Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

41

Copyright © 2002 Pearson Education, Inc. Slide 6-1

-

Upload

arpit-sharma -

Category

Documents

-

view

223 -

download

0

Transcript of Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 1/41

Copyright © 2002 Pearson Education, Inc. Slide 6-1

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 2/41

Copyright © 2002 Pearson Education, Inc. Slide 6-2

CHAPTER 6

Created by, David Zolzer, Northwestern State University—Louisiana

E-commerce Payment Systems

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 3/41

Copyright © 2002 Pearson Education, Inc. Slide 6-3

Learning Objectives

Describe the features of traditionalpayment systems

Discuss the current limitations of onlinecredit card payment systems

Understand the features and functionalityof digital wallets

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 4/41

Copyright © 2002 Pearson Education, Inc. Slide 6-4

Learning Objectives

Describe the features and functionality ofthe major types of digital payment

systems in the B2C arena Describe the features and functionality of

the major types of digital paymentsystems in the B2B arena

Describe the features and functionality ofelectronic billing presentment andpayment systems

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 5/41

Copyright © 2002 Pearson Education, Inc. Slide 6-5

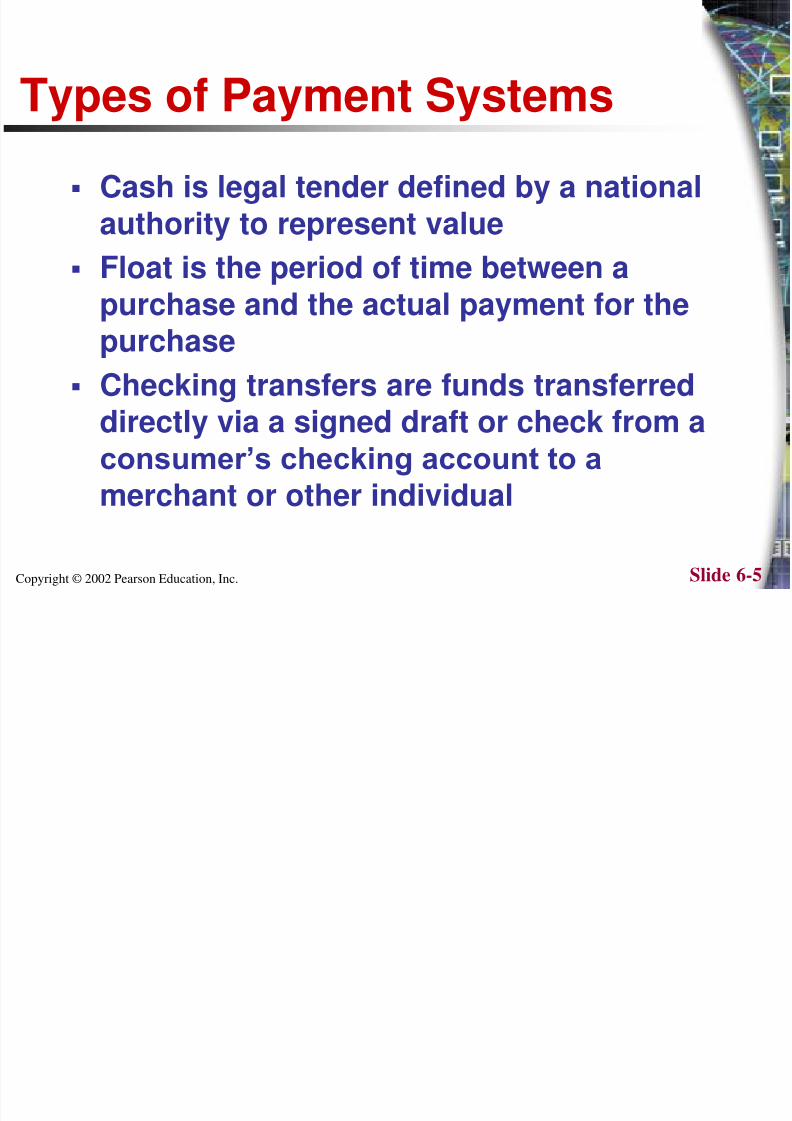

Types of Payment Systems

Cash is legal tender defined by a nationalauthority to represent value

Float is the period of time between apurchase and the actual payment for thepurchase

