CE2451 Engineering Economics & Cost Analysis · 1/29/2015 1 CE2451 Engineering Economics & Cost...

56

1/29/2015 1 CE2451 Engineering Economics & Cost Analysis Dr. M. Selvakumar Associate Professor Department of Civil Engineering Sri Venkateswara College of Engineering Objectives of this course • The main objective of this course is to make the Civil Engineering student know about the basic law of economics, how to organize a business, the financial aspects related to business, different methods of appraisal of projects and pricing techniques. At the end of this course the student shall have the knowledge of how to start a construction business, how to get finances, how to account, how to price and bid and how to assess the health of a project. 1/29/2015 2 SVCE, Sriperumbudur

Transcript of CE2451 Engineering Economics & Cost Analysis · 1/29/2015 1 CE2451 Engineering Economics & Cost...

1/29/2015

1

CE2451 Engineering Economics & Cost Analysis

Dr. M. Selvakumar

Associate Professor

Department of Civil Engineering

Sri Venkateswara College of Engineering

Objectives of this course

• The main objective of this course is to make the Civil Engineering

student know about the basic law of economics, how to organize a

business, the financial aspects related to business, different

methods of appraisal of projects and pricing techniques. At the end

of this course the student shall have the knowledge of how to start a

construction business, how to get finances, how to account, how to

price and bid and how to assess the health of a project.

1/29/2015 2SVCE, Sriperumbudur

1/29/2015

2

Unit 1: Basic Economics

Definition of economics - nature and scope of economic science -

nature and scope of managerial economics - basic terms and concepts -

goods - utility - value - wealth - factors of production - land - its

peculiarities - labour - economies of large and small scale -

consumption - wants - its characteristics and classification - law of

diminishing marginal utility – relation between economic decision and

technical decision.

1/29/2015 3SVCE, Sriperumbudur

Basic Economics

Unit 1

1/29/2015

3

Why Study Economics?

– All your life – starts from cradle to grave and beyond –

you will run up against the brutal truths of economics!

– Choosing your life’s occupation is the most important

economic decision you will make. Your future depends

not only on your own abilities but also on how economic

forces beyond your control affect your wages.

– Example, software Booming (2000-2010)

1/29/2015 5SVCE, Sriperumbudur

Logic of Economics

– Economic life is an enormously complicated hive

(enclosed structure) of activity, with people buying,

selling, bargaining, investing and persuading (induce

someone to do something).

– The ultimate purpose of economic science is to

understand this complex undertaking.

– Economics use the scientific approach to understand

economic life.

1/29/2015 6SVCE, Sriperumbudur

1/29/2015

4

Logic of Economics Cont…

– Often economics relies upon analyses and theories.

– Theoretical approach allows economists to make broad

generalizations.

– In addition, economics have developed a specialized

technique known as “econometrics”, which applies the

tools of statistics to economic problems.

1/29/2015 7SVCE, Sriperumbudur

Definitions of Economics

1/29/2015 8SVCE, Sriperumbudur

1/29/2015

5

Economics-Term Definition

The term economics is derived from the word “oeconomicus” by

Xenophon in 431 B.C. It is derived from two words economy and

science. Economy means proper utilization of resources. It

means economics is the science of economy or science of proper

utilization of resources. It is comprised of theories, laws, principle

related to utilization of resources so as to solve the economic

problems, satisfy the human wants or need and so on.

1/29/2015 9SVCE, Sriperumbudur

Definition by Sir James Steuart (1767)

Economy in general is the art of providing for all the

wants of a family, seeks to secure a certain fund of

subsistence (i.e. life) for all the inhabitants, to prevent

every circumstance which may render it precarious

(unstable/unsafe); to provide every thing necessary for

supplying the wants of the society, and to employ the

inhabitants (population) in such manner as naturally to

create reciprocal (mutual) relation.

1/29/2015 10SVCE, Sriperumbudur

1/29/2015

6

Definition by Smith & Say

• Adam Smith defined economics as “An Enquiry into the

Nature and Causes of the wealth of Nations.” (1776)

• J. B. Say (French economist) says that “ Economics is

the science which treats of wealth.”

1/29/2015 11SVCE, Sriperumbudur

Adam Smith wrote a book ‘Wealth of Nations’ (1776)

Jean-baptiste Say

1/29/2015 12SVCE, Sriperumbudur

1/29/2015

7

Definition by Marshall

• Dr. Alfred Marshall defined as “Economics is a study of

man’s actions in the ordinary business of life; it

requires how he gets his income and how he uses it.

Thus it is on one side a study of wealth and on the other

part of the study of man.”

1/29/2015 13SVCE, Sriperumbudur

Dr. Alfred Marshall

1/29/2015 14SVCE, Sriperumbudur

1/29/2015

8

Definition by Lionel Robbins (1932)

• Economics is a science which studies human behavior

as a relationship between ends and scare means which

have alternative uses.

1/29/2015 15SVCE, Sriperumbudur

Definition of Economics

• The branch of knowledge concerned with the

production, consumption and transfer of wealth.

• The condition of a region or group as regards material

prosperity.

1/29/2015 16SVCE, Sriperumbudur

1/29/2015

9

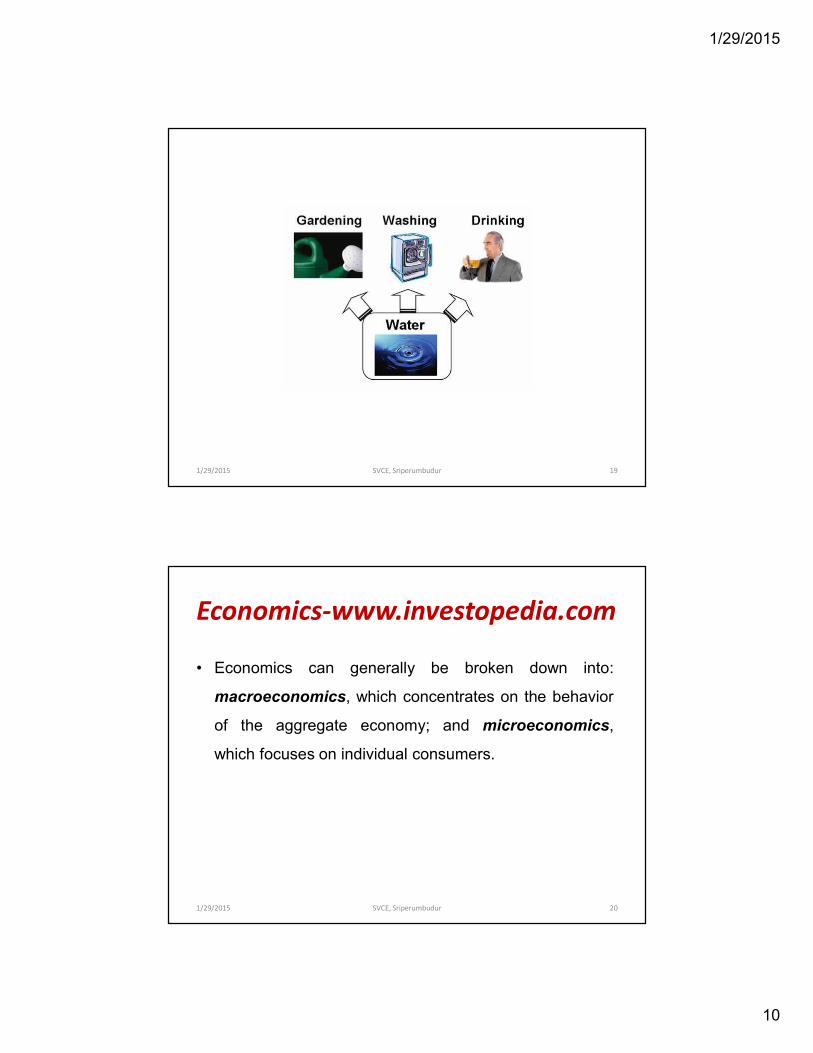

Economics-www.investopedia.com

• A “social science” that studies how individuals,

governments, firms and nations make choices on

allocating scarce resources to satisfy their unlimited

wants.

1/29/2015 17SVCE, Sriperumbudur

1/29/2015 SVCE, Sriperumbudur 18

1/29/2015

10

1/29/2015 SVCE, Sriperumbudur 19

Economics-www.investopedia.com

• Economics can generally be broken down into:

macroeconomics, which concentrates on the behavior

of the aggregate economy; and microeconomics,

which focuses on individual consumers.

1/29/2015 20SVCE, Sriperumbudur

1/29/2015

11

Macroeconomics

Macroeconomics (from the Greek prefix makro- meaning

"large" and economics) is a branch of economics

dealing with the performance, structure, behavior, and

decision-making of an economy as a whole, rather than

individual markets. This includes national, regional, and

global economies.

Example: GDP

1/29/2015 21SVCE, Sriperumbudur

Microeconomics

Microeconomics (from Greek prefix mikro- meaning

"small" and economics) is a branch of economics that

studies the behavior of individuals and small impacting

organizations in making decisions on the allocation of

limited resources.

