Center for Development Research (ZEF) University of Bonn

35

Food security challenges for the future - Agricultural productivity and the growing role of R&D Joachim von Braun Center for Development Research (ZEF) University of Bonn AGRINATURA Board meeting, ZEF April 2013

Transcript of Center for Development Research (ZEF) University of Bonn

Food security challenges for the future -Agricultural productivity and the growing role of R&D

Joachim von BraunCenter for Development Research (ZEF)

University of Bonn

AGRINATURA Board meeting, ZEF April 2013

Joachim von Braun, ZEF, March 2013

World food security?

• Availability

• Access

• Nutritional value

• Stability

Joachim von Braun, ZEF, March 2013

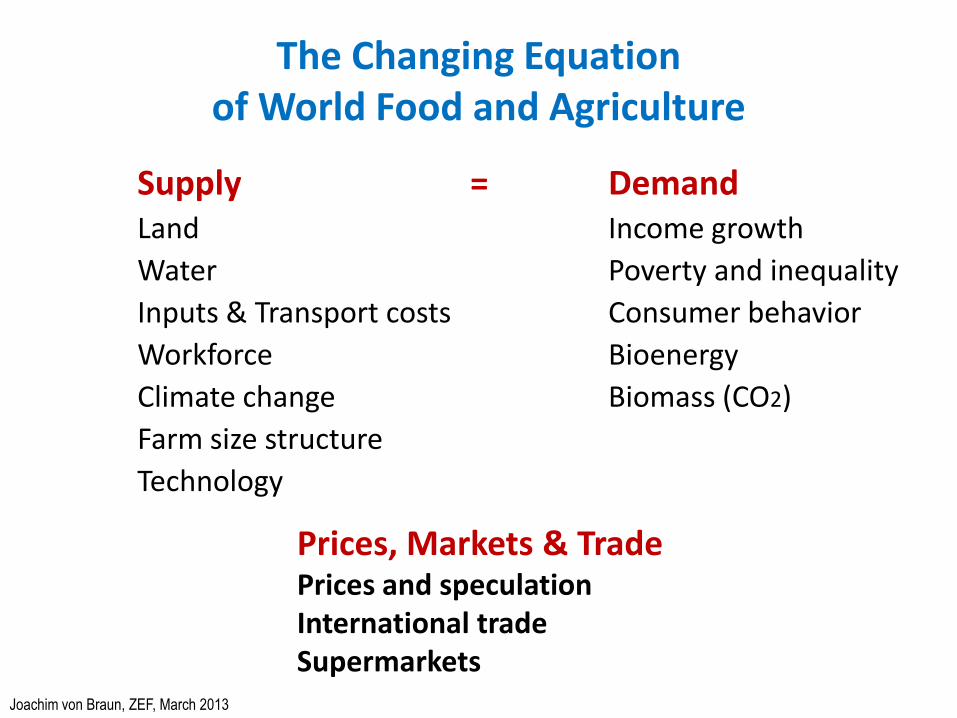

The Changing Equation of World Food and Agriculture

Supply =Land

Water

Inputs & Transport costs

Workforce

Climate change

Farm size structure

Technology

DemandIncome growth

Poverty and inequality

Consumer behavior

Bioenergy

Biomass (CO2)

