CFPB Mortgage Servicing Regulations ppt.ppt [Read...

25

The CFPB & Mortgage Servicing Regulations Barry D. Johnson 3333 Lee Parkway, Eighth Floor Dallas, Texas 75219

Transcript of CFPB Mortgage Servicing Regulations ppt.ppt [Read...

The CFPB & Mortgage Servicing RegulationsBarry D. Johnson

3333 Lee Parkway, Eighth FloorDallas, Texas 75219

Overview

• Introduce you to Dodd Frank• Introduce you to the CFPB• Regulations administered by CFPB• Discuss requirements of Mortgage Servicing

Regulations

Dodd Frank

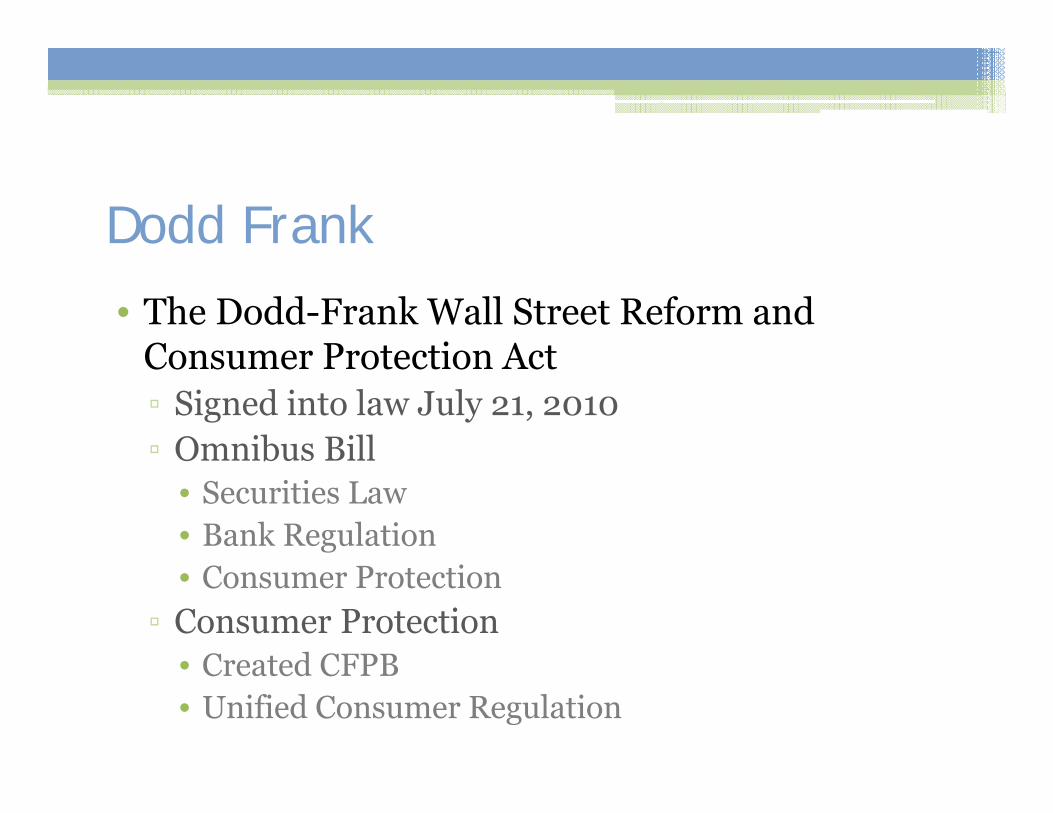

• The Dodd-Frank Wall Street Reform and Consumer Protection Act▫ Signed into law July 21, 2010▫ Omnibus Bill

• Securities Law• Bank Regulation• Consumer Protection

▫ Consumer Protection• Created CFPB• Unified Consumer Regulation

The CFPBConsumer Financial Protection Bureau• An agency like no other• Independent from political forces▫ “Housed” in Federal Reserve▫ “Non-Appropriated” Agency

