Ch-4 Production Theory

45

Ch 4 THE THEORY OF PRODUCTION Production theory forms the foundation for the theory of supply Managerial decision making involves four types of production decisions: 1. Whether to pro duce or to shut down 2. How much ou tput t o pr oduce 3. What i nput combi nati on to use 4. What type of technology to use Ch 5 Ch 4

-

Upload

jituhirapara1990 -

Category

Documents

-

view

221 -

download

0

Transcript of Ch-4 Production Theory

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 1/45

Ch 4 THE THEORY OFPRODUCTION

Production theory forms thefoundation for the theory of supply

Managerial decision making involvesfour types of production decisions:

1. Whether to produce or to shut

down

2. How much output to produce

3. What input combination to use

4. What type of technology to use

Ch 5

Ch 4

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 2/45

Production involves transformation

of inputs such as capital,

equipment, labor, and land into

output - goods and services

In this production process, the

manager is concerned with

efficiency in the use of the inputs

- technical vs. economical

efficiency

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 3/45

Two Concepts of Efficiency

Economic efficiency:

occurs when the cost of producing

a given output is as low as possible

Technological efficiency:

occurs when it is not possible to

increase output without increasing

inputs

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 4/45

The objective of efficiency willprovide us with some basic rules

about the manner in which firms

should utilize inputs to produce

goods and services

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 5/45

You will see that basic productiontheory is simply an application of

constrained optimization:the firm attempts either to minimizethe cost of producing a given levelof output

or

to maximize the output attainablewith a given level of cost.

Both optimization problems lead tosame rule for the allocation of inputs and choice of technology

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 6/45

Production Function

A production function is a table or amathematical equation showing themaximum amount of output that can beproduced from any specified set of inputs,

given the existing technology

f 2(x)f

1(x)

f 0(x)

x

Q Improvement of technology

f 0

(x) - f 2

(x)

Q = output

x = inputs

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 7/45

Production Function continued

Q = f(X1, X

2, …, X

k)

where

Q = output

X1, …, X

k= inputs

For our current analysis, let’s reduce theinputs to two, capital (K) and labor (L):

Q = f(L, K)

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 8/45

Production Table

Units of K Employed Output Quantity (Q)

8 37 60 83 96 107 117 127 128

7 42 64 78 90 101 110 119 120

6 37 52 64 73 82 90 97 104

5 31 47 58 67 75 82 89 954 24 39 52 60 67 73 79 85

3 17 29 41 52 58 64 69 73

2 8 18 29 39 47 52 56 52

1 4 8 14 20 27 24 21 17

1 2 3 4 5 6 7 8

Units of L Employed

Same Q can be produced with differentcombinations of inputs, e.g. inputs are substitutable

in some degree

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 9/45

All of these outputs are assumed to

be technically efficient

But which one is economically efficient?

That is the question facing the DM

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 10/45

Types of Production Functions

Production function with one variable

input

Production function with two variable

inputs Production function with all variable

inputs

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 11/45

Short-Run and Long-Run Production

In the short run some inputs are

fixed and some variable

e.g. the firm may be able to vary

the amount of labor, but cannotchange the amount of capital

in the short run we can talk about

factor productivity

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 12/45

In the long run all inputs become

variable e.g. the long run is the period in

which a firm can adjust all inputsto changed conditions

in the long run we can talk aboutreturns to scale (compare latter

with economies of scale, which

is a cost related concept)

