CFE Newsletter - Belgi뀦 · CFE Newsletter 2 Events ... Fiduciaire). Proponents of ownership...

13

1 February 2012 - 1/2012 CFE Newsletter 2 Events CFE Professional Affairs Conference 5 CFE Committees Fiscal Committee Professional Affairs Committee 6 CFE Internal 7 Pictures 10 Upcoming Events 11 Member Organisations’ Pages CONTENTS

Transcript of CFE Newsletter - Belgi뀦 · CFE Newsletter 2 Events ... Fiduciaire). Proponents of ownership...

CFE NEWS 1/2012

1

February 2012 - 1/2012CFE Newsletter

2 Events CFE Professional Affairs Conference

5 CFE Committees Fiscal Committee Professional Affairs Committee

6 CFE Internal

7 Pictures

10 Upcoming Events

11 Member Organisations’ Pages

CONTENTS

CFE NEWS 1/2012CFE NEWS 1/2012

2

Events

André Bert

CFE Professional Affairs Conference 2011New Regulatory Trends for Tax Advisers

by Rudolf Reibel, Fiscal and Professional Affairs Officer, CFE Office Brussels

Unlike the legal or audit profession, there is no harmonization of the tax pro-fession under EU law. Looking at the patchwork of professional regulation across Europe, the 4th CFE Profes-sional Affairs Conference in Brussels, held on 29 November 2011, endeav-oured to examine how EU law and na-tional budget consolidation efforts may impact national regulation.

EU law recognizes the Member States´ right to regulate access and exercise of the professions, for example, by re-quiring qualifications and professional indemnity insurance and by imposing conditions on ownership of firms and rules on professional conduct. This may, however, conflict with the free-dom of professionals to provide their services, temporarily or permanently, to clients from other Member States, as guaranteed by the Treaty on the Func-tioning of the European Union (TFEU). Indeed, a tax adviser who is not per-mitted to advertise in another Member State, or is required to first restructure his firm, will find it hard to enter new markets. To clarify the relationship be-tween these two principles, the Pro-fessional Qualifications (PQ) Directive (2005/36/EC) and the Services Direc-tive (2006/123/EC) were adopted.

Opening the confer-ence, André Bert, President of the Belgian Institute of Certified Account-ants and Tax Ad-visers, welcomed the participants and briefly portrayed the Belgian way of reg-ulating the tax pro-

fession, which is unique in Europe in so far as legal regulation only concerns the use of the title but not the permis-sion to give tax advice.

Ian Hayes, chairman of the CFE Pro-fessional Affairs Committee, pro-vided an overview of the regulation of the tax profes-sion in Europe. Regulation at the national level, al-though usually referred to as self-regulation, takes

diverse forms. While Austria, Belgium, the Czech Republic, France, Germany, Greece, Luxembourg, Poland, Roma-nia and the Slovak Republic require le-gal qualifications and mandatory mem-bership in professional bodies, Ireland, Latvia, the Netherlands, Russia, Spain, Switzerland and the United Kingdom rely on professional regulation by pri-vate associations for their voluntary members. In Finland, Italy and Malta there are private professional associa-tions that do not regulate qualification but, in practice, tax advisers are often members of other regulated profes-sions.

EU law impacts national regulation in various areas. The Services Directive (2006/123/EC) questions the justifica-tion of national rules on ownership, pro-fessional indemnity insurance and pric-ing where cross-border services are provided on a temporary basis, as well as advertising bans (on 5 April 2011, the European Court of Justice, based on the Services Directive, scrapped a canvassing prohibition for French ac-countants, Case C-109/09, Société Fiduciaire). Proponents of ownership rules for established tax firms were vin-dicated in the ECJ’s decision in Apoth-ekerkammer Saarland (Joined Cases C-171 and 172/07, Apothekerkammer Saarland), wherein the ECJ allowed for such restrictions for pharmacies in Germany.

As to professional qualifications, the proposal for a modernized PQ Directive, of 19 December 2011 (COM(2011)883 final), provides that Member States should grant partial access to a profes-sion on a permanent basis to profes-sionals with a qualification from anoth-er Member State.

While the Internal Market freedoms are usually associated with deregulation, a number of EU laws have introduced rules that impact tax advisers, although these laws seldom name the tax pro-fession specifically (note that the Anti-Money Laundering Directive (2005/60/EC) does specifically refer to tax ad-visers). These EU laws include the e-Commerce Directive (2000/31/EC) and the recently adopted Consumer Rights Directive (2011/83/EU), which, together with the Services Directive and the PQ Directive, contain 19 different points in respect of which a tax adviser may be required to inform his or her client (de-pending on (1) whether the client is a consumer and (2) the form and circum-stances pursuant to which the contract is concluded). They reflect a trend to replace regulation by client information requirements.

