CEZ Virtual Power Plant Auction 2006 · cez´s virtual power plant auction within ... blok 1 blok 2...

21

CEZ´S VIRTUAL POWER PLANT AUCTION WITHIN THE FRAMEWORK OF REGIONAL POWER MARKET DEVELOPMENT Press conference ČEZ, a. s. Hotel Palace, 25.7.2006 Alan Svoboda, Managing Director Sales and Trading Michal Skalka, Director Trading

Transcript of CEZ Virtual Power Plant Auction 2006 · cez´s virtual power plant auction within ... blok 1 blok 2...

CEZ´S VIRTUAL POWER PLANT AUCTION WITHIN THE FRAMEWORK OF REGIONAL POWER MARKET

DEVELOPMENT

Press conference ČEZ, a. s.Hotel Palace, 25.7.2006

Alan Svoboda, Managing Director Sales and TradingMichal Skalka, Director Trading

1

AGENDA

Regional power markets development Alan Svoboda

Regional power balance development

Price signal from surrounding countries

Virtual Power Plant auction Michal Skalka

Auctions in surrounding countries

Virtual Power Plant auction procedure

2

GERMAN POWER PRICES AS BENCHMARK FOR THE REGION CONTINUE INCREASING

EEX Forward 2007 (baseload)EUR/MWh

20

30

40

50

60

1/2004 5/2004 9/2004 1/2005 6/2005 10/2005 2/2006 6/2006

1 year forward

2 years forward

Source: EEX

Forward 2007

58.75 EUR/MWh

(17/7/2006)

3

0

10

20

30

40

1/2005 5/2005 9/2005 1/2006 5/2006

GERMAN PRICES ARE DRIVEN BY GROWING OIL PRICES, CO2

ALLOWANCES AND SUPPLY DEMAND SQUEEZE

30

40

50

60

70

80

1/2005 5/2005 9/2005 1/2006 6/2006

Brent oilUSD / bl

CO2 allowancesEUR/t

Source: Bloomberg, ECX

Growing supply / demand squeeze

Summer power blackouts in Europe happen regularly for several years … Reserves (of power supply) are low. (HN – Czech Business Daily)

Shutdowns of power plants in Germany and France enforced by current high temperatures reached several thousands megawatts installed capacity. (Platts)

Solution to the lack of supply is often import (France – the biggest power exporter – imported approx. 1,000 MW) or initiation of expensive backup units. (Platts,HN)

4

LACK OF POWER IMPACTS THE WHOLE REGION AND SPOT PRICES IN CRITICAL MOMENTS GROW SKY HIGH

Source:OTE, EEX, Platts

0

50

100

150

200

250

300

01.07

.2006

02.07

.2006

03.07

.2006

04.07

.2006

05.07

.2006

06.07

.2006

07.07

.2006

08.07

.2006

09.07

.2006

10.07

.2006

11.07

.2006

12.07

.2006

13.07

.2006

14.07

.2006

15.07

.2006

16.07

.2006

17.07

.2006

18.07

.2006

19.07

.2006

20.07

.2006

21.07

.2006

22.07

.2006

€/M

Wh

EEX and OKO* prices in July 2006(EUR/MWh, spot)

OKO

EEX

50 %840 MWNeckar -1

5 %1,440 MWBrokdorf

20 %806 MWBrunsbuttel

25 %1,316 MWKrummel

30-70 %1,310 MWUnterweser

Capacity reduce by CapacityPlant

Shutdowns in the region

* OKO = Czech Spot Market, organized by OTE

5

0

50

100

150

200

250

300

9.1.200

6 po

10.1.20

06 út

11.1.20

06 st

12.1 .20

06 čt

13.1.20

06 pá

14.1.20

06 so

15.1.20

06 ne

16.1 .20

06 po

17.1 .20

06 út

18.1.20

06 st

19.1.20

06 čt

20.1 .20

06 pá

21.1.20

06 so

22.1.20

06 ne

23.1.20

06 po

24.1.20

06 út

25.1 .20

06 st

26.1 .20

06 čt

27.1 .20

06 pá

28.1 .20

06 so

29.1 .20

06 ne

30.1.20

06 po

31.1 .20

06 út

Source:OTE, EEX

ČEPS´s actions are required more frequently to maintain stability of suppliesTowards that it must secure enough system tools (reserve capacity)Imports at 5,000 to 10 000 CZK/MWh

OKO

EEXEEX and OKO prices in January 2006(EUR/MWh, spot)

