interest 90,000

Cash 240,000

8. Capital Projects Fund:

Expenditures 840,000

Vouchers Payable/Cash 840,000

Fund Balance 840,000

Expenditures 840,000

18-3 1. Capital Projects Fund:

Cash 4,000,000

Term Bond Payable 2,000,000

Transfer from General Fund 2,000,000

General Fund:

Transfer to Capital Projects Fund 2,000,000

Cash 2,000,000

2. Debt Service Fund:

Expenditures 375,000

Cash 375,000

3. General Fund:

Cash 19,000

Revenue 19,000

Capital Assets

Cash 19,000

Accumulated Depreciation 21,000

Gain on Sale 7,000

Vehicles 33,000

4. Trust Fund:

Transfer to Special Revenue Fund 160,000

Cash 160,000

Special Revenue Fund:

Cash 160,000

Transfer from Trust Fund 160,000

http://downloadslide.blogspot.com

To download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.comTo download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.com

Test Bank to accompany Jeter and Chaney Advanced Accounting 3rd

Edition

18-14

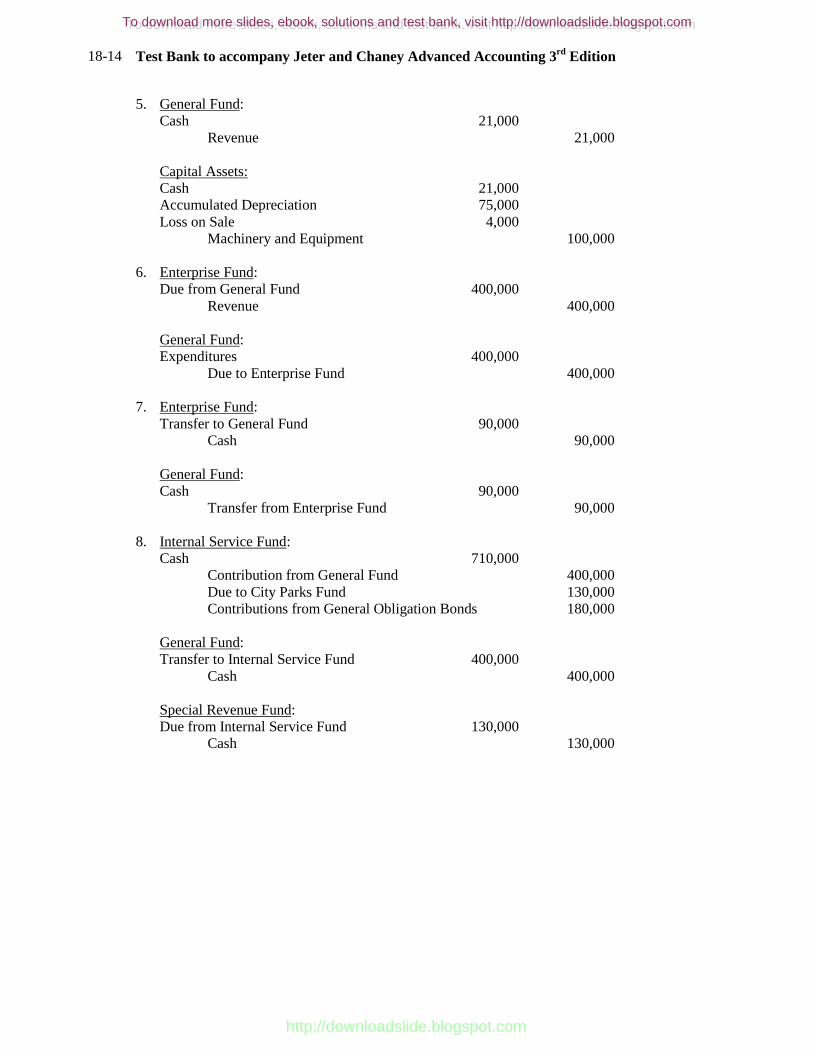

5. General Fund:

Cash 21,000

Revenue 21,000

Capital Assets:

Cash 21,000

Accumulated Depreciation 75,000

Loss on Sale 4,000

Machinery and Equipment 100,000

6. Enterprise Fund:

Due from General Fund 400,000

Revenue 400,000

General Fund:

Expenditures 400,000

Due to Enterprise Fund 400,000

7. Enterprise Fund:

Transfer to General Fund 90,000

Cash 90,000

General Fund:

Cash 90,000

Transfer from Enterprise Fund 90,000

8. Internal Service Fund:

Cash 710,000

Contribution from General Fund 400,000

Due to City Parks Fund 130,000

Contributions from General Obligation Bonds 180,000

General Fund:

Transfer to Internal Service Fund 400,000

Cash 400,000

Special Revenue Fund:

Due from Internal Service Fund 130,000

Cash 130,000

http://downloadslide.blogspot.com

To download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.comTo download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.com

Chapter 18 Introduction to Accounting for State and Local Governmental Units

18-15

9. Internal Service Fund:

Due from General Fund 20,000

Due from Special Revenue Fund 8,500

Revenue 28,500

General Fund:

Expenditures 20,000

Due to Internal Service Fund 20,000

Special Revenue Fund:

Expenditures 8,500

Due to Internal Service Fund 8,500

10. Agency Fund:

Cash 7,000

Customer Deposit Agency Fund Balance 7,000

11. Debt Service Fund:

Required Additions 40,000

Required Earnings 3,000

Fund Balance 43,000

18-4

Appropriations 28,000

Unreserved Fund Balance 5,000

Estimated Revenues 33,000

Revenues 27,250

Operating Transfers In 6,000

Expenditures 26,200

Encumbrances 3,000

Unreserved Fund Balance 4,050

Reserve for Encumbrances – Prior Year 1,500

Expenditures – Prior Year 1,500

http://downloadslide.blogspot.com

To download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.comTo download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.com

