CEI Economic Forum November 2009 - Central European Initiative RICHTER ppt.pdf · 0 10 20 30 40 50...

36

Ewa Korczyc and Kaspar Richter Ewa Korczyc and Kaspar Richter [email protected] [email protected] CEI Economic Forum November 2009

Transcript of CEI Economic Forum November 2009 - Central European Initiative RICHTER ppt.pdf · 0 10 20 30 40 50...

Ewa Korczyc and Kaspar RichterEwa Korczyc and Kaspar Richter

[email protected]@worldbank.org

CEI Economic Forum

November 2009

�� CEI countriesCEI countries

�� What we have seenWhat we have seen–– Stabilization Stabilization

�� Why countries are differentWhy countries are different–– Initial conditions, market size, depreciation and f iscal Initial conditions, market size, depreciation and f iscal

stimulusstimulus

�� What we can expectWhat we can expect–– Slow recoverySlow recovery

OverviewOverview

CEI countriesCEI countries

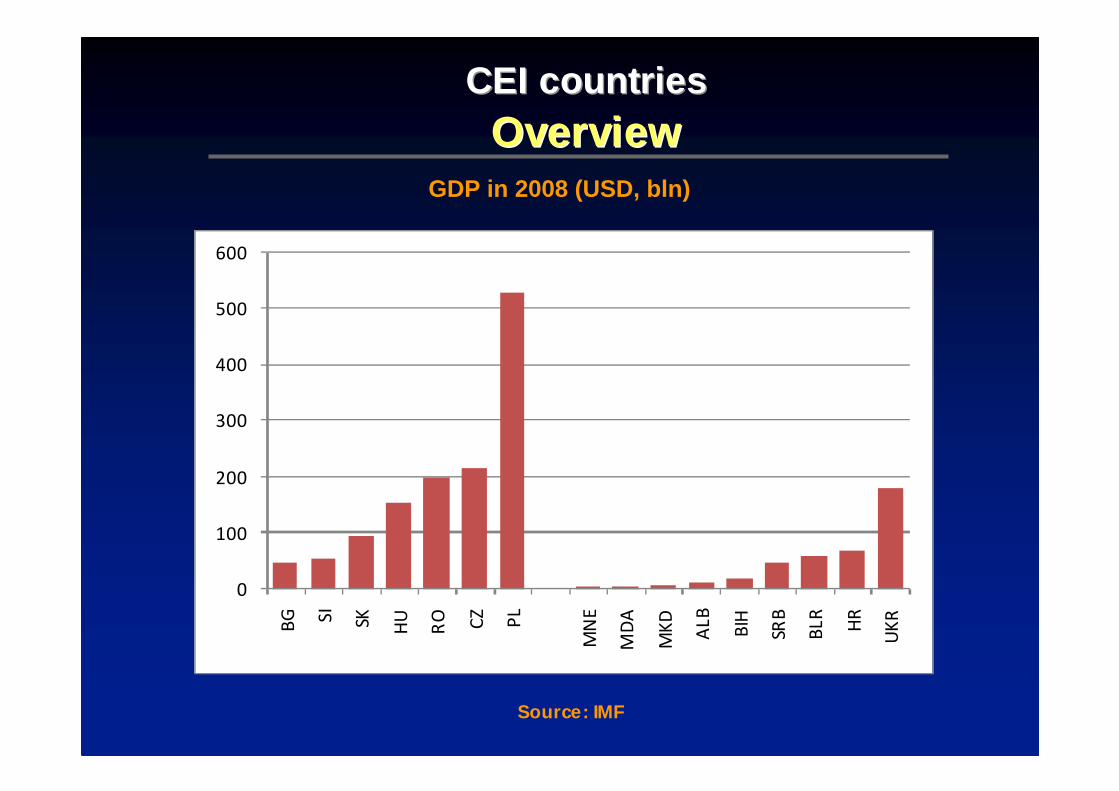

CEI countriesCEI countriesOverviewOverview

GDP in 2008 (USD, bln)