ALSO THE REQUIREMENTS OF GRID STABILITY MANAGEMENT GROW REGARDLESS THE COSTS

6

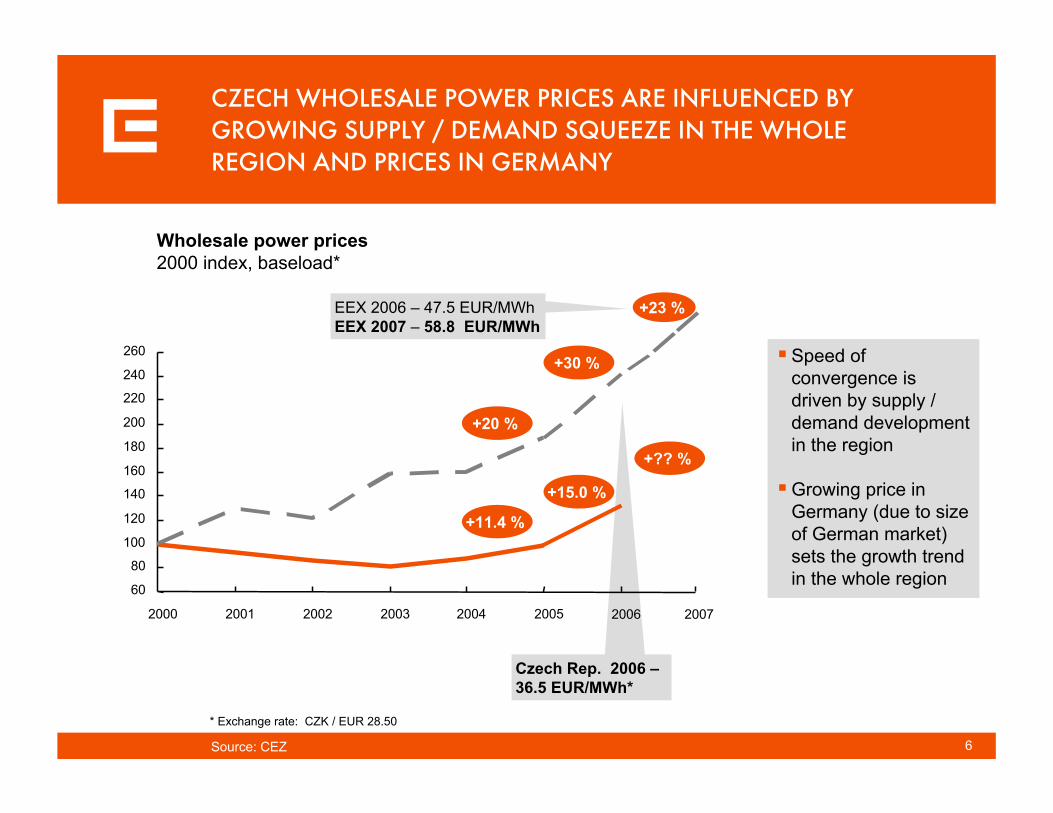

Wholesale power prices2000 index, baseload*

EEX 2006 – 47.5 EUR/MWhEEX 2007 – 58.8 EUR/MWh

Czech Rep. 2006 –36.5 EUR/MWh*

Speed of convergence is driven by supply / demand development in the region

Growing price in Germany (due to size of German market) sets the growth trend in the whole region

60

80

100

120

140

160

180

200

220

240

260

2000 2001 2002 2003 2004 2005 2006

+11.4 %

+15.0 %

+30 %

+20 %

2007

+23 %

+?? %

Source: CEZ

* Exchange rate: CZK / EUR 28.50

CZECH WHOLESALE POWER PRICES ARE INFLUENCED BY GROWING SUPPLY / DEMAND SQUEEZE IN THE WHOLE REGION AND PRICES IN GERMANY

7

36.5

47.5 47.5

62.0

74.0

~ 41.0~ 36.5

WHOLESALE PRICES IN THE CZECH REPUBLIC ARE STILL AMONGTHE LOWEST IN THE REGION THANKS TO UNRESERVED CAPACITY

Centrel

EEX

Czech Republic

Slovakia Hungary Germany Austria UK Italy

Wholesale power price*2006, baseload, EUR/MWh

Source:CEZ, Eurostat

* Comparing 2006 forward price as of 2005, assuming CZK/EUR 28.50

Rest of Europe

Prices in individual regions will converge over time driven by actions of tradersand increasing interconnectivity

