Central America Regional Competitiveness and Integration...

66

Central America Regional Competitiveness and Integration Interim Report May 27, 2012

Transcript of Central America Regional Competitiveness and Integration...

Central America

Regional Competitiveness and Integration

Interim Report

May 27, 2012

Overview of Study

Country Aquaculture Coffee Tourism

Costa Rica

El Salvador

Guatemala

Honduras

Nicaragua

Panama

Benchmark Vietnam Colombia Costa Rica

Value chain analysis conducted to contribute to The World Bank’s Central America

Competitiveness and Integration Study, which is intended to highlight the role of firm-level

productivity in promoting growth and development.

Eight value chain units (3 sectors across 5 countries) were analyzed to identify factors

contributing to low productivity and high costs in the region.

This presentation accompanies a Main Findings Report containing more detailed analysis

and recommendations.

1

1. Identifies dynamic linkages between production stakeholders and activities, which are key

determinants of competitiveness. The alignment of productive assets is as important as their

quantity/quality. Value chain analysis is particularly effective at identifying coordination failures.

2. Has economic viability and commercial sustainability at its core because of its market

focus. Value chains reflect how economic actors align themselves in response to market

demand.

3. Determines the distribution of value added between activities, both within and between

countries, or a country’s positioning within the global production chain.

4. Examines information flows between economic actors. The quality (content/speed) of

information flows can have a significant impact on the level of innovation and is particularly

important in knowledge–based industries.

5. Segments activities (e.g. production, processing, exporting etc.) allowing for a deeper

understanding of the constraints and opportunities within each segment and by extension the

industry as a whole. Segmentation also allows for the identification of entry points for SMEs

seeking to access regional/global markets.

Value chain analysis allows for more targeted and tailored competitiveness enhancing interventions

More so than country/sector level analysis a value chain approach to competitiveness:

2

Contents

1. Regional overview

2. Aquaculture value-chain

3. Tourism value-chain

4. Coffee value chain

3

Regional Overview

The need to shift the regional integration agenda

1. The rise of global value chains means competitiveness is now increasingly defined by non-

traditional factors such as private standards for market access, transport and logistic costs,

and network interoperability. Productivity, product customization, and time to market are more

important now than ever before.

2. The rise of global value chains has shifted the regional integration agenda from traditional

state-led free trade initiatives to the development of regional public goods such as intra-

regional transportation networks, market intelligence, production technologies and research

and development resources.

3. The development of regional public goods i.e. non-tradables such as infrastructure,

harmonized product standards and customs procedures is particularly important for regions

like Central America where countries share similar export product portfolios.

4. Central America has made significant progress on the traditional regional integration agenda

of lower tariffs and free trade agreements. The average MFN tariff has fallen from 40% to

10% since the 1980s. There are now 42 free trade agreements covering 237 bilateral

relationships representing 89% of intra-LAC trade.

5. The regional integration agenda in Central America has not adequately evolved to help firms

in the region access global value chains and compete effectively against foreign competition.

4

Regional Overview

The Lack of Regional Public Goods

1. Central America not effectively levering its proximity – in both a physical and cultural sense

- to major markets like the United States and the EU. The aquaculture, coffee, and tourism

value chains are weakened by poor market intelligence and trade promotion.

2. Weak end-market linkages lead to a poor understanding of customer needs resulting in

missed product development, value-addition, and branding opportunities.

3. All three value chains are weakened by a lack of research and development, technical

extension services, and poor intraregional transport and logistic networks.

4. International transport linkages could be improved; however the biggest challenges relate

to weak logistics and customs procedures that can cause shipping delays, product loss,

and impede product traceability and certification processes, which are increasingly

important for agribusiness products like coffee and aquaculture.

5. Coordinated efforts between public and private sector required to shift integration agenda

and build competitiveness are lacking.

5

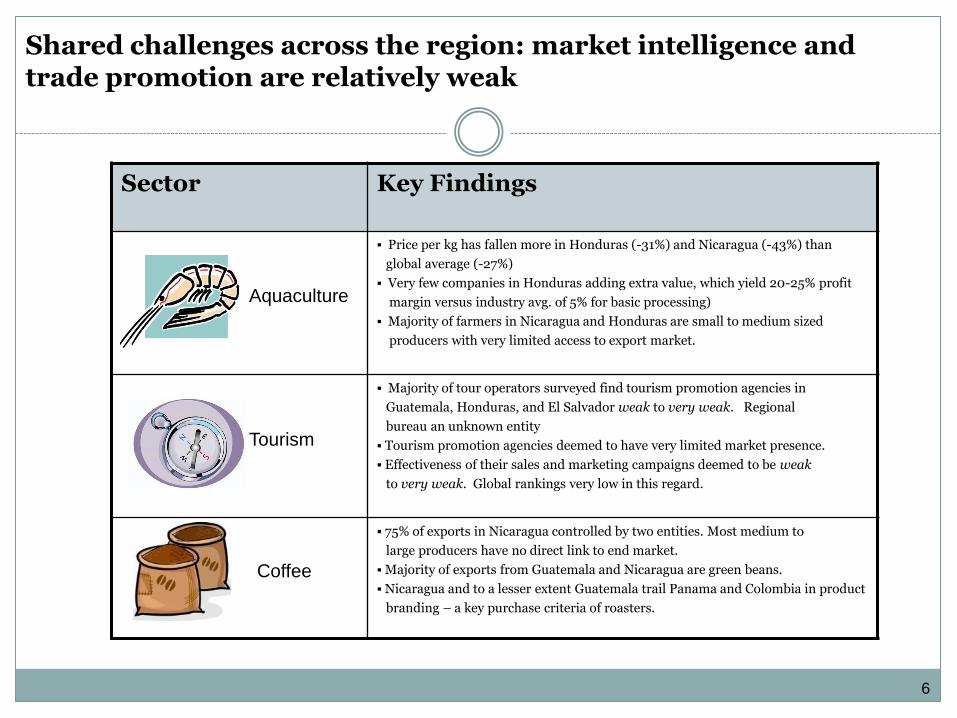

Shared challenges across the region: market intelligence and trade promotion are relatively weak

Sector Key Findings

Price per kg has fallen more in Honduras (-31%) and Nicaragua (-43%) than

global average (-27%)

Very few companies in Honduras adding extra value, which yield 20-25% profit

margin versus industry avg. of 5% for basic processing)

Majority of farmers in Nicaragua and Honduras are small to medium sized

producers with very limited access to export market.

Majority of tour operators surveyed find tourism promotion agencies in

Guatemala, Honduras, and El Salvador weak to very weak. Regional

bureau an unknown entity

Tourism promotion agencies deemed to have very limited market presence.

Effectiveness of their sales and marketing campaigns deemed to be weak

to very weak. Global rankings very low in this regard.

75% of exports in Nicaragua controlled by two entities. Most medium to

large producers have no direct link to end market.

