Cesar Chavez High School Charter School (A … · Cesar Chavez High School Charter School ......

86

Report of Independent Auditors and Financial Statements with Supplementary Information for Cesar Chavez High School Charter School (A Component Unit of Deming Public Schools) June 30, 2016

Transcript of Cesar Chavez High School Charter School (A … · Cesar Chavez High School Charter School ......

Report of Independent Auditors and Financial Statements

with Supplementary Information for

Cesar Chavez High School Charter School

(A Component Unit of Deming Public Schools)

June 30, 2016

INTRODUCTORYSECTION

ANNUALFINANCIALREPORTYEARENDEDJUNE30,2016

TABLEOFCONTENTS

Exhibit PageINTRODUCTORYSECTION DirectoryofOfficials 1FINANCIALSECTION ReportofIndependentAuditors 2 BasicFinancialStatements: Government‐wideFinancialStatements: StatementofNetPosition A‐1 6 StatementofActivities A‐2 7 FundFinancialStatements: BalanceSheet–GovernmentalFunds B‐1 8 ReconciliationoftheBalanceSheettotheStatementofNetPosition B‐1 10 StatementofRevenues,Expenditures,andChangesinFund Balances–GovernmentalFunds B‐2 11 ReconciliationoftheStatementofRevenues,Expendituresand ChangesinFundBalancesofGovernmentalFundstothe StatementofActivities B‐2 13 StatementofRevenues,Expenditures,andChangesinFund Balance–BudgetandActual OperatingFund(11000) C‐1 14 InstructionalMaterialsFund(14000) C‐2 15 TitleIIASAFund(24101) C‐3 16 TANF/GRADSFund(25152) C‐4 17 StatementofFiduciaryAssetsandLiabilities–AgencyFunds D‐1 18 Notestothefinancialstatements 19

Schedule PageREQUIREDSUPPLEMENTARYINFORMATIONSpecialRevenueFundsDescriptions 43CombiningBalanceSheet‐NonmajorSpecialRevenueFunds E‐1 44CombiningStatementofRevenues,ExpendituresandChangesinFund Balances‐NonmajorSpecialRevenueFunds E‐2 45StatementofRevenues,Expenditures,andChangesinFundBalance‐ BudgetandActual IDEA‐BEntitlementFund(24106) E‐3 46 TitleISchoolImprovementFund(24162) E‐4 47 MicrosoftSettlementFund(26170) E‐5 48 TeacherMentoringFund(27154) E‐6 49 PublicSchoolCapitalOutlayFund(31200) E‐7 50ScheduleofProportionateShareofNetPensionLiabilityofthe EducationalRetirementBoard F‐1 51ScheduleofContributionstotheEducationalRetirementBoardPensionPlan F‐2 52Notestorequiredsupplementalinformation F‐2 53

ANNUALFINANCIALREPORTYEARENDEDJUNE30,2016

TABLEOFCONTENTSSchedule Page

OTHERSUPPLEMENTALINFORMATION ScheduleofChangesinFiduciaryAssetsandLiabilities–AgencyFunds I 54 ScheduleofCollateralPledgedbyDepositoryforPublicFunds II 55 ScheduleofIndividualDepositAccounts III 56 ScheduleofCashReconciliation IV 57OTHERINFORMATION ScheduleofVendorInformation V 59ADDITIONALREPORTINGREQUIREMENTS ReportofIndependentAuditorsonInternalControloverFinancial ReportingandonComplianceandotherMattersBasedon anAuditofFinancialStatementsPerformedinAccordancewith GovernmentAuditingStandards 60 SummaryScheduleofPriorAuditFindings 62 ScheduleofFindingsandResponses 63 ExitConference 77

1

CESARCHAVEZHIGHSCHOOLCHARTERSCHOOLCOMPONENTUNITOFDEMINGPUBLICSCHOOLS

DIRECTORYOFOFFICIALSJUNE30,2016

GOVERNINGCOUNCIL AntoinetteZunich President VictorCruz Vice‐President NeimaHiguera Treasurer GloriaLopez Secretary GabeDominguez Member

SCHOOLOFFICIALS StanLyons Principal ChrisMasters BusinessManager

FINANCIALSECTION

2

REPORTOFINDEPENDENTAUDITORSGoverningCouncilCesarChavezHighSchoolCharterSchoolandTimothyKellerNewMexicoStateAuditorReportontheFinancialStatements

Wehaveauditedtheaccompanyingfinancialstatementsofthegovernmentalactivities,eachmajorfund,andtheaggregateremainingfundinformation,andthebudgetarycomparisonsfortheoperatingfundsand major special revenue funds of the Cesar Chavez High School Charter School (“Charter”), acomponentunitofDemingPublicSchools,asofandfortheyearendedJune30,2016,andtherelatednotestothefinancialstatements,whichcollectivelycomprisetheCharter’sbasicfinancialstatementsaslistedinthetableofcontents.WehavealsoauditedthefinancialstatementsoftheCharter’snonmajorgovernmental funds, fiduciary funds, and the respective budgetary comparisons for themajor capitalproject fund and all nonmajor funds presented as supplementary information, as defined by theGovernmentalAccountingStandardsBoard,inaccompanyingcombiningandindividualfundstatementsasofandfortheyearendedJune30,2016aslistedinthetableofcontents.Management’sResponsibilityfortheFinancialStatements

Management is responsible for the preparation and fair presentation of these financial statements inaccordancewithaccountingprinciplesgenerallyacceptedintheUnitedStatesofAmerica;thisincludesthe design, implementation, andmaintenance of internal control relevant to the preparation and fairpresentationoffinancialstatementsthatarefreefrommaterialmisstatement,whetherduetofraudorerror.Auditor'sResponsibility

Our responsibility is to express opinions on these financial statements based on our audit. Weconductedouraudit in accordancewithauditing standardsgenerallyaccepted in theUnitedStatesofAmericaand the standardsapplicable to financial audits contained inGovernmentAuditingStandards,issued by the Comptroller General of the United States. Those standards require that we plan andperformtheaudittoobtainreasonableassuranceaboutwhetherthefinancialstatementsarefreefrommaterialmisstatement.

Anauditinvolvesperformingprocedurestoobtainauditevidenceabouttheamountsanddisclosuresinthe financial statements. The procedures selected depend on the auditor’s judgment, including theassessmentof the risksofmaterialmisstatementof the financial statements,whetherdue to fraudorerror.InInmakingthoseriskassessments,theauditorconsidersinternalcontrolrelevanttotheentity’spreparationand fairpresentationof the financial statements inorder todesignauditprocedures thatare appropriate in the circumstances, but not for the purpose of expressing an opinion on theeffectivenessoftheentity’sinternalcontrol.Accordingly,weexpressnosuchopinion.

3

GoverningCouncilCesarChavezHighSchoolCharterSchoolandTimothyKellerNewMexicoStateAuditorAn audit also includes evaluating the appropriateness of accounting policies used and thereasonableness of significant accounting estimates made by management, as well as evaluating theoverallpresentationofthefinancialstatements.Webelievethattheauditevidencewehaveobtainedissufficientandappropriatetoprovideabasisforourauditopinions.Opinions

In our opinion, the financial statements referred to above present fairly, in allmaterial respects, therespective financial position of the governmental activities, each major fund, and the aggregateremaining fund information of the Cesar Chavez High School Charter School, a component unit ofDeming Public Schools, as of June 30, 2016, and the respective changes in financial position and therespective budgetary comparisons for the operating funds, special revenue funds and capital projectfundfortheyearthenendedinaccordancewithaccountingprinciplesgenerallyacceptedintheUnitedStatesofAmerica.Inaddition,inouropinion,thefinancialstatementsreferredtoabovepresentfairly,inall material respects, the respective financial position of each nonmajor special revenue fund andfiduciaryfundsoftheCesarChavezHighSchoolCharterSchoolasofJune30,2016,andtherespectivechanges in financial position and the respective budgetary comparisons for themajor capital projectfundandallnonmajorfundsfortheyearthenendedinaccordancewithaccountingprinciplesgenerallyacceptedintheUnitedStatesofAmerica.EmphasisofMatter

ReportingEntity

As discussed in Note 1, the financial statements of the School are intended to present the financialpositionandthechangesinfinancialpositionofonlyCesarChavezHighSchoolCharterSchool.Theydonotpurportto,anddonot,presentfairlythefinancialpositionofDemingPublicSchools,asofJune30,2016, the changes in its financial position for the year then ended in conformity in accordancewithaccountingprinciplesgenerallyacceptedintheUnitedStatesofAmerica.Ouropinionsarenotmodifiedwithrespecttothismatter.Restatement

AsdiscussedinNote17tothefinancialstatements,theCharter’smanagementdiscoveredcertainerrorsresulting in an overstatement of previously reported receivable balances. Accordingly, adjustmentstotaling$234,417havebeenmadetotheCharter’snetpositionasofJuly1,2015,tocorrecttheseerrors.Ouropinionsarenotmodifiedwithrespecttothismatter.

4

GoverningCouncilCesarChavezHighSchoolCharterSchoolandTimothyKellerNewMexicoStateAuditorOtherMatters

RequiredSupplementaryInformation

Management has omittedmanagement's discussion and analysis that accounting principles generallyaccepted in the United States of America require to be presented to supplement the basic financialstatements.Suchmissinginformation,althoughnotapartofthebasicfinancialstatements,isrequiredbytheGovernmentalAccountingStandardsBoardwhoconsiders it tobeanessentialpartof financialreporting for placing the basic financial statements in an appropriate operational, economic, orhistorical context. Our opinion on the basic financial statements is not affected by this missinginformation.Accounting principles generally accepted in the United States of America require that the Charter’sproportionateshareofthenetpensionliabilityandthescheduleoftheCharter’scontributionsonpages33 through38bepresented to supplement thebasic financial statements.Such information,althoughnot a part of the basic financial statements, is required by the Governmental Accounting StandardsBoard who considers it to be an essential part of financial reporting for placing the basic financialstatements in an appropriate operational, economic, or historical context. We have applied certainlimitedprocedures to the requiredsupplementary information inaccordancewithauditingstandardsgenerallyacceptedintheUnitedStatesofAmerica,whichconsistedof inquiriesofmanagementaboutthe methods of preparing the information and comparing the information for consistency withmanagement’s responses to our inquiries, the basic financial statements, and other knowledge weobtainedduringourauditofthebasicfinancialstatements.Wedonotexpressanopinionorprovideanassuranceontheinformationbecausethelimitedproceduresdonotprovideuswithsufficientevidencetoexpressanopinionoranyassurance.OtherSupplementalInformation

The Schedule of Changes in Fiduciary Assets and Liabilities‐Agency Funds, Schedule of CollateralPledgedbyDepositoryforPublicFunds,ScheduleofIndividualDepositAccounts,andScheduleofCashReconciliationare the responsibilityofmanagementandwerederived fromandrelatedirectly to theunderlying accounting and other records used to prepare the basic financial statements. Suchinformation has been subjected to the auditing procedures applied in the audit of the basic financialstatements and certain additional procedures, including comparing and reconciling such informationdirectlytotheunderlyingaccountingandotherrecordsusedtopreparethebasicfinancialstatementsor to the basic financial statements themselves, and other additional procedures in accordancewithauditingstandardsgenerallyaccepted in theUnitedStatesofAmerica. Inouropinion, theScheduleofChangesinFiduciaryAssetsandLiabilities‐AgencyFunds,ScheduleofCollateralPledgedbyDepositoryforPublicFunds,ScheduleofIndividualDepositAccounts,andScheduleofCashReconciliationarefairlystated,inallmaterialrespects,inrelationtothebasicfinancialstatementsasawhole.