Source: IMF

0

100

200

300

400

500

600

BG SI

SK HU

RO CZ

PL

MN

E

MD

A

MK

D

AL

B

BIH

SRB

BL

R

HR

UK

R

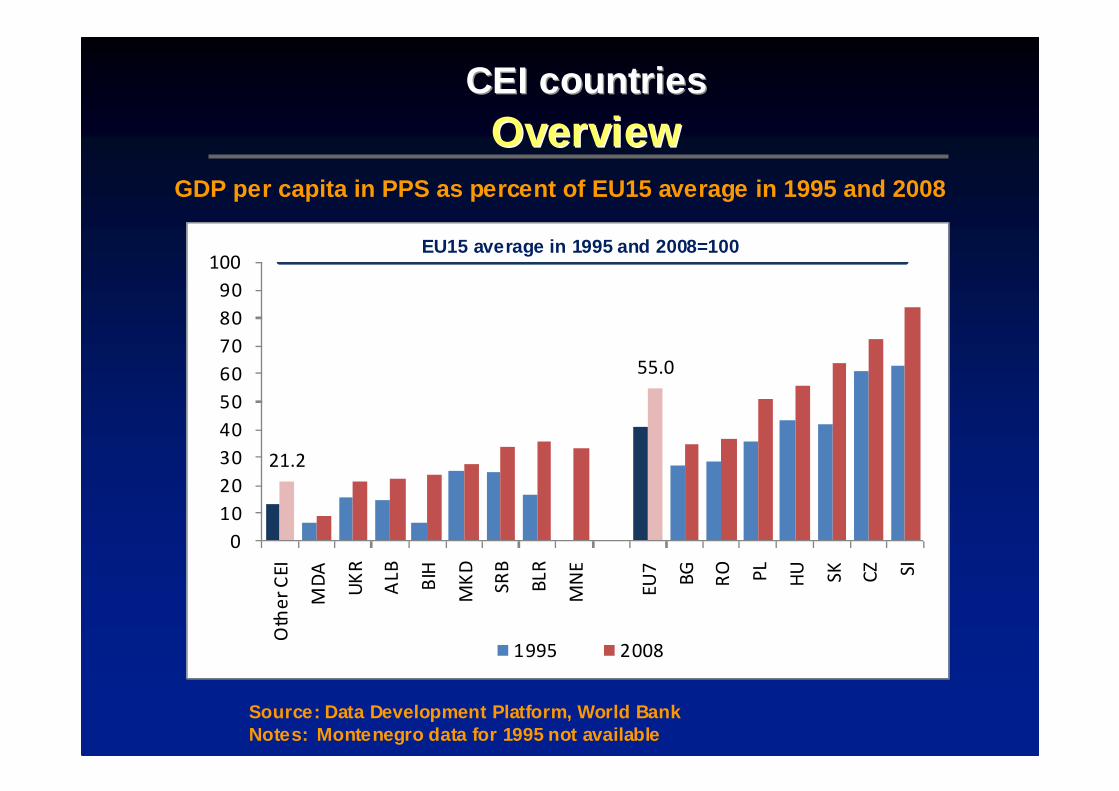

CEI countriesCEI countriesOverviewOverview

GDP per capita in PPS as percent of EU15 average in 1995 and 2008

Source: Data Development Platform, World BankNotes: Montenegro data for 1995 not available

EU15 average in 1995 and 2008=100

21.2

55.0

0

10

20

30

40

50

60

70

80

90

100O

the

r C

EI

MD

A

UK

R

AL

B

BIH

MK

D

SR

B

BL

R

MN

E

EU

7

BG

RO PL

HU SK

CZ SI

1995 2008

EU15 average in 1995 and 2008=100

What we have seenWhat we have seen

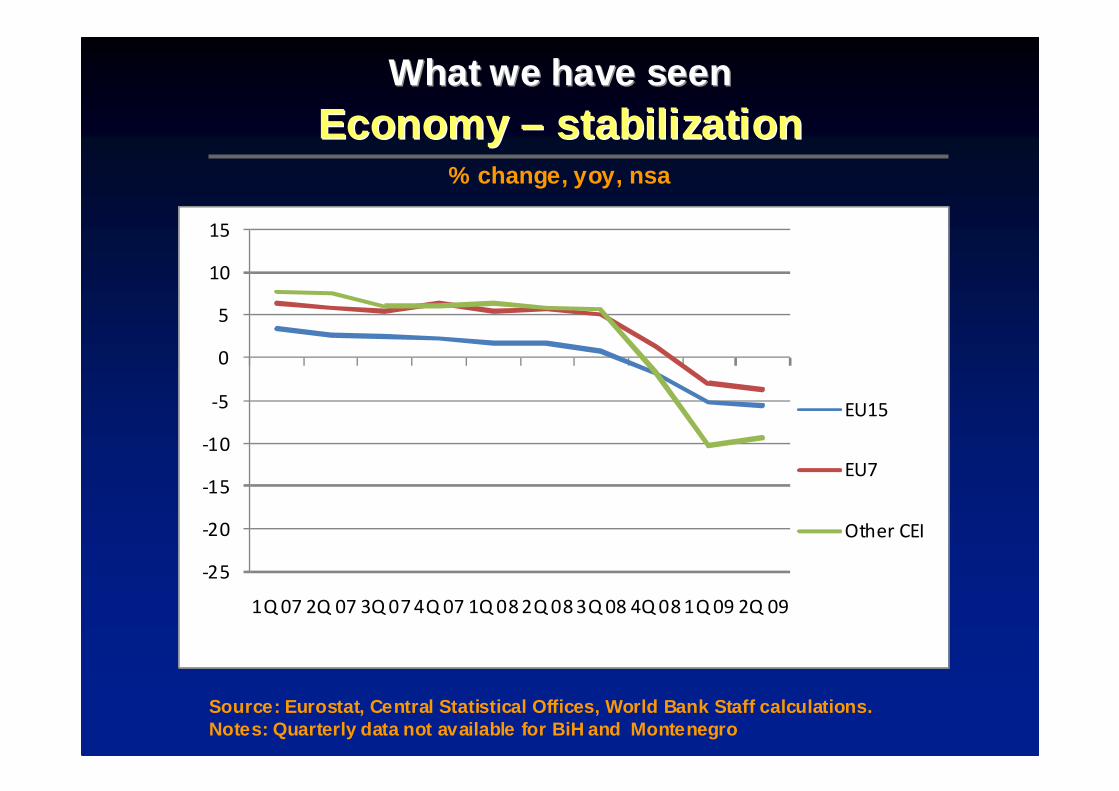

What we have seenWhat we have seenEconomy Economy –– stabilizationstabilization

% change, yoy, nsa

Source: Eurostat, Central Statistical Offices, Worl d Bank Staff calculations.Notes: Quarterly data not available for BiH and Mo ntenegro

-25

-20

-15

-10

-5

0

5

10

15

1Q 07 2Q 07 3Q 07 4Q 07 1Q 08 2Q 08 3Q 08 4Q 08 1Q 09 2Q 09

EU15

EU7

Other CEI

What we have seenWhat we have seenEconomy Economy –– stabilizationstabilization

% change, yoy, nsa

Source: Eurostat, Central Statistical Offices, Worl d Bank Staff calculations.

