Entrepreneur characteristics, competitive strategy, firm ...

CEO Characteristics, Firm Performance, and Corporate Political Contributions:

A Firm Level Analysis

Manohar Singh,

The Pennsylvania State University-Abington

Email: [email protected]

Vijaya Subrahmanyam,

Mercer University-Atlanta

Email: [email protected]

Anita Pennathur,

Florida Atlantic University

Email: [email protected]

CEO Characteristics, Firm Performance, and Corporate Political Contributions:

A Firm Level Analysis

Abstract:

We investigate if CEO characteristics and firm performance determine the choice of Political

Action Committee (PAC) contributions by firms. Using a unique, hand-collected database, we

also focus on the identity of the politicians receiving PAC contributions to examine the impact of

the value-relevance of such contributions. Examining data on corporate contributions made to

candidates seeking federal office during the 2002, 2004, and 2006 election cycles, we find that

CEO dominance and interest alignment influence strategic choices of firms with regards to

establishing PACs. Our analysis of value-relevant contributions shows that firms prefer to donate

to politicians representing the state of a firm’s headquarters, validating the truth to the old adage

that all politics is local. However, these targeted political contributions do not impact upon firm

performance.

JEL Classification: G 3, G34, K2

Keywords: Corporate Political Contributions; CEO Dominance; CEO Characteristics; Firm

Performance, Agency Theory

1. INTRODUCTION

In 2010, the Supreme Court in a landmark ruling in Citizens United v. Federal Election

Commission legalized independent corporate political spending. The Super Political Action

Committees (Super PACs) play an increasingly pivotal role during the election cycle, and

corporations have to take a stand on whether, and how, to embrace this new doctrine which now

allows them to make direct contributions to political groups. Public companies (such as Bank of

America, Target, and 3M) have taken some dissent from shareholders who are pushing the issue

of super PACs at annual meetings. Corporate political spending has been a key focus of

shareholder resolutions with over 500 filed in the past five years alone1. With some trepidation

about shareholder reactions, corporations are increasingly supporting organized political giving.

Overall, super PACs have raised $314 million through the end of June 2015, compared with $26

million at the same time in 20112.

While limited, previous research in corporate finance has examined whether such political

contributions by firms are value-adding in terms of both accounting and stock price performance

of the firm. Although corporate political activities may yield strategic advantages to politically

active firms, they may also be a manifestation of self-serving behavior of top management,

including the CEO. Agency theory suggests that CEO dominance and interest alignment may

determine corporate decisions on political spending. These decisions do not focus only on whether

to engage in political spending, but also, and more importantly, on how to target such spending.

Thus, the research focus of this paper is twofold: first, to understand if CEO characteristics,

1 http://siinstitute.org/press/2012/02282012_ProxyPreview2012_PressRelease_FINAL.pdf; http://www.uspirg.org/news/usp/spring-

shareholder-meetings-investors-call-increased-transparency-corporate-lobbying-and; https://si2news.files.wordpress.com/2014/08/si2-2014-

proxy-season-mid-year-review-corporate-political-activity-excerpt.pdf?width=100 2 http://www.huffingtonpost.com/entry/oligarchy-super-pac-megadonors-have-conquered-american-

politics_55bc1eece4b0b23e3ce2f5ec

specifically those reflecting CEO dominance and interest alignment, determine the choice of PAC

contributions, and second, to examine if firm performance impacts corporate political spending

decisions. Specifically, our study seeks to explain the rationale for engaging in corporate political

activity, and whether participating firms are able to make value-relevant choices in the PACs and

politicians that they target for such contributions.

Financial accounting literature notes that CEO incentive structures affect the behavior and

outcomes of firms, (Bebchuk, Cremers, and Peyer, 2008; Morse, Nanda, and Seru, 2011) and as a

result dominant CEOs with weak firm performance may lean toward greater political contribution

to influence policy in their favor. Using aggregate data on corporate contributions made to

candidates seeking federal office during the 2002, 2004, and 2006 election cycles, we investigate

whether CEO dominance and interest alignment influence political spending choices in terms of

establishing PACs. Furthermore, while we begin with a simple, binary variable which examines

the factors that precipitate into a decision to form a PAC or not, we construct a more nuanced

measure to examine the impact of “good” or “value-relevant” participation. We compile a unique

firm-level database which allows us to focus on the identity of the specific politicians who are the

recipients of PAC contributions, the committees in which they serve, and their home-location.

This enables us to investigate the performance impact of such contributions.

The decision to participate in corporate political activities, if directed towards influencing

policy favorably for the firm, should result in increased revenue leading to improved accounting

performance and greater wealth for the shareholders. Major strategic choices, as proposed by firm

top management, are scrutinized and approved by board of directors. However, a dominant CEO

could influence and sway the board to pursue particular political engagements as non-market

strategies. While a value-maximizing dominant CEO may direct such political activities for the

benefit of the shareholders, he may very well try to benefit himself in terms of promoting political

clout, increasing social status, achieving career aspirations, and increasing his personal wealth.

Such influence by the CEO would depend largely on three factors: his dominance over the decision

making system, the degree of alignment of interests of the CEO with those of the shareholders in

terms of his ownership and compensation contract, and the level of firm performance. We define

firm performance to include both accounting and market value measures. To clearly delineate the

complexity of interaction among the three factors, we first examine the link between political

contributions and CEO characteristics. Second, we investigate whether or not political activities -

to the extent determined by CEO characteristics - enhance firm performance. While the first set

of tests will shed light on whether potential agency conflict, proxied by CEO dominance and

interest alignment, influences corporate political stances, the second set of tests will verify if

political contributions are actually detrimental to shareholder interests or whether they help align

CEO-shareholder interests. However, it may be possible that political engagements improve

accounting performance and shareholder wealth while simultaneously promoting a CEO’s

personal interests. In this sense, political engagements may not be strictly characterized as agency

costs.

While the analysis explains the rationales behind firm political participation, a more

important and interesting question asks how firms target their political contributions. From the

firm’s viewpoint, such targeted spending may be perceived as ‘good’ when the firm donates to

the politicians who can influence firm performance. We form a unique database and develop

several proxies to measure “good” political spending by firms. Our measure focuses on the

identity of the politicians who receive political contributions from the firm. We define a “value-

relevant” or a “good” political contribution as one where the contributions are directed to

members of the U.S. House of representatives or the Senate who are in a position to influence

the performance of the firm. To this end, we examine the specific committee assignments as

well as the location of the politicians to whom firms donate to see if firms are able to influence

policy. It is plausible to argue that by making donations to politicians from their home state or

to those who serve in relevant industry committees, firms stand to gain.

Recent literature (Hillman, Keim, and Schuler, 2004; Bebchuk and Cohen, 2005; Hersch,

Netter, and Pope, 2008; Bennett and Loucks, 2008; Cooper, Gulen, and Ovtchinkkikov, 2010;

Barclift, 2011; Mathur and Singh, 2011) has increasingly focused on corporate political

participation and its bearing on accounting performance and firm value. Mathur and Singh (2011)

summarize the literature and present two broad schools of thought on corporate political

contributions and shareholder value. One strand of thought holds that corporate political spending

may be value-adding when corporations make political contributions to favorably influence policy

stance(s). Conversely, agency-theoretic perspectives may view political contributions as a

manifestation of managerial consumption and consider them to be profligate expenditures. Farrell,

Hersch, and Netter (2001), Ozer (2010), and Prabhat (2012) suggest that political contributions

may or may not enhance shareholder value, and that there is often a playoff between managerial

versus shareholder power. To the extent that political engagements may help a firm promote

legislation restricting entry or competition in its industry, political contributions made by that firm

help create shareholder value. A firm's involvement in political activity, however, may be largely

driven by management who exercise control over the allocation of resources within a firm.

Executive ownership stake and compensation structures often dictate managerial preferences

regarding political leanings and consequent PAC contributions that may not always promote

optimal accounting performance or the shareholders’ interests, thus destroying firm value and

shareholder wealth.