5

GoverningCouncilCesarChavezHighSchoolCharterSchoolandTimothyKellerNewMexicoStateAuditorTheotherinformation,ScheduleofVendorInformationperthetableofcontentshasnotbeensubjectedtotheauditingproceduresappliedintheauditofthebasicfinancialstatements,andaccordingly,wedonotexpressanopinionorprovideanyassuranceonit.OtherReportingRequiredbyGovernmentAuditingStandardsInaccordancewithGovernmentAuditingStandards,wehavealsoissuedourreportdatedNovember23,2016, on our consideration of the Cesar Chavez High School Charter School’s, a component unit ofDemingPublicSchools,internalcontroloverfinancialreportingandonourtestsofitscompliancewithcertainprovisionsoflaws,regulations,contracts,andgrantagreementandothermatters.Thepurposeof that report is to describe the scope of our testing of internal control over financial reporting andcompliance and the results of that testing, and not to provide an opinion on internal control overfinancialreportingoroncompliance.ThatreportisanintegralpartofanauditperformedinaccordancewithGovernmentAuditing Standards in considering the Cesar ChavezHigh School Charter School’s, acomponentunitofDemingPublicSchools,internalcontroloverfinancialreportingandcompliance.

Albuquerque,NewMexicoNovember23,2016

BASICFINANCIALSTATEMENTS

19

CESARCHAVEZHIGHSCHOOLCHARTERSCHOOL(COMPONENTUNITOFDEMINGPUBLICSCHOOLS)NOTESTOTHEFINANCIALSTATEMENTSNote1–SummaryofSignificantAccountingPoliciesCesarChavezHighSchoolCharterSchool(the“Charter”)isorganizedunderthelawsoftheStateofNewMexicoandauthorizedbyDemingPublicSchools(the“District”).TheCharterisacomponentunitoftheDistrict.Theaccompanying financialstatementsdonotpurport to,anddonot,represent the financialposition and changes in financial position of the reporting entity of the District, in accordance withaccountingprinciplesgenerallyacceptedintheUnitedStatesofAmerica(GAAP).TheCharteroperatesunderaGoverningCouncil.TheGoverningCouncilisauthorizedtoestablishpoliciesandregulationsforitsowngovernmentconsistentwiththelawsofthestateofNewMexicoandtheregulationsoftheStateBoardofEducationandtheLegislativeFinancialCommittee.TheGoverningCounciliscomprisedoffivemembers.The Charter provides public education opportunities for children from first through twelfth grade,including but not limited to classroom and vocational studies; as well as school oriented social andathleticactivities.The financial statements of theCharter havebeenprepared in conformitywith accountingprinciplesgenerally accepted in the United States of America (GAAP) as applied to governmental units. TheGovernmentalAccountingStandardBoard(GASB)istheacceptedstandard‐settingbodyforestablishinggovernmental accounting and financial reporting principles. The GASB periodically updates itscodification of the existingGovernmentalAccounting andFinancialReporting Standardswhich, alongwith subsequent GASB pronouncements (Statements and Interpretations), constitutes GAAP forgovernmentalunits.ThemoresignificantoftheCharter’saccountingpoliciesaredescribedbelow.The GASB issued GASB Statement No. 68, Accounting and Financial Reporting for Pensions – anamendment of GASB StatementNo. 27 (GASB No. 68), which is effective for financial statements forperiods beginning after June 15, 2014. GASB No. 68 replaces the requirements of Statement No. 27,Accounting for Pensions by State and Local Governmental Employers, as well as the requirements ofStatement No. 50, PensionDisclosures, as they relate to pensions that are provided through pensionplans administered as trusts or equivalent arrangements (hereafter jointly referred to as trusts) thatmeetcertaincriteria.TherequirementsofStatements27and50remainapplicableforpensionsthatarenot covered by the scope of GASB No. 68. It establishes standards for measuring and recognizingliabilities,deferredoutflowsofresources,deferredinflowsofresources,andexpense/expenditures.Fordefinedbenefitpensions,GASBNo.68 identifies themethodsandassumptionsthatshouldbeusedtoproject benefit payments, discount projected benefit payments to their actuarial present value, andattributethatpresentvaluetoperiodsofemployeeservice.Notedisclosureandrequiredsupplementaryinformation requirements about pensions also are addressed. The impact of this statement to theCharter is the requirement of net pension liability associatedwith the defined benefit pension to bereflectedinitsStatementsofNetPosition.

A. Reportingentity

GASB Statement No. 61 an amendment of GASB Statement No. 14, established criteria fordetermining the government reporting entity and component unit that should be includedwithin the reporting entity. Based on the criterion in GASB No. 61, the Charter has nocomponentunits.

20

CESARCHAVEZHIGHSCHOOLCHARTERSCHOOL(COMPONENTUNITOFDEMINGPUBLICSCHOOLS)NOTESTOTHEFINANCIALSTATEMENTSNote1–SummaryofSignificantAccountingPolicies(continued)

B. Government‐widefinancialstatements

Thegovernment‐widefinancialstatements(i.e.,thestatementofnetpositionandthestatementofactivitiesandchangesinnetposition)reportinformationonallofthenon‐fiduciaryactivitiesoftheprimarygovernment.Forthemostpart,theeffectofinterfundactivityhasbeenremovedfromthesestatements.GASBNo.63,FinancialReportingofDeferredOutflowsofResources,DeferredInflowsofResources,andNet Position, andGASBNo. 65, ItemsPreviouslyReported asAssets and Liabilities, amendGASBNo.34,BasicFinancialStatements–andManagement’sDiscussionandAnalysis forStateandLocalGovernments, to incorporatedeferredoutflowsof resourcesanddeferred inflowsofresourcesinthefinancialreportingmodel.Deferred outflows of resources – a consumption of net position by the government that isapplicabletoafuturereportingperiod.Ithasapositiveeffectonnetposition,similartoassets.Deferred inflows of resources – an acquisition of net position by the government that isapplicable to a future reporting period. It has a negative effect on net position, similar toliabilities.Netposition–theresidualoftheneteffectsofassets,deferredoutflowsofresources,liabilities,anddeferredinflowsofresources.The statement of activities demonstrates the degree to which the direct expenses of a givenfunctionorsegmentareoffsetbyprogramrevenues.Directexpensesarethosethatareclearlyidentifiable with a specific function or segment. Program revenues include 1) charges tocustomers or applicants who purchase, use, or directly benefit from goods, services, orprivileges provided by a given function or segment and 2) grants and contributions that arerestricted to meeting the operational or capital requirements of a particular function orsegment.Taxesandotheritemsnotproperlyincludedamongprogramrevenuesarereportedinsteadasgeneralrevenues.Separate financial statements are provided for governmental funds and fiduciary funds, eventhoughthelatterareexcludedfromthegovernment‐widefinancialstatements.

C. Measurementfocus,basisofaccounting,andfinancialstatementpresentation

The government‐wide financial statements are reported using the economic resourcesmeasurement focus and the accrual basis of accounting, as is the fiduciary fund financialstatement.Revenuesarerecordedwhenearnedandexpensesarerecordedwhena liability isincurred,regardlessofthetimingofrelatedcashflows.Grantsandsimilaritemsarerecognizedasrevenueassoonasalleligibilityrequirementsimposedbytheproviderhavebeenmet.

21

CESARCHAVEZHIGHSCHOOLCHARTERSCHOOL(COMPONENTUNITOFDEMINGPUBLICSCHOOLS)NOTESTOTHEFINANCIALSTATEMENTSNote1–SummaryofSignificantAccountingPolicies(continued)

C. Measurementfocus,basisofaccounting,andfinancialstatementpresentation(continued)Governmental fund financial statements are reported using the current financial resourcesmeasurement focusand themodifiedaccrualbasisof accounting.Revenuesare recognizedassoonastheyarebothmeasurableandavailable.Revenuesareconsideredtobeavailablewhentheyarecollectiblewithinthecurrentperiodorsoonenoughthereaftertopayliabilitiesofthecurrentperiod.Forthispurpose,thegovernmentconsidersrevenuestobeavailableiftheyarecollected within 60 days of the end of the current fiscal period. Expenditures generally arerecorded when a liability is incurred, as under accrual accounting. However, debt serviceexpenditures, as well as expenditures related to compensated absences and claims andjudgments,arerecordedonlywhenpaymentisdue.Grants and similar items are recognized as revenue as soon as all eligibility requirementsimposedbytheproviderhavebeenmet.Onlytheportionofspecialassessmentsreceivableduewithin the current fiscal period is considered to be susceptible to accrual as revenue of thecurrent period. All other revenue items are considered to be measurable and available onlywhencashisreceivedbythegovernment.Governmental funds are used to account for the Charter’s general government activities,includingthecollectionanddisbursementofspecificorlegallyrestrictedmonies,theacquisitionor construction of capital assets, and the servicing of long‐term debt. Governmental fundsinclude:TheGeneral Fund is theprimary operating fundof theCharter, and accounts for all financialresources,exceptthoserequiredtobeaccountedforinotherfunds.

TheSpecialRevenueFundsaccountfortheproceedsofspecificrevenuesourcesthatarelegallyrestrictedtoexpendituresforspecifiedpurposes.TheCapitalProjectsFundsaccount for theacquisitionof fixedassetsorconstructionofmajorcapitalprojectsnotbeingfinancedbyproprietaryornonexpendabletrustfunds.

Under the requirements of GASB No. 34, the Charter is required to present certain of itsgovernmental fundsasmajor fundsbaseduponcertaincriteria.Themajor fundspresented inthe fund financial statements include the following (in addition to the General fund), whichinclude funds thatwere not required to be presented asmajor butwere at the discretion ofmanagement.

InstructionalMaterialsFund(14000)– isusedtoaccountforthemoniesreceivedfromtheNew Mexico Public Education Department (NMPED) for the purposes of purchasinginstructionalmaterials(books,manuals,periodicals,etc.)usedintheeducationofstudents.

22

CESARCHAVEZHIGHSCHOOLCHARTERSCHOOL(COMPONENTUNITOFDEMINGPUBLICSCHOOLS)NOTESTOTHEFINANCIALSTATEMENTSNote1–SummaryofSignificantAccountingPolicies(continued)

C. Measurementfocus,basisofaccounting,andfinancialstatementpresentation(continued)TitleI‐IASA(24101)–fundusedtoaccountforfederalresourcesadministeredbytheNMPEDto provide assistance to educationally deprived students in low‐income areas of the Charter.RequiredbytheNMPEDManualofProcedurestobeaccountedforasaseparatefundwithintheSpecialRevenueFunds(P.L.103‐382).