-25

-20

-15

-10

-5

0

5

10

15

1Q 07 2Q 07 3Q 07 4Q 07 1Q 08 2Q 08 3Q 08 4Q 08 1Q 09 2Q 09

ALB

BLR

MKD

MDA

SRB

UKR

HR

EU7 Other CEI

-25

-20

-15

-10

-5

0

5

10

15

1Q 07 2Q 07 3Q 07 4Q 07 1Q 08 2Q 08 3Q 08 4Q 08 1Q 09 2Q 09

BG

CZ

HU

PL

RO

SI

SK

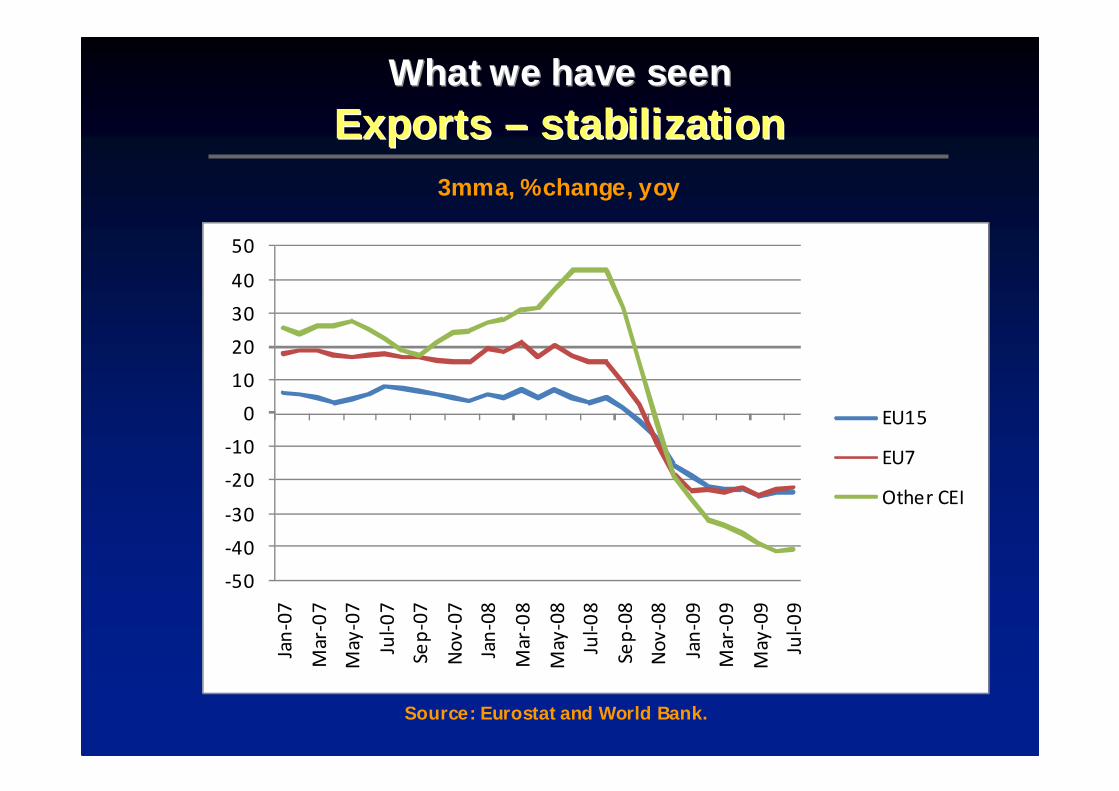

What we have seenWhat we have seenExports Exports –– stabilizationstabilization

3mma, %change, yoy

Source: Eurostat and World Bank.

-50

-40

-30

-20

-10

0

10

20

30

40

50

Jan

-07

Mar-

07

May

-07

Jul-

07

Se

p-0

7

No

v-0

7

Jan

-08

Mar-

08

May

-08

Jul-

08

Se

p-0

8

No

v-0

8

Jan

-09

Mar-

09

May

-09

Jul-

09

EU15

EU7

Other CEI

What we have seenWhat we have seenExports Exports –– stabilizationstabilization

3mma, %change, yoy

Source: Eurostat and World Bank.

-60

-50

-40

-30

-20

-10

0

10

20

30

40

50

60

70

Jan

-07

Mar

-07

Ma

y-0

7

Jul-

07

Se

p-0

7

No

v-0

7

Jan

-08

Mar

-08

Ma

y-0

8

Jul-

08

Se

p-0

8

No

v-0

8

Jan

-09

Mar

-09

Ma

y-0

9

Jul-

09

BG

CZ

HU

PL

RO

SI

SK -60

-50

-40

-30

-20

-10

0

10

20

30

40

50

60

70

Jan

-07

Mar

-07

Ma

y-0

7

Jul-

07

Se

p-0

7

No

v-0

7

Jan

-08

Mar

-08

Ma

y-0

8

Jul-

08

Se

p-0

8

No

v-0

8

Jan

-09

Mar

-09

Ma

y-0

9

Jul-

09

ALB

BLR

BIH

MKD

MDA

MNE

SRB

UKR

HR

EU7 Other CEI

What we have seenWhat we have seenImports Imports –– stabilizationstabilization

3mma, %change, yoy

Source: Eurostat and World Bank.

-50

-40

-30

-20

-10

0

10

20

30

40

50Ja

n-0

7

Ma

r-0

7

May

-07

Jul-

07

Se

p-0

7

No

v-0

7

Jan

-08

Ma

r-0

8

May

-08

Jul-

08

Se

p-0

8

No

v-0

8

Jan

-09

Ma

r-0

9

May

-09

Jul-

09

EU15

EU7

Other CEI

What we have seenWhat we have seenImports Imports –– stabilizationstabilization

3mma, %change, yoy

Source: Eurostat and World Bank.