Example: L&T company

1/29/2015 22SVCE, Sriperumbudur

1/29/2015

12

1/29/2015 23SVCE, Sriperumbudur

NATURE OF ECONOMICS

1/29/2015 24SVCE, Sriperumbudur

1/29/2015

13

Nature of Economic Science

The most fundamental propositions of economic

analysis are the propositions of the general ‘Theory of

Value’.

1/29/2015 25SVCE, Sriperumbudur

Nature of Economic Science

“Economics is a Science and an Art”

Like every other field of study, economics has two aspects,

one of science, the other of art; the one of knowledge, the

other of action; the one of principles, the other of their

application. Each science seeks to study and to understand

the world in some aspect, to reduce the multitude of facts to

order, and to understand their relations.1/29/2015 26SVCE, Sriperumbudur

1/29/2015

14

Nature of Economic Science

“Economics is a Science and an Art”

Then, however, whatever truth is discovered may be found to

be capable of some uses or applications, either in the hands

of the scientists themselves or in the hands of another body

of men, variously named practical workers, technicians, and

inventors, who develop the art side of the subject.

1/29/2015 27SVCE, Sriperumbudur

“Economics is a Science and an Art”

Economics is both art and science. It is called a science

because it is the scientific study of relationships between

economic variables, behavior of consumers and firms, nature

of market and economy, effect of change in one or more

economic variables on the others and so on.

Nature of Economic Science

1/29/2015 28SVCE, Sriperumbudur

1/29/2015

15

“Economics is a Science and an Art”

Economics is an art. The different theories, laws are

explained with the help of graphs, figures, tables, charts,

equations etc simplifying and generalizing them.

Nature of Economic Science

1/29/2015 29SVCE, Sriperumbudur

“Economics is a Science and an Art”

Simplification is to make them easily understandable and

generalization is to make them applicable to all economies.

In order to explain theories, laws and relationships between

economic variables we make some assumptions.

Nature of Economic Science

1/29/2015 30SVCE, Sriperumbudur

1/29/2015

16

“Economics is a Science and an Art”

The assumptions define the conditions for the application of

theories, laws and the relationships. That’s why economics is

an art.

Nature of Economic Science

1/29/2015 31SVCE, Sriperumbudur

“Economics is a Positive Science or Normative Science”

Economics is sometimes divided into two parts. Positive

economics and normative economics. The former deals with

how the economic problem is solved; the later deals with how

the economic problem should be solved.

Nature of Economic Science

1/29/2015 32SVCE, Sriperumbudur

1/29/2015

17

“Economics is a Positive Science or Normative Science”

For example, the effect of price or rent control on the

distribution of income are problems of positive economics.

On the other hand, the desirability of these effects on income

distribution is a problem of normative economics.

Therefore, economics is a positive as well as normative

science.

Nature of Economic Science

1/29/2015 33SVCE, Sriperumbudur

MANAGERIAL ECONOMICS

1/29/2015 34SVCE, Sriperumbudur

1/29/2015

18

Managerial economics as defined by Edwin Mansfield is

"concerned with application of the economic concepts and

economic analysis to the problems of formulating rational

managerial decision.“

Managerial Economics

1/29/2015 35SVCE, Sriperumbudur

It is sometimes referred to as business economics and is a

branch of economics that applies microeconomic analysis to

decision methods of businesses or other management units.

As such, it bridges economic theory and economics in

practice. It draws heavily from quantitative techniques such

as regression analysis, correlation and calculus.

Managerial Economics

1/29/2015 36SVCE, Sriperumbudur

1/29/2015

19

Managerial decision areas include:

1. assessment of investible funds

2. selecting business area

3. choice of product

4. determining optimum output

Managerial Economics

1/29/2015 37SVCE, Sriperumbudur

Managerial decision areas include:

5. determining price of product

6. determining input-combination and technology

7. sales promotion.

Managerial Economics

1/29/2015 38SVCE, Sriperumbudur

1/29/2015

20

Managerial economics to a certain degree is prescriptive

in nature as it suggests course of action to a managerial

problem.

Scope of Managerial Economics

1/29/2015 39SVCE, Sriperumbudur

Problems can be related to various departments in a firm like

production, accounts, sales, etc.

Demand decision.

Production decision.

Theory of exchange or Price Theory.

All human economic activities

Scope of Managerial Economics

1/29/2015 40SVCE, Sriperumbudur

1/29/2015

21

Demand refers to the willingness to buy a commodity.

Demand, here, defines the market size for a commodity,

i.e. who will buy the commodity. Analysis of the demand is

important for a firm as its revenue, profit, income of the

employees depend on it.

Demand Decision

1/29/2015 41SVCE, Sriperumbudur

A firm needs to answer four basic questions:

What to produce?

How to produce?

how much to produce? and

for whom to produce?

Production Decision

1/29/2015 42SVCE, Sriperumbudur

1/29/2015

22

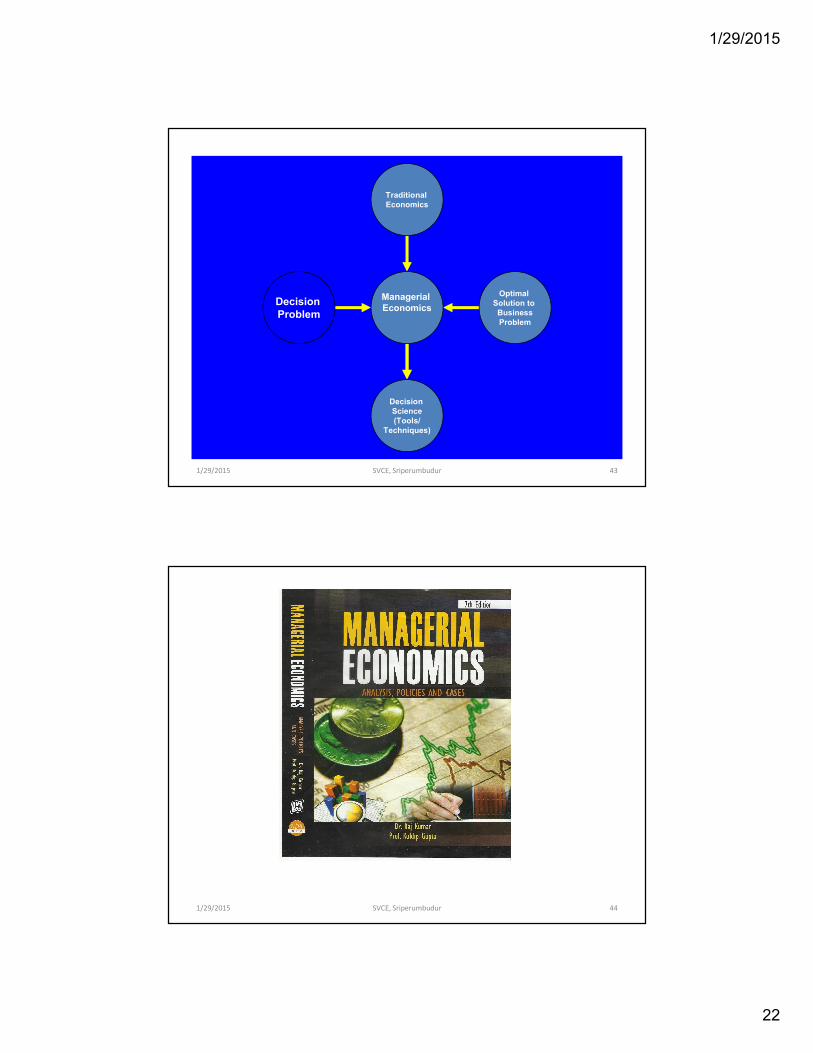

Traditional Economics

Optimal Solution to BusinessProblem

Decision Science(Tools/

Techniques)

