CFTC and SEC Finalize Product Definitions Rules under...

33

Joint Rulemaking on the Definition of Product Terms Under Title VII July 31, 2012 CFTC and SEC Finalize Product Definitions Rules under Title VII of the Dodd-Frank Act Key Takeaways: > The CFTC and the SEC significantly clarified the scope of the definitions of “swap,” “security- based swap” and “mixed swap” under Title VII of the Dodd-Frank Act. > Traditional insurance products that satisfy criteria established for a safe harbor are outside of the scope of Title VII, as are insurance agreements entered into before the effective date of the product definitions rules and the providers of which meet certain criteria. > Guarantees of swaps are part of swaps while guarantees of security-based swaps are not part of security-based swaps or treated as separate security-based swaps. > Many types of consumer products (e.g., mortgages, consumer loans) and commercial agreements (e.g., employment agreements, distribution contracts) which might otherwise fit within the broad statutory definition of “swap” are exempted from the reach of Title VII. > Loan participations that “reflect” an ownership interest in the underlying loan will not be considered swaps or security-based swaps, provided that they meet certain criteria. Both LSTA- and LMA-style loan participations should be outside of Title VII. > The Commissions provided significant guidance regarding the statutory forward contract exclusion in the definition of “swap.” The CFTC affirmed that it would apply the existing precedent in conducting a “facts and circumstances” analysis of whether a forward contract was outside the scope of Title VII. It also expanded an existing interpretation permitting parties to a forward contract to “book-out” the delivery requirement without upsetting the contract’s status as exempt. The CFTC provided guidance on whether a forward contract with embedded optionality would be within Title VII’s reach. > Many types of foreign exchange derivatives are “swaps,” though some physically settled FX products may be exempted from certain aspects of Title VII by the Secretary of the Treasury. > The Commissions clarified that swaptions, forward swaps, forward rate agreements, contracts for differences and commodity options are all “swaps” under Title VII. > The Commissions provided extensive guidance on whether a particular instrument is considered a swap, a security-based swap or a mixed swap. Such determinations are made prior to execution and, subject to certain exceptions, status generally does not change during the contract’s life. > Derivatives overlying interest or monetary rates are generally swaps while derivatives overlying yields on securities (other than certain exempt securities) are generally security- based swaps. Contents Introduction ........................................... 2 Background ..................................... 2 The Product Definitions Rule .......... 3 Statutory definitions of swap, security- based swap and mixed swap ............... 3 Swap ............................................... 3 Security-based swap ....................... 4 Mixed swap ..................................... 4 Which products are outside Title VII notwithstanding broad statutory definitions? ........................................... 4 Insurance products.......................... 5 Insurance Safe Harbor .................... 6 Insurance Grandfathering ............... 6 Consumer and commercial agreements ..................................... 8 Loan participations ........................ 10 Forward contracts ......................... 10 Which products are within Title VII’s reach? ................................................. 14 Foreign exchange products .......... 14 Guarantees of Title VII Derivatives 15 Swaptions, forward swaps, forward rate agreements and contracts for differences ..................................... 15 How to know if a Title VII Derivative is a swap, SBS or MS? ............................. 16 Rates vs. yields ............................. 16 Treatment of total return swaps containing references to interest rates .............................................. 17 Typical TRS scenario – SBS (single share) ............................................ 17 TRS – MS scenario (single share with unrelated currency exposure) 17 ....................................................... 17 Derivatives overlying futures ......... 18 Narrow-Based Security Indexes ... 18 Index CDS ..................................... 20 How are mixed swaps treated? .......... 22 Obtaining guidance as to a particular transaction’s status?........................... 23 Anti-Evasion Rules ............................. 23 What happens next? .......................... 24 Final reflections .................................. 24 Appendix 1.......................................... 27 Appendix 2.......................................... 32

Transcript of CFTC and SEC Finalize Product Definitions Rules under...

Joint Rulemaking on the Definition of Product Terms Under Title VII

July 31, 2012

CFTC and SEC Finalize Product Definitions Rules under Title VII of the Dodd-Frank Act

Key Takeaways:

> The CFTC and the SEC significantly clarified the scope of the definitions of “swap,” “security-

based swap” and “mixed swap” under Title VII of the Dodd-Frank Act.

> Traditional insurance products that satisfy criteria established for a safe harbor are outside of

the scope of Title VII, as are insurance agreements entered into before the effective date of

the product definitions rules and the providers of which meet certain criteria.

> Guarantees of swaps are part of swaps while guarantees of security-based swaps are not

part of security-based swaps or treated as separate security-based swaps.

> Many types of consumer products (e.g., mortgages, consumer loans) and commercial

agreements (e.g., employment agreements, distribution contracts) which might otherwise fit

within the broad statutory definition of “swap” are exempted from the reach of Title VII.

> Loan participations that “reflect” an ownership interest in the underlying loan will not be

considered swaps or security-based swaps, provided that they meet certain criteria. Both

LSTA- and LMA-style loan participations should be outside of Title VII.

> The Commissions provided significant guidance regarding the statutory forward contract

exclusion in the definition of “swap.” The CFTC affirmed that it would apply the existing

precedent in conducting a “facts and circumstances” analysis of whether a forward contract

was outside the scope of Title VII. It also expanded an existing interpretation permitting

parties to a forward contract to “book-out” the delivery requirement without upsetting the

contract’s status as exempt. The CFTC provided guidance on whether a forward contract

with embedded optionality would be within Title VII’s reach.

> Many types of foreign exchange derivatives are “swaps,” though some physically settled FX

products may be exempted from certain aspects of Title VII by the Secretary of the Treasury.

> The Commissions clarified that swaptions, forward swaps, forward rate agreements, contracts

for differences and commodity options are all “swaps” under Title VII.

> The Commissions provided extensive guidance on whether a particular instrument is

considered a swap, a security-based swap or a mixed swap. Such determinations are made

prior to execution and, subject to certain exceptions, status generally does not change during

the contract’s life.

> Derivatives overlying interest or monetary rates are generally swaps while derivatives

overlying yields on securities (other than certain exempt securities) are generally security-

based swaps.

Contents Introduction ........................................... 2

Background ..................................... 2 The Product Definitions Rule .......... 3

Statutory definitions of swap, security-based swap and mixed swap ............... 3

Swap ............................................... 3 Security-based swap ....................... 4 Mixed swap ..................................... 4

Which products are outside Title VII notwithstanding broad statutory definitions? ........................................... 4

Insurance products .......................... 5 Insurance Safe Harbor .................... 6 Insurance Grandfathering ............... 6 Consumer and commercial agreements ..................................... 8 Loan participations ........................ 10 Forward contracts ......................... 10

Which products are within Title VII’s reach? ................................................. 14

Foreign exchange products .......... 14 Guarantees of Title VII Derivatives 15 Swaptions, forward swaps, forward rate agreements and contracts for differences ..................................... 15

How to know if a Title VII Derivative is a swap, SBS or MS? ............................. 16

Rates vs. yields ............................. 16 Treatment of total return swaps containing references to interest rates .............................................. 17 Typical TRS scenario – SBS (single share) ............................................ 17 TRS – MS scenario (single share with unrelated currency exposure) 17 ....................................................... 17 Derivatives overlying futures ......... 18 Narrow-Based Security Indexes ... 18 Index CDS ..................................... 20

How are mixed swaps treated? .......... 22 Obtaining guidance as to a particular transaction’s status?........................... 23 Anti-Evasion Rules ............................. 23 What happens next? .......................... 24 Final reflections .................................. 24 Appendix 1.......................................... 27 Appendix 2.......................................... 32

Joint Rulemaking on the Definition of Product Terms Under Title VII 2

> The Commissions established criteria for determining whether an index credit default swap

will be considered a swap or a security-based swap, establishing tests based on the number

or concentration of the underlying index’s components and the amount of public information

available about such components.

> The Commissions adopted procedures that will allow market participants to obtain

determinations from the Commissions as to whether a particular agreement is a swap, a

security-based swap or a mixed swap.

> The CFTC adopted (and provided guidance concerning) anti-evasion rules that treat as swaps

transactions that are willfully structured to evade Title VII while the SEC declined to adopt any

such rules, instead relying on existing anti-fraud and anti-manipulation provisions of the

federal securities laws that are applicable to security-based swaps.

Introduction

Background

Under Title VII of the Dodd-Frank Wall Street Reform and Consumer Protection

Act (the “Dodd-Frank Act”),1 the Securities and Exchange Commission’s (the

“SEC”) and the Commodity Futures Trading Commission’s (the “CFTC,” together

with the SEC, the “Commissions”) regulatory authority over derivatives and

related matters is keyed to particular product categories. The CFTC has

authority over “swaps.” The SEC has authority over “security-based swaps”

(“SBSs”).2 The Commissions share jurisdiction over mixed swaps (“MSs”).

3

These terms permeate nearly all of Title VII’s operative provisions and their

scope dictates not only which agency regulates a given product, but also whether

a particular product will be subject to regulation under Title VII at all.

Understanding the parameters of these terms is critical in analyzing and

understanding virtually every aspect of Title VII and the rules thereunder. Indeed,

this is why so much of the timing for various compliance requirements has been

keyed to the final entity definitions rule previously adopted by the Commissions

(the “Entity Definitions Rule”)4 and the final product definitions rule (the

“Product Definitions Rule”), which is the subject of this note.5

1 Pub. L. 111-4173, 124 Stat. 1376 (2010).

2 Authority over “security-based swap agreements” (“SBSAs”) is split, though in a different manner

than is applicable to MSs. An SBSA is an agreement of which “a material term is based on the price, yield, value or volatility of any security or any group or index of securities, including any interest therein,” but which is not an SBS. For instance, swaps overlying a broad-based index of securities or swaps overlying U.S. treasuries (which are exempted securities under the federal securities laws) are SBSAs. The CFTC has general regulatory and enforcement authority over SBSAs, but the SEC also has antifraud and certain other authority. The Commissions emphasized that SBSAs will only be subject to the books and records requirements applicable to swaps under CFTC rules. Product Definitions Rule at 320-24.

