Center for Global Development - cgdev.org · South African UEPS CardholdersSouth African UEPS...

22

June 14, 2006 June 14, 2006 Center for Center for Global Development Global Development

-

Upload

vuongthuan -

Category

Documents

-

view

215 -

download

0

Transcript of Center for Global Development - cgdev.org · South African UEPS CardholdersSouth African UEPS...

June 14, 2006June 14, 2006

Center forCenter forGlobal DevelopmentGlobal Development

2

Safe Harbor StatementSafe Harbor StatementSafe Harbor Statement

The Private Securities Litigation Reform Act of 1995 provides a “safe harbor” for certain forward-looking statements so long as such information is identified as forward-looking and is accompanied by meaningful cautionary statements identifying important factors that could cause actual results to differ materially from those projected in the information.

The use of words such as “may”, “might”, “will”, “should”, “expect”, “plan”, “anticipate”, “believe”, “estimate”, “project”, “intend”, “future”, “potential” or “continue”, and other similar expressions are intended to identify forward-looking statements.

All of these forward-looking statements are based on estimates and assumptions by ourmanagement that, although we believe to be reasonable, are inherently uncertain. Forward-looking statements involve risks and uncertainties, including, but not limited to, economic, competitive, governmental and technological factors outside of our control, that may cause our business, industry, strategy or actual results to differ materially from the forward-looking statements.

These risks and uncertainties may include those discussed in the Company’s annual report on Form 10-K for the year ended June 30, 2005 on file with the Securities and Exchange Commission, and other factors which may not be known to us. Any forward-looking statement speaks only as of its date. We undertake no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise, except as required by law.

3

Our MissionOur MissionOur Mission

Provide

a secure and affordable

electronic transaction platform

as well as financial services for

the world’s unbanked and under-banked

4

Traditional Systems Do Not Meet the Needs of the UnbankedTraditional Systems Do Not Meet the Needs of the UnbankedTraditional Systems Do Not Meet the Needs of the Unbanked

Limited purchasing

power

Littleimmediate

value

Lackof

choice

Mustusecash

5

Our SolutionOur SolutionOur Solution

Banked

Cashless

Low Cost

Offline

Reliable

Secure

Multiple Products

Competitive services

Choice

Peace of mind

6

UEPS PlatformUEPS PlatformUEPS Platform

Works offline

Enroll

Load

Spend

Settle

Biometric authentication

Robust data

Recoverable

Multiple applications

7

UEPS Operation

Cardholder Merchant

Mainframe

8

Multiple ProductsMultiple ProductsMultiple Products

Payment Applications:

Spending 3rd-party payments

Debit orders

Services:Lending, Insurance,

Savings,Money Transfers

Systems:Welfare, Wage,

Medical,Voting

Extended Applications:

Loyalty, Marketing,Identification, Public Records

UtilityServices:

Pre-paid Electricity,Water, Telephone,

Transportation

9

Benefits of Our SolutionBenefits of Our SolutionBenefits of Our Solution

10

South African UEPS CardholdersSouth African UEPS CardholdersSouth African UEPS Cardholders3.6 MM Cardholders

Grants, in thousands, paid in the three months ending March 31, 2006

Eastern Cape

KwaZulu-Natal

Limpopo

Northern Cape

North West

8014,607

2,832

2,089

402

11

UEPS Adoption at the Point of SaleUEPS Adoption at the Point of SaleUEPS Adoption at the Point of Sale

Card Holder Transactions: Merchant Loads Each Calendar Month

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

Jan-05 Feb-05 Mar-05 Apr-05 May-05 Jun-05 Jul-05 Aug-05 Sep-05 Oct-05 Nov-05 Dec-05 Jan-06 Feb-06 Mar-06

12

Namibia and BotswanaNamibia and BotswanaNamibia and Botswana

New entry pointBanking

Potential to demonstrate full platform

Financial servicesWage paymentMoney transferGovernment welfareSocial securityHealthcare services

Namibia

Botswana

13

Healthcare: HIV / AIDSHealthcare: HIV / AIDSHealthcare: HIV / AIDS

Client

Pharmacy

Doctor

Hospital

ClinicOutreach

MainframeReporting

14

Africa – Strong FocusAfrica Africa –– Strong FocusStrong Focus

Namibia(pop. 2MM)

