CEDS 2010 Update

37

Texoma Comprehensive Economic Development Strategy 2010 Annual Update

-

Upload

tcog-community-economic-development -

Category

Documents

-

view

221 -

download

0

Transcript of CEDS 2010 Update

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 1/37

TexomaComprehensive

Economic

Development Strategy2010 Annual Update

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 2/37

Page 1 of 37

ContentsI. BACKGROUND ............................................................................................................................................ 2

Program Coordination .............................................................................................................................. 3

II. REGIONAL ANALYSIS ................................................................................................................................. 4

Population ................................................................................................................................................. 4

Industry and Occupation ........................................................................................................................... 7

Targeted Industries and Occupations ................................................................................................... 7

Baseline Cluster Analysis ..................................................................................................................... 12

Business Environment ............................................................................................................................. 18

Texoma Innovation Index and Analysis............................................................................................... 19

Workforce ............................................................................................................................................... 25

Skill Needs for Available, Critical, and Projected Jobs ........................................................................ 25

Key Trends ........................................................................................................................................... 27

III. PROGRESS REPORT ................................................................................................................................. 29

Ongoing Regional Projects .................................................................................................................. 30

Recent Successes .................................................................................................................................... 30

EDA Awards......................................................................................................................................... 30

Other Achievements in Economic Development ................................................................................. 31

IV. SCOPE OF WORK FOR 2010 ................................................................................................................... 33

Appendix A. ................................................................................................................................................. 34

EDA Distress Criteria- TEXOMA Statistical Report .................................................................................. 34

Economic Distress Criteria- Primary Elements .................................................................................... 34

Economic Distress Criteria- Geographic Components ........................................................................ 34

Appendix B. ................................................................................................................................................. 35

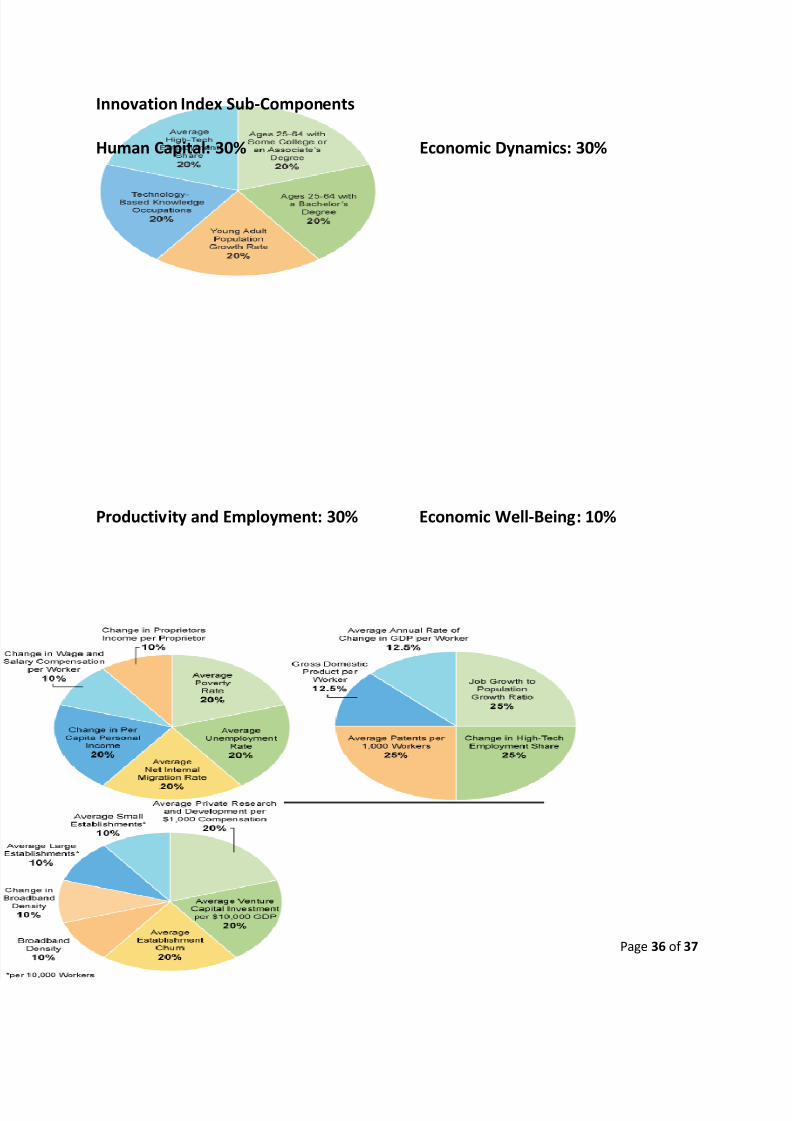

Innovation Index Methodology .................................................................................................................. 35

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 3/37

Page 2 of 37

I. BACKGROUND

Texoma Council of Governments (TCOG) is the EDA-designated Economic Development District

(EDD) for Cooke, Fannin, and Grayson Counties. The purpose of an EDD is to engage in the full

range of economic development activities listed and described in a region’s EDA-approved

Comprehensive Economic Development Strategy (CEDS). Activities include coordinating andimplementing economic development activities in the District, carrying out economic

development research, planning, implementation and advisory functions identified in the CEDS,

and coordinating the development and implementation of the CEDS with a District’s respective

local, State, federal and private organizations.

CEDS emphasizes regionalism as a key factor in the way communities should approach their

respective economic development efforts. In today’s global economy, communities maximize

their economic development efforts with collaborative partnerships with neighboring

communities to pool information and resources. When one community succeeds in its

economic development efforts impacts are felt not only in that community, but throughout thecounty and surrounding counties in the region.

Building strong economies takes decades. Economic development is a broad concept that

encompasses a varying range of definitions and activities. Economic strength is often measured

in terms of business retention and expansion and job creation and therefore defined by the

latest statistic reflecting a community’s business environment or unemployment rate. However,

improvements in a community’s infrastructure, education, and housing over time are

considered to be activities positive for future economic development though they are not

always directly associated with business retention and expansion or job creation outcomes. In

order to leverage the full potential of a regional economy, stakeholders and community leaders

should engage in long-term planning that guides strategies for investments based on eachcommunity’s unique mix of assets.

In 2007, TCOG, serving in its capacity as the Texoma EDD, and the TCOG Economic

Development Policy Advisory Board (EDPAC), collected input from the region’s communities

and drafted the 2007- 2012 Texoma CEDS that identified key issues and goals for economic

development in Texoma. This document, will address the goals and projects identified in the

2007- 2012 CEDS, outline recent economic development activities, provide a brief regional

economic analysis by including recent regional planning effort’s conclusions and surveys, and

define the scope of work for TCOG and regional economic development stakeholders in 2009.

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 4/37

Page 3 of 37

Program Coordination

The Texoma Economic Development District (EDD) coordinates economic development

activities in the three-county Texoma region. All three counties have elected to be part of the

district’s organization and programming. The EDD provides information about economic

development strategy and initiatives, sources of funds for businesses and public agencies, andcommunity data when requested.

The CEDS is coordinated by staff at the Texoma Council of Governments (TCOG) with input from

its Board of Directors, members, timely and significant research and analysis reports as noted in

the appendices, and information from the counties‘, municipalities‘, and special districts‘

comprehensive plans and infrastructure capital improvement plans. The Council of

Governments also contacted area specialists in the fields of downtown revitalization,

education, economic development and workforce development.

In addition to local government efforts, TCOG has initiated a number of economic development

training seminars designed for local officials and economic development practitioners. These

training seminars have focused on the rules and regulations regarding sales tax for economic

development in Texas.

The name and address of the local contact is:

Texoma Council of Governments

Ryan Gleason, Community Development Director

1117 Gallagher Drive Suite 300

Sherman, Texas 75090

Voice: (903) 813-3520Fax: (903) 813-3539

To obtain a copy of the 2010-2011 CEDS Annual Update, please contact TCOG’s Economic

Development Office at (903) 813-3523.

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 5/37

Page 4 of 37

2

4

6

8

10

2000 2007 2008 Dec-09

Seasonally Adjusted

Unemployment Rates

Cooke

Fannin

Grayson

Texas

US

Source: TRACER

2000 2006 2008

Cooke 36,363 38,355 38,407

Fannin 31,242 32,991 33,229

Grayson 110,595 117,900 118,804

0

20

40

60

80

100

120

140

P o p u l a t i o n (

1 , 0

0 0 )

Texoma Population by County

II. REGIONAL ANALYSIS Population

Although there has been a greatdeal of discussion in Texoma

concerning population growth

associated with the northern

suburban sprawl of the Dallas-

Fort Worth (DFW) Metroplex,

Texoma has not experienced

significant changes in

population. The only exceptions

are perhaps the communities

closest to Collin County, such as

Tioga and Van Alstyne. As seen inFigure 1 the region’s most

populous county is Grayson.

Growth has remained fairly

constant since 2000 throughout

the region, with most of

Texoma’s population growth in the last ten years concentrated in Grayson County.

In 2007, the American economy

began to slow significantly,

mostly because of a real-estateslump and related financial

problems. In December 2007,

the economy entered a

recession, according to a

committee of academic

economists, overseen by the

National Bureau of Economic

Research, which is widely

considered the arbiter of

recessions.Figure 2. Source: LCMI Tracer, Texas Workforce Commission

Figure 1. Source: Decennial Census and American Community Survey.

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 6/37

Page 5 of 37

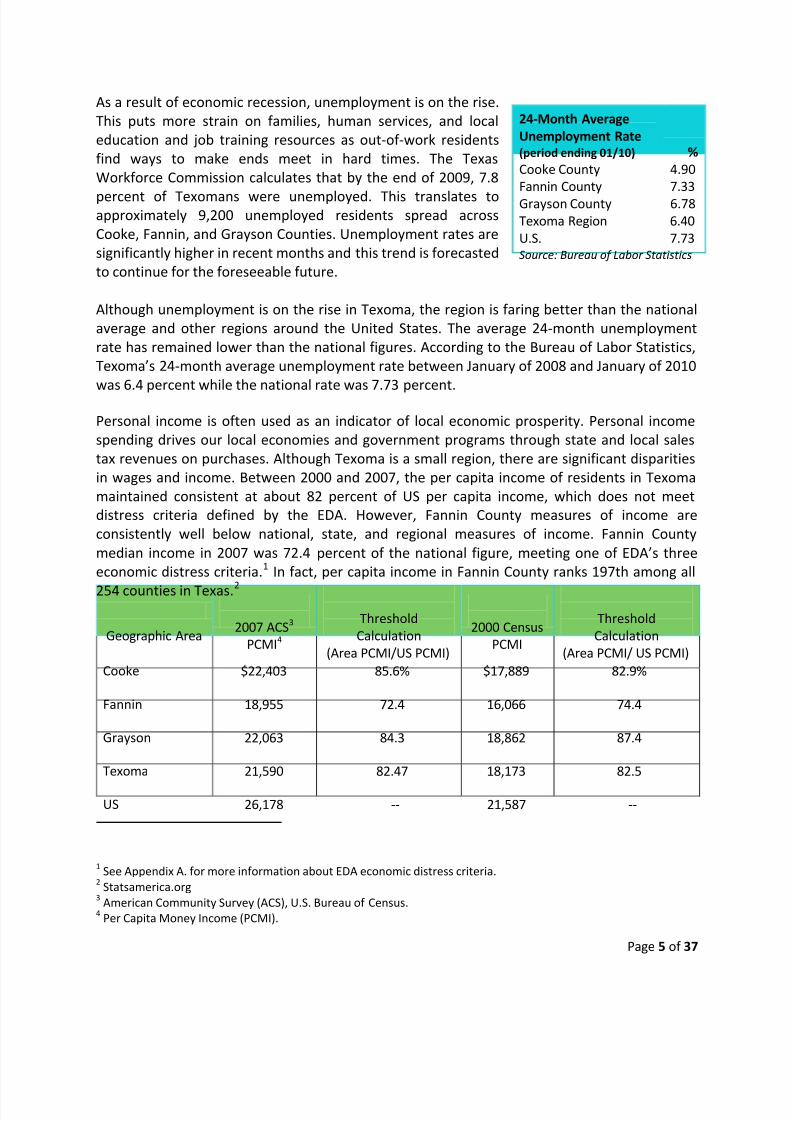

As a result of economic recession, unemployment is on the rise.