3 Dodd-Frank Act § 712(a)(8).

4 See Noah Melnick, Caird Forbes-Cockell, Jeff Cohen, Robin Maxwell & Jacques Schillaci, CFTC

and SEC Finalize a Key Piece of the Dodd-Frank Act Registration Requirements Puzzle with the Final Entity Definitions Rules, but Many Pieces of the Puzzle Remain Missing, 32 Future & Derivatives L. Rep’t 15 (June 2012).

5 Among other things, swap dealers (“SDs”) and major swap participants (“MSPs”) must register with

the CFTC by no later than the effective date of the Product Definitions Rule. The SEC has yet to adopt regulations on the registration of security-based swap dealers and major security-based swap participants, and so no registration timetable is available for such entities.

Joint Rulemaking on the Definition of Product Terms Under Title VII 3

The statutory definitions of swap, SBS and MS are exceptionally broad although

they do include some carve-outs and contemplate other carve-outs to be effected

by way of rulemaking. Nevertheless, in light of the requirement for rules further

defining them and the Commissions being empowered to adopt regulations

affecting them,6 there has been significant debate about their scope since the

Dodd-Frank Act was first enacted.

The Product Definitions Rule

In separate votes held on July 6 and July 10, 2012, the SEC and the CFTC,

respectively, approved a final version of the Product Definitions Rule.7 While Title

VII of the Dodd-Frank Act defines many of these terms, it also requires, in some

cases, the Commissions to adopt regulations “further defining” various terms and,

in other cases, permits them to do so. A previous advanced notice of rulemaking

and notice of proposed rulemaking shed some light on the Commissions'

thinking, but only with the adoption of the final Product Definitions Rule is their

approach clear. Among other things, the Product Definitions Rule provides

guidance on whether certain types of agreements and transactions are within or

outside the definitions of swap and SBS, and provides rules and guidance to help

identify MSs.

This note summarizes the key components of the Product Definitions Rule, but

we begin by discussing the statutory definitions of swap, SBS and MS to provide

the proper context in which to understand the Product Definitions Rule since it

largely comprises a narrowing of the statutory definitions of swap and SBS. For

ease of reference, we have included the full text of the statutory definitions of

swap and SBS, as well as MS, in Appendices 1 and 2, respectively.

Statutory definitions of swap, security-based swap and mixed

swap

Swap

Title VII’s statutory definition of the term “swap” is very broad. The statute

enumerates a number of specific types of derivative products that are within the

definition of “swap,” and includes in the term’s definition any agreement “that is,

or in the future becomes, commonly known to the trade as a swap.” In addition,

the statute defines “swap” to include any contract or transaction that provides for

payment “that is dependent on the occurrence, nonoccurrence, or the extent of

the occurrence of an event or contingency associated with a potential financial,

economic, or commercial consequence.”8 This includes, among other things,

credit default swaps on broad-based indices, various other credit derivatives,

most interest rate swaps and currency swaps. SBSs are generally excluded from

6 Dodd-Frank Act § 712(d)(1).

7 Further Definition of “Swap,” “Security-Based Swap,” and “Security-Based Swap Agreement”;

Mixed Swaps; Security-Based Swap Agreement Recordkeeping, available at http://www.cftc.gov/ucm/groups/public/@newsroom/documents/file/federalregister071012c.pdf.

8 Dodd-Frank Act § 721(a)(21). See Appendices 1 and 2 hereto.

Joint Rulemaking on the Definition of Product Terms Under Title VII 4

the definition of “swap” with the exception of MSs, which constitute both swaps

and SBSs. See Appendices 1 and 2 for the full text of the statutory definitions of

these terms.

Security-based swap

SBS is defined as a transaction or contract that would be a swap except that it

overlies a security, loan, narrow-based security index or the occurrence of an

event related to a single issuer of securities or a narrow-based index of securities

issuers.9 For example, single-name credit default swaps (“CDSs”), index CDS

overlying a narrow-based index and total return swaps (“TRSs”) overlying

individual equities are SBSs. See Appendices 1 and 2 for the full text of the

statutory definitions of these terms.

Mixed swap

Under Title VII, an MS is an SBS that is also based on rates, commodities,

currencies and other asset classes or reference subject matter that typically

underlie swaps.10

Although SBSs are generally carved-out of the definition of

“swap,” MSs are exceptions to that carve-out and constitute both SBSs and

swaps. See Appendices 1 and 2 for the full text of the statutory definitions of

these terms.

Which products are outside Title VII notwithstanding broad

statutory definitions?

As the Commissions observed, the definitions of “swap” and SBS (any swap,

SBS or MS, a “Title VII Derivative”) could be read to include a number of

agreements and financial products that have not historically been considered

swaps, SBSs or MSs, including many insurance, consumer and commercial

transactions.11

The Product Definitions Rule explicitly exempts a number of such

transactions from those definitions. The Product Definitions Rule also provides

guidance on the treatment of forward contracts under Title VII, specifically

regarding what types of contracts involve the forward sale of a “nonfinancial

commodity” for physical settlement such that they will be outside of the “swap”

definition, as well as guidance concerning security forwards, loan participations

and various other products.

9 Dodd-Frank Act § 761(a)(6).

10 See 7 U.S.C. § 1a(47)(D); 15 U.S.C. § 78c(a)(68)(D).

11 Product Definitions Rule at 16-17.

Joint Rulemaking on the Definition of Product Terms Under Title VII 5

Examples of products and transactions exempted from Title VII

(each as discussed in more detail below)

> Insurance products that meet certain criteria (or are on a list adopted by the

Commissions) the providers of which satisfy certain requirements

> A broad array of consumer products and transactions (e.g., mortgages,

consumer loans, etc.)

> A number of commercial transactions (e.g., employment agreements, leases,

etc.)

> Loan participations

> Forward contracts overlying nonfinancial commodities (e.g., agricultural

commodities, “intangible” commodities, etc.) that are intended to be settled by

physical delivery

> Security forwards

Insurance products

The Commissions adopted a non-exclusive safe harbor12

for insurance products

that satisfy a two-part test (the “Insurance Safe Harbor”). To satisfy the

Insurance Safe Harbor and thus be outside the definitions of swap and SBS, an

insurance agreement or transaction must (1) either be among those specific

products listed by the Commissions (the “Enumerated Products”) or satisfy a

number of product criteria (the “Product Test”), and (2) be provided by a person

or entity that satisfies various provider criteria (the “Provider Test”). The

Commissions also adopted a grandfathering provision (“Insurance

Grandfathering”) excluding from the definitions of swap and SBS pre-effective

insurance transactions (i.e., entered into on or before the effective date of the

Product Definitions Rule) satisfying the Provider Test.13

12

The mere fact that an insurance contract or transaction does not satisfy the Insurance Safe Harbor does not necessarily make it a Title VII Derivative. Product Definitions Rule at 67.

13 Id. at 57-58.

Joint Rulemaking on the Definition of Product Terms Under Title VII 6

Insurance Safe Harbor

Insurance Grandfathering

Enumerated Products14

> Surety bonds > Health insurance > Property and casualty

insurance

> Fidelity bonds > Long-term care

insurance

> Annuities

> Life insurance15

> Title insurance > Disability insurance

> Default insurance on individual

residential mortgage

> Reinsurance of any of the

foregoing

14

The Commissions expressly declined to include the following types of transaction on the list of Enumerated Products: guaranteed investment contracts, funding agreements, structured settlements, deposit administration contracts, immediate participation guaranty contracts, industry loss warrants and catastrophe bonds. Product Definitions Rule at 41-42.

15 The Commissions noted that certain variable life insurance products and annuities are securities and are, therefore, outside the scope of Title VII regardless of the operation of the Insurance Safe Harbor. Product Definitions Rule at 24 n. 42.

If the Product Test is satisfied or the product is an Enumerated Product and

the Provider Test is satisfied, then

Insurance Safe Harbor applies and product is not a swap or SBS (n.b.

product falling outside the Insurance Safe Harbor is not necessarily a Title VII Instrument).

If entered into on or prior to the effective date of the Product Definitions and

the Provider Test is satisfied, then

Insurance Grandfathering applies and product is not a swap or SBS.

Joint Rulemaking on the Definition of Product Terms Under Title VII 7

Product Test

Product Test is satisfied if ALL of the following are true:

> Beneficiary required to (i) have insurable interest16

in agreement’s subject

matter and (ii) carry risk of loss throughout agreement’s duration

> Loss must occur and be proven before payment, and payment must be

limited to the value of the insurable interest

> Insurance is not traded separately from the insured interest17

> With respect to financial guaranty insurance only, any acceleration of

payment (on obligor default or insolvency) is at insurer’s sole discretion

Provider Test

The insurance product must be provided:

> by a person subject to supervision either by a state insurance commissioner

or by the United States (or an agency or instrumentality of either), provided

that the product is regulated as insurance;

> directly or indirectly, by the United States, a state, or any of their respective

agencies or instrumentalities, or pursuant to a statutorily authorized

program;18

> with respect to reinsurance, by a person (the “Reinsurer”) to another person

(the “Cedant”), where:

> the Cedant satisfies the Provider Test,

> the agreement to be reinsured satisfies the Product Test,

> the Reinsurer is not prohibited by applicable law from offering reinsurance

to the Cedant, and

> the total amount reimbursable by all Reinsurers does not exceed the

claims that could be paid by the Cedant (except as otherwise permitted

under applicable law); or

> with respect to property and casualty insurance placed through a surplus line

broker with a non-admitted insurer, by a person either:

> located outside of the United States and listed on the Quarterly Listing of

Alien Insurers maintained by the National Association of Insurance

16

The Commissions indicated that they would interpret the meaning of “insurable interest” consistent with the law governing the contract at issue, but reserved the right to depart from state law if they became aware of evasive conduct. Product Definitions Rule at 42-43.