At the national level, due to the cur-rent public debt crisis, a new demand for regulation may arise from Member States’ efforts to increase tax compli-ance by extending control over tax adviser dealings, such as forms of en-hanced cooperation and tax avoidance reporting duties.

Martin Frohn, from the European Commission, Directorate-General In-ternal Market and Services, explained that professional regulation and the In-ternal Market freedoms do not neces-sarily conflict with one another.

According to ECJ case law, any restric-tion on the fundamental freedoms of the TFEU must not be discriminatory and must be justified and proportionate in light of an overriding reason of gen-eral interest. In regard to restrictions

Ian Hayes

CFE NEWS 1/2012CFE NEWS 1/2012

CFE NEWS 1/2012

3

on temporary services, the Services Directive goes one step further by lim-iting possible justifications for restric-tions to public policy, public security, public health and environmental pro-tection (professional qualifications are already dealt with under the PQ Direc-tive), leaving a number of requirements under national law without possible justification. One example is profes-sional indemnity insurance, which may be justified in the country where a tax adviser is established (Article 23(1) of the Services Directive) but may not be required in regard to a temporary activ-ity. Other examples include legal form, pricing and shareholding requirements.

The Services Directive was required to be implemented by the end of 2009 but, in practice, there have been substan-tial delays in regard to certain Member States. In 2010, the Commission, along with the Member States, undertook a “mutual evaluation” peer review of se-lected remaining requirements, which led the Commission to conclude that the degree of convergence was still be-low expectations.

Following publication of the mutual evaluation results in Communication COM(2011)20 of 27 January 2011, the Commission sent a questionnaire to the Member States querying them con-cerning requirements they continue to impose on services from other Member States. Interestingly, tax advice is one of three sectors that are being scruti-nized. One reason for this is the diversi-ty in professional regulation. The Com-mission denied, however, that there is a particular focus on deregulating the tax profession, although some require-ments could be made easier. The Com-mission noted that there would be fur-ther action taken in this regard in 2012.

Martin Frohn made it clear that, despite

the obligation to remove unjustified restrictions on cross-border activity, Member States are not prevented from introducing professional regulation at this stage.

Brian Redford, from the UK tax au-thorities (HM Revenue & Customs), spoke from the perspective of a tax administration that is in the process of reconsidering its relationship with the tax profession through its “Tax Agent Strategy”. This is part of HMRC’s effort to reconcile the seemingly conflicting aims of raising revenues by GBP 7 bil-lion per year, reducing administrative costs by 25% and achieving greater taxpayer satisfaction. The strategy fol-lows up on other recent measures to improve HMRC´s performance through a more customer-oriented approach. These include the deployment of cus-tomer relationship officers to deal with the 800 largest businesses in the Unit-ed Kingdom and a categorization of the “mass market” of small and medium-sized enterprises and individual tax-payers into levels of compliance with different strategies to deal with each level.

The Tax Agent Strategy focuses on bet-ter involvement of “tax agents” in day-to-day dealings. Tax agents are per-sons who represent taxpayers before HMRC. These can be professionals but also friends or family of taxpayers. HMRC estimates that 70% of tax agents are qualified members of professional bodies. It is proposed that agents will have the possibility to log into their cli-ents´ data accounts and modify data, which should avoid a great number of time-consuming phone calls.

There are no restrictions as to who can represent a taxpayer before HMRC and HMRC does not attribute levels of competence to tax agents, give any form of orientation to consumers or refuse agents who have been expelled from professional bodies for breach of professional rules.

Brian Redford mentioned a substan-tive tax risk resulting from the number of sophisticated criminal cyber attacks on HMRC´s systems, which could be lowered by better knowing the tax

agent community. This would make it much easier to distinguish bona fide operators from fraudsters. This has led HMRC to suggest that tax agents should be obliged to register with HMRC. In return, they would get ac-cess to self-service tools to handle their clients´ files, with HMRC remain-ing an observer. Having this insight into the tax agent community and their dealings, HMRC would prefer to leave the question of regulation unresolved, stating that HMRC would not have the resources or the commercial exper-tise to administer the profession itself. However, HMRC would be in a position to analyse the extent to which formal qualification and continuing profession-al development (CPD) requirements, affiliation and professional indemnity insurance are actually linked to com-petence and taxpayer compliance. Any decision on regulation in the future would have to deal with the question of grandfathering for practising tax agents with no or little formal qualification.

Brian Redford mentioned that the re-sults from a major UK public consulta-tion on the Tax Agent Strategy would be published on 6 December 2011.

As examples of both a regulated and a non-regulated country, profession-als from Germany and the Netherlands advocated their respective system of (non-) regulation.

Speaking in favour of regulation by law, Herbert Becherer, from the German

Federal Chamber of Tax Advisers, pre-sented the German model.