Majority of exports from Guatemala and Nicaragua are green beans.

Nicaragua and to a lesser extent Guatemala trail Panama and Colombia in product

branding – a key purchase criteria of roasters.

Tourism

Aquaculture

Coffee

6

Lack of Regional Public Goods: Low levels of public R&D

Source: Public Agricultural Research in Latin America and the Caribbean, ASTI Report (2009).

Govt. Share of Total Public Ag R&D Spend (1996-2006)

0

5

10

15

20

25

30

35

Cos

ta R

ica

El S

alva

dor

Gua

tem

ala

Hon

dura

s

Nicar

uagu

a

Pan

ama

1991

2001

2006

Total Spend on Ag Research (Millions of 2005 PPP Dollars)

1. Total spend on ag-related R&D

has fallen since 1991 in every

country except Costa Rica and

Nicaragua.

2. Intensity of agricultural R&D

spend in Central America is

amongst the lowest in Latin

America at 0.3% versus 1+% in

Argentina, Brazil, Chile and

Uruguay.

3. Government share of total ag-

related R&D in the region has

generally fallen. Academia and

NGO spend has increased

underscoring their growing

importance.

R&D intensity = total R&D spend divided by total value of sector

7

1996 2006 Change

Argentina 41.7 55.4 33%

Brazil 80.6 81.2 1%

Costa Rica 40.5 39.5 -2%

El Salvador 76 78 3%

Guatemala 81.1 67.8 -16%

Honduras 17.4 14.6 -16%

Nicaruagua 30.7 32.7 7%

Panama 78.4 74.2 -5%

Benchmark

Lack of Regional Public Goods: Poor Intraregional Infrastructure

1. Advantage of geographic proximity to

U.S. market undermined by:

Relatively high cost of national

and intraregional transportation

costs

Lengthy export delays at

outbound transit points

(ports/airports).

2. Region’s exports are particularly

sensitive to transport costs due to

their low value-to-weight ratios and

perishability. It is estimated that if

transport costs were lowered by 10%

the LAC region’s exports might grow

by 30%.

0

5

10

15

20

25

30

Bra

zil

Colo

mbia

Cost

a Rica

El S

alva

dor

Gua

temala

Hond

uras

Nicar

uagua

Pan

ama

USA

Time to Export (Days)

24

18

6

17

13

9

14 13

14

National & Intra-regional Freight Rates

(Nicaragua pt. of origin)

Sources: InterAmerican Development Bank, stakeholder interviews and World Bank Doing Business Report 2012 8

Route Cost% of Intl Freight

Rate to Miami

Chinandega - Corinto $230 38%

Matagalpa - Corinto $760 59%

Segovia - Corinto $960 64%

Jinotega - Corinto $850 62%

Chinandega - P. Limón $1,130 31%

Chinandega - P. Cortes $1,830 51%

Lo

w

Med

ium

H

igh

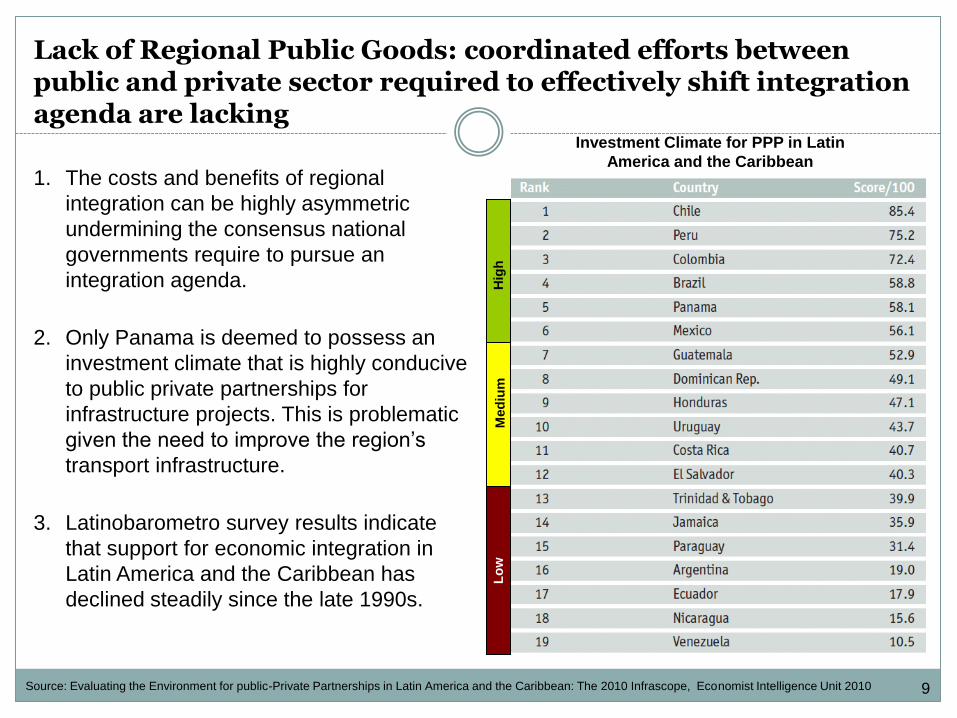

Lack of Regional Public Goods: coordinated efforts between public and private sector required to effectively shift integration agenda are lacking

Investment Climate for PPP in Latin

America and the Caribbean

Source: Evaluating the Environment for public-Private Partnerships in Latin America and the Caribbean: The 2010 Infrascope, Economist Intelligence Unit 2010

1. The costs and benefits of regional

integration can be highly asymmetric

undermining the consensus national

governments require to pursue an

integration agenda.

2. Only Panama is deemed to possess an

investment climate that is highly conducive

to public private partnerships for

infrastructure projects. This is problematic

given the need to improve the region’s

transport infrastructure.

3. Latinobarometro survey results indicate

that support for economic integration in

Latin America and the Caribbean has

declined steadily since the late 1990s.

9

Regional Overview

Overarching recommendations

1. Improve the quantity and quality of regional public goods (RPG). The competitiveness of

aquaculture, coffee, and tourism in the region have been undermined by a lack of R&D,

market intelligence, and trade promotion. All three of these RPGs could be provided more

effectively and efficiently on a regional basis versus country-level institutions and initiatives.

2. Improve security: exporters in the region incur both explicit and hidden security costs. Added

transport and security service fees represent explicit costs; however, actual security costs are

much higher if the cost of lost tour business (region-wide) and early harvesting of crops to

avoid theft (aquaculture in Nicaragua) are also included.

3. Reduce transport and logistics costs. Transport and logistics costs constitute one of the

biggest obstacles to the region’s competitiveness in aquaculture, coffee, and tourism. To

reduce delays and improve the region’s time to market performance port and airport cargo

handling procedures should be streamlined and customs documentation standardized across

countries and modes of transport.