17 The assignment of an insurance contract that is typical in the insurance industry and authorized by state law is not “trading” under the Product Test. The “health insurance exchanges” created under the auspices of the Federal Patient Protection and Affordable Care Act would not be “exchanges” under the Product Test. Id. at 28.

18 Some examples offered by the Commissions include deposit insurance, crop insurance, flood insurance, terrorism risk insurance and insurance of pension obligations. Id. at 48.

Joint Rulemaking on the Definition of Product Terms Under Title VII 8

Commissioners; or

> meeting the eligibility criteria for non-admitted insurers under applicable

state law.

Consumer and commercial agreements

Noting that the definitions of “swap” and SBS could be read to include many

consumer and commercial agreements, the Commissions enumerate several

types of agreements in the Product Definitions Rule that are not Title VII

Derivatives.

Examples of consumer agreements that are not Title VII Derivatives

> Agreements to acquire or lease real or personal property, to obtain a

mortgage, to provide personal services, or to sell or assign rights owned by a

consumer

> Agreements to purchase products or services for personal or household

purposes at a fixed price or a capped or collared price at a future date or

over a period of time (e.g., agreements to buy home heating fuel)

> Agreements providing an interest rate cap or lock on a consumer loan or

mortgage, provided that the benefit is only realized if the loan or mortgage is

made

> Consumer loans or mortgages with variable rates or embedded interest rate

options, including loans whereby the interest rate changes upon an event

related to the consumer (i.e., in the event of default)

> Consumer product warranties, extended service plans or buyer protection

plans

> Consumer options to acquire, lease or sell real or personal property

> Consumer agreements where the consumer may cancel the transaction

without legal cause

> Consumer guarantees of the credit card debt, automobile loans or mortgage

of a friend or relative

Examples of commercial agreements that are not Title VII Derivatives

> Employment contracts and retirement benefit arrangements

> Sales, servicing and distribution arrangements

> Agreements to effect a business combination (e.g., a merger)

> Agreements to purchase, sell, lease or transfer real property, intellectual

property, equipment or inventory

> Warehouse lending arrangements used to build an inventory of assets in

Joint Rulemaking on the Definition of Product Terms Under Title VII 9

Examples of commercial agreements that are not Title VII Derivatives

anticipation of the securitization of those assets

> Mortgage or mortgage purchase commitments

> Sales of installment loan agreements or receivables

> Commercial loans, including those with embedded interest rate locks, caps

or floors in certain circumstances

> Commercial agreements containing escalation clauses linked to an

underlying commodity, such as an interest rate or the consumer price index

The Commissions emphasized that these lists are not exhaustive, and the

Commissions speculated that “[t]here may be other, similar types of agreements,

contracts, and transactions that also should not be considered” Title VII

Derivatives. The Commissions indicated that they will consider the factors listed

below in determining whether an unenumerated agreement or transaction is or is

not a Title VII Derivative. The Commissions also made clear that a party to an

agreement that is not enumerated and does not satisfy all of the factors below

may seek a determination from the Commissions.19

19

Product Definitions Rule at 142-50.

Factors weighing against finding that a consumer or commercial agreement is a Title VII Derivative

> Payment obligations not severable from the agreement

> It is not traded on an organized market or over the counter

> With respect to consumer agreements, it involves

o an asset consumer owns, is beneficiary of or is

purchasing, and

o a service provided to or by the consumer.

> Re commercial agreements: agreement is entered into by

commercial or non-profit entities as principal to serve an

independent commercial or business purpose and is not

used for speculative purposes

Joint Rulemaking on the Definition of Product Terms Under Title VII 10

Loan participations

Loan participations20

that “reflect” an ownership interest in the underlying loan are

not Title VII Derivatives, provided they satisfy the criteria listed below.

Accordingly, neither LMA-style nor LSTA-style loan participations would be Title

VII Derivatives. This reflects a departure from the proposed rule, which looked to

see whether or not a “true participation” had been achieved.21

Loan Participation Criteria

A loan participation will not be considered a Title VII Derivative if:

> the grantor of the participation is either a lender or a participant in the

underlying loan,

> the aggregate participation in the underlying loan of all participants does not

exceed the principal amount of the loan,

> the grantor of the participation does not grant a greater interest than it holds

in the loan,

> the purchase price of the participation is paid in full and not financed, and

> the participation provides the participant all of the economic benefit and risk

of the portion of the underlying loan that is the subject of the participation.

Forward contracts

Examples of Forward Contracts within the Forward Contract Exclusion

> A forward contract in a nonfinancial commodity intended to be physically

settled is not rendered outside the exclusion if settled by a “book-out” of the

physical settlement requirement.

> Under the Brent Interpretation, an investment fund taking delivery of gold as

part of investment strategy not within the exclusion because its activity would

not be considered “commercial” in nature, a but a gold forward used by a

jewelry manufacturer owned by an investment fund would be within the

exclusion since it is being used to meet the commercial needs of the jewelry

business.

> A forward contract having embedded optionality will be within the exclusion if

it satisfies certain criteria. For example, a forward contract would not fall

outside the exclusion merely because it allows a counterparty the option to

renew or to alter the location of physical delivery.

> Forward contracts with embedded volumetric optionality that meet a set of

20

The Commissions cautioned, however, that a loan participation could be considered a security under the federal securities laws or an “identified banking product” under federal banking laws. Product Definitions Rule at 162.

21 Id. at 161-66.

Joint Rulemaking on the Definition of Product Terms Under Title VII 11

criteria will also be within the exclusion. For instance, a forward contract for a

nonfinancial commodity that allowed a counterparty to alter the volume to be

delivered as a result of changed needs or market conditions would still be

within the exclusion.

> Physical exchange transactions for physical delivery and fuel delivery

transactions are within the forward contract exclusion.

Title VII’s definitions of swap and SBS exclude forward contracts (the “Title VII

Forward Exclusion”), which are defined as “any sale of a nonfinancial

commodity or security for deferred shipment or delivery, so long as the

transaction is intended to be physically settled.”22

The CFTC explained that it

would interpret the Title VII Forward Exclusion in a manner consistent with

existing CFTC guidance and precedents on the exclusion from the scope of

commodity futures for forward contracts, treating them instead as “commercial

merchandising transactions” outside the scope of regulation.23

The CFTC also

specifically discussed and expanded on the “Brent Interpretation”24

and

enumerated several types of commodities that will be considered “nonfinancial”

within the scope of the Title VII Forward Exclusion. The CFTC also withdrew the

“Energy Exemption”25

and provided additional guidance about the treatment of

forwards containing embedded optionality.

Brent Interpretation

Under the Brent Interpretation, as applied to the Title VII Forward Exclusion, a

forward contract remains outside the scope of Title VII even if the parties to the

contract “book-out” the obligation to deliver the nonfinancial commodity at some

time after the forward contract was agreed. Under these circumstances, there

will be no physical delivery of the commodity under the contract, but the CFTC

indicated that such a contract would remain excluded from Title VII, provided that

the parties intended for physical delivery at the time the agreement was signed,

and that the “book-out” was the subject of a subsequent, separately negotiated

agreement.26

The CFTC also expanded the Brent Interpretation, which originally

applied only to forward contracts for oil, to include all nonfinancial commodities.27

According to the CFTC, only contracts for “commercial” purposes are eligible for

the Brent Interpretation, and the term “commercial” in this context means “related

22

7 U.S.C. § 1a(47)(B)(ii). 23

Product Definitions Rule at 74-78. 24

See Statutory Interpretation Concerning Forward Transactions, 55 Fed. Reg. 39188 (Sept. 25, 1990).

25 See Exemption for Certain Contracts Involving Energy Products, 58 Fed. Reg. 21286 (Apr. 20, 1993).

26 The CFTC also noted that the “[i]ntent to make or take delivery can be inferred from the binding delivery obligation for the commodity referenced in the contract and the fact that the parties to the contract do, in fact, regularly make or take delivery of the referenced commodity in the ordinary course of their business.” Product Definitions Rule at 80.

27 Id. at 78-82, 85-86. As noted above, in connection with the expansion of the Brent Interpretation, the CFTC withdrew the “Energy Exemption,” which had previously expanded the Brent Interpretation to forward contracts for energy commodities other than oil. Id. at 83-85.

Joint Rulemaking on the Definition of Product Terms Under Title VII 12

to the business of a producer, process, fabricator, refiner or merchandiser.” The

agency noted that, while an enterprise need not be engaged solely in commercial

activity for its forward contracts to be within the Title VII Forward Exclusion, it

would abide by its longstanding view of the Brent Interpretation that a hedge

fund’s investment activity is not commercial activity. Thus, the CFTC explained

that if an investment vehicle takes delivery of gold as part of an investment

strategy, that activity would not be considered a commercial merchandising

transaction and would not be covered by the Brent Interpretation. If, however,

the investment vehicle used a forward contract for gold to supply the raw

materials to support a business (e.g., a jewelry manufacturer) that it owned, such

a contract could satisfy the Brent Interpretation.28

Nonfinancial commodities

The CFTC also provided significant guidance as to which commodities would be

considered “nonfinancial” and thus eligible for the Title VII Forward Exclusion. It

explained that a “nonfinancial” commodity is:

> one that can be physically delivered and

> is an exempt commodity29

or an agricultural commodity.30

The CFTC also stated that an intangible commodity is also a nonfinancial

commodity if it:

> is not an “excluded commodity,”31

> can be physically delivered,

> can be “conveyed in some manner,” and

> can be consumed.32

The CFTC also clarified that “environmental commodities” are intangible

commodities (and thus, nonfinancial commodities), though it declined to provide a

definition of “environmental commodity.”33

The CFTC also interpreted forward

contracts for nonfinancial commodities to include physical exchange transactions

and fuel delivery agreements.34

Forwards with embedded optionality

Commodity options are explicitly included within the definition of “swap.”35

The

Commissions, however, provided guidance with respect to whether a forward

28

Product Definitions Rule at 81-82. 29

The Commodity Exchange Act defines an “exempt commodity” as one that is neither an “excluded commodity or an agricultural commodity. 7 U.S.C. § 1a(20). Excluded commodities include interest rates, currency, security indexes, commercial indexes, etc. 7 U.S.C. § 1a(19).