TANF/GRADS(25162)–accountsforprovidinggrantstoStatesorTerritoriestoassistneedyfamilies with children so that children can be cared for in their own homes; to reducedependencybypromoting jobpreparation,work,andmarriage; toreduceandpreventout‐of‐wedlockpregnancies;andtoencouragetheformationandmaintenanceoftwoparentfamilies.SocialSecurityAct,TitleIV,PartA,asamended;PersonalResponsibilityandWorkOpportunityReconciliationActof1996,PublicLaw104‐193.Thefundwascreatedbystategrantprovision.

Public School Capital Outlay (31200) – to account for the state resources to providereimbursementforrentoffacilities..AGENCYFUNDS

Theagencyfundsarecustodialinnature(assetsequalliabilities)anddonotpresentresultsofoperationsorhaveameasurementfocus.Agencyfundsareaccountedforusingtheaccrualbasisofaccounting.ThesefundsareusedtoaccountforassetsthattheCharterholdsforothersinanagencycapacity.

Agency Fund (23000) – to account for monies held in custodial account (assets equalliabilities)forthebenefitofothers.Individualaccountsareidentifiedbynameinthesupportingschedulesectionofthisreport.Asageneralrule,theeffectofinterfundactivityhasbeeneliminatedfromthegovernment‐widefinancialstatements.Programrevenuesarecategorizedas(a)chargesforservices,whichincluderevenuescollectedforlabfeesandlostbooks,etc.,(b)program‐specificoperatinggrants,whichincludesrevenuesreceivedfromstateandfederalsourcessuchasTitleIIASA,IDEA‐BEntitlement,andotherStateand Federal funding to be used as specified within each program grant agreement, and (c)program‐specific capital grants and contributions,which include revenues from state sourcessuchasspecialcapitaloutlayfundingtobeusedforcapitalprojects.

Internally dedicated resources are reported as general revenues rather than as programrevenues.

23

CESARCHAVEZHIGHSCHOOLCHARTERSCHOOL(COMPONENTUNITOFDEMINGPUBLICSCHOOLS)NOTESTOTHEFINANCIALSTATEMENTSNote1–SummaryofSignificantAccountingPolicies(continued)

C. Measurementfocus,basisofaccounting,andfinancialstatementpresentation(continued)When both restricted and unrestricted resources are available for use, it is the government’spolicytouserestrictedresourcesfirst,thenunrestrictedresourcesastheyareneeded.The Charter reports all direct expenses by function in the statement of activities. Directexpensesarethosethatareclearlyidentifiablewithafunction.TheCharterdoesnotcurrentlyemploy indirect cost allocation systems. Depreciation expense is specifically identified byfunctionandisincludedinthedirectexpenseofeachfunction.

D. Assets,LiabilitiesandNetPositionorEquity

Cash:Cashconsistsofmoniesheldinacheckingaccountwithafinancialinstitution.

Capital Assets: Property and equipment of the primary government is depreciated using thestraightlinemethodoverthefollowingestimatedusefullives:

Buildingimprovements 7‐30yearsEquipment 5‐20yearsFurniture&fixtures 20years

UnspentGrantFunds:TheCharter recognizesgrant revenueat the timetherelatedexpense ismade if the expenditure of funds is the prime factor for determining eligibility forreimbursement; therefore, amounts received andnot expended in the SpecialRevenueFundsareshownasunspentgrantfunds.

Pensions:Forthepurposeofmeasuringthenetpensionliability,deferredoutflowsofresourcesanddeferredinflowsofresourcesrelatedtopensions,andpensionexpense,informationaboutthefiduciarynetpositionoftheNewMexicoEducationalRetirementBoard(ERB)andadditionsto/deductions from ERB’s fiduciary net position have been determined on the same basis astheyarereportedbytheERB,ontheeconomicresourcesmeasurementfocusandaccrualbasisofaccounting.Forthispurpose,benefitpayments(includingrefundsofemployeecontributions)are recognizedwhen due and payable in accordancewith the benefit terms. Investments arereportedatfairvalue.Net Position: In the government‐wide financial statements, fund equity is classified as netpositionandisdisplayedinthreecomponents:

24

CESARCHAVEZHIGHSCHOOLCHARTERSCHOOL(COMPONENTUNITOFDEMINGPUBLICSCHOOLS)NOTESTOTHEFINANCIALSTATEMENTSNote1–SummaryofSignificantAccountingPolicies(continued)

D. Assets,LiabilitiesandNetPositionorEquity(continued)Netinvestmentincapitalassets:Consistsofcapitalassetsincludingrestrictedcapitalassets,netofaccumulateddepreciationandreducedbytheoutstandingbalancesofanybonds,mortgages,notes, or other borrowings that are attributable to the acquisition, construction, orimprovementofthoseassets.

RestrictedNetPosition:Consistsofnetpositionwithconstraintsplacedontheuseeitherby(1)external groups such as creditors, grantors, contributors, or laws or regulation of othergovernments;or(2)lawthroughconstitutionalprovisionsorenablinglegislation.Descriptionsfortherelatedrestrictionsfornetpositionarerestrictedfor“debtserviceorcapitalprojects.”

UnrestrictedNetPosition:Allothernetpositionthatdonotmeetthedefinitionof“restricted”or“investedincapitalassets,netofrelateddebt.”

TheGovernment‐wideStatementofNetPositionreportsadeficit$(4,585)netpositionofwhich$24,253isrestrictedbyenablinglegislation.

Fund Balance: In the governmental financial statements, fund balance is classified and isdisplayedintwocomponents:

Restricted – Consists of amounts that are restricted to specific purposes as a result of a)externally imposed by creditors (such as through debt covenants), grantors, contributors, orlaws or regulations of other governments; or b) imposed by law through constitutionalprovisionsorenablinglegislation.

Unassigned–Representsfundbalancethathasnotbeenassignedtootherfundsandthathasnotbeenrestricted,committed,orassignedtospecificpurposeswithinthegeneralfund.InterfundTransactions:Quasi‐externaltransactionsareaccountedforasrevenues,expendituresor expenses. Transactions that constitute reimbursements to a fund fromexpenditures/expenses initiallymadefromit thatareproperlyapplicabletoanotherfund,arerecorded as expenditures/expenses in the reimbursing fund and as reductions ofexpenditures/expensesinthefundthatisreimbursed.

All other interfund transactions, except quasi‐external transactions and reimbursements arereportedastransfers.Nonrecurringornon‐routinepermanenttransfersofequityarereportedasresidualequitytransfers.Allotherinterfundtransfersarereportedasoperatingtransfers.

Estimates: The preparation of financial statements in conformity with accounting principlesgenerallyacceptedintheUnitedStatesofAmericarequiresmanagementtomakeestimatesandassumptions that affect certain reported amounts and disclosures. Accordingly, actual resultscould differ from those estimates. Significant estimates affecting the Charter’s financialstatementsincludemanagement’sestimateoftheusefullivesofcapitalassets.

25

CESARCHAVEZHIGHSCHOOLCHARTERSCHOOL(COMPONENTUNITOFDEMINGPUBLICSCHOOLS)NOTESTOTHEFINANCIALSTATEMENTSNote1–SummaryofSignificantAccountingPolicies(continued)

E. Revenues

StateEqualizationGuarantee:Charters intheStateofNewMexicoreceivea ‘stateequalizationguaranteedistribution’whichisdefinedas“thatamountofmoneydistributedtoeachChartertoinsurethattheCharter’soperatingrevenue,includingitslocalandfederalrevenuesasdefined(in Chapter 22Article 8 Section 22‐8‐25) is at least equal to the charter’s program cost. Thefunding formula related to the state equalization guarantee determines whether any fundswouldrevertbacktothestate.FederalGrants: TheCharter receives revenues fromvariousFederaldepartments (bothdirectandindirect),whicharelegallyrestrictedtoexpendituresforspecificpurposes.TheseprogramsarereportedasSpecialRevenueFunds.Eachprogramoperatedunderitsownbudget,whichhasbeenapprovedbytheFederalDepartmentortheflowthroughagency(usuallytheNMPED).ThevariousbudgetsareapprovedbytheLocalSchoolBoardandtheNMPED.

F. PensionsForpurposesofmeasuringthenetpensionliability,deferredoutflowsofresourcesanddeferredinflowsofresourcesrelatedtopensions,andpensionexpense,informationaboutthefiduciarynetpositionoftheEducationalRetirementBoard(ERB)andadditionsto/deductionsfromERB’sfiduciarynetpositionhavebeendeterminedonthesamebasisastheyarereportedbyERB,ontheeconomicresourcesmeasurement focusandaccrualbasisofaccounting.For thispurpose,benefitpayments(includingrefundsofemployeecontributions)arerecognizedwhendueandpayableinaccordancewiththebenefitterms.Investmentsarereportedatfairvalue.

G. Deferredoutflows/inflowsofresources

Inadditiontoassets,thestatementofnetpositionwillsometimesreportseparatesectionsfordeferredoutflows/inflowsofresources.Theseseparate financialstatementelements,deferredoutflows/inflowsofresources,representsadecrease/increaseofnetpositionthatappliestoafuture period(s) and so will not be recognized as an outflow/inflow of resources(expense/expenditure or revenue/income) until then. In the government‐wide financialstatements, long‐term debt and other long‐term obligations are reported as liabilities in thestatementofnetposition.

26

CESARCHAVEZHIGHSCHOOLCHARTERSCHOOL(COMPONENTUNITOFDEMINGPUBLICSCHOOLS)NOTESTOTHEFINANCIALSTATEMENTS

Note2–Stewardship,ComplianceandAccountability

A. BudgetaryInformationBudgets for the General, Special Revenue, and Capital Projects Funds are prepared bymanagementandareapprovedby theGoverningCouncilandtheSchoolBudgetandPlanningUnitoftheNMPED.Auxiliarystudentactivityaccounts(agencyfunds)arenotbudgeted.These budgets are prepared on the cash basis, excluding encumbrances, and secureappropriationoffundsforonlyoneyearandreconciledtothemodifiedaccrualGAAPfinancialstatements. Carryover funds must be re‐appropriated in the budget of the subsequent fiscalyear.

Actual expenditures may not exceed the budget on a line item basis, i.e., each budgetedexpenditure must be within budgeted amounts. Budgets may be amended in two ways. If abudgettransferisnecessarywithinamajorcategorycalleda‘series,’thismaybeaccomplishedwithonlylocalBoardofEducationapproval.Ifatransferbetween‘series’orabudgetincreaseisrequired,approvalmustalsobeobtainedfromNMPED.The budgetary information presented in these financial statements has been amended inaccordancewiththeaboveprocedures.The Charter follows these procedures in establishing the budgetary data reflected in thefinancialstatements:

1. In April or May, the governing council submits to the School Budget Planning Unit(SBPU) of the NMPED a proposed operating budget for the ensuing fiscal yearcommencing July 1. The operating budget includes proposed expenditures and themeans of financing them. All budgets submitted to the NMPED by the Charter shallcontain headings and details as described by law and have been approved by theNMPED.