Legal qualification requirements pro-tect the recipients, notably consumers, who generally have no expert knowl-

edge to judge the competence of their adviser. Although the German state exam requires a high level of compe-tence, admission is not limited to uni-versity graduates or academics.

In Germany, the majority of the shares of a tax firm must be held by tax advis-Martin Frohn and Brian Redford

Herbert Becherer

CFE NEWS 1/2012

4

CFE NEWS 1/2012

ers, lawyers or auditors. Mr Becherer argued that such ownership rules serve the client, as they prevent conflicts of interests since otherwise tax advisers could come under pressure to align their activities with the profit expecta-tions of outside investors. Banks or in-surance companies could seek to sell their products through the tax adviser, taking advantage of his/her special relationship of trust with the client. In-deed, allowing non-professional inves-tors to become majority shareholders would not increase competition (as the European Commission argues in regard to audit firms) because, unlike manufacturing businesses, tax firms needed no major outside capital invest-ment to be successful. On the contrary, there would be a risk that investors would start buying up tax firms, in-creasing market concentration.

Referring to the United Kingdom, Her-bert Becherer made the point that intro-ducing regulation might allow govern-ments to take a less rigorous stance towards monitoring tax agent behav-iour.

Although fully in agreement with the importance of independent and highly qualified advice, Dick Barmentlo, from

the Dutch tax advis-er association NOB, argued in favour of not regulating the profession by law. In the Netherlands, about two out of three tax advisers are members of one of the two profes-sional bodies, the remainder not be-

ing affiliated. The two bodies require professional education at a master’s level and CPD, professional indemnity insurance and compliance with a code of conduct that includes sanctions. A right of non-disclosure of client infor-mation towards tax authorities and tax courts, although not contained in the legislation, is recognized by case law. Thus, clients are free to opt for optimal protection of their rights by choosing an affiliated tax adviser or opt to have low-cost advice. This leaves the market open to development.

Although there is no desire in the Netherlands to introduce regulation, the recent Dutch concept of “horizon-tal monitoring”, whereby the taxpayer, the tax authorities and the tax adviser agree to having tax compliance moni-tored by the adviser, could be regarded as a form of state certification, as the agreement gives recognition to the tax adviser.

The Dutch and German examples trig-gered a discussion on whether or not clients are actually able to judge wheth-er the complexity of their case requires high quality professional advice. This was affirmed by Dick Barmentlo who observed that clients were aware of the added value of an affiliated tax adviser, therefore, having professional rules to comply with did not mean a competi-tive disadvantage. From the UK experi-ence, Brian Redford observed that the judgement of SMEs in regard to the quality of advisers is often very weak, which has led to numerous cases of dissatisfaction. Dick Barmentlo doubt-ed whether regulation could overcome the problem of poor performance of some professionals.

The panel discussion touched upon the use of EU freedoms to escape national regulation, for example, by persons that have failed to qualify or have been excluded from the profession in one Member State and return to the profession through an establishment in another. There have been cases where the first Member State has refused to give these persons permission to practice. Mr Frohn confirmed that such situations have been the subject of a number of complaints. The ECJ has recognized the potential for abuse but the answer would depend on the facts of the case. Therefore, it would be difficult to predict the ECJ’s decision in a particular case. He recalled the ECJ case law on the establishment of companies (Centros, C-212/97, Überseering, C-208/00 and Inspire Art, C-167/01), arguing that the use of an advantageous regime in another Member State is legitimate and, as such, does not involve circumvention. However, the PQ Directive allows professionals to return to practice in their original Member State only after having obtained a professional qualification or

exercised the profession in their new Member State for two years.

Another question concerned cross-bor-der online tax advice. Mr Frohn con-firmed that, indeed, for online services, qualification requirements and other professional regulation of the client´s Member State do not apply, as the e-Commerce Directive provides for the country of origin principle, meaning the tax adviser is subject only to the rules of his/her Member State of establish-ment. Legally, this could indeed give an advantage over local tax advisers. This should, however, not be over-estimat-ed, as success in the market most of all requires knowledge of the local tax law and language and, often enough, personal contact. Regulatory condi-tions are only one aspect that firms will consider when deciding in which coun-try to establish. Participants raised the thought whether the considered switch from the origin to the destination prin-ciple in VAT (see the Commission´s Communication COM(2011)851 of 6 December 2011 on the future of VAT) might support a similar switch in the question of regulation of cross-border services.

Lastly, looking into the future, voluntary professional rules may come through standardization of tax advice at the EU level. In June 2011, the European Commission proposed a regulation that would empower itself to mandate the development of such standards. Panel members mentioned that there could be some merit in standardized forms for accounting, invoicing or tax returns but not standardization of the advisory activity proper, as such services are tai-lored to the client´s specific needs.