-60

-50

-40

-30

-20

-10

0

10

20

30

40

50

60

70

Jan

-07

Mar

-07

Ma

y-0

7

Jul-

07

Se

p-0

7

No

v-0

7

Jan

-08

Mar

-08

Ma

y-0

8

Jul-

08

Se

p-0

8

No

v-0

8

Jan

-09

Mar

-09

Ma

y-0

9

Jul-

09

BG

CZ

HU

PL

RO

SI

SK -60

-50

-40

-30

-20

-10

0

10

20

30

40

50

60

70

Jan

-07

Mar

-07

Ma

y-0

7

Jul-

07

Se

p-0

7

No

v-0

7

Jan

-08

Mar

-08

Ma

y-0

8

Jul-

08

Se

p-0

8

No

v-0

8

Jan

-09

Mar

-09

Ma

y-0

9

Jul-

09

ALB

BLR

BIH

MKD

MDA

MNE

SRB

UKR

HR

EU7 Other CEI

What we have seenWhat we have seenIndustrial production Industrial production –– reboundrebound

3mma, wda, %change, yoy

Source: Eurostat, statistical Offices, and World Ba nk.Notes: Other CEI without BiH and Albania

-40

-30

-20

-10

0

10

20

Jan

-07

Mar-

07

May

-07

Jul-

07

Se

p-0

7

No

v-0

7

Jan

-08

Mar-

08

May

-08

Jul-

08

Se

p-0

8

No

v-0

8

Jan

-09

Mar-

09

May

-09

Jul-

09

EU15

EU10

Other CEI

What we have seenWhat we have seenIndustrial production Industrial production –– reboundrebound

3mma, %change, yoy

Source: Eurostat, Statistical Offices, and World B ank.

-50

-40

-30

-20

-10

0

10

20

Jan

-07

Mar

-07

Ma

y-0

7

Jul-

07

Se

p-0

7

No

v-0

7

Jan

-08

Mar

-08

Ma

y-0

8

Jul-

08

Se

p-0

8

No

v-0

8

Jan

-09

Mar

-09

Ma

y-0

9

Jul-

09

BG

CZ

HU

PL

RO

SI

SK

EU7 Other CEI

-50

-40

-30

-20

-10

0

10

20

Jan

-07

Mar

-07

Ma

y-0

7

Jul-

07

Se

p-0

7

No

v-0

7

Jan

-08

Mar

-08

Ma

y-0

8

Jul-

08

Se

p-0

8

No

v-0

8

Jan

-09

Mar

-09

Ma

y-0

9

Jul-

09

ALB

BLR

BIH

MKD

MDA

MNE

SRB

UKR

HR

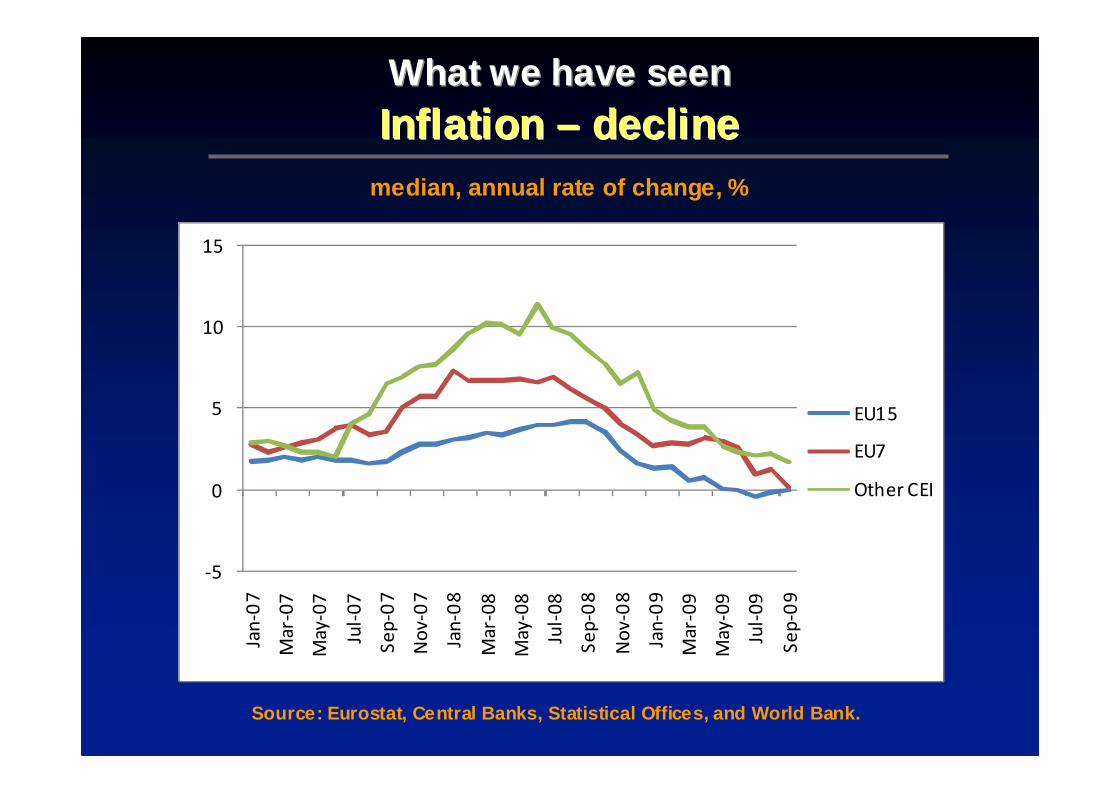

What we have seenWhat we have seenInflation Inflation –– declinedecline

median, annual rate of change, %

Source: Eurostat, Central Banks, Statistical Office s, and World Bank.