Prices, Markets & TradePrices and speculationInternational tradeSupermarkets

Joachim von Braun, ZEF, March 2013

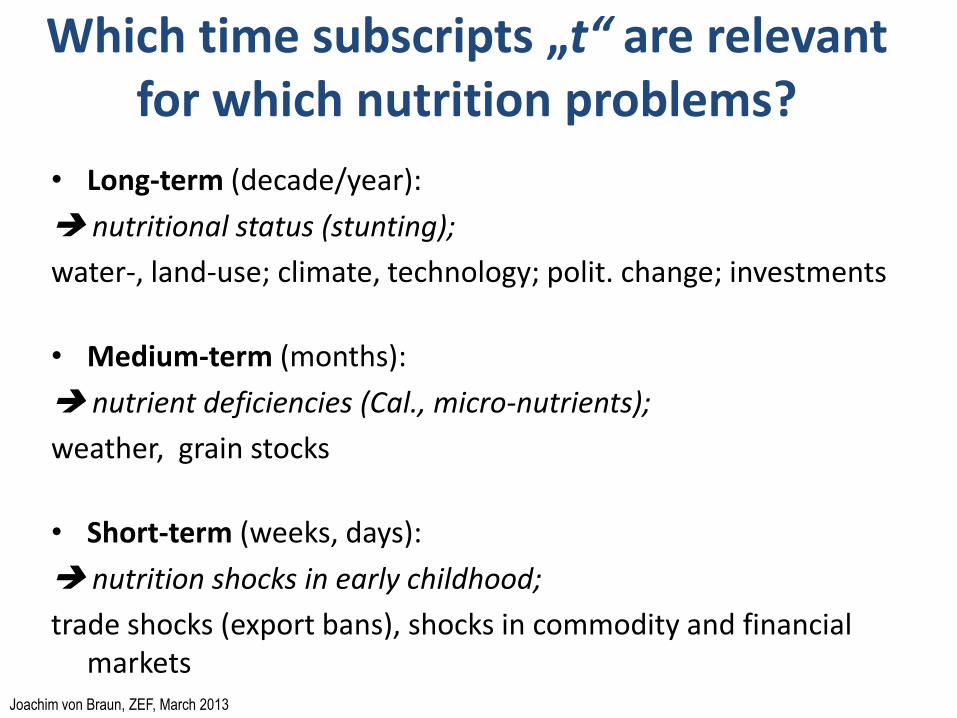

Which time subscripts „t“ are relevant for which nutrition problems?

• Long-term (decade/year):

nutritional status (stunting);

water-, land-use; climate, technology; polit. change; investments

• Medium-term (months):

nutrient deficiencies (Cal., micro-nutrients);

weather, grain stocks

• Short-term (weeks, days):

nutrition shocks in early childhood;

trade shocks (export bans), shocks in commodity and financialmarkets

Joachim von Braun, ZEF, March 2013

Consumption and food security challenge production

Joachim von Braun, ZEF, March 2013

World population 2050- from 7 to 9 Billion -

Source: Worldmapper 2009.

The 9 Billion will eat like 12 Billion

Joachim von Braun, ZEF, March 2013

Increased Global Food Demand 2010 – 2021 ca. + 20% per decade

Quelle: OECD – FAO Agriculture Outlook 2012-2020, 2012.

0,0

5,0

10,0

15,0

20,0

25,0

30,0

35,0W

eize

n

Gro

bkö

rner

Rei

s

Öls

aate

n

Pro

tein

meh

l

Pfl

anzl

ich

e Ö

le

Zuck

er

Rin

dfl

eisc

h

Sch

wei

nef

leis

ch

Gef

lüge

l

Sch

afe

Bu

tter

Käs

e

Vo

llmilc

hp

ulv

er

Mag

erm

ilch

pu

lver

Fisc

h

%

Joachim von Braun, ZEF, March 2013

Energy and climate change impact on the demand and supply side

Joachim von Braun, ZEF, March 2013

Nexus Perspective neededwater - food - energy

Bonn2011 Conference: The water, energy and food security nexusSolutions for the Green Economy, 16-18 Nov. 2011