2. In May or June of each year, the proposed “operating” budget will be reviewed and

approved by the SBPU and certified and approved by governing council at a publichearing ofwhich notice has been published by the governing councilwhich fixes theestimatedbudgetfortheCharterfortheensuingfiscalyear.

3. Thegoverningcouncilmeeting,whilenotintendedforthegeneralpublic,isopenforthe

generalpublicunlessaclosedmeetinghasbeencalled.

27

CESARCHAVEZHIGHSCHOOLCHARTERSCHOOL(COMPONENTUNITOFDEMINGPUBLICSCHOOLS)NOTESTOTHEFINANCIALSTATEMENTSNote2–Stewardship,ComplianceandAccountability(continued)

A. BudgetaryInformation(continued)

4. The“operating”budgetwillbeusedbytheCharteruntiltheyhavebeennotifiedthatthebudgethasbeenapprovedbytheSBPUandthegoverningcouncil.Thebudgetshallbeintegrated formally into the accounting system. Encumbrances shall be used as anelement of control and shall be integrated into the budget system. The Charter shallmakecorrections,revisionsandamendmentstotheestimatedbudgetsfixedbythelocalschool board to recognize actual cash balances and carryover funds, if any. TheseadjustmentsshallbereviewedandapprovedbytheSBPU.

5. Thesuperintendent isauthorized to transferbudgetedamountsbetweendepartments

within any fund; however, any revisions that alter the total expenditures of any fundmustbeapprovedbythegoverningcouncilandtheNMPED.

6. Budget change requests are processed in accordance with Supplement 1 (Budget

Preparation andMaintenance) of theManual of Procedures Public School AccountingandBudgeting.SuchchangesareinitiatedbytheCharterandapprovedbytheSBPU.

7. Legalbudgetcontrolforexpendituresisbyfunction.8. Appropriations lapse at fiscal year end. Funds unused during the fiscal year may be

carriedoverintothenextfiscalyearbybudgetingthoseinthesubsequentfiscalyear’sbudget.Thebudgetof theCharterhasbeenamendedduring thecurrent fiscalyear inaccordancewiththeseprocedures.Thebudgetschedulesincludedintheaccompanyingfinancialstatementsreflecttheapprovedbudgetandamendmentsthereto.

9. Formalbudgetary integration isemployedasamanagementcontroldeviceduringthe

yearfortheGeneralFund,SpecialRevenueFunds,andCapitalProjectsFunds.10. BudgetsfortheGeneral,SpecialRevenueandCapitalProjectsareadoptedonabasisnot

consistent with generally accepted accounting principles (GAAP). Encumbrances aretreatedthesamewayforGAAPpurposesandforbudgetpurposes.

The governing council may approve amendments to the appropriated budget, which arerequiredwhenachangeismadeaffectingbudgetedendingfundbalance.NewMexicostatelawprohibitsaGovernmentalAgencyfromexceedinganindividuallineitem.The accompanying Statements of Revenues, Expenditures and Changes in Fund Balance –BudgetandActualcomparisonsof the legallyadoptedbudgetwithactualdataonabudgetarybasis.

28

CESARCHAVEZHIGHSCHOOLCHARTERSCHOOL(COMPONENTUNITOFDEMINGPUBLICSCHOOLS)NOTESTOTHEFINANCIALSTATEMENTSNote3‐Cash

Depositsoffundsmaybemadeininterestornon‐interestbearingcheckingaccountsinoneormorebanksorsavingsandloanassociationswithinthegeographicalboundariesoftheCharter.DepositsmaybemadetotheextentthattheyareinsuredbyanagencyoftheUnitedStatesorbycollateraldepositedassecurityorbybondgivenbythefinancialinstitution.Therateofinterestinnon‐demandinterest‐bearingaccountsshallbesetbytheStateBoardofFinance,butinnocaseshalltherateofinterestbelessthanonehundredpercentoftheaskedpriceonUnitedStatestreasurybillsofthesamematurityonthedayofdeposit.ThecollateralpledgedislistedonScheduleIofthisreport.Thetypesofcollateralallowedarelimited to direct obligations of the United States Government and all bonds issued by anyagency,CharterorpoliticalsubdivisionoftheStateofNewMexico.AccordingtotheFederalDepositInsuranceCorporation,publicunitdepositsarefundsownedbythepublicunit.Timedeposits,savingsdepositsandinterestbearingaccountsofapublicunitin an institution in the same state will be insured up to the standard maximum depositinsuranceamountof$250,000 foralldepositaccountsoutof stateandup to$250,000 foralltimeandsavingaccountsplusupto$250,000foralldemanddepositaccountsheldatasingleinstitutioninstate.Deposits: New Mexico State Statutes require collateral pledged for deposits in excess of thefederaldepositinsurancetobedelivered,orajointsafekeepingreceiptbeissued,totheSchoolsforaleastonehalfoftheamountondepositwiththeinstitution.TheschedulelistedbelowwillmeettheStateofNewMexicorequirementsinreportingtheinsuredportionofthedeposits.

1stNewMexico Bank Totalamountsofdeposits $ 862,179 FDICcoverage (250,000) Totaluninsuredpublicfunds 612,179 Pledgedcollateralheldbypledgingbank trustdepartmentoragentbutnot inCharter’sname ‐ Uninsuredanduncollateralized 612,179 Collateralrequirement(50%ofuninsuredpublicfunds) 306,090 Pledgedsecurity (745,540) Totalunder(over)collateralized $ (413,910)

29

CESARCHAVEZHIGHSCHOOLCHARTERSCHOOL(COMPONENTUNITOFDEMINGPUBLICSCHOOLS)NOTESTOTHEFINANCIALSTATEMENTSNote3–Cash(continued)

CustodialCreditRisk–Deposits:Custodialcreditriskistheriskthatintheeventofabankfailure,thegovernment’sdepositsmaynotbereturnedtoit.Thegovernmentdoesnothaveadepositpolicy for custodial credit risk, other than following state statutes as put forth in the PublicMoney Act (Section 6‐10‐1 to 6‐10‐63, NMSA 1978). At June 30, 2016, the Charter was notexposedtocustodialcreditrisk.

Note4–AccountsReceivableAccountsReceivablesasofJune30,2016areasfollows: TitleI Other Operational IASA PSCOC Nonmajorfunds TotalDistrictreceivable $ 83,962 ‐ ‐ ‐ 83,962Stategrants ‐ ‐ 93,291 ‐ 93,291Federalgrants ‐ 65,228 ‐ 28,321 93,549 Total $ 83,962 65,228 93,291 28,321 270,802

Theabovereceivablesaredeemed100%collectible.Note5–InterfundReceivablesandPayables“Interfund balances” have primarily been recordedwhen funds overdraw their share of pooled cashwhen the Charter is waiting for grant reimbursements. The composition of interfund balances as ofJune30,2016isasfollows: Interfund Interfund Receivables Payables MajorFunds: GeneralFund $ 181,569 ‐ CapitalOutlayFunds ‐ 93,291 TitleIIASAFunds ‐ 59,957 NonMajorFunds: IDEA‐BEntitlementFunds ‐ 14,661 TitleISchoolImprovementFunds ‐ 13,660 Total $ 181,569 181,569

30

CESARCHAVEZHIGHSCHOOLCHARTERSCHOOL(COMPONENTUNITOFDEMINGPUBLICSCHOOLS)NOTESTOTHEFINANCIALSTATEMENTSNote6–CapitalAssetsAsummaryofcapitalassetsandchangesoccurringduringtheyearendedJune30,2016,includingthosechangespursuanttotheimplementationofGASBStatementNo.34. Balance Balance June30,2015 Additions Deletions June30,2016 CapitalAssetsusedin GovernmentalActivities Leaseholdimprovements $ 303,725 206,789 ‐ 510,514 Furniturefixturesand equipment 155,435 ‐ ‐ 155,435 TotalCapitalAssets beingdepreciated 459,160 206,789 ‐ 665,949 LessAccumulatedDepreciation Leaseholdimprovements 32,010 8,419 ‐ 40,429 Furniturefixturesand equipment 80,845 22,314 ‐ 103,159 Totalaccumulated depreciation 112,855 30,733 ‐ 143,588 Governmentalactivities capitalassets,net $ 346,305 176,056 ‐ 522,361Depreciation expense for the year ended June 30, 2016 was charged to governmental activities asfollows: SchoolAdministration $ 1,349 Operation&Maintenance 29,384 $ 30,733Note7–OperatingLeasesOperatingLeases–TheCharterleasesthebuildingsundershort‐termcancelableoperatinglease.RentalcostfortheyearendedJune30,2016was$93,291,withafutureobligationof$80,988foryearendingJune30,2017.

31

CESARCHAVEZHIGHSCHOOLCHARTERSCHOOL(COMPONENTUNITOFDEMINGPUBLICSCHOOLS)NOTESTOTHEFINANCIALSTATEMENTSNote8–RiskManagementThe Charter is a member of the New Mexico Public Schools Insurance Authority (NMPSIA). TheAuthoritywas created to provide comprehensive core insurance programs by expanding the pool ofsubscriberstomaximizecostcontainmentopportunities forrequiredinsurancecoverage.TheCharterpaysanannualpremiumtotheNMPSIAbasedonclaimexperienceandthestatusofthepool.TheRiskManagementProgram includesWorkersCompensation,GeneralandAutomobileLiability,AutomobilePhysicalDamage,andPropertyandCrimecoverage.AlsoincludedundertheriskmanagementprogramareBoiler,MachineryandStudentAccidentInsurance.The New Mexico Public Schools Insurance Authority is self‐insured for property and liability lossesbelow $250,000 and purchased excess insurance above the self‐insured retention. The self‐insuredretention aggregate for property is set at $2,000,000 with a $1,000,000 stop loss. The self‐insuredretentionaggregateforliabilityis$3,000,000witha$1,000,000stoploss.Incase theNMPSIA’sassetsarenotsufficient tomeet its liabilityclaims, theagreementprovides thatsubscribers,includingtheCharter,cannotbeassessedadditionalpremiumstocovertheshortfall.AsofJune30,2016,therehavebeennoclaimsthathaveexceededinsurancecoverage.Note9–OtherRequiredIndividualFundDisclosuresGenerally accepted accounting principles require disclosures as part of the Combined Statements ofcertaininformationconcerningindividualfundsincluding:

A. Deficit fundbalanceof individualfunds.ThefollowingfundsreportedadeficitfundbalanceatJune30,2016:

None

B. Excessofexpendituresoverappropriations.ThefollowingfundsexceededapprovedbudgetaryauthorityfortheyearendedJune30,2016:

MajorFunds:TitleI‐instructional $ 3,854

NonmajorFunds:TitleISchoolImprovement‐instructional $ 13,660

32

CESARCHAVEZHIGHSCHOOLCHARTERSCHOOL(COMPONENTUNITOFDEMINGPUBLICSCHOOLS)NOTESTOTHEFINANCIALSTATEMENTSNote10–PensionPlanEducationalRetirementBoardPlan description. The Educational Retirement Board (ERB) was created by the state’s EducationalRetirement Act, Section 22‐11‐1 through 22‐11‐52, NMSA 1978, as amended, to administer the NewMexico Educational Employees’ RetirementPlan (Plan). ThePlan is a cost‐sharing,multiple employerpensionplanestablished toprovide retirementanddisabilitybenefits for certified teachersandotheremployees of the state’s public schools, institutions of higher learning, and state agencies providingeducational programs. The Educational Retirement Act assigns the authority to establish and amendbenefit provisions to the Board of Trustees; the state legislature has the authority to set or amendcontribution rates and other terms of the Plan. The Plan is a pension trust fund of the State of NewMexico.ERBissuesapubliclyavailablefinancialreportandacomprehensiveannualfinancialreportthatcanbeobtainedatwww.nmerb.org.Benefits provided. A member’s retirement benefit is determined by a formula which includes threecomponentparts:themember’sfinalaveragesalary(FAS),thenumberofyearsofservicecredit,anda0.0235multiplier.TheFASistheaverageofthemember’ssalariesforthelastfiveyearsofserviceoranyotherconsecutive five‐yearperiod,whichever isgreater.Abrief summaryofPlancoverageprovisionsfollows:Formembers employed before July 1, 2010, amember is eligible to retirewhenone of the followingeventsoccurs:themember’sageandearnedservicecreditadduptothesumor75ormore;thememberisatleastsixty‐fiveyearsofageandhasfiveormoreyearsofearnedservicecredit;orthememberhasservicecredittotaling25yearsormore.

Chapter288,Lawsof2009changedtheeligibilityrequirementsfornewmembersfirstemployedonorafter July1,2010.Theeligibility foramemberwhoeitherbecomesanewmemberonorafter July1,2010,oratanytimepriortothatdaterefundedallmembercontributionsandthenbecame,orbecomes,reemployedafterthatdateisasfollows:themember’sageandearnedservicecreditadduptothesumof 80 ormore; themember is at least sixty‐seven years of age and has five ormore years of earnedservicecredit;orthememberhasservicecredittotaling30yearsormore.

Thebenefitispaidasamonthlylifeannuitywithaguaranteethat,ifthepaymentsmadedonotexceedthe member’s accumulated contributions plus accumulated interest, determined as of the date ofretirement, the balancewill be paid in a lump sum to themember’s surviving beneficiary. There arethreebenefitoptionsavailable:singlelifeannuity;singlelifeannuitymonthlybenefitreducedtoprovidefor a 100% survivor’s benefit; or single life annuitymonthlybenefit is reduced toprovide for a50%survivor’sbenefit.

33

CESARCHAVEZHIGHSCHOOLCHARTERSCHOOL(COMPONENTUNITOFDEMINGPUBLICSCHOOLS)NOTESTOTHEFINANCIALSTATEMENTSNote10–PensionPlanEducationalRetirementBoard(continued)Allretiredmembersandbeneficiariesreceivingbenefitsreceiveanautomaticcostoflivingadjustment(COLA) to theirbenefiton July1 following the laterof1) theyearamemberretires,or2) theyearamember reaches age 65 (Tier 1 and Tier 2) or age 67 (Tier 3). Tier 1 membership is comprised ofemployeeswhobecamememberspriortoJuly1,2010.Tier2membershipiscomprisedofemployeeswhobecamemembersafterJuly1,2010,butpriortoJuly1,2013.Tier3membershipiscomprisedofemployeeswho becamemembers on or after July 1, 2013. As of July1, 2013, for current and futureretireestheCOLAisimmediatelyreduceduntilthePlanis100%funded.TheCOLAreductionisbasedonthemedianretirementbenefitofallretireesexcludingdisabilityretirements.Retireeswithbenefitsatorbelowthemedianandwith25ormoreyearsofservicecreditwillhavea10%COLAreduction;their average COLA will be 1.6%. Once the funding is greater than 90%, the COLA reductions willdecrease.Theretireeswithbenefitsatorbelowthemedianandwith25ormoreyearsofservicecreditwillhavea5%COLAreduction;theiraverageCOLAwillbe1.8%.MembersondisabilityretirementareentitledtoaCOLAcommencingonJuly1ofthethirdfullyearfollowingdisabilityretirement.Amemberon regular retirement who can prove retirement because of a disability may qualify for a COLAbeginningJuly1inthethirdfullyearofretirement.Amember is eligible for adisabilitybenefit provided (a)heor shehas credit for at least10yearsofservice,and(b)thedisabilityisapprovedbyERB.Themonthlybenefitisequalto2%ofFAStimesyearsofservice,butnot lessthanthesmallerof(a)one‐thirdofFASor(b)2%ofFAStimesyearofserviceprojected to age 60. The disability benefit commences immediately upon the member’s retirement.Disabilitybenefitsarepayableasamonthlylifeannuity,withaguaranteethat,ifthepaymentsmadedonot exceed the member’s accumulated contributions, determined as of the date of retirement, thebalance will be paid in a lump sum to the member’s surviving beneficiary. If the disabled membersurvivestoage60,theregularoptionalformsofpaymentarethenapplied.AmemberwithfiveormoreyearsofearnedservicecreditondeferredstatusmayretireondisabilityretirementwheneligibleundertheRuleof75orwhenthememberattainsage65.Contributions. The contribution requirements of defined benefit plan members and the Charters areestablished in state statute under 22‐11‐21 NMSA 1978. For the fiscal year ended June 30, 2016employers contributed 13.90% of employees’ gross annual salary to the Plan. Employees earning$20,000or less contributed7.90%andemployeesearningmore than$20,000contributed10.70%oftheir gross annual salary. For fiscal year ended June 30, 2015 employers contributed 13.90%, andemployees earning $20,000or less continued to contribute 7.90%and employees earningmore than$20,000contributedanincreasedamountof10.70%oftheirgrossannualsalary.ContributionstothepensionplanfromtheCharterwere$163,184,fortheyearendedJune30,2016.

34

CESARCHAVEZHIGHSCHOOLCHARTERSCHOOL(COMPONENTUNITOFDEMINGPUBLICSCHOOLS)NOTESTOTHEFINANCIALSTATEMENTSNote10–PensionPlanEducationalRetirementBoard(continued)PensionLiabilities,PensionExpense,andDeferredOutflowsofResourcesandDeferredInflowsofResourcesRelated to Pensions: The total ERB pension liability, net pension liability, and certain sensitivityinformation were based on an actuarial valuation performed as of June 30, 2015. The employer’sproportionate share of these amounts, reported as of June 30, 2016, was established as of themeasurementdateJune30,2015.AtJune30,2016,theCharterreportedaliabilityof$1,480,695foritsproportionateshareofthenetpensionliability.TheCharter’sproportionofthenetpensionliabilityisbased on the employer contributing entity’s percentage of total employer contributions for the fiscalyearendedJune30,2015.AtJune30,2015,theCharter’sproportionwas.02286%percent,whichwasandecreaseof.00653%percentfromitsproportionmeasuredasofJune30,2014.FortheyearendedJune30,2016,theCharterrecognizedpensionexpenseof$54,371.AtJune30,2016,theCharterreporteddeferredoutflowsofresourcesanddeferredinflowsorresourcesrelatedtopensionsfromthefollowingsources: Deferred

OutflowsofResources

DeferredInflowsofResources

Differencesbetweenexpectedandactualexperience $‐ $27,450Changesofassumptions 50,929 ‐Netdifferencebetweenprojectedandactualearningsonpensionplaninvestments

‐

6,665

Changes in proportion and differences between theCharter contributions and proportionate share ofcontributions

88,498

307,430

The Charter’s contributions subsequent to themeasurementdate

163,184

‐

Total $302,611 $341,547

$163,184 reported as deferred outflows of resources related to pensions resulting from the ChartercontributionssubsequenttothemeasurementdateJune30,2015willberecognizedasareductionofthenetpensionliabilityintheyearendedJune30,2017.Otheramountsreportedasdeferredoutflowsof resources and deferred inflows of resources related to pensions will be recognized in pensionexpenseasfollows:

YearendedJune30: 2017 $ (61,641) 2018 (66,481) 2019 (94,537) 2020 20,566

35

CESARCHAVEZHIGHSCHOOLCHARTERSCHOOL(COMPONENTUNITOFDEMINGPUBLICSCHOOLS)NOTESTOTHEFINANCIALSTATEMENTSNote10–PensionPlanEducationalRetirementBoard(continued)Actuarial assumptions. As described above, the total ERB pension liability, net pension liability, andcertainsensitivity informationarebasedonanactuarialvaluationperformedasofJune30,2015.TheliabilitiesreflecttheimpactofSenateBill115,signedintolawonMarch29,2013,andnewassumptionsadopted by the ERB Board of Trustees on June 12, 2015. Specifically, the liabilities measured as ofJune30,2015,incorporatethefollowingassumptions:

1. Allmemberswith an annual salary ofmore than $20,000will contribute 10.70% during thefiscalyearendingJune30,2015thereafter.

2. Membershiredafter June30,2013willhaveanactuariallyreducedretirementbenefit if theyretirebeforeage55andtheirCOLAwillbedeferreduntilage67.