Decision Problem

Managerial Economics

1/29/2015 43SVCE, Sriperumbudur

1/29/2015 44SVCE, Sriperumbudur

1/29/2015

23

1/29/2015 45SVCE, Sriperumbudur

GOODS, UTILITY, VALUE & WEALTH

1/29/2015 46SVCE, Sriperumbudur

1/29/2015

24

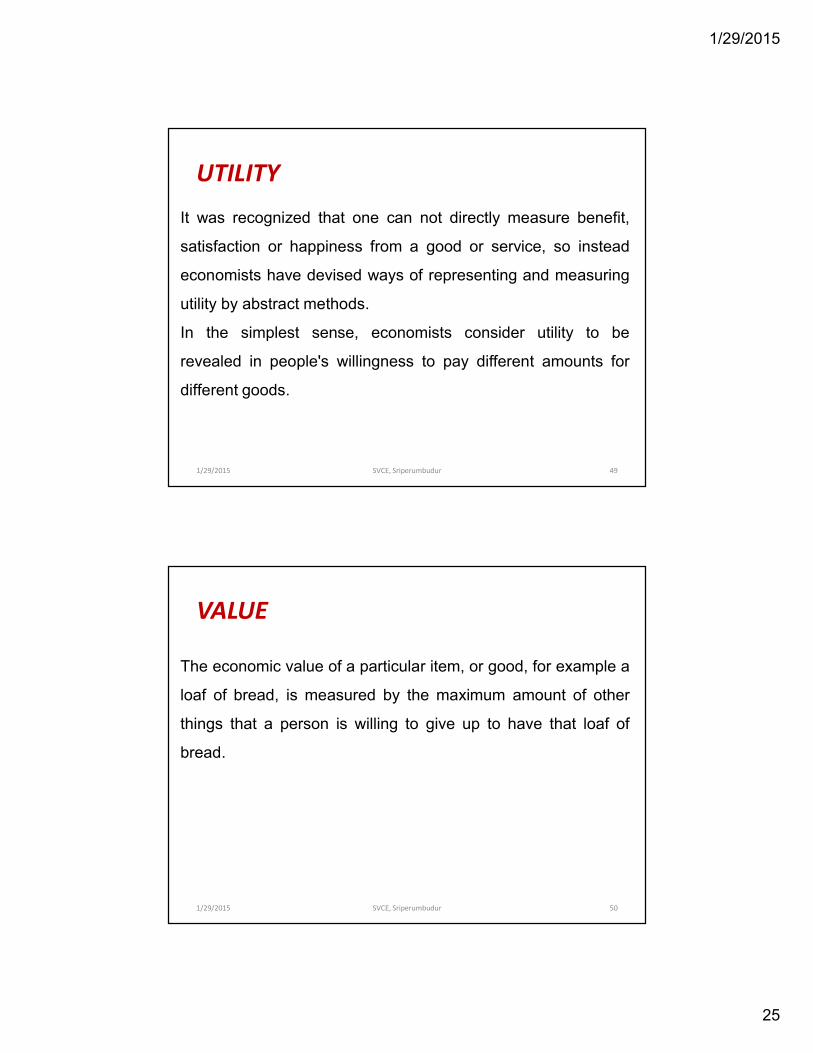

GOODS

Goods - Objects that can satisfy people's wants.

GOODS

Free Goods Economic Goods

Consumer Goods Producer Goods (Capital Goods)

Durable Consumer Goods

Non-durable Consumer Goods

1/29/2015 47SVCE, Sriperumbudur

UTILITY

Utility is usefulness, the ability of something to satisfy needs or

wants.

Utility is an important concept in economics and game theory,

because it represents satisfaction experienced by the

consumer of a good.

1/29/2015 48SVCE, Sriperumbudur

1/29/2015

25

UTILITY

It was recognized that one can not directly measure benefit,

satisfaction or happiness from a good or service, so instead

economists have devised ways of representing and measuring

utility by abstract methods.

In the simplest sense, economists consider utility to be

revealed in people's willingness to pay different amounts for

different goods.

1/29/2015 49SVCE, Sriperumbudur

VALUE

The economic value of a particular item, or good, for example a

loaf of bread, is measured by the maximum amount of other

things that a person is willing to give up to have that loaf of

bread.

1/29/2015 50SVCE, Sriperumbudur

1/29/2015

26

VALUE

If we simplify our example “economy” so that the person only

has two goods to choose from, bread and pasta, the value of a

loaf of bread would be measured by the most pasta that the

person is willing to give up to have one more loaf of bread.

1/29/2015 51SVCE, Sriperumbudur

VALUE

Thus, economic value is measured by the most someone is

willing to give up in other goods and services in order to obtain

a good, service, or state of the world.

1/29/2015 52SVCE, Sriperumbudur

1/29/2015

27

VALUE

In a market economy, dollars (or some other currency) are a

universally accepted measure of economic value, because the

number of dollars that a person is willing to pay for something

tells how much of all other goods and services they are willing

to give up to get that item.

This is often referred to as “willingness to pay.”

1/29/2015 53SVCE, Sriperumbudur

VALUE

In general, when the price of a good increases, people will

purchase less of that good.

This is referred to as the law of demand—people demand less

of something when it is more expensive (assuming prices of

other goods and peoples’ incomes have not changed).

1/29/2015 54SVCE, Sriperumbudur

1/29/2015

28

VALUE

By relating the quantity demanded and the price of a good, we

can estimate the demand function for that good.

From this, we can draw the demand curve, the graphical

representation of the demand function.

1/29/2015 55SVCE, Sriperumbudur

WEALTH

Measure of the value of all of the assets of worth owned by a

person, community, company or country. Wealth is the found

by taking the total market value of all the physical and

intangible assets of the entity and then subtracting all debts.

Essentially, wealth is the accumulation of resources. People

are said to be wealthy when they are able to accumulate many

valuable resources or goods. Wealth is expressed in a variety

of ways. For individuals, net worth is the most common

expression of wealth, while countries measure by gross

domestic product (GDP) or GDP per capita.1/29/2015 56SVCE, Sriperumbudur

1/29/2015

29

FACTOR OF PRODUCTION

In economics, factors of production are the inputs to the

production process. Finished goods are the output. Input

determines the quantity of output i.e. output depends upon

input. Input is the starting point and output is the end point of

production process and such input-output relationship is called

a production function. There are three basic factors of

production: land, labor, capital.

1/29/2015 57SVCE, Sriperumbudur

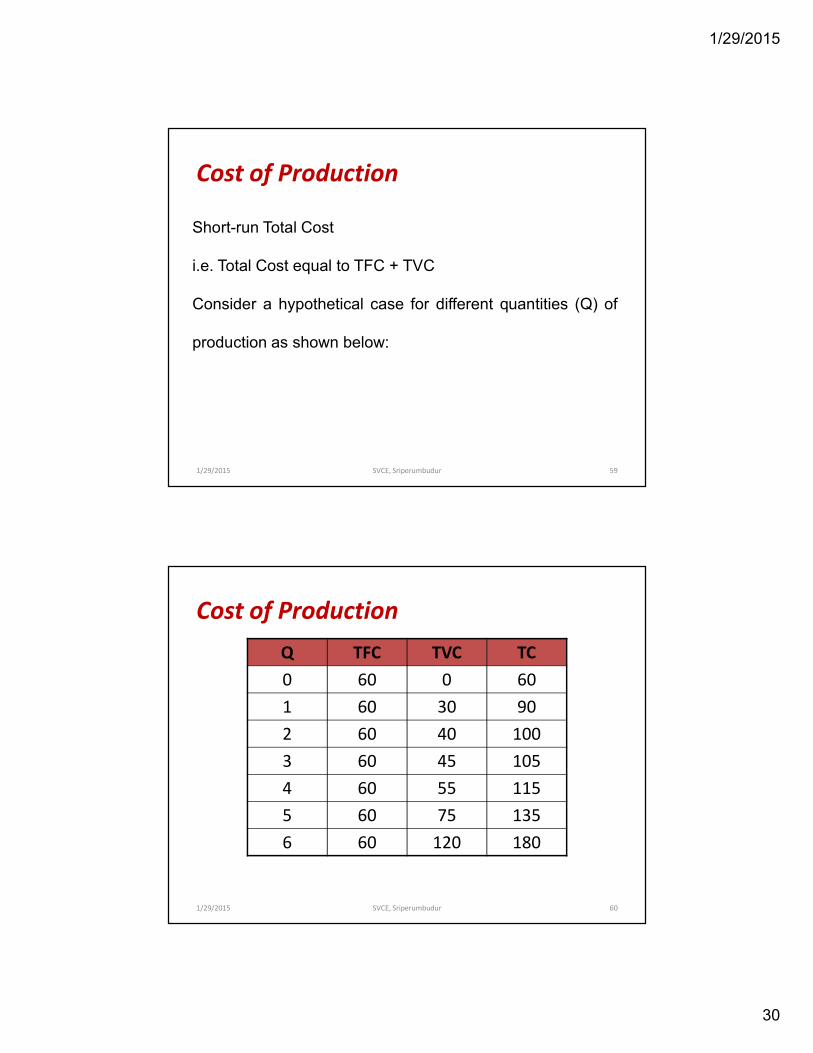

Cost of ProductionShort-run Total Cost

In the short run, one or more (but not all) factors of

production (land, labour, machinery and materials) are fixed

in quantity. Total Fixed Cost (TFC) refers to total obligation

incurred by the firm per unit of time for all fixed inputs. Total

Variable Cost (TVC) are the total obligations incurred by the

firm per unit of time for all variable inputs it uses.