While the ruling in Citizens United v. Federal Election Commission, and the last U.S.

election season, may have brought some of these issues to the forefront once again, issues

surrounding political contributions by firms are not unique to the U.S. Corporate political

spending activity can differ globally. Faccio (2006) documents that the most number of politically

connected firms are found in countries with high levels of corruption and weak legal systems.

Fisman (2001) examines political connections between Indonesian firms and the Suhorto family

to document a loss of firm value on the news of the President’s poor health. Research shows mixed

results in terms of the performance impact of political connectedness. Bobkari, Kosset, and Saffar

(2012) examine a sample of firms headquartered in 12 developed and 11 developing countries to

examine how the political connections of publically traded firms impact their accounting

performance and financing decisions. They find that politically connected firms have better

performance as measured by ROA, and that these firms are also more liquid than their non-

politically connected counterparts. Moreover, the authors document that political connection is

associated with increased financial leverage and debt maturity.

Mobarak and Purbasari (2006) find that firms with political ties to President Suhorto

are more profitable and export-oriented than their non-connected counterparts. However,

Facio (2010) documents that despite the advantages of political connectedness, such firms

document worse accounting performance when compared to their non-connected peers.

Similarly, examining politically connected firms in France, Bertrand et al. (2007) find a

negative correlation between firm performance and the political connections of its CEO.

Examining the impact of location, Facio and Parsley (2009) document that firms located in the

politician’s hometown lose value upon news of the unexpected death of the politician.

We extend this line of research by evaluating if political connectedness through PAC

participation is aimed at value creation and if it actually helps firms create value. Our results show

that firms with dominant CEOs, proxied by CEO duality, have a greater propensity to make PAC

contributions. While CEO age in absolute terms does not influence corporate political decisions,

CEO age relative to the board impacts such decisions. PAC contributions are more likely in

instances when the firm has a relatively older CEO. We also find support for the agency-theoretic

argument that political participation increases with CEO compensation. With respect to interest

alignment, larger ownership holdings by CEOs lessen the propensity for political engagement. The

second objective of our paper is to investigate the relationships between CEO characteristics,

political participation, and firm performance, as poorly performing firms may be more likely to be

politically engaged. Our full sample results show that strong CEOs with interests aligned with

those of shareholders, make value-maximizing decisions for the firm, as proxied by firm stock

return and firm ROA. Thus, it appears that, to the extent CEO characteristics predict PAC

contributions; PAC determines performance.

A unique aspect of this study is that we construct a hand-collected dataset of the politicians

receiving contributions from firms to examine the “value-relevance” of such contributions. We

match firm location and industry with the home-state and Committee assignments of the politicians

receiving PAC donations. We then investigate the sub-sample of participating firms to investigate

whether firms make value-relevant contributions. The results for CEO dominance reinforce

findings of the full sample results; while we document some linkages between CEO dominance

and value-relevant contributions, there is no strong evidence that dominant CEOs contribute more

to politicians who can impact the firm. From an interest alignment perspective, our results show

that CEOs with a higher equity stake in the firm align themselves by making greater contributions

to politicians from their home state. Interestingly, we find that firms with higher institutional

ownership donate less to politicians from the home state, perhaps reflecting a reluctance of large

investors to openly court politicians.

An important contribution of our paper is to investigate how firm performance impacts

PAC contributions, as it could be the case that poorly performing firms will make larger value-

relevant contributions in an attempt to favorably influence politicians. Overall, our results

demonstrate that well performing firms make fewer value-relevant donations. We find that better

performing firms, measured by stock return, donate less to politicians from their home state, while

firms with higher ROAs and ROEs tend to donate less to politicians who hold committee

assignments in the industry in which the firm operates. In summary, our results suggest that firm

performance may impact influence ‘good’ (value-enhancing) decision making.

The remainder of the paper is as follows. We discuss the theoretical and empirical

framework to develop our hypotheses in Section 2, and present the data and methodology in

Section 3. Section 4 provides the results and discussion, while conclusions are presented in the

Section 5.

2. LITERATURE REVIEW AND RESEARCH HYPOTHESES

In order to develop the hypotheses, we discuss three main strands of the literature

pertaining to CEO characteristics, political participation, and firm performance.

(i) CEO Dominance and Corporate Political Contributions

Leadership theorists often believe that CEOs make strategic and tough corporate decisions,

set the vision and direction for their companies, and thereby directly influence firm performance.

On the one hand, a powerful CEO with a strong network may benefit shareholders by garnering

valuable information via his connections and thus make value-adding decisions for the firm

(Engelberg, Gao, and Parsons, 2012). Alternately, a powerful CEO may heighten agency conflicts,

endorse managerial entrenchment, defuse the board, and endanger firm value (Bebchuk, Cremers,

and Peyer, 2011; Brown, Jr., 2012). Mande and Son (2012) find that CEO centrality, i.e., their

relative power within the board, can lead to earnings manipulation. For the most part, the board’s

role is defined by its relationship with corporate officers, particularly the CEO, since management

is privy to information while most directors have little ‘independent’ information other than that

provided at board meetings (Khurana, 2002; Brown, Jr., 2012). Moreover, if the CEO is also the

Chair of the board (CEO Duality), the agenda and information disseminated is controlled by the

CEO.

Literature has not reached any consensus on whether firms with CEO duality have

outperformed those firms with split CEO-Chairs (Jensen, 1993; Dahya and Travlos, 2000; Brown,

Jr., 2012). Lasfer (2006) studies the relationship between managerial ownership and board

structure for UK boards. He finds that higher managerial ownership entrenches managers by

allowing the CEO to create a board that is unlikely to monitor. Such a board is dominated by

executive directors, a dual CEO/Chairman, and has a lower probability of a non-executive director

as chairman. This result is more pronounced for large firms than for small firms. While board

composition has been shown to be an effective governance mechanism, Brown, Jr. (2012) argues

that by influencing board selection, the CEO neutralizes (renders the board less effective) the

monitoring function of the board and since the CEO hires and fires other managers, he often makes

the most important business decisions.

Decisions regarding corporate political activity, and the level of such commitments, often

rest with the CEO and senior executives. In examining the proclivity of top management in firms’

decision to engage in political activity, Ozer (2010) notes that CEOs with long-term tenure realize

how changes in the political environment impact their firm's decisions. Thus, older and longer

tenured CEOs may favorably influence decision making in the firms’ favor or in an agency-

theoretic construct, entrenchment may manifest itself in profligate consumption. Corporate

political contributions are often viewed as non-market strategies utilized by management of firms

to gain competitive advantage (Ozer and Lee, 2009; Ozer, 2010). This may take the form of

utilizing connections, lobbying, and donating (time and funds) so as to nudge politicians to

advance the agenda of the manager(s) or the firm by reducing disclosure requirements and industry

competition, and reducing legislative restrictions on executive compensation among others.

Given the literature detailed above, we hypothesize that CEO characteristics that define the

CEO centrality impact a firm’s decision to engage in corporate political activity through PACs.

CEO dominance hypothesis: Political engagements as perquisite consumption are agency

driven, and firms with dominant CEOs are more likely to be politically engaged. Firms

with greater number of executive board members (insiders), duality (same CEO-Chair),

older CEOs (entrenched) or long tenured CEOs - as measures of CEO dominance - have

greater likelihood of political engagement through PACs. Moreover, CEO dominance

characteristics will be positively related to the percentage of “value-relevant”

contributions made by participating firms.

(ii) Interest Alignment and Corporate Political Contributions

Morse, Nanda, and Seru (2011) find evidence that powerful CEOs get paid more. They

argue that powerful CEOs are able to persuade boards enough to slant the weights on their

performance in their favor, and thus opportunistically extract rents in the form of masked incentive

pay, consequently hurting firm performance. Agency-theoretic studies show that interest

alignment often manifests in compensation packages. Given asymmetry of information, and weak

governance structures, self-serving managers may promote their interests at the cost of

shareholders. Managers may use their political connections to promote their own career prospects

and attain socio-political status. Thus, political contributions may be more a management

perquisite consumption rather than being value relevant for the firm (Aggarwal, Meschke, and

Wang, 2012; Ozer, 2010). Studying the design of executive compensation contracts, Lord and

Saito (2012) examine factors that affect CEOs’ personal risks by examining the real value of

executive pay, the riskiness of firm equity, the value of their equity portfolios, and the delta of

such equity holdings and note that the impact on CEOs’ personal risks impacts the design of their

compensation contracts. Farrell, Hersch, and Netter (2001) focus on individual executive

contributions to PACs and their compensation packages and argue that well designed executive

contracts align interests of management and shareholders, and provide evidence that firms make

higher PAC contributions when their management has greater equity and stock-options. They

report that the incentive structures of CEOs are significantly related to PAC contributions.