Tanzania(pop. 37MM)

Kenya(pop. 34MM)

Nigeria(pop. 129MM)

Botswana(pop. 1.6MM)

Zambia(pop. 11MM)

South Africa(pop. 44MM)

15

Large NeedLarge NeedLarge Need

Brazil

Mexico

China

India

Indonesia

Malaysia

16

InteroperabilityInteroperabilityInteroperability

UEPS V/MC EMVGiftCard

Offline Online

17

Mobile PaymentsMobile PaymentsMobile Payments

18

Program EvaluationProgram EvaluationProgram Evaluation

Evaluation

Government

Donor / NGO

IndividualsAssistance

Information

19

Financial CharacteristicsFinancial CharacteristicsFinancial Characteristics

Low capital costs

Low operating costs

Broad channel for additional products

Supports micro-enterprise

20

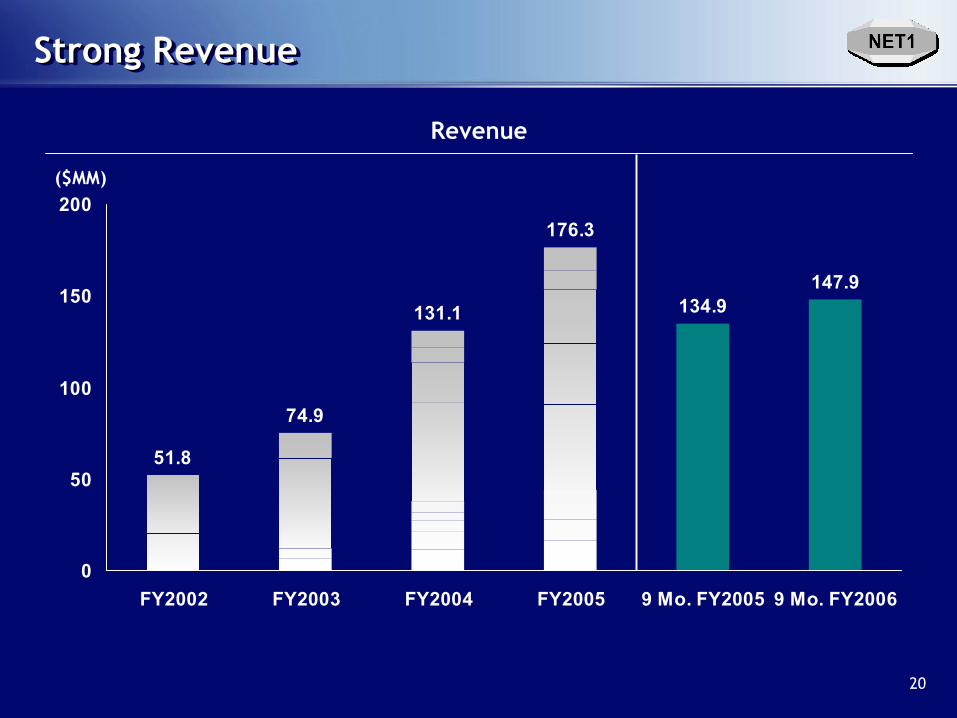

Strong RevenueStrong RevenueStrong Revenue

Revenue

51.8

74.9

131.1

176.3

134.9147.9

0

50

100

150

200

FY2002 FY2003 FY2004 FY2005 9 Mo. FY2005 9 Mo. FY2006

($MM)

21

Strong Net IncomeStrong Net IncomeStrong Net Income

Earnings Growth

8.513.1 13.3

44.634.4

43.7

0.0

10.0

20.0

30.0

40.0

50.0

FY2002 FY2003 FY2004 FY2005 9 Mo.FY2005

9 Mo.FY2006

($MM)

Earnings to shareholders Reorganization costs

DilutedEPS ($US) 0.27 0.37 0.38 0.80 0.62 0.76

11.1

June 14, 2006June 14, 2006

Center forCenter forGlobal DevelopmentGlobal Development