1/29/2015 58SVCE, Sriperumbudur

1/29/2015

30

Cost of Production

Short-run Total Cost

i.e. Total Cost equal to TFC + TVC

Consider a hypothetical case for different quantities (Q) of

production as shown below:

1/29/2015 59SVCE, Sriperumbudur

Cost of Production

Q TFC TVC TC

0 60 0 60

1 60 30 90

2 60 40 100

3 60 45 105

4 60 55 115

5 60 75 135

6 60 120 180

1/29/2015 60SVCE, Sriperumbudur

1/29/2015

31

Cost of Production

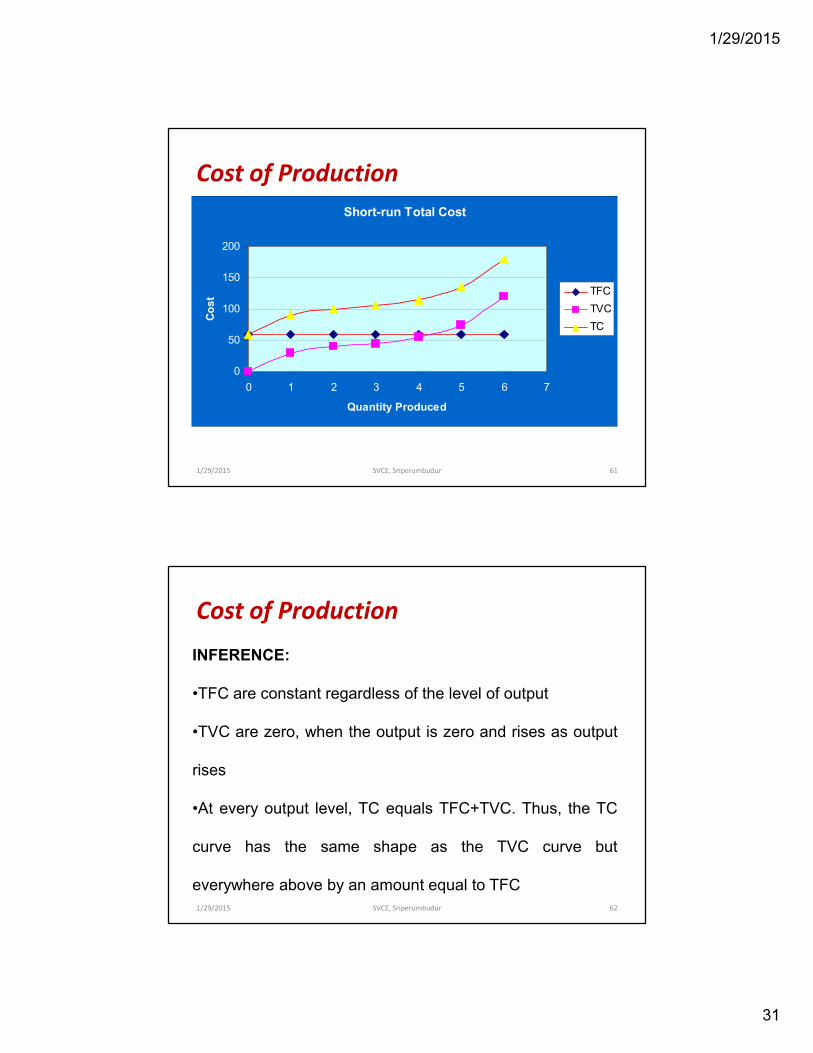

Short-run Total Cost

0

50

100

150

200

0 1 2 3 4 5 6 7

Quantity Produced

Co

st

TFC

TVC

TC

1/29/2015 61SVCE, Sriperumbudur

Cost of Production

INFERENCE:

•TFC are constant regardless of the level of output

•TVC are zero, when the output is zero and rises as output

rises

•At every output level, TC equals TFC+TVC. Thus, the TC

curve has the same shape as the TVC curve but

everywhere above by an amount equal to TFC

1/29/2015 62SVCE, Sriperumbudur

1/29/2015

32

Cost of Production

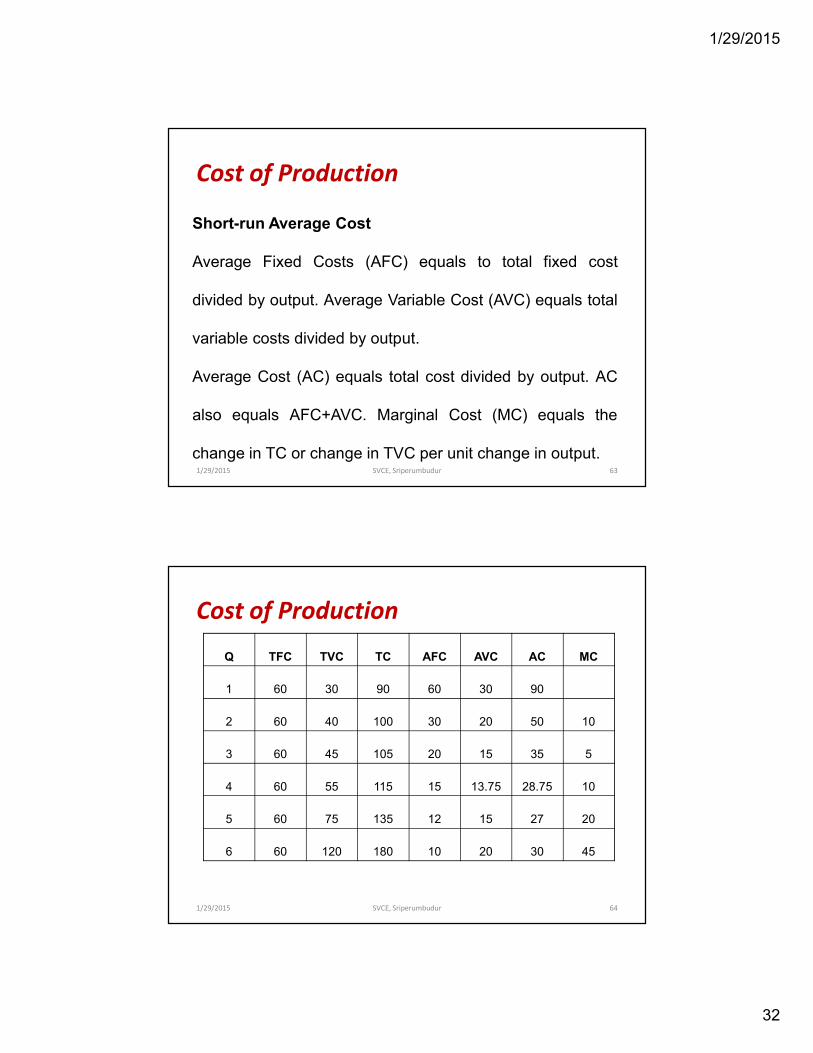

Short-run Average Cost

Average Fixed Costs (AFC) equals to total fixed cost

divided by output. Average Variable Cost (AVC) equals total

variable costs divided by output.

Average Cost (AC) equals total cost divided by output. AC

also equals AFC+AVC. Marginal Cost (MC) equals the

change in TC or change in TVC per unit change in output.1/29/2015 63SVCE, Sriperumbudur

Cost of Production

Q TFC TVC TC AFC AVC AC MC

1 60 30 90 60 30 90

2 60 40 100 30 20 50 10

3 60 45 105 20 15 35 5

4 60 55 115 15 13.75 28.75 10

5 60 75 135 12 15 27 20

6 60 120 180 10 20 30 45

1/29/2015 64SVCE, Sriperumbudur

1/29/2015

33

Cost of Production

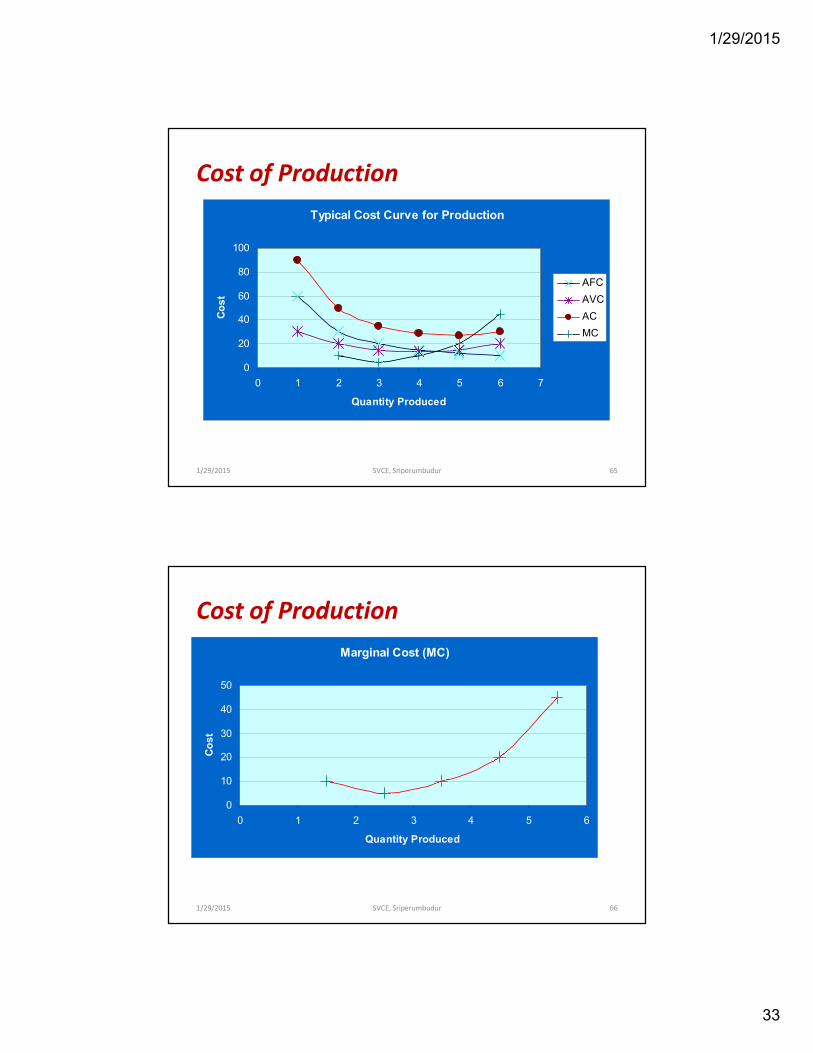

Typical Cost Curve for Production

0

20

40

60

80

100

0 1 2 3 4 5 6 7

Quantity Produced

Co

st

AFC

AVC

AC

MC

1/29/2015 65SVCE, Sriperumbudur

Cost of Production

Marginal Cost (MC)