Hartzell and Starks (2003) document the role played by institutions in corporate

governance and in determining compensation levels by voting preferences. They also note that

accounting for firm and industry, institutional ownership concentration is positively related to the

pay-for-performance sensitivity. Increasingly, global institutional investors call for more

transparency and disclosure in corporate political and lobbying expenditures3. Ozer, Oneonta, and

3 Gilbert, K, “Institutional Investors Demand Disclosure on Companies’ Political Spending,” Institutional Investor, June 06,

2012, http://www.institutionalinvestor.com/article.aspx?articleID=3041331; “Investor group reacts to Aetna political

contributions report, says lack of disclosure underscores need for greater transparency in corporate political and lobbying

expenditures”, The Sacramento Bee, August 30th, 2012;

http://www.sacbee.com/2012/08/30/4771462/investor-group-reacts-to-aetna.html

Ahsan (2010) examine the influence of the different institutional owners on corporate political

strategies. Their results demonstrate that institutional investors with a long time horizon are more

in favor of firms’ engagement in political strategies.

In strategic decisions such as political engagement by the firm, CEOs’ ownership stakes,

as well as their compensation, may influence their alignment with the investors in the firm. The

discussion from the literature above leads us to hypothesize as follows:

Interest-Alignment Hypothesis: Within agency conflict perspective, our null hypothesis is

formulated in terms of political activities as positive value propositions that are incentive

driven, and firms with CEOs who have higher ownership stakes, or better compensation

packages, have relatively greater degree of interest alignment with shareholders and thus

are more likely to participate in or contribute to firm’s PAC activities. Additionally, CEO

interest alignment characteristics will be positively related to the percentage of “value-

relevant” contributions made by participating firms.

(iii) CEO Characteristics, Corporate Political Contributions and Firm Performance

Given the research described earlier on CEO dominance, a value-maximizing CEO may

engage in political activity and use his connections to sway legislative policies that favor the firm.

Alternately, he may encourage such political activity largely to gain socio-political status for

himself and thus increase his own wealth, often at the expense of the shareholders. There is no

clear consensus in the literature that political contributions characterize investments that create

corporate value.

One stream of related research has demonstrated strong links between CEO dominance and

lowered firm value, lower profitability, exploitative behavior, poorer decision making, lower

turnover, and lower firm performance (Adams, Almeida, and Ferreira, 2005; Bebchuck, Cremers,

and Peyer, 2008). Adam, Almeida, and Farreira (2005) find that stock returns are most variable

in firms in which dominant CEOs can influence decision making. Measuring CEO centrality via

CEO's pay slice, Bebchuck, Cremers, and Peyer (2008) find that controlling for firm-specific

characteristics, high CEO pay slice is correlated with lower firm-specific variability of returns.

Coates (2011) compares valuations of firms, with varying levels of lobbying and contributions to

corporate PACs, before and after Citizens United, and finds that outside of heavily regulated

industries, political activity is associated with lower firm value. Examining corporate donations to

political candidates for federal offices in the US, Aggarwal, Meschke, and Wang (2012) note that

contributing firms’ operating characteristics show consistently low free cash flow and weak

performance (returns). They suggest that managers make political donations because of their own

political interests, which may often not coincide with the political interests of their shareholders.

An alternate stream of literature suggests that politically engaged firms may be better

positioned to sway policy in their favor, and such ‘political capital’ investment (in the form of

contributions) may be value-adding. Faccio (2006) suggests that there is a ‘political risk premium’

attached to politically engaged firms supporting a positive link between political engagements and

corporate performance. Cooper, Gulen, and Ovtchinnikov (2010) use US FEC data on political

contributions made by public firms and find a very high rate of return for firms participating in the

political contribution process, especially for firms that support candidates from the state where the

firm is headquartered. Farber, Johnson, and Petroni (2007) and Liebman and Reynolds (2009)

argue that if the benefits gained from political contributions are higher than PAC costs, there is a

real economic benefit for firms to participate in the political process.

The value consequences of corporate political contributions combined with an influential

and powerful CEO may lead to board decisions that may be less than optimal for the shareholder

unless the interests of the CEO are aligned with those of the shareholders via compensation

contracts or ownership stakes. Aslan and Grinstein (2012) study political contributions and their

relationship to CEO pay and note that controlling for industry and CEO and board characteristics,

a one standard deviation increase in CEOs’ political connections result in a 9 percent rise in CEO

compensation and a 17 percent decline in pay-performance sensitivity.

The literature above does not point to a definitive conclusion as to whether political

participation by firms is agency driven or not. Such an answer may only be reached after we test

and estimate the performance impact of such political activities. To summarize the arguments

from the literature above, in one possible scenario, political engagements reflect self-serving

behavior by the CEO at the cost of shareholders. Here, we expect a positive relation between CEO

characteristics reflecting agency conflict (dominance) and PAC contributions, and a negative

relation between PAC contributions and firm performance. In an alternative scenario, political

engagements are value-adding. In this case, we expect to see a positive relation between CEO

interest alignment (ownership and compensation) and PAC contributions and also between PAC

contributions and firm performance. Yet another scenario exists. In this instance, while political

engagements promote the personal interests of a CEO, they also are shareholder value enhancing.

While we may find a positive relation between CEO dominance (a proxy for agency conflict) and

the choice to associate with and contribute to a PAC, we cannot interpret these findings in terms

of agency conflict. Political engagements, in this instance, are actually interest aligning choices

wherein both the parties realize gain. So, formally hypothesizing the triangular relation between

CEO characteristics, political strategic choices, and firm performance is an interesting, albeit a

complex one. We postulate our third hypothesis relating CEO characteristics, corporate political

contributions, and firm performance as follows.

Firm performance hypothesis: Corporate political strategies are shareholder value

enhancing and promote CEO interests as well. A greater degree of CEO dominance and

greater interest alignment is associated with greater degree of political participation via

PACs and better firm performance. Moreover, CEO dominance and interest alignment

characteristics will be positively related to the “value-relevant” contributions made by

participating firms.

We first examine the impact of CEO characteristics and interest alignment on both the

likelihood of engaging in political activity. Next, we focus on participating firms alone to examine

the impact of CEO characteristics and interest alignment on the percentage of “value-relevant”

contributions made by the firm. Prior to describing the data and methodology adopted, we discuss

the control variables that also potentially impact the choice of political participation by firms.

(iv) Control Variables

Literature shows that firms that make political contributions on average have lower returns,

higher book-to-market, lower cash flow, and higher leverage compared to non-contributing firms

and that political connectivity gives firms greater access and more favorable rates to debt financing

(Faccio, Masulis, and McConnell, 2006; Faccio, 2010; Johnson and Mitton, 2003; Khwaja and

Mian, 2005; Cull and Xu, 2005; Claessens, Feijen, and Laeven, 2008; Cooper, Gulen, and

Ovtchinnikov, 2010). Furthermore, recent researchers point to a positive relationship between firm

size and political activity (Cooper, Gulen, and Ovtchinnikov, 2010; Macher, Mayo, and Schiffer,

2011). While board size appears to have a link to firm value, there is no clear consensus in literature

whether smaller boards are more effective than larger boards (Jensen, 1983; Yermack, 1996; Klein,

1998; Eisenberg, Sundgren, and Wells, 1998; Hermalin and Weisbach, 2003; and Coles, Daniel,

and Naveen, 2008). Research has shown that added growth opportunities as a result of political

connectedness increase the willingness of firms to contribute to PACs (Mathur, Singh, Thompson,

and Nejadmalayeri 2012). We utilize market to book ratio to capture higher growth opportunities.