This puts more strain on families, human services, and local

education and job training resources as out-of-work residents

find ways to make ends meet in hard times. The Texas

Workforce Commission calculates that by the end of 2009, 7.8

percent of Texomans were unemployed. This translates toapproximately 9,200 unemployed residents spread across

Cooke, Fannin, and Grayson Counties. Unemployment rates are

significantly higher in recent months and this trend is forecasted

to continue for the foreseeable future.

Although unemployment is on the rise in Texoma, the region is faring better than the national

average and other regions around the United States. The average 24-month unemployment

rate has remained lower than the national figures. According to the Bureau of Labor Statistics,

Texoma’s 24-month average unemployment rate between January of 2008 and January of 2010

was 6.4 percent while the national rate was 7.73 percent.

Personal income is often used as an indicator of local economic prosperity. Personal income

spending drives our local economies and government programs through state and local sales

tax revenues on purchases. Although Texoma is a small region, there are significant disparities

in wages and income. Between 2000 and 2007, the per capita income of residents in Texoma

maintained consistent at about 82 percent of US per capita income, which does not meet

distress criteria defined by the EDA. However, Fannin County measures of income are

consistently well below national, state, and regional measures of income. Fannin County

median income in 2007 was 72.4 percent of the national figure, meeting one of EDA’s three

economic distress criteria.1

In fact, per capita income in Fannin County ranks 197th among all

254 counties in Texas.2

1See Appendix A. for more information about EDA economic distress criteria.

2Statsamerica.org

3American Community Survey (ACS), U.S. Bureau of Census.

4Per Capita Money Income (PCMI).

24-Month Average

Unemployment Rate(period ending 01/10) %

Cooke County 4.90

Fannin County 7.33

Grayson County 6.78

Texoma Region 6.40

U.S. 7.73Source: Bureau of Labor Statistics

Geographic Area2007 ACS3

PCMI4

Threshold

Calculation

(Area PCMI/US PCMI)

2000 Census

PCMI

Threshold

Calculation

(Area PCMI/ US PCMI)

Cooke $22,403 85.6% $17,889 82.9%

Fannin 18,955 72.4 16,066 74.4

Grayson 22,063 84.3 18,862 87.4

Texoma 21,590 82.47 18,173 82.5

US 26,178 -- 21,587 --

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 7/37

Page 6 of 37

Wages and income in Texoma

continue to remain below national

averages, but the local effects are

positively complimented by lower cost

of living. Since 2000, regional percapita income has declined slightly in

comparison to national wage trends.

In 2000, the decennial census

measured per capita income in Texoma at $18,173, which is 84.18 percent of national per

capita income, and in 2007, the American Community Survey reported per capita income in

Texoma at $21,590, or 82.47 percent of the national per capita income. The median value of

homes in the three counties in Texoma remains well below the national and state median home

values.

The Economic Development Administration (EDA) determines eligibility and investment rates of

applicants based upon defined measures of economic distress. An applicant’s eligibility is

primarily based up their ability to demonstrate that the geographic area of impact of the

proposed project has, (1) an unemployment rate for the most recent twenty four month period

for which data is available that is at least one percentage point greater than the national

average, (2) per capita income that is eighty percent or less of the national average per capita

income, (3) a designation as a Special Impact Area by EDA.6 EDA requests that applicants

provide the latest data available in the proposed project ’s region or area of impact. Economic

distress data for each county in Texoma is provided in appendix A.

5Median House Value (MHV)

6EDA may designate a Special Impact Area if an applicant presents the appropriate data that a project serves a

region, or area of a region that: (1) Has a unique or urgent circumstance that would necessitate waiver of the CEDS

requirements, (2) Involves a project undertaken by an Indian Tribe, (3) Is rural and severely distressed, (4) Is

undergoing a transition in its economic base as a result of changing trade patterns, (5) Exhibits a substantial

reliance on a natural resource for its economic well-being, or (6) Has been designated as a Federally-Declared

Disaster area.

2007 MHV5

In $

% of National MHV5

Cooke $109,600 60.5%

Fannin 75, 400 41.7

Grayson 91,100 50.3

U.S. 181,000 --Source: ACS 2006-2008

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 8/37

Page 7 of 37

Industry and Occupation

Industry and occupational analyses provide insights into the foundation of a region’s

competitive advantages. Understanding a region’s key industries and high-demand occupations

help economic development practitioners and local policy makers see how firms fit into the

local economy so they may make informed decisions about local development initiatives.

This section provides information about the targeted industries and occupations of Workforce

Solutions Texoma (WST), our region’s local workforce board, and a baseline industry and

occupational cluster analysis generated by statsamerica.org, an EDA-funded online economic

analysis tool. Each source provides useful information about key areas of growth and decline

while utilizing different methodologies.

Targeted Industries and Occupations

In order to most efficiently target workforce and business needs in Texoma, Workforce

Solutions Texoma develops a list of targeted industries and occupations. WST focuses theirservices on these areas because they are high-growth or high-demand industries in which

residents seeking employment are most likely to become employed at a livable wage. WST

developed this list of targeted industries and occupations by consulting both regional leaders

and the rich market data provided by the Labor Market and Career Information (LMCI), a

division of the Texas Workforce Commission (TWC).

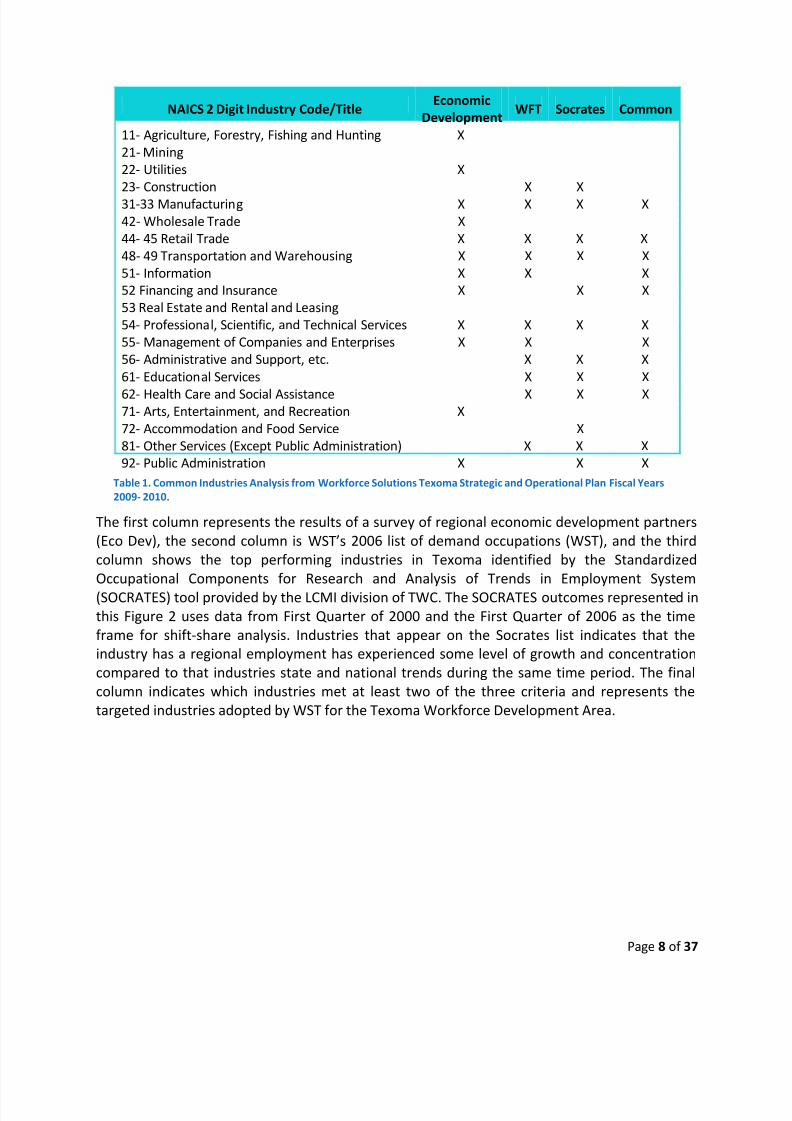

Workforce Texoma talked with local economic development organizations to determine which

industries they are currently targeting. Economic Development Corporations take direction

from their respective city councils and therefore, the industries they are targeting have been

adopted in conjunction with their city’s strategic planning. In order to develop a comprehensivelist of industries from which to begin the targeting analysis, Workforce Texoma utilized three

existing lists, the North American Industry Classification System (NAICS), Texas Governor Rick

Perry’s Industry Cluster Initiative, and Ray Perryman’s list of targeted industries in his report

Texas Our Texas. A crosswalk was developed in order to align the three lists. Economic

developers were asked to indicate which industries on the NAICS and Perry lists they are

targeting. In addition to the input provided by the economic development partners, the

occupations included on Workforce Texoma’s current Demand Occupations List were

integrated into the crosswalk to more fully analyze the industries the Workforce Board should

prioritize.

Figure 2 illustrates the results of the crosswalk analysis and charts which NAICS industries were

identified or targeted by at least two of the three methods of analysis.

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 9/37

Page 8 of 37

The first column represents the results of a survey of regional economic development partners

(Eco Dev), the second column is WST’s 2006 list of demand occupations (WST), and the third

column shows the top performing industries in Texoma identified by the Standardized

Occupational Components for Research and Analysis of Trends in Employment System

(SOCRATES) tool provided by the LCMI division of TWC. The SOCRATES outcomes represented in

this Figure 2 uses data from First Quarter of 2000 and the First Quarter of 2006 as the time

frame for shift-share analysis. Industries that appear on the Socrates list indicates that the

industry has a regional employment has experienced some level of growth and concentration

compared to that industries state and national trends during the same time period. The final

column indicates which industries met at least two of the three criteria and represents the

targeted industries adopted by WST for the Texoma Workforce Development Area.

NAICS 2 Digit Industry Code/TitleEconomic

DevelopmentWFT Socrates Common

11- Agriculture, Forestry, Fishing and Hunting X

21- Mining

22- Utilities X

23- Construction X X

31-33 Manufacturing X X X X

42- Wholesale Trade X

44- 45 Retail Trade X X X X

48- 49 Transportation and Warehousing X X X X

51- Information X X X

52 Financing and Insurance X X X

53 Real Estate and Rental and Leasing

54- Professional, Scientific, and Technical Services X X X X

55- Management of Companies and Enterprises X X X

56- Administrative and Support, etc. X X X

61- Educational Services X X X

62- Health Care and Social Assistance X X X71- Arts, Entertainment, and Recreation X

72- Accommodation and Food Service X

81- Other Services (Except Public Administration) X X X

92- Public Administration X X X

Table 1. Common Industries Analysis from Workforce Solutions Texoma Strategic and Operational Plan Fiscal Years

2009- 2010.