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 13/45

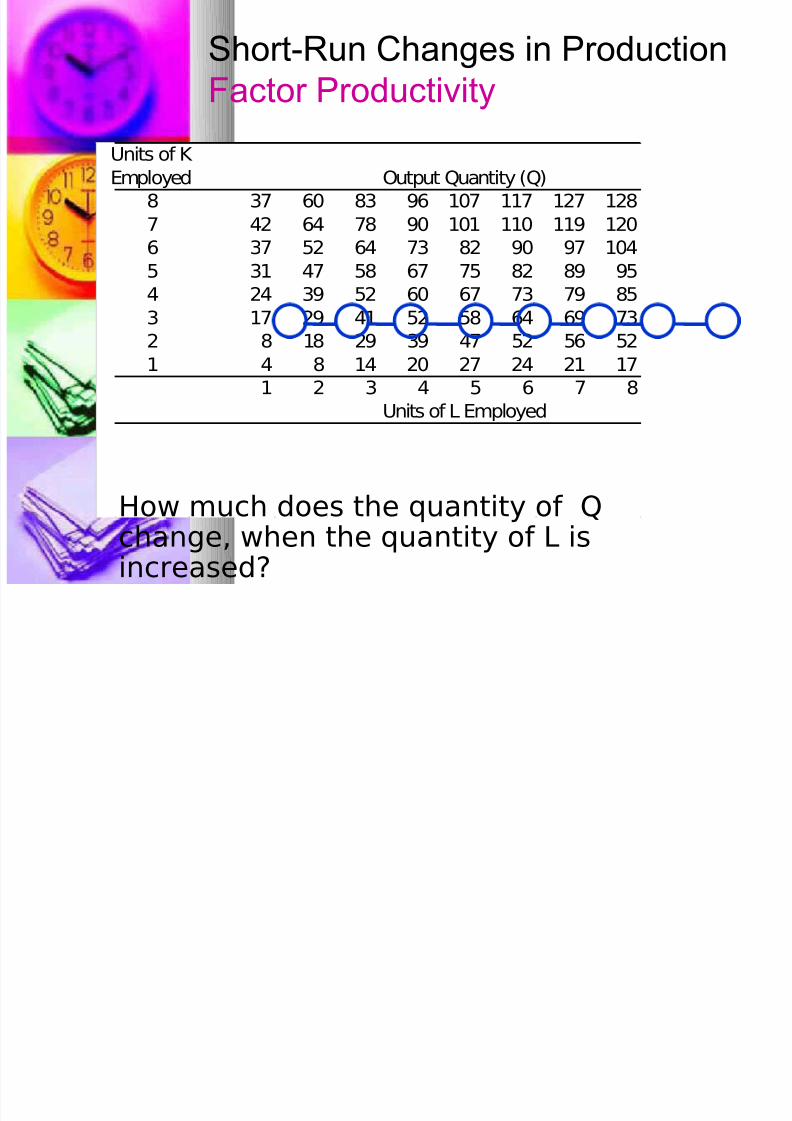

Short-Run Changes in Production

Factor Productivity

Units of K

Employed Output Quantity (Q)

8 37 60 83 96 107 117 127 128

7 42 64 78 90 101 110 119 120

6 37 52 64 73 82 90 97 104

5 31 47 58 67 75 82 89 954 24 39 52 60 67 73 79 85

3 17 29 41 52 58 64 69 73

2 8 18 29 39 47 52 56 52

1 4 8 14 20 27 24 21 17

1 2 3 4 5 6 7 8

Units of L Employed

How much does the quantity of Q

change, when the quantity of L isincreased?

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 14/45

Long-Run Changes in Production

Returns to Scale

Units of K

Employed Output Quantity (Q)

8 37 60 83 96 107 117 127 128

7 42 64 78 90 101 110 119 120

6 37 52 64 73 82 90 97 104

5 31 47 58 67 75 82 89 954 24 39 52 60 67 73 79 85

3 17 29 41 52 58 64 69 73

2 8 18 29 39 47 52 56 52

1 4 8 14 20 27 24 21 17

1 2 3 4 5 6 7 8

Units of L Employed

How much does the quantity of Q change,when the quantity of both L and K is

increased?

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 15/45

Relationship Between Total, Average,and Marginal Product: Short-Run

Analysis

Total Product (TP) = total quantity of

output

Average Product (AP) = total product

per total input

Marginal Product (MP) = change in

quantity when one additional unit of

input used

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 16/45

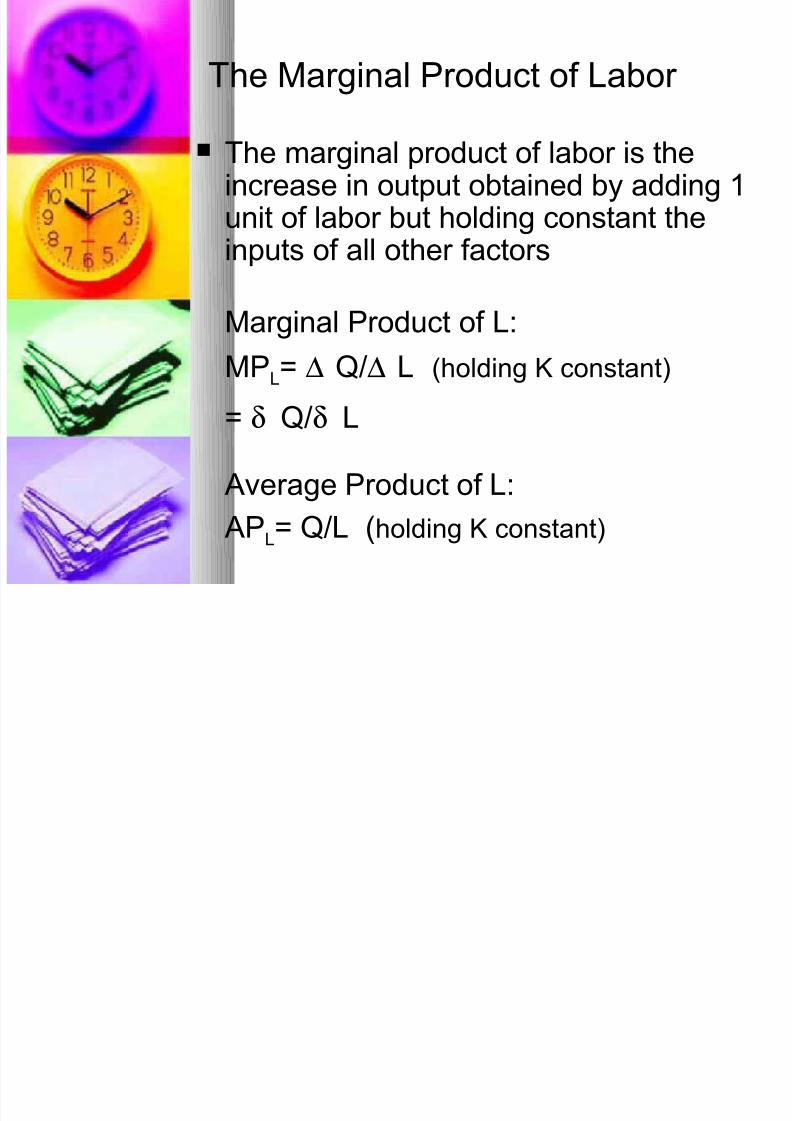

The Marginal Product of Labor

The marginal product of labor is theincrease in output obtained by adding 1unit of labor but holding constant theinputs of all other factors