3. COLAsformostretireesarereduceduntilERBattainsa100%fundedstatus.4. TheseassumptionswereadoptedbytheERBBoardonJune12,2015, inconjunctionwiththe

six‐yearexperiencestudyperiodendingJune30,2014,and5. Forpurposesofprojectingfuturebenefits, it isassumedthatthefullCOLAispaidinallfuture

years.On June 12, 2015, the ERB Board of Trustees approves the following changes to economic anddemographicassumptionsusedinthefiscalyear2015actuarialcalculationofthetotalpensionliability:

1. Lowerwageinflationfrom4.25%to3.75%2. Updatethemortalitytablestoincorporategenerationalimprovements3. Updatedemographicassumptionstousecurrentlypublishedtables,whichmayresultinminor

calculationchanges4. Removepopulationgrowthassumptionforprojections5. Lowerpopulationgrowthfrom.50%tozero

The actuarial methods and assumptions used to determine contribution rates included in themeasurementareasfollows: ActuarialCostMethod EntryAgeNormalAmortizationMethod LevelPercentageofPayrollRemainingPeriod Amortized–closed30yearsfromJune30,2012toJune30,2042AssetValuationMethod 5 year smoothed market for funding valuation (fair value for financial

valuation)Inflation 3.00%SalaryIncreases Composition: 3% inflation, plus 1.25% productivity increase rate, plus

stepratepromotional increases formemberswith less than10yearsofservice

InvestmentRateofReturn 7.75%RetirementAge ExperiencebasedtableofageandserviceratesMortality 90%ofRP‐2000CombinedMortalityTablewithWhiteCollarAdjustment

projectedto2014usingScaleAA(oneyearsetbackforfemales)

36

CESARCHAVEZHIGHSCHOOLCHARTERSCHOOL(COMPONENTUNITOFDEMINGPUBLICSCHOOLS)NOTESTOTHEFINANCIALSTATEMENTSNote10–PensionPlanEducationalRetirementBoard(continued)The long‐term expected rate of return on pension plan investments is determined annually using abuilding‐blockapproachthatincludesthefollowing:1)rateofreturnprojectionsarethesumofcurrentyield plus projected changes in price (valuation, defaults, etc.), 2) application of key economicprojections (inflation, real growth, dividends, etc.), and 3) structural themes (supply and demandimbalances, capital flows, etc.). These items are developed for each major asset class. Estimates ofgeometric 30‐year expected rates of return by major asset class for 2015 are summarized in thefollowingtable: Long‐TermExpected

Asset TargetAllocation RealRateofReturn DomesticEquities 20% 7.50‐7.75%InternationalEquities 15% 8.00‐9.25%FixedIncomeSecurities 28% 3.75‐6.75%AlternativeAssets 36% 6.50‐9.50%Cash 1% 3.25%Total 100%

Discountrate:Asinglediscountrateof7.75%wasusedtomeasurethetotalERBpensionliabilityasofJune30,2015and2014.Thisdiscountratewasbasedontheexpectedrateofreturnonpensionplaninvestmentsof7.75%.Basedontheassumptionsdescribedaboveandtheprojectionofcashflows,thePlan’s fiduciary net position and future contributions were projected to be available to finance allprojected future benefit payments of current pension planmembers. The long‐term expected rate ofreturnonPlan investmentswasappliedtoallperiodsofprojectedbenefitpaymentstodeterminethetotalpensionliability.TheprojectionofcashflowsusedtodeterminethissinglediscountrateassumedthatPlancontributionswillbemadeatthecurrentstatutorylevels.Additionally,contributionsreceivedthroughtheAlternativeRetirementPlan (ARP), ERB’s defined contributionplan, are included in theprojection of cash flows.ARPcontributionsareassumedtoremainatalevelpercentageofERBpayroll,wherethepercentageofpayrollisbasedonthemostrecentfiveyearcontributionhistory.

37

CESARCHAVEZHIGHSCHOOLCHARTERSCHOOL(COMPONENTUNITOFDEMINGPUBLICSCHOOLS)NOTESTOTHEFINANCIALSTATEMENTSNote10–PensionPlanEducationalRetirementBoard(continued)SensitivityoftheCharter’sproportionateshareofthenetpensionliabilitytochangesinthediscountrate.Thefollowingtableshowsthesensitivityofthenetpensionliabilitytochangesinthediscountrateasofthe fiscalyearend2015. Inparticular, the tablepresents theCharter’snetpension liabilityunder thecurrentsinglerateassumption,asifitwerecalculatedusingadiscountrateonepercentagepointlower(6.75%)oronepercentagepointhigher(8.75%)thanthesinglediscountrate.

1%Decrease(6.75%)

CurrentDiscountRate(7.75%)

1%Increase(8.75%)

The Charter’s proportionateshareofthenetpensionliability

$ 1,992,385

$ 1,480,695

$1,050,837

Pension plan fiduciary net position. Detailed information about the ERB’s fiduciary net position isavailable in the separately issued audited financial statements as of and for June 30, 2015 and 2014whicharepubliclyavailableatwww.nmerb.org.Payables to the pension plan. The Charter remits the legally required employer and employeecontributionsonamonthlybasis toERB.TheERBrequires that thecontributionsbe remittedby the15thdayofthemonthfollowingthemonthforwhichcontributionsarewithheld.AtJune30,2016theCharterowedtheERB$39,538forthecontributionswithheldinthemonthofJune2016.Note11–RetireeHealthCareContributionsPlanDescription.TheChartercontributes to theNewMexicoRetireeHealthCareFund,acost‐sharingmultiple‐employer defined benefit postemployment healthcare plan administered by theNewMexicoRetireeHealthCareAuthority(RHCA).TheRHCAprovideshealthcareinsuranceandprescriptiondrugbenefits to retired employees of participating New Mexico government agencies, their spouses,dependents, and surviving spouses and dependents. TheRHCABoardwas established by theRetireeHealth Care Act (Chapter 10, Article 7C, NMSA 1978). The Board is responsible for establishing andamendingbenefitprovisionsofthehealthcareplanandisalsoauthorizedtodesignateoptionaland/orvoluntarybenefitslikedental,vision,supplementallifeinsurance,andlong‐termcarepolicies.Eligible retirees are: 1) retirees who make contributions to the fund for at least five years prior toretirementandwhoseeligibleemployerduringthatperiodoftimemadecontributionsasaparticipantintheRHCAplanontheperson’sbehalfunlessthatpersonretiresbeforetheemployer’sRHCAeffectivedate, inwhichevent the timeperiodrequired foremployeeandemployercontributionsshallbecometheperiodoftimebetweentheemployer’seffectivedateandthedateofretirement;2)retireesdefinedbytheActwhoretiredpriortoJuly1,1990;3)Formerlegislatorswhoservedatleasttwoyears;and4)formergoverningauthoritymemberswhoservedatleastfouryears.

38

CESARCHAVEZHIGHSCHOOLCHARTERSCHOOL(COMPONENTUNITOFDEMINGPUBLICSCHOOLS)NOTESTOTHEFINANCIALSTATEMENTSNote11–RetireeHealthCareContributions(continued)TheRHCAissuesapubliclyavailablestand‐alonefinancialreportthatincludesfinancialstatementsandrequiredsupplementary informationforthepostemploymenthealthcareplan.ThatreportandfurtherinformationcanbeobtainedbywritingtotheRetireeHealthCareAuthorityat4308CarlisleNE,Suite104,Albuquerque,NM87107.FundingPolicy–TheRetireeHealthCareAct(Section10‐7C‐13NMSA1978)authorizestheRHCABoardtoestablishthemonthlypremiumcontributionsthatretireesarerequiredtopayforhealthcarebenefits.Eachparticipatingretireepaysamonthlypremiumaccordingtoaservicebasedsubsidyrateschedulefor the medical plus basic life plan plus an additional participation fee of five dollars if the eligibleparticipant retired prior to the employer’s RHCA effective date or is a former legislator or formergoverningauthoritymember.Formerlegislatorsandgoverningauthoritymembersarerequiredtopay100%oftheinsurancepremiumtocovertheirclaimsandtheadministrativeexpensesoftheplan.Themonthly premium rate schedule can be obtained from the RHCA or viewed on their website atwww.nmrhca.state.nm.us.The employer, employee and retiree contributions are required to be remitted to the RHCA on amonthlybasis.Thestatutoryrequirementsfortheemployerandemployeecontributionscanbechangesby the NewMexico State Legislature. Employers that chose to become participating employers afterJanuary1,1998,arerequiredtomakecontributionstotheRHCAfundintheamountdeterminedtobeappropriatebytheboard.TheRetireeHealthCareAct(Section10‐7C‐15NMSA1978) is thestatutoryauthority thatestablishesthe required contributions of participating employers and their employees. For employees thatweremembersofanenhancedretirementplan(statepoliceandadultcorrectionalofficermembercoverageplan1;municipalpolicemembercoverageplans3,4or5;municipalfiremembercoverageplan3,4or5; municipal detention officer member coverage plan 1; and members pursuant to the JudicialRetirement Act) during the fiscal year ended June 30, 2015, the statutes required each participatingemployer to contribute 2.5% of each participating employee’s annual salary; and each participatingemployeewasrequiredtocontribute1.25%oftheirsalary.Foremployeesthatwerenotmembersofanenhanced retirement plan during the fiscal year ended June 30, 2015, the statute required eachparticipating employer to contribute 2.0% of each participating employee’s annual salary; eachparticipatingemployeewasrequiredtocontribute1.0%oftheirsalary.Inaddition,pursuanttoSection10‐7C‐15(G)NMSA1978, at the first session of the Legislature following July 1, 2013, the legislatureshallreviewandadjustthedistributionspursuanttoSection7‐1‐6.1NMSA1978andtheemployerandemployee contributions to the authority in order to ensure the actuarial soundness of the benefitsprovidedundertheRetireeHealthCareAct.The Charter’s contributions to the RHCA for the years ended June 30, 2016, 2015, and 2014 were$17,396,$16,638,and$14,533,respectively,whichequaltherequiredcontributionsforeachyear.

39

CESARCHAVEZHIGHSCHOOLCHARTERSCHOOL(COMPONENTUNITOFDEMINGPUBLICSCHOOLS)NOTESTOTHEFINANCIALSTATEMENTSNote12–ContingentLiabilitiesAmountsreceivedorreceivable fromgrantoragenciesaresubject toauditandadjustmentbygrantoragencies.Anydisallowedclaims, includingamountsalreadycollected,mayconstitutea liabilityof theapplicable funds.Theamount, ifany,ofexpenditureswhichmaybeallowedby thegrantorcannotbedeterminedatthistime,althoughtheCharterexpectssuchamount,ifany,tobeimmaterial.The Charter is sometimes involved in various claims and lawsuits arising in the normal course ofbusiness.Althoughtheoutcomeoftheselawsuitsinnotpresentlydeterminable,itistheopinionoftheCharter’slegalcounselthattheresolutionofthesematterswillnothaveamaterialadverseeffectonthefinancialconditionoftheCharter.Note13–RelatedPartiesTheCharterleasesaschoolbuildingfromtheDistrict.Theleaseisrenegotiatedannually,andcurrentlyrequirespaymentannuallyof$700timestheaverage full‐time‐equivalentenrollmentontheeightiethandonehundredtwentiethdayofthepriorschoolyear.TheCharterpaid$93,291inrenttotheDistrictduringtheyearendedJune30,2016.Note14–MemorandumofUnderstandingandJointPowersAgreementsTransportation–MemorandumofUnderstandingParticipants DemingPublicSchools DemingCesarChavezCharterHighSchoolResponsibleparty DemingPublicSchoolsandDemingCesarChavezCharterHighSchoolDescription Provideto/fromtransportationforalleligiblestudents.Termofagreement OneyearbeginningJuly1,2015AmountofProject NomonetarypaymentfromtheCharterDistrictcontributions BusserviceAuditresponsibility TheDistrict

40

CESARCHAVEZHIGHSCHOOLCHARTERSCHOOL(COMPONENTUNITOFDEMINGPUBLICSCHOOLS)NOTESTOTHEFINANCIALSTATEMENTSNote14–MemorandumofUnderstandingandJointPowersAgreements(continued)

Nutrition–MemorandumofUnderstanding

Participants DemingPublicSchools DemingCesarChavezCharterHighSchoolResponsibleparty DemingPublicSchoolsandDemingCesarChavezCharterHighSchoolDescription Providestudentswithapprovedmealsforbreakfastandlunch.Termofagreement OneyearbeginningJuly1,2015AmountofProject NomonetarypaymentfromtheCharterDistrictcontributions NutritionservicesprovidedbyDPSAuditresponsibility TheDistrictJointPowersAgreementsParticipants CooperativeEducationServices DemingCesarChavezCharterHighSchoolResponsibleparty DemingCesarChavezCharterHighSchoolDescription Procurementservices.Termofagreement OngoingbeginningNovember11,2009(#206)AmountofProject NostatedlimitDistrictcontributions PaymentasquotedandauthorizedAuditresponsibility DemingCesarChavezCharterHighSchoolNote15–EvaluationofSubsequentEventsTheSchoolhasevaluatedsubsequenteventsthroughNovember23,2016,thedatewhichthefinancialstatementswereavailabletobeissued.Note16–SubsequentPronouncementsStatement 77‐ Tax Abatement Disclosures: Financial statement users need information about certainlimitations on a government’s ability to raise resources. This includes limitations on revenue‐raisingcapacityresultingfromgovernmentprogramsthatusetaxabatementstoinducebehaviorbyindividualsandentitiesthatisbeneficialtothegovernmentoritscitizens.Taxabatementsarewidelyusedbystateand local governments, particularly to encourage economic development. For financial reportingpurposes,thisStatementdefinesataxabatementasresultingfromanagreementbetweenagovernmentandanindividualorentityinwhichthegovernmentpromisestoforgotaxrevenuesandtheindividualorentitypromisestosubsequentlytakeaspecificactionthatcontributestoeconomicdevelopmentorotherwisebenefitsthegovernmentoritscitizens.