Test Bank to accompany Jeter and Chaney Advanced Accounting 3rd

Edition

18-16

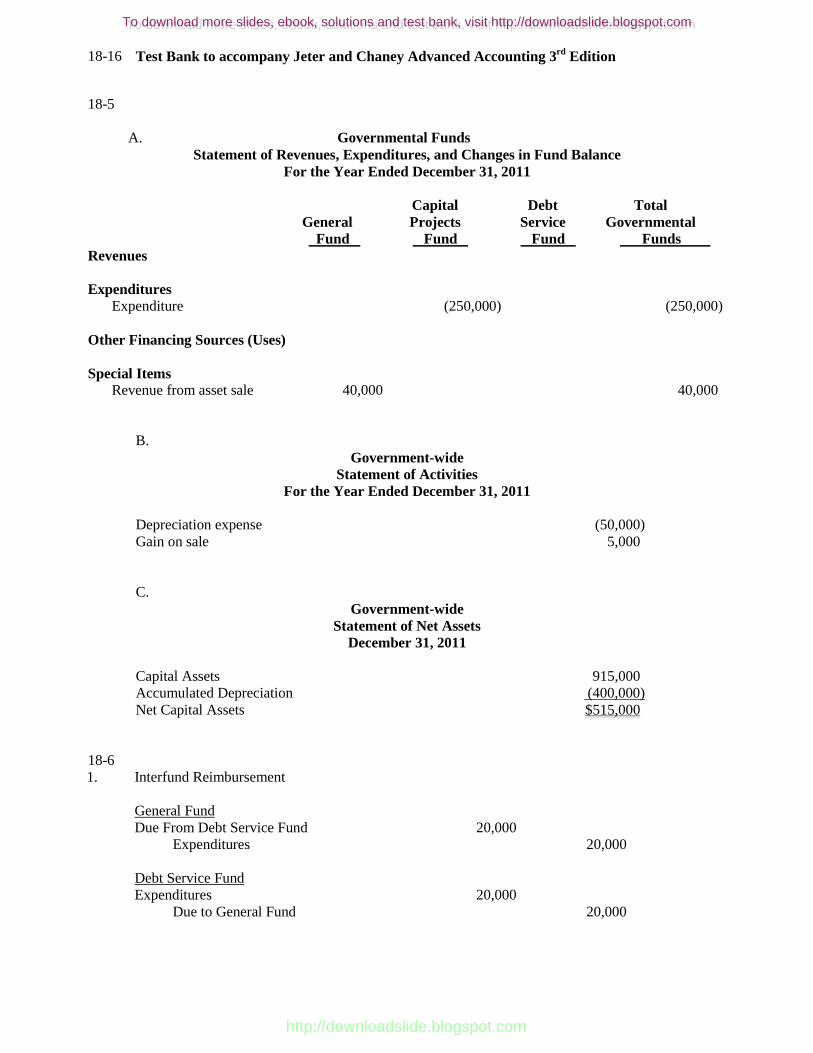

18-5

A. Governmental Funds

Statement of Revenues, Expenditures, and Changes in Fund Balance

For the Year Ended December 31, 2011

Capital Debt Total

General Projects Service Governmental

Fund Fund Fund Funds

Revenues

Expenditures

Expenditure (250,000) (250,000)

Other Financing Sources (Uses)

Special Items

Revenue from asset sale 40,000 40,000

B.

Government-wide

Statement of Activities

For the Year Ended December 31, 2011

Depreciation expense (50,000)

Gain on sale 5,000

C.

Government-wide

Statement of Net Assets

December 31, 2011

Capital Assets 915,000

Accumulated Depreciation (400,000)

Net Capital Assets $515,000

18-6

1. Interfund Reimbursement

General Fund

Due From Debt Service Fund 20,000

Expenditures 20,000

Debt Service Fund

Expenditures 20,000

Due to General Fund 20,000

http://downloadslide.blogspot.com

To download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.comTo download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.com