Marginal Product of L:

MPL= ∆ Q/∆ L (holding K constant)

= δ Q/δ L

Average Product of L:

APL= Q/L (holding K constant)

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 17/45

Short-Run Analysis of Total,Average, and Marginal Product

If MP > AP thenAP is rising

If MP < AP thenAP is falling

MP = AP when APis maximized

TP maximizedwhen MP = 0

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 18/45

Law of Diminishing Returns(Diminishing Marginal Product)

Holding all factors constant except one, thelaw of diminishing returns says that:

As additional units of a variable input arecombined with a fixed input, at some pointthe additional output (i.e., marginalproduct) starts to diminish e.g. trying to increase labor input without

also increasing capital will bringdiminishing returns

Nothing says when diminishing returns willstart to take effect, only that it will happenat some point

All inputs added to the production processare exactly the same in individual

productivity

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 19/45

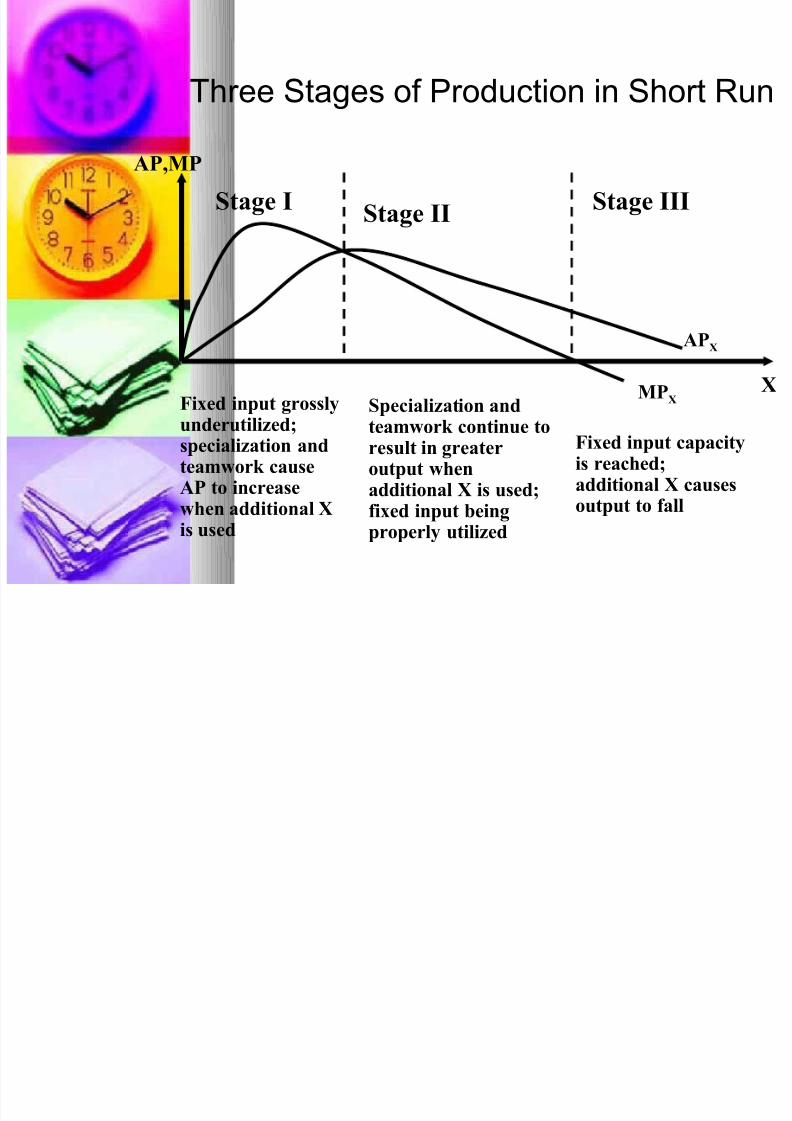

Three Stages of Production in Short Run

AP,MP

X

Stage IStage II

Stage III

APX

MPX

Fixed input grosslyunderutilized;specialization andteamwork causeAP to increasewhen additional Xis used

Specialization andteamwork continue toresult in greateroutput whenadditional X is used;fixed input beingproperly utilized

Fixed input capacityis reached;additional X causesoutput to fall

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 20/45

Stage-1 Stage-2 Stage-3Qu

a

n

ti

t

y

Input-L

L1 L2 L3

TP

MP

AP

Increasing

Return

Decreasing

Return

NegativeReturn

Stage-2 is rational and Stage-1 and 3 are irrational

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 21/45

How to Determine the OptimalInput Usage

We can find the answer to this fromthe concept of derived demand

The firm must know how many units of output it could sell, the price of theproduct, and the monetary costs of employing various amounts of theinput L

Let us for now assume that the firm isoperating in a perfectly competitivemarket for its output and its input

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 22/45

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 23/45

Optimal Decision Rule:

A profit maximizing firm operating in

perfectly competitive output and input

markets will be using optimal amount

of an input at the point at which themonetary value of the input’s marginal

product is equal to the additional cost

of using that input (L)

- in other words, when MRP = MLC

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 24/45

Production in the Long-Run

All inputs are now considered to be

variable (both L and K in our case) How to determine the optimal

combination of inputs?