Joachim von Braun, ZEF, March 2013

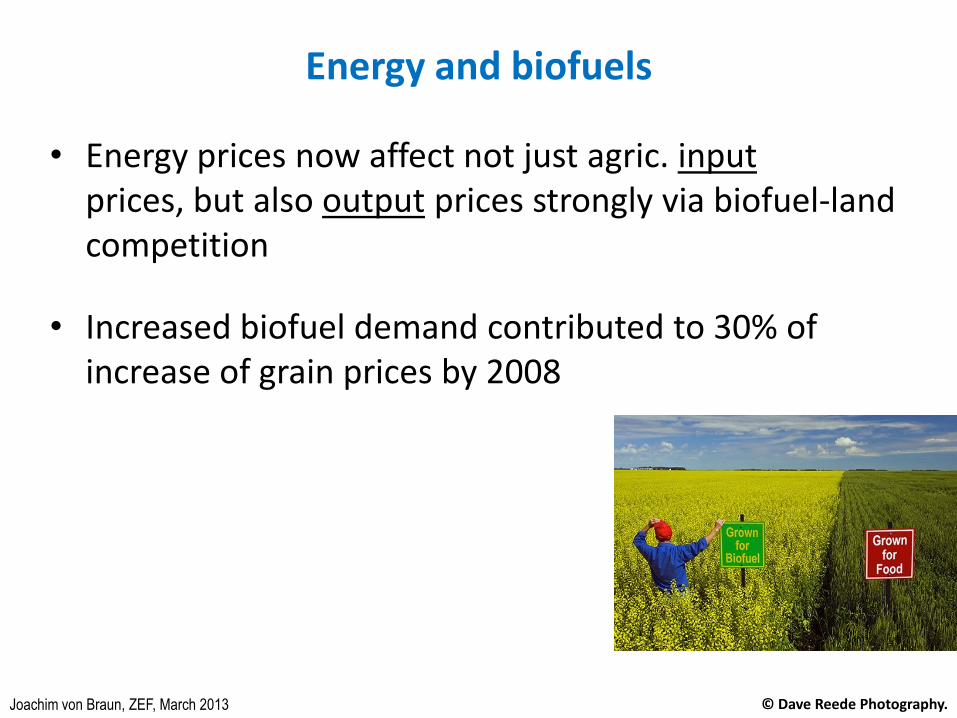

Energy and biofuels

• Energy prices now affect not just agric. input prices, but also output prices strongly via biofuel-land competition

• Increased biofuel demand contributed to 30% of increase of grain prices by 2008

© Dave Reede Photography.

Joachim von Braun, ZEF, March 2013

Increase of global energy consumption by 40 % in 2030

Biomass for energy use will grow

Source: IEA, 2009

Joachim von Braun, ZEF, March 2013

Climate change implications for agriculture

• Substitution to drought resistant crop species

• Demand for development of drought resistant varieties

Dry DaysSoil Moisture

Source: IPCC 2007. Figure shows changes for 2080-2099 relative to 1980-1999

Joachim von Braun, ZEF, March 2013

Farm size and land

Joachim von Braun, ZEF, March 2013

How did farm size change in past 40 years (1970 – 2010)

Change of

numbers of

farms (%)

Average size

in (ha)

from – to

China + … 0,6 - 0,4

Africa + … 1,6… (2007)

India + 58 2,2 - 1,2

Brazil + 6 59 - 68

US - 26 374 - 418

Sweden - 47 32 - 43

Source: FAOSTAT, US Census Bureau, IBGE, Statistics Sweden, Eurostat

Joachim von Braun, ZEF, March 2013

Total arable land is limited

• Climate change, urbanization and degradation affectarable land

• Protection of forests imposes further environmental limits

1220

1240

1260

1280

1300

1320

1340

1360

1380

1400

1420

Global Arable Land (Mio ha)

Source: FAOSTAT

Joachim von Braun, ZEF, March 2013

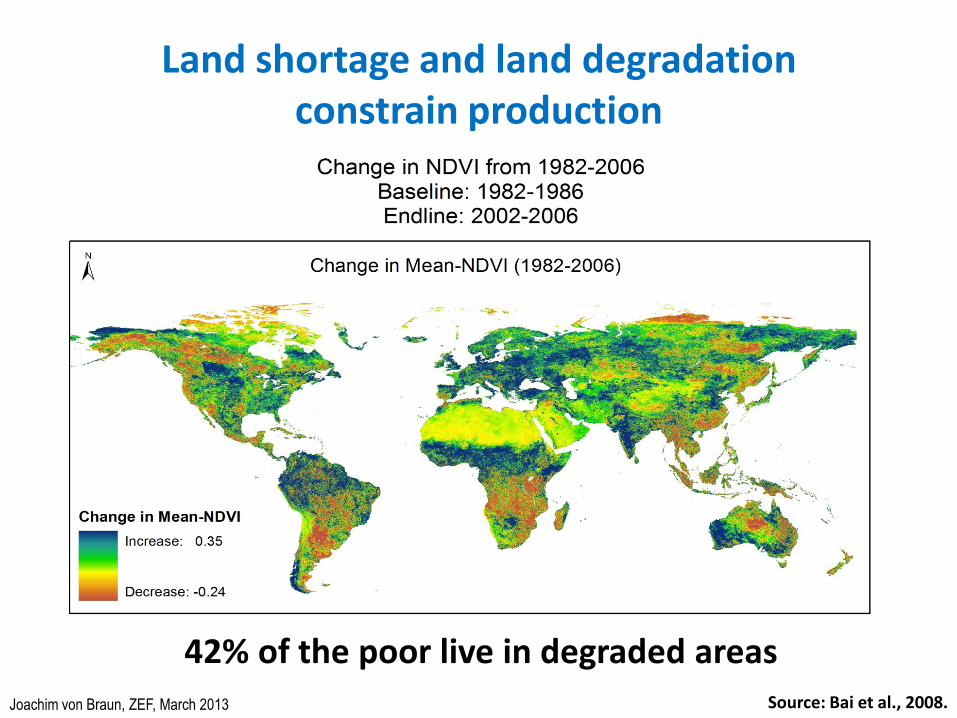

Land shortage and land degradationconstrain production

42% of the poor live in degraded areasSource: Bai et al., 2008.