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 10/37

Page 9 of 37

Texoma Area Targeted Industries

After analyzing the results of the input from the economic development partners, current list of

demand occupations, and the information provided by SOCRATES, the following list of targeted

industries, based on two-digit NAICS codes, was adopted for the Texoma Workforce

Development Area (Cooke, Fannin, and Grayson Counties):

Construction

The Texoma Area has seen an active commercial and residential construction trade for a

number of years. Continued retail development will continue to keep commercial

construction brisk, and the 2005 announcement of more than 2,000 jobs with Ruiz

Foods and the opening Tyson Fresh Meats in Sherman in 2006. New construction jobs

are on the horizon should Panda Energy International Inc. obtain the air permit and

follow through with plans to develop a 500-MW combined-cycle natural gas power plant

in Sherman.

Manufacturing – including Advanced Manufacturing and Aerospace and Defense

Even though a large number of the jobs lost locally were in manufacturing, the Texoma

region has a reputation of a strong work ethic consistent with the needs of

manufacturers. All of the local economic developers are currently targeting

manufacturing, and the local airport plays a major role in the future of the area.

Retail Trade

The addition of a major retail development is Grayson County has provided

approximately 1,000 new jobs in recent years. The retail sector has always been ademand sector, but pressure from newly created manufacturing jobs is causing retail

wages to go up.

Transportation and Warehousing

Truck driving has traditionally been a good occupation for Workforce Texoma

customers. Increased traffic into the area based on new manufacturing locations may

provide additional opportunities in this sector.

Information – including Information and Computer Technology

One of Texoma’s largest sectors of the manufacturing industry is in semiconductors with

companies including Texas Instruments, MEMC Southwest, and GlobiTech, Inc. Although

these industries have historically provided many, well-paying jobs in Texoma, they are in

decline with numerous plant closures and reductions in workforce.

Professional, Scientific, and Technical Services

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 11/37

Page 10 of 37

With the continued emphasis on Manufacturing, and particularly with the emerging

focus on advanced manufacturing, drafters will continue to be in demand. The Area is

also interested in attracting research and development.

Educational Services

The Texoma Area is home to 34 independent school districts with a combined annual

enrollment of almost 33,000 students. Teaching is a good occupational choice.

Health Care and Social Assistance

Two of Texoma’s largest employers are Wilson N. Jones Memorial Hospital in Sherman

and Texoma Medical Center in Denison. With more than 1,000 employees each, these

two hospitals offer ongoing employment opportunities in the healthcare field. TMC

recently opened a new hospital facility that includes more beds, surgery rooms, andmore emergency and trauma beds.

Other Services (except Public Administration)

Automotive and diesel mechanics are included in this NAICS category. Texoma has a

thriving automotive market and a number of dealerships offering opportunities for

trained mechanics.

Texoma Targeted Occupations

The Labor Market and Career Information (LMCI) division of the Texas Workforce Commission(TWC) recently released occupational projections through 2012. This study presented

information including: Occupations Adding the Most Jobs, Fastest Growing Occupations,

Occupations with the Most Annual Average Openings. The historical makeup and current trends

in the local labor market support this list. A number of the jobs included in this list are also

included in the current Workforce Texoma Demand Occupations List.

After developing the list of Occupations in Demand, the list was sorted by wage, and those

occupations with an average entry wage greater that the Texoma adopted Target Wage of

$9.00 per hour were placed on the DRAFT Target Occupations List. This list was then compared

with the previous target occupations list, and local training programs to create the final

Targeted Occupations List.

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 12/37

Page 11 of

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 13/37

Page 12 of 37

Baseline Cluster Analysis

Cluster analyses of industry and occupation networks are a relatively new approach in regional

development that focuses on the knowledge, skills and abilities of the individuals who work in

certain jobs. A cluster is a network of industries, people, and organizations in close geographic

proximity.

This cluster analysis provides fast insights into the talent base that drives a local or regional

economy. With this tool, economic development professionals can begin to structure effective

collaborations with businesses managers, educators, and workforce development

professionals. This baseline cluster analysis must be paired with a discussion of the unique

characteristic of firms that make up these clusters in our region in order to understand the

nuanced relationships that create Texoma’s economic base. Two clusters, referred to by the

same label, in different regions will vary in their actual industry composition according to their

“base” industry, industry mix and degree of industrial diversification, anchoring firms, ancillary

and supporting industries, integral organizations, informal (i.e., “know-how sharing”)arrangements and critical growth poles.

This type of analysis is useful in a number of different ways. By understanding the dynamics of

growth within a cluster, an economic development professional can communicate more

effectively with educators and workforce development professionals to build a talent pipeline

needed to support businesses in Texoma. The baseline occupational and industry cluster

analyses provided in this section measure characteristics of clusters over time. The information

provided is simply a point-in-time analysis of existing clusters in Texoma. Further study should

be done to identify clusters that are at-risk, emerging, or have the potential for future growth.

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 14/37

Page 13 of 37

Texoma Occupation Clusters

Working with occupational data can quickly become overwhelming, so to simplify analysis and

aid in understanding, the tool focuses on fifteen knowledge-based occupation clusters.

Occupation clusters help to analyze the regional knowledge-based workforce in greater detail,

determine how well occupation cluster strengths align with the region’s industry clusterstrengths, understand the local workforce and educational situation within the broader regional

economic development context, bridge the gap between workforce and economic

development when constructing a regional economic development strategy, diagnose how well

positioned the region is to participate effectively in a knowledge-based innovation economy.

The following chart illustrates the number of jobs in each cluster, the cluster’s share of total

regional employment, and the location quotient of the cluster (a measurement of how

concentrated that cluster is in Texoma compared to the nation.

The table below looks at Texoma and identifies those occupations with the strongest

percentage change and the largest increase in the number of jobs from 2001 to 2007. Agents

and business managers of artists, performers, and athletes had the largest percentage change,

but that occupational segment is relatively small. Photographers represent the largest growth

category in absolute terms, with 99 new jobs added in that occupational category.

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 15/37

Page 14 of 37

Texoma Baseline Occupational Cluster Analysis (2007)

Description Occupation ClusterEmployment

Occ. Cluster Share of Total Emp.

Occupation ClusterEmployment LQ

Managerial, Sales, Marketing and HR 7,235 7.3% 0.87

Skilled Production Workers: Technicians, Operators, Trades,

Installers & Repairers

9,115 9.2% 1.22

Health Care and Medical Science (Aggregate) 4,918 5.0% 0.94

Health Care and Medical Science (Medical Practitionersand Scientists)

912 0.9% 0.77

Health Care and Medical Science (Medical Technicians) 902 0.9% 0.86

Health Care and Medical Science (Therapy, Counseling

and Rehabilitation )

3,105 3.1% 1.04

Mathematics, Statistics, Data and Accounting 1,405 1.4% 0.61

Legal and Financial Services, and Real Estate (L & FIRE) 6,505 6.6% 0.81

Information Technology (IT) 1,189 1.2% 0.62

Natural Sciences and Environmental Management 425 0.4% 0.97

Crop and Livestock Workers 6,677 6.8% 4.49

Primary/Secondary and Vocational Education, Remediation

& Social Services

5,434 5.5% 1.07

Building, Landscape and Construction Design 495 0.5% 1.00

Engineering and Related Sciences 965 1.0% 0.96

Personal Services Occupations 1,642 1.7% 0.85

Arts, Entertainment, Publishing and Broadcasting 1,309 1.3% 0.66

Public Safety and Domestic Security 1,326 1.3% 1.18

Postsecondary Education and Knowledge Creation 932 0.9% 0.76

Job Zone 2 33,867 34.3% 0.99

Job Zone 1 14,603 14.8% 0.99

Technology-Based Knowledge Clusters 5,828 5.9% 0.72

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 16/37

Page 15 of 37

Texoma Industry Clusters

The industry cluster analysis helps the practitioner to see networks of businesses that are

creating wealth in their local or regional economy. The tool focuses on seventeen clusters

across the United States in order to provide a framework that is easy to understand. It also

allows users to combine individual counties to define custom regions.

Close geographic proximity and engagement in similar or related economic activities are the

key factors leading to development of clusters. These characteristics enhance the likelihood of

exchanges among cluster firms, facilitating mutual support, and economic growth. “When

members of a cluster are located in close proximity, they can capture synergies that increase

productivity, innovative capacity and new business formation.”7

The linkages between spatial

proximity and innovation potential are particularly important from a regional development

perspective. In particular, supportive policies and a nurturing business environment may

further strengthen the innovative milieu and thus enhance regional advantages.

Industry clusters help to describe how industries in a region compare to each other, identify

growth trends through regional location quotient analysis, reveal emerging industries in a

region, analyze the mix of clusters in a diverse region that might include both rural and urban

areas, rethink business expansion strategies, reveal groups of industries that have similar

workforce needs, prioritize groups of firms that have growth potential, and create regional

identities and improve marketing effectiveness.

On average, U.S. counties specialize in slightly more than two industry clusters (LQ > 1.2,

meaning that the cluster’s share of employment in the county is at least 20 percent higher than

the cluster’s share of employment nationally).8

With data provided by this tool, users can create a matrix to show industry employment

location quotients for each county in the region and for the region as a whole. This matrix

enables practitioners to see the overall competitive strengths of the region’s economy.

However, cluster analysis must be used judiciously because it relies upon historical data, and

the past is not a perfect predictor for the future. For example, a region currently specialized in a

particular cluster may not have a bright future if the national and global outlook for that cluster

is one of decline.

7Porter, M. 2001. Clusters of innovation: Regional foundations of U.S. Competitiveness. Available from

http://www.usistf.org/download/documents/Clusters-of-Innovation/Clusters-of-Innovation.pdf . 8 Unlocking Rural Competitiveness: The Role of Regional Clusters. Available from

http://www.statsamerica.org/innovation/reports/trifold_single_pages.pdf .