To illustrate this case we will use productionisoquants.

An isoquant is a curve showing all possible

combinations of inputs physically capable of

producing a given fixed level of output.

It is also known as Iso-Product Curve, Equal

Product Curve, Production Indifference Curve

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 25/45

Example 2 Production Table

Units of K

Employed Output Quantity (Q)

8 37 60 83 96 107 117 127 128

7 42 64 78 90 101 110 119 120

6 37 52 64 73 82 90 97 1045 31 47 58 67 75 82 89 95

4 24 39 52 60 67 73 79 85

3 17 29 41 52 58 64 69 73

2 8 18 29 39 47 52 56 52

1 4 8 14 20 27 24 21 171 2 3 4 5 6 7 8

Units of L

IsoquantUnits of K Employed

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 26/45

An Isoquant

Graph of Isoqua

0

1

2

3

4

5

6

7

1 2 3 4 5 6 7X

Y

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 27/45

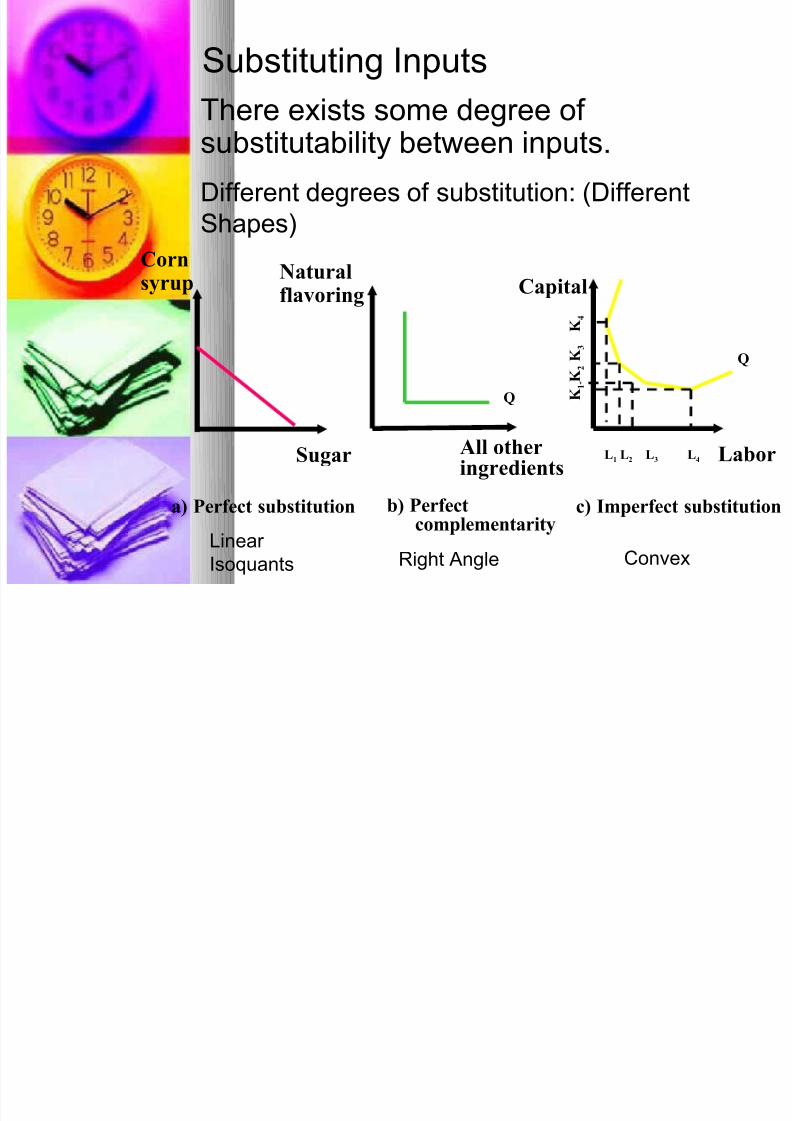

Substituting Inputs

There exists some degree of

substitutability between inputs.

Different degrees of substitution: (Different

Shapes)

Sugar

a) Perfect substitution b) Perfectcomplementarity

All otheringredients

Naturalflavoring

Q

Q

Capital

LaborL1 L2 L3 L4

K1

K2

K3

K4

Corn

syrup

c) Imperfect substitution

Linear

Isoquants Right Angle Convex

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 28/45

Substituting Inputs continued

In case the two inputs are

imperfectly substitutable, theoptimal combination of inputs

depends on the degree of

substitutability and on the relative

prices of the inputs

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 29/45

Substituting Inputs continued

The degree of imperfection insubstitutability is measured with marginalrate of technical substitution (MRTS):

MRTS = ∆ L/∆ K

(in this MRTS some of L is removed from

the production and substituted by K tomaintain the same level of output)

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 30/45

Law of Diminishing Marginal Rateof Technical Substitution:

Table 7.8 Input Combinatio

for Isoquant Q = 52

C ombination L K

A 6 2

B 4 3

C 3 4

D 2 6

E 2 8

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 31/45

Law of Diminishing Marginal Rate of Technical Substitution continued

0

1

2

3

4

5

6

7

2 3 4 6 8X

Y

∆ X = 2∆ Y = -1

∆ X = 1

∆ Y = -1

∆ X = 1

∆Y =- 2

A

BC

DE

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 32/45

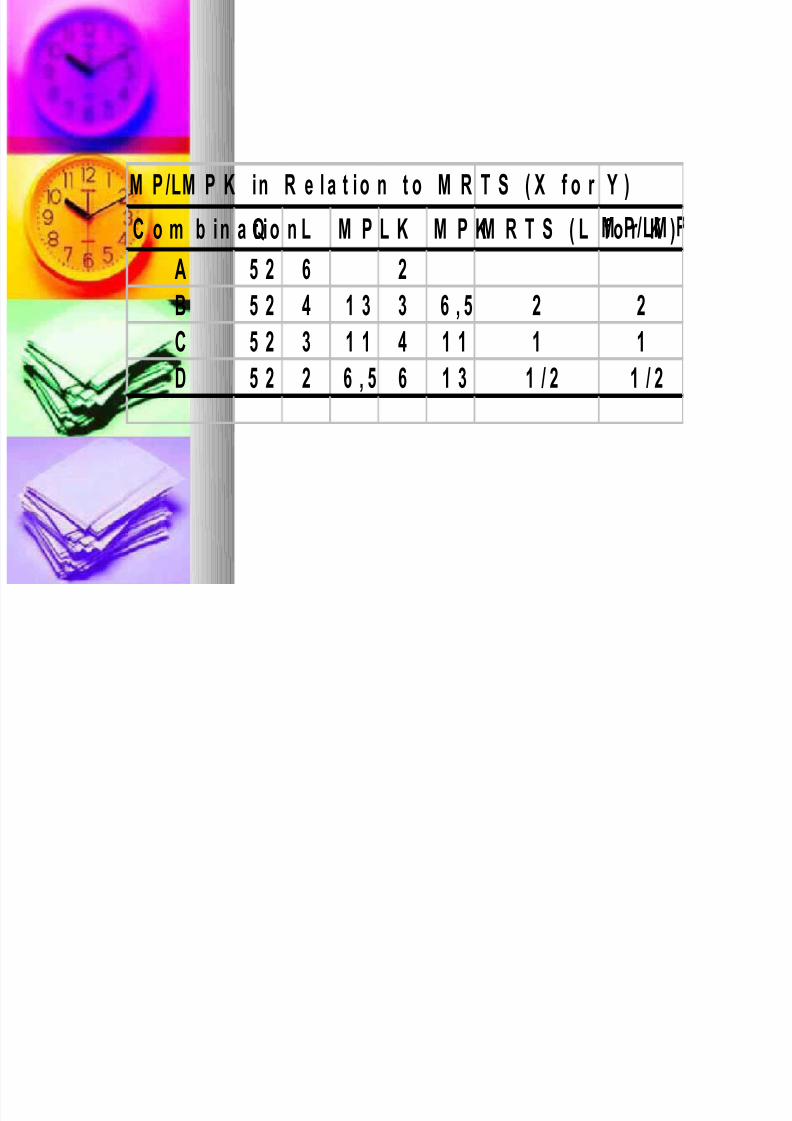

MRTS = ∆ L/ ∆ K = - MP L /MP K

Units of K

Employed Output Quantity (Q)

8 37 60 83 96 107 117 127 128

7 42 64 78 90 101 110 119 120

6 37 52 64 73 82 90 97 1045 31 47 58 67 75 82 89 95

4 24 39 52 60 67 73 79 85

3 17 29 41 52 58 64 69 73

2 8 18 29 39 47 52 56 52

1 4 8 14 20 27 24 21 171 2 3 4 5 6 7 8

Units of L

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 33/45

M P L/ M P K in R e l a t i o n t o M R T S ( X f o r Y )