• Funding from Federal Reserve, not Congress▫ Director appointed by President with advice and

consent▫ Testimony/Reports to Congress▫ “Advisory” Directors

Legal Challenges to CFPB

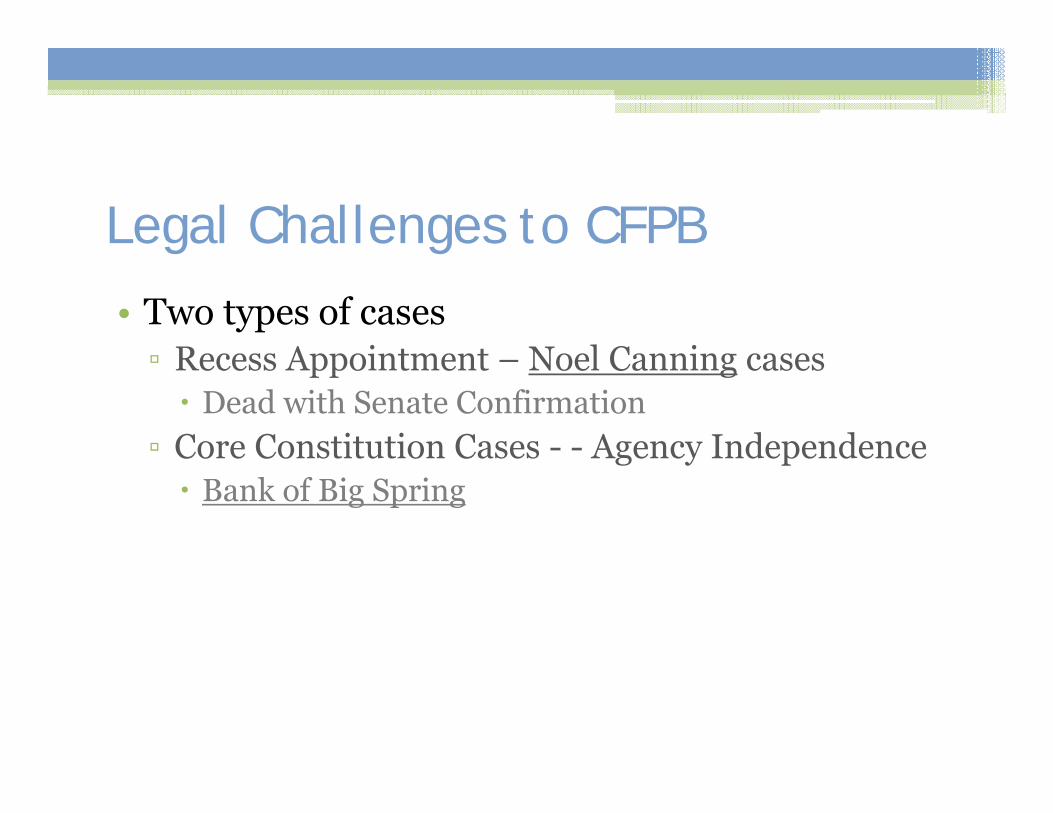

• Two types of cases▫ Recess Appointment – Noel Canning cases Dead with Senate Confirmation

▫ Core Constitution Cases - - Agency Independence Bank of Big Spring

What Industries Does CFPB Regulate?CFPB

Mortgage Originators and

Servicers

Credit Card

Pay Day Loans Pawn Transactions

Student Loans

Debt Collection

Substantial Service Providers to Regulated Industries

What Does CFPB Do?CFPB

Consumer Advocate

Study/RecommendLegal Changes

Consumer Dispute Resolution

Regulation

Investigate/Prosecute Violations

UDAP Authority – Consumer Finance Products

Regulations

• Three Types▫ Inherited regulations▫ New regulations required by Dodd-Frank▫ New discretionary regulations

Inherited Regulations

• Most of the consumer “Alphabet” regulations (A-CC)▫ Includes: Regulations X (RESPA) – formerly HUD Regulation Z (TILA) – formerly Federal Reserve

▫ First actions of CFPB was to adopted the former regulations first on interim, then final basis

CFPB’s Mandatory Rule Docket

• Dodd-Frank required CFPB to issue regulations to be effective January of 2014▫ Regulation Z (TILA) ability to repay (Qualified

Mortgage)▫ Regulation Z (TILA) HOEPA Amendments▫ Loan Originator Compensation (TILA)▫ ECOA – Appraisal Rules/Valuation Independence▫ Higher Priced Mortgage Rules (TILA)▫ Mortgage Servicing (TILA and RESPA)