Despite different regulatory approach-es, the panel members agreed that the respective national regimes have each created a competitive professional en-vironment that pays regard to client protection. Although convergence is likely to be increased by EU law grind-ing off some obstacles to cross-border activity, an EU-wide regulation of the profession is neither feasible nor desir-able.

Dick Barmentlo

CFE NEWS 1/2012CFE NEWS 1/2012

CFE NEWS 1/2012

5

CFE Committees since July 2011

Fiscal Committee

On 14 September 2011, Fiscal Com-mittee Chairman Gottfried Schellmann spoke at a tax and development con-ference in Bonn, hosted by the German Ministry for Economic Cooperation an Development and the German devel-opment organisation giz (formerly gtz) on the appropriate tax measures and policies to improve the situation in de-veloping countries. He argued that the existence of a qualified tax profession in developing countries would facilitate compliance for enterprises and be a re-liable partner for the administration.

On 29 and 30 September, the 123rd meeting of the CFE Fiscal Commit-tee was held in Malta. Among the topics discussed was the European Commission´s CCCTB proposal, measures at national level to raise tax revenues and consolidate budgets and OECD developments, in particular the Guidelines on Multinational Enterpris-es. The Committee decided to have annual updates of the CFE Transfer Pricing summary issued in June 2011.

Direct Tax Sub-Committee Chairman Ian Young attended the meetings of the United Nations´ “Committee of Experts in International Co-operation in Tax Matters” in Geneva from 24-28 Octo-ber 2011.

On 24 November 2011, CFE submitted its Opinion Statement on the CCCTB proposal to the European institutions, the representations of member states and a number of associations.

On the same day, Gottfried Schellmann attended a workshop on property taxa-tion and enhanced tax administration hosted by the European Commission´s Directorate-General for Economic and Financial Affairs in Brussels.

On 8 December 2011, Isabelle Rich-elle and Volker Heydt (both ECJ Task Force) spoke on a European Parlia-ment workshop on double taxation in Brussels.

The European Commission´s Business Expert Group on VAT in which the CFE participates met on 25 October and 8 December 2011 in Brussels. CFE participants are currently: Indirect Tax Sub-Committee Chairman Christian Amand, Petra Pospišilova and Tomasz Michalik.

On 30 January 2012, the Fiscal Com-mittee met for the 124th time in Brus-sels. The Committee members dis-cussed with guest speaker Bertrand Lapalus from the European Commis-sion the reform of the EU VAT system. Another subject discussed was the CFE response to the public consulta-tion of OECD on changes to the Com-mentary to Art.5 of the Model Tax Con-vention on Permanent Establishment. The CFE Opinion Statement on this matter was submitted to OECD on 17 February 2012.

On the same day, CFE hosted the 2012 Tax Dinner with representatives from the European Institutions (see related page in this Newsletter).

ECJ Task Force

The ECJ Task Force met on 27 Octo-ber 2011 in Brussels and on 31 Janu-ary 2012 in Vienna. Between Septem-ber 2011 and February 2012, it adopted Opinion Statements on three ECJ cas-es. These concerned the tax treatment of inbound dividends in the EU and in relations with EEA and third countries (Haribo and Österreichische Salin-en, C-436 and 437/08), the evidential requirements imposed by the ECJ in the context of infringement procedures (Commission vs. Portugal, C-105/08) and the ECJ case-law on transfer pric-ing related to loans (SGI, C-311/08).

Professional Affairs Committee At its 29 September 2011 meeting, the PAC dealt a.o. with the implementa-tion of the EU Services Directive, the Professional Qualifications Green Pa-per and service standardisation. The Committee also completed its survey on the involvement of tax advisers in legislation and its effect on national tax laws in which 18 CFE member bodies from 16 countries had participated. On 7 October 2011, the CFE submitted its Opinion Statement on the Profes-sional Qualifications Green Paper.

On 11 October 2011, Stephen Cole-clough, Ian Hayes and Rudolf Reibel took part in a meeting in London with delegates from AOTCA (Asia Oce-ania Tax Consultants Association) and STEP (Society of Trust and Estate Practitioners) preparing a common re-search project to be presented in 2012 involving member bodies of the three bodies from more than 35 countries.

On 7 November 2011, CFE Vice Presi-dent Henk Koller took part in a panel discussion on cross-border mobility of professionals at the “Public Conference on the Modernisation of the Profession-al Qualifications Directive” organised by the EU Commission in Brussels.

On 29 November 2011, CFE hosted its 4th Professional Affairs Conference in Brussels on “New regulatory trends for tax advisers” (see related article in this Newsletter).

The CFE Opinion Statement on the proposal for an EU Regulation on Standardisation was submitted to members of the European Parliament on 24 January 2012.