10

Regional Overview

Overarching recommendations

4. Redefine proximity to market: Getting close to the customer in terms of understanding their

product and service needs is more important than geographic proximity. The majority of

shrimp exports are in commodity form and the vast majority of coffee exports are made-up of

green beans with limited specialty coffee designations indicating more value can be captured

by understanding/satisfying end-customer needs.

5. Create a constituency for, and technical capacity to pursue, a regional integration agenda.

The opportunity cost of not pursuing increased regional integration should be made more

explicit. Technical capacity of regional and national institutions to pursue regional integration

in close consultation with the private sector should be improved.

11

Contents

1. Regional overview

2. Aquaculture value-chain

3. Tourism value-chain

4. Coffee value chain

12

Aquaculture Value Chain (White legged shrimp)

Key Findings

1. Both Honduras and Nicaragua are competing in the highly commoditized end of the shrimp

aquaculture industry (i.e. basic processing and packaging). This highly competitive

segment of the market has seen global prices fall by 27% since 1995 – price declines in the

key U.S. market have been even more pronounced at 80.5% since 2000.

2. Honduras and Nicaragua managing declining prices of -- 31% and 43% respectively. Price

drop has placed a premium on production efficiencies. Both countries trail Vietnam on key

performance benchmarks: yields and feed conversion ratios.

3. Industry in Honduras and to a lesser extent Nicaragua is dominated by a small number of

vertically integrated firms. Smaller producers have little access to global value chains due

to lack of technical support and market intelligence. Linkages between larger and smaller

players are effectively non-existent.

13 Note: basic processing entails de-heading, de-veining, and tail-off. Shrimp are then individually quick frozen (IQF).

Global Overview: significant increases in production from Asia has seen global prices fall dramatically

0

1000000

2000000

3000000

4000000

5000000

6000000

7000000

0

5000000

10000000

15000000

20000000

25000000

30000000 0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

199

5

199

6

199

7

199

8

199

9

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

27% Decrease in Avg. Global Prices $/kg 530% Increase in Volume (T)

389% Increase in $(000) Value

Source: FAO Global Stats

The [US market] prices trend has been decreasing with an average drop of 80.5% between 2000 and 2010, from US$11.82 to 6.55 per kilo, primarily due to strong competition from Asian countries such as Thailand, Indonesia, China, and Vietnam, which sell 65% of the shrimp imported into the United States. FIINPESCA-FAO/OSPESCA/SWEDEN Project. Marketing study for lobster and shrimp fisheries in Central America and viability to establish a regional certification. 2009.

14

Global Vietnam Honduras Nicaragua

%Change

in

$/kg Value

1995-2010

-27% -28% -31% -43%

Regional Overview: while Honduras is losing market share and Nicaragua is gaining market share, unit prices in both countries are declining faster than the global rate

Global Vietnam

Vietnam

Market

Share

Honduras Honduras

Market

Share Nicaragua

Nicaragua

Market

Share % Change

in Tons

Produced

1995-2010

531% 680% +28% 263% -29% 735% +38%

% Change

in $ Value

1995-2010 389% 492% +27% 263% -32% 422% +8%

Source: FAO Global Stats 15

Honduras Nicaragua

% GDP 2% 1.3%

Employment (Direct and Indirect)

30,000 25,000

% Exports 4.4% 4.5%

%Ha Cultivated by Large Producers

70 73

%Ha Cultivated by Other Producers

30 27

44%

14%

12%

11%

10%

8%

1%

Share of Shrimp Production in Central America 2000-07

Honduras

Nicaragua

Belize

Guatemala

Panama

Costa Rica

El Salvador

Source: FAO FIPM 2011, Case Interviews, ANDAH

Regional Overview: shrimp aquaculture is an important sector in Honduras and Nicaragua but the industry is dominated by fewer than 10 companies

16

Inter- mediaries

Med. Farms

Local/Region. Market

Consumers

Processing Plant

Import Broker

Client

Consumers

Processing Plant

Client

Processing Plant

Larva Lab

Small Farms

Suppliers of Primary Materials

Raw Inputs Production Processing Export/ Import

Marketing Processing Retail

Large Farm

Ice Plant

Suppliers of Financing

The vast majority of producers are small and medium in size and lack technical knowledge, access to financing, and access to export markets.

The value chain is dominated by large, vertically-integrated, export-oriented firms. They control their own in-country ice plants, larva and R&D labs, farms, processing plants, and export operations.

Regional Overview: industry is bifurcated between globally competitive large vertically integrated firms and hundreds of smaller players with little market access

In Honduras SENASA and ANDAH support the value chain for large firms

17

Ref: Based on stakeholder interviews (Honduras, April 2012)

$/l

b

Honduras: despite dominating the sector, large integrated companies only capture 25% of the value of frozen, commodity-grade white leg shrimp tails produced, processed, and exported

18

Ref: Based on stakeholder interviews with Large Producers (Honduras, April 2012). Note: Basic processing includes de-heading & de-veining. “Value-add processing” includes spicing, breading, skewering.

A more promising model: margins jump significantly when value added goes beyond standard de-heading and de-veining of shrimp

$

/lb

Processing for Export:

includes de-heading,

de-veining, and instant

quick freeze (IQF)

Value-add Processing:

includes the above

plus activities such as

spicing, breading, pre-

cooking, and

skewering.

Basic to higher

margin processing

19

Ref: Based on stakeholder interview with producers (Honduras, April 2012 ), Vietnam figures from World Bank

HONDURAS Small Producer

Farm Gate Price: $0.95/pound Small Producer

Production Cost: $0.77/pound

HONDURAS Large Producer

Production Cost: $1.10/pound

(Integrated producer)

VIETNAM Medium Producer Farm Gate Price:

$1.73/pound Medium Producer Production Cost: $1.38/pound

Honduras: technical assistance and economies of scale could lower key input costs, especially for feed, which is 36% of production costs for large producers and 65% for small ones