8

5860626466

68707274

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

THANKS TO GROWTH OF ECONOMY POWER DEMAND IN THE CZECH AND SLOVAK REPUBLICS WILL INCREASE BY 10 TWH

25

26

27

28

29

30

31

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

CR

SR

Consumption in TWh

Source: CR: ERÚ,CEZ; SR: UCTE

By 2012 Czech consumption will increase by 7 TWh and Slovak by 3 TWh

Significant demand growth is driven by economy growth and FDI (TPCA and Hyundai in CR, PSA in SR)

Based on H1 2006 development Czech consumption is likely to grow even faster

Yoy change in 2007 in Czech and Slovak Republics to reach approx. 2 TWh

yoy change 2.0%

yoy change 1.3%

Growth in 1 - 5/2006 4.0%resp. 3.3 % ( normalized temperature)

Actual data 2002 - 2005

Actual data 2002 - 2005

Industrial production growth 1 - 5/2006

12.3 %

GDP growth Q1 2006

7.4%

Consumption in TWh

9

BY 2020 20 GW INSTALLED CAPACITY WILL REACH END OF ITS LIFETIME

Supply / Demand development in CENTREL(CR, SR, Hungary, Poland), GW*

0

10

20

30

40

50

20 GW CENTREL´s reserve capacity on fast decline

Significant investments in power generation will be needed to secure self-sufficiency in power

Mere capacity renewal will not be enough to meet growing demand

Also availability of Polish coal power is already uncertain

High demand

Medium demand

Low demand

* peak demand vs. net installed capacity

Nuclear

Lignite

Hardcoal

Oil/gas

Hydro

Source: CEZ

~

10

0

1 000

2 000

3 000

4 000

5 000

2006 2007 2008 2009 2010 2011

SLOVAKIA ALONE WILL LOSE 25% OF POWER IN THE NEXT THREE YEARS WITHOUT REPLACEMENT AND WILL CEASE TO BE SELF-SUFFICIENT IN POWER PRODUCTION

Starting 2007 Slovakia will cease to be self-sufficient in power generation

Source: Platts, CEZ, SE

gas

hydro

nuclear

coal

- 24%

Available capacity in SlovakiaMW

Nováky A

Nováky B

Vojany 1

Vojany 2

J. Bohunice

J. Bohunice

IPP

Total 2006

Total 2008

Totalcumulative

TG 2 a TG

blok 3 a 4

blok 3 a 4

blok 25 a 26

blok 1

blok 2

2006

2008

2006-2010

2006-2010

54

220

220

220

440

440

200

1,154

440

1,794

Plant UnitCapacity

(MW)Shutdown

year

Yoy capacitydecline 14%

11

CEZ WILL MOVE MOST OF ITS EXPORTS TO SLOVAKIA AND HUNGARY

0%10%20%30%40%50%60%70%80%90%

2004 2005 2006 2007

GermanySlovakia

Source:CEZ

Germany60 / 40

Austria7 / 5

Slovakia30 / 55

EUR 0.13**

EUR 12.5**

Poland3 / 0

Germany

AustriaSlovakia

Hungary

Poland CEZ´s power export structure in %

Export TWh

2.7 2.3-2.2

Czech – SlovakPower import / export balance

2005 2006 2007

20 16 14 14

12

FAST DEMAND GROWTH ALONG WITH SIGNIFICANT POWER CAPACITY DECOMISSIONING AT THE END OF THIS YEAR WILL RESULTY IN 8 TWH DEFICIT

0.4

2.7

1.4

1.4

2.2

8.1

Demandgrowth

J.Bohuniceshutdown

Vojany andNováky

shutdown

Demandgrowth

Tušimiceshutdown

Yoy balancechange in CR

and SR

Elimination of deficit of >8 TWh (approx. 11% CR demand) possible only via

imports orinitiation of expansive units (till now reserved)

Both will have a strong impacton regional wholesale price development

Yoy change of power balance in CR and SRTWh

Source:Slovak balance change – Platts, Energy in East Europe Issue 82 (decreased by 10% to reflect own consumption); CEZ

Temporaryduring retrofit

SR ČR

13

ERA OF RESERVE CAPACITY SURPLUS USED FOR EXPORTS OUTSIDE OF CZECH AND SLOVAK REPUBLICS WILL BE OVER IN THREE YEARS

Source: CEZ

105

110

115

120

125

2006 2007 2008 2009 2010 2011

Czech and Slovak power market supply and demand development TWh

supply in CR+SR, incl. imports from Poland and Ukraine

demand in CR+SR, incl. possible export to Germany, Austria and Hungary Need to operate

more expansive and less reliable capacity More frequent price spikes and crisis situations including risk of black-outsNeed for fast new capacity construction