30 The CFTC has defined the term “agricultural commodity” by regulation. See 17 C.F.R. § 1.3(zz).

31 See note 29.

32 Product Definitions Rule at 93-95.

33 Id. at 95-99.

34 Id. at 104-07.

35 The CFTC has proposed revisions to its options rules, but did not provide additional guidance with respect to the treatment of commodity options in the Product Definitions Rule.

Joint Rulemaking on the Definition of Product Terms Under Title VII 13

contract over a nonfinancial commodity with “embedded optionality” will be

considered within the Title VII Forward Exclusion.36

The CFTC also provided guidance with respect to forward contracts with

“volumetric optionality” that grant a party the option to adjust the amount of a

commodity to be delivered.37

Security forwards

Title VII expressly excludes purchases and sales of securities on a fixed or

contingent basis and sales of securities for deferred shipment or delivery that are

intended to be physically settled (i.e., forward contracts on securities) from the

definition of swap and SBS. With respect to security forwards, the sale occurs at

the time the contract is entered into with performance deferred or delayed, and if

intended to be physically settled, such contracts are within the security forward

exclusion to the swap and SBS definitions.38

These contracts could also fit within

the other statutory carve-out for certain purchases and sales of securities on a

fixed or contingent basis from the definitions of swap and SBS.39

In addition to

36

The CFTC specified that a renewal option in a forward contract would not be considered an embedded option. Product Definitions Rule at 122.

37 The CFTC explicitly stated that “requirements” and “outputs” forward contracts do not contain volumetric optionality and are within the Title VII Forward Exclusion. Id. at 119-20.

38 Id. at 138.

39 Id.

Forward contract with embedded optionality will not be a swap if the embedded option:

> may be used to adjust the forward contract price, but does not change the

contract’s overall nature as a forward;

> does not affect the delivery term, such that the “predominant feature” of the

forward contract is actual delivery; and

> cannot be severed and marketed separately from the forward contract.

Forward contract with volumetric optionality will not be a swap if:

> the optionality does not undermine the nature of the contract as a forward;

> the “predominant feature” of the forward contract is actual delivery;

> the optionality cannot be severed and marketed separately from the forward;

> at the time of the agreement, the seller of the underlying commodity intends to

deliver that commodity if the optionality is exercised;

> both counterparties are “commercial parties;” and

> the decision to exercise the optionality is based on physical factors or

regulatory requirements that are outside the parties’ control and that are

influencing demand for or supply of the commodity.

Joint Rulemaking on the Definition of Product Terms Under Title VII 14

restating this, the Commissions provided guidance that contracts for the future

delivery of mortgage-backed securities purchased through the “To-Be-

Announced” market are considered security forwards.40

Which products are within Title VII’s reach?

In addition to explicitly carving out a number of categories of agreements and

transactions, the Commissions adopted regulations and provided guidance with

respect to certain groups of transactions that are Title VII Derivatives.

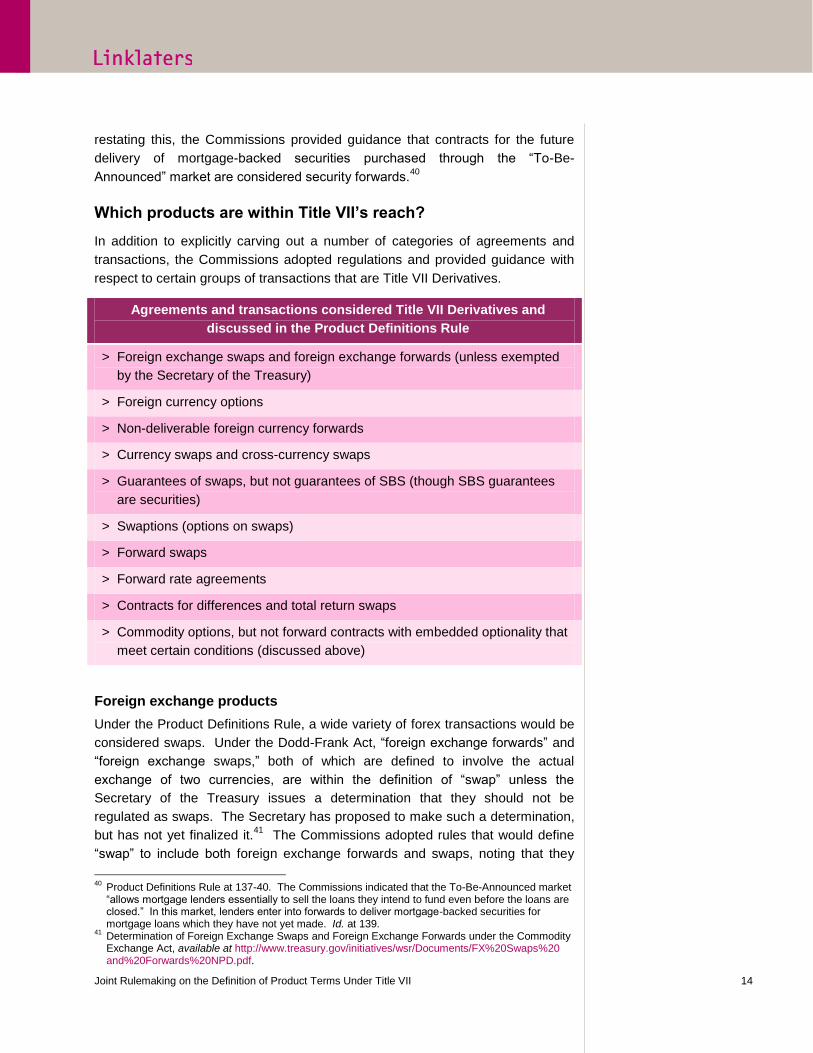

Agreements and transactions considered Title VII Derivatives and

discussed in the Product Definitions Rule

> Foreign exchange swaps and foreign exchange forwards (unless exempted

by the Secretary of the Treasury)

> Foreign currency options

> Non-deliverable foreign currency forwards

> Currency swaps and cross-currency swaps

> Guarantees of swaps, but not guarantees of SBS (though SBS guarantees

are securities)

> Swaptions (options on swaps)

> Forward swaps

> Forward rate agreements

> Contracts for differences and total return swaps

> Commodity options, but not forward contracts with embedded optionality that

meet certain conditions (discussed above)

Foreign exchange products

Under the Product Definitions Rule, a wide variety of forex transactions would be

considered swaps. Under the Dodd-Frank Act, “foreign exchange forwards” and

“foreign exchange swaps,” both of which are defined to involve the actual

exchange of two currencies, are within the definition of “swap” unless the

Secretary of the Treasury issues a determination that they should not be

regulated as swaps. The Secretary has proposed to make such a determination,

but has not yet finalized it.41

The Commissions adopted rules that would define

“swap” to include both foreign exchange forwards and swaps, noting that they

40

Product Definitions Rule at 137-40. The Commissions indicated that the To-Be-Announced market “allows mortgage lenders essentially to sell the loans they intend to fund even before the loans are closed.” In this market, lenders enter into forwards to deliver mortgage-backed securities for mortgage loans which they have not yet made. Id. at 139.

41 Determination of Foreign Exchange Swaps and Foreign Exchange Forwards under the Commodity Exchange Act, available at http://www.treasury.gov/initiatives/wsr/Documents/FX%20Swaps%20 and%20Forwards%20NPD.pdf.

Joint Rulemaking on the Definition of Product Terms Under Title VII 15

would cease to be regulated as such if the Treasury finalizes its determination

although they would still be subject to various other requirements under Title

VII.42

In addition, the Commissions adopted rules defining the term “swap” to include

other forex products, including foreign currency options,43

non-deliverable foreign

currency forwards (“NDFs”),44

currency swaps and cross-currency swaps.45

The Commissions did acknowledge that certain types of forex transactions are

excluded from Title VII. The Commissions stated that Title VII’s definition of

“foreign exchange forward” could be read to include some foreign exchange spot

transactions, which typically settle two days after the trade date, but reasoned

that Congress had not intended Title VII to reach such spot trades. They

concluded that bona fide forex spot transactions would not be considered

swaps.46

In addition, the CFTC explained that retail foreign currency options that

are executed off of an exchange by non-ECPs pursuant to Section 2(c)(2)(B) of

the Commodity Exchange Act would be considered outside the definition of

“swap.”47

Guarantees of Title VII Derivatives

Under the Product Definitions Rule, the term “swap” includes a guarantee of a

swap if the counterparty would have recourse to the guarantor.48

The CFTC

indicated that it will issue a separate release discussing the practical implications

of including guarantees within the definition of “swap.” Conversely, the guarantee

of an SBS is not itself an SBS or part of the guaranteed SBS. The SEC will

consider issuing rules on the reporting of such guarantees and the impact of SBS

guarantees on the extraterritorial reach of its Title VII regulations. Additionally, a

guarantee of an SBS is a security under the Securities Act of 1933 (the “1933

Act”).49

Swaptions, forward swaps, forward rate agreements and contracts for

differences

The Commissions also provided interpretations that a number of other derivative

products would be considered Title VII Derivatives. Under the Product Definitions

Rule, both options and forwards on Title VII Derivatives would themselves be

42

Product Definitions Rule at 168-70. 43

Forex options that are traded on a national securities exchange are securities under the federal securities laws, and are thus not Title VII Derivatives. Id. at 174.