Industry effects have been controlled for in the literature to capture the different regulatory and

policy issues (Schuler, Rehbein, and Cramer, 2002; Macher, Mayo, and Schiffer, 2011). In order

to isolate industry effects on PAC contributions and their performance impact, we use one-digit

SIC codes as industry dummies.

3. DATA AND METHODOLOGY

(i) Data

We begin with a sample of all S&P 500 firms. Next, we obtain information on PAC

contributions from the Center for Responsive Politics (CRP). CRP provides a record of PAC

contributions information derived from national corporate filings from the Federal Election

Commission (FEC). We compile data on aggregate corporate contributions made to candidates

seeking federal office during the 2002, 2004, and 2006 election cycles. The financial market crisis

that ensued in 2007 changed the political rhetoric and climate in the country leading to fierce

partisanship, and the emergence of extreme positions and factions in both political parties. As

both the fierce partisanship and the economic crisis have influenced the election cycles beginning

in 2008, we do not extend the sample period beyond the 2006 election cycle, since we do not want

to confound our results. Our initial sample of firms making political contributions comprises of

289 firms for 2002, 315 firms for 2004, and 301 firms for 2006. Next, we obtain annual income

statement and balance sheet information on the firms from COMPUSTAT, eliminating financial

firms (SIC codes 6000-6999) from our sample. We then acquire board information from The

Corporate Library’s (TCL) Board Analyst database, which compiles data on firm proxy

statements. We extract proxy information for our sample of firms for the years 2000-2006. Our

final sample matches PAC contributions data from the CRP, board data from TCL, and financial

data from COMPUSTAT, leaving us with a dataset of 1204 firm year observations for the period

of 2002 to 2006.

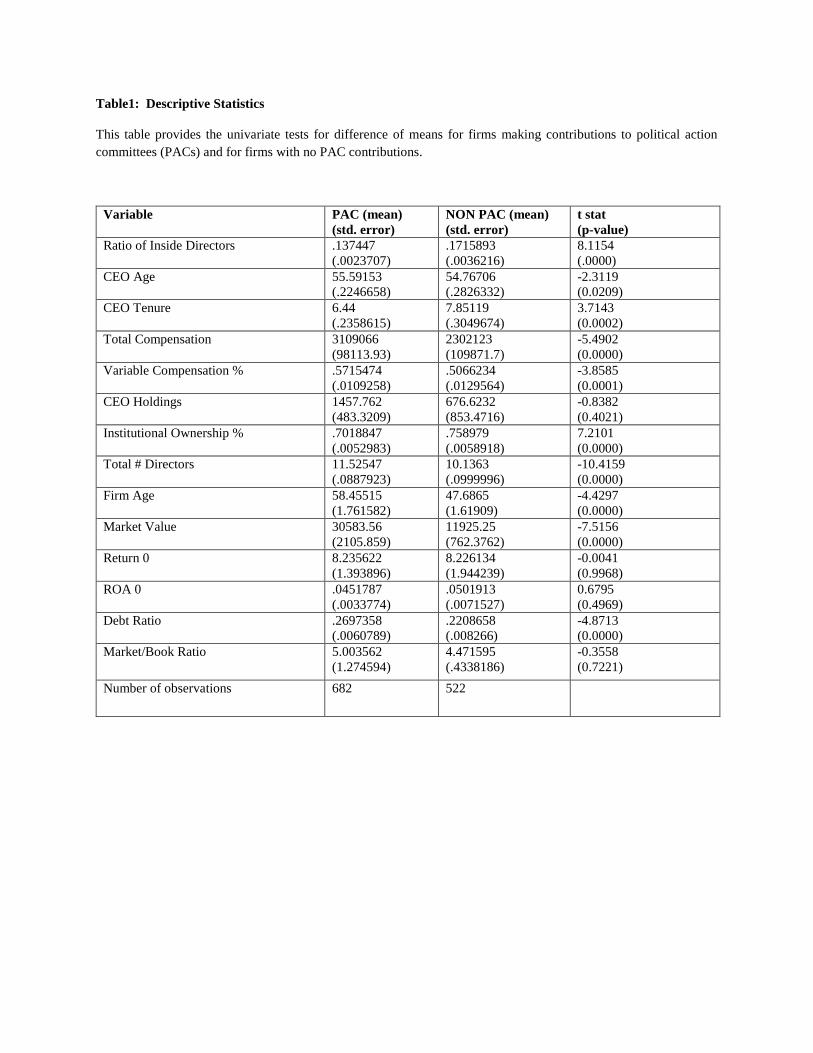

Table 1 provides the univariate tests of difference of means for the firms in our sample for

both the PAC contributing and non-contributing firms in our sample.

<insert Table 1 about here>

Within our sample of 1204 firm- observations, a total of 682 observations pertain to firms

that have an active PAC while 522 pertain to firms that do not. The politically active firms in our

sample have a significantly higher number of directors on their board (12) when compared to the

non-PAC contributing firms (10). However, PAC firms have a significantly lower percentage of

inside directors (14%) than non-PAC firms (17%). The average CEO in a PAC contributing firm

is 56 years of age, compared to the average CEO age of 55 years in a non- contributing firm; this

difference is statistically different at the 5% level. CEOs of contributing firms have served

significantly lower tenures (6 years) when compared to their non-contributing counterparts (8

years). Moreover, CEOs in politically active firms earn significantly higher total compensations

and variable compensations when compared to CEOs in firms which do not make political

contributions. Although there is no significant difference in the CEO ownership stake between

the two types of firms, PAC contributing firms have a marginally lower institutional ownership

than non-contributing firms. Contributing firms are significantly older as well and are, on average,

about 10 years older than non-contributing firms. The average contributing firm is also

significantly larger, with a market value of almost three times that of the non-contributing firm.

PAC contributing firms are also significantly more leveraged. However, the lagged returns and

market to book ratios are not significantly different for the two types of firms. Overall, the

univariate statistics presented above demonstrate significant differences in CEO and firm-level

characteristics between contributing and non-contributing firms.

(ii) Methodology

Full Sample:

We begin our analysis of the propensity of a firm to make a political contribution by

estimating the following probit model:

Likelihood to Contribute = ß0 + ß1 (CEO Dominance/Interest Alignment) + ß2 (Control Variables)

+ ɛ (1)

The dependent variable is a binary variable which equals one for PAC contributing firms,

and zero otherwise. The independent variables that measure CEO dominance include the ratio of

inside directors, CEO age, and CEO tenure to test the CEO dominance hypothesis. The

independent variables for the test of the interest alignment hypothesis include the ratio of CEO

holdings to total common equity, percentage of institutional ownership, the natural log of CEO’s

total compensation, and percent variable compensation. Our control variables are board size, firm

size (natural log of the market value of equity), lagged return, growth opportunities (market/book

ratio), leverage (debt/assets ratio), and industry effects (one-digit SIC code industry dummies).

In order to determine how PAC contributions, as determined by CEO characteristics,

impact firm performance, we estimate a two-stage model. At the first stage, we estimate the extent

to which CEO characteristics predict PAC contributions via the following model:

Total Contribution = ß0 + ß1 (CEO Dominance/Interest Alignment) + ß2 (Control Variables) + ɛ

(2)

where, the CEO dominance, interest alignment, and control variables are the same as

described earlier.

At the second stage, we relate the predicted PAC contribution to firm performance via the

following model:

Firm Performance = ß0 + ß1 (Predicted PAC Contribution) + ß2 (Control Variables) + ɛ (3)

where, contemporaneous stock return, ROA, and ROE, are the firm performance measures. The

predicted contributions are obtained from the first step of the estimations, and the control variables

are firm size, two-year sales growth rate, debt ratio, and industry effects.

Participating Firms Sample:

While one of the motivations of the paper is to analyze differences between

participating firms and non-participating firms, a more discerning aim is to examine whether firms

are able to benefit from such participation. We therefore repeat the estimations above for our

sample of participating firms alone. We develop proxies which focus on the identity of politicians

receiving political contributions from firms. We define a ‘value-relevant’ (good) contribution as

one where a firm donates to a politician who is deemed to be in a position to positively impact the

firm.