8.1 2.9 5.9 2.8 4.6Annual change

14

DEFICIT CAN BE COVERED BY IMPORTS FROM MORE EXPANSIVE MARKETS OF GERMANY AND AUSTRIA RESP. BY LOWERING EXPORTS TO THESE COUNTRIES

Poland

Hungary

Ukraine

Source: UCTE, CEPS

First case: due to problems in Polish grid CEPS provided 400MW emergency support; Second case: due to cumulative 200MW generation fallout

Breach of confirmed contracts should happen only in exceptional cases

Poland is likely to lower exports in the next year; in July 2006 PSE twice canceled contracted cross border supplies due to lack of generation outputIn 2008 – 2015 complete decommissioning of up to ~5000 MW is expected due to environmental concerns

Already in deficit (2005 imports of 16% total consumption, prices at German levels)

Limited export possibilities of Burstyn island of 550 MW exhausted (UCTE technical limits), additionally used for supplies to Hungary

15

EU ETS INCENTIVISED CEZ TO ACCELERATE AND INCREASE ITS INVESTMENTS IN GENERATION

EU ETS driven plan**

Original plan

2005 07 10 12 15 2020

€ 700 M

€ 350 M

30 Mton

34 Mton

38 Mton

INVE

STM

ENTS

*EM

ISSI

ON

S

NAP

Source:CEZ

* CO2 directly related projects

ILUSTRATIVE SCENARIO

16

AGENDA

Regional power markets development Alan Svoboda

Regional power balance development

Price signal from surrounding countries

Virtual Power Plant auction Michal Skalka

Auctions in surrounding countries

Virtual Power Plant auction procedure

17

2006

Commodityexchange

Tradingtransac.

Bilateraltransac.

36.5

42.0

43.2 – 44.0

First indicators of 2007 wholesale prices in the regionEUR/MWh*

2007

2006

SEauction

Discotenders

36.5

42.8 – 44.6

~ 42.5

2007

2006

Tradingtransac.

40.0

47.52007

PRICE LEVEL OF ALREADY SIGNED CONTRACTS IN THE REGION CONFIRMS THAT THERE IS AN INCREASING MARKET DEMAND FOR ELECTRICITY CONTRACTED 1 YEAR AHEAD

Source:CEZ, SE, MVM, TFS, Press clippings, KBK; transactions executed in 2006

Note: CZK/EUR 28.50, SKK/EUR 38.6, HUF/EUR 280.0

CR66

SR29

Hungary39

5

15

10

In the map volume traded in TWh (est.) vs. respective country's consumption

18

CEZ WILL OFFER THE VIRTUAL POWER PLANT ON EQUAL TERMS (SET BY THE ANTITRUST OFFICE) THIS YEAR AS LAST YEAR

Basic facts

Requirement to offer VPP in public auction set by the Antitrust Office as one of the conditions for integration of CEZ + 5 DISCOS

VPP guarantees third parties access to CEZ generation capacity, including the possibility to place an exact shape of generation diagram

Total supply 400 MW (with decrease to 240 MW in summer months) divided into 8 blockswith 50 MW

Minimum output represents minimum electricity off-take in corresponding season so that the real power plants wouldn’t fall under the technical operation minimum

Available capacity of virtual power plant blockMW

0

10

20

30

40

50 maximum output

minimum output

1 2 3 4 5 6 7 8 9 10 11 12 months

zdroj: ÚOHS; ČEZ, a. s.

19

VIRTUAL POWER PLANT IS AGAIN OF A HIGH INTEREST

Auction participants can be energy traders financially and personally independent on CEZ, a. s.

Auction is set up by independent auction office Fin-servis, a.s.www.fsk.cz

Number of registered participants

zdroj: ČEZ, a. s.

31.5.2006auction

announcement

3.7.2006start of the

registration round

26.7.2006 at 15.00 hodin

end of the registration round

2.8.2006 start of the 1st

auction round

0

5

10

15

20

25

2005 2006

reguests 44 ?

Already confirmed17

20?16

20

EVALUATION AND PUBLICATION OF AUCTION RESULTS WILL TAKE PLACE IMMEDIATELY AFTER IT’S TERMINATION ON 2.8.

Virtual power plant auction takes place on 2.8.2006 at the premises of Ceskomoravska komoditní burza Kladno, nam. Sitna 3105 organized by independent auction office Fin-servis, a.s.

CEZ expects further electricity sales until the complete sources exhaustion by auctions

CEZ will inform about all sales auctions without delay