Joachim von Braun, ZEF, March 2013

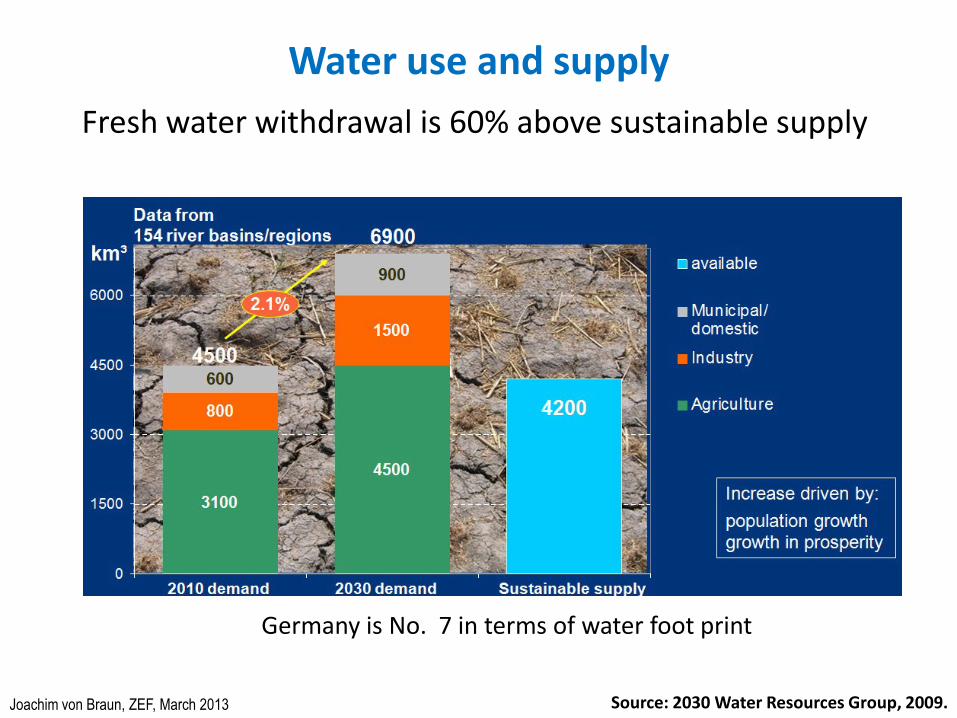

Water use and supply

Germany is No. 7 in terms of water foot print

Source: 2030 Water Resources Group, 2009.

Fresh water withdrawal is 60% above sustainable supply

Joachim von Braun, ZEF, March 2013

Investment in land(sales and long term lease)

Source: Land Matrix Homepage (accessed May 6, 2012)

Data: Land Matrix Project, April 2012

Joachim von Braun, ZEF, March 2013

Productivity, technology and R&D feed the world

Joachim von Braun, ZEF, March 2013

Global Agric. Production Growth

Annual growth rates (%)

0

0,5

1

1,5

2

2,5

3

2002-2011 2012-2021

Source: OECD – FAO Agriculture Outlook 2012, 2012.

Joachim von Braun, ZEF, March 2013

Yield gaps: where may they be tapped?

Source: N.D Mueller et.al. Nature 2012

Joachim von Braun, ZEF, March 2013

Innovation feeds the world

Source: IFPRI, 2012 Global Policy Report, 2013.

Sources of productivity growth in world agriculture

Beitrag vonTFP

Inputintensivierung

Bewässerung

Anbauflächen-erweiterung

Joachim von Braun, ZEF, March 2013

Innovation: Economic Regime and Agriculture

Lao PDR

Cambodia

Mauritania

Nepal

Cote d'IvoireBangladeshSudan

Ethiopia

Guinea

EritreaSierra Leone

Myanmar

Haiti

Tajikistan GhanaZambia

LesothoYemen, Rep.