44 Unlike a foreign exchange forward, under an NDF, the parties do not physically deliver the underlying currencies, but instead settle the contract in a reserve currency. The Commissions determined that NDFs do not meet the statutory definition of foreign exchange forwards and are thus not subject to the Secretary of the Treasury’s exemptive authority. They also determined that NDFs are outside of the scope of the Title VII Forward Exclusion. Id. at 175-77.

45 Id. at 173-83.

46 Id. at 183-86.

47 The CFTC explained that the Dodd-Frank Act’s failure to expressly exclude such transactions from the definition of “swap” appears to be a scrivener’s error. Product Definitions Rule 187-90.

48 Financial guaranty insurance in respect of a swap will be treated like any other swap guarantee. Id. at 68. Even a guarantee offered only partial recourse to the guarantor is within the definition of “swap.” Id. at 69-70.

49 Id. at 73-74.

Joint Rulemaking on the Definition of Product Terms Under Title VII 16

Title VII Derivatives.50

Forward rate agreements, which “provid[e] for the future

(executory) payment based on the transfer of interest rate risk between the

parties” are swaps under Title VII.51

Finally, a contract for differences, “an

agreement to exchange the difference in value of an underlying asset between

the time at which [the contract] is established and the time at which it is

terminated,” is a Title VII Derivative.52

How to know if a Title VII Derivative is a swap, SBS or MS?

Determining what type of Title VII Derivative (i.e., swap, SBS or MS) a product is

dictates whether the CFTC’s or the SEC’s regulations (or both) will apply to a

particular transaction or market participant. The Product Definitions Rule

provides guidance to assist counterparties in making this determination.

According to the Commissions, market participants should make a determination

as to whether a Title VII Derivative is a swap, an SBS or an MS prior to execution

“but no later than when the parties offer to enter into” the Title VII Derivative.53

Such a determination generally lasts throughout the term of a transaction, even if

the asset underlying the derivative changes in certain circumstances (although

any amendment will be treated as a new transaction and require a new

determination to be made), subject to certain exceptions (as discussed in more

detail below).

Rates vs. yields

Under the Product Definitions Rule, Title VII Derivatives overlying interest or

other monetary rates54

are generally swaps, while such instruments overlying the

yield, price or value of a single security, loan or a narrow-based security index

are generally SBSs. Thus, for instance, an instrument referencing the London

Interbank Offer Rate (“LIBOR”) would be a swap, but an instrument referencing

the yield on a corporate note by reference to that note would be an SBS.55

If a

rate contained in a Title VII Derivative references a security yield but is fixed at

the time of execution, however, that instrument would be a swap (assuming it

does not otherwise reference a security, loan or narrow-based index) and not an

SBS or an MS, though if that rate were to fluctuate or “reset” during the life of the

instrument, it would be an SBS or an MS.56

50

Product Definitions Rule at 192-93. 51

Id. at 190-92. 52

Id. at 193-95. 53

Id. at 202. 54

Among the types of monetary rates, the Commissions list interbank offered rates (e.g., LIBOR, Euribor), money market rates (e.g., the Federal Funds Effective Rate), government target rates (e.g., the Federal Reserve’s discount rate), general lending rates (e.g., the prime rate, rates in the commercial paper market) and rates derived from indexes of other rates.

55 If, however, a Title VII Derivative references the yield of a U.S. treasury or other “exempted securities” (as referenced in Section 3(a)(12) of the Securities Exchange Act of 1934 as of January 11, 1983) or an index comprised solely of such exempted securities, it is a swap. Product Definitions at 203-10.

56 Product Definitions Rule at 232-34.

Joint Rulemaking on the Definition of Product Terms Under Title VII 17

Treatment of total return swaps containing references to interest rates

The Commissions set forth considerable guidance on how total return swaps

(“TRSs”) that are SBSs (e.g., a TRS on a single loan, security or narrow-based

index), but which contain references to interest rates, should be treated.

Generally, where a TRS buyer’s (i.e., the total return receiver’s) financing

payment is calculated with reference to a rate such as LIBOR, that TRS may still

be considered an SBS if it otherwise would be (i.e., if it references a security,

loan or narrow-based index).57

If, however, a TRS creates “additional interest

rate or currency exposures that are unrelated to the financing of the SBS, or

otherwise shift[s] or limit[s] risks that are related to the financing of the SBS,” the

TRS will be considered an MS.58

Typical TRS scenario – SBS (single share)

TRS – MS scenario (single share with unrelated currency exposure)

In response to comments, the Commissions also provided guidance with respect

to quanto equity59

and compo equity60

swaps. Because the exchange rate

exposure in a quanto equity swap is “incidental” to the exposure to the underlying

57

The Commissions noted that the calculation of a financing rate in a currency other than that of the underlying asset also would not cause a TRS to become a mixed swap. Product Definitions Rule at 212.

58 Product Definitions Rule at 210-13. As an example, the Commissions point out that if counterparties include interest rate caps, collars, calls or puts in the terms of a TRS that would otherwise be an SBS, it would be considered an MS. If the two branches of such a TRS were documented separately, however, they would likely be considered a separate swap and an SBS.

59 A quanto equity swap is one that “provide[s] a U.S. investor with currency-protected exposure to a non-U.S. equity index by translating the percentage equity return in the currency of such non-U.S. equity index into U.S. dollars.” Id. at 213.

60 A compo equity swap is one in which “the parties assume exposure to, and the total return is calculated based on, both the performance of specified foreign stocks and the change in the relevant exchange rate.” Id. at 215.

Final Exchange of € for £, settled in ¥

Initial Exchange of Forward € for £

Depreciation

Appreciation + Dividends

LIBOR + X%

Total Return Receiver

Total Return Payer

Depreciation

Appreciation + Dividends

LIBOR + X% Total Return

Receiver Total Return

Payer

Joint Rulemaking on the Definition of Product Terms Under Title VII 18

security index, a quanto equity swap is considered an SBS where the underlying

index is narrow-based. In contrast, because a compo equity swap offers the TRS

buyer exposure to that currency risk, it will be considered an MS (to the extent

that, without the currency aspect, it would be considered an SBS).61

The

Commissions also explained that, while a TRS overlying a single loan is an SBS,

a TRS overlying more than one loan is a swap.62

Derivatives overlying futures

Generally, a Title VII Derivative overlying a security future (including a future on a

narrow-based index of securities) is an SBS, but such an instrument overlying

any other type of future is a swap. However, the treatment of Title VII Derivatives

overlying a future on a foreign government debt security is more complicated.

Under SEC Rule 3a12-8, futures on the government securities of 21 different

nations63

are carved out of the definition of “security future” and are thus subject

to CFTC regulation. A Title VII Derivative overlying futures contracts on those 21

nations’ debt securities are swaps, not SBSs, if they satisfy a number of criteria

identified by the Commissions.64

Title VII Derivatives overlying the actual debt

securities of those nations, however, are SBSs.65

Narrow-Based Security Indexes

One of the more complicated topics discussed by the Commissions in the

Product Definitions Rule is what constitutes a narrow-based security index. As

noted above, a Title VII Derivative that overlies a narrow-based security index is

an SBS, while such an instrument overlying a broad-based security index is a

swap. Under the Commodity Exchange Act and the Securities Exchange Act of

1934 (the “1934 Act”), an index is considered narrow-based if any of the

following are true:

> It has nine or fewer components

> Any single component comprises > 30% of its weighting

> Its five highest-weight components comprise > 60% of its weighting

> The lowest-weighted component securities comprising 25% of the index’s

weighting have an aggregate dollar value of average daily trading volume

< $50 million (or < $30 million if the index has > 15 components)66

The Commissions discussed previous joint guidance as to whether a volatility

index or an index of debt securities are considered narrow-based and concluded

61

Product Definitions Rule at 213-15. 62

Id. at 216. 63

Those nations include the United Kingdom, Canada, Japan, France and Switzerland. See 17 C.F.R. § 240.3a12-8(a)(1).

64 In order to qualify as a swap (rather than an SBS), such a Title VII Derivative must (1) reference a “qualifying foreign futures contract” as defined in Rule 3a12-8, (2) be traded on or through a board of trade, (3) be cash settled, (4) not be entered into by the foreign country issuer referenced by the futures contract, and (5) the foreign government’s debt securities must not be registered under the Securities Act of 1933 or be the subject of a registered American Depository Receipt. Id. at 227.

65 Id. at 223-31.

66 15 U.S.C. 78c(a)(55)(B).