On 2 February 2012, Ian Hayes and Rudolf Reibel attended a conference on the proposal for modernisation of the Professional Qualifications Direc-tive in Brussels, hosted by the EU Commission.

CFE NEWS 1/2012

6

CFE NEWS 1/2012

CFE InternalCFE Participation in other events since July 2011:

On 20 October 2011, CFE President Stephen Coleclough represented CFE as a panellist at a conference in Malta on the future of VAT, hosted by the Malta Institute of Management.

On 11 November 2011, Stephen Coleclough attended the 31st National Congress of the Italian CFE member organisation ANTI in Turin.

On 18 November 2011, the President spoke at the AOTCA Annual International Taxation Seminar in Bali about recent OECD developments.

On 1 December 2011, Uta Gayer and Rudolf Reibel from the CFE Office gave a presentation on CFE and the European tax profession at the “Forum for the Future” in Brussels, the Belgian congress of the economic professions, co-hosted by the Belgian Institute of Accountants and Tax Advisers.

On 2 and 3 February 2012, CFE President Stephen Coleclough and the Board members Gottfried Schellmann, Herbert Becherer and Jiři Nekovář spoke at a conference on the occasion of the 10th anniversary of the Rus-sian Chamber of Tax Advisers.

CFE NEWS 1/2012CFE NEWS 1/2012

CFE NEWS 1/2012

7

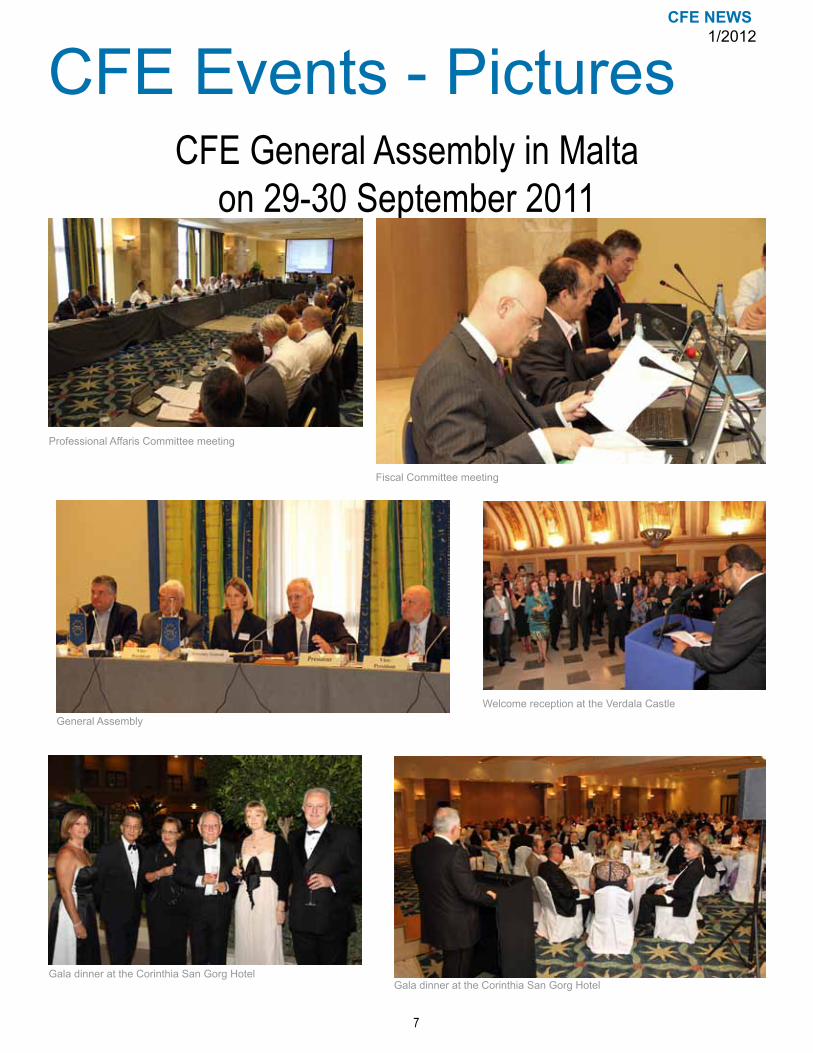

CFE Events - PicturesCFE General Assembly in Malta

on 29-30 September 2011

Fiscal Committee meeting

Welcome reception at the Verdala Castle

Gala dinner at the Corinthia San Gorg Hotel

Professional Affaris Committee meeting

Gala dinner at the Corinthia San Gorg Hotel

General Assembly

CFE NEWS 1/2012

8

CFE NEWS 1/2012

CFE Professional Affairs Conference on 29 November 2011

Bob van der Made (PricewaterhouseCoopers, The Netherlands), Tina Riches (CIOT, UK) and Stephen Coleclough (CFE)