41

CESARCHAVEZHIGHSCHOOLCHARTERSCHOOL(COMPONENTUNITOFDEMINGPUBLICSCHOOLS)NOTESTOTHEFINANCIALSTATEMENTSNote16–SubsequentPronouncements(continued)Althoughmanygovernmentsoffer tax abatements andprovide information to thepublic about them,theydonotalwaysprovidetheinformationnecessarytoassesshowtaxabatementsaffecttheirfinancialpositionandresultsofoperations,includingtheirabilitytoraiseresourcesinthefuture.ThisStatementrequires disclosure of tax abatement information about (1) a reporting government’s own taxabatementagreementsand (2) those thatareentered intobyothergovernmentsand that reduce thereporting government’s tax revenues. The requirements are effective for reporting periods beginningafterDecember15,2015.Statement78‐PensionsProvidedthroughCertainMultiple‐EmployerDefinedBenefitPensionPlans:Theobjective of this Statement is to address a practice issue regarding the scope and applicability ofStatement No. 68, Accounting and Financial Reporting for Pensions. This issue is associated withpensionsprovidedthroughcertainmultiple‐employerdefinedbenefitpensionplansandtostateorlocalgovernmentalemployerswhoseemployeesareprovidedwithsuchpensions.This Statement amends the scope and applicability of Statement 68 to exclude pensions provided toemployeesofstateorlocalgovernmentalemployersthroughacost‐sharingmultiple‐employerdefinedbenefitpensionplan that (1) isnota stateor localgovernmentalpensionplan, (2) isused toprovidedefinedbenefitpensionsbothtoemployeesofstateorlocalgovernmentalemployersandtoemployeesofemployersthatarenotstateorlocalgovernmentalemployers,and(3)hasnopredominantstateorlocalgovernmental employer (either individually or collectively with other state or local governmentalemployers thatprovidepensions through thepensionplan).ThisStatementestablishes requirementsforrecognitionandmeasurementofpensionexpense,expenditures,andliabilities;notedisclosures;andrequired supplementary information for pensions that have the characteristics described above. TherequirementsareeffectiveforreportingperiodsbeginningafterDecember15,2015.Statement 82 ‐ Pension Issues – an amendment of GASB StatementsNo. 67,No. 68, andNo. 73: ThisStatementistoaddresscertainissuesthathavebeenraisedwithrespecttoStatementsNo.67,FinancialReporting for Pension Plans, No. 68, Accounting and Financial Reporting for Pensions, and No. 73,AccountingandFinancialReporting forPensionsandRelatedAssetsThatAreNotwithintheScopeofGASBStatement68,andAmendmentstoCertainProvisionsofGASBStatements67and68.Specifically,thisStatementaddressesissuesregarding(1)thepresentationofpayroll‐relatedmeasuresinrequiredsupplementary information,(2)theselectionofassumptionsandthetreatmentofdeviationsfromtheguidanceinanActuarialStandardofPracticeforfinancialreportingpurposes,and(3)theclassificationof paymentsmade by employers to satisfy employee (planmember) contribution requirements. TherequirementsareeffectiveforreportingperiodsbeginningafterJune15,2016.

42

CESARCHAVEZHIGHSCHOOLCHARTERSCHOOL(COMPONENTUNITOFDEMINGPUBLICSCHOOLS)NOTESTOTHEFINANCIALSTATEMENTSNote17–RestatementThe Charter determined that its 2015 net position balance was overstated as a result of anoverstatement of 2015 receivables balances of Title I IASA, School Improvement, IDEA‐BEntitlementandTitle IStimulusrevenuesrecognized in fiscalyears2013and2014.Asaresultof theerror,anetadjustmenttotheJune30,2015statementofnetpositionfortheCharterwasrecordedtodecreasenetpositionby$234,417.TheimpactonpreviouslyrecordedentitywidenetpositionasofJune30,2015isadecreaseof$234,417andthereisnoimpacttothechangeinnetpositionfortheyearthenended.Inaddition,anetadjustmenttotheJune30,2015operationalfundwasrecordedtodecreasefundbalanceby $234,417. The impact on previously recorded fund balance as of June 30, 2015 is a decrease of$234,417andthereisnoimpacttothechangeinfundbalancefortheyearthenended.

REQUIREDSUPPLEMENTARYINFORMATION

43

CESARCHAVEZHIGHSCHOOLCHARTERSCHOOL(COMPONENTUNITOFDEMINGPUBLICSCHOOLS)SPECIALREVENUEFUNDSJUNE30,2016TheSpecialRevenueFundsareusedtoaccountforFederal,StateandLocalfundedgrants.Thesegrantsare awarded to the Charter with the purpose of accomplishing specific educational tasks. GrantsaccountedfortheSpecialRevenueFundsinclude:

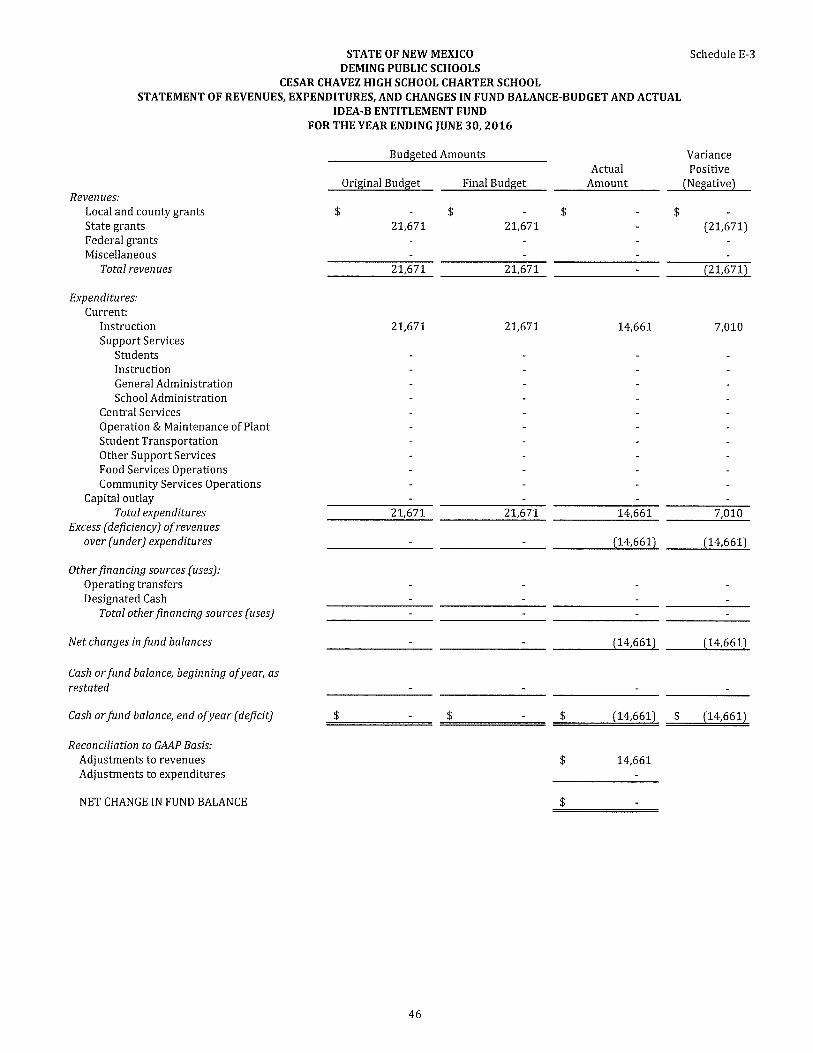

IDEABEntitlement(24106)–toaccountforaprogramfundedbyaFederalgranttoassisttheCharter in providing free appropriate public education to all handicapped children. FundingauthorizedbyIndividualswithDisabilitiesEducationAct,PartB,Section611‐620,asamended,Public Laws 91‐230, 93‐380, 94‐142, 98‐199, 99‐457, 100,639, and 101‐476, 20 U.S.C. 1411‐1420.

Title I School Improvement (24162) – accounts for the federal assistance provided to theCharterfortheimprovementofeducationalopportunitiestodeprivedchildren.(Authority,P.L.103‐382).

Microsoft Settlement (26170) – On November 6, 2001, the United States and Microsofttentatively agreed to the entry of a revised proposed Final Judgment to resolve the UnitedStates’civilantitrustcaseagainstMicrosoft.Thesettlementincludedthepurchaseofqualifyinghardware, and non‐custom software used with the hardware acquired through the use ofGeneral Purpose Vouchers or “Professional Development Services” or “IT Support Services”used in connection with the hardware or software acquired through the use of the GeneralPurposeVouchersand/orSoftwareVouchers.

Teacher Mentoring (27154) – created by P.L. 107‐110 to improve teacher and principalqualityandensurethatallteachersarehighlyqualified.

OTHERSUPPLEMENTALINFORMATION

OTHERINFORMATION

STATE OF NEW MEXICODEMING PUBLIC SCHOOLS

SCHEDULE OF VENDOR INFORMATION FOR Purchases Exceeding $60,000 (excluding GRT)CESAR CHAVEZ HIGH SCHOOL

CHARTER SCHOOLPREPARED DATED JUNE 30, 2016

Schedule V

Agency Number Agency Name Agency Type RFB#/RFP# (If applicable) Type of Procurement Vendor Name

Did Vendor

Win Contract?

$ Amount of Awarded Contract

$ Amount of AmendedContract

Physical address of vendor (City, State)

Did the Vendor provide

documentation of eligibility for

in-state preference?