Joint Rulemaking on the Definition of Product Terms Under Title VII 19

that this guidance applies in the Title VII context, except to the extent it conflicts

with the Commissions’ new rules on index credit default swaps (“CDS”).67

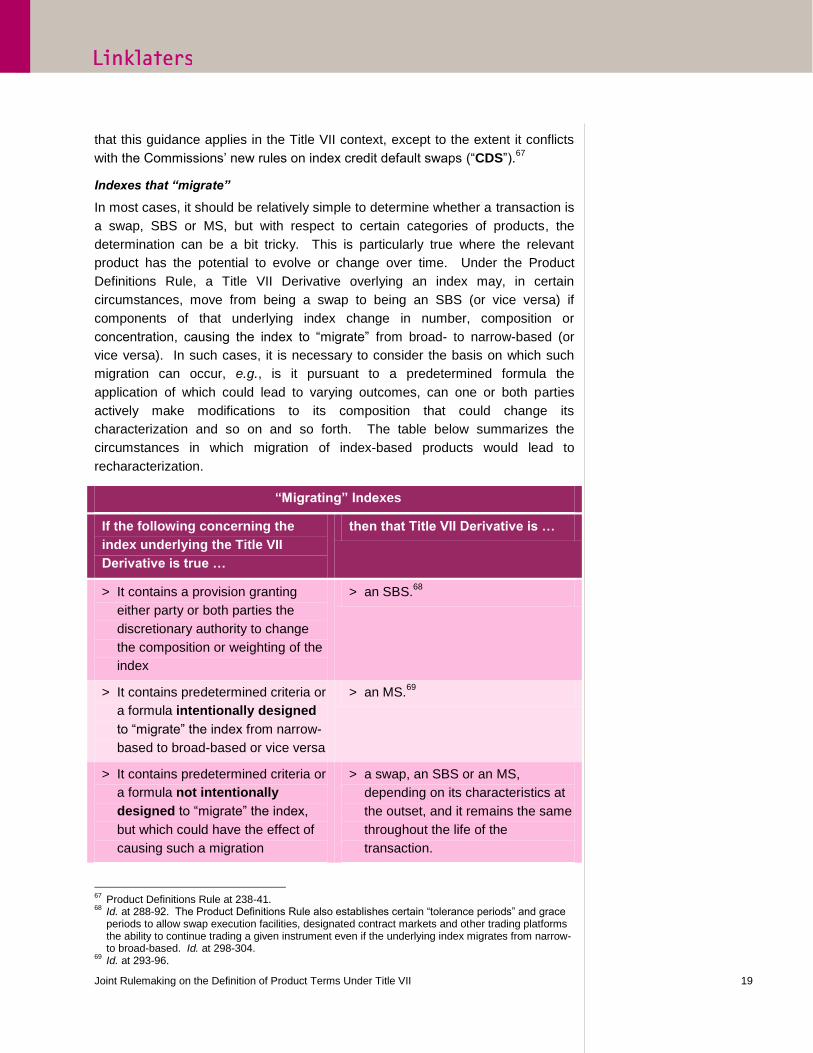

Indexes that “migrate”

In most cases, it should be relatively simple to determine whether a transaction is

a swap, SBS or MS, but with respect to certain categories of products, the

determination can be a bit tricky. This is particularly true where the relevant

product has the potential to evolve or change over time. Under the Product

Definitions Rule, a Title VII Derivative overlying an index may, in certain

circumstances, move from being a swap to being an SBS (or vice versa) if

components of that underlying index change in number, composition or

concentration, causing the index to “migrate” from broad- to narrow-based (or

vice versa). In such cases, it is necessary to consider the basis on which such

migration can occur, e.g., is it pursuant to a predetermined formula the

application of which could lead to varying outcomes, can one or both parties

actively make modifications to its composition that could change its

characterization and so on and so forth. The table below summarizes the

circumstances in which migration of index-based products would lead to

recharacterization.

“Migrating” Indexes

If the following concerning the

index underlying the Title VII

Derivative is true …

then that Title VII Derivative is …

> It contains a provision granting

either party or both parties the

discretionary authority to change

the composition or weighting of the

index

> an SBS.68

> It contains predetermined criteria or

a formula intentionally designed

to “migrate” the index from narrow-

based to broad-based or vice versa

> an MS.69

> It contains predetermined criteria or

a formula not intentionally

designed to “migrate” the index,

but which could have the effect of

causing such a migration

> a swap, an SBS or an MS,

depending on its characteristics at

the outset, and it remains the same

throughout the life of the

transaction.

67

Product Definitions Rule at 238-41. 68

Id. at 288-92. The Product Definitions Rule also establishes certain “tolerance periods” and grace periods to allow swap execution facilities, designated contract markets and other trading platforms the ability to continue trading a given instrument even if the underlying index migrates from narrow- to broad-based. Id. at 298-304.

69 Id. at 293-96.

Joint Rulemaking on the Definition of Product Terms Under Title VII 20

“Migrating” Indexes

If the following concerning the

index underlying the Title VII

Derivative is true …

then that Title VII Derivative is …

> The parties amend or modify the

Title VII Derivative during its life

> a swap, an SBS or an MS,

depending on its characteristics at

the time of the amendment or

modification.

Index CDS

An index CDS offers credit protection on a basket of reference entities or

reference obligations rather than a single entity, loan or security. Like other Title

VII Derivatives, if an index CDS references either an index of securities or the

occurrence or non-occurrence of a credit event relating to issuers of securities in

a narrow-based index, it would be an SBS, though if it references a broad-based

index, it would be a swap. In the Product Definitions Rule, the Commissions

provide further definition of the terms “narrow-based security index” and “issuers

of securities in a narrow-based security index” with respect to index CDS.

Specifically, they indicate that if an index CDS is based on an index of loans that

are not securities, an event relating to one of those loans would be considered an

event relating to the borrower. If that borrower is an issuer of securities, the

index CDS based on that index of loans may be considered an SBS if the index

of loans is narrow-based. Such an index of loans would be considered an “index

of issuers” under the SBS definition.70

The Commissions also provide extensive guidance on the conditions under which

an index of securities or an index of issuers of securities underlying an index

CDS will be considered narrow-based. First, an index will be considered narrow-

based if it satisfies any of the three prongs borrowed from the Commissions’ debt

security index test (the “Numbers and Concentration Test”). Even if an index is

not narrow-based under the Numbers and Concentration Test, it will be

considered narrow-based if at least 80% of its components meet at least one of

the criteria established by the Commissions to ensure that adequate public

information concerning those components is available (the “Public Information

Availability Test”), and no single component that does not satisfy the Public

Information Availability Test represents 5% or more of the index’s weighting.71

The details of these tests are contained in the table below.

70

Product Definitions Rule at 245-47. 71

The Commissions indicated that the Public Information Availability Test is designed in part to ensure that indexes are not constructed in a manner to allow their component entities to circumvent the disclosure and reporting requirements of the federal securities laws. Id. at 267.

Joint Rulemaking on the Definition of Product Terms Under Title VII 21

Numbers and Concentration Test

If an index has any of the following characteristics, it is a narrow-based

index, and the overlying index CDS is an SBS:72

With respect to indexes of

securities…

With respect to indexes of issuers of

securities…

> Nine or fewer securities (count

securities issued by affiliated

issuers as one) in the index

(security only considered an index

component if credit event with

respect to it or its issuer results in

or affects payments under the

index CDS)

> Effective notional amount of any

issuer’s securities > 30% of the

index’s weighting

> Aggregate effective notional

amount allocated to the securities

of any five non-affiliated issuers >

60% of the index’s weighting

> Nine or fewer non-affiliated issuers

of securities in the index (issuer

only considered index component if

credit event with respect to it

results in or affects payments

under the index CDS)

> Effective notional amount of any

reference entity > 30% of the

index’s weighting

> Aggregate effective notional

amount of any five non-affiliated

reference entities > 60% of the

index’s weighting

Even if an index is not deemed narrow-based under the Numbers and

Concentration Test, it may be found to be so under the Public Information

Availability Test.

Public Information Availability Test

Determine which of the reference entities (for an index of issuers of securities)

or issuers of reference securities (for an index of securities) satisfy at least one

of the following criteria:

N.b., if at least 80% of the notional amounts of the index are allocated to

reference entities or securities whose issuers satisfy one of the criteria

below, and any individual entity or issuer does not satisfy the below

criteria represents 5% or less of the notional amount of the index, then

the index will be considered narrow-based, and the index CDS overlying

it will be an SBS.

Otherwise, the index will be considered broad-based and the overlying

72

In applying the Numbers and Concentration Test, market participants should treat an issuer of a security or a reference entity, along with all of its affiliates, as a single entity, except with respect to issuers of asset-backed securities (“ABS”), each of which are treated as a separate reference entity or reference obligation. For instance, if an index references multiple affiliates that collectively comprise 30% of an index’s weighting, those affiliates would be considered a single component in the index and the second prong of the Numbers and Concentration Test would be met. Product Definitions Rule at 257-59.

Joint Rulemaking on the Definition of Product Terms Under Title VII 22

Public Information Availability Test

index CDS will be a swap.

> The reference entity or the reference obligation issuer is subject to periodic

reporting under the 1934 Act;73

> The reference entity or the reference obligation issuer is a foreign private

issuer eligible to rely on the exemption provided by Rule 12g3-2(b) under the

1934 Act;

> The reference entity or the reference obligation issuer has a worldwide

market value of outstanding common equity held by non-affiliates ≥ $700mm;

> A non-ABS reference entity or non-ABS reference obligation issuer has

outstanding notes, bonds, debentures, loans or evidences of indebtedness

(other than revolving credit facilities) > $1 billion;

> The reference obligation is an exempted security or the reference entity

issues an exempted security;

> The reference entity or the reference obligation issuer is a government or

political subdivision of a foreign country;

> With respect to an ABS reference entity or ABS reference obligation issuer,

such ABS was registered under the 1933 Act and has publicly available

distribution reports; or

> With respect to index CDS transactions between ECPs,

> for non-ABS, the reference entity or the reference obligation issuer, makes

available to the public or the ECP information required by Rule

144A(d)(4);74

> for non-ABS, financial information about the reference entity or the

reference obligation issuer is otherwise publicly available; or

> for ABS, information of the type and level included in public distribution

reports for similar ABS is publicly available about the ABS and its issuer.

How are mixed swaps treated?

According to the Product Definitions Rule, the category of MSs is intentionally

narrow under Title VII and was designed to prevent gaps in the regulation of

swaps and SBSs. The Commissions adopted a regulation that lays out which of

each agency’s rules will apply with respect to uncleared bilateral transactions in

MSs entered into by at least one counterparty that is dual registered as (1) either

73

With respect to the first four prongs of the Public Information Availability test, a component reference entity or issuer of securities may determine whether they meet the criteria by looking to both themselves and their affiliates. Thus, if a reference entity is not a reporter under the Exchange Act, it will nonetheless satisfy the first prong of the test if one of its affiliates is. Similarly, in determining whether it has a worldwide market value of $700 million, an issuer would add its worldwide market value to that of all of its affiliates. Product Definitions Rule at 278-82.