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 17/37

Page 16 of 37

Texoma Baseline Industry Cluster Analysis (2008)9 Description QCEW10 Cluster-

Establishments Industry ClusterEstablishmentsLQ11

QCEW ClusterEmployment Industry Cluster

Employment LQ QCEW ClusterWages Industry

ClusterAnnualWages LQ

Total, All Industries 4184 1.00 65,955 1.00 $2,384,881,506 1.00 Advanced Materials 86 1.32 564 0.22 $23,457,140 0.18Agribusiness, FoodProcessing

156 2.34 915 0.59 $38,446,998 0.85

Apparel & Textiles 27 0.71 12 0.02 $315,487 0.02Arts, Entertainment,Recreation & VisitorIndustries

120 0.98 963 0.37 $22,138,936 0.31

Biomedical/ Biotechnical(Life Sciences) 408 4.01 4,106 1.81 $170,190,906 1.82

Business & FinancialServices 536 0.83 3,005 0.52 $121,079,033 0.32

Chemicals & ChemicalBased Products 49 1.51 1,223 1.10 $51,555,838 0.99

Defense & Security 106 0.76 982 0.30 $45,655,682 0.28Education & KnowledgeCreation 79 0.87 5,873 0.93 $193,101,943 0.91

Energy (Fossil &Renewable) 402 1.46 4,590 1.16 $210,816,846 1.02

Forest & Wood Products 76 0.84 787 0.65 $28,440,922 0.69

Glass & Chemicals 15 1.49 55 0.21 $2,489,080 0.26Information Technology &Telecommunications 150 0.75 736 0.24 $30,848,206 0.16

Transportation & Logistics 101 1.07 1,283 0.66 $58,564,270 0.84ManufacturingSupercluster 125 1.94 6,061 1.92 $376,155,484 2.43

9A list of the detailed six-digit NAICS definitions for each of the 17 industry clusters is available from

http://www.statsamerica.org/innovation/reports/sections/appendix_I.pdf . 10

Quarterly Census of Employment and Wages (QCEW)11

Location Quotient (LQ)

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 18/37

Page 17 of 37

Primary Metal Mfg 8 2.88 442 2.04 $20,192,759 2.02Fabricated Metal ProductMfg 62 2.20 1,692 2.25 $66,996,159 2.36

Machinery Manufacturing 22 1.57 649 1.12 $37,947,017 1.45Computer & ElectronicProduct Mfg 13 1.48 1,363 2.24 $172,809,560 4.23

Electrical Equipment,Appliance & ComponentMfg

2 0.59 0 0.00 $0 0.00

Transportation EquipmentMfg 18 2.52 1,917 2.39 $78,209,989 1.94

Mining 8 1.44 0 0.00 $0 0.00Printing & Publishing 65 0.71 295 0.23 $10,331,495 0.17

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 19/37

Page 18 of 37

Business Environment

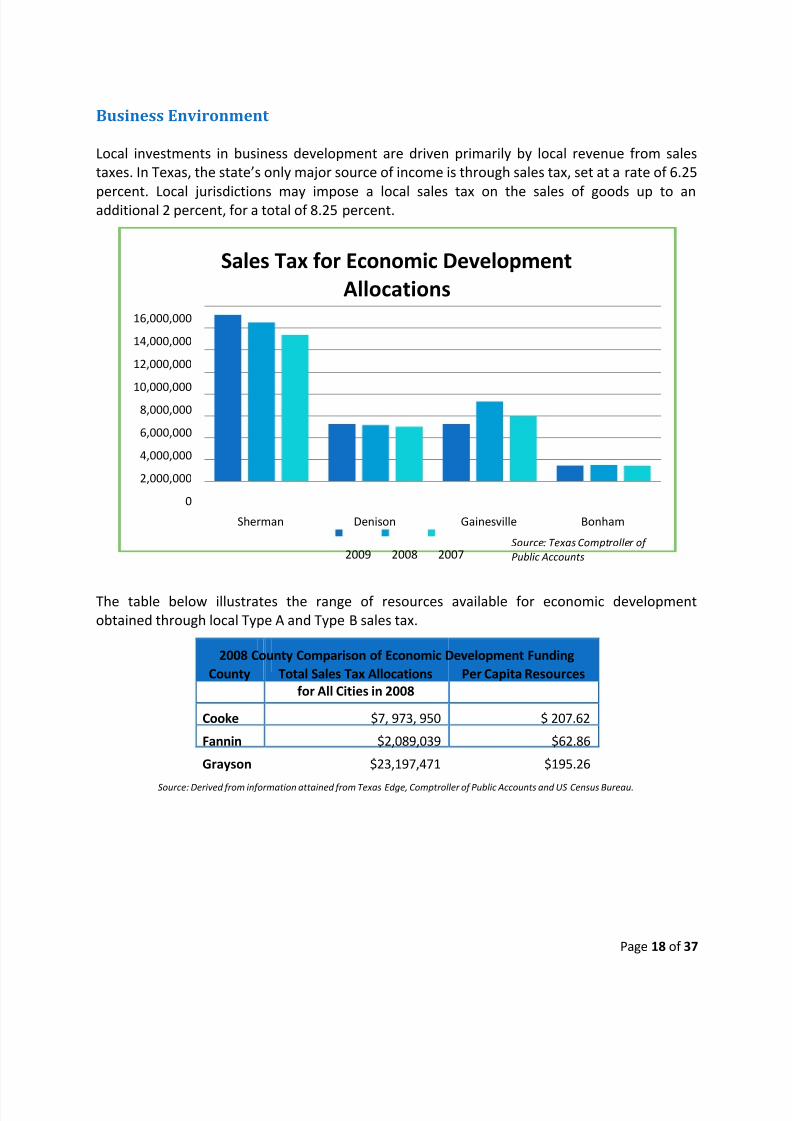

Local investments in business development are driven primarily by local revenue from sales

taxes. In Texas, the state’s only major source of income is through sales tax, set at a rate of 6.25

percent. Local jurisdictions may impose a local sales tax on the sales of goods up to anadditional 2 percent, for a total of 8.25 percent.

The table below illustrates the range of resources available for economic development

obtained through local Type A and Type B sales tax.

2008 County Comparison of Economic Development Funding

County Total Sales Tax Allocations

for All Cities in 2008

Per Capita Resources

Cooke $7, 973, 950 $ 207.62

Fannin $2,089,039 $62.86

Grayson $23,197,471 $195.26

Source: Derived from information attained from Texas Edge, Comptroller of Public Accounts and US Census Bureau.

0

2,000,000

4,000,000

6,000,000

8,000,00010,000,000

12,000,000

14,000,000

16,000,000

Sherman Denison Gainesville Bonham

Sales Tax for Economic Development

Allocations

2009 2008 2007Source: Texas Comptroller of

Public Accounts

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 20/37

Page 19 of 37

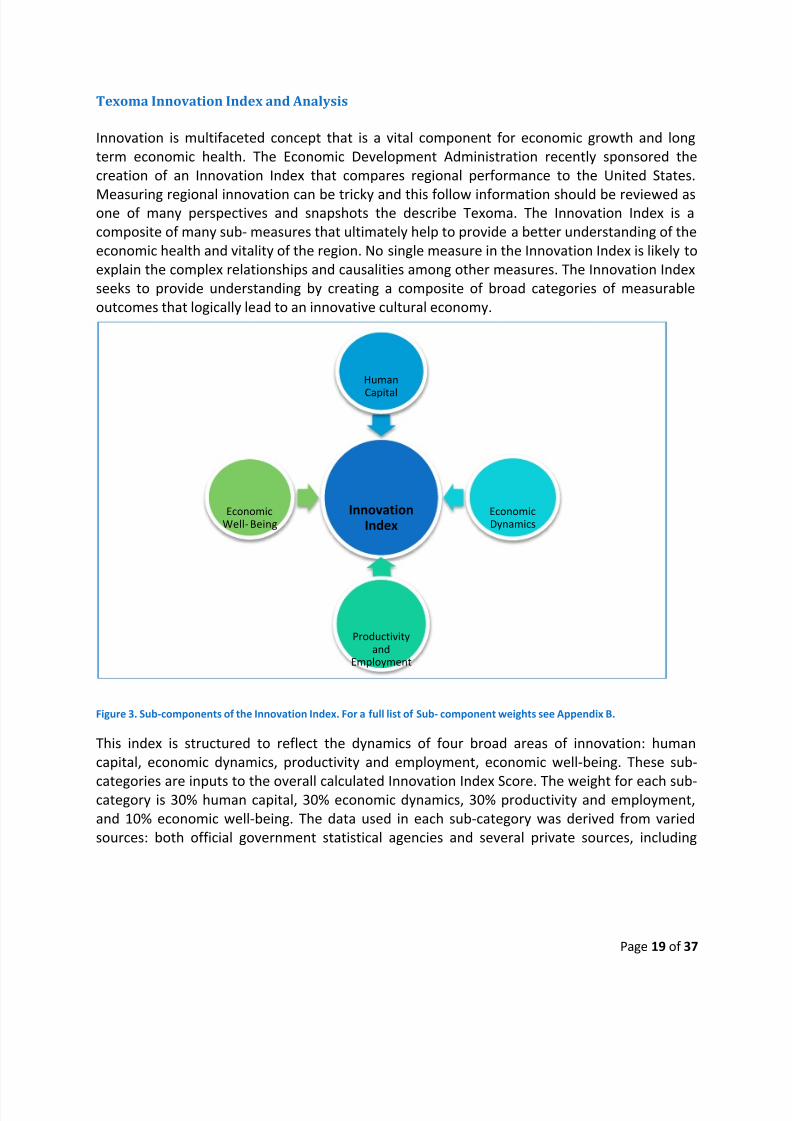

Texoma Innovation Index and Analysis

Innovation is multifaceted concept that is a vital component for economic growth and long

term economic health. The Economic Development Administration recently sponsored the

creation of an Innovation Index that compares regional performance to the United States.

Measuring regional innovation can be tricky and this follow information should be reviewed asone of many perspectives and snapshots the describe Texoma. The Innovation Index is a

composite of many sub- measures that ultimately help to provide a better understanding of the

economic health and vitality of the region. No single measure in the Innovation Index is likely to

explain the complex relationships and causalities among other measures. The Innovation Index

seeks to provide understanding by creating a composite of broad categories of measurable

outcomes that logically lead to an innovative cultural economy.

Figure 3. Sub-components of the Innovation Index. For a full list of Sub- component weights see Appendix B.

This index is structured to reflect the dynamics of four broad areas of innovation: human

capital, economic dynamics, productivity and employment, economic well-being. These sub-

categories are inputs to the overall calculated Innovation Index Score. The weight for each sub-category is 30% human capital, 30% economic dynamics, 30% productivity and employment,

and 10% economic well-being. The data used in each sub-category was derived from varied

sources: both official government statistical agencies and several private sources, including

InnovationIndex

Human

Capital

EconomicDynamics

Productivityand

Employment

EconomicWell- Being

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 21/37

Page 20 of 37

Moody’s economy.com, Innovation Economy 360, and Economic Modeling Specialists, Inc.

(EMSI).12

In updated research using a descriptive cross-sectional regression model, the research team

found that the following indicators have a positive and significant relationship to increases in

GDP per worker:

1. Change in high-tech employment share

2. Average small establishments per 10,000 workers

3. Percent of population, ages 25-64, with some college or an associate’s degree

4. Population growth rate for ages 25-44

The Innovation Index is designed to highlight factors that indicate a region is more or less ready

to participate in the knowledge economy. The index is not by itself intended to directly guide

decisions about investments in the region as the data used to calculate the analysis may not be

the latest available and, therefore, unable to reflect recent events in Texoma.

Interpreting the Innovation Index (also referred to as the portfolio index) can get complex given

its broad, multi-metric nature with both innovation inputs and outputs. In order to identify

those specific factors with the greatest influence on economic growth, while controlling for

some non-innovation factors, the Innovation Index research team statistically analyzed the

innovation input data. Interpreting the results is simpler than the portfolio approach because

there is only one output measure―economic growth (i.e., GDP-per-worker growth).

12A complete list of calculations, models, and definitions used in the Texoma Innovation Index is available from

http://www.statsamerica.org/innovation/reports/sections2/C.pdf .

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 22/37

Page 21 of 37

75 80 85 90 95 100

Texoma

Texas

Oklahoma

U.S.

86.6

94.2

83.7

100

Texoma Texas Oklahoma U.S.

Innovation Score86.6 94.2 83.7 100

Innovation Index

80 85 90 95 100 105

Texoma

Texas

Oklahoma

U.S.