CFPB’s Discretionary Docket

• TILA and RESPA Unification▫ “Early” TIL & GFE “Loan Disclosure”▫ “Final” TIL & HUD-1 “Closing Disclosure”▫ Effective (mandatory use) August 1, 2015

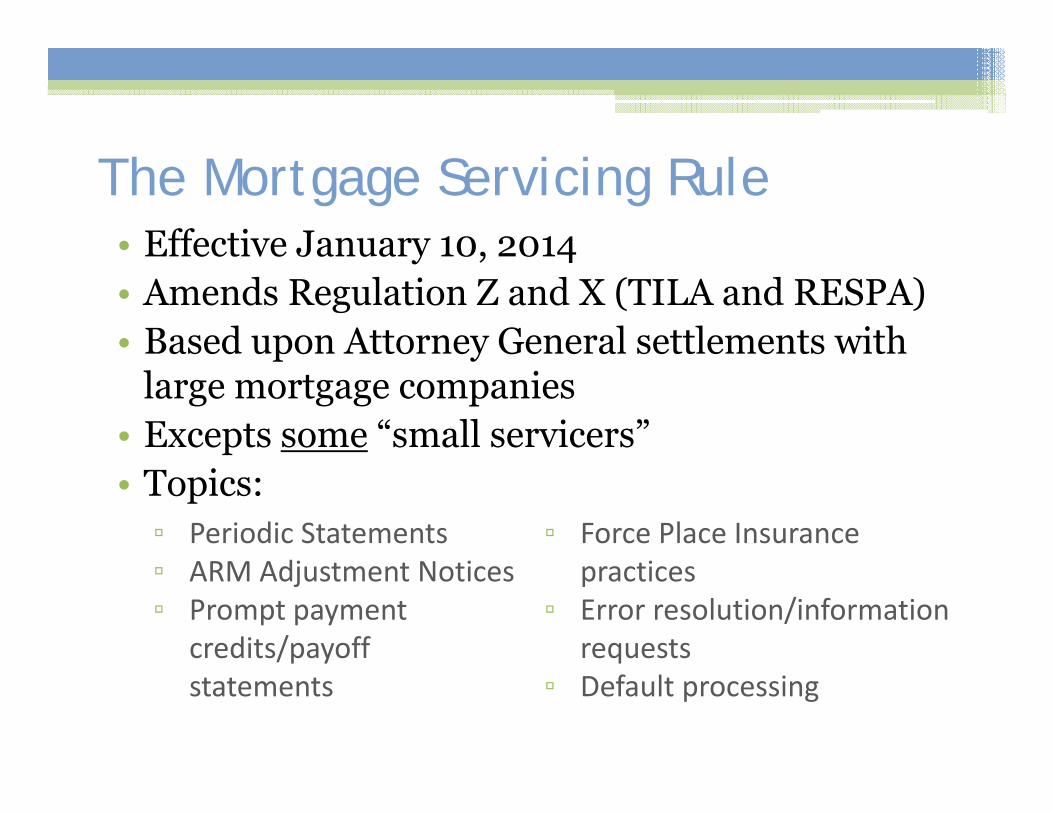

The Mortgage Servicing Rule• Effective January 10, 2014• Amends Regulation Z and X (TILA and RESPA)• Based upon Attorney General settlements with

large mortgage companies• Excepts some “small servicers”• Topics:▫ Periodic Statements▫ ARM Adjustment Notices▫ Prompt payment

credits/payoff statements

▫ Force Place Insurance practices

▫ Error resolution/information requests

▫ Default processing

Periodic Statements

• Uniform Statements from all servicing companies

• Two forms: ▫ Current Loans▫ Defaulted Loans

ARM Adjustment Notices• Old Law ▫ Notice of Intent (payment) adjustment 45 days

before adjustment – Exploding ARMs• New Law ▫ Warning notice 210-240 days before first

adjustment▫ Change notice 60-120 days before each change▫ Expanded information on notice

Prompt Payment – Payoff Statements• Payments must be credited effective day received unless

delay does not affect change to consumer• Provides uniform structure for “Partial Payments”▫ Accept and credit▫ Returns▫ Place in suspense

• Credit Rules for “Nonconforming Payments”▫ Servicer sets “Reasonable Rules” for payments▫ Cashier’s check?