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

65%

36%

Margin Margin

20

33%

20% 18%

7%

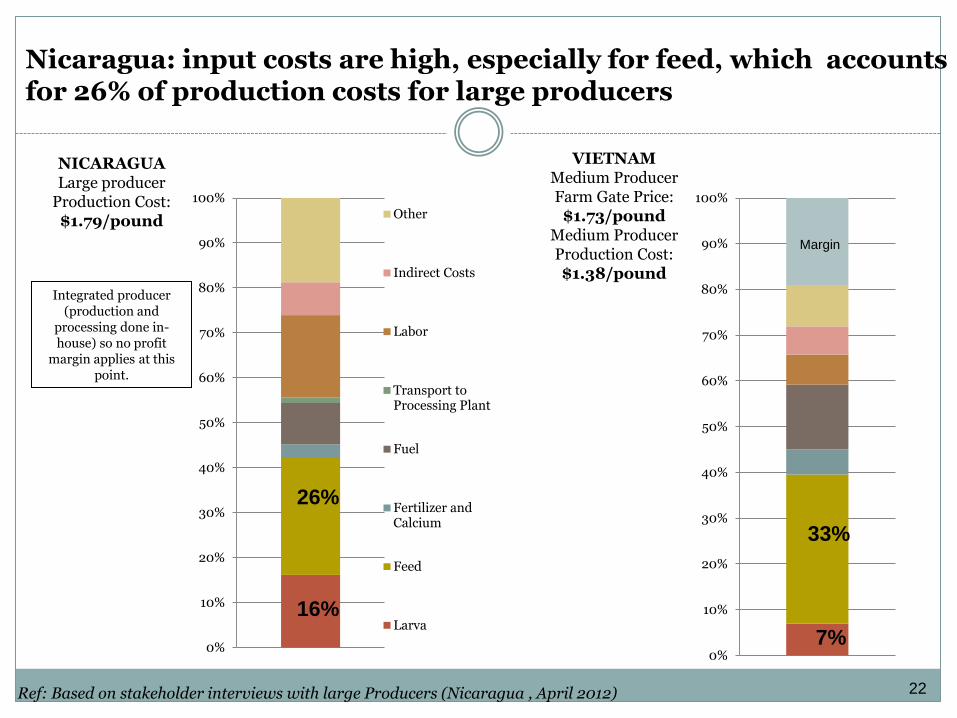

Ref: Based on stakeholder interviews with large Producers (Nicaragua , April 2012)

Nicaragua: despite dominating the sector, large integrated producers capture only 30% of retail value

21

NICARAGUA Large producer

Production Cost: $1.79/pound

VIETNAM Medium Producer Farm Gate Price:

$1.73/pound Medium Producer Production Cost: $1.38/pound

Nicaragua: input costs are high, especially for feed, which accounts for 26% of production costs for large producers

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Other

Indirect Costs

Labor

Transport to Processing Plant

Fuel

Fertilizer and Calcium

Feed

Larva

26%

Ref: Based on stakeholder interviews with large Producers (Nicaragua , April 2012)

Margin

22

Integrated producer (production and

processing done in-house) so no profit

margin applies at this point.

33%

16%

7%

Sh

rim

p F

arm

ers

80% small & medium farmers. Mostly intensive farming. Avg. yield/ ha: 11.7T

564 seafood processing plants. 10% YoY added capacity since 2002

Strong links between agents and farmers. Agents often provide credit and info., purchase shrimp onsite, store and ensure quality standards before transport to processing plant

Ag

ents

/Wh

ole

sale

rs

70% Vol.

30% Vol. Pro

cess

ors

/Ex

po

rter

Diversified international export markets

Japan: 30.6%

USA: 24.3%

EU: 17.1%

Other: 28%

International Markets

Local Markets: Less than 1%

Larva

Feed & Misc.

Inputs

70% of larva imported from China. Rest of input needs met in-country

Ref: WB, FAO, NACA, IDH

Vietnam Intl Benchmark: value chain is highly integrated with wholesalers providing producers with credit, production technologies, market information, and transportation services

23

Ref: Based on NACA, Shrimp Price Study Phase 3

Global commodity: per pound prices for Vietnamese white leg shrimp are comparable to those of Honduran and Nicaragua

24

Benchmarking: Honduras and Nicaragua lag Vietnam in key productivity measures

Yields Feed Conversion

Ratios

Vietnam 11.7T/ha 1.2 : 1

Central America (Small producers)

2T/ha 2 : 1

Central America

(Large producers)

0.5T/ha 1.5 : 1

Feed conversion ratios are the key determinant in a producer’s ability to

economically grow larger shrimp, which carry a premium on the market.

The larger the shrimp the lower # per lb and higher the $ per lb

U.S. Wholesale Price ($/lb) for Farm Raised White Legged Shrimp (Sept 2011)

Count

per lb

25

Typical size from

Central America.

Recommendations for Aquaculture in Honduras and Nicaragua

1. The government in Honduras and Nicaragua needs to develop a long-term national growth strategy for aquaculture that supports large, medium, and small-scale producers. The private sector should play an active role in the strategy development process via a public private dialogue.

2. The government should develop new production models for small-scale producers. Pilots programs should be undertaken to identify viable models that can be scaled-up nationally. New production models should be comprehensive in nature taking into account financial, logistical, and commercial aspects to ensure the model is self-sustaining.

3. Improve market intelligence to identify distributer and buyer relationships, such as Marks and Spencer, where local firms can secure higher profit margins through the sale of higher value-added products.

4. Deepen research and development efforts to improve feed conversation ratios and yields. Extension services should be strengthened to support commercial up-take of new production technologies.

5. The activities of the newly formed Aquaculture Network of the Americas (RAA) should be expanded to include market intelligence and trade promotion. Current activities in the area of technology transfer should also be deepened.

26

Contents

1. Regional overview

2. Aquaculture value-chain

3. Tourism value-chain

4. Coffee value chain

27

Tourism Value Chain Key Findings

1. The tourism sector is an important source of employment and export revenues in Central America. Applying a multiplier of 2.5: the sector accounts for 10.6% of the region’s GDP and 8.9% of employment – both higher figures than the global average.

2. Tourism promotion agencies in El Salvador, Guatemala, and Honduras are deemed to be relatively ineffective. Absence of information and promotional materials cited as impeding sales efforts in the United States. Regional tourism body is an unknown entity.

3. 60% of respondents expressed interest to strong degree of interest in a regional tour packages. 50% of respondents believe intra-regional travel logistics is the biggest obstacle to a regional tour offering.

4. All three countries deemed to be weak in key product performance areas: safety and security, quality of attractions, quality of accommodations, and quality of local tour operators. Security is the most frequently cited concern.

5. Locally, there is a relatively low appreciation for the importance/benefits of the tourism sector.

Sources: 1Tour Operators Initiative for Sustainable Tourism Development, 2003; 2Fletcher Project Team Tour Operator Survey 2012 28

Global Overview: the tourism industry is a large and growing part of the global economy

Sources: 1Word Bank Yearbook of Tourism Statistics, as of 4/17/12 2WTTC, “World Economic Impact: 2012;” 2CAVC Report

Global Economic Impact of

Tourism (2011)2

2.8 3.3 4.9 5.3

0246

GDP

Emplo

y...