-5

0

5

10

15Ja

n-0

7

Mar-

07

May-0

7

Jul-

07

Se

p-0

7

No

v-0

7

Jan

-08

Mar-

08

May-0

8

Jul-

08

Se

p-0

8

No

v-0

8

Jan

-09

Mar-

09

May-0

9

Jul-

09

Se

p-0

9

EU15

EU7

Other CEI

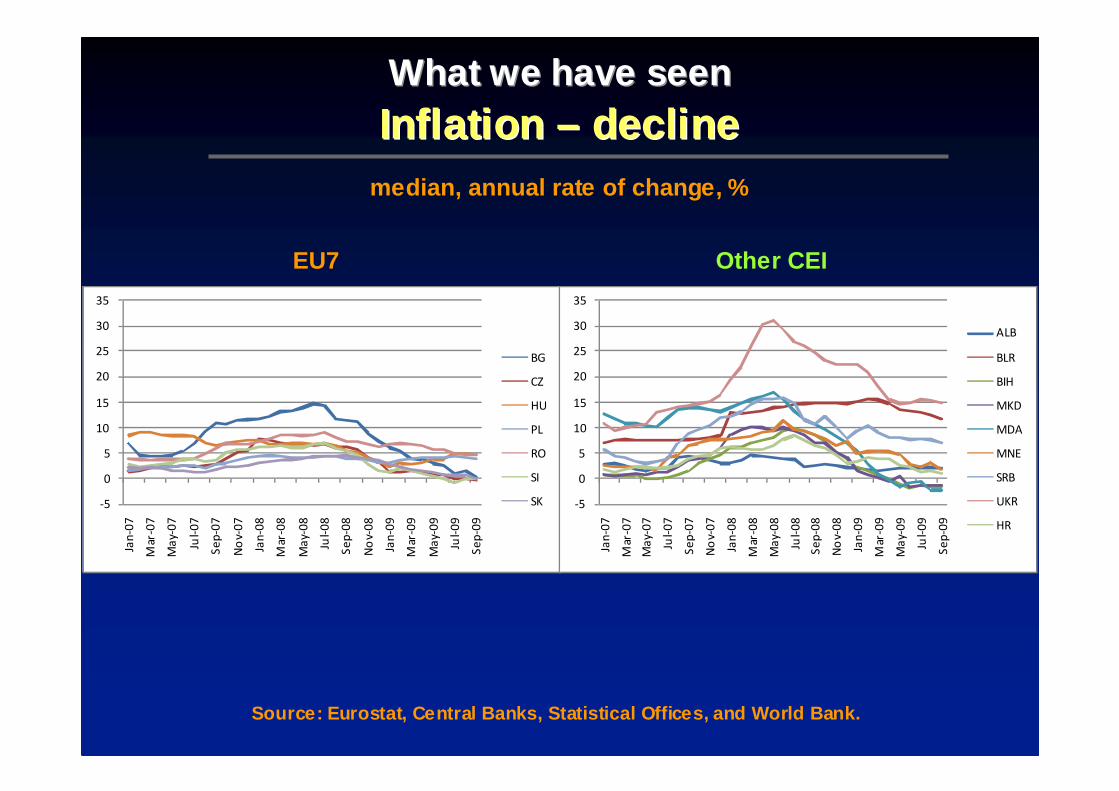

What we have seenWhat we have seenInflation Inflation –– declinedecline

median, annual rate of change, %

Source: Eurostat, Central Banks, Statistical Office s, and World Bank.

-5

0

5

10

15

20

25

30

35

Jan

-07

Mar

-07

Ma

y-0

7

Jul-

07

Se

p-0

7

No

v-0

7

Jan

-08

Mar

-08

Ma

y-0

8

Jul-

08

Se

p-0

8

No

v-0

8

Jan

-09

Mar

-09

Ma

y-0

9

Jul-

09

Se

p-0

9

BG

CZ

HU

PL

RO

SI

SK -5

0

5

10

15

20

25

30

35

Jan

-07

Mar

-07

Ma

y-0

7

Jul-

07

Se

p-0

7

No

v-0

7

Jan

-08

Mar

-08

Ma

y-0

8

Jul-

08

Se

p-0

8

No

v-0

8

Jan

-09

Mar

-09

Ma

y-0

9

Jul-

09

Se

p-0

9

ALB

BLR

BIH

MKD

MDA

MNE

SRB

UKR

HR

EU7 Other CEI

What we have seenWhat we have seenCapital flows Capital flows –– strong bond issuance in EU7, no recovery in Other C EIstrong bond issuance in EU7, no recovery in Other C EI

Gross capital inflows to EU7 and Other CEI (US$ billion)

Source: World Bank Global Prospect Group, World Ban k Staff calculations.Notes: EU7* does not include Slovenia, Other CEI** is without Albania, BiH and Montenegro

EU7* Other CEI**

0

5

10

15

20

25

1Q

07

2Q

07

3Q

07

4Q

07

1Q

08

2Q

08

3Q

08

4Q

08

1Q

09

2Q

09

3Q

09

Banks

Equity

Bonds

0

5

10

15

20

25

1Q

07

2Q

07

3Q

07

4Q

07

1Q

08

2Q

08

3Q

08

4Q

08

1Q

09

2Q

09

3Q

09

Banks

Equity

Bonds

What we have seenWhat we have seenSovereign bonds Sovereign bonds –– easing of CDS in EU7easing of CDS in EU7

5-Year Credit Default Swaps (%)

Source: World Bank Global Prospect

Group, World Bank Staff calculations.

0

1 00

2 00

3 00

4 00

5 00

6 00

7 00

8 00

Jan

-07

Ap

r-0

7

Jul-

07

Oc

t-0

7

Jan

-08

Ap

r-0

8

Jul-

08

Oc

t-0

8

Jan

-09

Ap

r-0

9

Jul-

09

Oc

t-0

9

BG

CZ

HU

PL

RO

SI

SK0

100 0

200 0

300 0

400 0

500 0

600 0

Jan

-07

Ap

r-0

7

Jul-

07

Oc

t-0

7

Jan

-08

Ap

r-0

8

Jul-

08

Oc

t-0

8

Jan

-09

Ap

r-0

9

Jul-

09

Oc

t-0

9

UKR

HR

0

100

200

300

400

500

600

700

800

Jan

-07

Ap

r-0

7

Jul-

07

Oc

t-0

7

Jan

-08

Ap

r-0

8

Jul-

08

Oc

t-0

8

Jan

-09

Ap

r-0

9

Jul-

09

Oc

t-0

9

IT

GR

DE

ES

What we have seenWhat we have seenStock market Stock market –– recoveryrecovery

Stock Market Indices (January 2008=100)

Source: Reuters, World Bank Staff Calculations

0

20

40

60

80

100

120

Jan

-08

Ma

r-0

8

Ma

y-0

8

Jul-

08

Se

p-0

8

No

v-0

8

Jan

-09

Ma

r-0

9

Ma

y-0

9

Jul-

09

Se

p-0

9

EURO

STOXX

IT

DE

Source: Reuters, World Bank Staff

calculations.