C o m b i n a t i o nQ L M P L K M P KM R T S ( L f o r K )M P L/ M

A 5 2 6 2B 5 2 4 1 3 3 6 , 5 2 2

C 5 2 3 1 1 4 1 1 1 1

D 5 2 2 6 , 5 6 1 3 1 / 2 1 / 2

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 34/45

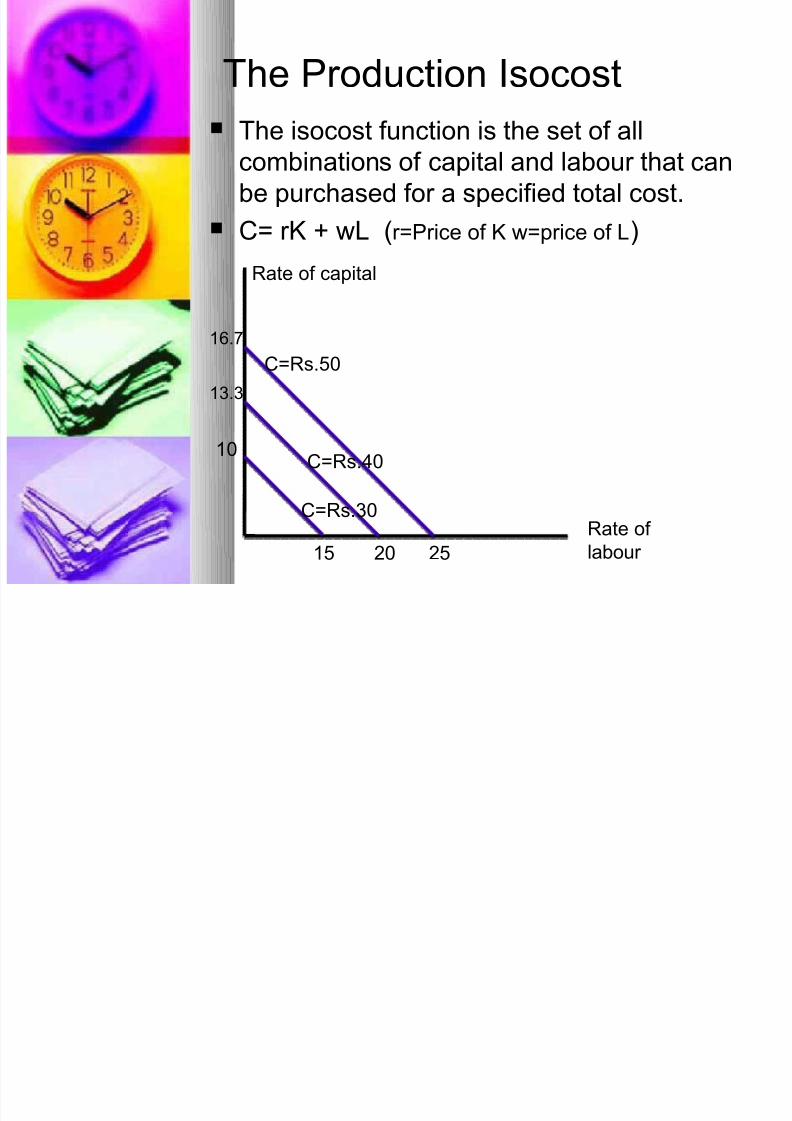

The Production Isocost

The isocost function is the set of allcombinations of capital and labour that can

be purchased for a specified total cost.

C= rK + wL (r=Price of K w=price of L)

Rate of capital

Rate of

labour

16.7

13.3

10

15 20 25

C=Rs.50

C=Rs.40

C=Rs.30

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 35/45

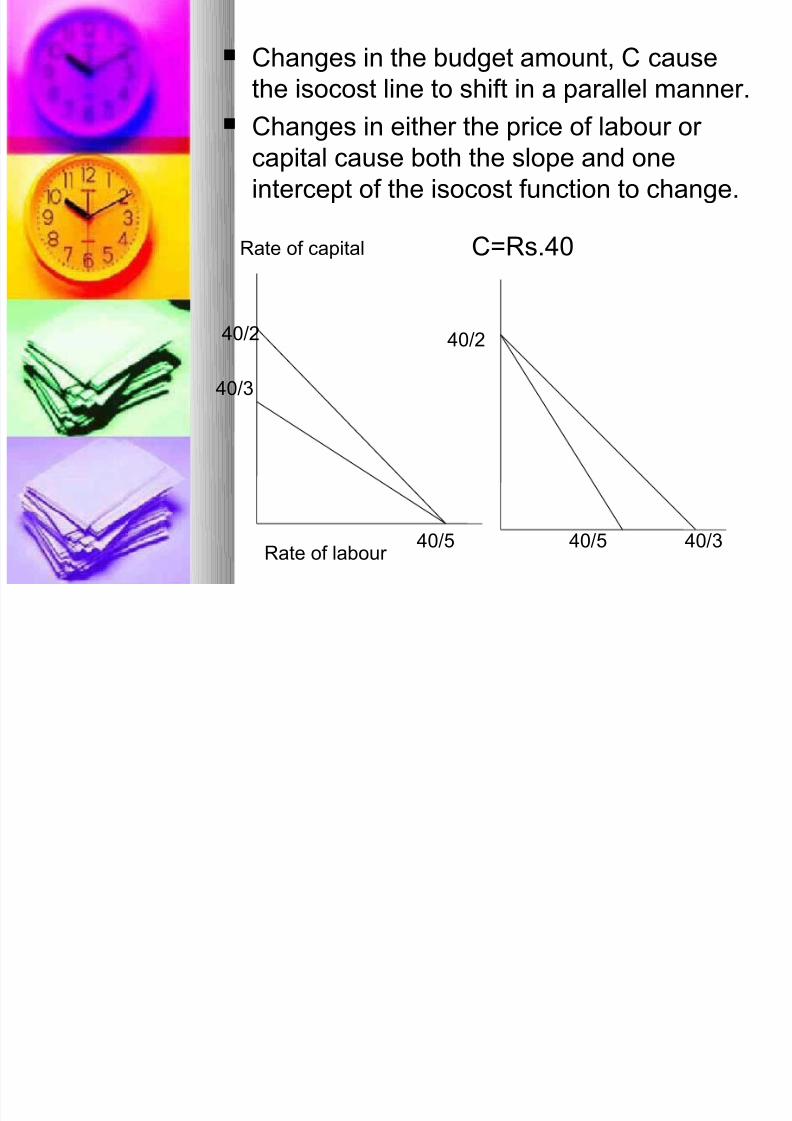

Changes in the budget amount, C cause

the isocost line to shift in a parallel manner.

Changes in either the price of labour or

capital cause both the slope and one

intercept of the isocost function to change.