Chapter 18 Introduction to Accounting for State and Local Governmental Units

18-17

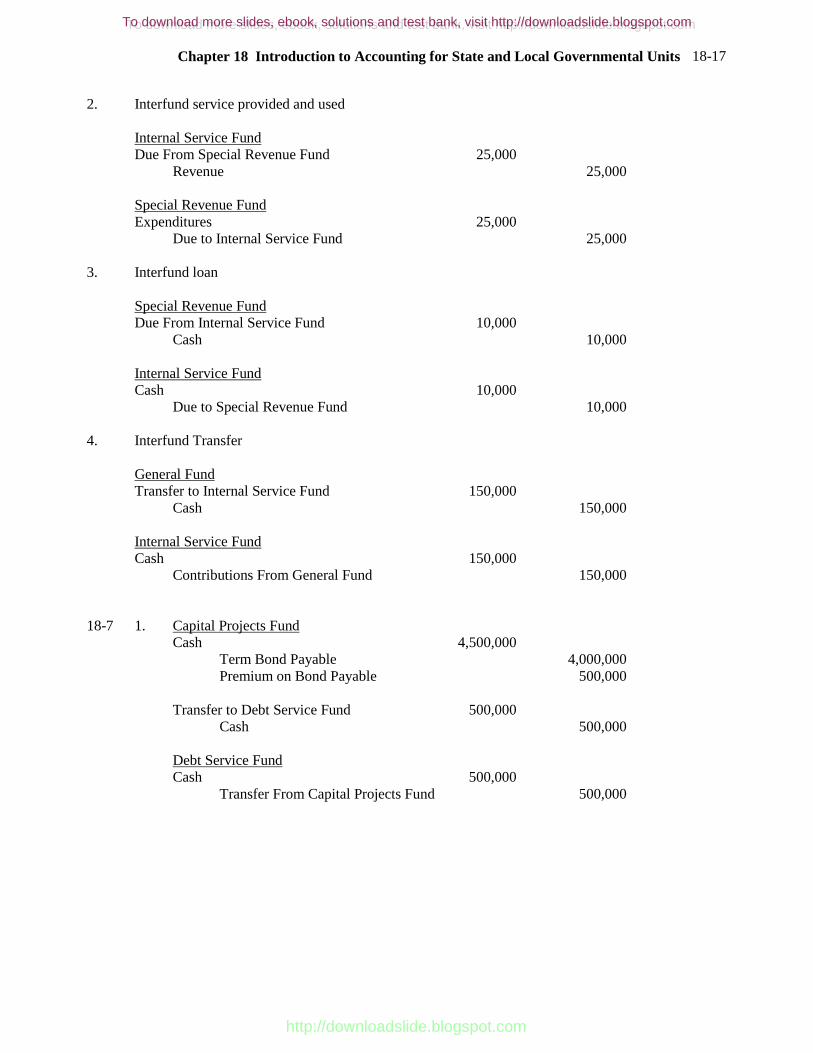

2. Interfund service provided and used

Internal Service Fund

Due From Special Revenue Fund 25,000

Revenue 25,000

Special Revenue Fund

Expenditures 25,000

Due to Internal Service Fund 25,000

3. Interfund loan

Special Revenue Fund

Due From Internal Service Fund 10,000

Cash 10,000

Internal Service Fund

Cash 10,000

Due to Special Revenue Fund 10,000

4. Interfund Transfer

General Fund

Transfer to Internal Service Fund 150,000

Cash 150,000

Internal Service Fund

Cash 150,000

Contributions From General Fund 150,000

18-7 1. Capital Projects Fund

Cash 4,500,000

Term Bond Payable 4,000,000

Premium on Bond Payable 500,000

Transfer to Debt Service Fund 500,000

Cash 500,000

Debt Service Fund

Cash 500,000

Transfer From Capital Projects Fund 500,000

http://downloadslide.blogspot.com

To download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.comTo download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.com