In order to develop variables that represent proxies for ‘value-relevant’ (good)

contributions by firms’ PACs, we hand-collected data from the FEC database using the following

steps. We first search in the full sample database for a PAC associated with each firm name in the

FEC database. If we find a PAC associated with the firm, we include the firm in a new

‘participating firm’ subsample to gather detailed data for each of these firms. For each of these

participating firms, we create three separate subsample datasets for each year to gather information

from the FEC database. Next, under the ‘PAC’ information from the FEC Database, we use the

‘Summary’ tab to find the ‘location’ and ‘Industry’ for each year for the participating firm in

question and add these fields to the participating firms’ subsample database. Following this, from

the ‘Recipients’ tab within the PAC Data (within the FEC Database), we collect the entire list of

names of House members and Senate recipients for each year along with the amount that each

politician received in ‘contributions’ for the year from the firm’s PAC for each participating firm.

We sort, by year, each list of Senators and House members, by the ‘amount of contribution’. We

then highlight the top five contributions for each firm for each year4 separately for the House and

Senate. Next, we select the tab ‘Politicians & Elections’ within the FEC database and do a search

within this section for each politician’s location and committee assignments for our list of

recipients for each firm for every year. Using the data from this section, we create corresponding

fields in the participating firms’ subsample database on each politician’s committee assignments

and location for each year.

In summary, we first examine if a firm is a participating firm and include it in a

‘participating’ firm database and collect information on its location and industry for the years 2002,

2004 and 2006. Following that, we gather information on a firm’s PAC contribution to the House

members and Senators (using the FEC database) and rank these contributions in descending order

of the dollar value of the contributions and also gather information on the location of the

politicians’ in question for each year for each firm. We then focus on the top 5 contributions of the

PAC to the House (and the Senate) members and define value-relevant contributions in two ways:

1. A contribution is considered value-relevant (good) if the recipient’s committee

assignment in the year in question (2002, 2004 or 2006) matches the industry in which

the contributing firm operates. If not we consider it a ‘non-value relevant’ (bad)

contribution.5 For each year, we define the value relevance ratio based on ‘industry

match’ as follows:

Industry Match = $ of value relevant contributions to the House (Senate)

members/Total $ value of all contributions to House (Senate) members.

4 The top five contributions may include several or all the contributions made. For instance if 30 house members received $5000 each, all 30 would be included. 5 The Congressional committee assignment was matched to the industry of the firm. The industry and location for each firm was listed under the FEC database under ‘Summary Information for each firm’ and was collected in creating the database. Besides matching the industry, in all cases, if the Congressional committee assignment for the House member or Senator was in ‘Appropriations’, ‘Budget’ or ‘Ways and Means’, we included it as value-relevant as well.

2. A contribution is considered value-relevant (good) if the Location of the House member

(or Senator) in the year in question (2002, 2004 or 2006) matches the contributing firm’s

headquarter location. If not, we consider it a ‘non-value relevant (or bad) contribution.

For each year, we define the value relevance ratio based on ‘location match’ as follows:

Location Match= $ value relevant contributions to the House (Senate) (based on

location)/Total $ value all contributions to the House (Senate).

4. EMPIRICAL RESULTS

Our first set of estimations test the CEO dominance hypothesis. We model the propensity

to make PAC contributions as a function of CEO dominance, as proxied by the ratio of inside

directors, CEO duality, CEO age, rCEOage (CEO age relative to the board) and CEO tenure. We

check for the VIF statistics and our results do not find any strong indication of multicollinearity

among our explanatory variables. Table 2 provides the results of the probit estimations for the

CEO dominance hypothesis.

<insert Table 2 about here>

Contrary to our null hypothesis that firms with a higher ratio of inside directors would be

more likely to make a PAC contribution; we find that such firms are significantly less likely to be

politically engaged via a PAC involvement. This result is both statistically and economically

significant. A 1% increase in the ratio of inside directors leads to a 2.25% decrease in the

probability of a PAC contribution. While the above results do not support the agency view of

political engagements, our results on CEO duality (Model 2 of Table 2) strongly support the

hypothesis that dominant CEOs who hold the dual title of CEO/Chair would be more likely to be

politically engaged.

We hypothesized that firms with older, and therefore more entrenched CEOs, would be

more likely to engage in a PAC contribution; however our results do not support such a link

between CEO age and PAC contributions. However, it is possible that the dynamics of the board

decision-making are influenced by the relative age of CEO with respect to that of the rest of the

board. For example, if there are several older board members, the CEO may not be as dominant as

in a firm where the board, on average, is younger. To measure the CEO age relative to the board

we construct a new variable, rCEOAGE. We define this variable as CEO age divided by the

number of directors on the board who are more than 70 years of age. This ratio captures relative

experience of the CEO compared to the board. The expectation is that for firms where the board

is composed of relatively younger directors, the CEO is more influential or dominant. This

variable combines the plurality of older directors as well as the relative age of the CEO. Indeed,

we find that firms with relatively older CEOs have a stronger positive propensity to make PAC

contributions (Model 4 of Table 2). Therefore, while CEO age in absolute terms may not influence

corporate political decisions, CEO age relative to the board impacts such decisions. Using tenure

as a proxy for CEO dominance, we had predicted that firms with longer serving CEOs would be

more likely to contribute to a PAC. Our results show the opposite; CEOs with longer tenures are

significantly less likely to be involved in PAC contributions.6

Overall, our results show mixed evidence that firms with dominant CEOs are more likely

to make firm level political contributions via PACs. However, for firms with entrenched CEOs,

6 The impact of CEO age and tenure may vary over firm performance; older CEOs or those with longer tenures in poorly performing firms may

be more likely to engage in PAC contributions. In order to test the impact of performance and CEO age (tenure), we interact return with CEO age (tenure). We find no significant relation between the interaction variables and the likelihood of making a PAC contribution.

the likelihood of PAC contributions decreases, except in instances where the CEO holds a dual

title, and when the CEO is older relative to the board of directors.

Examining the control variables, we find that firms that are larger, older, and those with a

greater number of directors are significantly more likely to be involved in a PAC contribution,

while firms with lower levels of leverage (total debt ratios) are significantly less likely to make

PAC contributions. We do not find any link between political contributions and lagged return or

market to book ratios. As we had anticipated that the likelihood of PAC contributions could

potentially vary by industry, our estimations include dummies for one-digit industry SIC codes.

We find that firms in SIC code 4, which encompasses transportation, communications, electric,

gas, and sanitary services are significantly more likely to be politically involved, perhaps due to

the regulatory nature of these industries. Thus, it appears that some industries see a significant

advantage to being politically active.

<insert Table 3 about here>

While the results above pertain to the complete sample of participating and non-

participating firms, we next turn to the sample of participating firms alone. As mentioned earlier,

this smaller set comprises of a hand-collected dataset where we match the politicians to firm-level

PAC donations by House (Senate) Committee assignments and by geographical location of the

firm headquarters and the home-state of the recipient politician. Table 3 provides the results for

CEO dominance estimations for value-relevant contributions made by committee assignment and

by location.7 Unlike the results for the full sample, we document a positive relation between the

ratio of inside directors and the percentage of value-relevant contributions made by the firm,

7 We report the results for contributions made to the U.S. House of Representatives members. Results for Senate contributions are available upon request.

measured by the Location variable. While the results for the full sample show that firms with more

inside directors are less likely to participate in a PAC, our results here show that in instances when

such firms do make PAC donations, inside directors appear to see the advantages of making

donations to ‘local’ politicians who may be in the position to impact the firm. However, when

value-relevance is measured by the committee assignment of the recipient politician, we are unable

to find a significant link between CEO dominance, as measured by the ratio of inside directors and

PAC contributions.