92.3

100.4

89.9

100

Human Capital Sub-Component

Human Capital Index

Score

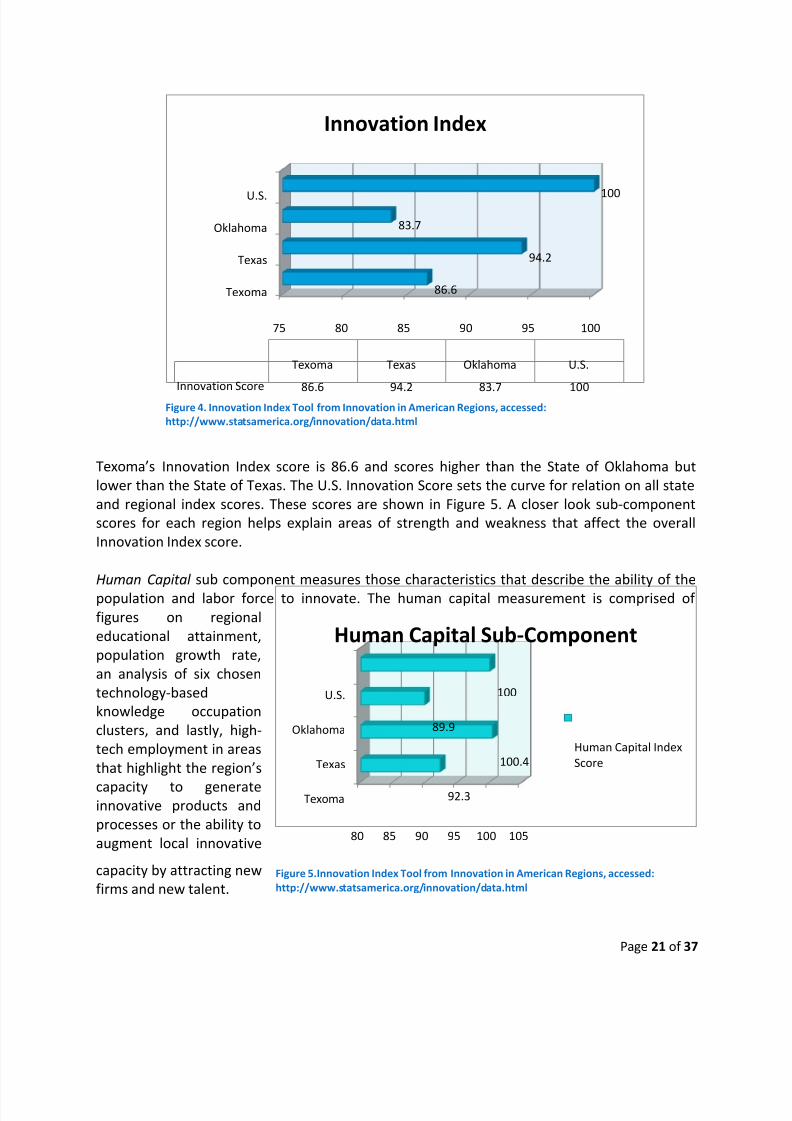

Texoma’s Innovation Index score is 86.6 and scores higher than the State of Oklahoma but

lower than the State of Texas. The U.S. Innovation Score sets the curve for relation on all state

and regional index scores. These scores are shown in Figure 5. A closer look sub-component

scores for each region helps explain areas of strength and weakness that affect the overall

Innovation Index score.

Human Capital sub component measures those characteristics that describe the ability of the

population and labor force to innovate. The human capital measurement is comprised of

figures on regional

educational attainment,

population growth rate,

an analysis of six chosen

technology-based

knowledge occupation

clusters, and lastly, high-

tech employment in areas

that highlight the region’s

capacity to generateinnovative products and

processes or the ability to

augment local innovative

capacity by attracting new

firms and new talent.

Figure 4. Innovation Index Tool from Innovation in American Regions, accessed:

http://www.statsamerica.org/innovation/data.html

Figure 5.Innovation Index Tool from Innovation in American Regions, accessed:

http://www.statsamerica.org/innovation/data.html

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 23/37

Page 22 of 37

0 50 100

Texoma

Texas

Oklahoma

U.S.

79.9

83.8

73.7

100

Economic Dynamics

Sub-Component

Economic Dynamics

Index Score

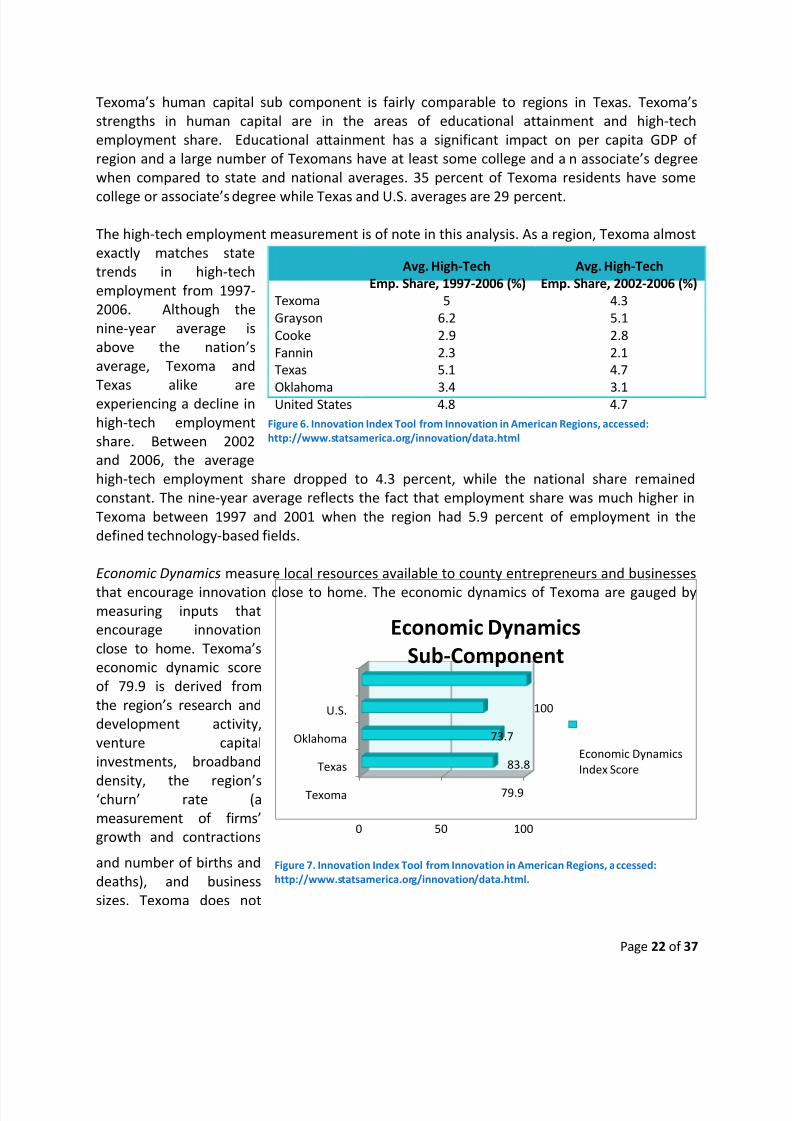

Texoma’s human capital sub component is fairly comparable to regions in Texas. Texoma’s

strengths in human capital are in the areas of educational attainment and high-tech

employment share. Educational attainment has a significant impact on per capita GDP of

region and a large number of Texomans have at least some college and a n associate’s degree

when compared to state and national averages. 35 percent of Texoma residents have some

college or associate’s degree while Texas and U.S. averages are 29 percent.

The high-tech employment measurement is of note in this analysis. As a region, Texoma almost

exactly matches state

trends in high-tech

employment from 1997-

2006. Although the

nine-year average is

above the nation’s

average, Texoma and

Texas alike are

experiencing a decline in

high-tech employment

share. Between 2002

and 2006, the average

high-tech employment share dropped to 4.3 percent, while the national share remained

constant. The nine-year average reflects the fact that employment share was much higher in

Texoma between 1997 and 2001 when the region had 5.9 percent of employment in the

defined technology-based fields.

Economic Dynamics measure local resources available to county entrepreneurs and businesses

that encourage innovation close to home. The economic dynamics of Texoma are gauged bymeasuring inputs that

encourage innovation

close to home. Texoma’s

economic dynamic score

of 79.9 is derived from

the region’s research and

development activity,

venture capital

investments, broadband

density, the region’s‘churn’ rate (a

measurement of firms’

growth and contractions

and number of births and

deaths), and business

sizes. Texoma does not

Avg. High-Tech

Emp. Share, 1997-2006 (%)

Avg. High-Tech

Emp. Share, 2002-2006 (%)

Texoma 5 4.3

Grayson 6.2 5.1

Cooke 2.9 2.8

Fannin 2.3 2.1

Texas 5.1 4.7

Oklahoma 3.4 3.1United States 4.8 4.7

Figure 6. Innovation Index Tool from Innovation in American Regions, accessed:

http://www.statsamerica.org/innovation/data.html

Figure 7. Innovation Index Tool from Innovation in American Regions, accessed:

http://www.statsamerica.org/innovation/data.html.

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 24/37

Page 23 of 37

0 50 100

Texoma

Texas

Oklahoma

U.S.

83.5

94.3

74

100

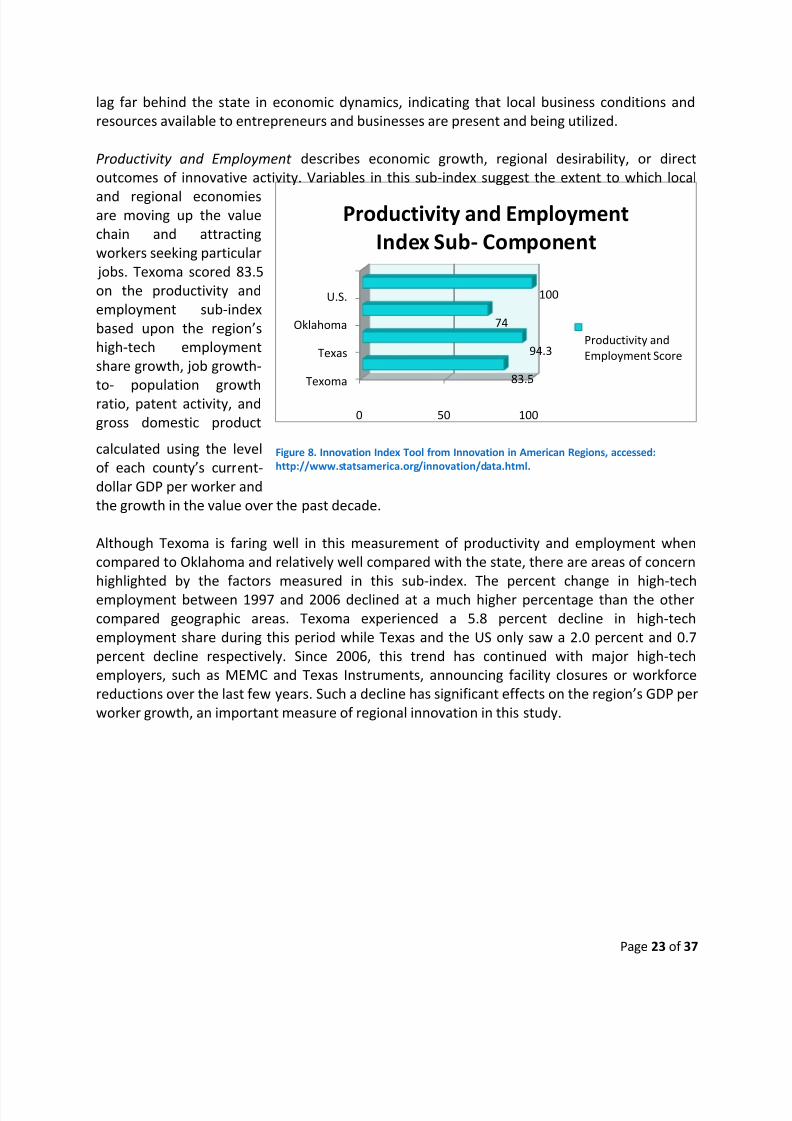

Productivity and Employment

Index Sub- Component

Productivity and

Employment Score

lag far behind the state in economic dynamics, indicating that local business conditions and

resources available to entrepreneurs and businesses are present and being utilized.