Test Bank to accompany Jeter and Chaney Advanced Accounting 3rd

Edition

18-18

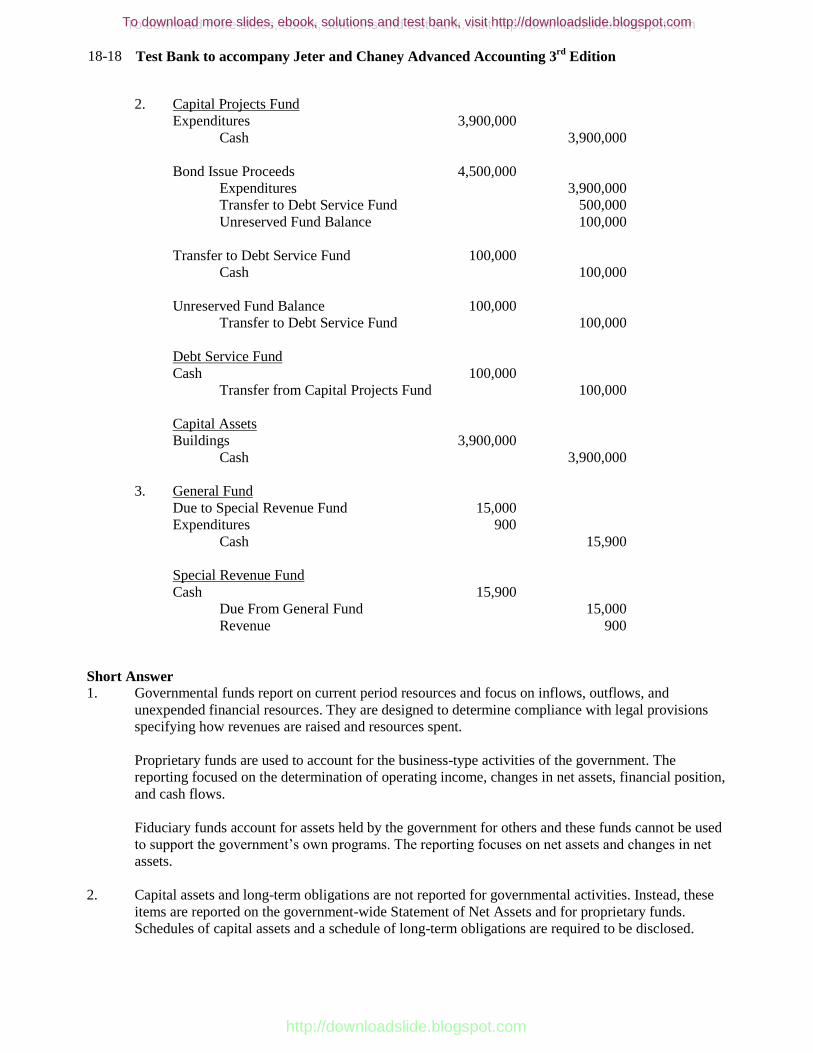

2. Capital Projects Fund

Expenditures 3,900,000

Cash 3,900,000

Bond Issue Proceeds 4,500,000

Expenditures 3,900,000

Transfer to Debt Service Fund 500,000

Unreserved Fund Balance 100,000

Transfer to Debt Service Fund 100,000

Cash 100,000

Unreserved Fund Balance 100,000

Transfer to Debt Service Fund 100,000

Debt Service Fund

Cash 100,000

Transfer from Capital Projects Fund 100,000

Capital Assets

Buildings 3,900,000

Cash 3,900,000

3. General Fund

Due to Special Revenue Fund 15,000

Expenditures 900

Cash 15,900

Special Revenue Fund

Cash 15,900

Due From General Fund 15,000

Revenue 900

Short Answer

1. Governmental funds report on current period resources and focus on inflows, outflows, and

unexpended financial resources. They are designed to determine compliance with legal provisions

specifying how revenues are raised and resources spent.

Proprietary funds are used to account for the business-type activities of the government. The

reporting focused on the determination of operating income, changes in net assets, financial position,

and cash flows.

Fiduciary funds account for assets held by the government for others and these funds cannot be used

to support the government’s own programs. The reporting focuses on net assets and changes in net

assets.

2. Capital assets and long-term obligations are not reported for governmental activities. Instead, these

items are reported on the government-wide Statement of Net Assets and for proprietary funds.

Schedules of capital assets and a schedule of long-term obligations are required to be disclosed.

http://downloadslide.blogspot.com

To download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.comTo download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.com

Chapter 18 Introduction to Accounting for State and Local Governmental Units

18-19

Short Answer Questions from the Textbook Solutions

1. Fund Entities

Governmental Funds

(1) General Fund - to account for all unrestricted resources except those required to be accounted for

in another fund.

(2) Special Revenue Funds - to account for the proceeds of specific revenue sources (other than

expendable trusts, or for major capital projects) that are legally restricted to expenditures for

specified purposes.

(3) Capital Projects Funds - to account for financial resources segregated for the acquisition of major

capital facilities (other than those financed by Enterprise Funds).

(4) Debt Service Funds - to account for the accumulation of resources for, and the payment of, interest

and principal on general obligation long-term debt.

(5) Permanent Funds – to account for resources that are legally restricted to the extent that only

earnings, and not principal, may be used for purposes that support the government’s programs –

that is, for the benefit of the government or its citizenry.

Proprietary Funds

(6) Enterprise Funds – to account for the provision of goods or services to the general public on a

continuing basis where all or most of the costs involved are financed by user charges, or where

periodic determination of revenue earned, expenses incurred, and /or net income is appropriate for

management control, accountability, or other purposes.

(7) Internal Service Funds - to account for the financing of goods or services provided by one

department or agency to other departments or agencies of the governmental unit, or to other

governmental units, on a cost – reimbursement basis.

Fiduciary Funds

(8) Pension (and Other Employee Benefit) Trust Funds – used to report resources that are required to

be held in trust for the members and beneficiaries of defined benefit pension plans, defined

contribution plans, other postemployment benefit plans, or other employee benefit plans.

(9) Investment Trust Funds – used to report the external portion of investment pools reported by the

sponsoring government.

(10) Private-Purpose Trust Funds – used to report escheat property and to report all other trust

agreements under which principal and income benefit individuals, private organizations, or other

governments.