• Payoff Statements must be provided within 7 days of request

Force Place Insurance• Cannot be placed without notice to consumer▫ 45 day warning notice▫ 30 day warning notice▫ Insurance can be placed 15 days after second letter▫ Annual renewal notices 45 days before renewal▫ Required content of notices

• Requirement to convert and promptly refund if consumer supplies evidence

• Change must be bona fides and recordable• Servicer must have “reasonable Basis” to force

place

Error Resolution – Information Request• Larger than QWR – not limited to “servicing”• Procedure▫ Acknowledge within 5 days▫ 30-45 days to correct/explain error or supply

information or prior to foreclosure sale• Excluded from definition of Error▫ Origination/underwriting issues▫ Sale/securitization of loans

• Exceptions (no response required)▫ Duplicate requests▫ Overbroad requests▫ Received after servicing transfer

▫ Confidential/proprietary information

▫ Irrelevant requirement

Additional Areas Covered by Rule• Servicer to establish policies and procedures to

comply with rule• Create a “Servicing File” containing▫ All legal documentation▫ All correspondence▫ Loan/payment histories▫ All “notes” related to account/call history

Default Processing

• Timelines (mandatory) on contact with customer• Single point of contact (SPOC)• Loss Mitigation processing

Default Timelines• Day of missed payment (Payment Due Date) is

Day 1• On or before Day 36▫ Servicer to make 3 attempts at Live Contact If by phone – 3 calls at different times of day

▫ Servicer diligence to locate contact information• On or before Day 45▫ Servicer to send form of SPOC letter

• “First Legal” (Posting in Texas) cannot happen until after Day 120

SPOC

• Assigned on or before Day 45• Can be person or team• Full access to all customer records (payment

histories, etc.)• Full authority to discuss Loss Mitigation options▫ SAFE licensing requirements

• Stay assigned to customer until default cured and 2 consecutive payments

Loss Mitigation

• No dual track processing - - if customer is being considered for Loss Mitigation Foreclosure on hold

• A process – like loan application• Servicers do not have to offer all forms of Loss