Productivity and Employment describes economic growth, regional desirability, or direct

outcomes of innovative activity. Variables in this sub-index suggest the extent to which local

and regional economiesare moving up the value

chain and attracting

workers seeking particular

jobs. Texoma scored 83.5

on the productivity and

employment sub-index

based upon the region’s

high-tech employment

share growth, job growth-

to- population growth

ratio, patent activity, and

gross domestic product

calculated using the level

of each county’s current-

dollar GDP per worker and

the growth in the value over the past decade.

Although Texoma is faring well in this measurement of productivity and employment when

compared to Oklahoma and relatively well compared with the state, there are areas of concern

highlighted by the factors measured in this sub-index. The percent change in high-tech

employment between 1997 and 2006 declined at a much higher percentage than the other

compared geographic areas. Texoma experienced a 5.8 percent decline in high-tech

employment share during this period while Texas and the US only saw a 2.0 percent and 0.7

percent decline respectively. Since 2006, this trend has continued with major high-tech

employers, such as MEMC and Texas Instruments, announcing facility closures or workforce

reductions over the last few years. Such a decline has significant effects on the region’s GDP per

worker growth, an important measure of regional innovation in this study.

Figure 8. Innovation Index Tool from Innovation in American Regions, accessed:

http://www.statsamerica.org/innovation/data.html.

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 25/37

Page 24 of 37

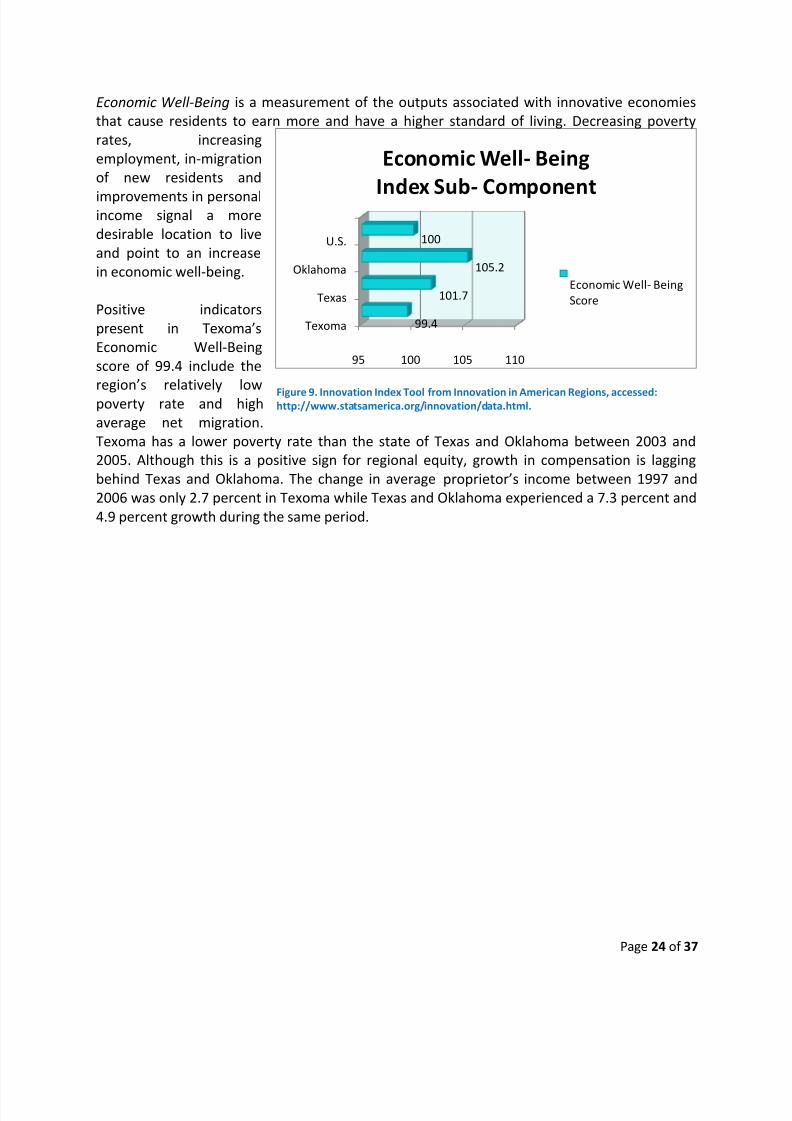

95 100 105 110

Texoma

Texas

Oklahoma

U.S.

99.4

101.7

105.2

100

Economic Well- Being

Index Sub- Component

Economic Well- Being

Score

Economic Well-Being is a measurement of the outputs associated with innovative economies

that cause residents to earn more and have a higher standard of living. Decreasing poverty

rates, increasing

employment, in-migration

of new residents and

improvements in personalincome signal a more

desirable location to live

and point to an increase

in economic well-being.

Positive indicators

present in Texoma’s

Economic Well-Being

score of 99.4 include the

region’s relatively low

poverty rate and high

average net migration.

Texoma has a lower poverty rate than the state of Texas and Oklahoma between 2003 and

2005. Although this is a positive sign for regional equity, growth in compensation is lagging

behind Texas and Oklahoma. The change in average proprietor’s income between 1997 and

2006 was only 2.7 percent in Texoma while Texas and Oklahoma experienced a 7.3 percent and

4.9 percent growth during the same period.

Figure 9. Innovation Index Tool from Innovation in American Regions, accessed:http://www.statsamerica.org/innovation/data.html.

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 26/37

Page 25 of 37

Workforce

Addressing the challenges of a global economy requires a shift away from traditional economic

development models. Instead of low-wage rates and tax incentives, regions in industrialized

countries compete today on the quality of their skilled workforce and incentives that reward

innovation.13

Workforce development is usually tied closely to educational attainment and communication

and collaboration between workforce/education organizations, economic development

organizations, and the private sector, resource allocation, and effectiveness of service delivery.

The development of skills necessary to fill high wage jobs is critical to the continued economic

development efforts in the region, especially as our region experiences changes in labor market

demands.

Schools educate and prepare the future workforce for the region. Youth who do not aspire to

higher education and who lack career training opportunities are lost to a cycle of poverty thatwill envelope their families and children and continued to be repeated in their children. The

region’s public schools, colleges, and workforce boards provide education opportunities for

Texoma residents to gain skills and training necessary to enter the labor force.

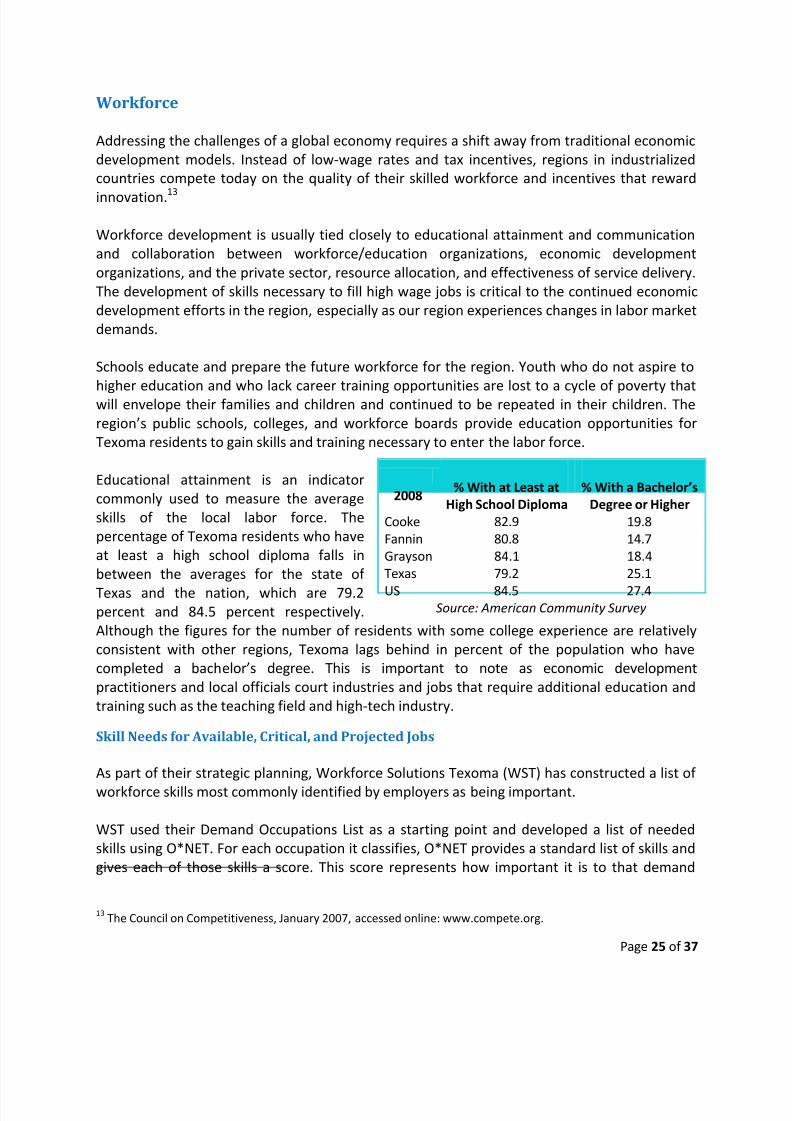

Educational attainment is an indicator

commonly used to measure the average

skills of the local labor force. The

percentage of Texoma residents who have

at least a high school diploma falls in

between the averages for the state of

Texas and the nation, which are 79.2percent and 84.5 percent respectively.

Although the figures for the number of residents with some college experience are relatively

consistent with other regions, Texoma lags behind in percent of the population who have

completed a bachelor’s degree. This is important to note as economic development

practitioners and local officials court industries and jobs that require additional education and

training such as the teaching field and high-tech industry.