0

10

20

30

40

50

0 1 2 3 4 5 6

Quantity Produced

Co

st

1/29/2015 66SVCE, Sriperumbudur

1/29/2015

34

Cost of Production

Note

•MC schedules are plotted halfway between successive

levels of output

•While AFC curve falls continuously as output is expanded,

the AVC, the AC and MC curves are U-shaped. The MC

curve reaches the lowest point at a lower level of output

than either the AVC or AC curve

1/29/2015 67SVCE, Sriperumbudur

Cost of Production

The portion of MC intersects the AVC and AC at their lowest

points. This is so because whenever extra or marginal

amount added to total cost (or variable cost) is less than the

average of that cost, the curve necessarily falls. Conversely,

whenever the marginal amount added to TC (or TVC) is

greater than the average of TC, the average cost rises.

1/29/2015 68SVCE, Sriperumbudur

1/29/2015

35

Cost of Production

AVC = AC – AFC

When

MC < AC AC curve fall continuously

MC = AC Minimum AC

MC > AC AC starts rising

1/29/2015 69SVCE, Sriperumbudur

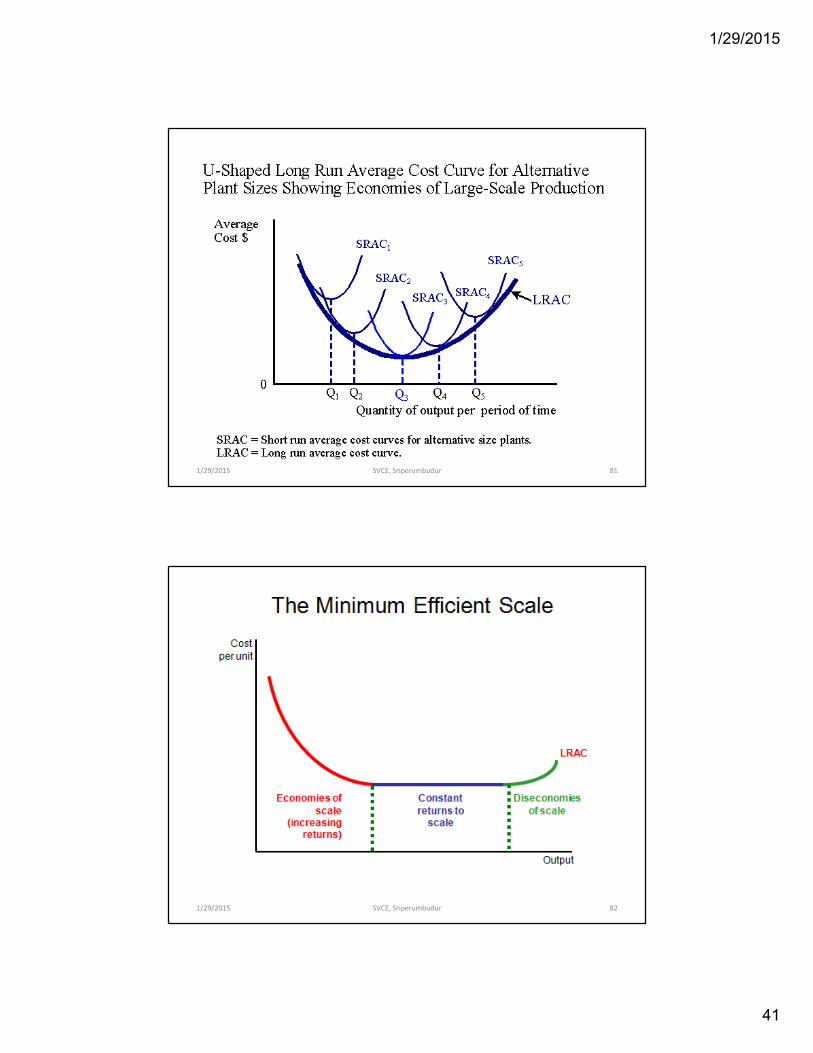

Long Run Cost

Long-run is the time period long enough for a firm to be able

to vary the quantity used of all inputs. Thus, in the long-run,

there are no fixed factor and hence no fixed cost and the

firm can build any size or scale of plant.

1/29/2015 70SVCE, Sriperumbudur

1/29/2015

36

Long Run Cost

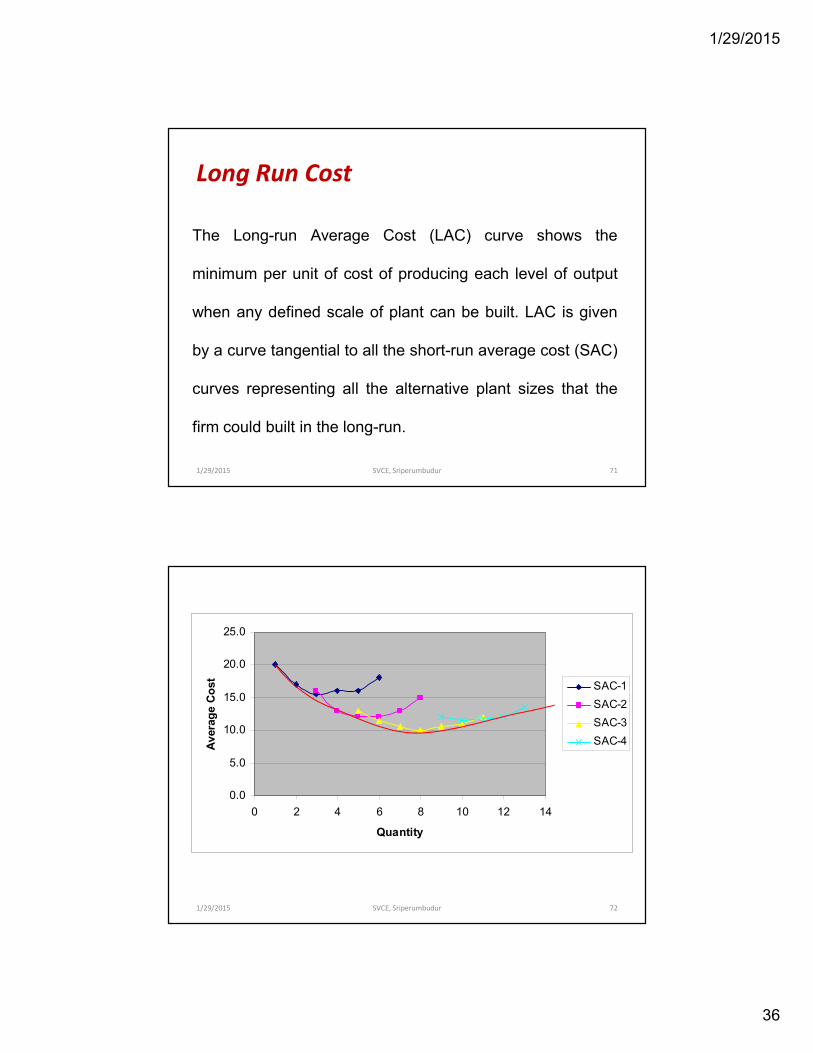

The Long-run Average Cost (LAC) curve shows the

minimum per unit of cost of producing each level of output

when any defined scale of plant can be built. LAC is given

by a curve tangential to all the short-run average cost (SAC)

curves representing all the alternative plant sizes that the

firm could built in the long-run.

1/29/2015 71SVCE, Sriperumbudur

0.0

5.0

10.0

15.0

20.0

25.0

0 2 4 6 8 10 12 14

Quantity

Avera

ge C

ost

SAC-1

SAC-2

SAC-3

SAC-4

1/29/2015 72SVCE, Sriperumbudur

1/29/2015

37

Long Run Cost

If the firm expected to produce 2 units of output per unit of

time it would built the scale of plant given by SAC-1 and

operate it at point A where AC is 17. we could have drawn

many more SAC curves in the figure one for each

alternative scales of plant that the firm could built in the long

run. By then drawing a tangent to all these SAC curves, we

could get the LAC curve.1/29/2015 73SVCE, Sriperumbudur

Shape of Curve

While the SAC curve and the LAC curve have been drawn

as U-shaped, the reason for their shapes is quite different.