We find mixed results for our second model; CEO duality. While we find that for the full

sample, dual CEOs are more likely to contribute, our analysis of the value-relevance of

contributions shows that CEOs holding a dual title of CEO/Chair are significantly less likely to

make contributions to politicians in based on the location proxy. On the other hand, dual CEOs are

marginally more likely to make contributions to politicians holding committee assignments in the

industries in which their firms operate. We do not find any significant impact of CEO age, relative

CEO age (rCEOAGE), or CEO tenure on the value-relevant PAC contribution made by the firms,

measured by either geographical location or by committee assignment. So, in summary, while

overall the relative age of the CEO to the board (rCEOAGE) and CEO tenure does impact firm

decisions regarding whether to contribute to a PAC or not, it does not seem to stem from additional

value perceived to arise from the politician’s geographical location or committee assignments in

the given year. Examining the control variables, it appears that larger firms are significantly less

likely to make value-relevant contributions, regardless of the dominance proxy used in the models.

We also find some evidence that firms with higher debt ratios are less likely to participate in value-

relevant PAC donations. Overall, our results for CEO dominance follow our results for the full

sample, while there are some linkages between value-relevant contributions and our proxies for

CEO dominance, there is no strong evidence pointing to entrenched or dominant CEOs making

higher contributions to politicians who may be in positions to help their firm.

Our next set of estimations presents the impact of interest alignment characteristics on the

likelihood of PAC contributions by the firm. Based on the literature (Farrell, Hersch, and Netter,

2001; Ozer, 2010; Aslan and Grinstein, 2012), we hypothesized that firms having CEOs who are

more aligned with their shareholders are more active through PACs. Table 4 provides the results

of the interest alignment probit estimations, where we model the likelihood of setting up a PAC as

determined by the ratio of CEO holdings, institutional ownership, CEO total compensation, and

CEO variable compensation.

<insert Table 4 here>

Our results suggest that interest alignment, as proxied by CEO holdings, is negatively

related to the likelihood of making political contributions. Thus, our first proxy for interest

alignment refutes our hypothesis that CEOs who are more aligned with shareholders are more

likely to be politically active. Our compensation-based measures of interest alignment, total

compensation and incentive-based variable compensation, are positively related to the probability

of participating in firm’s PAC. Our results are consistent with past studies (Farrell, Hersch, and

Netter, 2001; Ozer, 2010; and Aslan and Grinstein, 2012); we also find that CEOs with higher

amounts of total compensation and variable compensation are significantly more likely to make

political contributions (at the 1% and the 5% levels of significance, respectively). Our findings of

positive link between total pay and the likelihood of having a PAC may reflect both, CEO

dominance and/or better interest alignment. In either case, it suggests that CEOs view political

activities as positive value propositions. We interpret the variable compensation results as

indicating that political engagements are viewed by CEOs as value-adding.

Given the argument that institutional ownership serves as an effective governance

mechanism, we expect that firms with greater institutional ownership are more likely to be

politically active via PACs. However, our results show that institutional ownership is not a

significant determinant of PAC contributions. This may appear to be in contrast with Ozer,

Oneonta, and Ahsan (2010) who note that institutional investors favor firms’ investment decisions

in corporate political strategies. However, these authors also state that the roles institutional owners

play in corporate political strategies differ based on the horizon of these institutional firms making

these decisions.

Our analysis of the control variables shows that larger firms and firms in the SIC code 4

(transportation, communications, electric, gas, and sanitary services) are significantly more likely

to be politically active. We also find that older firms and firms with larger boards are more likely

to make PAC contributions. These results are robust to choice of interest alignment proxy. There

is also evidence that larger firms are more likely to contribute to a PAC.

<insert Table 5 here>

Again, we examine the impact of value-relevant contributions for participating firms and

we next provide the results for the interest alignment variables. We had predicted a positive

relation between the interest alignment proxies and the percentage of value-relevant contributions

made by the firm. A perusal of Table 5 shows that all our CEO interest alignment variables are

highly significant (at the 1% level), as measured by the Location match variable. While our full

sample results show that CEOS with larger holdings are less likely to participate in PACs.

However, for those firms that do participate, we find that the CEO holdings is positively and

significantly related to the percent of value-relevant donations made by the firm. CEOs with larger

equity stakes donate more to local politicians whom they perceive to be in positions to help the

firm. On the other hand, we find the percentage of institutional ownership is negatively related to

the percentage of value-relevant contributions, as measured by location match of the politician

receiving such contributions. It may be that institutional owners are hesitant to allow the firm to

openly court politicians and may serve as a neutralizing agent when it comes to making blatant

political spending decisions. Ozer et al. (2010) find that institutional investors are mostly

concerned about the long-term value of the firm, and to this end, it appears that such owners do

not perceive contributing to local politicians as being of a long-term strategic advantage.

The other variables of total and variable compensation are also significantly negatively

related to the percentage of value-relevant contributions made by the firms. Contrasting these

findings with those for the full sample of participating and non-participating firms, our results

indicate that while CEOs earning higher total and variable compensation are more likely to

participate in PACs, it appears that this does not incentivize them to focus on local (value relevant)

contributions alone. The results are consistent with literature that indicates that political

contributions may be more a management perquisite consumption rather than being value-adding

for the firm. Interestingly, we are unable to document any significant linkages between our other

value-relevant proxy, the committee assignment of the recipient politician, and any of our interest

alignment proxies.

Furthermore, to judge if decisions by the CEO to engage in PAC is agency driven, we must

test if CEO characteristics relate to the decision to engage in a PAC, and to the extent that they do

relate, how PAC participation contributes to performance. Coates (2011) finds that outside of the

regulated industries where there is extensive political lobbying, political activity is associated with

lower firm value. Aslan and Grinstein (2012) note that compensation explained by ‘political

capital’ of executives is associated with an average increase of 0.3% in firms’ operating

performance. Our next set of estimations test for this relationship as defined in our firm

performance hypothesis, and we provide these results in Table 6. In the first step of our

estimations, we quantify the extent to which CEO dominance and interest alignment predict

political contributions. In the second step we relate the predicted contributions to performance.

Thus, we ask if CEOs make value-maximizing decisions for the firm when engaging in political

contributions. Our proxies for performance are contemporaneous firm return, firm ROA, and firm

ROE.

<insert Table 6 about here>

We present the results of our analysis for our first performance variable, contemporaneous return

in Columns 1 and 2 of Table 6, wherein we model total contribution as a function of the CEO

dominance and interest alignment characteristics detailed in the previous estimations. In the first

step, we ascertain whether dominant CEOs and those CEOs whose interests are aligned with those

of the firm are politically active (Column 1, Table 6). We find that the amount of total contribution

is significantly and negatively related to CEO holdings and increases when there are more inside

directors in the firm. Further, we document that firms with higher market value, firms with larger

boards, and more leveraged firms also make larger political contributions.

Having established that strong and less aligned CEOs are politically active, we next

investigate if such CEOs are able to make value-maximizing decisions for the firm. In the second

step of our estimations, we relate the predicted contributions to the measures of corporate

performance (measured by contemporaneous return). Column 2 of Table 6 presents these results.

Our results show that total PAC contributions, to the extent explained by CEO characteristics, are

strongly and positively related to firm performance, as measured by stock returns. Thus, the results

suggest that political engagement via PACs are performance enhancing and are not necessarily

agency driven and detrimental to shareholder interests.

Our second proxy for firm performance is contemporaneous ROA, and we provide the

results of the estimations in Column 3 and 4 of Table 6. We find that the amount of total

contribution is significantly and positively related to CEO total compensation and marginally

increases when there are more inside directors in the firm. Turning to the control variables, we

document that firms with higher market value, firms with larger boards, and more leveraged firms

also make larger political contributions. Once again, we find that firms with higher levels of

political contributions are better performing firms, as measured by their ROAs (Column 4). It

appears that the dominant and/or interest aligned CEOs use political engagement through PAC

contributions to enhance firm performance. Therefore, not only are PAC contributions value-

adding, they may not actually be agency conflict driven. Thus, our results support Cooper, Gulen,

and Ovtchinnikov (2010) who note that public firms that contribute to political campaigns are

significantly correlated with a high rate of return, but do not support those of Coates (2011) who

finds that more politically engaged firms tend to be poorly performing firms. In our third set of

performance estimations, we examine the impact of contributions on firm ROE. We note in

Column 5 that the amount of total contribution is positively and significantly related to both CEO

total compensation and the ratio of inside directors. However, unlike our other performance

variables, we are unable to document a significant relation between ROE and PAC contributions.