Checking transfers are funds transferred

directly via a signed draft or check from aconsumer’s checking account to a

merchant or other individual

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 6/41

Copyright © 2002 Pearson Education, Inc. Slide 6-6

Most Common Payment Systems,Based on Number or TransactionsPage 284, Figure 6.1

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 7/41Copyright © 2002 Pearson Education, Inc. Slide 6-7

Most Common Payment Systems,Based on Dollar AmountPage 285, Figure 6.2

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 8/41Copyright © 2002 Pearson Education, Inc. Slide 6-8

Types of Payment Systems

Credit card represent an account that extendscredit to consumers, permits consumers topurchase items while deferring payment, andallows consumers to make payments to multiplevendors at one time

Credit card associations are nonprofitorganizations that set standards for issuingbanks

Issuing banks actually issue credit cards andprocess transactions

Processing centers or clearing houses handleverification of accounts and balances

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 9/41Copyright © 2002 Pearson Education, Inc. Slide 6-9

Types of Payment Systems

Stored value payments systems areaccounts created by depositing funds intoan account and from which funds are paid

out or withdrawn as needed Debit cards immediately debit a checking

or other demand deposit account

Accumulating balance payment systemsare accounts that accumulateexpenditures and to which consumersmake periodic payments

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 10/41Copyright © 2002 Pearson Education, Inc. Slide 6-10

Dimensions of PaymentSystemsPage 288,

Table 6.1

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 11/41Copyright © 2002 Pearson Education, Inc. Slide 6-11

Current E-commerce PaymentSystems

Digital Cash generate a private form ofcurrency that can be spent at e-commerce

sites Online store value systems rely on

prepayments, debit cards, or checkingaccounts to create value in an account

that can be used for e-commerceshopping

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 12/41Copyright © 2002 Pearson Education, Inc. Slide 6-12

Current E-commerce PaymentSystems

Digital accumulating balance payment systemsaccumulate small charges and bill the consumerperiodically. These systems are especially suited

for processing micropayments for digitalaccounts

Digital credit accounts extend the onlinefunctionality of existing credit card paymentsystems

Digital checking systems create digital checks fore-commerce remittances and extend thefunctionality of existing bank checking systems

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 13/41Copyright © 2002 Pearson Education, Inc. Slide 6-13

How an Online Credit CardTransaction WorksPage 292, Figure 6.4

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 14/41Copyright © 2002 Pearson Education, Inc. Slide 6-14

Limitations of Online CreditCard Payment Systems

Security Neither the merchant not the consumer can be

fully authenticated

Merchant Risk Consumers can repudiate charges

Cost Roughly 3.5% of purchase plus transaction fee

Social Equity Young adults do not have credit cards

Almost 100 million adult Americans cannotafford cards or are considered poor risks

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 15/41Copyright © 2002 Pearson Education, Inc. Slide 6-15

SET: Secure ElectronicTransaction Protocol

An open standard for the e-commerceindustry developed and offered by

MasterCard and Visa as a way to facilitateand encourage improved security forcredit card transactions

Uses a digital certificate to verify a

sender’s identity

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 16/41Copyright © 2002 Pearson Education, Inc. Slide 6-16

How SET Transaction WorkPage 295, Figure 6.5

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 17/41Copyright © 2002 Pearson Education, Inc. Slide 6-17

B2C Digital Payment Systems

Digital Wallets

Digital Cash

Online Stored Value Systems Smart Card Stored Value Systems

Digital Accumulating Balance PaymentSystems

Digital Credit Card Payment Systems

Digital Checking Payment Systems

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 18/41Copyright © 2002 Pearson Education, Inc. Slide 6-18

Digital Wallets

Authenticates the consumer through theuse of digital certificates or other

encryption methods, stores and transfersvalue, and secures the payment processfrom the consumer to the merchant

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 19/41Copyright © 2002 Pearson Education, Inc. Slide 6-19

Promised Functionality ofDigital WalletsPage 297, Table 6.2

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 20/41Copyright © 2002 Pearson Education, Inc. Slide 6-20

Types of Digital WalletsPage 298, Figure 6.6

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 21/41Copyright © 2002 Pearson Education, Inc. Slide 6-21

Digital Wallets

Client-based digital wallets are softwareapplications that consumers install on theircomputer, and that offer consumer convenience

by automatically filling out forms at online stores Server-based digital wallets are software-based

authentication and payment services andproducts sold to financial institutions that marketthe systems to merchants either directly or as a

part of their financial service package Electronic Commerce Modeling Language is a

standard of digital wallets

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 22/41Copyright © 2002 Pearson Education, Inc. Slide 6-22