Rate of capital

Rate of labour

C=Rs.40

40/2

40/3

40/5

40/2

40/5 40/3

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 36/45

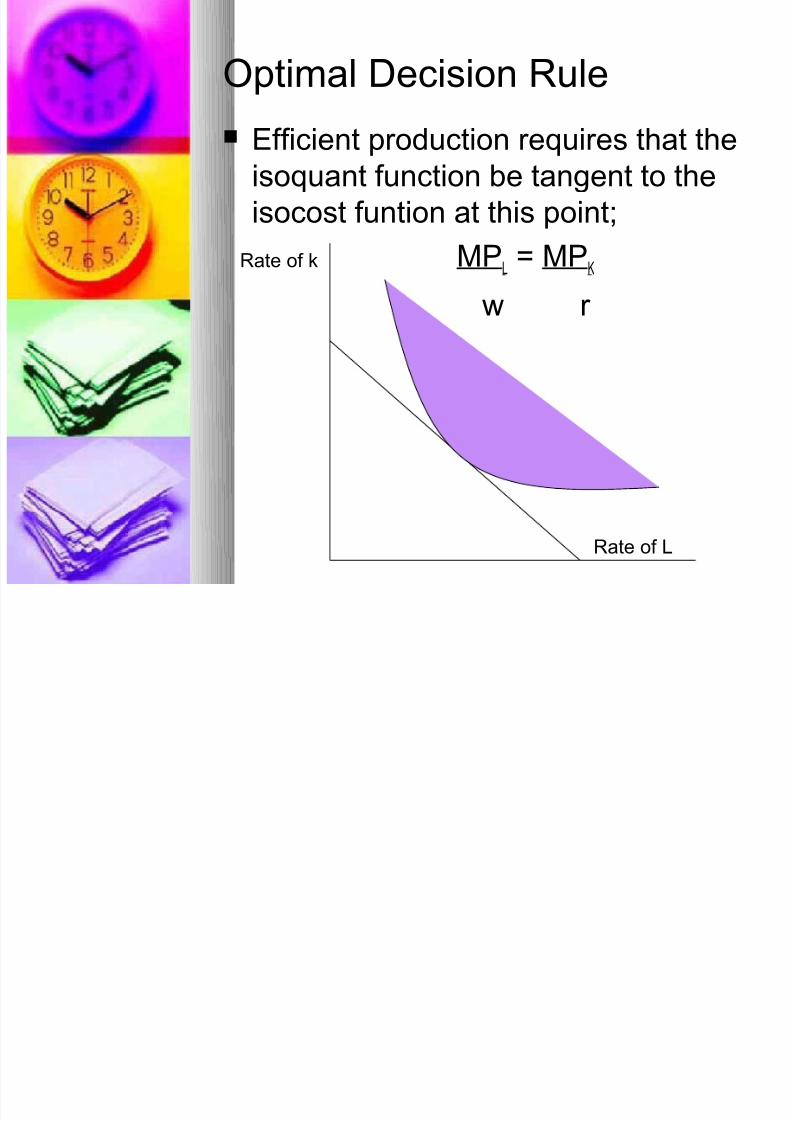

Optimal Decision Rule

Efficient production requires that theisoquant function be tangent to the

isocost funtion at this point;

MPL= MP

K

w r

Rate of L

Rate of k

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 37/45

Optimal Decision Rule

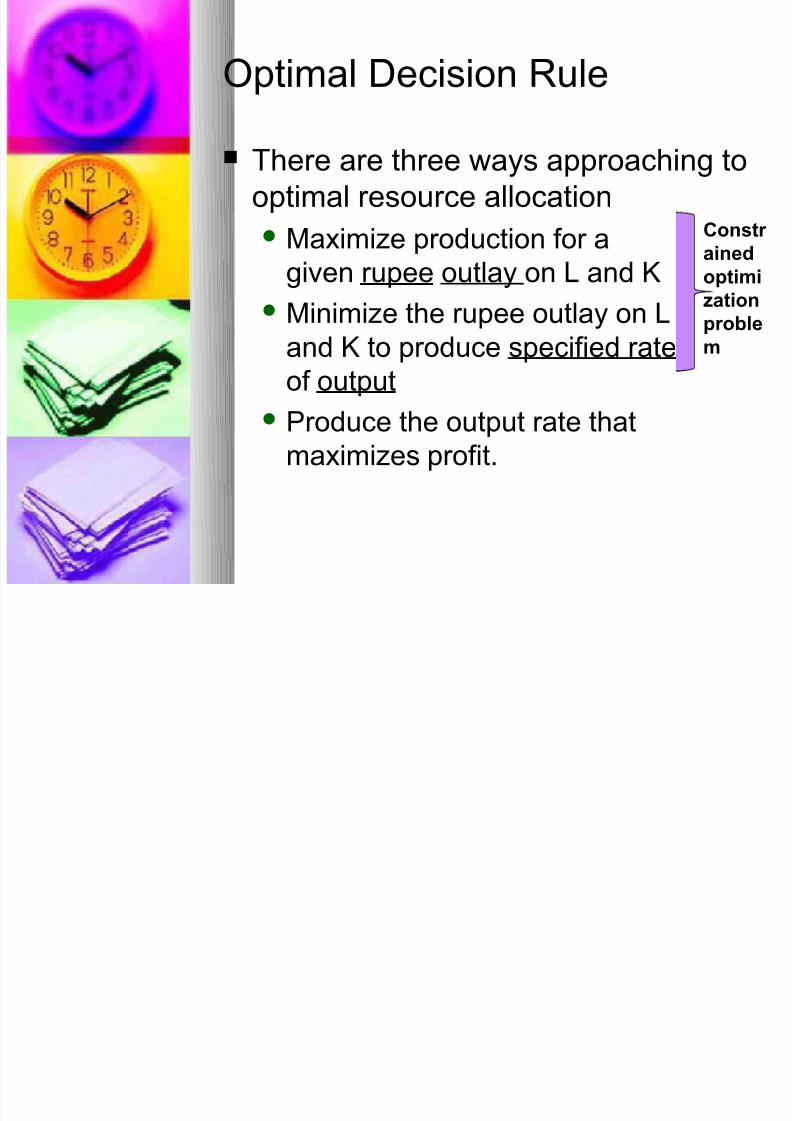

There are three ways approaching to

optimal resource allocation

Maximize production for a

given rupee outlay on L and KMinimize the rupee outlay on L

and K to produce specified rate

of output

Produce the output rate thatmaximizes profit.