Inve

stm

ent

Exports

Perc

enta

ge

2.8 3.3

9.1 8.7

0

5

10

GDP Employment

Direct

IndirectPe

rcen

tage

Multiplier Effect of Tourism (2011)2

• Directly created 98+ million jobs in 20111

• Multiplier effect of tourism is estimated between 2.3 - 2.52

Global tourism receipts (1995-2010)1

0

200

400

600

800

1000

1200

1995 2000 2005 2010

World

Bill

ion

s in

US$

29

Global Overview: tourism is a highly complex and competitive industry made-up of numerous customer segments

Boating

Relaxation Golf

Beach

Snorkeling

Scuba Diving

Surfing

Wind Surfing

Adventure

Nature

Agricultural

Zero Carbon

Protected

Rural

Community

Archeological

Religious

Language

Cruise

Excursion 3

Excursion 2

Excursion 1

Eco

Cultural

Sea Kayaking

30

Regional Overview: tourism plays an especially important role in the Central American economy

9.2 8 9.2 4.8

10.68.9

7.1

11.6

02468

101214

GDP

Emplo

ymen

t

Inves

tment

Exports

Global Central America

Economic Impact of the Tourism Industry (2011)1*

Sources: 1Word Bank Yearbook of Tourism Statistics, as of 4/17/12; 2WTTC, “World Economic Impact: 2012,” *Percentages represent combined direct and indirect impacts, include Belize

Tourism Receipts for Central America (1995-2010)1

Perc

enta

ge

# o

f Jo

bs

(in

th

ou

san

ds)

Mill

ion

s U

S$

0

500

1000

1500

2000

2500

3000

1995 2000 2005 2010

Costa Rica

El Salvador

Guatemala

Honduras

Nicaragua

Panama

Job Creation (2010)

31

Regional Overview: growth rates have leveled off. Per the WEF 5 of 6 countries in the region have lost competitiveness

WEF Tourism Competitiveness Rankings (out of 139)

2003-2008 2008-2010

Costa Rica 12.6% -5.0%

El Salvador 18.6% -16.0%

Guatemala 16.3% 3.9%

Honduras 11.3% 2.4%

Nicaruagua 12.7% 1.0%

Panama 22.6% 7.3%

CAGR Visitor Expenditures

Source: SITCA. Does not include revenues from daytime visits (e.g. cruise ships) and World Economic Forum 2011 Tourism Competitiveness Report

2011 2009 Change

Costa Rica 44 42 -2

El Salvador 96 94 -2

Guatemala 86 70 -16

Honduras 88 83 -5

Nicaruagua 100 103 3

Panama 56 55 -1

32

End Market Analysis: Overview of CAVC Tourism Channel Survey

1. Objective: Identify strengths and weaknesses within the Central America tourism value chain. Focus: El Salvador, Guatemala, and Honduras with Costa Rica as the international benchmark

2. Target Respondents:

United States and Canadian based outbound tour operators

Outbound tour operators account for 12% of intl. arrivals to the region*

Survey conducted April 2012

3. 27 Respondents included

Representative of the Virtuoso Consortium, comprising over 330 agencies with more than 7,200 elite travel providers

Representative of Latour, a leading expert in travel to Central America, featuring multi-destination tours

Representatives of the United States Tour Operators Association

*Source: Tour Operators Initiative for Sustainable Tourism Development, 2003

Survey results not statistically significant but directionally very clear

33

Car Rental

Accommodations Resorts, Int’l Hotels, Rental, Boutique Hotels, Camping

Travel Agencies

. . Internet, Guidebooks,

Travel Media

. Activities and Attractions Cultural Eco Beach

Key Public Sector Support Institutions

Tourism Boards, Ministries of Tourism,

Police

Key Private Sector Support Institutions

Tourism Chambers & Associations, Banks,

NGOs, Universities, Trainers, Property

Developers

Cultural Eco Beach

End Markets North America, Europe, Latin America

International Transport

Selection and Booking

Planning Word of Mouth /

Social Networking Travel Agencies / Tour Operators

Internet Booking

Inbound Tour Operators

Direct Booking

Self Drive Cruise Lines International Airlines

Domestic Transport

Tour Bus Domestic

Flights

Value-forming Organizations

International Bus Lines

BEC Product & Service

Providers

Local Guides & Key Operational Staff

Handicraft Producers

Restaurants

Tour Operators

SME Suppliers

Entertainment

Taxi/Car Service

. .

. . .

.

. . . . . . . . .

. . .

. .

. . . .

. .

.

Sources: CAVC Report

Channel survey highlighted weak end market linkages

Survey

results

indicate

linkages to

end market

are weak.

34

Question: Based on your experience, how effective are the tourism promotion agencies of the following? Where 1=not at all effective and 7=highly effective.

Eff

ecti

ve

In

effe

ctiv

e

10 respondents did not know 12 respondents

did not know.

N=25

Survey Results: trade promotion agencies are relatively weak compared to Costa Rica

Source: Fletcher Tour Operator Survey April 2012 35

Survey Results: lack of market intelligence results in ineffective marketing, sales, and branding efforts

Source: Fletcher Tour Operator Survey April 2012 and World Economic Forum 2011 Tourism Competitiveness Report

Costa Rica

Honduras

Guatemala

El Salvador

Effective Ineffective

Costa Rica (14)

UAE (1)

Honduras (66)

El Salvador (69)

Guatemala (105)

Venezuela (139)

Effectiveness of Marketing and Branding (WEF Rank)

Inef

fect

ive

Ef

fect

ive

36

Question: How integrated (i.e. coordinated) are the local service providers in the following countries? Where 1=not at all integrated and 7=highly integrated

5.96

3.59 4

3.62

0

1

2

3

4

5

6

7

Costa Rica El Salvador Guatemala Honduras

N=25

Inte

gra

ted

N

ot

inte

gra

ted

Survey Results: lack of integration amongst local services providers highlights coordination failures

Source: Fletcher Tour Operator Survey April 2012 37

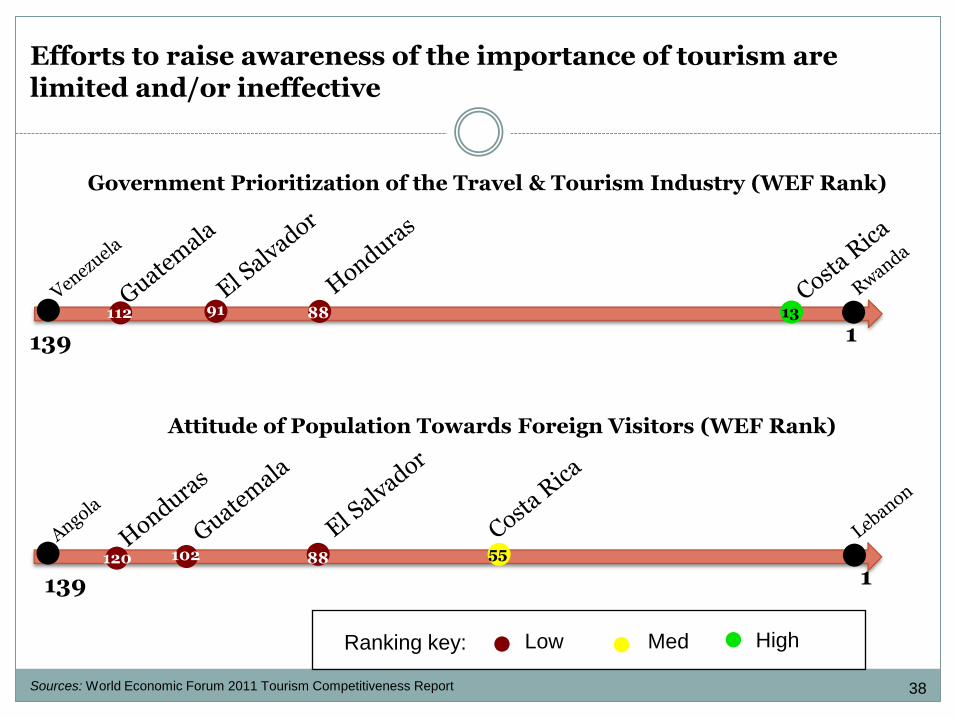

Efforts to raise awareness of the importance of tourism are limited and/or ineffective