The SAC curves decline at first, but eventually rise because

of the LAW of Diminishing Marginal Returns (resulting from

the existence of fixed inputs in the short-run)

1/29/2015 74SVCE, Sriperumbudur

1/29/2015

38

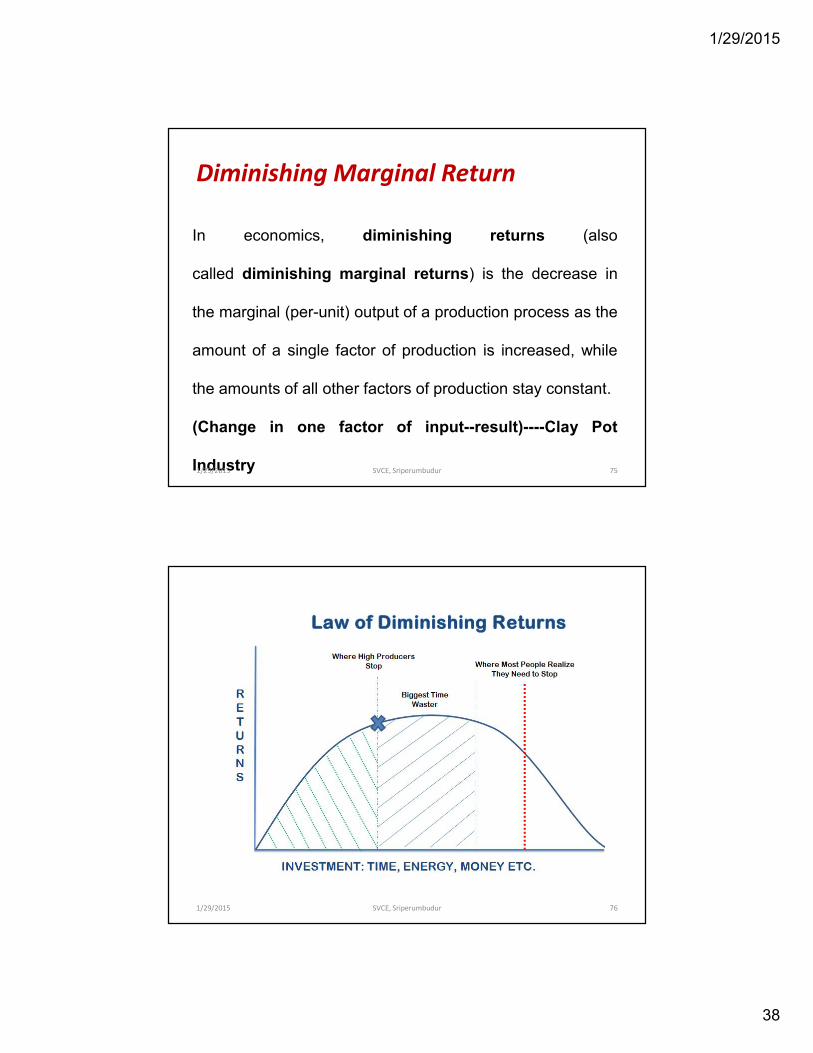

Diminishing Marginal Return

In economics, diminishing returns (also

called diminishing marginal returns) is the decrease in

the marginal (per-unit) output of a production process as the

amount of a single factor of production is increased, while

the amounts of all other factors of production stay constant.

(Change in one factor of input--result)----Clay Pot

Industry1/29/2015 75SVCE, Sriperumbudur

1/29/2015 76SVCE, Sriperumbudur

1/29/2015

39

Shape of Curve

In the long-run, there are no fixed inputs and the shape of

the LAC curve is determined by economies and

diseconomies of scale. That is, as output expands from very

low levels, increasing return to scale causes LAC curve to

decline initially. But as output becomes larger and larger,

diseconomies of scale may become prevalent, cause LAC

curve to start rising.1/29/2015 77SVCE, Sriperumbudur

• As a firm becomes too large, it becomes costlyto keep control of a sprawling corporateempire and so often results in bureaucracy asexecutives implement more and more levelsof management. As firms increase in size,managers will initially provide a net benefit tothe firm and increase productivity, however,as a firm grows and covers a largergeographical area and/or employs morepeople, a principle agent problem arises,leading to lower productivity.

EXAMPLE CASE

1/29/2015 78SVCE, Sriperumbudur

1/29/2015

40

• To counter this, executives introducestandards and controls in order to maintainproductivity and this necessitates the hiring ofmore managers to apply these thesestandards and controls, hence the proportionof managerial to working class begins to leantowards managerial and the companybecomes "top-heavy". However, theseadditional managers are not providingadditional output, they are spending theirtime implementing standards and carrying outsupervision that is unnecessary in smallerfirms, hence the cost-per-unit has increased.1/29/2015 79SVCE, Sriperumbudur

Shape of Curve

Empirical studies seem to indicate that for some firms the

LAC is either U-shaped and has a flat bottom (implying

constant return to scale over wide range of output) or is L-

shaped (indicates that over the observed levels of outputs

there were no diseconomies of scale)

1/29/2015 80SVCE, Sriperumbudur

1/29/2015

41

1/29/2015 81SVCE, Sriperumbudur

1/29/2015 82SVCE, Sriperumbudur

1/29/2015

42

Human Wants

Man is a bundle of desires.