0

20

40

60

80

100

120

Jan

-08

Ma

r-0

8

May

-08

Jul-

08

Sep

-08

No

v-0

8

Jan

-09

Ma

r-0

9

May

-09

Jul-

09

Sep

-09

BG

CZ

HU

PL

RO

SI

SK0

20

40

60

80

1 00

1 20

Jan

-08

Mar

-08

Ma

y-0

8

Jul-

08

Se

p-0

8

No

v-0

8

Jan

-09

Mar

-09

Ma

y-0

9

Jul-

09

Se

p-0

9

BIH

MKD

MNE

SRB

UKR

HR

What we have seenWhat we have seenBanks Banks –– interbank rates down, spreads persistentinterbank rates down, spreads persistent

Interbank rates (3 months)

Source: World Bank Global Prospect Group, World Ban k Staff calculations.

Interbank rate spreads over Libor

0

5

10

15

20

25

30

35

40

Jan

-08

Mar

-08

Ma

y-0

8

Jul-

08

Se

p-0

8

No

v-0

8

Jan

-09

Mar

-09

Ma

y-0

9

Jul-

09

Se

p-0

9

BG

CZ

HU

PL

RO

SI

SK

SRB

UKR

IT

AT

-50 0

0

50 0

1 000

1 500

2 000

2 500

3 000

3 500

IT SI AT CZ SK PL BG HU RO SRB UKR

average June

20 08

average Feb

20 09

average 1H

Oct 2009

What we have seenWhat we have seenParent banks Parent banks –– easing of CDSeasing of CDS

European Banks’ 5-year CDS (bps)

Source: Bloomberg, Datastream, World Bank Staff cal culations.

0

100

200

300

400

500

600Ja

n-0

8

Mar-

08

May-0

8

Jul-

08

Se

p-0

8

No

v-0

8

Jan

-09

Mar-

09

May-0

9

Jul-

09

Se

p-0

9

Raiffeisen

Deutsche Bank

Soc Generale

Unicredit

Intesa

ERSTE

SEB Bank

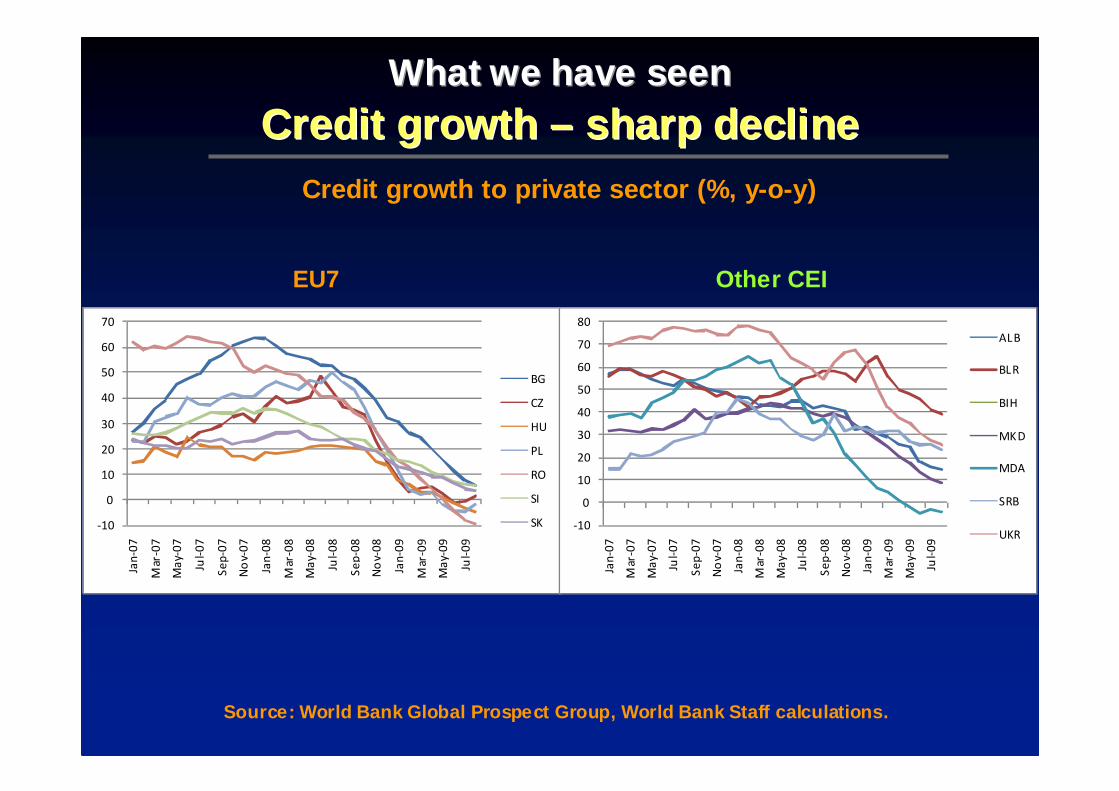

What we have seenWhat we have seenCredit growth Credit growth –– sharp declinesharp decline

Credit growth to private sector (%, y-o-y)

Source: World Bank Global Prospect Group, World Ban k Staff calculations.