Government Prioritization of the Travel & Tourism Industry (WEF Rank)

Sources: World Economic Forum 2011 Tourism Competitiveness Report

1 139

112 91

88 13

Attitude of Population Towards Foreign Visitors (WEF Rank)

1 139

120

102

88

55

High Med Low Ranking key:

38

Survey Results: How interested are you in offering a multi-country tour package to Central America?

7%

33%

27%

13%

20% 1 - Not at all interested

2

3

4 - Neither disinterested nor interested

5

6

7 - Very interested

Comments from U.S. tour operators (N=15): Would love to operate multi country tour packages such as Panama & Costa Rica, Costa Rica &

Nicaragua, Guatemala & Honduras Haven't thought about it previously, but don't see why this wouldn't be feasible. I'm not sure of the Air connections but this is primary is combining destinations. Generally

multi-country tours sell well, but we haven't been able to do this in Central America in the past. We do lots of combo tours to Europe, it'd be great to offer that in Central America. Would be willing if I had clients that requested it The need for this only occurs if a client wants it. Usually time and money limit to one country Ease of organization will influence our decision.

60% interested to very

interested.

Source: Fletcher Tour Operator Survey April 2012 39

Question: What do you see as the biggest obstacle to a multi-country tour package to

Central America?

Comments from U.S. tour operators:

Lack of frequency and convenience of flights to/from major tourism areas, lack of infrastructure (roads, hotels, restaurants going to or at major tourism areas, lack of support from local companies, monopolies are making the product too expensive

27.3%

4.5% 50.0%

4.5%

4.5% 9.1%

Lack of market demand

Lack of support from local partners

Logistics of inter-regional travel too difficult No promotional support

Too expensive

No significant challenges

N=22

Source: Fletcher Tour Operator Survey April 2012

Survey Results: poor intra-regional transport links seen as biggest obstacle to regional tourism

Logistics of intra-regional travel too difficult

40

Question 2: How important are the following factors in your decision to offer a tour package to a particular destination? Where 1=not at all important and 7=very important

5.77 6.6 6.32

4.92

5.92 5.28 5.48

5.92 6

4.24

0

1

2

3

4

5

6

7

N=26

= Most important

Source: Fletcher Tour Operator Survey April 2012

Security is the number one factor when offering a tour package

41

Question 10: How does each country perform in the following five areas? Where 1=very weak and 7=very strong

6.45

5.95 6.09 6.29

5.77

3.3 3.05

3.65 3.53

2.43 4.81

3.26 3.9 3.83

2.79

3.55 3.21 3.32

3.11

2.21

0

1

2

3

4

5

6

7

Quality of attractions

Safety and security Quality of accommodations

Quality of local tour operators

Effectiveness of marketing and sales

campaign

Costa Rica

El Salvador

Guatemala

Honduras

N=22

Str

on

g

Wea

k

El Salvador, Guatemala, Honduras deemed to be relatively weak in key performance areas compared to the regional leader Costa Rica

Source: Fletcher Tour Operator Survey April 2012 42

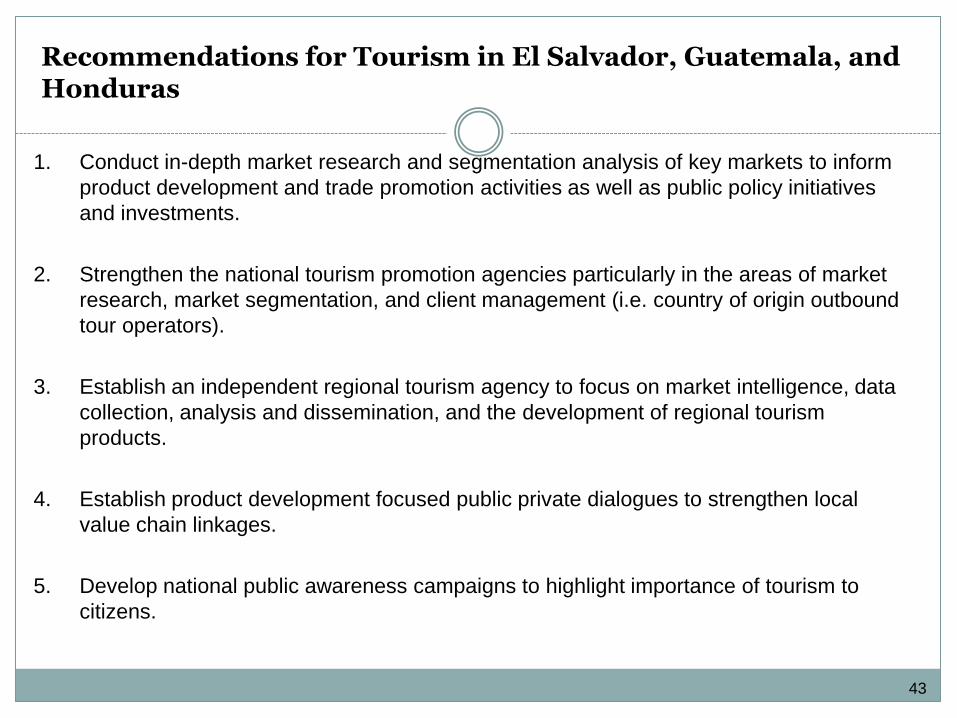

Recommendations for Tourism in El Salvador, Guatemala, and Honduras

1. Conduct in-depth market research and segmentation analysis of key markets to inform

product development and trade promotion activities as well as public policy initiatives

and investments.

2. Strengthen the national tourism promotion agencies particularly in the areas of market

research, market segmentation, and client management (i.e. country of origin outbound

tour operators).

3. Establish an independent regional tourism agency to focus on market intelligence, data

collection, analysis and dissemination, and the development of regional tourism

products.

4. Establish product development focused public private dialogues to strengthen local

value chain linkages.

5. Develop national public awareness campaigns to highlight importance of tourism to

citizens.

43

Contents

1. Regional overview

2. Aquaculture value-chain

3. Tourism value-chain

4. Coffee value chain

44

Coffee Value Chain

Key Findings

1. Quality and yield are variable due to lack of adequate technical assistance and access to financing.

2. The competitive environments result in limited value addition. Guatemala: Small producers capture little value added because they often sell only cherry coffee. Nicaragua: Medium/large producers must work with two main exporters.