(11) Agency Funds – used to report resources held by the reporting government in a purely custodial

capacity (assets equal liabilities). Agency funds typically involve only the receipt, temporary

investment, and remittance of fiduciary resources to individuals, private organizations, or other

governments.

2. Government-wide statements are now required to help users assess the benefits and costs of various

programs in a manner comparable to the appraisal of profit seeking businesses. For example, the revenues

generated by a program can be compared to the expenses incurred by that program. The new requirements

http://downloadslide.blogspot.com

To download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.comTo download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.com

Test Bank to accompany Jeter and Chaney Advanced Accounting 3rd

Edition

18-20

also enable a reconciliation to be made between the fund statements and these new government-wide

statements.

By providing this information, the government-wide statements should contribute to meeting the

operational accountability aspects of the overall objective stated in the conceptual framework: fulfilling

government’s duty to be publicly accountable and enabling users to assess that accountability.

3. A governmental fund is an expendable fund entity. The accounting and reporting emphasis for a

governmental fund is on the inflow, outflow, and unexpected balance of net financial resources and on the

compliance with detailed legal provisions that specify the types of revenue to be raised and the purposes

for which the financial resources may be used.

The accounting and reporting emphasis of a proprietary fund is similar to that of a commercial enterprise.

Thus, both current and fixed assets and current and noncurrent liabilities are accounted for in the records of

proprietary fund entities. In addition, revenue, expenses (including depreciation) and net income are

determined and reported for proprietary fund entities.

4. Fiduciary funds are classified as governmental funds or as proprietary funds depending upon whether or

not their resources must be maintained intact. If the resources of a fiduciary fund may be expected to carry

out its designated activities it is classified as a governmental (expendable) fund entity. If the principal of

the fiduciary fund must be maintained intact it is classified as a proprietary (nonexpendable) fund entity.

5. A disbursement to another fund is treated as a receivable on the records of the fund that makes the

disbursement when the disbursement constitutes an advance or loan to another fund.

A disbursement to another fund is treated as an expenditure on the records of the fund that makes the

disbursement when the disbursement constitutes a quasi-external transaction or a reimbursement. Quasi-

external transactions are interfund transactions that would be treated as revenue, expense or expenditures if

they were consummated with an organization external to the governmental unit. Reimbursements are

transactions which involve the transfer of resources from one fund to another in order to reimburse the

recipient fund for expenditures made by it that are properly expenditures of the reimbursing fund.

All interfund transactions other than quasi-external transactions, reimbursements, and loans or advances

are interfund transfers and are recorded as a transfer to other funds on the records of the fund that makes

the disbursements.

6. Bonds payable may be included in the records of an Enterprise Fund, the government-wide statement of

net assets and under some circumstances in the records of an internal Service Fund.

7. Property and other nonfinancial resources may be included in the records of an Enterprise Fund, an

Internal Service Fund, a nonexpendable Trust Fund and the government-wied statement of net assets.

8. Estimated revenues and appropriations are formally recorded in the records of the General Fund to assist in

the control and administration of general fund expenditures. In particular, the formal recording of

appropriations is intended to assist administrators in complying with specific legal restrictions on the

amount of various classifications of expenditures. Since the resources of a Capital Projects Fund can be

expended for only the single authorized project for which the fund was created, the fund balance itself

serves an adequate measure of and control over unexpended appropriation authority. Thus, there is no

necessity to formally record the budgeted revenue and appropriation for the capital project.

9. Not all major capital facilities acquisitions are accounted for in Capital Projects Funds. Construction or

http://downloadslide.blogspot.com

To download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.comTo download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.com

Chapter 18 Introduction to Accounting for State and Local Governmental Units

18-21

acquisition of capital facilities financed by Enterprise Funds are accounted for in the records of those

funds. In addition, there may be instances in which the resources of the General Fund or a Special Revenue

Fund are appropriated for the acquisition of a major capital facility. So long as such acquisitions do not

involve the issuance of general obligation long-term debt securities, they may be accounted for in the fund

which appropriates the resources rather than in a separate Capital Projects Fund.