1/29/2015 83SVCE, Sriperumbudur

Human Wants

Basically requires food, cloth & shelter

Wants vary based on education, temperature &

taste

1/29/2015 84SVCE, Sriperumbudur

1/29/2015

43

1/29/2015 85SVCE, Sriperumbudur

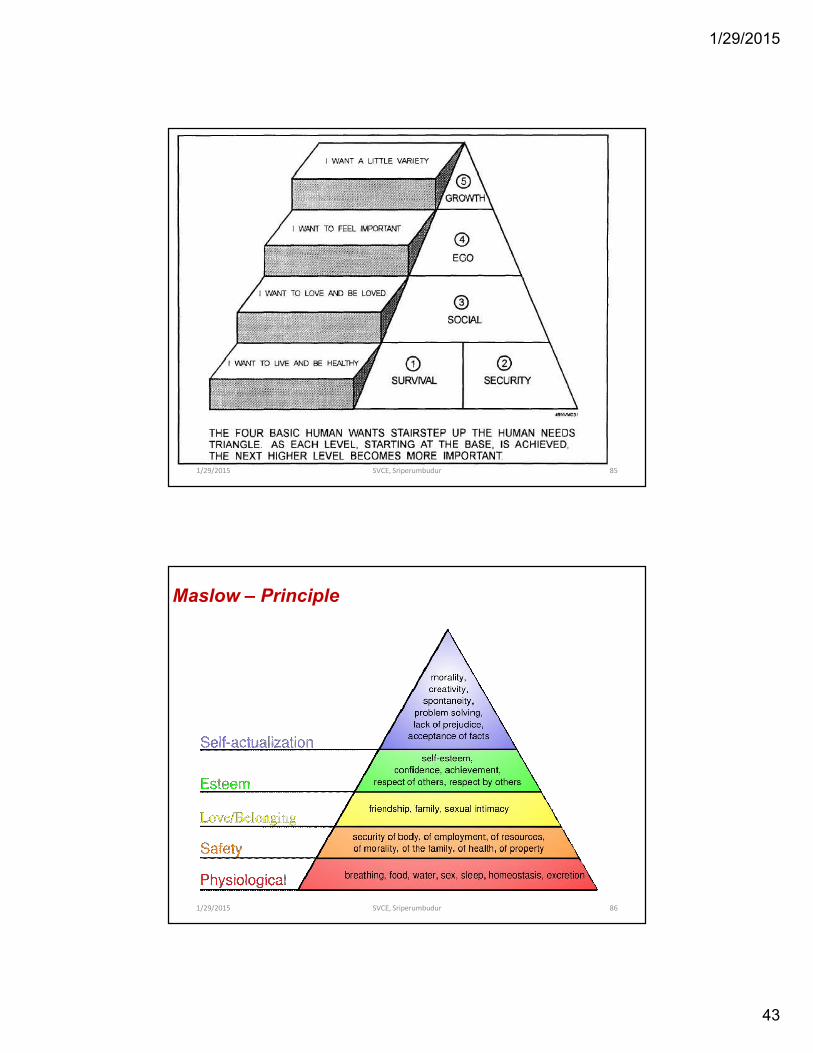

Maslow – Principle

1/29/2015 86SVCE, Sriperumbudur

1/29/2015

44

1/29/2015 87SVCE, Sriperumbudur

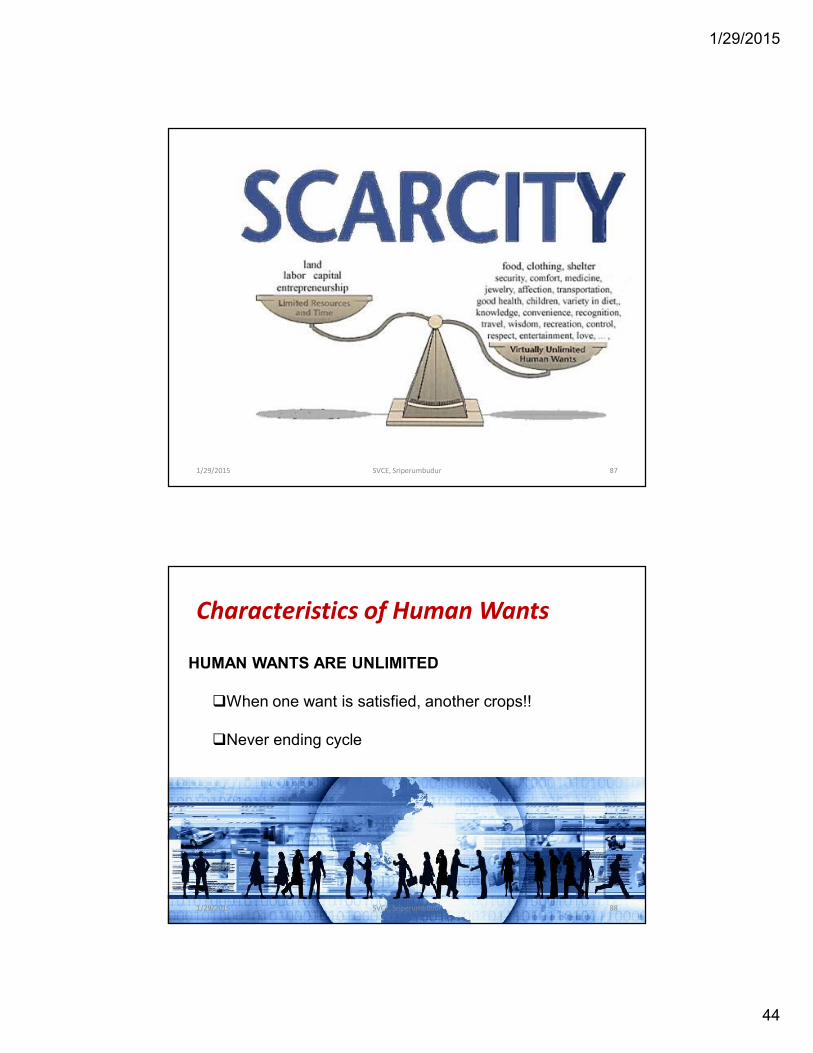

Characteristics of Human Wants

HUMAN WANTS ARE UNLIMITED

When one want is satisfied, another crops!!

Never ending cycle

1/29/2015 88SVCE, Sriperumbudur

1/29/2015

45

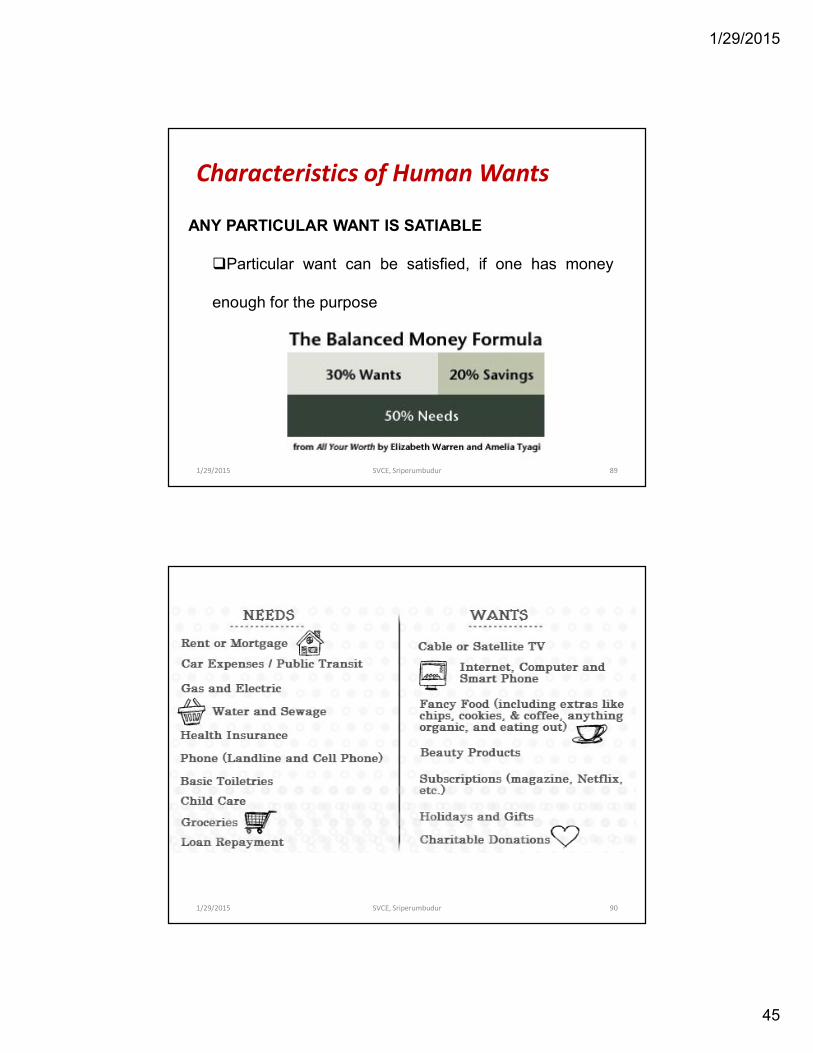

Characteristics of Human Wants

ANY PARTICULAR WANT IS SATIABLE

Particular want can be satisfied, if one has money

enough for the purpose

1/29/2015 89SVCE, Sriperumbudur

1/29/2015 90SVCE, Sriperumbudur

1/29/2015

46

Characteristics of Human Wants

WANTS ARE COMPLEMENTARY

We want things in group

A single thing may need another for full satisfaction

Example: car needs petrol

1/29/2015 91SVCE, Sriperumbudur

Characteristics of Human Wants

WANTS ARE COMPETIVE

One commodity competes with another

Since we have limited disposal of money, accepting

something and rejecting others

1/29/2015 92SVCE, Sriperumbudur

1/29/2015

47

Characteristics of Human Wants

WANTS ARE BOTH COMPLEMENTARY & COMPETIVE

Machines Versus Man

Competes as well as go along with each other

1/29/2015 93SVCE, Sriperumbudur

Characteristics of Human Wants

WANTS ARE ALTERNATIVE

COFFEE VS TEA

OWN HOUSE VS RENTED

1/29/2015 94SVCE, Sriperumbudur

1/29/2015

48

1/29/2015 95SVCE, Sriperumbudur

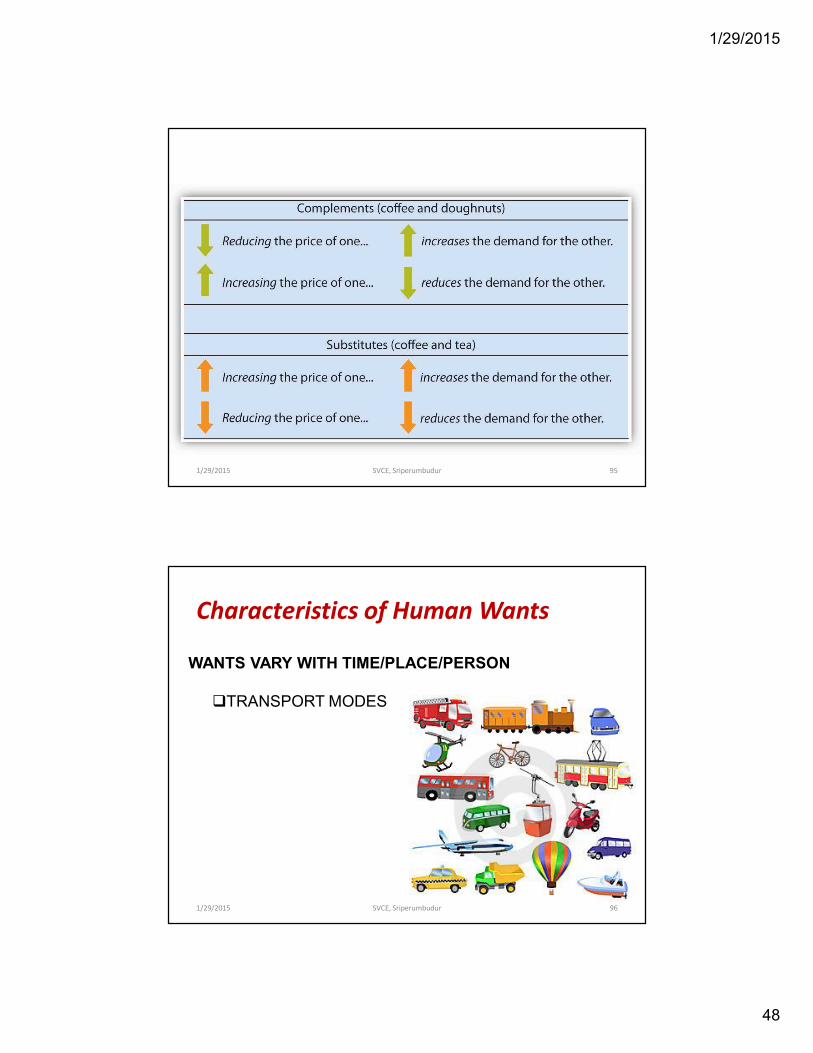

Characteristics of Human Wants

WANTS VARY WITH TIME/PLACE/PERSON

TRANSPORT MODES

1/29/2015 96SVCE, Sriperumbudur

1/29/2015

49

Why ‘wants’ important in economics?