With respect to control variables, we document that firm size is negatively related to both firm

return and firm ROA, while sales growth is positively related to firm performance, measured by

both return and ROA.

In our last set of estimations, we examine the same performance variables for our sub-

sample of contributing firms and report these results in Table 7.

<insert Table 7 about here>

Panel A of Table 7 reports the results for the location match. Columns 1 and 2 examine

performance as measured by return. We show that total value-relevant contributions are positively

related to CEO holdings and negatively related to total compensation and firm size in the first stage

estimations. Examining the impact on contemporaneous return (Column 2), we note contributions

to local politicians are very significantly and negatively related to contemporaneous return. Thus,

value-relevant contributions, as defined by our measure in terms of contributions to local

politicians, may not be much value adding.

Turning to our next proxy of performance, ROA, we show that similar to

contemporaneous return, total value-relevant contributions are negatively related to CEO total

compensation and positively related to CEO holdings (Column 3). However, contributions based

on location appear to have no significant impact on firm ROA. One explanation for this could be

that ROA is typically used as a managerial performance measure that may have more to do with

asset efficiency and therefore may be influenced minimally by value relevant contributions based

on location

We turn to our last performance proxy, ROE, in Columns 5 and 6 of Table 7. Once again

we note a positive relation between CEO holdings and the firm’s value-relevant contribution

noting that as CEOs interests are more aligned to the shareholders, value-relevant contributions

increase. These value relevant contributions to local politicians appear to pay off in terms of

accounting returns, as measured by ROE, and we document a very significant and positive relation

between value-relevant contributions and firm ROE in Column 6 in Table 7, Panel A.

Panel B of Table 7 repeats the analysis for our other value-relevant measure, industry

match, based on committee assignments of the politicians. We do not find any significant relation

between value-relevant contributions and performance as measured by contemporaneous return

(Column 2). Thus, while the full-sample results show a positive relation between PAC

contributions and market return, there appears to be no additional value added by donating to

politicians holding industry relevant Committee Assignments. However, when examining

accounting measures, we see a significantly negative relation between firm performance

(measured by ROA and ROE) and value-relevant contributions (Columns 4 and 6). Thus, PAC

contributions based on industry match may in fact be detrimental to value. We also note that

smaller firms made larger value-relevant contributions. As political engagement is more costly for

smaller firms overall, we see that while they made lower contributions overall (Table 6), those

that contributed made significantly more value-relevant contributions based on industry match as

they perhaps more judiciously chose to contribute to those politicians that they perceived as value-

adding. Overall, the performance estimations provide evidence demonstrating a negative relation

between firm performance and value-relevant PAC contributions implying value relevant

contributions did not lead to better performance. Our estimations in Table 7 allow us to examine

the linkages among CEO characteristics, political engagement, and firm performance. Our results

show that value-relevant contributions are not agency driven.

5. CONCLUSIONS

Motivated by studies on corporate governance and agency theory, our study extends the

literature on CEO dominance and corporate strategy by examining CEO characteristics and firm

performance to investigate their impact on strategic choices regarding political engagement by

corporations. Academic research also explores whether corporate political activity, as a non-

market strategy, is value relevant. Therefore, our study uses a unique, hand-collected dataset to

investigate whether firms make value relevant political contributions.

The purpose of our study is two-fold. First we want to investigate the linkages between

CEO characteristics and the likelihood of PAC participation. For the full sample of firms, our

results on CEO characteristics and the likelihood of PAC contributions shows mixed results. We

find that firms with dominant CEOs, as measured by CEO duality, have a greater propensity to

make PAC contributions, while longer tenured CEOs are less likely to contribute. Furthermore,

while CEO age in absolute terms does not influence corporate political decisions, CEO age relative

to the board impacts such decisions. Firms with relatively older CEOs have a stronger propensity

to contribute to PACs. A unique contribution of our paper is that we examine the value-relevance

of firm contributions by matching firm location and industry with the home-state and committee

assignments of the politicians receiving contributions. Overall, our results for CEO dominance

follows that of the full sample results; while there are some linkages between CEO dominance and

value-relevant contributions, there is no strong evidence documenting that dominant CEOs

contribute more to politicians who are in the position to influence the environment in which the

firm operates.

Examining the interest alignment variables for the full sample, we find that our

compensation-based measures of interest alignment are positively linked to the firm participation

in a PAC. Looking at the value-relevance for contributing firms, we find that CEOs with a greater

equity stake in the firm align themselves by making higher contributions to politicians from their

home-state. However, firms with higher institutional ownership tend to donate less to politicians

from the home, perhaps reflecting a reluctance of large investors to openly court politicians.

It is plausible that PAC contributions impact performance. Therefore, the second objective

of our paper is to investigate the relationships between CEO characteristics, political participation,

and firm performance The results for the full sample of firms show that strong CEOs who are

aligned with the firm make value-maximizing decisions for the firm, as proxied by firm return and

firm ROA. We also investigate how firm performance is related to the value-relevance of the

contributions. Overall, our results demonstrate that contributions to local politicians are not value

adding and donations made to politicians who hold Committee assignments in the industry in

which the firm operates do not perform better.

Our results have implications in the CEO dominance and agency-theoretic literature since

we focus on CEO influence on decision making and strategy. Although not unequivocal, our

results - that dominant CEOs and CEOs with better interest alignment are more likely to be

politically active, and that PAC contribution associate positively with firm performance - suggest

that strategic political decisions may not be agency driven and may in fact be value enhancing.

REFERENCES

Adams, R.B., H. Almeida and D. Ferreira (2005), ‘Powerful CEOs and Their Impact on

Corporate Performance’, Review of Financial Studies, Vol. 18, pp. 1403-1432.

Aggarwal, R. K., Meschke, F., and Wang, T. Y. (2012). Corporate political donations: investment or agency?. Business and Politics, 14(1).

Agrawal, A. and C. Knoeber (2001), ‘Do Some Outside Directors Play a Political Role?’, Journal

of Law and Economics, Vol. XLIV, (April), pp. 179-198.

Aslan, H. and Y. Grinstein (2012), ‘Political Contributions and CEO Pay,’ Working paper,

University of Houston.

Barclift, J.Z. (2011), ‘Corporate Governance and CEO Dominance,’ Washburn Law Journal,

Vol. 50, pp. 611-634.

Bebchuk, L.A. and A. Cohen (2005), ‘The Costs of Entrenched Boards’, Journal of Financial

Economics, Vol. 78, pp. 409-33.

Bebchuk, L.A., M. Cremers and U. Peyer (2008), ‘CEO Centrality’, The Harvard John M. Olin

Discussion Paper Series, Discussion Paper No. 601, ISSN 1936-5349 (print), ISSN 1936-5357

(online).

Bebchuk, L.A., M. Cremers and U. Peyer (2011), ‘CEO Pay Slice and Firm Performance’,

Journal of Financial Economics, Vol. 102, Issue 1, (October), pp. 199–221.

Bertrand, M., F. Kramaraz, A. Schoar, and D. Thesmar (2007), ‘Politicians, Firms and the Political Business Cycle: Evidence from France’, Working Paper, University of Chicago.

Bennett, R.W. and C. Loucks (2008) ‘PAC Contributions from Sectors of the Financial Services

Industry - 1998-2002’, Atlantic Economic Journal, Vol. 36, pp. 395-405.

Boubkari, N., J.C. Cosset, and W. Saffar (2012), ‘The Impact of Political Connections on Firms’

Operating Performance and Financing Decisions’, The Journal of Financial Research, Vol .

34(3), pp. 397-423.

Brown, J. R. (2012), ‘Neutralizing the Board of Directors and the Impact on Diversity’,

Available at SSRN: http://ssrn.com/abstract=1938427 or http://dx.doi.org/10.2139/ssrn.1938427

Claessens, S., E. Feijen and L. Laeven (2008), ‘Political Connections and Preferential Access to

Finance: The Role of Campaign Contributions’, Journal of Financial Economics, Vol. 88, Issue

3, (June), pp. 554–580.