Marioara Piroi and Mihaela Gabriela Piroi (both SC Group Expert Con-sulting 2000 SPL, Romania) and Florentina Susnea (Camera Consul tantilor Fiscali, Romania)Sophie Maletras and Martin Frohn (both European Commission) and Uta Gay-

er (CFE)

Participants to the CFE Professional Affairs Conference on 29 November 2011

Ian Hayes (CFE) and Brian Redford (HMRC, UK)

André Bert (IAB/IEC, Belgium), Dick Barmentlo (KPMG, The Netherlands) and Henk Koller (CFE)

CFE NEWS 1/2012CFE NEWS 1/2012

CFE NEWS 1/2012

9

Piergiorgio Valente (CFE), Gottfried Schellmann (CFE) and An-dreas Strub (Council of the EU)

Piergiorgio Valente (CFE) and Kestutis Sadauskas (Euro-pean Commission)

Sabev Momchil (European Commission) and Stephen Coleclough (CFE)

Kestutis Sadauskas (European Commission), Thomas Carroll (European Commission) and Gilles Mourre (European Commission)

Ian Young (CFE) and Pervenche Berès (European Parliament)

Gottfried Schellmann (CFE), Rolf Diemer (European Commission) and Herbert Becherer (CFE)

CFE Annual Tax Dinner on 30 January 2012

CFE NEWS 1/2012

10

CFE NEWS 1/2012

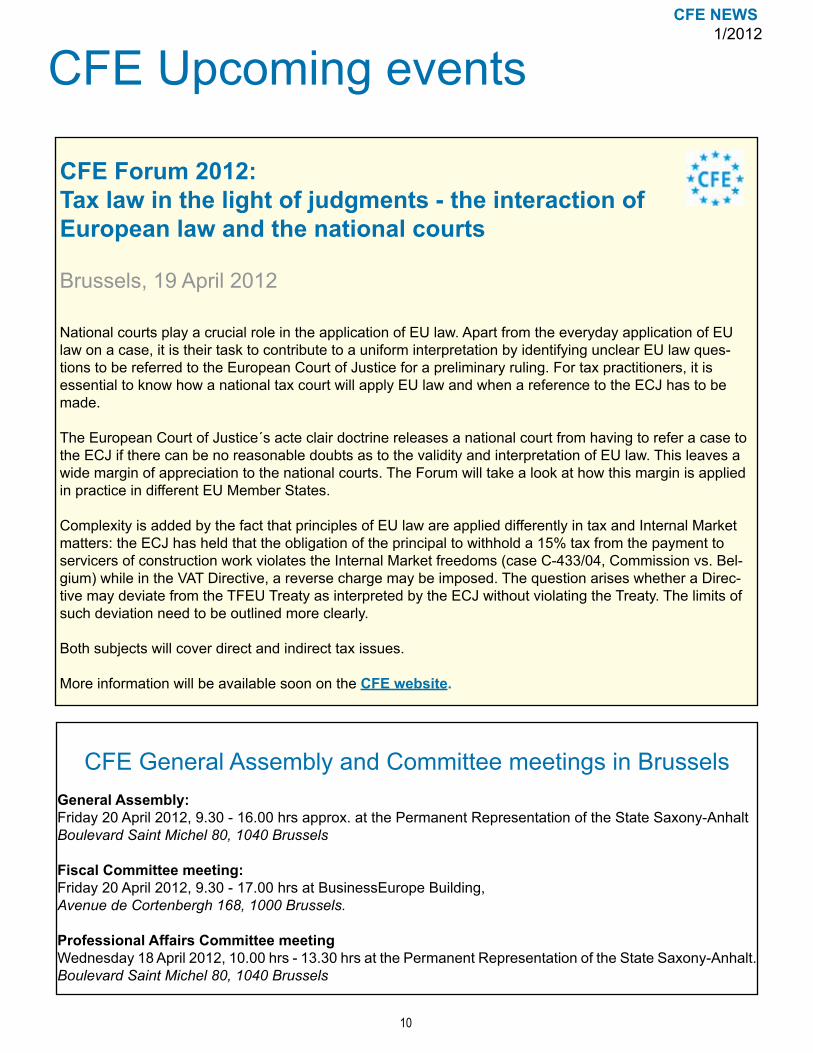

CFE Forum 2012:Tax law in the light of judgments - the interaction of European law and the national courts

Brussels, 19 April 2012

National courts play a crucial role in the application of EU law. Apart from the everyday application of EU law on a case, it is their task to contribute to a uniform interpretation by identifying unclear EU law ques-tions to be referred to the European Court of Justice for a preliminary ruling. For tax practitioners, it is essential to know how a national tax court will apply EU law and when a reference to the ECJ has to be made.