Constr

ained

optimization

proble

m

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 38/45

Optimal Decision Rule

a

b

c

d

Rs.100

Rs.150

20

10

Rate of K

Rate of L

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 39/45

Optimal decision Rule

If the condition for efficient

production is not met, there is some

way to substitute one input for the

other that will result in an increase atno change in total cost.

Profit maximization requires that

inputs be hired until MRPK=r and

MRPL=w

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 40/45

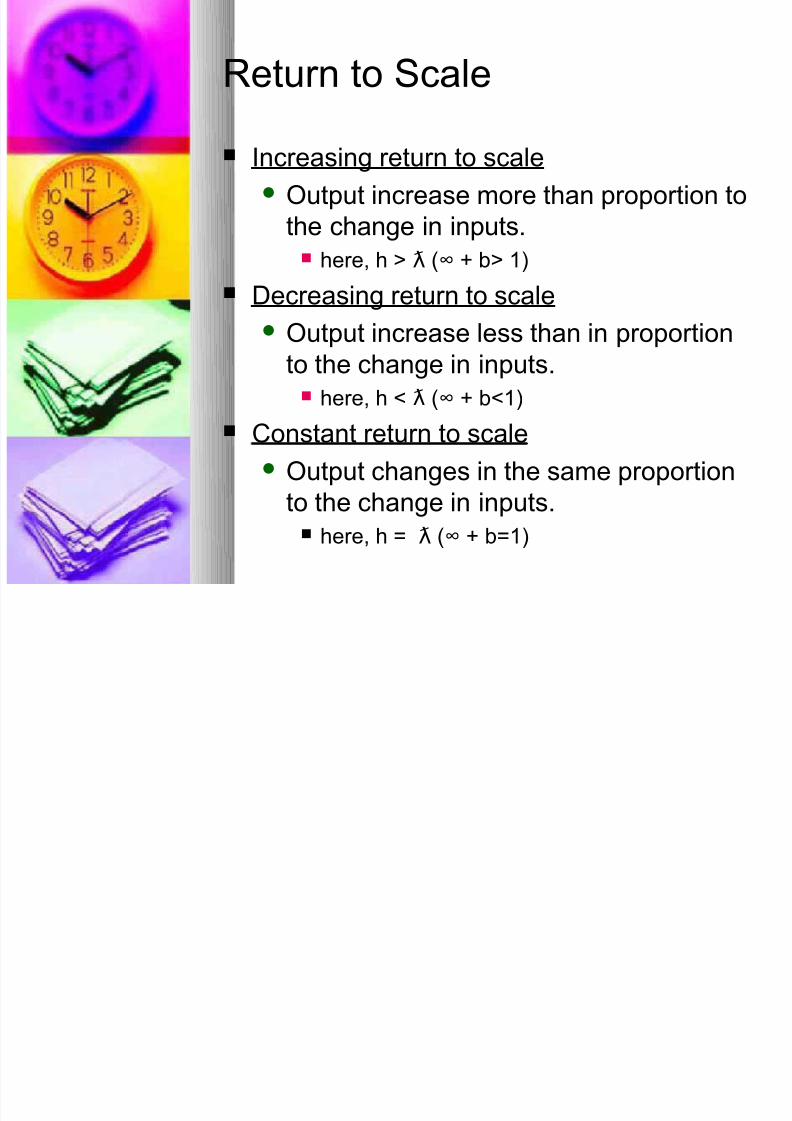

Economies of Scale

Economies of ScaleA given rate of input of K and L

defines the scale of production.

Change in Scale

Proportionate changes in both inputs

Return to scale

The magnitude of the change in the

rate of output relative to the change inscale.

For eg. P.F. is Q= f(K,L) then

hQ= f( K, L)ƛ ƛh factor change in output when ƛ factor change in both variable

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 41/45

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 42/45

Sources of Economies of

Scale

Reasons for increase

in ROS

Technologies Specialization of

labour

Inventory economy

(increase or replacement)

Reasons for decrease

in ROS

Poor mgt. with thegrowth of the firm.

Transportation cost

Employing large no.

of local labour force.

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 43/45

Economies of Scope

It refers to per-unit cost reductions

that occur when a firm produces two

or more products instead of just one.

Firm can make use of its;Excess capacity

Unique skill or comparative

advantage in marketing to develop

complementary products.

For eg. :- P&G sells all kinds of cleaning

products as well some are complementary such

as laundry det., bleach, and fabric softeners.

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 44/45

Measure of economies of scale

S =TC(QA) + TC(QB) – TC(QA,QB)

TC(QA,QB)

8/6/2019 Ch-4 Production Theory

http://slidepdf.com/reader/full/ch-4-production-theory 45/45

Estimating production function