Coates, I. V., and John, C. (2012). Corporate politics, governance, and value before and after

Citizens United. Journal of Empirical Legal Studies, 9(4), 657-696.

Coles, J.L., N.D. Daniel and L. Naveen (2008), ‘Boards: Does One Size Fit All?’, Journal

of Financial Economics, Vol. 87, No. 2, pp. 329-356.

Cooper, M., H. Gulen and A.V. Ovtchinnikov (2010), ‘Corporate Political Contributions and

Stock Returns’, The Journal of Finance, Vol. LXV, No. 2, (April), pp. 687-724.

Cull, R. and L.C. Xu (2005), ‘Institutions, Ownership and Finance: The Determinants of Profit

Reinvestment among Chinese firms’, Journal of Financial Economics, Vol. 77, pp. 117–146.

Dahya, J. and N.G. Travlos (2000), ‘Does the One Man Show Pay? Theory and Evidence on the

Dual CEO Revisited’, European Financial Management, Vol. 6, No. 1, 88-98.

Fisman, R. (2001), ‘Estimating the Value of Political Connections’, American Economic

Review, Vol. 91, pp. 1095–1102.

Eisenberg, T., S. Sundgren and M. Wells (1998), ‘Larger Board Size and Decreasing Firm Value

in Small Firms’, Journal of Financial Economics, Vol. 48, No. 1, pp. 35-54.

Engelberg, J., Gao, P., and Parsons, C. A. (2012). The Price of a CEO's Rolodex. Review of

Financial Studies,.

Faccio, M. (2006), ‘Politically Connected Firms’, American Economic Review, Vol. 96, pp.

369–386.

Faccio, M., R.W. Masulis and J.J. McConnell (2006), ‘Political Connections and Corporate

Bailouts’, Journal of Finance, Vol. 61, pp. 2597-635.

Faccio, M., and D.C. Parsley, (2009), ‘Sudden Deaths: Taking Stock of Geographic Ties’,

Journal of Financial and Quantitative Analysis, Vol. 44(03), pp. 683-718.

Faccio, M. (2010), ‘Differences between Politically Connected and Nonconnected Firms: A

Cross-Country Analysis,’ Financial Management (Blackwell Publishing Limited), Vol. 39 Issue

3 (Autumn), pp. 905-928.

Farrell, K.A., P.L. Hersch and J.M. Netter (2001), ‘Executive Compensation and Executive

Contributions to Corporate PACs’, Advances in Financial Economics, Vol. 6., pp. 39-56

Farber, D.B., M.F. Johnson and K.R. Petroni (2007), ‘Congressional Intervention in the Standard

Setting Process: An Analysis of the Stock Option Accounting Reform Act of 2004’, Accounting

Horizons, Vol. 21, pp. 1-22.

Hartzell, J.C. and L.T. Starks (2003), ‘Institutional Investors and Executive Compensation’, The

Journal of Finance, Vol. 58, Issue 6 (December), pp. 2351–2374.

Hermalin, B. E. and M.S. Weisbach (2003), ‘Board of Directors as Endogenously Determined

Institution: A Survey of the Economic Literature’, Federal Reserve Bank of New York Economic

Policy Review, Vol. 9, No. 1, pp. 1-20.

Hersch, P., J.M. Netter and C. Pope (2008), ‘Do Campaign Contributions and Lobbying

Expenditures by Firms Create Political Capital?’, Atlantic Economic Journal, Vol. 36, pp. 395-

405.

Hillman, A.J., G.D. Keim and D. Schuler (2004), ‘Corporate Political Activity: A Review and

Research Agenda’, Journal of Management, Vol. 30, pp. 837

Jensen, M.C. (1993), ‘The Modern Industrial Revolution, Exit, and the Failure of Internal

Control systems’, Journal of Finance, Vol. 48, pp. 831-880.

Johnson, S. and T. Mitton (2003), ‘Cronyism and Capital Controls: Evidence from Malaysia’,

Journal of Financial Economics, Vol. 67, pp. 351–382.

Khurana, R. (2002), ‘Searching for a Corporate Savior: The Irrational Quest for Charismatic

CEOs’, Published by Princeton University Press, (pages 20-21).

Khwaja, A.I. and A. Mian (2005), ‘Do Lenders Favor Politically Connected Firms? Rent

Provision in an Emerging Financial Market’, Quarterly Journal of Economics, Vol. 120,

pp.1391–1411.

Klein, A. (1998), ‘Firm Performance and Board Committee Structure,’ Journal of Law and

Economics, Vol. 41, No. 1, pp. 275-304.

Liebman, B.H. and K.M. Reynolds (2009), ‘The Returns from Rent Seeking: Campaign

Contributions, Firm Subsidies and The Byrd Amendment’, Canadian Journal of Economics,

Revue Canadienne d’Economique, Vol. 39, pp. 1345-69.

Lasfer, M. A. (2006), 'The Interrelationship Between Managerial Ownership and Board

Structure', Journal of Business Finance & Accounting, Vol. 33, (7) & (8) (September/October),

pp. 1006-103

Lord, R. A., and Saito, Y. (2012). Does Compensation Structure Alleviate Personal CEO Risks?.

Journal of Business Finance & Accounting, 39(9‐10), 1272-1297.

Macher, J.T., J.W. Mayo and M. Schiffer (2011), ‘The Influence of Firms on Government’, The

B.E. Journal of Economic Analysis & Policy, Vol 11, Issue 1, pp. 1-25.

Mande, V. and M. Son (2012), ‘CEO Centrality and Meeting or Beating Analysts’ Forecasts’,

Journal of Business Finance and Accounting, Vol. 39, pp 82-112.

Mathur, I. and M. Singh (2011), ‘Corporate Political Strategies’, Accounting and Finance, Vol.

51, pp. 252-277.

Mathur, I., Singh, M., Thompson, F., and Nejadmalayeri, A. (2013). Corporate governance and

lobbying strategies. Journal of Business Research, 66(4), 547-553.

Mobarak, A.M., and D.P. Purbasari, (2006), ‘Corrupt Protection for Sale to Firms: Evidence from

Indonesia’, Unpublished working paper, University of Colorado at Boulder.

Morse, A., V. Nanda and A. Seru (2011), ‘Are Incentive Contracts Rigged by Powerful CEOs?’

The Journal of Finance, Vol. 66, No.5, (October), pp. 1461–1867.

Ozer, M. and S.H. Lee (2009), ‘When Do Firms Prefer Individual Action to Collective Action in

The Pursuit of Corporate Political Strategy? A New Perspective on Industry Concentration’,

Business and Politics, Vol. 11, Issue 1, article 4.

Ozer, M. (2010), ‘Top Management Teams and Corporate Political Activity: Do Top

Management Teams Have Influence on Corporate Political Activity?’, Journal of Business

Research, Vol. 63, Issue 11, pp. 1196-1201.

Ozer, M., E. Alakent and M. Ahsan (2010), ‘Institutional Ownership and Corporate Political

Strategies: Does Heterogeneity of Institutional Owners Matter?’, Strategic Management Review,

Vol. 4(1), pp. 18-29.

Prabhat, S. (2012), ‘Do Political Contributions Enhance, Shareholder Equity Value?’ Indian

School of Business, Working Paper.

Schuler, D., K. Rehbein and R. Cramer (2002), ‘Pursuing Strategic Advantage Through Political

Means: A Multivariate Approach’, Academy of Management Journal, Vol. 45, pp. 659-672.

Yermack, D. (1996), ‘Higher market Valuation of Companies with a Small Board of Directors’,

Journal of Financial Economics, Vol. 40, No. 2, pp. 185-211.

Table1: Descriptive Statistics

This table provides the univariate tests for difference of means for firms making contributions to political action

committees (PACs) and for firms with no PAC contributions.

Variable PAC (mean)

(std. error)

NON PAC (mean)

(std. error)

t stat

(p-value)

Ratio of Inside Directors .137447

(.0023707)

.1715893

(.0036216)

8.1154

(.0000)

CEO Age 55.59153

(.2246658)

54.76706

(.2826332)

-2.3119

(0.0209)

CEO Tenure 6.44

(.2358615)

7.85119

(.3049674)

3.7143

(0.0002)