The European Court of Justice´s acte clair doctrine releases a national court from having to refer a case to the ECJ if there can be no reasonable doubts as to the validity and interpretation of EU law. This leaves a wide margin of appreciation to the national courts. The Forum will take a look at how this margin is applied in practice in different EU Member States.

Complexity is added by the fact that principles of EU law are applied differently in tax and Internal Market matters: the ECJ has held that the obligation of the principal to withhold a 15% tax from the payment to servicers of construction work violates the Internal Market freedoms (case C-433/04, Commission vs. Bel-gium) while in the VAT Directive, a reverse charge may be imposed. The question arises whether a Direc-tive may deviate from the TFEU Treaty as interpreted by the ECJ without violating the Treaty. The limits of such deviation need to be outlined more clearly.

Both subjects will cover direct and indirect tax issues.

More information will be available soon on the CFE website.

CFE Upcoming events

CFE General Assembly and Committee meetings in BrusselsGeneral Assembly: Friday 20 April 2012, 9.30 - 16.00 hrs approx. at the Permanent Representation of the State Saxony-AnhaltBoulevard Saint Michel 80, 1040 Brussels

Fiscal Committee meeting: Friday 20 April 2012, 9.30 - 17.00 hrs at BusinessEurope Building, Avenue de Cortenbergh 168, 1000 Brussels.

Professional Affairs Committee meetingWednesday 18 April 2012, 10.00 hrs - 13.30 hrs at the Permanent Representation of the State Saxony-Anhalt.Boulevard Saint Michel 80, 1040 Brussels

CFE NEWS 1/2012CFE NEWS 1/2012

CFE NEWS 1/2012

11

Member Organisations’ Pages

New Presidium of the Chamber of Tax Advisers of the Czech Republic

The new members of the KDP ČR bodies were elected at the Election General Meeting held on 7 October 2011 in Prague, Žofín Palace.The new President of the Chamber of Tax Advisers of the Czech Republic is Mrs. Alena Foukalová who has replaced, after fifteen years, Mr. Jiří Nekovář, who did not candidate for this post for another election period anymore. Mr. Martin Tuček has become the Vice President of the Chamber.The Chamber Presidium was elected in the following composition (from the left): Edita Ševcovicová, David Hubal, Jiří Nesrovnal, Alena Foukalová (President), Martin Tuček (Vice President), Jana Skálová, Tomáš Hajdušek, Zdeněk Burda, Milan Vodička.

New Presidium of the Chamber of Tax Advisers of the Czech Republic

International German Tax Advisers Congress in Nice

The sixth international congress of Bundessteuerber-aterkammer will take place on 27th and 28th September 2012 this year in the south of France. The congress offers the opportunity to tax advisers from other countries to get information about important rules which must be followed by their clients who wish to establish a branch in France or invest in real estates. Experts in legal and tax questions, mostly French residents, will update the attendants with everything worth knowing. The participants will enjoy an extraordinary social program offering a gala dinner in the legendary Hotel “Negresco” and interesting excursions.

50th annual German Congress for Tax Advisers in Berlin

On 7th and 8th May 2012 BStBK will hold its traditional annual German congress for tax advisers (DEUTSCHER STEUERBERATERKONGRESS) for the fiftieth time. The most prominent speaker will be the German Minister of Fi-nance, Dr. Wolfgang Schäuble. In addition to various work-shops and fora this congress, that attracts every year well over 1,300 participants, offers to its visitors from Germany and abroad an excellent platform for interesting discussions and new contacts with colleagues and guests from politics, business and administration. A festive and interesting so-cial program will complete the event and will invite you to discover new sides of Berlin, a permanently changing city.

For more details and to register please click on the BStBK website

Professor Dr. Albert J. Rädler

We deeply regret that Prof. Dr. Albert J. Rädler passed away on Saturday, 25 February 2012.Professor Rädler, Chairman of the CFE Fiscal Committee from 1985 – 1988 and awarded with the CFE Badge of Honour in 2009 for his out-standing services to the CFE, was an internationally recog-nized authority in the field of taxation and an advocate of the CFE.Through his decades of commitment to the CFE Fiscal Committee he contributed greatly to the excellent reputation enjoyed by this committee today.

We shall dearly miss Professor Rädler.

Dr. François Lambrechts

We are very sad to inform you that Dr. François Lambrechts passed away on Sat-urday, 25 February 2012.

Dr. Lambrechts, President of the CFE in 2002, and later on Honorary President was a fellow of the first hour, convinced by the idea of a European tax adviser organisation and its objectives for the profession.

Throughout his life he felt deeply attached to the organisation and showed great interest in the progress of the CFE.

We shall dearly miss Dr. Lambrechts.