74 Market participants may apply the same affiliation standard described in note 73 with respect to the first two prongs of the special tests for index CDS transactions between ECPs. Id. at 279.

Joint Rulemaking on the Definition of Product Terms Under Title VII 23

an SD or MSP and (2) either an SBS dealer or major SBS participant. The

regulation specifies that such transactions will generally be subject to SEC rules,

but will also be subject to CFTC rules regarding capital, reporting, examinations,

position limits and enforcement. The Commissions also established a procedure

by which exchanges and clearing organizations that wish to list, trade or clear an

MS may obtain a determination from them that such an organization may comply

with only one Commission’s rules rather than attempting to comply with both.75

Obtaining guidance as to a particular transaction’s status?

The Product Definitions Rule creates a procedure to seek a joint interpretation

from the Commissions as to whether a particular instrument is a swap, an SBS or

an MS. To obtain such a determination, a market participant must submit (1)

material information about the instrument in question, (2) a statement of the

instrument’s economic purposes and characteristics, and (3) the requestor’s own

determination of whether the instrument is a swap, an SBS or an MS. The rule

generally requires the Commissions to provide an interpretation within 120 days

or to provide a written explanation for why they have not issued such an

interpretation.76

Anti-Evasion Rules

In the Product Definitions Rule, the CFTC adopted broad anti-evasion rules that

include within the definition of swaps “transactions that are willfully structured to

evade the provisions of Title VII.” In addition to a general anti-evasion provision,

the CFTC’s anti-evasion rules specifically target transactions designed to

disguise swaps as identified banking products or foreign exchange swaps and

forwards subject to the Treasury Department exclusion discussed above.

Further, the CFTC adopted a rule making it illegal to enter into a transactions

outside of the United States “to willfully evade or attempt to evade” Title VII, and

considering such transactions subject to Title VII.77

Evasive transactions will also

be included in determining whether a person should register as an SD or MSP.78

In determining whether a transaction is evasive, the CFTC emphasized that it

would not consider the form or documentation of a transaction dispositive, but

would instead “examine its actual substance and purpose.” The CFTC also

provided guidance indicating that it would not consider willfully evasive

transactions that were structured in a certain manner for a “legitimate business

purpose.” It also indicated it would consider the extent to which a transaction

involved fraud or deceit in determining whether it was willfully evasive. The

agency specified that transactions that fall within the Title VII Forward Exclusion

would not be considered evasive, and that where one party to an evasive

75

Product Definitions Rule at 310-18. 76

Id. at 324-29. 77

Id. at 334-41. 78

Id. at 343.

Joint Rulemaking on the Definition of Product Terms Under Title VII 24

transaction was innocent and did not partake of the effort to evade Title VII, the

CFTC would only impose sanctions on the guilty party.79

The SEC declined to adopt any anti-evasion rules under Title VII, noting that SBS

are “securities” and are subject to the full panoply of anti-fraud and anti-

manipulation rules of the federal securities laws.80

What happens next?

The compliance deadlines or effective dates of many of the final rules previously

adopted by the CFTC are triggered by the effectiveness of the Product Definitions

Rule and the Entities Definitions Rule, the latter of which is already effective.

Among others things, by the effective date of the Product Definitions Rule, SDs

and MSPs must register with the CFTC, comply with internal business conduct

standards, and commence real-time reporting of swap transactions. The

effective date of the Product Definitions Rule is 60 days after its publication in the

Federal Register. Assuming that the Product Definitions Rule are soon

published, that registration deadline will be in late September or early October

2012.

Notably, the CFTC only issued proposed guidance on whether non-U.S. swap

market participants will be required to register on June 29, 2012.81

The comment

period on that guidance extends until August 27, 2012, and it is unlikely that the

CFTC will finalize it by the registration deadline. In the absence of final guidance,

it is unclear how non-U.S. entities should determine what their registration and

compliance obligations are. While there is a reasonable possibility that the CFTC

will grant no-action relief to non-U.S. entities until the guidance is finalized, at the

moment, foreign market participants are at a disadvantage in terms of knowing

how to proceed.

Final reflections

More than two years following the enactment of the Dodd-Frank Act, significant

rulemaking progress has been made, but much remains to be done. While the

adoption of final entity and product definitions is a significant step in the right

direction, we have yet to see a host of very important rules from the

Commissions. In particular, the CFTC’s proposed guidance on the extraterritorial

application of Title VII is very clearly in the proposal stage, and we have yet to

see similar guidance from the SEC. The SEC also continues to lag behind the

CFTC on a number of other important rulemaking topics. Additionally, virtually no

progress has been made in the area of international harmonization and we have

already begun to see adverse reactions from regulators abroad in response to

the CFTC’s proposed guidance on the extraterritorial application of Title VII. As

79

Product Definitions Rule at 341-55. 80

Id. at 355-56. 81

Cross-Border Application of Certain Swaps Provisions of the Commodity Exchange Act, 77 Fed. Reg. 41214 (July 12, 2012), available at http://www.cftc.gov/ucm/groups/public/@lrfederalregister/documents/file/2012-16496a.pdf.

Joint Rulemaking on the Definition of Product Terms Under Title VII 25

such, we expect it to be quite some time before the full parameters of the

international regulatory landscape become clear even as significant progress

continues to be made domestically in the United States.

Joint Rulemaking on the Definition of Product Terms Under Title VII 26

//

Authors: include some of the individuals listed as Contacts.

This publication is intended merely to highlight issues and not to be comprehensive, nor to provide legal advice. Should you have any questions on issues reported here or on other areas of law, please contact one of your regular contacts, or contact the editors.

© Linklaters LLP. All Rights reserved 2012

Linklaters in the U.S. provides leading global financial organizations and corporations with legal advice on a wide range of domestic and cross-border deals and cases. Our offices are located at 1345 Avenue of the Americas, New York, New York 10105. Linklaters LLP is a multinational limited liability partnership registered in England and Wales with registered number OC326345. It is a law firm authorized and regulated by the Solicitors Regulation Authority. The term partner in relation to Linklaters LLP is used to refer to a member of Linklaters LLP or an employee or consultant of Linklaters LLP or any of its affiliated firms or entities with equivalent standing and qualifications. A list of the names of the members of Linklaters LLP and of the non-members who are designated as partners and their professional qualifications is open to inspection at its registered office, One Silk Street, London EC2Y 8HQ, England or on www.linklaters.com.

Please refer to www.linklaters.com/regulation for important information on our regulatory position.

We currently hold your contact details, which we use to send you newsletters such as this and for other marketing and business communications.

We use your contact details for our own internal purposes only. This information is available to our offices worldwide and to those of our associated firms.

If any of your details are incorrect or have recently changed, or if you no longer wish to receive this newsletter or other marketing communications, please let us know by emailing us at [email protected].

Contacts

For further information

please contact:

Caird Forbes-Cockell

Partner

(+1) 212 903 9040

Jeffrey Cohen

Partner

(+1) 212 903 9014

Robin Maxwell

Partner

(+1) 212 903 9147

Noah Melnick

Senior Associate

(+1) 212 903 9203

Alissa Clare

Senior Associate

(+1) 212 903 9365

Don Macbean

Senior Associate

(+1) 212 903 9062

Matthew Rench

Senior Associate

(+1) 212 903 9071

Jacques Schillaci

Professional Support Lawyer

(+1) 212 903 9341

If you have any questions, please contact the people on the right or your usual

Linklaters contacts.