How Microsoft’s Passport

Wallet WorksPage 300, Figure 6.7

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 23/41

Copyright © 2002 Pearson Education, Inc. Slide 6-23

Digital Cash

Also called e-cash

Digital forms of value storage or value

exchange that have limited convertibilityinto other forms of value and requireintermediaries to convert

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 24/41

Copyright © 2002 Pearson Education, Inc. Slide 6-24

Examples of Digital CashPage 302, Table 6.3

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 25/41

Copyright © 2002 Pearson Education, Inc. Slide 6-25

Digicash: How First GenerationDigital Cash WorkedPage 303,

Figure 6.8

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 26/41

Copyright © 2002 Pearson Education, Inc. Slide 6-26

Digital Cash

Online stored value payment systemspermit consumers to make instant, online

payments to merchants and otherindividuals based on value stored in anonline account

Smart cards as store value systems are

based on credit-card-sized plastic cardsthat have embedded chips that storepersonal information

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 27/41

Copyright © 2002 Pearson Education, Inc. Slide 6-27

Online Stored Value SystemsPage 305,

Table 6.4

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 28/41

Copyright © 2002 Pearson Education, Inc. Slide 6-28

How Ecount.com Works: AStored Value SystemPage 305, Figure 6.9

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 29/41

Copyright © 2002 Pearson Education, Inc. Slide 6-29

Digital Accumulating BalancePayment Systems

Allow users to make micropayments andpurchases on the Web, accumulating a

debit balance for which they are billed atthe end of the month

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 30/41

Copyright © 2002 Pearson Education, Inc. Slide 6-30

Digital Accumulating BalancePayment SystemsPage 309, Table 6.5

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 31/41

Copyright © 2002 Pearson Education, Inc. Slide 6-31

Digital Credit Card PaymentSystems

Seek to extend the functionality of existingcredit cards for use as online shopping

payment tools

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 32/41

Copyright © 2002 Pearson Education, Inc. Slide 6-32

Digital Credit Card PaymentSystemsPage 309, Table 6.6

C C

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 33/41

Copyright © 2002 Pearson Education, Inc. Slide 6-33

How a Digital Credit CardPayment System WorksPage 310, Figure 6.10

Di i l Ch ki P

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 34/41

Copyright © 2002 Pearson Education, Inc. Slide 6-34

Digital Checking PaymentSystems

Seek to extend the functionality of existingchecking accounts for use as online

shopping payment tools

Di i l Ch ki P

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 35/41

Copyright © 2002 Pearson Education, Inc. Slide 6-35

Digital Checking PaymentSystemsPage 312, Table 6.7

H Di i l Ch ki W k

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 36/41

Copyright © 2002 Pearson Education, Inc. Slide 6-36

How Digital Checking Works:EcheckPage 313, Figure 6.11

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 37/41

Copyright © 2002 Pearson Education, Inc. Slide 6-37

B2B Payment Systems

More complex than B2C systems

Must link into exist ERP and EDI systems

Two main types Systems that replace traditional banks

Existing banking systems extending to theB2B marketplace

K F t f B2B P t

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 38/41

Copyright © 2002 Pearson Education, Inc. Slide 6-38

Key Features of B2B PaymentSystemsPage 316, Table 6.8

El t i Billi P t ti

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 39/41

Copyright © 2002 Pearson Education, Inc. Slide 6-39

Electronic Billing Presentationand Payment

New forms of online payment systems formonthly bills

Allow consumers to view billselectronically and pay them throughelectronic funds transfers from bank orcredit card accounts

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 40/41

Copyright © 2002 Pearson Education, Inc. Slide 6-40

Growth of EBPP MarketPage 318, Figure 6.12

8/2/2019 Ch_06 (Moiz Husain's Conflicted Copy 2012-03-07)

http://slidepdf.com/reader/full/ch06-moiz-husains-conflicted-copy-2012-03-07 41/41

Types of EBPP SystemsPage 320, Figure 6.13

![Lamb, Marketing 5CE, Chapter 6, Student Handoutcollege.cengage.com/.../11-student_handouts/ch_06.pdf · Title: Microsoft PowerPoint - Ch 06.ppt [Compatibility Mode] Author: StaffOne](https://static.fdocuments.in/doc/165x107/5f5819d31a087a274b0fb3c3/lamb-marketing-5ce-chapter-6-student-title-microsoft-powerpoint-ch-06ppt.jpg)