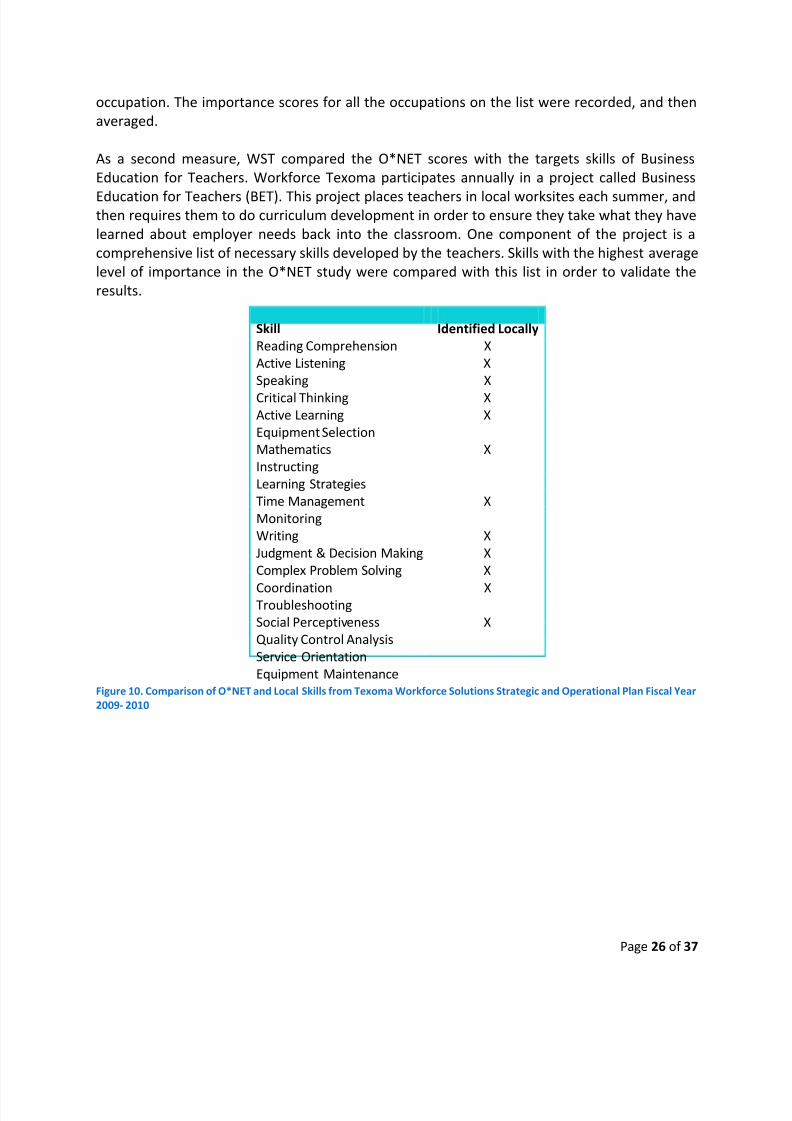

Skill Needs for Available, Critical, and Projected Jobs

As part of their strategic planning, Workforce Solutions Texoma (WST) has constructed a list of

workforce skills most commonly identified by employers as being important.

WST used their Demand Occupations List as a starting point and developed a list of needed

skills using O*NET. For each occupation it classifies, O*NET provides a standard list of skills and

gives each of those skills a score. This score represents how important it is to that demand

13The Council on Competitiveness, January 2007, accessed online: www.compete.org.

2008% With at Least at

High School Diploma

% With a Bachelor’s

Degree or Higher

Cooke 82.9 19.8

Fannin 80.8 14.7

Grayson 84.1 18.4

Texas 79.2 25.1

US 84.5 27.4Source: American Community Survey

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 27/37

Page 26 of 37

occupation. The importance scores for all the occupations on the list were recorded, and then

averaged.

As a second measure, WST compared the O*NET scores with the targets skills of Business

Education for Teachers. Workforce Texoma participates annually in a project called Business

Education for Teachers (BET). This project places teachers in local worksites each summer, andthen requires them to do curriculum development in order to ensure they take what they have

learned about employer needs back into the classroom. One component of the project is a

comprehensive list of necessary skills developed by the teachers. Skills with the highest average

level of importance in the O*NET study were compared with this list in order to validate the

results.

Skill Identified Locally

Reading Comprehension X

Active Listening X

Speaking X

Critical Thinking XActive Learning X

Equipment Selection

Mathematics X

Instructing

Learning Strategies

Time Management X

Monitoring

Writing X

Judgment & Decision Making X

Complex Problem Solving X

Coordination XTroubleshooting

Social Perceptiveness X

Quality Control Analysis

Service Orientation

Equipment MaintenanceFigure 10. Comparison of O*NET and Local Skills from Texoma Workforce Solutions Strategic and Operational Plan Fiscal Year

2009- 2010

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 28/37

Page 27 of 37

Key Trends

Texoma is in the midst of a transition away from the traditional economic development model

that targets manufacturing as the primary source of industry and employment. This is largely

due to the fact that communities in Texoma are experiencing a major decline in manufacturing

growth and expansion.

2000 2006 Change

Super Sector Title # of

Workers

% of

Labor

Force

# of

Workers

% of

Labor

Force

# of

Workers

% of

Labor

Force

Natural Resources &

Mining583 1% 1,501 2% 918 1%

Construction 3,433 6% 3,719 6% 286 0%

Manufacturing 12,852 21% 9,336 15% (3,516) -6%

Trade,

Transportation, &

Utilities

11,834 19% 11,903 19% 69 0%

Information 663 1% 635 1% (28) 0%

Financial Activities 3,654 6% 3,536 6% (118) 0%

Professional &

Business Services3,428 6% 3,330 5% (98) 0%

Education & Health

Sciences14,970 24% 16,543 27% 1,573 3%

Leisure & Hospitality 5,093 8% 5,854 9% 761 1%

Other Services 1,252 2% 1,442 2% 190 0%

Government 3,869 6% 3,926 6% 57 0%Table 2. Workforce Solutions Texoma Strategic and Operational Plan Fiscal Year 2009- 2010.

The 2007-2012 Texoma CEDS affirmed the goal of promoting Lake Texoma as a tourism

destination and support region’s associated tourist destinations such as historic sites and

heritage sites and state parks and refuges. According to the Army Corps of Engineers, Lake

Texoma attracts more than six million visitors a year and generates millions of dollars in tax

revenue through associated spending in recreation activities, retail purchases,

accommodations, and food service. The table above indicates that Texoma already has a slight

competitive advantage in leisure & hospitality.

Rather than reactively addressing the region’s losses in manufacturing, a rea leaders have

discussed ways to capitalize on assets in Texoma. The leisure & hospitality captures many

aspects of tourism in the broadest sense. Tourism has been identified repeatedly as a largely

untapped and source of economic growth and diversification, from utilizing the reg ion’s unique

cultural, ecological, and historical sites. Leaders in Texoma have turned their focus to explore

the feasibility of developing a bi-state regional brand for Texoma that markets the tourism

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 29/37

Page 28 of 37

assets of Texoma. With the new world-class casinos of the Chickasaw and Choctaw Nations, the

steady attraction of Lake Texoma, and the growth of the D/FW Metroplex and Oklahoma City,

the Texoma region is in the ideal location for living, working, and playing. Attracting visitors,

new residents, and even new business to this region through a coordinated marketing effort

will generate revenues for all of Texoma’s communities and attractions.

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 30/37

Page 29 of 37

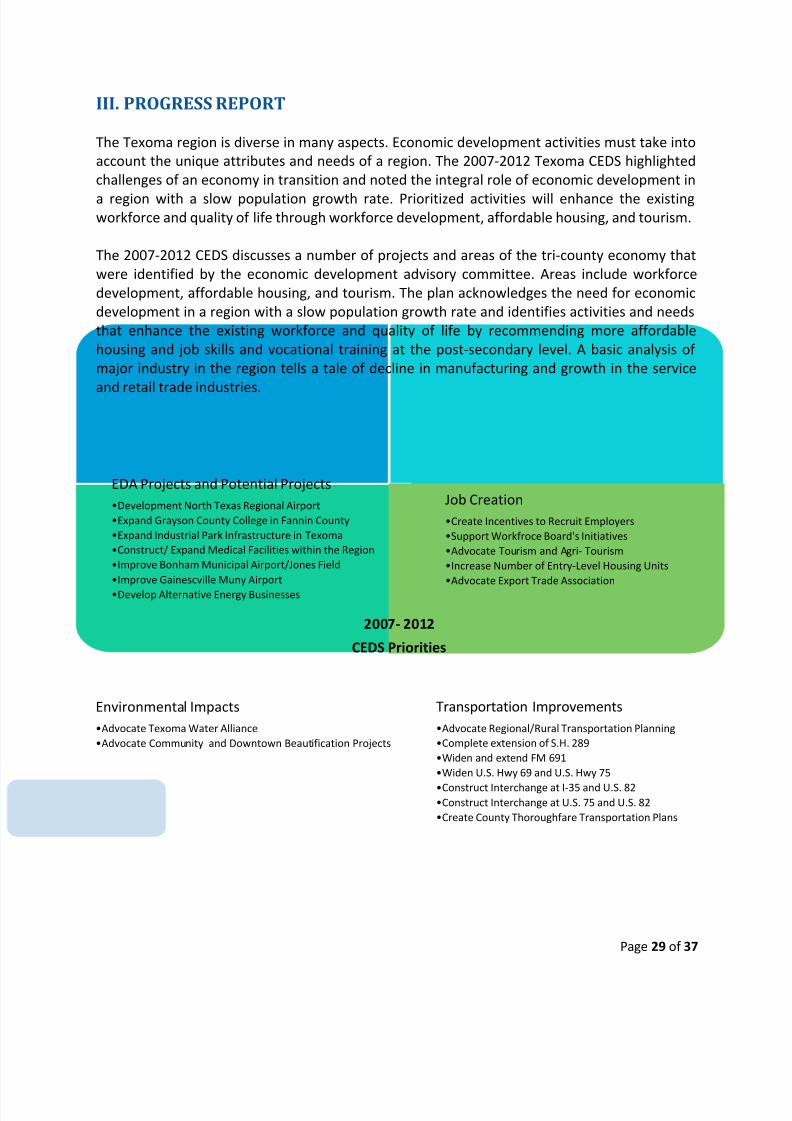

EDA Projects and Potential Projects

•Development North Texas Regional Airport

•Expand Grayson County College in Fannin County

•Expand Industrial Park Infrastructure in Texoma

•Construct/ Expand Medical Facilities within the Region

•Improve Bonham Municipal Airport/Jones Field

•Improve Gainescville Muny Airport

•Develop Alternative Energy Businesses

Job Creation

•Create Incentives to Recruit Employers

•Support Workfroce Board's Initiatives

•Advocate Tourism and Agri- Tourism

•Increase Number of Entry-Level Housing Units

•Advocate Export Trade Association

Environmental Impacts

•Advocate Texoma Water Alliance

•Advocate Community and Downtown Beautification Projects

Transportation Improvements

•Advocate Regional/Rural Transportation Planning

•Complete extension of S.H. 289

•Widen and extend FM 691

•Widen U.S. Hwy 69 and U.S. Hwy 75

•Construct Interchange at I-35 and U.S. 82•Construct Interchange at U.S. 75 and U.S. 82

•Create County Thoroughfare Transportation Plans

2007- 2012

CEDS Priorities

III. PROGRESS REPORT

The Texoma region is diverse in many aspects. Economic development activities must take into

account the unique attributes and needs of a region. The 2007-2012 Texoma CEDS highlighted

challenges of an economy in transition and noted the integral role of economic development in

a region with a slow population growth rate. Prioritized activities will enhance the existingworkforce and quality of life through workforce development, affordable housing, and tourism.

The 2007-2012 CEDS discusses a number of projects and areas of the tri-county economy that

were identified by the economic development advisory committee. Areas include workforce

development, affordable housing, and tourism. The plan acknowledges the need for economic

development in a region with a slow population growth rate and identifies activities and needs

that enhance the existing workforce and quality of life by recommending more affordable

housing and job skills and vocational training at the post-secondary level. A basic analysis of

major industry in the region tells a tale of decline in manufacturing and growth in the service

and retail trade industries.

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 31/37

Page 30 of 37

Ongoing Regional Projects

Texoma Regional Marketing. The Texoma Council of Governments (TCOG) and residents of the

Texoma region have a strong connection with South Oklahoma through the natural movement

of human and physical capital. The regions share a common labor shed, retail market, and

cultural economics, making bi-state relationships necessary for positive economic outcomes inour communities. Lake Texoma may be the single greatest asset in southern Oklahoma and

northern Texas, yet there is no comprehensive or unified approach to either protecting it for

future generations or marketing it as an economic development resource. In April of 2009, the

Texoma Regional Consortium hosted a forum in which more than 200 people came together to

begin discussing these issues. There was considerable agreement that Lake Texoma has the

potential to anchor a brand for the region that promotes significant economic activity in Texas

and Oklahoma. Thoughtful development of this resource can contribute to a strong economic

future by improving the “quality of place” that attracts and keeps young professionals and

entrepreneurs in the region. While there is a tremendous amount of work to be done in the

long-term to ensure that the potential of Lake Texoma is fully realized, the overwhelming

opinion was that a marketing plan is the first achievable step.