Burkina Faso

Mali RwandaTanzania

Madagascar

Mozambique

Brazil

China

Guatemala

Sri Lanka

Vietnam

Indonesia

India

Kenya

Senegal

UgandaMalawi

Bolivia

Pakistan

Nigeria

Zimbabwe

BeninCameroon

12

34

56

Inn

ova

tion

0 1 2 3 4 5EconIncentiveRegime

Low Innovation - Low Incentive Low Innovation - High Incentive

High Innovation - Incentive High Innovation - Low Incentive

Source: Pangaribowo and Gerber (2013), calculation based on KEI 2012

Econ and Institution Regime: tariff and nontariff barriers, regulatory quality and rule of lawSource: KAM (2012) and WDI (2010)

Joachim von Braun, ZEF, March 2013

Markets and prices

Joachim von Braun, ZEF, March 2013

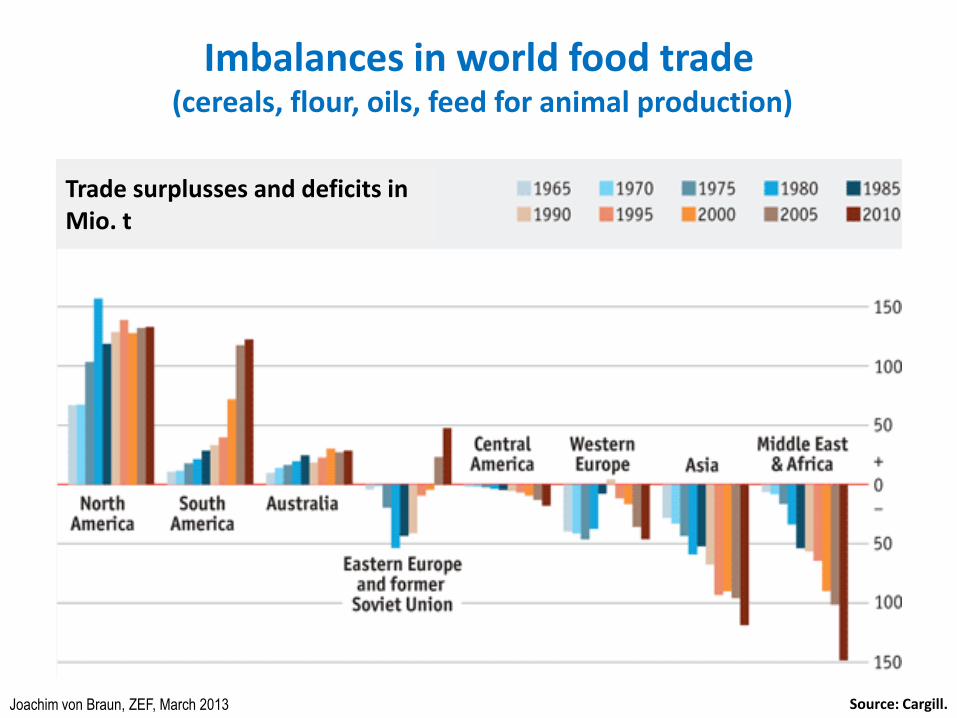

Imbalances in world food trade(cereals, flour, oils, feed for animal production)

Source: Cargill.

Trade surplusses and deficits in Mio. t

Joachim von Braun, ZEF, March 2013

Food price crises 2008 and 2011: New price levels, volatility, extreme spikes

Quelle: FAO, FAO Giews.