CFE NEWS 1/2012

12

CFE NEWS 1/2012

LL.M. International Tax Law Viennawww.international-tax-law.at

In a time of globalization, international tax law has gained in importance. The LL.M. program at the WU meets the increas-ing demands for training and education by offering courses the intensity of which is second to none worldwide. Both the full-time and part-time programs are aimed at university grad-uates from all parts of the world who would like to acquire additional specialist knowledge, as well as at professionals wishing to participate in such a program while they continue to work. The main emphasis is on conveying specialist knowl-edge in international tax law, as well as on making an interdis-ciplinary link to related areas of knowledge. With renowned experts from all over the world as lecturers, education at the highest international level with a great degree of practical relevance is guaranteed. The academic degree “Master of Laws” (LL.M.) is conferred on all graduates in accordance with the rules and regulations of the Austrian University Act.

The next full-time course starts in September 2012, deadline for applications is April 15, 2012.

In co-operation withAkademie der Wirtschaftstreuhänder

Czech-Slovak Forum

The Chamber of Tax Advisers of the Czech Re-public organises, together with the Slovak Chamber of Tax Advisers, the 5th common conference focused on the topic “Tax issues in the context of Czech and Slovak tax laws”. Besides tax advisers, the conference will be attended also by representatives of the Supreme Administrative Courts and state administrations from both the countries. The topics for discussion will be in particular – Tax-recognisable and non-tax-recognisable expenses in the link to accounting – material and time contexts of expenses and incomes – selected prob-lems. Tax-recognisable and non-tax-recognisable expenses. Contingency items in accounting and taxes. Errors in the field of accounting and impacts on income tax while respecting preclusion. Selected judgements and explanations to tax-recognisable and non-tax-recognisable expenses. Carrousel deals from the viewpoint of VAT with a focus on practical parts of issues supported by case law.The conference will be held on 16-17 April 2012 in Brno in the Congress Hall of Hotel Continental, the official languages being Czech and Slovak, interpretation into other languages is not ensured.

For more information please visit the web site of the Cham-ber: http://www.kdpcr.cz/.

3rd International Conference “Taxes without borders”, Poland-Germany

On 9-10 September 2011 the regional branches of the Polish National Chamber of Tax Advisers (Lubuski, Wielkopolski, Dolnośląski, Zachodniopomorski) organ-ized in Zielona Góra the 3rd International Conference “Taxes without borders”. It was held in co-operation with Brandenburg Chamber of Tax Consultants (Steuerber-aterkammer Brandenburg). This year the discussion fo-cused on VAT implications of international supplies, in particular chain and triangular transactions. The event was attended by the tax administration representa-tives, judges of the administrative courts, tax academics and tax practitioners from both countries co-organizing the conference, as well as special quests from Russia, Ukraine and the Czech Republic.

Tax Seminar in Ostrava, Poland-Czech Republic

On 5 September 2011 the Chamber of Tax Advisers of the Czech Republic in cooperation with the Polish National Council of Tax Advisers held an extraordinary Czech-Polish seminar on the topic of the ”Basics of the Polish tax system in terms of Income Tax, Employment and VAT”. It gave the insight into the fundamentals of the Polish tax law, as viewed from the practical perspective.

The 2012 International Tax Conference

The 2012 International Indirect Tax Conference organ-ised by the IIT and CIOT will take place on Tuesday 21 February 2012 at the Royal Garden Hotel in London. Jointly chaired by Stephen Coleclough, President of the Confederation Fiscal Europeenne and Vice-President of the CIOT, and Michael Conlon QC, President of the IIT, the conference will bring together leading specialists with multinational corporations, top professional firms and Governmental specialists. More details can be found on the CFE Events page.

New website and contact number of APCF

The Associação Portuguesa de Consultores Fiscais (APCF) has a new website: www.apcf.eu

as well a new phone number: +351 (0)2 109 36 108

CFE NEWS 1/2012CFE NEWS 1/2012

CFE NEWS 1/2012

13

Impressum

EditorDr. Herbert Becherer (CFE Vice-President)

Contents (unless otherwise indicated):

Rudolf Reibel LL.M. (Fiscal and Professional Affairs Officer, CFE Brussels Office)

LayoutLaëtitia Bois (Administrative Assistant, CFE Brussels Office)

DisclaimerThe Confédération Fiscale Européenne (CFE) distributes this report to enhance public access to information about European policies in general. The CFE accepts no responsibility or liability whatsoever with regard to the material. The links will connect you to sites which are in no way controlled by the CFE, and CFE is not responsi-ble for their content, or indeed for any further links which may support.

CFE Office Confédération Fiscale Européenne188A, Av. de TervurenB-1150 [email protected]

CFE General SecretariatHaus der Steuerberater Behrenstrasse 42D-10117 [email protected]

UnsubscribeTo unsubscribe from this newsletter, please send an email to:[email protected]

CommentsIf you have comments please do not hesitate to contact the Brussels office at [email protected] or phone number +32 2 761 00 91.