Mitigation, but customers have to be informed of what options are available

Loss Mitigation Continued

• What is not Loss Mitigation:▫ Payment Agreements▫ Short Term Forbearance Plans

• What is Loss Mitigation:▫ Forbearance▫ Modification▫ Short Sale▫ Deed in Lien

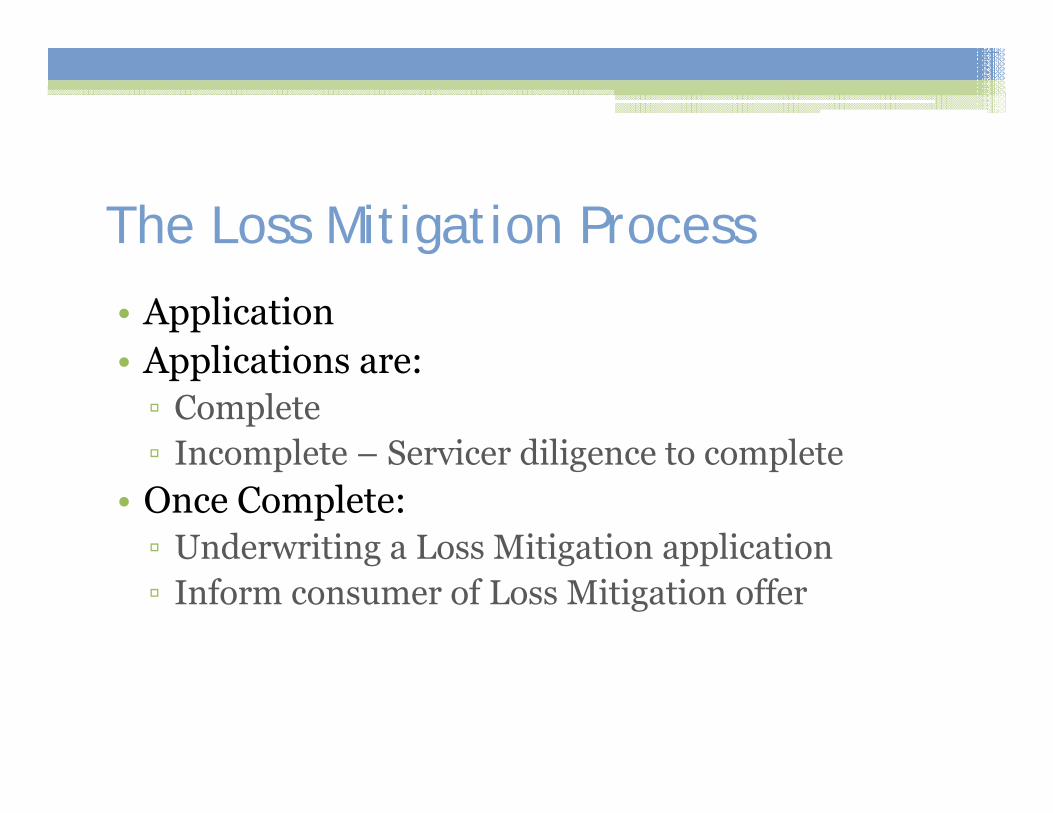

The Loss Mitigation Process

• Application• Applications are:▫ Complete▫ Incomplete – Servicer diligence to complete

• Once Complete:▫ Underwriting a Loss Mitigation application▫ Inform consumer of Loss Mitigation offer

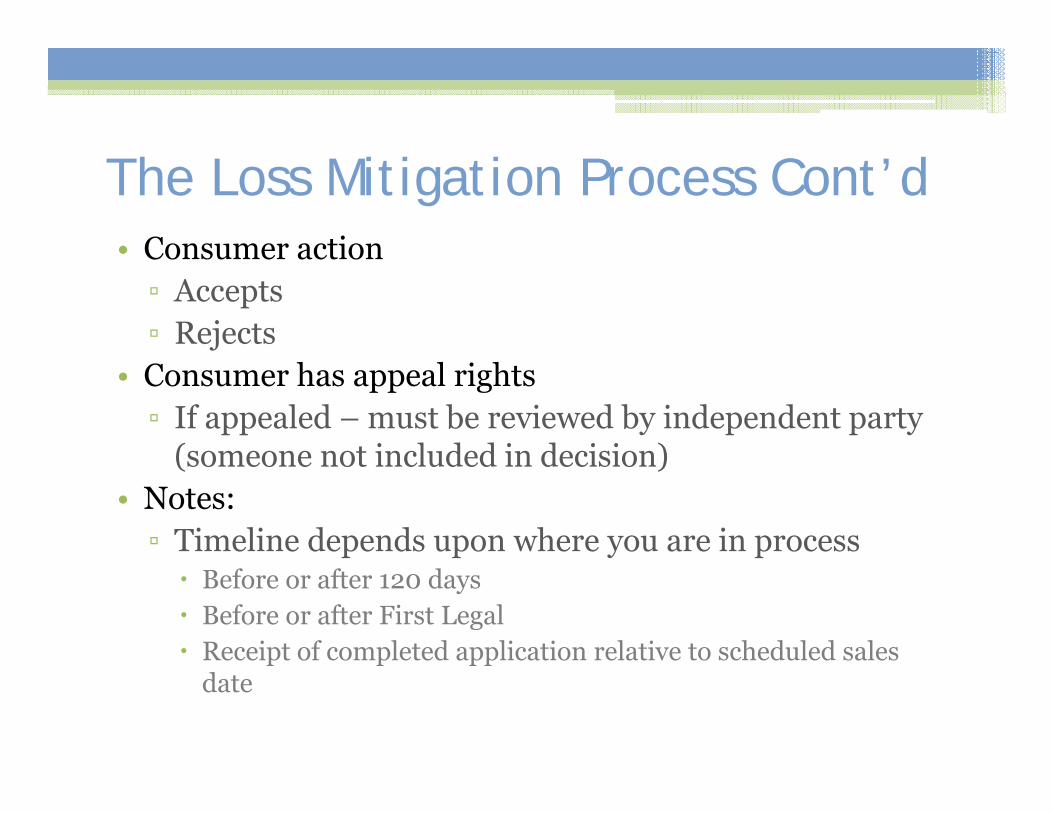

The Loss Mitigation Process Cont’d• Consumer action▫ Accepts▫ Rejects

• Consumer has appeal rights▫ If appealed – must be reviewed by independent party

(someone not included in decision)• Notes:▫ Timeline depends upon where you are in process Before or after 120 days Before or after First Legal Receipt of completed application relative to scheduled sales

date