0,0

50,0

100,0

150,0

200,0

250,0

300,0

0

100

200

300

400

500

600

700

800

900

1000

1/2

00

0

8/2

00

0

3/2

00

1

10

/20

01

5/2

00

2

12

/20

02

7/2

00

3

2/2

00

4

9/2

00

4

4/2

00

5

11

/20

05

6/2

00

6

1/2

00

7

8/2

00

7

3/2

00

8

10

/20

08

5/2

00

9

12

/20

09

7/2

01

0

2/2

01

1

9/2

01

1

4/2

01

2

Pre

is in

$ p

ro T

on

ne

Reispreis $/t

Weizenpreis $/t

Globaler Getreidepreisindex

Ind

ex

Joachim von Braun, ZEF, March 2013

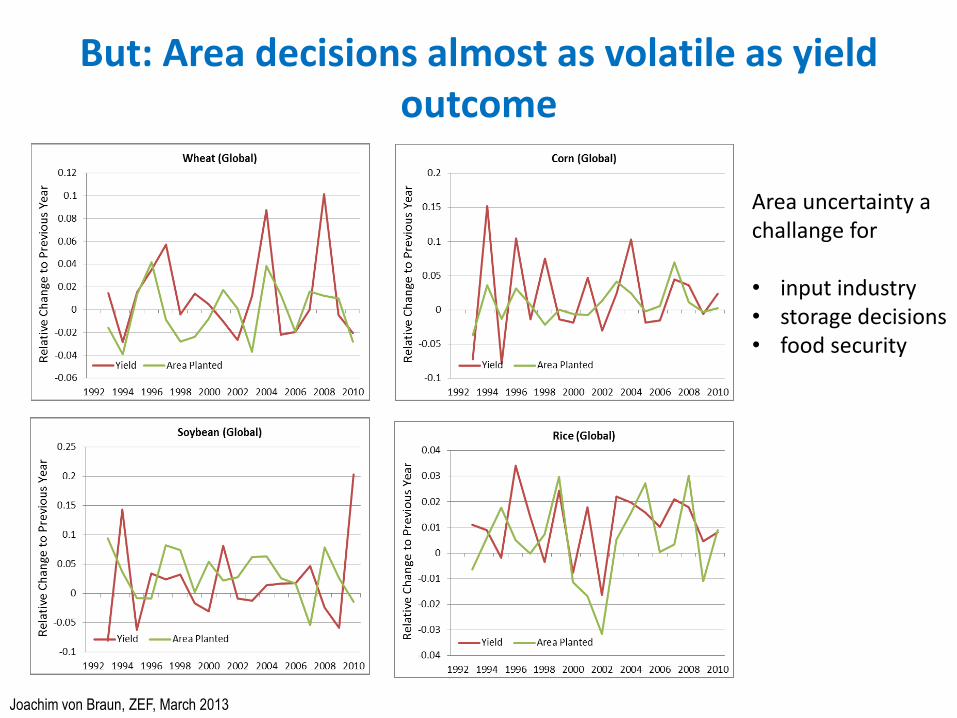

But: Area decisions almost as volatile as yieldoutcome

Area uncertainty a challange for

• input industry• storage decisions• food security

Joachim von Braun, ZEF, March 2013

Oil Prices Remain High

Source: USDA Outlook 2013

Joachim von Braun, ZEF, March 2013

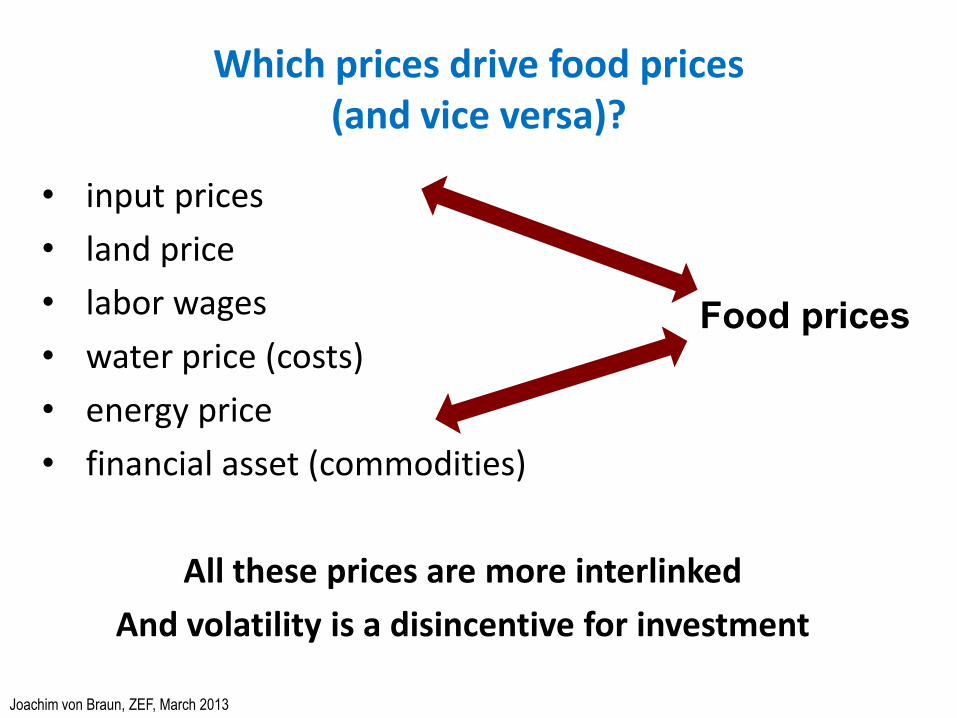

Which prices drive food prices (and vice versa)?