3. Competitiveness suffers due to inadequate infrastructure and export procedures. Export costs for Guatemala and Nicaragua are higher than competitor’s (Colombia).

4. Weak institutional support constrains productivity, promotion, and market linkages.

Guatemala: Anacafé lacks scaled-up technical assistance to small producers

Nicaragua: CONACAFÉ lags in external promotion and technical assistance due to financial constraints

5. End markets recognize the region’s quality but marketing and branding is poor.

End-market demand for information is not met (coffee cup profiles, origin, quantities, logistics).

Nicaragua: Lacking nation and region branding inhibits market growth.

45

Global Overview: industry is experiencing strong growth particularly in the specialty coffee segment

Two main varieties:

• Arabica (higher-quality)

• Robusta

Market prices fluctuate, often

dramatically

Production is cyclical but global output

increased 42% from 1990 to 2012

Rapid growth in high-quality, specialty

coffee

80,000

90,000

100,000

110,000

120,000

130,000

140,000

World Output (000 bags)

0

50

100

150

200

250

300

1990 1995 2000 2005 2010

Historical Coffee Prices – NY (USc/lb)

42% increase

Ref: International Coffee Organization 46

Global Overview: strong growth in specialty coffee is driven by end-market roasters’ desire for quality and differentiation

Overall volume growth is driven by Brazil, China, and developed markets

Specialty coffee growth is driven by US and EU

Specialty roasters increasingly demand quality and differentiation

Traceability and upstream information are key to specialty segment

0

2

4

6

8

10

12

14

16

18

20

2001 2008 2012 (projected)

US Sales of Specialty Coffee ($ billion)

Ref: Bolton, Dan. Coffee Industry Shifts Under Tough Economy. Specialty Retailing. August 2009. 47

Regional Overview: Coffee is critical to the region’s GDP and exports

Ref: International Coffee Organization, National Coffee Association (Anacafé) of Guatemala

Share of GDP (2010)

Costa Rica 4.4%

El Salvador 1.7%

Guatemala 0.9%

Honduras 5.4%

Nicaragua 2%

Panama 0.84%

Note: Panama is excluded from the above because coffee is under 1% of its export earnings.

48

Regional Overview: prices for Central American coffee are keeping up with world market trends but output increases vary within the region

0

10

20

30

40

50

60

70

80

0

200

400

600

800

1000

1200

1400

1600

1800

2000 Nicaragua

Output (000 bags)

Prices (USc/lbs)

Linear (Output (000 bags))

0

50

100

150

200

250

3000

3200

3400

3600

3800

4000

4200

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

Guatemala

Output (000 bags)

Prices (USc/lbs)

Linear (Output (000 bags))

Output and Avg. Price to Growers

0

50

100

150

200

250

US

D/

100

lb

s

Prices to Growers

Colombia

Guatemala

Nicaragua

Avg. C.A.

Ref: International Coffee Organization 49

Regional Overview: Central America is keeping up with market prices but is not capturing the specialty market’s growth

Central America has a long history, recognized quality, and is well-positioned in the market and geographically

Share of world output is relatively flat or declining

The region is not capturing the tremendous growth in world specialty markets

Ref: International Coffee Organization 50

Quality and yield are variable due to lack of adequate technical assistance and access to financing

Inadequate technical assistance and access to financing constrain producers’ ability to:

Increase yield and produce consistent quality;

Reduce vulnerability to climate change, which makes yields volatile;

Increase mechanization where possible, reducing vulnerability to future labor

shortages;

Increase investment in infrastructure and replacement of aging coffee trees.

Interest rates vary between large and small producers

Large Producer Small Producer

Guatemala 6-14% 14-18%

Nicaragua 13% 7%

Smaller producers secure

lower interest rates due to strength of

cooperatives

51

The competitive environment in Nicaragua results in medium and large producers being held captive by two main exporters

1. Small producers work through cooperatives

to access international markets, technical

assistance, and financing

2. Two exporters in Nicaragua control 75% of

all exports. The lack of competition in this

segment of the value chain can constrain

the flow of market information and impede

innovation.

52

National Nicaraguan Coffee Association (CONACAFE)

Small producers

(1- 10 Mzn) N=22,500

Medium producers

(10-50 mzn)

N=14,900

Large producers (50+ mzn) N=6,000

Cooperatives N=4000

Wet Mill

Wet Mill

Exporters / Intermediary (Cisa & Atlantic ≈ 75% market share)

N=65

Importers Importers Importers

Roasters Roasters Roasters

US Europe East Asia

Harvest

Retail

Exporting

Importing/ Trading

Dry Mill

Wet Mill

Roasting

Roasting

Production

Inputs

Promotion

Research & Education

National roasters

Packaging

Retail

Nicaragua

Dry Mill

Commercial-grade coffee (lower quality)

53

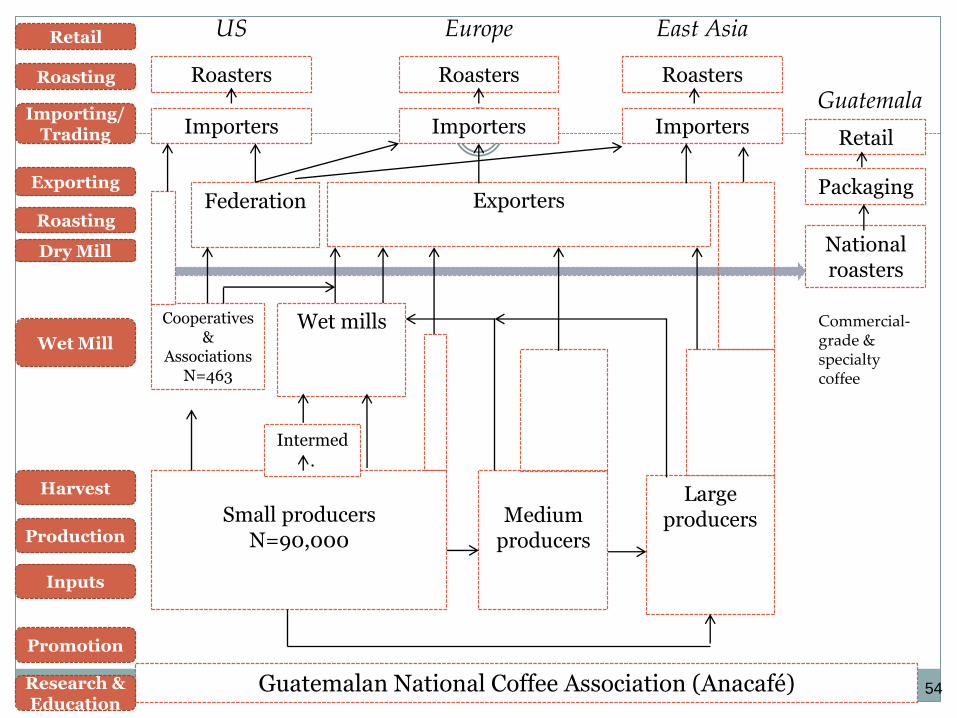

Guatemalan National Coffee Association (Anacafé)

Small producers

N=90,000

Medium

producers

Large producers

Cooperatives &

Associations N=463

Wet mills

Intermed.