The characteristics of human wants need a close study as

they give birth to some of the most important laws of

science of economics!!

1/29/2015 97SVCE, Sriperumbudur

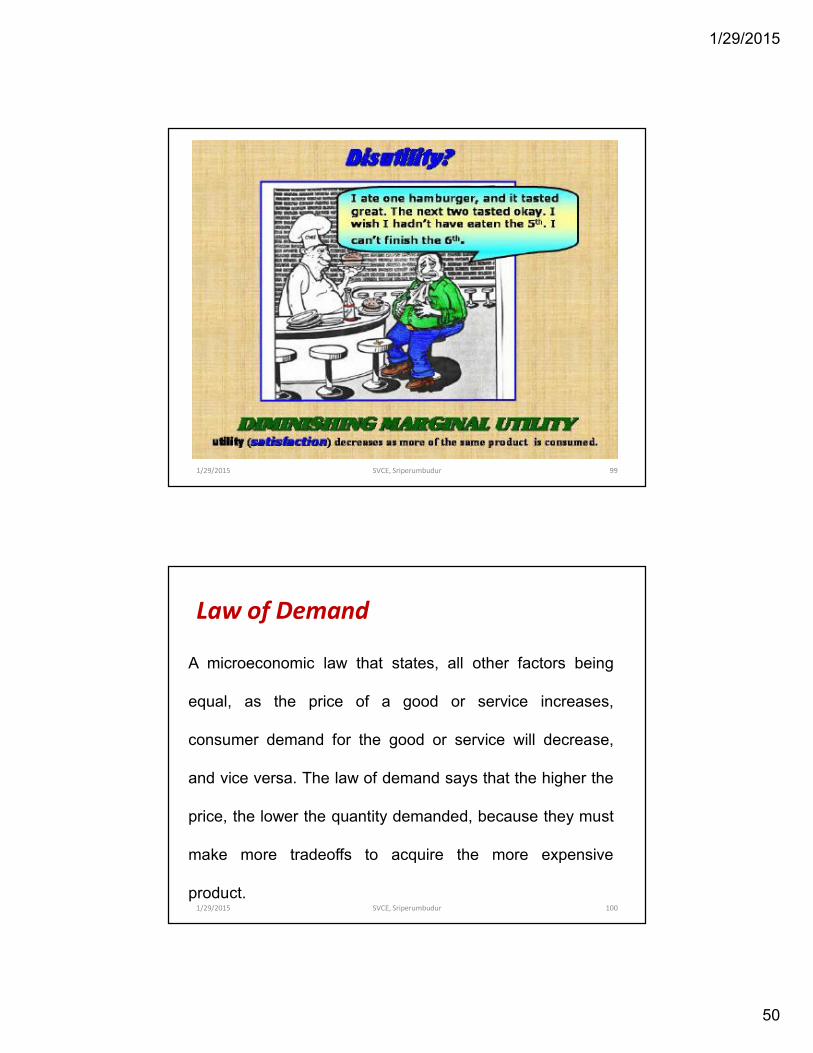

Law of Diminishing Utility

A law of economics stating that as a person increases

consumption of a product - while keeping consumption of

other products constant - there is a decline in the marginal

utility that person derives from consuming each additional

unit of that product.

1/29/2015 98SVCE, Sriperumbudur

1/29/2015

50

1/29/2015 99SVCE, Sriperumbudur

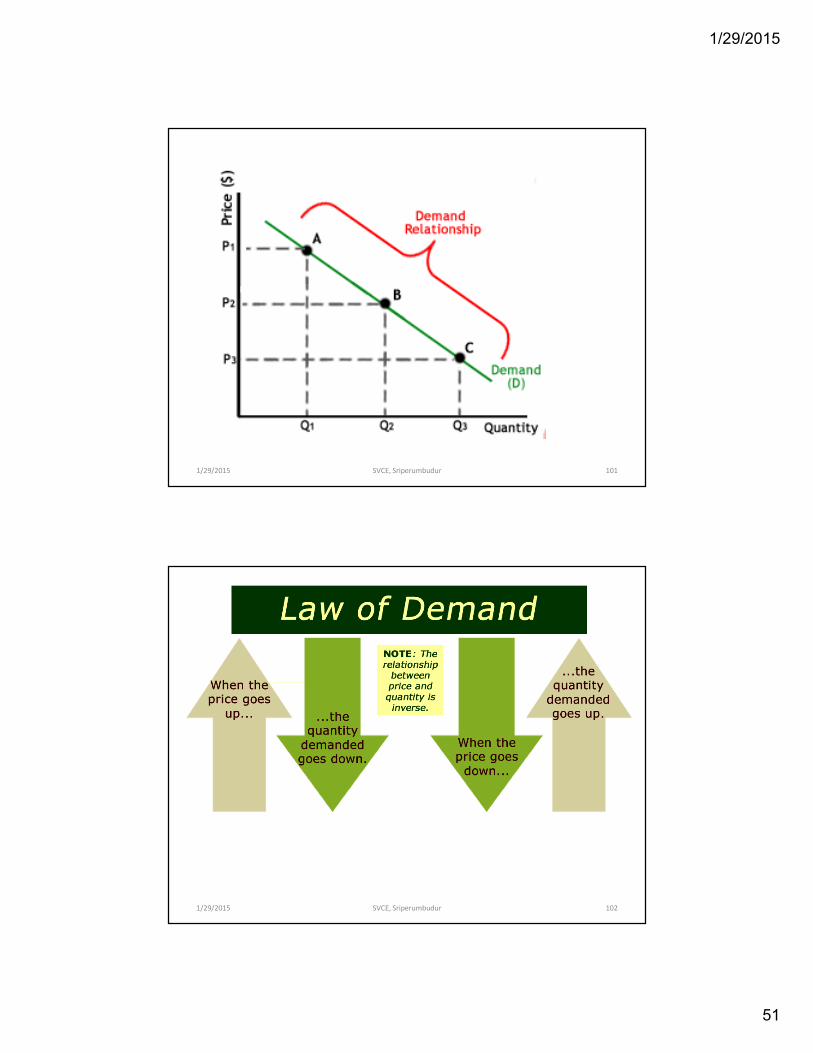

Law of Demand

A microeconomic law that states, all other factors being

equal, as the price of a good or service increases,

consumer demand for the good or service will decrease,

and vice versa. The law of demand says that the higher the

price, the lower the quantity demanded, because they must

make more tradeoffs to acquire the more expensive

product.1/29/2015 100SVCE, Sriperumbudur

1/29/2015

51

1/29/2015 101SVCE, Sriperumbudur

1/29/2015 102SVCE, Sriperumbudur

1/29/2015

52

Consumers’ Surplus

An economic measure of consumer satisfaction, which is

calculated by analyzing the difference between what

consumers are willing to pay for a good or service relative to

its market price. A consumer surplus occurs when the

consumer is willing to pay more for a given product than the

current market price.

1/29/2015 103SVCE, Sriperumbudur

Consumers’ Surplus

For example, assume a consumer goes out shopping for a

CD player and he or she is willing to spend 2500. When this

individual finds that the player is on sale for 1500,

economists would say that this person has a consumer

surplus of 1000..

1/29/2015 104SVCE, Sriperumbudur

1/29/2015

53

1/29/2015 105SVCE, Sriperumbudur

Classification of Wants

Necessaries

Necessaries of Existence

Necessaries of Efficiency

Conventional Necessaries

Comfort

Luxuries

1/29/2015 106SVCE, Sriperumbudur

1/29/2015

54

Necessaries

Necessaries

Necessaries of Existence: Without which we

cannot exist e.g. food

Necessaries of Efficiency: some goods may not

be necessary to live, but necessary to make us

efficient worker. E.g. table & chair are necessary

for better writing1/29/2015 107SVCE, Sriperumbudur

Conventional Necessaries

These are the things which we are forced to use by social

custom. For example, we must dress according to our

manner acceptable to people

1/29/2015 108SVCE, Sriperumbudur

1/29/2015

55

Comforts

Having satisfies our wants for the necessaries of life, we

desire to have some comforts too. For a student, a book, a

table and a chair are necessary; but cushioned chair is

comfort. Comforts make for a fuller life.

1/29/2015 109SVCE, Sriperumbudur

Luxuries

Man does not stop even at comforts. After comforts have

been provided, he wants luxuries too. Luxury is defined as a

superfluous (additional) consumption, something we could

easily do without. Luxuries car; jewellery; silk cloth; washing

machine;

1/29/2015 110SVCE, Sriperumbudur

1/29/2015

56

THE END1/29/2015 111SVCE, Sriperumbudur

![[Selvakumar, 5(8):August2018] ISSN2348–8034 DOI-10.5281 ...](https://static.fdocuments.in/doc/165x107/62a60c92727fde34dc67e5d0/selvakumar-58august2018-issn23488034-doi-105281-.jpg)