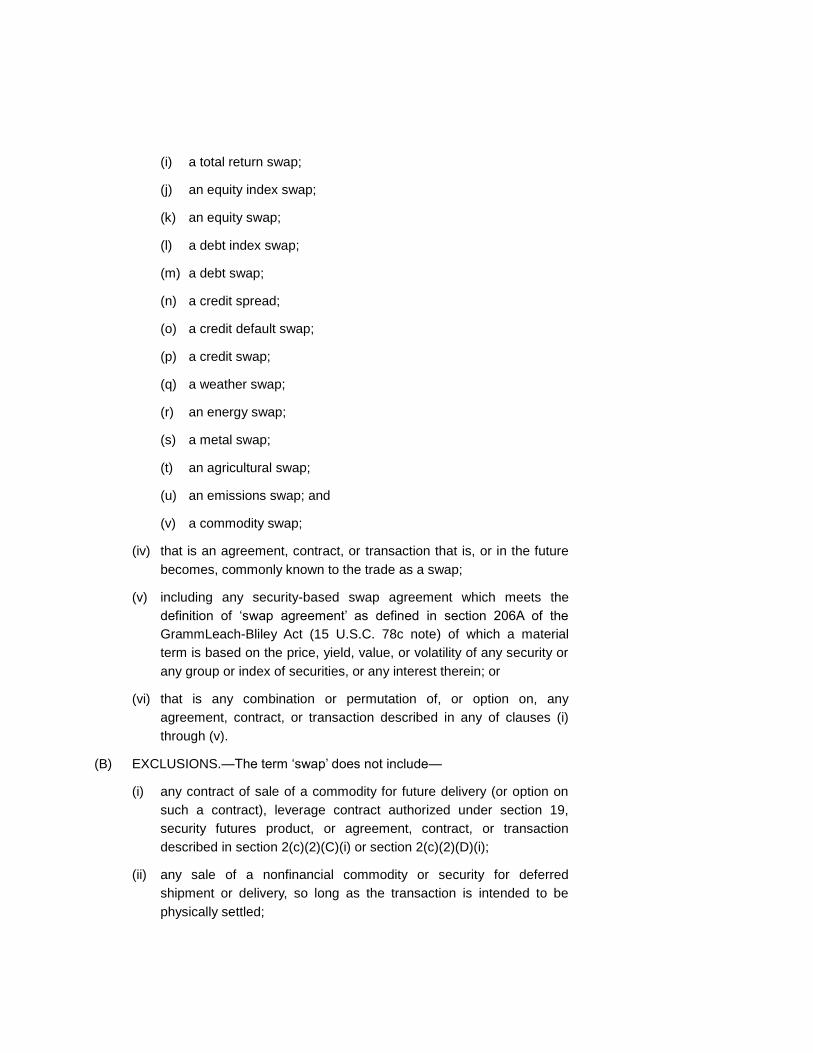

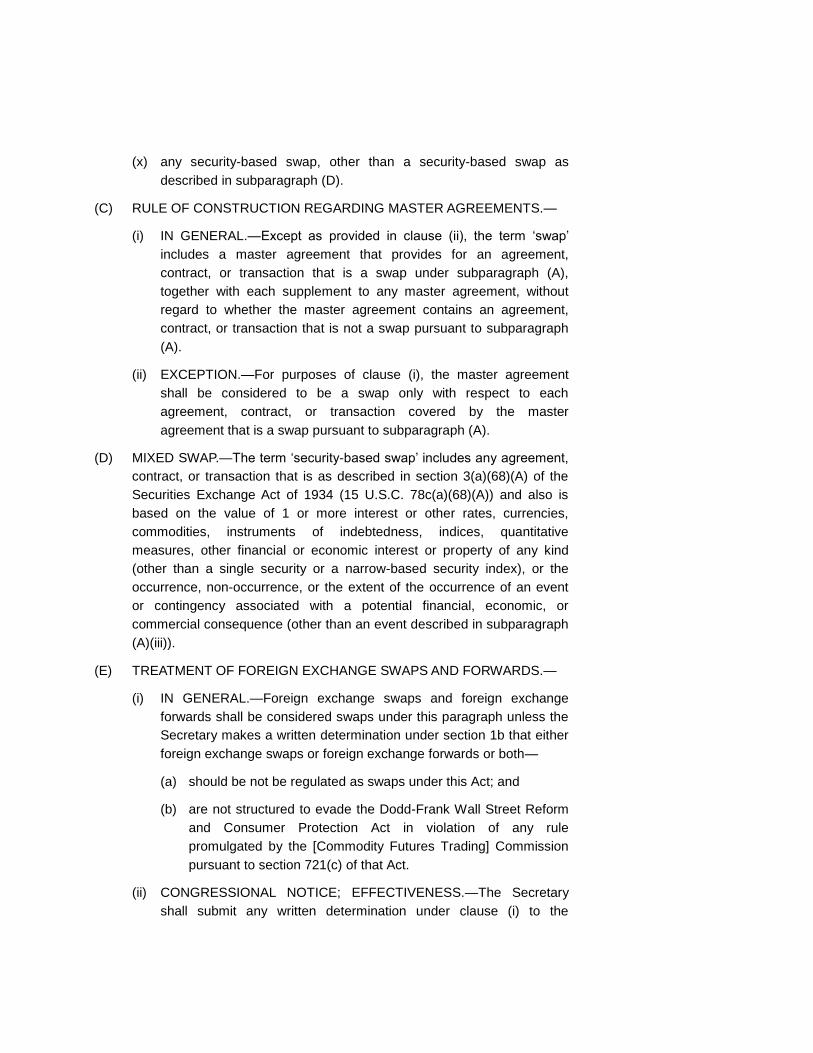

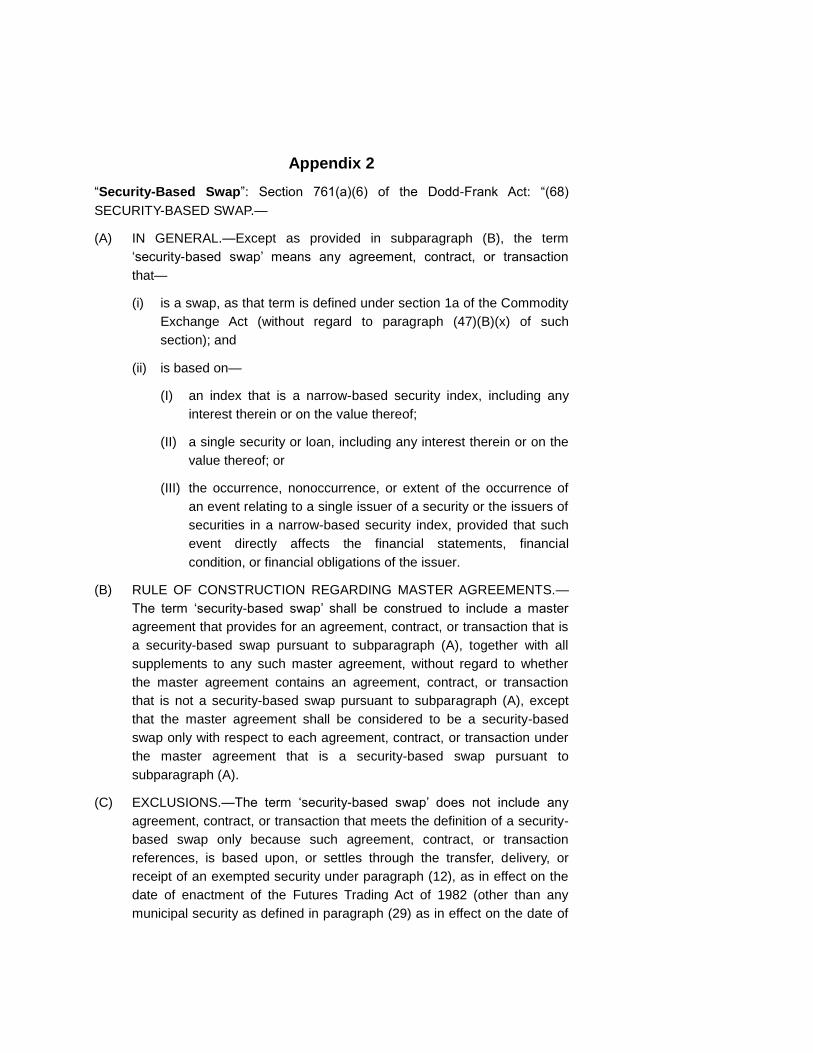

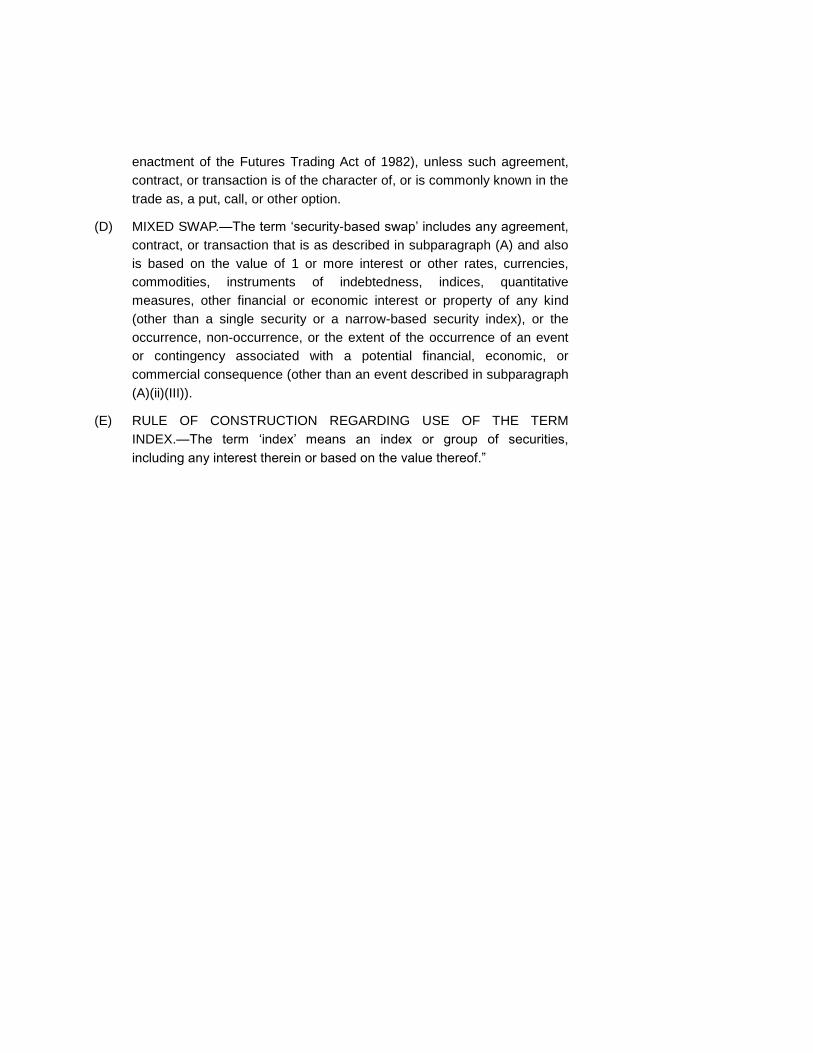

Appendix 1

“Swap”: Section 721(a)(21) of the Dodd-Frank Act: “(47) SWAP.—

(A) IN GENERAL.—Except as provided in subparagraph (B), the term ‘swap’

means any agreement, contract, or transaction—

(i) that is a put, call, cap, floor, collar, or similar option of any kind that is

for the purchase or sale, or based on the value, of 1 or more interest

or other rates, currencies, commodities, securities, instruments of

indebtedness, indices, quantitative measures, or other financial or

economic interests or property of any kind;

(ii) that provides for any purchase, sale, payment, or delivery (other than

a dividend on an equity security) that is dependent on the