-10

0

10

20

30

40

50

60

70

Jan

-07

Mar

-07

Ma

y-0

7

Jul-

07

Se

p-0

7

No

v-0

7

Jan

-08

Mar

-08

Ma

y-0

8

Jul-

08

Se

p-0

8

No

v-0

8

Jan

-09

Mar

-09

Ma

y-0

9

Jul-

09

BG

CZ

HU

PL

RO

SI

SK -10

0

10

20

30

40

50

60

70

80

Jan

-07

Mar

-07

Ma

y-0

7

Jul-

07

Se

p-0

7

No

v-0

7

Jan

-08

Mar

-08

Ma

y-0

8

Jul-

08

Se

p-0

8

No

v-0

8

Jan

-09

Mar

-09

Ma

y-0

9

Jul-

09

ALB

BLR

BIH

MKD

MDA

SRB

UKR

EU7 Other CEI

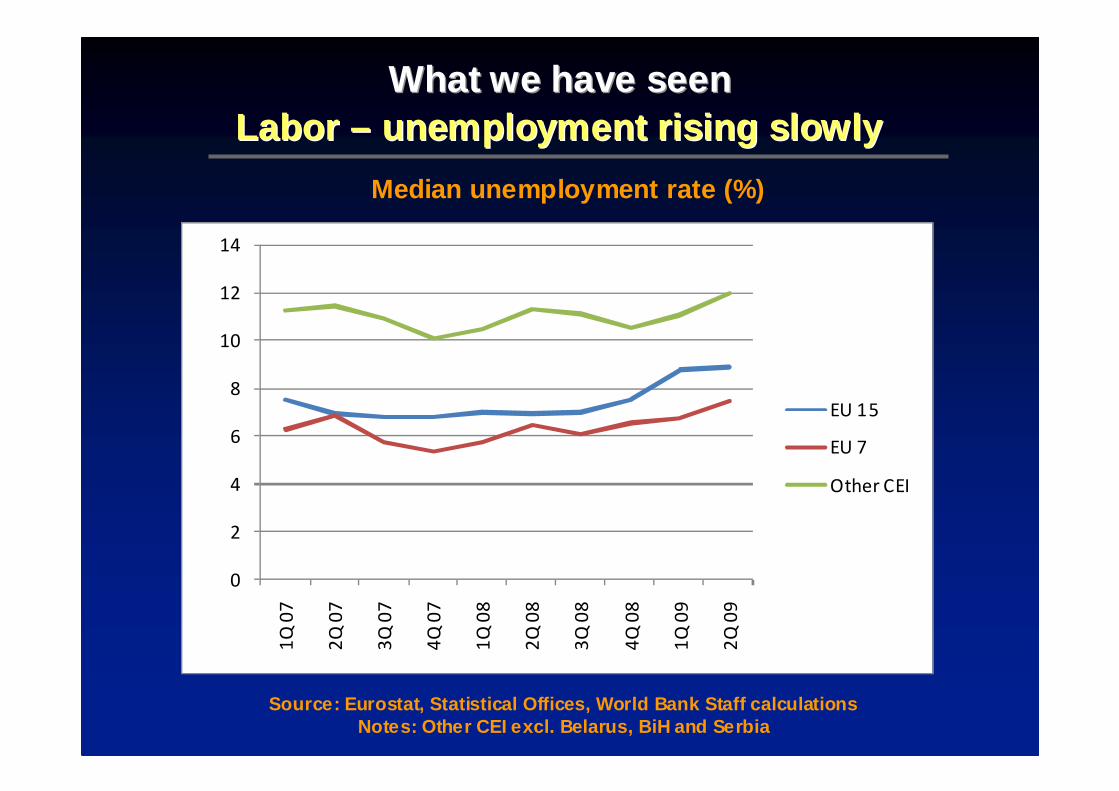

What we have seenWhat we have seenLabor Labor –– unemployment rising slowlyunemployment rising slowly

Source: Eurostat, Statistical Offices, World Bank S taff calculationsNotes: Other CEI excl. Belarus, BiH and Serbia

Median unemployment rate (%)

0

2

4

6

8

10

12

14

1Q

07

2Q

07

3Q

07

4Q

07

1Q

08

2Q

08

3Q

08

4Q

08

1Q

09

2Q

09

EU 15

EU 7

Other CEI

Why countries are differentWhy countries are different

Why countries are differentWhy countries are differentProjected downturn increases with initial macro imb alancesProjected downturn increases with initial macro imb alances