Did the Vendor provide

documentation of

eligibility for

veterans' preference?

Brief Description of the Scope of Work

If the procurement is attributable to a Component Unit, Name of Component Unit

NONE

59

60

REPORTOFINDEPENDENTAUDITORSONINTERNALCONTROLOVERFINANCIALREPORTINGANDONCOMPLIANCEANDOTHERMATTERSBASEDONANAUDITOFFINANCIALSTATEMENTSPERFORMEDINACCORDANCEPERFORMEDINACCORDANCE

WITHGOVERNMENTAUDITINGSTANDARDSGoverningCouncilCesarChavezHighSchoolCharterSchoolDeming,NewMexicoandTimothyKellerNewMexicoStateAuditorWehaveaudited, inaccordancewiththeauditingstandardsgenerallyacceptedintheUnitedStatesofAmerica and the standards applicable to the financial audits contained in Government AuditingStandards issued by the Comptroller General of the United States, the financial statements of thegovernmentalactivities,eachmajorfund,thebudgetarycomparisonsoftheoperatingfundsandmajorspecial revenue funds of Cesar Chavez High School Charter School (“School”) as of and for the yearendedJune30,2016,andtherelatednotestothefinancialstatements,whichcollectivelycomprisetheSchool’s basic financial statements, and the individual funds, related budgetary comparisons, andfiduciary fund of the School, presented as supplementary information, and have issued our reportthereondatedNovember23,2016.InternalControlOverFinancialReporting

Inplanningandperformingourauditof the financial statements,weconsidered theSchool’s internalcontrol over financial reporting (internal control) to determine the audit procedures that areappropriateinthecircumstancesforthepurposeofexpressingouropinionsonthefinancialstatements,butnot for thepurposeofexpressinganopinionon theeffectivenessof theSchool’s internal control.Accordingly,wedonotexpressanopinionontheeffectivenessoftheSchool’sinternalcontrol.Ourconsiderationofinternalcontrolwasforthelimitedpurposedescribedintheprecedingparagraphandwasnotdesignedtoidentifyalldeficienciesininternalcontrolthatmightbematerialweaknessesorsignificant deficiencies and therefore, material weaknesses or significant deficiencies may exist thatwerenotidentified.However,asdescribedintheaccompanyingscheduleoffindingsandresponses,weidentified certain deficiencies in internal control that we consider to be material weaknesses andsignificantdeficiencies.A deficiency in internal control exists when the design or operation of a control does not allowmanagementoremployees,inthenormalcourseofperformingtheirassignedfunctions,toprevent,ordetectandcorrect,misstatementsonatimelybasis.

61

GoverningCouncilCesarChavezHighSchoolCharterSchoolDeming,NewMexicoandTimothyKellerNewMexicoStateAuditorAmaterialweaknessisadeficiency,orcombinationofdeficiencies,ininternalcontrolsuchthatthereisa reasonable possibility that a material misstatement of the entity's financial statements will not beprevented,ordetectedandcorrected,ona timelybasis.Weconsider thedeficienciesdescribed in theaccompanyingscheduleoffindingsandresponsesasitems2016‐11.

A significantdeficiency is adeficiency, or a combinationofdeficiencies, in internal control that is lesssevere than a material weakness, yet important enough to merit attention by those charged withgovernance. We consider the deficiencies described in the accompanying schedule of findings andresponsesasitems2016‐001tobesignificantdeficiencies.

ComplianceandOtherMatters

AspartofobtainingreasonableassuranceaboutwhethertheSchool’sfinancialstatementsarefreefrommaterial misstatement, we performed tests of its compliance with certain provisions of laws,regulations, contracts, and grant agreements, noncompliance with which could have a direct andmaterialeffectonthedeterminationoffinancialstatementamounts.However,providinganopiniononcompliancewiththoseprovisionswasnotanobjectiveofouraudit,andaccordingly,wedonotexpresssuchanopinion.Theresultsofourtestsdisclosedinstancesofnoncomplianceorothermattersthatarerequired to be reported under Government Auditing Standards and which are described in theaccompanyingscheduleof findingsandresponsesas items2013‐001,2013‐004,2016‐002,2016‐003,2016‐004,2016‐005,2016‐006,2016‐007,2016‐008,2016‐009,2016‐010,2016‐012.

CesarChavezHighSchoolCharterSchool’sResponsetoFindings

TheSchool’sresponsetothefindingsidentifiedinourauditaredescribedintheaccompanyingscheduleoffindingsandresponses.TheSchool’sresponseswerenotsubjectedtotheauditingproceduresappliedintheauditofthefinancialstatementsand,accordingly,weexpressnoopiniononthem.

PurposeofthisReport

The purpose of this report is solely to describe the scope of our testing of internal control andcompliance and the result of that testing, and not to provide an opinion on the effectiveness of theentity’s internal control or on compliance. This report is an integral part of an audit performed inaccordance with Government Auditing Standards in considering the entity’s internal control andcompliance.Accordingly,thiscommunicationisnotsuitableforanyotherpurpose.

Albuquerque,NewMexicoNovember23,2016

62

CESARCHAVEZHIGHSCHOOLCHARTERSCHOOL(COMPONENTUNITOFDEMINGPUBLICSCHOOLS)SUMMARYSCHEDULEOFPRIORAUDITFINDINGSFortheYearEndedJune30,20162013‐001CashReporting(Non‐Compliance inAccordancewith theNewMexicoStateAuditRule,DoesnotRisetotheLevelofSignificantDeficiency)Condition:Theschool’sactualcashinbankwas$38,745morethanthatreportedtotheNewMexico Public Education Department on the School’s year end cash report. Although thereconciledbalancewasaccurately reflectedon the cash report, itdidnotagree to thecashbalancesbyfundinthatsamereport.CurrentStatus:RepeatedReasonforfindingreoccurrence:TheSchoolwasnotabletoidentifyandcorrectthedifferenceincashbeforethefinalyearendreportswereprepared.CorrectiveActionPlan:ThepreviousauditentriesthroughJune30,2015havebeenmadetothe general ledger. The Business Manager for DCCCHSwill submit the corrections to theNMPEDontheupcomingDecember2016quarterlyreports.PersonResponsible:CharterSchoolBusinessManager2013‐004 Budgetary Controls (Non‐Compliance in Accordancewith theNewMexicoStateAuditRule,DoesnotRisetotheLevelofSignificantDeficiency)Condition: The school incurred expenditures in excess of budgetary authority in thefollowingfundsandfunctions: Generalfund‐instructionalmaterials:$1,109CurrentStatus:RepeatedReason for finding reoccurrence: The district did not request the budget adjustments toalleviatethesebudgetsoverrunsfortheCharter.CorrectiveActionPlan: The Principal and Governing Council will establish an appropriatepolicy and timeline of budgetary review prior to April 2016. The Business Manager willcoordinatewithDemingPublicSchoolsonanongoingbasistoensurethatthebudgetforeachfundisenteredintotheOperatingBudgetManagementSystem(OBMS).PersonResponsible:CharterSchoolPrincipalandGoverningCouncil

63

CESARCHAVEZHIGHSCHOOLCHARTERSCHOOL(COMPONENTUNITOFDEMINGPUBLICSCHOOLS)SCHEDULEOFFINDINGSANDRESPONSESFortheYearEndedJune30,20162013‐001 NMPED Cash Reporting, (Non‐Compliance in Accordance with the NewMexicoStateAuditRule,DoesnotRisetotheLevelofSignificantDeficiency)

Condition:We noted the NMPED Cash Report for 11000, 24000, and 31200 Fund did notagreetothegeneralledgerbalance,wenotedanetdifferenceof$35,257.

Management has not made progress in regards to reconciling cash report to the generalledger.

Criteria:PerstateauditruleSection6.20.2.13(D)and(E)ofNMAC,theauditreportofeachschooldistrictshallincludeacashreconciliationschedulewhichreconciledthecashbalanceasof theendof theprevious fiscalyear to thecashbalanceat theendof thecurrent fiscalyear.

Effect:TheNMPEDdoesnothaveanaccurateaccountingoftheSchool’sactivity.

Cause:TheSchoolscashreportdoesnotincludeadjustmentspreviouslymadetothegeneralledger.

Auditor’sRecommendation:Werecommendthatpoliciesandproceduresbeimplementedtoensure that all adjustments be completed before the final reports are submitted to thedepartment. Additionally, an individual should review the report to ensure that the reportmatchedthegeneralledgerandthecashaccountsasappropriate.

ManagementResponse:ThepreviousauditentriesthroughJune30,2015havebeenmadetothe general ledger. The Business Manager will submit the corrections to NMPED on theupcomingquarterlyreportsendingDecember2016.

64

CESARCHAVEZHIGHSCHOOLCHARTERSCHOOL(COMPONENTUNITOFDEMINGPUBLICSCHOOLS)SCHEDULEOFFINDINGSANDRESPONSESFortheYearEndedJune30,20162013‐004BudgetaryConditions(Non‐ComplianceinAccordancewiththeNewMexicoStateAuditRule,DoesnotRisetotheLevelofSignificantDeficiency)

Condition: The School has expenditure functions where actual expenditures exceededbudgetaryauthority:

TitleI $3,854

TitleISchoolImprovement $13,660

Managementhasnotmadeprogressinregardstobudgetaryconditions.

Criteria:PerNMAC6.20.2.9(A)everyschooldistrictshallfollowbudgetrequirementsstatedin Sections 22‐8‐5 through 22‐8‐12.2 NMSA 1978, and procedures of the department inpreparing, submitting,maintainingandreportingbudgetary information.Budgetarycontrolshallbeatthefunctionlevel.Over‐expenditureofafunctionshallnotbeallowed.

Per NMAC 6.20.2.10.B, School districts shall submit budget adjustment requests for theoperating budget to the department for budget increases, budget decreases, transfersbetween functional categories, and transfers from the emergency reserve account.Expenditures shall not be made by the school district until budget authority has beenestablished and approval received from the department. Budget adjustments shall not beincorporated into the school district’s accounting system until approval is received by thedepartment.

Effect: The Schoolwas out of compliancewith NewMexico state statute and funds spentcouldbeconsideredunallowable.

Cause: The School did not have an approved budget adjustment request (BAR)aforementionedfederalflow‐throughfundssubmitted.

Auditor’sRecommendation:WerecommendtheSchoolestablishapolicyofbudgetaryreviewattheendofeachquarterandhavetheboardapprovethenecessarybudgetaryadjustmentstoensurefundsarenotoverexpended.WerecommendthatallBARsareproperlycompletedfor all changes in funding received and that all BARs are approved by the board andsubmittedtothedepartmentpriortotheendoftheyear.

Management’sResponse: ThePrincipalandGoverningCouncilwillestablishanappropriatepolicy and timeline of budgetary review prior to April 2017. The Business Manager willcoordinatewithDemingPublicSchoolsonanongoingbasistoensurethatthebudgetforeachfundisenteredintotheOperatingBudgetManagementSystem(OBMS).

65