Exporters

Importers Importers Importers

Roasters Roasters Roasters

US Europe East Asia

Federation

Harvest

Retail

Exporting

Importing/ Trading

Dry Mill

Wet Mill

Roasting

Roasting

Production

Inputs

Promotion

Research & Education

National roasters

Packaging

Retail

Guatemala

Commercial-grade & specialty coffee

54

45%

64%

19%

16%

6%

3%

14%

5%

17% 12%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Nicaragua Guatemala

Other Costs

Financial Services

Repair & Maintenance

Fertilizers

Labor

Fertilizer is the 2nd biggest on-farm expense

Future labor shortages

could increase labor costs

In Guatemala theft, not incl. security personnel costs, can account for

up to 8% of production costs.

Cost Breakdown for Producers in Nicaragua and Guatemala

Producers’ ability to benefit from value added is affected by theft, fertilizer prices, and labor costs

Social security tax on seasonal labor and mandatory benefits

for full-time staff increase labor costs

55

The competitive environment in Nicaragua results in high value addition for small producers

Guatemala receives higher market prices ($250) than Nicaragua ($218) but Nicaragua’s small producers capture more value

In Nicaragua, small producers are usually organized and sell processed “parchment coffee”

FOB $/100lbs (green coffee)

Guatemala $250

Nicaragua $218

Parchment Green Roasted Parchment Green Roasted

$150.93 $18.00 $7.00 $10.00 $30.00

$784.07

NICARAGUA VALUE ADDED coffee sells at $1,000/100lbs

(Large Producer)

$154.28 $29.40 $7.00 $27.59 $30.00

$751.73

NICARAGUA VALUE ADDED coffee sells at 1,000/100 lbs

(Small Producer)

56

The competitive environment in Guatemala results in limited value addition for small producers

Guatemala receives higher market prices ($250) than Nicaragua ($218) but Guatemala’s small producers capture less value

In Guatemala, small producers are usually not organized and sell unprocessed “cherry coffee”

$35 $3

$117 $95

$30

$720

$-

$200

$400

$600

$800

$1,000

Guatemala value added when roasted coffee sells at $1,000/100lbs (If Producer Sells Cherry Coffee)

FOB $/100lbs (green coffee)

Guatemala $250

Nicaragua $218

$720

$155

$95 $30

0

100

200

300

400

500

600

700

800

900

1000

Guatemala value added when roasted coffee sells at

$1,000/100lbs (If Producer Sells Parchment Coffee)

Cherry Parchment Green Roasted Parchment Green Roasted

57

In Nicaragua, both large and small producers sell value-added parchment

coffee

Large producers have their own wet mills, and small producers use wet mills

belonging to cooperative

Small producers in Nicaragua benefit from a strong cooperative system through which they can access value-added wet mills

$150.93

$18.00 $7.00 $10.00 $30.00

$777.07

Nicaragua value added when roasted coffee sells at $1,000/100lbs

Completed by one entity

58

YIELD: quintales of parchment coffee per manzana ( QQ/manzana = 100lb/0.7 hectare)

Nicaragua Guatemala Panama Colombia

Small Producer

25 QQ 16QQ n/a 25 QQ

Large Producer

34 QQ 20QQ 45 QQ 40 QQ

Benchmarking: Yields

59

Snapshot: Nicaragua Import/Export fees (per TEU) are relatively costly

Procedures Costs

Import taxes and fees $200.00

Phytosanitary import permits and certificates $100.00

Customs duties $5.00

Inspection - container movement fee (per inspection)*

$16.50

Inspection - agent fees (per inspection)* $35.00

Warehousing ($33/day after first 10 days)

Total minimum cost $356.50

*NOTE: Inspection can be conducted by either/both Magfor and/or Customs.

Procedures Costs

Phytosanitary export permits and certificates

$50.00

Entering export documents into CETREX

$25.00

Taxes (1% of FOB)

Customs

$70.00

Total minimum cost

$145.00

Imports Exports

61

Poor institutional support constrains productivity, external promotion, and market linkages

Guatemala’s Anacafé lacks scaled-

up technical assistance to small

producers. Incentivized to support

export ready producers to maximize

funding levels.

Nicaragua’s CONACAFÉ lags in

external promotion efforts and

technical assistance. Funding levels

are relatively low.

Anacafé receives 1% of all export

revenues by law

CONACAFÉ receives $0.10/100lbs

exported, regardless of export price

Lack of institutional support Differing funding mechanisms

62

Assuming an export price of $2.50 per pound:

• Anacafé earns USD $2.50 per 100lbs exported

• CONACAFÉ earns $0.10 per 100lbs exported.

End markets recognize Central American coffee’s quality but marketing and branding is largely inadequate

End-market demand for origin information is increasing

Consumer and roaster are increasingly preferring more direct connection to farmers

Guatemala’s Anacafé rivals Colombia’s famous export promotion efforts but other countries lag behind

“I wish that there was a better chain of

information from the areas of origin that I am interested in, or even areas that I’m not.”

(Boutique roaster in California)

“I love to try new things, but because I am not familiar with Nicaragua as

a single origin, I must go out and educate myself, and it is time-

consuming.” (U.S.-based roaster)

“The more communication that goes on between farmers and exporters or

coffee buyers, the better. The value that I see in what I bring as a coffee

buyer is that I am ensuring producers that for as long as their coffee is of a

certain quality, I am going to buy it… Having an assured buyer every year

motivates them to produce good-quality coffee.” (Roaster in New York)

63

Recommendations for coffee in Central America

1. Strengthen end-market linkages via greater emphasis on market intelligence, trade

promotion, and branding.

2. Strengthen producer access to market information

3. Deepen regional specialty coffee association role in value chain focusing on coffee cup

profiles, origin, traceability and relationship management with roasters.

4. Develop new financing models to improve access to credit for small scale producers in

Guatemala and medium scale producers in Nicaragua.

5. Increase production-related R&D to improve yields and consistency of product quality.

Strengthen extension services to support up-take of new technologies.

64

Kenneth Hynes

Skype: ken hynes

Tel: +1-617-312-3213

Contact information

65

C O N T R I B U T E D B Y T H E F L E T C H E R S C H O O L O F L A W & D I P L O M A C Y

A N D T H E F O L L O W I N G S T U D E N T S :

K R I S A N N E C A M P O S

E L I Z A B E T H H E N R Y

S T E P H A N I E L A N D E R S

A N D R E A M O L I N A

J O N A T H A N T O R N

66