Cumulative output drop 2008-10 vs. bank-related cap ital inflows in 2Q 07-1Q 08

Source: IMF, World Bank, DEC PG, World Bank Staff c alculations

BG

CZ

HU

PL

RO

SI

SK

IT

AT

BLR

MKD

MDA

SRB

UKR

HR

-12

-10

-8

-6

-4

-2

0

2

4

0 1 2 3 4 5 6 7 8

Cu

mu

lati

ve

ou

tpu

t d

rop

20

08

-10

Bank related capital inflows in 2Q 07-1Q 08 as percent of 2008 GDP

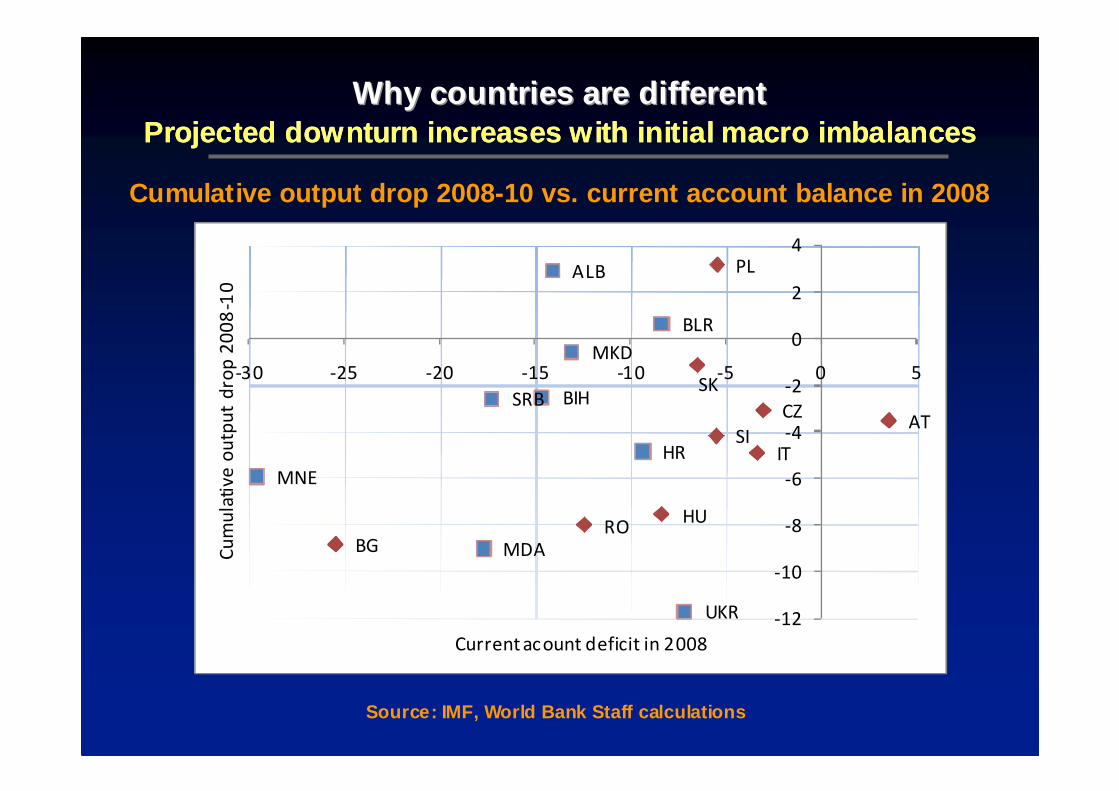

Why countries are different Why countries are different Projected downturn increases with initial macro imb alancesProjected downturn increases with initial macro imb alances

Cumulative output drop 2008-10 vs. current account balance in 2008

Source: IMF, World Bank Staff calculations

BG

CZ

HU

PL

RO

SI

SK

IT

AT

ALB

BLR

BIH

MKD

MDA

MNE

SRB

UKR

HR

-12

-10

-8

-6

-4

-2

0

2

4

-30 -25 -20 -15 -10 -5 0 5

Cu

mu

lati

ve

ou

tpu

t d

rop

20

08

-10

Current acount deficit in 2008

Why countries are different Why countries are different Projected downturn increases with initial macro imb alancesProjected downturn increases with initial macro imb alances

Cumulative output drop 2008-10 vs. inflation rate i n 2008

Source: IMF, World Bank Staff calculations

BG

CZ

HU

PL

RO

SI

SK

IT

AT

ALB

BLR

BIH

MKD

MDA

MNE

SRB

UKR

HR

-12

-10

-8

-6

-4

-2

0

2

4

0 5 10 15 20 25 30

Cu

mu

lati

ve

ou

tpu

t d

rop

20

08

-10

Inflation rate in 2008

Why countries are different Why countries are different Size of domestic marketSize of domestic market

Merchandise Exports as % of GDP in 2008

Source: IMF IFS, IMF, World Bank

0

10

20

30

40

50

60

70

80R

O PL

BG SI

CZ

HU SK IT AT

ALB

MD

A

UK

R

MK

D

BLR

Why countries are different Why countries are different Monetary policyMonetary policy

Exchange Rates vs. Euro(Aug08 = 100)

Source: ECB. Reuters, World Bank Staff Calculations

80

90

100

110

120

130

140

150

160

170

180

Au

g-0

8

Sep

-08

Oct

-08

No

v-0

8

De

c-0

8

Jan

-09

Feb

-09

Ma

r-0

9

Ap

r-0

9

May

-09

Jun

-09

Jul-

09

Au

g-0

9

Sep

-09

Oct

-09

ALB

BLR

MDA

SRB

UKR

80

90

100

110

120

130

140

150

160

170

180

Au

g-0

8

Sep

-08

Oct

-08

No

v-0

8

De

c-0

8

Jan

-09

Feb

-09

Ma

r-0

9

Ap

r-0

9

May

-09

Jun

-09

Jul-

09

Au

g-0

9

Sep

-09

Oct

-09

CZ

HU

RO

PL

EU7 Other CEI

Why countries are different Why countries are different Monetary policyMonetary policy

Source: ECB. World Bank Staff Calculations

Real Effective Exchange Rates (Aug08 = 100)

70

80

90

100

110

120

Au

g-0

8

Sep

-08

Oct

-08

No

v-0

8

De

c-0

8

Jan

-09

Feb

-09

Ma

r-0

9

Ap

r-0

9

May

-09

Jun

-09

Jul-

09

MKD

HR

UKR

MDA

Why countries are different Why countries are different Fiscal policyFiscal policy

General Government Balance Percent of GDP

Source: IMF WEO

-10

-8

-6

-4

-2

0

2

4

EU

15

EU

7

Oth

er C

EI

BG CZ

HU PL

RO S

I

SK

ALB

BLR

BIH

MK

D

MD

A

MN

E

SR

B

UK

R

HR

2008

2009

2010

EU7 Other CEI

What we can expectWhat we can expect

What we can expectWhat we can expectGrowth Growth –– slow recoveryslow recovery

Source: IIMF WEO

-10

-8

-6

-4

-2

0

2

4

6

8

10

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

EU7

EU15

Other CEI

What we can expectWhat we can expectCurrent account balance Current account balance –– improvingimproving

Percent of GDP

Source: IMF WEO

-35

-30

-25

-20

-15

-10

-5

0

5

10

BG CZ

HU PL

RO S

I

SK IT AT

AL

B

BLR

BIH

MK

D

MD

A

MN

E

SR

B

UK

R

HR

2008 2009 2010

What we can expectWhat we can expect

Poverty and vulnerabilityPoverty and vulnerabilityPercentage Point Change in Poverty and Vulnerabilit y 2010

(In percent of the population; most recent versus p re-crisis growth projection)

Source: The Crisis Hits Home - Stress Testing Househ olds in Europe and Central Asia, World Bank

THANK YOU!THANK YOU!