• input prices

• land price

• labor wages

• water price (costs)

• energy price

• financial asset (commodities)

All these prices are more interlinked

And volatility is a disincentive for investment

Food prices

Joachim von Braun, ZEF, March 2013

Getting ready for the Bioeconomy

Joachim von Braun, ZEF, March 2013

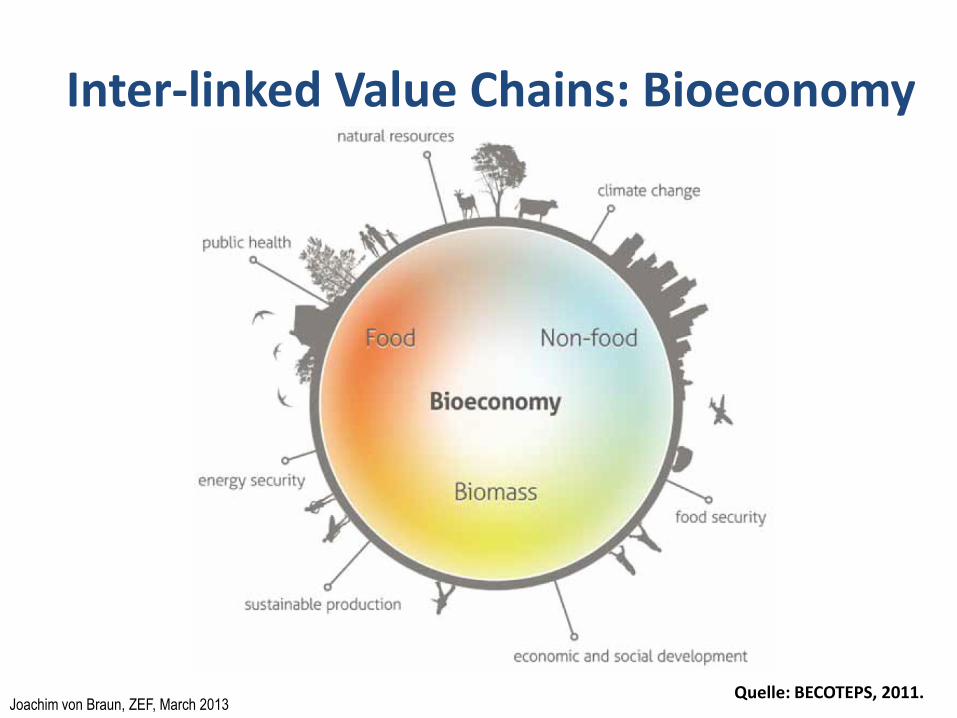

Inter-linked Value Chains: Bioeconomy

Quelle: BECOTEPS, 2011.

Joachim von Braun, ZEF, March 2013

Biomass and its products -- Bioeconomy

Biomass

Foods and beverages______________

Bio-energy

Staples / animal feeds

Bio materials

Biochemicals

Source: Bioeconomy Council, Germany, 2010

Joachim von Braun, ZEF, March 2013

Towards zero waste and reduced losses

Source: J. Gustafson et.al. FAO 2011

Waste and losses are very different things, and Kilogram is not appropriate unit of measurement

Joachim von Braun, ZEF, March 2013

Strategic food and nutrition security agenda1. Risk prevention: Promotion of agriculture productivity across

value chains with research and technology and investment (public and private) to address price levels and risks on supply side in sustainable ways.

2. Risk management: Facilitation of reduced market volatility and spikes with appropriate stocks, more trade openness, appropriate regulation, and international cooperation.

3. Social protection: productive safety nets, (conditional) cash transfers; expanded action for nutrition security of children.

4. Insurance systems: insurance of crops, peoples health and disabilities, public insurance mechanisms for catastrophic events in poor countries (e.g. regional droughts, climate shocks)

Joachim von Braun, ZEF, March 2013

EU science agenda: key for international food security

• Sustainable food security under climate change: modelling, benchmarking and policy research,

• Sustainable growth and intensification of agricultural systems under current and future resource availability,

• Assessing and reducing trade-offs between food production, biodiversity and ecosystem services,

• Adaptation to climate change and Greenhouse gas mitigation

See: FACCE – JPI, Strategic Research Agenda. Agriculture, Food Security, and Climate Change 2012

www.faccejpi.com