The Texoma Council of Governments (TCOG) was asked to take the lead on this project with a

particular emphasis on identifying potential funding sources and coordinating the activities of a

Steering Committee. Stakeholders, including the Choctaw Nation, Denison Development

Alliance, the City of Sherman, Private Developers, Rural Enterprises of Oklahoma, Inc., Southern

Oklahoma Development Association, and Workforce Solutions Texoma, have met to discuss

strategies for developing a regional brand that can market the virtues of the region’s assets.

Recent Successes

EDA Awards

Center for Workplace Learning. In 2003, the Center for Workplace Learning at Grayson County

College received a Public Works, Economic Adjustment Infrastructure Investments by EDA.

Grayson County College was the recipient for a $1,700,000 public works investment

($1,000,000 EDA investment and $700,000 applicant investment). To date, this successful

project has created 1268 jobs and 1175 existing jobs have been retained for a total of 2443 jobs

created and retained.

Grayson County Community College, Fannin Campus. Grayson County College was awarded an

EDA Economic Adjustment grant in August of 2009 to partially fund the construction of apermanent building in Fannin County. The $2 million matching grant will help Grayson County

College replace their extension site in Bonham with a new facility, the Rayburn Center, which

will house regional business and industrial one-stop workforce training and education for

Fannin County. The Rayburn Center has been designed as a regional center for advancing

economic productivity and viability with the creation of a regional one-stop location for local

business incubation and instruction in advanced techniques and processes of management,

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 32/37

Page 31 of 37

manufacturing, assembly, workforce training and retention, and competition. The Rayburn

Center will be located on 100 acres of donated land on U.S. Highway 82.

In order to raise the $2 million in matching funds required of the EDA grant, Grayson County

College is in the process of annexing Fannin County in their taxing district. Fannin County

residents currently pay out-of-district rates when they register for GCC classes. Shouldannexation be approved, Fannin County residents would pay approximately thirty percent less

for each 3 hour course. Fannin County voters will decide on May 8, 2010 whether or not they

approve paying the same tax rate currently being paid by Grayson County taxpayers in

exchange for a break in tuition rates and the construction of a permanent GCC facility in

Bonham.

Other Achievements in Economic Development

North Texas Regional Airport (NTRA). Over the last few years the North Texas Regional Airport

(NTRA) has positioned itself to be the region’s center of aviation travel and training with hopes

of attracting economic activity from the Dallas/Fort Worth Metroplex, only sixty miles to thesouth. As part of a multi-jurisdiction collaborative effort, NTRA has developed a marketing

strategy for its hundreds of shovel-ready acres of industrial land with runway, highway and

railway access. The extension of HWY 289 was completed in December of 2009 and now links

the airport with Lake Texoma and the DFW Metroplex along the airport’s eastern edge. NTRA

continues to enhance its facilities and site feature with completion of the first phase of the

$16.9 million Capital Improvement Program. In April 2009, the water drainage system was

updated to correct the undersized water drainage and a $4.0 million taxiway rehabilitation

project is still underway that will completely overlay the airports taxiways. In 2010, NTRA will

revisit and update their 2002 Master Plan in order to systematically plan their capital

improvement projects for the coming years.

Transportation. In December 2008, The Sherman-Denison Planning Organization (MPO)

completed a Corridor Plan for FM 691 to provide recommendations for short and long term

improvements integral to serve the added capacity due to developments of the US 75/FM 691

interchange and NRTA. Through meetings with stakeholders, the study determined the desired

“look and feel” of the right away and recommended a general approach for collaborative

management between Grayson County, TxDOT, the Cities of Sherman and Denison, and the

Grayson County Regional Mobility Authority, that includes options for a new ramping scheme at

US 75 and recommendations for the development of a Corridor Access Management Plan to

study the access management tools that can implemented to accommodate existing local and

regional traffic capacity demands.

Texoma Area Paratransit System (TAPS) launched its first fixed bus routes on August 24th with

the Roo and Viking Routes that links Austin College and Grayson County College with shopping

outlets in the area.

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 33/37

Page 32 of 37

Industry. Panda Energy will be building a combined cycle natural gas plant in Sherman to meet

the increased power needs of North Texas. Richard Evans with Panda Energy said the plant will

be located on Progress Drive and will sit on 20 acres out of a 205-acre parcel of land. The

Sherman generating station will supply the power needs of 400,000 to 450,000 homes.

Construction could begin by the first quarter 2010. After that, it will be about 27 months before

the plant is up and running. The construction phase of the plant will require 500 construction jobs. Once the plant is up and running, Evans said the plant could mean well-paying jobs for up

to 27 people.

The City of Sherman and Grayson county commissioners have approved incentives to bring

Panda Energy to Sherman. Even with rebates and incentives, Panda Energy will still be paying

taxes of $100 million a year.

Health Care. In December of 2009, Texoma Medical Center (TMC) moved into their new facility

located at the corner of U.S. Hwy 75 and State Hwy 69 next to the 140,000 square-foot CIGNA

call center. The new hospital center has 165 beds, room to expand to 241 beds based on need,

a bigger Emergency Department with 26 beds with 4 trauma beds, and an adjacent three-story,

120,000-square-foot medical office building that will open in early 2010. The CIGNA call center

and TMC have added more than 150 million dollars in property tax value for the city of Denison.

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 34/37

Page 33 of 37

IV. SCOPE OF WORK FOR 2010

In 2010, TCOG will work with area leaders to pursue the development of a brand and

comprehensive marketing study for Texoma; reflecting the objective for growth in tourism

identified at the 2009 Lake Texoma Symposium. This activity is a significant step towards the

development of Texoma as Lake Texoma and the Casinos and Resorts in Southern Oklahomaare a major economic driver of the region and subsequently, a major factor is transforming the

Texoma labor market.

TCOG, in its role as the Texoma Economic Development District, will continue to work with the

region’s economic development leaders to prepare the CEDS updates. This will include tracking

emerging regional trends and performance of regional clusters, as well as maintaining an open

dialogue with local officials and the private sector about regional activities and goals. TCOG will

also organize and host additional economic development training opportunities for Texoma’s

economic development practitioners and local officials.

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 35/37

Page 34 of 37

Appendix A.

EDA Distress Criteria- TEXOMA Statistical Report

Economic Distress Criteria- Primary Elements

(As of May 2010)

Threshold

Standard

U.S.

Figure

Texoma

Figure

Texoma

Threshold

Comparison

24- month Average Unemployment Rage

(BLS, period ending in January 2010)

One

percentage

point above

national

average

7.73% 6.40% -1.33%

2007 Per Capita Money Income (ACS) 80% or lessof US

average

$26,178 $21,590 82.47%

2007 Per Capita Personal Income (BEA)

80% or less

of US

average

$38,615 $29,865 77.34%

2000 Per Capital Money Income (Decennial Census)

80% or less

of US

average

$21,587 $18,173 84.18%

Economic Distress Criteria- Geographic Components

(As of May 2010)

County24 Month

Unemployment

Threshold

Comparison

ACS

PCMI

BEA

PCPI

Threshold

Comparison

Census

PCMI

(2000)

Threshold

Comparison

Cooke 4.90 % -2.83% $22,403 85.6% $36,787 95.3% 82.9%

Fannin 7.33% -0.4% $18,955 72.4% $25,258 65.4% 74.4%

Grayson 6.78% -0.95% $22,063 84.3% $28,901 74.8% 87.4%

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 36/37

Page 35 of 37

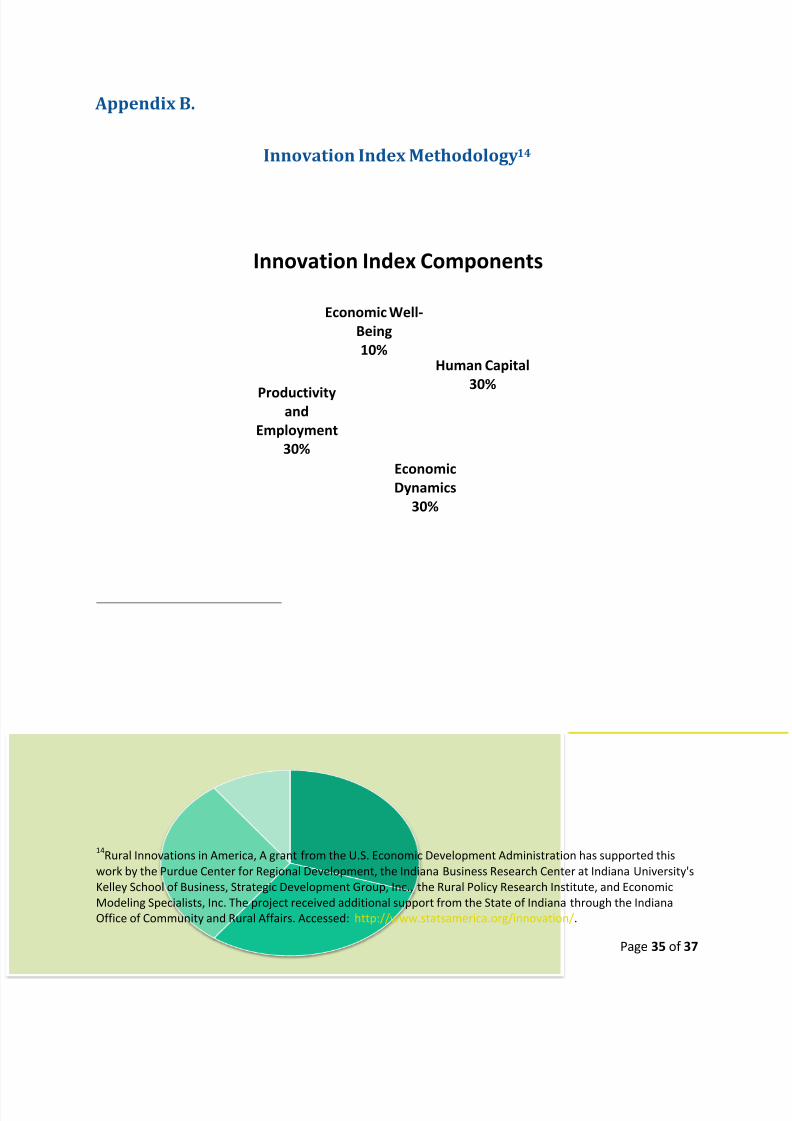

Appendix B.

Innovation Index Methodology14

14Rural Innovations in America, A grant from the U.S. Economic Development Administration has supported this

work by the Purdue Center for Regional Development, the Indiana Business Research Center at Indiana University's

Kelley School of Business, Strategic Development Group, Inc., the Rural Policy Research Institute, and Economic

Modeling Specialists, Inc. The project received additional support from the State of Indiana through the Indiana

Office of Community and Rural Affairs. Accessed: http://www.statsamerica.org/innovation/.

Human Capital

30%

Economic

Dynamics

30%

Productivityand

Employment

30%

Economic Well-

Being

10%

Innovation Index Components

8/4/2019 CEDS 2010 Update

http://slidepdf.com/reader/full/ceds-2010-update 37/37

Innovation Index Sub-Components

Human Capital: 30% Economic Dynamics: 30%

Productivity and Employment: 30% Economic Well-Being: 10%