10. Unpaid interest on bonds payable incurred since the last payment date is not accrued as an expenditure and

liability of the Debt Service Fund at year end. This exception to expenditure accrual is justified because

financial resources that are appropriated in other funds or from general tax levies for transfer to or receipt

by Debt Service Funds are usually appropriated in the period in which the interest on the debt must be

paid. To accrue the Debt Service Fund expenditure and liability in one year, but record the transfer or

collection of the financial resources appropriated for this purpose in a later year, would be confusing and

potentially misleading.

11. Interfund activity includes the following four items

1. Interfund loans – Interfund loans should be reported as interfund receivables in the lender fund

and as an interfund payable in the borrower fund.

2. Interfund services provided and used – (previously known as quasi-external transactions) sales

and purchases of goods and services between funds for a price approximating their external

exchange value. Interfund services provided and used should be reported as revenues in seller

funds and expenses or expenditures in the purchaser funds. Unpaid amounts should be reported

as interfund receivables and payables in the fund balance sheet or the statement of net assets.

3. Interfund transfers – (formerly known as either residual equity transfers or operating transfers)

flows of assets without an equivalent flow of assets in return and without a requirement for

repayment. In government funds, transfers should be reported as ‘other financing uses’ in the

funds and as ‘other financing sources’ in the funds receiving the transfer. In proprietary funds,

transfers should be reported after non-operating revenues and expenses.

4. Interfund reimbursements – repayments from the funds responsible for the particular expenditure

or expense to the funds that initially paid for them. Reimbursements should not be displayed in

the financial statements.

http://downloadslide.blogspot.com

To download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.comTo download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.com

Test Bank to accompany Jeter and Chaney Advanced Accounting 3rd

Edition

18-22

12. 1. Bonds Payable: F, J, and in some circumstances G.

2. Reserve for Encumbrances; A, B, D, and H.

3. Equipment: F, G, and J

4. Appropriations: A, B, and D.

5. Estimated Revenue; A and B.

6. Property Taxes Receivable; A, B, C, D, H, and J

7. Construction Work in Progress: F, G, and J.

8. Accumulated Depreciation: F, G, H, and J.

9. Depreciation Expense: F, G, H, and J.

10. Required Earnings: C.

13. On the Statement of Net Assets, the primary reconciling items include capital assets and long-term

liabilities. Capital assets used in governmental activities are not financial resources and are not reported

in the funds. Long-term liabilities are not due and payable in the current period and are not reported in

the governmental funds.

In reconciling the net assets, the primary differences are capital expenditures, sales of assets, bond

proceeds, and interest expense. Governmental funds report capital outlays as expenditures while

governmental activities report depreciation expense over the life of the asset. In the statement of

activities, the gain or loss from the sale is reported, while in the governmental funds, the proceeds from

the sale are reported as revenues. Bond proceeds provide current financial resources to government

funds, but issuing debt increases long-term liabilities on the statement of assets. In government funds,

the interest paid is deducted, while in the statement of activities, interest expense is recognized

according to the accrual method.

Business Ethics

Business ethics solutions are merely suggestions of points to address. The objective is to raise the students'

awareness of the topics, and to invite discussion. In most cases, there is clear room for disagreement or

conflicting viewpoints.

1. The current periods financial statements would only reflect the amounts actually paid in the current

period (current financial resources).

2. Under GASB 45, the liability for future amounts to be paid would have to be reported on a present

value basis on the government-wide statement of net assets.

3. Since the actual outlay associated with an increased benefit does not have to be paid in the current

period, the decision defers the economic consequences until a future period.

4. One issue to consider is whether the government is concerned about future fiscal responsibility. If

the debt does not have to be recorded on the books, it might give an unrealistic view of the financial

responsibility for future payments that the government has offered. Also, because in many cases, the

benefits are not guaranteed, there is a likelihood that the benefits might be canceled in the future if

the government can not afford them.

http://downloadslide.blogspot.com

To download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.comTo download more slides, ebook, solutions and test bank, visit http://downloadslide.blogspot.com